The debate over international taxation and the so-called Two Pillar proposals has been driven largely by the G20 and the Organisation for Economic Cooperation and Development, (the OECD). But in recent years the United Nations has started to flex its muscles in this space. This is unsurprising, because the UN represents the wider world view outside the 40-odd countries which make up the G20/OECD.

All of this is behind the story that RNZ ran at the start of the week about the United Nations Committee on Economic, Social and Cultural Rights statement on tax policy. The RNZ ran this statement under the banner headline “UN Report questions fairness of GST”, in which it pointed out that GST can be regressive for low-income earners.

In fact, the UN Committee statement went much further than GST. It noted the terms of reference to the United Nations Framework Convention on International Tax Cooperation, which had been adopted by the General Assembly,

“This development represents an important opportunity to create global tax governance that enables state parties to adopt fair, inclusive and effective tax systems and combat related illicit financial flows.”

“regressive and ineffective tax policies”

The key paragraph to the UN Committee statement is paragraph 4, which refers to “regressive and ineffective tax policies”, having

“…a disproportionate impact on low-income households, women, and disadvantaged groups. One such example is a tax policy that maintains low personal and corporate income taxes without adequately addressing high income inequalities. In addition, consumption taxes such as value added tax can have adverse effects on disadvantaged groups such as low-income families and single parent households, which typically spend a higher percentage of their income on everyday goods and services. In this context, the Committee has called upon States Parties to design and implement tax policies that are effective, adequate, progressive and socially just.”

It’s the reference to consumption taxes that was picked up by RNZ. The regressivity of GST is well known and was noted by the last Tax Working Group. The general approach we’ve taken here to that issue is to try and ameliorate the impact by benefits or transfer payments such as Working for Families and Accommodation Supplement to lower income families.

The thing is though, as Alan Bullôt, of Deloitte noted in the RNZ story, GST is a very effective tool for the government to raise a large amount of money relatively easy. In fact, GST represents about 25% of all tax revenue a point I repeated when I discussed the whole story on RNZ’s The Panel last Monday.

Principles of a well-designed tax system

But the Committee statement is interesting beyond the GST issue because it goes on in paragraph 6 to set out what it regards as the principles of a well-designed tax system. It suggests, for example,

“…ensuring that those with higher income and wealth, in particular those at the top of the income and wealth spectrums, are subject to a proportionate and appropriate tax burden.”

That can be clearly interpreted as a call for a capital gains tax or some form of capital taxation, a point I made to The Panel.

The Committee also fires a few shots over international tax, stating

“The Committee has observed situations in some States where low effective corporate tax rates, wasteful tax incentives, weak oversight and enforcement against illicit financial flows, tax evasion and tax avoidance, and the permitting of tax havens and financial secrecy drive a race to the bottom, depriving other States of significant resources for public services such as health, education and housing and for social security and environmental policies.”

That clearly targets tax havens, but it’s also a shot across the likes of Ireland, for example, with its low corporate tax rate.

A global minimum tax

The Committee also calls for a “global minimum tax on the profits of large multinational enterprises across all jurisdictions where they operate and to explore the possibility of taxing those enterprises as single firms based on the total global profits, with the tax then apportioned fairly among all the countries in which they undertake their activities.”

That’s quite the statement even if probably forlorn given the Trump administration’s recent declarations. It’s probably what the less developed world is after, because they’re quite concerned they’re losers under the current system. This is going to lead to wider clashes over the G20/ OECD proposal, which I think to be frank, is probably dead. In any case, I thought it was always noteworthy that Pakistan, the World’s fifth most populous country and Nigeria, the sixth most populus country and also Africa’s largest economy, both refused to sign up for Two Pillars.

Now economically, that was not highly significant because the economies are small relative to the giant economies of the developed world. However, I think this refusal points to existing issues and this statement underlines there’s global tensions ahead on this question of international tax.

As I said, the Trump administration basically is saying no go. But I think you will see countries attempting to find ways of taxing what they regard as their part of the international multinationals’ income. So, plenty ahead in this space.

Rising GST debt

Now moving on, another RNZ report picked up that there had been a substantial growth in GST debt. Allan Bullôt, of Deloitte raised a concern this could be creating zombie companies. In particular he noted the amount of GST collected but not paid to the Government, has risen from $1.9 billion in March 2023 to $2.6 billion by March 2024.

As mentioned earlier, GST represents 25% of tax revenue. It also represents just under 40% of all tax debt and has been rising sharply. That’s a reflection of the economic slowdown and the cash flow crunch that’s happening to a lot of businesses.

Even so, this is a matter where Inland Revenue has a number of resources it can deploy, and one Alan mentioned is the power to notify credit reporting agencies about tax debt. According to the Inland Revenue, it only did that three times in the year ended 20 June 2024 and not at all during the June 2023 year.

This means that people were trading and doing business with companies without realising the potential risk. What that might mean is that you provide services to a company which is struggling with GST debt, and lo and behold, you suddenly find you’ve got a bad debt on your hand.

Creating zombie companies?

This is a major issue and as Allan put it,

“That’s grown and grown. I get very nervous we’re creating zombie companies … if you’re three or four GST returns behind, it’s incredibly unlikely if you’re a retail or service business that you’ll ever come back. If you’re three of four GST payments behind, it’s incredibly unlikely that your retail or service business will ever come back.

Maybe if you’re a property developer who’s got big assets that you sell and settle your debt. But if you’re a normal business, a restaurant or something like that, you go belly up.”

This is an area where Inland Revenue has information which is not available to the general public and maybe it should be making that more widely available. There’s a question here to my mind, of what proportion of debt you would report. The Inland Revenue I think has every right to say this person owes X amount of GST, or is behind on GST, but bear in mind in some cases the debt is inflated by interest and penalties. Or in some cases there may have been estimated assessments.

Notwithstanding this Allan is right to raise concerns and I expect we will see more money being granted to Inland Revenue in this year’s Budget to chase this debt.

Meanwhile, jam tomorrow in the Australian Budget

It was the Australian budget on Tuesday night our time in which the ruling Australian Labor Party promised modest tax cuts starting in July 2026, with a further round in July 2027. Under the proposed cuts, a worker on average earnings of A$79,000 per year (about NZ$86,800) will receive A$268 in the first year and that will rise to A$536 in the second year. In addition, there will be a A$150 energy rebate payable in A$75 instalments.

