- Two recent Inland Revenue reports may be of interest to the new Government

- Happy 20th Birthday to the New Zealand Super Fund

When the shape and tax policies of the new Coalition Government were announced one of the first surprises for me was the appointment of Simon Watts, the National MP for North Shore, as Minister of Revenue. I was surprised by this because Andrew Bayly has been National’s Spokesperson for Revenue for the past four years.

During that time, he has built up knowledge and background in this area. And I know that colleagues who have met him believe he understands the issues involved in the portfolio. So, it is a surprise to see Andrew overlooked for this portfolio. Obviously, there are reasons behind that, but it still means that Simon Watts will be picking up a portfolio with little background knowledge on how Inland Revenue has been operating. But no doubt he’ll get up to speed quickly. It will be interesting to see what’s in the Inland Revenue and Treasury Briefings to Incoming Minister. And we’ll report on that when those briefings are released in due course.

No foreign buyer’s tax but plenty of “buffer” still

In terms of the headlines about what what’s happened, it is no surprise to hear that the foreign buyers’ tax proposed by National is off the table. That was obviously a precondition of getting New Zealand First on board. The coalition is “committed to delivering tax relief” with increases to tax thresholds from 1st July 2024.

But beyond that, it’s not clear what’s to happen. National’s agreement with Act confirms “…no ongoing commitment to income tax changes, including threshold adjustments beyond those to be delivered in 2024.” Furthermore, the two parties recognise “that details of [National’s] Fiscal Plan may be subject to amendment in response to significant new information or events.”

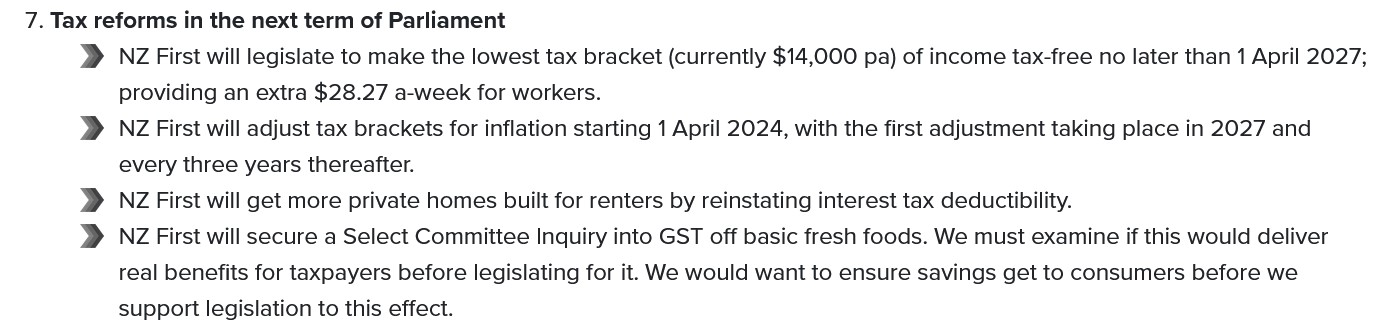

The agreement with New Zealand First refers to letting “Kiwis keep more of what they earn with tax relief of up to $100 per fortnight for an average income per household and a Family Boost childcare tax credit of up to $150 per fortnight.”

At the press conference following the signing of the Coalition agreement the incoming Prime Minister Luxon, said in response to the cancellation of the foreign buyer’s tax that National believes there is a “buffer” available to allow the proposed tax threshold adjustments to happen next July. They actually have a buffer around the finances.

Interestingly, when you go through both coalition documents there is no reference to “budget surplus” in either document. But there is a commitment to restore fiscal responsibility and deliver value for money. So, what does that mean? It could be that the Coalition might be prepared to allow deficits to run longer than was previously said. Otherwise, there’s no mention of how the gap created by the lack of the foreign buyer’s tax will be met. We might get a clearer idea with the mini-Budget which is going to be part of the Half Year Economic Fiscal Update to be released in mid-December.

Accelerated restoration of mortgage interest deductibility

National campaigned on a phased restoration of full mortgage interest deductibility for residential rental properties. That timeline will be accelerated under the agreement with Act. From 1st April 2024, it’s going to be 60%, then 80% from 1st April 2025 and 100% from 1st April 2026.