Otherwise, there weren’t many other tax measures to report. That was hardly surprising because two days later, Prime Minister Anthony Albanese announced that the Federal Election would be held on 3rd May. The Budget was therefore what you might call a typical pre-election budget, promising jam tomorrow if you vote for the ALP.

One tax measure of note was that the Australian Tax Office is getting further funding for dealing with tax avoidance and tax evasion. I think that’s a pretty standard pattern we’re seeing around the world. The British had what they call their Spring Statement this week, the half yearly report by the Chancellor of the Exchequer or Finance Minister.

No new tax measures were announced. But like the ATO, HM Revenue and Customs was allocated more money to target tax evasion, with the expectation that it would achieve about a billion pounds a year in additional revenue, which seems very light given the scale of the UK economy.

Mega Marshmallows food or confectionery?

Finally, this week, a couple of years back, we discussed the Mega Marshmallows Value Added Tax (VAT) case from the United Kingdom. Basically, it involved the VAT treatment of large marshmallows. If deemed to be food they would be zero-rated for VAT purposes, but if they were confectionery, they would be standard rated which at 20% means quite a significant sum is at stake.

I will cite this and its very well-known predecessor the ‘Max Jaffa’ case involving Jaffa Cakes from the 1990s, when people make suggestions about maybe reducing the GST on food to help with the cost of living, particularly for lower-income families. It’s a well-meant policy except the practical issues you run across lead to absurdities at the margins. My view on this topic is if you want to assist people at the lower end of the income scale, it’s better give them income rather than try and fiddle with the GST system because there are unintended consequences, and this mega marshmallow case is a classic example.

The case involves unusually large marshmallows. The recommendation by the manufacturer is that they should be roasted as they’re marketed as part of the North American tradition of roasting marshmallows over an open fire. Except it’s not clear in fact, if that actually happens.

The story so far is that after HM Revenue and Customs lost in the First-Tier Tribunal, it appealed to the Upper-Tier Tribunal which basically said, “Nope, we’re not hearing it.” So HMRC appealed again to the Court of Appeal which has now issued its ruling. The Court of Appeals determined it was not absolutely clear whether in fact these marshmallows can only be eaten if they are cooked, in which case they must be food, or they can be eaten with the fingers, in which case they are confectionery.

Accordingly, the key issue is whether they are normally eaten with the fingers. This is a question of fact about which the first-tier tribunal has not made a finding. In some cases, it will be obvious from the nature of the product whether it is normally eaten with the fingers or in some other way. But that is not clear with this particular product.

The Court of Appeals therefore sent the case back to the First-Tier Tribunal to decide on this question of fact. Are these mega marshmallows mostly eaten with the fingers? If so they’re confectionery and subject to VAT at 20%. Alternatively, are they mostly cooked as supposedly intended, and therefore zero-rated food.

Time for the UK to apply VAT to food?

This case came to my attention through the UK tax thinktank Tax Policy Associates which is run by the estimable Dan Neidle, a former tax partner at the mega law firm Clifford Chance. Commenting on the Court of Appeal’s decision, he pointed out the sheer absurdity and costs involved and questioned why this was so. “Why do we have a horribly complicated set of rules that mostly benefit people on high incomes (because they spend more on food)? “

His solution – scrap zero-rating on food, in other words, adopt the approach we have here in New Zealand and tax everything. He estimates that would raise about £25 billion which could be used to reduce the standard rate of VAT from 20% to 17%.

Warming to his theme Dan thinks a better idea would be “Cut the rate to 18% and use the remaining [money] in benefit increases and tax cuts targeting those on low incomes, so they’re not out of pocket from the loss of the 0% rate.”

It’s the first time I can recall a British commentator suggest this. I doubt it will happen, but it’s just a reminder that although our GST is highly comprehensive, we don’t have these absurd but entertaining cases involving marshmallows of unusual size.

But a comprehensive GST is regressive, and I think a better approach is to address that by means of transfers to lower incomes rather than tinkering with exemptions. You never know, there may be something in this space in the Budget, we’ll find out next month.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

There have been several constant themes throughout this year. A surprising one has been the question of how we tax capital and whether we should have a capital gains tax. Throughout the year there have been a steady stream of stories on the topic. Meanwhile the Labour Party is currently reviewing its tax policy, and whether it’s going to go with a wealth tax or a capital gains tax.

A place where talent does not want to live

Intriguingly, Inland Revenue has added to this mix right at the end of the year with the release of an issues paper on the effect of the Foreign Investment Fund (FIF) rules on immigration.

Earlier this year I discussed a New Zealand Institute of Economic Research report called The place where talent does not want to live, which looked at the impact of the FIF rules on migrants to New Zealand. The NZIER report concluded that the FIF rules were acting as a hindrance to investors, particularly those migrants coming here who have previously invested in offshore startup companies.

The report also discussed an issue I’ve encountered fairly regularly of the impact of the FIF rules for American citizens. Even though they may have been resident in New Zealand for many years, because they are American citizens they still have to file U.S. tax returns. As a result, a mismatch arises for them between the FIF rules, which basically act as a quasi-wealth tax, and the realisation basis of capital gains tax that applies in America.

Inland Revenue policy officials have been aware of this issue for some time. In fact, I spoke to several officials earlier this year about the issues and potential options. The topic was highlighted as an option for review and was included in the Government’s tax and social work policy programme released last month. This report has therefore come out quicker than I expected which is a pleasant surprise.

The problem with the FIF rules

The problem is set out very clearly in paragraph 1.5 of the issues paper.

“Migrants will generally have made their investments without awareness of the FIF rules and may not be organised so that they can fund the tax on deemed rather than actual income. This is particularly a problem for illiquid investments acquired pre migration…. Because the FIF tax is imposed in years before realisation and on deemed rather than actual income, FIF taxes paid may not be creditable against foreign taxes charged on the sale of the investment.“

This highlights a key point about the FIF rules – they’re highly unique by world standards. When I’m discussing them with overseas clients and advisers, to make them more understandable I tend to explain them from the viewpoint that they’re a quasi-wealth tax. As the quote above notes problems also emerge whether the tax paid under the FIF rules can be fully utilised in the United States, for example.

Fixing the problem – taxing the capital gains?

The paper canvasses several options for reform, including one of simply increasing the current $50,000 threshold above which the FIF rules automatically apply. A key proposal is that maybe the investments subject to the FIF rules should be taxed on what is called revenue account. That is only dividends received and any gain in the value of those investments attributed to New Zealand on disposal would be taxed. In other words, an investor would be taxed on dividends and then when the investment was disposed of, a capital gains would be become payable.

Now to buttress this option the paper proposes that there should be an exit tax. In other words, if someone elects to use the revenue account method, but then decides no, actually New Zealand isn’t working out for us for whatever reasons, and they become a non-tax resident, this migration would trigger an exit charge. I’ve seen this in other jurisdictions and current FIF rules do have a provision covering it. This approach should be pretty understandable to investors coming here.

Maybe a deferral basis?

Another alternative is a so-called deferral basis, is where the FIF rules would apply on a realisation basis. This would be achieved in a way similar to how withdrawals on foreign superannuation schemes are currently taxed when the tax charge arises on withdrawal or transfer into a New Zealand based Qualifying Recognised Overseas Pension Scheme.

The taxable amount would be based on a deemed 5% per annum income from the date of their migration, with an interest charge for deferral. Again, this would be buttressed by an exit tax.

What happens overseas?

Picking up on what I was saying at the start about the question of taxation of capital, most other jurisdictions don’t encounter this issue to the same extent as we do because they usually have a capital gains tax regime that applies to comprehensive capital gains. Actually, in paragraphs 2.3 and 2.4 I find there’s some intriguing commentary from Inland Revenue on this issue.

“Because New Zealand does not tax capital gains without the FIF rules, no New Zealand tax would ever be paid on an investment in a foreign company that paid no dividends and was sold for a capital gain.”

This is an interesting insight to the issues caused by non-taxation. In effect without the FIF rules the Government is forsaking potential revenue. I always thought the expansion of the FIF rules in 2006 was really a sidestep around the difficult issue of taxing capital. And of course, despite having kicked the capital gains tax can down the road back in 2006, it’s still there.

Tax driven behaviour, or just a rational investment choice?

The issues paper goes on, quite controversially in my view, to argue that without the FIF rules in New Zealand, residents have a tax driven incentive to invest in foreign companies that enjoy low effective tax rates and do not pay significant dividends. Speaking with 40 years of tax experience, yes taxes do drive investment behaviour.

But this argument sidesteps a huge criticism, which is still valid, of the current FIF rules. When they were introduced in 2006, many of the submissions against them argued that the New Zealand stock market is so small in global terms that investors would be unwise to be fully invested here, and therefore should be spreading their risk by diversification and investing in offshore markets.

That is as valid a criticism of the FIF rules now as it was back in 2006. And of course, memories of the 1987 stock market crash, which was actually quite catastrophic by world standards, still run deep in many areas. We now have this scenario here where the FIF rules were designed because the Government wanted some revenue. It saw tax driven behaviour happening offshore, but it ignored a key fact, the importance of diversification. And if you don’t tax the capital but you want the revenue, where do you go from there?

Backdating the introduction of the changes?

Anyway, the whole paper is a very worthwhile read. It has one further highly interesting suggestion that changes could be back dated to take effect from 1st April 2025 and the start of the next tax year. Such a swift law change doesn’t happen with issues papers. Normally there’s usually another year or so before legislation is introduced and then comes into effect.

This option is actually very encouraging for migrants. I have had a number of inquiries on this issue, and I know of clients who have backed away from New Zealand because of the FIF rules. So, they will be looking at the proposals with great interest.

The paper also canvasses whether it should apply to new migrants or to existing New Zealand tax residents. That’s a good question it should certainly apply to migrants who can reorganise their affairs in anticipation, but I believe it should also apply to U.S. citizens who still have to file U.S. tax returns and are very disadvantaged by the current FIF rules.

Worth noting that although this is largely a tax measure it’s important to the Government because the existing FIF rules are seen (as the NZIER report noted) as a hindrance to attracting high quality migrants. Changing the law is seen as a priority as part of the Government’s general economic programme,

Submissions are open now and continue until 27th of January. I urge everyone interested in this topic to submit. We will be submitting a paper on this ourselves. We will also be contacting clients on this matter as it’s quite a welcome Christmas present.

The year in review

Moving on, its been a very busy year in tax. And I guess the biggest story in many ways was the Budget on 30th May, with the promised increase in tax thresholds finally being enacted with effect from 31st July. That was certainly the most eagerly anticipated one, and according to my data reads, it was the most read transcript over the year.

The tax cuts which weren’t

These tax cuts as they were called (which they’re not because they’re only inflation adjustments) also highlighted a big and continuing problem with our tax system, which the politicians apparently don’t want to address. The threshold adjustments only factored in inflation from 2018. They therefore effectively locked in the inflationary effect of the non-adjustment between 1st October 2010 (the last time the thresholds were adjusted) and the 2018 baseline.

On the other hand, in order to help pay for these adjustments which will reduce government revenue, the threshold on Working for Families which has been at $42,700 since 1st July 2018, was not increased. This means that families with income above that threshold have their Working for Families credits abated at 27.5%. Consequently, they face some of the highest effective marginal tax rates in the country.

And as I have repeatedly said in past podcasts, our politicians are very much less than transparent about the impact of what’s called fiscal drag. That is, as wages increase with inflation, they pull taxpayers up into higher tax brackets. We have a particularly big problem around the now $53,500 threshold where the tax rate jumps from 17.5% to 30%, the biggest single jump in the whole tax scale.

To bang a drum already beat repeatedly, this hinders a discussion around what is happening with our tax system? How much revenue have we really raised because politicians have been happy to use fiscal drag to quietly increase the tax take.

But the main effect is that the burden of tax falls on low to middle income earners who face significantly higher marginal tax rates because of the effect of abatements on people receiving social support, such as Working for Families.

So overall, those tax threshold adjustments were welcome. They were overdue, but they were one step forward and two steps sideways and half a step back because there’s no comprehensive commitment to ensuring that we have regular threshold adjustments.

If America can do it, why not here?

Just as an aside, in America all thresholds are automatically index-linked. Countries vary on their treatment of inflation and thresholds. And in low inflation periods, you can get away with not needing to do it every year, but you can’t leave such adjustments for 14 years without finally having to do something.