The agreement with Act includes the repeal of the Clean Car Discount and a commitment to

“Ensure the concepts of Act’s income tax policy considered as a pathway to delivering National’s promised tax relief subject to no earner being worse off than they would be under National’s plan.”

A couple of New Zealand First surprises

There are a couple of interesting initiatives in the New Zealand First agreement neither of which were part of their election policies.

The first is “By or before 2026, assess the impact inflation has had on the average tax rates phased by income earners.” This is an implicit acknowledgment of the impact of not increasing income tax thresholds since 2010. We should actually get a measure of the consequential effect of fiscal drag. I wonder if this initiative would include Working for Families’ abatement level. However, there’s no commitment to take action on the findings.

More funding for Inland Revenue investigation

More importantly, and already incoming Minister of Finance Nicola Willis has included the impact of this in the “buffer”, the Coalition Government will “increase funding for IRD tax audits to urgently expand the IRD tax audit capacity, minimise taxation losses due to insufficient IRD oversight, and to ensure greater integrity and fairness in our tax system.”

How this will be achieved, is going to be very interesting to see. Obviously, it should mean an increase in resources for Inland Revenue. Exactly how much we probably won’t see the full details until the full year’s Budget next May. Still, this is a surprise, including the fact that it has got sign off from Act as well, who are generally committed to lower taxes. (Incidentally, Inland Revenue ought to be safe from Act’s proposal to reduce the public sector headcount by reference to a 2017 baseline, because its staffing level has fallen from 5,519 in June 2017 to 4,130 in June 2023).

Sharing GST with Councils?

The agreement with Act contains a couple of other proposals of varying interest. Firstly, the new Government will not progress the development and delivery of National’s manifesto commitment to a “Taxpayer’s Receipt” for taxpayers. Although minor it’s interesting that Act didn’t want that.

On the other hand, in terms of local government financing, there’s a couple of things here which I think are really interesting and potentially significant. Firstly, they are to consider sharing a portion of GST collected on new residential builds bills with councils. This is part of Act’s commitment to wanting to expand development and housing, that it thinks there should be more revenue sharing going on councils. I agree we should be looking at how councils fund themselves because my view is the current model is unsustainable, particularly for very small councils. A shake up in this area is well overdue and sharing GST receipts is one option going forward.

Road user charging & a congestion charge for Auckland?

The Act agreement calls for work to replace the fuel excise taxes with electronic road user charging for all vehicles starting with electric vehicles, which are currently exempt from road user charges. Does this mean the Auckland regional fuel tax isn’t to be repealed until this new system is in place? The agreements are not clear on this point. [It appears that unless a specific National policy is covered by one or both the agreements it remains National policy. This would appear to include the reduction in the Bright-line test timeframe to two years].

During the election campaign Auckland Mayor Wayne Brown asked if the Auckland regional fuel tax goes how was Auckland going to fund that gap.

The Act agreement has a specific commitment to “Work with Auckland Council to implement time of use road charging to reduce congestion and improve tight travel time reliability.” Again, that’s something that Mayor Wayne Brown has mentioned recently. And maybe it’s tied into that question of a replacement for the regional fuel tax.

A public health levy?

Also of interest in the Act Coalition Agreement is a reference in its immigration policy introducing “a five-year renewable parent category visa, conditional on covering healthcare costs, with consideration for public health care levy.” It’s not clear whether this levy refers to those people coming in under that immigration category or a wider public health care levy. It doesn’t appear to be a commitment in Act’s election promises.

39% trustee rate

The Agreements are silent on whether the outgoing Labour Government’s intention to increase the trustee tax rate to 39% will be implemented. This is part of an existing tax bill which lapsed when the last Parliament rose. This particular bill must be reintroduced because it includes setting the annual income tax rates, which must be passed each year to enable the funding of the government. This initial silence implies that that the increase in the 39% Trustee tax rate is going to remain. We’ll have to wait and see but we’ll probably get more specific information when the Half-Year Economic Fiscal Update is released next month.

In the meantime…

I will be presenting a webinar on the likely tax direction and policies of the Coalition for CCH Wolters Kluwer this coming Wednesday Now what? Tax policy post the 2023 General Election – CCH Learning NZ by which time we should have more specifics.

(This is an edited transcript of part of the Podcast recorded on Friday 24th November)

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.