A year of anniversaries

2024 was quite a big year for me personally. I started working in tax 40 years ago in Britain and it so happened that the British budget on 30th October had several announcements which have huge significance not just for UK migrants who have moved here but also for many Kiwis. So, I find myself, somewhat ironically, still doing a lot of work on the impact of British taxation.

It’s also been 20 years since I started Baucher Consulting and as I said in the podcast much has changed, and yet in some ways little has changed. One constant which hasn’t really changed is the behavioural impact of tax- this week’s discussion of the FIF regime is the latest example. I’d like to thank everyone who’s supported me over the these past 20 years.

Our fantastic guests

Looking at some other highlights of the year in terms of the podcast, we had a lot of great guests this year and my thanks again to all of them. My particular favourite episode was the Titans of Tax with Sir Rob McLeod, Robin Oliver and Geof Nightingale. Many thanks to Sir Rob, Robin and Geof for giving up their time. It was a fantastic discussion and very, very enjoyable. It was extremely well received all around. It was fascinating to just sit back and listen and to three experts who’ve been very heavily involved in the last three major tax working groups.

My thanks also to all my other guests this year, including the four finalists for this year’s Tax Policy Charitable Trusts Scholarship. Again, thank you so much for your input. Very interesting to talk to you, and the future of tax policy is in good hands.

Inland Revenue goes full throttle on compliance work

One of the big themes for the year, and less of a surprise, was Inland Revenue’s ramping up its enforcement approach. One of our guests very early in the year (and thanks again) was Tracy Lloyd, service leader of Compliance Strategy and Innovation at Inland Revenue. Tracy’s podcast was a really interesting one looking at what tools Inland Revenue is using and how it’s ramping up its investigative activities.

We’ve seen Inland Revenue’s more aggressive approach constantly through throughout the year. It has made announcements about cracking down on the construction sector, looking at liquor stores. Pretty much every week there’s a media release that another tax fraudster has been jailed or received substantial fines or home detention. In addition Inland Revenue is making use of information received through the Common Reporting Standards on the Automatic Exchange of Information.

These things will continue to come through. Inland Revenue got $116 million over four years to beef up its investigation activities and to improve its tax collection. As part of this we’re seeing a crackdown on student loan debt, which is a much more problematical issue mainly because the biggest portion of debt is held by persons overseas. It’s therefore not so easy to collect.

Inland Revenue’s activities will continue to ramp up but I think it may start to find there’s increasing push back as it clamps down. I think it’s previously been slow in responding, and during the COVID pandemic that was understandable. But right now, the faster it responds to debt issues developing, the better for all of us. Zombie businesses which linger on are no good to anyone.

The surprising continuing debate over capital gains

But the other big thing this year has been a surprising one. It’s the question of the shape of the tax system and persistent media stories about whether we should have a wealth tax or capital gains tax. This is a topic I don’t see going away. I see the pressure mounting on it because as, the Government’s main agency, Treasury, is pointing out we have ongoing demographic pressures in relation to superannuation and funding health.

And as I keep pointing out, we also have the question of climate change. We have insurers withdrawing cover and I think that means the Government will be expected to step in. And that means sharing the burden, which means ultimately some form of tax increases. All this means the composition of the tax base will continue to be a matter of debate.

Of course, we have options like capital gains tax, wealth taxes, or as Dr. Andrew Coleman suggested (another one of the fascinating podcasts this year) maybe we should rethink our issue of Social Security taxes, where again we’re a unique jurisdiction in that we don’t have them. We used to have such taxes way back from the early 1930s through until late 60s, before they were finally abolished,

So overall lots to discuss this year. I’d like to thank all my guests again, and all the listeners, readers and all those who chip in and comment away. Your comments are read and always welcome. And on that note, everyone have a very happy festive season. We’ll be back with what’s new in the tax world in January 2025.

more on Inland Revenue’s crackdown on student loan debt

and why we might need to pay more tax

At an event for the Young International Fiscal Association, the Revenue Minister, Simon Watts announced the Government’s Tax and Social Policy Work Programme. These work programmes are a working document updated frequently so that after a change of government they reflect the new government’s priorities in tax policy and social policy areas.

According to the speech made by the Revenue Minister, the work programme under the current government is designed to support rebuilding of the economy and improve fiscal sustainability by simplifying tax, reducing compliance costs and addressing integrity risks.

There are six areas of priorities going forward: economic growth and productivity, modernising the tax system, social policy, the integrity of the tax system, strengthening international connections and other agency work.

Out with the old, in with the new

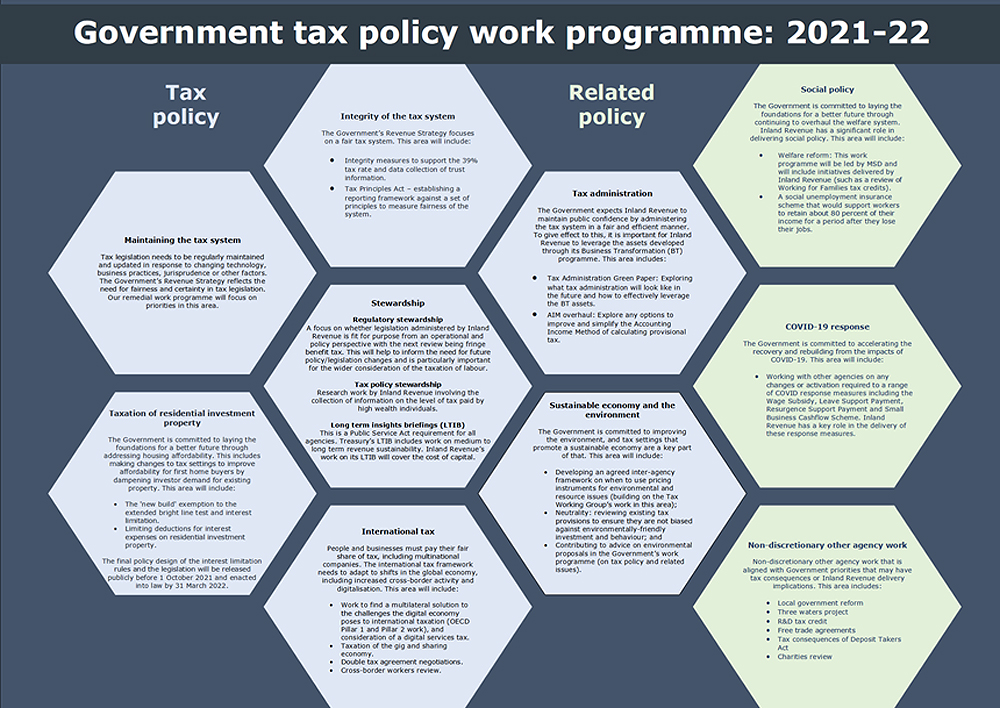

It’s interesting to have a look at what changes have been made since the programme was last officially updated back in 2021-22.

There under the Labour Government, there were 10 work streams of tax policy and related policy matters some of which overlap with the updated programme. Social policy integrity of the tax system, maintaining the tax system were all part of the 2021-2022 work programme and they’ll be part of every work programme going forward.

On the other hand, the COVID-19 response and the taxation of residential investment property were two major areas back in 2021-22 which are no longer there. As is well known the current government when it came in repealed all the work in relation to changes to the taxation of residential investment property.

Tax policy changes already happening

Drilling into the latest workstreams, some of them are already underway such as improvements to employee share schemes, implementation of the Crypto-asset Reporting Framework, simplification of the Approved Issuer Levy reporting including allowing retrospective registration and changes to inward pension transfers. All these are in the current tax bill before the House.

The other interesting things they’ve added in here, which we’ll watch with some interest, are exploring compliance cost reductions, including improving tax compliance with small businesses. Now you recall last week in my review of Inland Revenue’s annual report one of the areas Inland Revenue felt that business transformation hadn’t delivered as much as had been hoped for, was in reducing compliance costs for small businesses.

I totally support what Inland Revenue are doing, but the issue that they’ve run up against is that sometimes it has to accept the trade-off between good tax policy and the risk of tax seepage around the margins. If a policy allows a deduction or other benefit for taxpayers such as SMEs that meet certain criteria, you get certain deductions, Inland Revenue is always concerned about people exploiting that. The question that arises is does the wish to reduce compliance costs outweigh the risk that some of those measures might be abused?

A place where talent wants to live?

An interesting one that caught my eye was their plan to review the Foreign Investment Fund rules. This is something that was mentioned in passing by the Minister of Revenue at the recent New Zealand Law Society Tax Conference. This looks to address the issues raised by the report The place where talent does not want to live in relation to the problems the Foreign Investment Fund regime causes for investors migrating here.

Another interesting one is reviewing the thin capitalisation rules for infrastructure. That’s almost certainly tied up to the desire to have public/private partnerships help build infrastructure in the country. What it would almost certainly mean is that the current thin capitalisation rules (which basically limit interest deductions for international multi-nationals, which have more than 60% debt asset ratio) would almost certainly be relaxed.

In terms of other agency work Inland Revenue is considering, is an improved information sharing agreement with the Ministry of Business and Innovation and Employment, student loans, the question of final year fees free and overseas based borrower settings, the highly topical Treaty of Waitangi settlement, Local Water Done Well and supporting the all-of-Government response to organised crime. (Organised crime often represents tax evasion so it will always fall in the ambit of Inland Revenue).

Changes to the taxation of the Super Fund?

A big work programme, probably in terms of modernising the tax system, would be exempting the New Zealand Superannuation Fund from income tax. This would be quite significant as the New Zealand Superannuation Fund probably contributes $1 billion a year in company income tax. On the other hand, the Government will probably then be able to dial back completely its contributions to the scheme. In other words, the fund would now be expected to be self-funding going forward, which is quite possible now it’s reached a near critical mass of at least $70 billion in value.

The document’s fairly light on detail, just a one pager, but it gives you an insight as to where the priorities are right now. There are no real big surprises and we’ll watch and bring developments as these policies mature and are brought to fruition.

Student loan debt – Inland Revenue ups the ante

Moving on, last week I talked at some length about Inland Revenue’s actions around the collection of student loan debt and it so happened that yesterday Inland Revenue’s Marketing and Communications Group Manager Andrew Stott appeared on RNZ’s 9:00am to Noon with Catherine Ryan. They discussed what Inland Revenue is doing with its extra $116 million of funding over the next four years. This Includes an additional $4 million for recovering overdue student loan debt.

Quite a lot of interesting commentary came out of this interview. One of the first surprises was that many young people going overseas don’t know that their student loan debt, once they leave the country, starts to accrue interest. Therefore, they get behind surprisingly quickly. As is known, only 29% of overseas based borrowers are making repayments at the moment, and the student loan debt is now up to $2.37 billion, $2.2 billion of which is owed by overseas borrowers. A substantial number of whom are based in Australia.

So that’s now obviously a focus both operationally and in the latest work programme. I’m particularly interested to know more about what is planned in the overseas based borrower settings. What does Inland Revenue consider it needs to improve its ability to collect debt under the student loan scheme?

Inland Revenue has been allocated $4 million in funding to get cracking on recovering debt and it’s expected to produce a four to one return this year, which is expected to rise to eight to one next year. It will meet those targets pretty comfortably I’d say. Apparently in the first quarter of its new financial year – 1st July to 30th September this year it’s already collected $60 million in overdue debt up 50% from last year.

A surprising statistic

I guess the big surprise that came out of the interview was when Mr. Stott noticed that most of the debt is owed by people in their 40s or 50s who had never got round to repaying Inland Revenue. These people had been much younger when they went overseas with student loan debt which then accumulated as interest and penalties were added. This does beg the question that if people went overseas in their 20s and we’re now chasing them in their 40s and 50s, what was Inland Revenue doing in between?

As I said in last week’s podcast, relying on late payment and interest charges for enforcement just doesn’t work. We know from research in other areas when a person’s debt blows out (and probably the threshold is as low as $10,000), people will put their head in the sand and not take action because the matter feels too big to manage. Mr Stott mentioned that there’s several debts running into tens of thousands. I have seen one where it’s over $100,000. The average debt owed is about $17,000, but it’s the old overseas debtors, obviously larger debts, that Inland Revenue is going to be targeting.

As part of this it is talking to anyone who returns to New Zealand who has a debt of at least $1,000. They can now identify such persons thanks to the information sharing that goes on between New Zealand Customs and Inland Revenue.

Inland Revenue also have the ability to detain/prevent someone from leaving until they have a conversation about payment of debt. According to Mr Stott the group being targeted are those who have persistently not engaged with Inland Revenue. They have not responded to Inland Revenue at all. They’ve simply just said now go away, I’m not going to talk to you and ignored them. They will be fined and will find themselves having an extra stay at the airport just prior to departure.

Deducting debts from overseas salaries?

Inland Revenue has the ability to issue deduction notices requiring amounts to be withheld from payments to Inland Revenue debtors. (According to an Official Information Act response I got from Inland Revenue, it issued over 42,000 such notices in the year ended 30th June 2024).

Mr Stott was asked whether it could do the same in Australia? Can Inland Revenue ask the Australian Tax Office (ATO) to issue the equivalent to a deduction notice so that an employee working in Australia has part of their salary deducted to pay student loan debt. The answer is yes it can, but it’s not easily done. It’s termed a “garnishee order” in Australia and requires a court order. Consequently, Inland Revenue hasn’t really used such orders.

It seems to me that is something Inland Revenue really will need to look at closely, because if you’ve got 70% non-compliance and you’ve got an estimated 900,000 student loan debtors in Australia, it would be worthwhile establishing a process to enable garnishee orders to happen more frequently.

It may be that they have to ask the ATO to amend legislation, which would delay everything. But it would appear that they have the tools already, so it will be interesting to see if that’s employed more frequently.

Increased audit activity

The other thing Inland Revenue has ramped up is audit activities. It has apparently already launched 2,000 audits in the first quarter of its new financial year. This is up 50% on the previous year. Incidentally, 10% of those, are targeting the largest companies in the in the country.

As previously mentioned, Inland Revenue have recently targeted bottle stores and the construction industry. The next group of people that they’re going to be talking to now are vape stores, nail salons and hairdressers. Because in all cases they suspect cash income is not being declared, so these businesses will be the subject of unannounced visits.

The focus in Inland Revenue now is on enforcement and debt collection and there are more signs of it. So, I’ll repeat what I’ve said previously. If you have debt with Inland Revenue approach them to discuss it. You will find that if you take proactive action, it will be reasonable in most cases, unless you have a history of non-payment In which case good luck. Taking proactive action is the best approach, because tax debt is something you simply can’t put your head in the sand and hope it goes away. It won’t. Inland Revenue has got many more resources now, and the net is closing.

Why we might need to pay more tax

Finally, earlier in the week, I was one of several commentators Susan Edmunds of RNZ spoke to for a story on why we might need to pay more tax. Her story picked up the recent speech by the Treasury’s chief economic adviser Dominick Stephens which noted that the country appears to be running a fiscal deficit of 2.4% of GDP – that’s about $10 billion – and the pressure that’s building on demographic change, the ageing population, and rising healthcare costs. The article also referenced, Treasury’s 2021 Statement on the long term fiscal position He Tirohanga Mokopuna. I repeated that I think it is a matter of when, not if, the tax take has to rise when you put all these factors together.

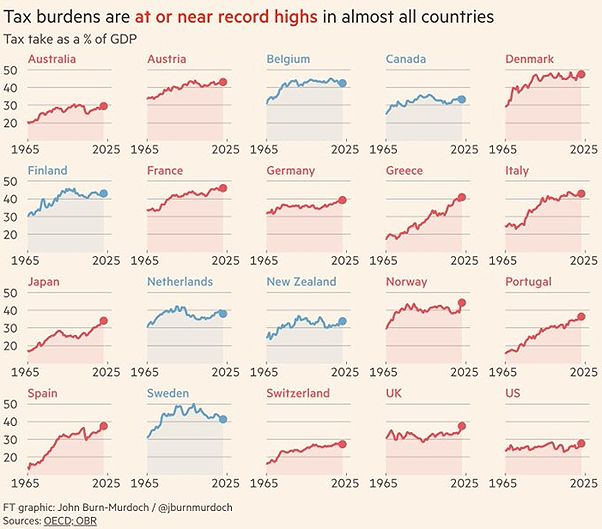

It’s also worth noting that the recent UK budget I covered a couple of weeks back increased taxes. Subsequently, the Financial Times had a very interesting graphic noting that tax burdens as a percentage of GDP for the last 50 years are at all-time highs in 14 of the 20 countries highlighted.

The pressure on tax revenues is a global problem, so we are not alone in trying to deal with these issues.

I think the break point, so to speak, will be the increasing cost of dealing with the damage as a result of extreme weather events. And I note that last week the Helen Clark Foundation released a report on the question of climate change and insurance premiums. My personal view is we need to get moving on this sooner rather than later, because that will help ease the transition.

Other jurisdictions we compare ourselves with, such as Australia and the UK, have a 45% top rate. And of course, in Europe the rates are much higher, still around 50% or so. I remain firmly committed to the broad-based low-rate approach, which means if we do broaden the base, we can hold tax rates down below these levels.

More tax, or less costs?

There was a nice to and fro in the comments on the LinkedIn post I put up with one commenter noting that we also need to reduce costs. Managing our expenses is part of what we have to do here, but if we’re talking about 2.4% of GDP, I think the pressures are too great for such a big gap to be easily closed just by better enforcement and cost management.

University of Auckland Professor in Economics Robert McCullough, thinks that this tax debate will define the next election in terms of “if we’ve got these expectations, how are we going to pay for everything?”

We shall see. And as always, we will bring you developments as they happen.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

the winners of this year’s Tax Policy Charitable Trust Scholarship are announced.

A preview of next week’s United Kingdom Budget.

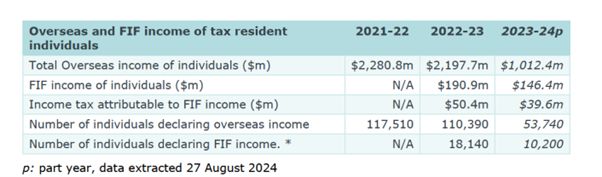

Inland Revenue regularly releases Official Information Act requests that it has answered. One from last month was in relation to the amount of overseas income reported by individuals. My attention was first drawn to this OIA by Robyn Walker of Deloitte (thanks Robyn) who like me, and many other professionals were quite surprised when we saw the number of people reporting Foreign Investment Fund (FIF) income.

Is there under-reporting?

According to Inland Revenue, which only really started gathering exact data on this in the 2023 income year, 18,140 individuals reported a total of $190.9 million of FIF income for that year.

When you consider that based on the latest Census 28% of the population of New Zealand were born outside the country, it seems to me that the amount of overseas income being reported, and in particular in relation to FIF income, is probably below what we would expect to see. And that’s what caught Robyn’s eye. One or two other advisors have made the same comment.

It could be because we deal in this space, there’s a bit of an echo chamber effect because we will regularly advise on these matters. If we’re dealing with a fairly high proportion of overseas migrants, and our practise Baucher Consulting does, then it’s natural we might think there is a broader scale of overseas investments generally.

But the number seems incredibly low in relation to the FIF income being reported, and also generally speaking, when you think about the number of overseas persons declaring overseas income.

A question of non-compliance

The issue therefore arises as to whether in fact we have non-compliance happening. I raised my concerns about this with Jenny Ruth of Good Returns. In our practice we regularly encounter clients coming to us who have realised that they have not been compliant with the Foreign Investment Fund regime. In some cases, they’ve come to us on another matter and in the course of discussions, it’s emerged that they have not been compliant. At any one time we are usually filing disclosures and bringing tax returns up to date.

Complexity and non-compliance

In my view this possible level of non-compliance speaks to the complexity of the Foreign Investment Fund regime. It’s not a capital gains tax, it operates as a quasi-wealth tax. That’s how I describe it to taxpayers and whenever I’m speaking to overseas advisors on the matter.

Old habits die hard

The FIF regime is not intuitive and I’m often dealing with people who come from overseas jurisdictions which have capital gains tax. They’re aware that where there’s a disposal there is a tax point that’s triggered. This may seem strange to say, but I’ve found in my practise that people’s tax habits developed in their country of origin take long to die even after many years in New Zealand.

Now, coincidentally, just to give some idea of the complexities involved in the FIF regime, Inland Revenue has just released a draft interpretation statement for consultation on the income tax issues involved in using the cost method to determine FIF income.

The Cost Method and the FIF regime

Those who have investments within the regime will be familiar that a fair dividend rate of 5% will apply to the value of your Foreign Investment Fund interest as of the start of the tax year. The alternative is to look at the total realised and unrealised gains of your portfolio including dividends over the year and report that instead, if that’s the lower amount. Incidentally that option way is not available for KiwiSaver funds or for the New Zealand Super Fund which is why it’s regularly one of the largest taxpayers in the country.

But what happens if your FIF interest is unlisted? The cost method generally applies when an investor is holding shares in an unlisted overseas company. And so this interpretation statement explains when that cost method may be applied and how it operates. As is now common, there are lots of examples and flow charts which explain the process. But the fact that there’s an interpretation statement on this matter which has set out and explains when you can or cannot use it the methodology, speaks to the complexity of the regime, and also the compliance costs involved in this.

The cost regime is generally to be used when the values of shares are not readily available. As part of that it will require the taxpayers to find and obtain an initial market value of the overseas stock, so they have a base cost for the purposes of the FIF calculations. It’s possible in some circumstances to use the net asset value of the accounts, usually if those accounts are audited.

Practical problems with the FIF regime

But as can be seen when people are required to obtain independent valuations this means additional compliance costs in what is already quite an involved regime. The other reason why the FIF regime causes consternation amongst taxpayers is the tax liability is not based on cash flows. A tax liability arises under the FIF regime even if the company in question is a growth company and not paying any dividends. Earlier this year I discussed a reportThe place where talent does not want to live, about the issues the FIF regime creates for startup companies and New Zealand resident investors.

All of this just underlines the complexities of the FIF regime. As I told Jenny Ruth of Good Returns, whenever I hear someone arguing “Oh well, capital gains tax is very complicated” I immediately think, ‘Well, they’ve clearly never dealt with the Foreign Investment Fund or financial arrangements regimes.’

Complexity leads to non-compliance?

Anyway, the upshot of all of this is there’s probably a considerable amount of non-compliance happening in in relation to reporting of FIF income. And Inland Revenue are now cracking down on this by making use of the information now available to them under the Common Reporting Standards on the Automatic Exchange of Information.

Now this is an OECD information sharing initiative which started in 2017. Inland Revenue which started a compliance project in late 2019 using this data. But then Covid turned up so that project had to be parked but it has now been reinitiated. As a result, I’ve recently taken on clients contacted by Inland Revenue advising it has received information under the Common Reporting Standards. The clients have been asked for an explanation about their apparent non-disclosure of overseas income and ‘invited’ to make the relevant income disclosures.

Keep in mind also that in the May Budget Inland Revenue was given $116 million over the next four years for investigation activity. The upshot is we’re probably going to see a lot more disclosures about FIF income when we’re looking at the numbers for the 2025 year.

In the meantime, I urge readers and listeners to consider their position and check with their tax advisor if they think they may have investments within the Foreign Investment Fund regime and have not made the disclosures they should have.

And the winners are…

Now moving on, the winners of this year’s Tax Policy Charitable Scholarship were announced in Wellington on Tuesday night. The Tax Policy Charitable Trust was established by Tax Management New Zealand and its founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa New Zealand. Three of this year’s finalists, Matthew Handford, Claudia Siriwardena and Matthew Seddon have appeared on the podcast over the past few months discussing their proposals.

The format for Tuesday night was that the four finalists, having already prepared a 4000-word final submission, would then present their proposals to a judging panel and the audience, as part of a Q&A.

The judging panel consisted of Joanne Hodge, who’s a former tax partner at Bell Gully and a member of the last Tax Working group. Professor Craig Elliffe Professor of Law at the University of Auckland and another member of the last Tax Working Group. Nick Clark, Senior Fellow of Economics and Advocacy at the New Zealand Initiative and Chris Cunniffe, Strategic Advisor of Tax Management New Zealand. A pretty daunting panel to be frank.

According to Chris Cunniffe “the quality of the presentations on Tuesday night was exceptionally good” and in the end the judges were unable to separate Matthew Seddon and Andrew Paynter.

Winners Andrew Paynter (left) and Matthew Seddon (right) with the judging panel

Matthew’s proposal, is to extend withholding taxes to payments received by independent contractors.

Andrew works as a policy adviser in Inland Revenue. His proposal is to increase the GST rate to 17.5% and introduce a GST refund tax credit for lower and middle income individuals. This would be a means tested individualised credit and would be paid at a flat rate to all qualifying tax resident individuals under a particular income threshold. It’s a fascinating proposal and I’ve reached out to Andrew about appearing on the podcast in the near future.

In the meantime, congratulations to the winners Andrew and Matthew and also to the runners up Claudia and Matthew Handford. Don’t be surprised if you see something popping up in legislation in the near future involving one or more of these proposals. They were all of a very high standard this year, so well done everyone.

UK Budget preview

And finally this week, a brief preview of next week’s UK budget. The new Labour government has been in office now for three months and it’s finally getting around to announcing its first budget. That is part of what they call the Autumn budget statement.

The UK has two budget statements a year, but this one is going to be quite significant because there’s a lot of noise and chatter around tax changes. A quite significant part of my practice at the moment is advising New Zealanders going to the UK, and migrants coming here, and the tax implications involved.

I’m therefore watching this budget with some interest because we know there are going to be two proposals, the final details of which will come out, which will have an impact for quite a number of people. Firstly the so-called foreign income and gains exemption, which is the UK equivalent of our transitional resident’s exemption. This was first announced by the Conservatives in their Spring budget in March this year, but then the General Election happened so full details of the proposals were not released.

Related to that, and this is surprisingly important for a large number of people, are changes to the domicile regime also announced by the Conservatives. At present domicile is incredibly important for determining a person’s liability for UK inheritance tax, which is payable at 40% above net assets over £325,000. It appears the UK will move to a more residence-based regime, but we don’t yet know the details.

I’m therefore watching this with great interest and there are bound to be other measures which are likely to affect New Zealanders going to the UK, or the UK migrants moving here. We’ll therefore keep you abreast of developments in next week’s podcast.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week the ninth edition of the OECD’s Tax Policy Reforms was released. This is an annual publication that provides comparative information on tax reforms across countries and tracks policy developments over time. This edition covers tax reforms in 2023 for the 90 member jurisdictions of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

Reversing the trend

It’s a fascinating document which tracks trends of what’s happening around the tax world at both a macro and micro level. The report has three parts: a macroeconomic background, then a tax revenue context, and then part three is the guts of the report with details of tax policy reforms around the world.

There is an enormous amount in here to consider and the executive summary lays out the ‘balancing act’ issues pretty clearly.

“Policymakers are tasked with raising additional domestic resources while simultaneously extending or enhancing tax relief to alleviate the cost-of-living crisis… On the one hand, governments further protected and broadened their domestic tax bases, increased rates, or phased out existing tax relief. On the other hand, reforms also kept or expanded personal income tax relief to households, temporary VAT [GST] reductions, or cuts to environmentally related excise taxes.”

A key observation for 2023 was a trend towards reversing the responses to the COVID-19 pandemic. Instead, as the report notes “2023 has seen a relative decrease in rate cuts and base narrowing measures in in favour of rate increases and base broadening initiatives across most tax types.”

“A notable shift”

This includes “A notable shift occurred in the taxation of business, where the trend in corporate income tax rate cuts seems to have halted with far more jurisdictions implementing rate increases than decreases for the first time since the first edition of the Tax Policy Reforms report in 2015.”

This is a pretty significant change. I think actually when you consider last week’s speech by Dominick Stephens of Treasury, it was setting out the context for why having got over the crisis of responding to the pandemic, countries are realising they’ve got to deal with the demographic issues of ageing populations and funding superannuation.

Climate considerations

Beyond these concerns, there is the immediate impact of climate change and its growing effects. The executive summary picks up on this issue:

“Climate considerations are also increasingly influencing the design and use of tax incentives, with more jurisdictions implementing generous base narrowing measures to promote clean investments and facilitate the transition towards less carbon intensive capital.”

And on that point, I hope all the listeners and readers down in Dunedin and Otago are safe and well at the moment.

Paying for superannuation

The other thing picked up is that in referencing that point I made a few minutes ago about population ageing. There has been a growing trend amongst countries to increase Social Security contribution taxes. Alongside Australia, and to a lesser extent Denmark, we are unique in that we don’t have social security contributions. However, elsewhere in the OECD social security contributions raise increasingly significant amounts of revenue.

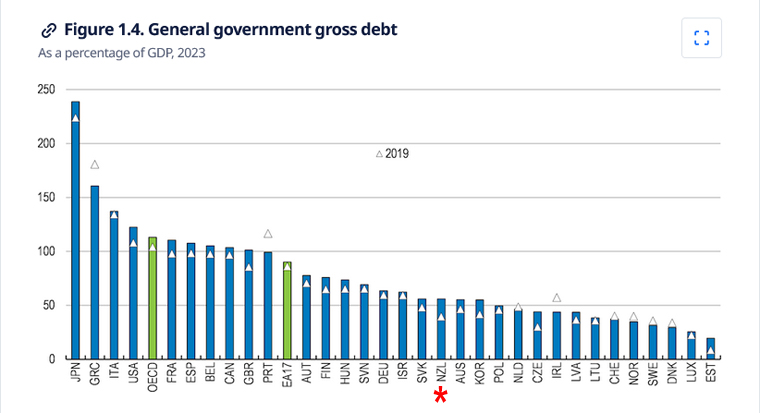

The report begins with a macroeconomic background. It notes that for the OECD as a whole in 2023 government debt rose by about nine percentage points, reaching 113% of GDP. For context, New Zealand’s debt-to-GDP ratio is just over 50%.

As the macroeconomic summary notes after generally decreasing in 2022 Government deficits increased again in 2023 following the energy crisis triggered by the war in Ukraine. Consequently,

“As debts and interest rates increased, interest payments have started to rise as a share of GDP. Even so, in 2023 they mostly remained below the average over 2010 to 2019, except notably for Australia, Hungary, New Zealand, the United Kingdom, and the United States.”

In short, we definitely have issues to deal with in terms of debt management and rising costs.

Responding to growing deficits

The report then notes that responses to growing deficits have been to start at increasing taxes. In general tax revenue terms,

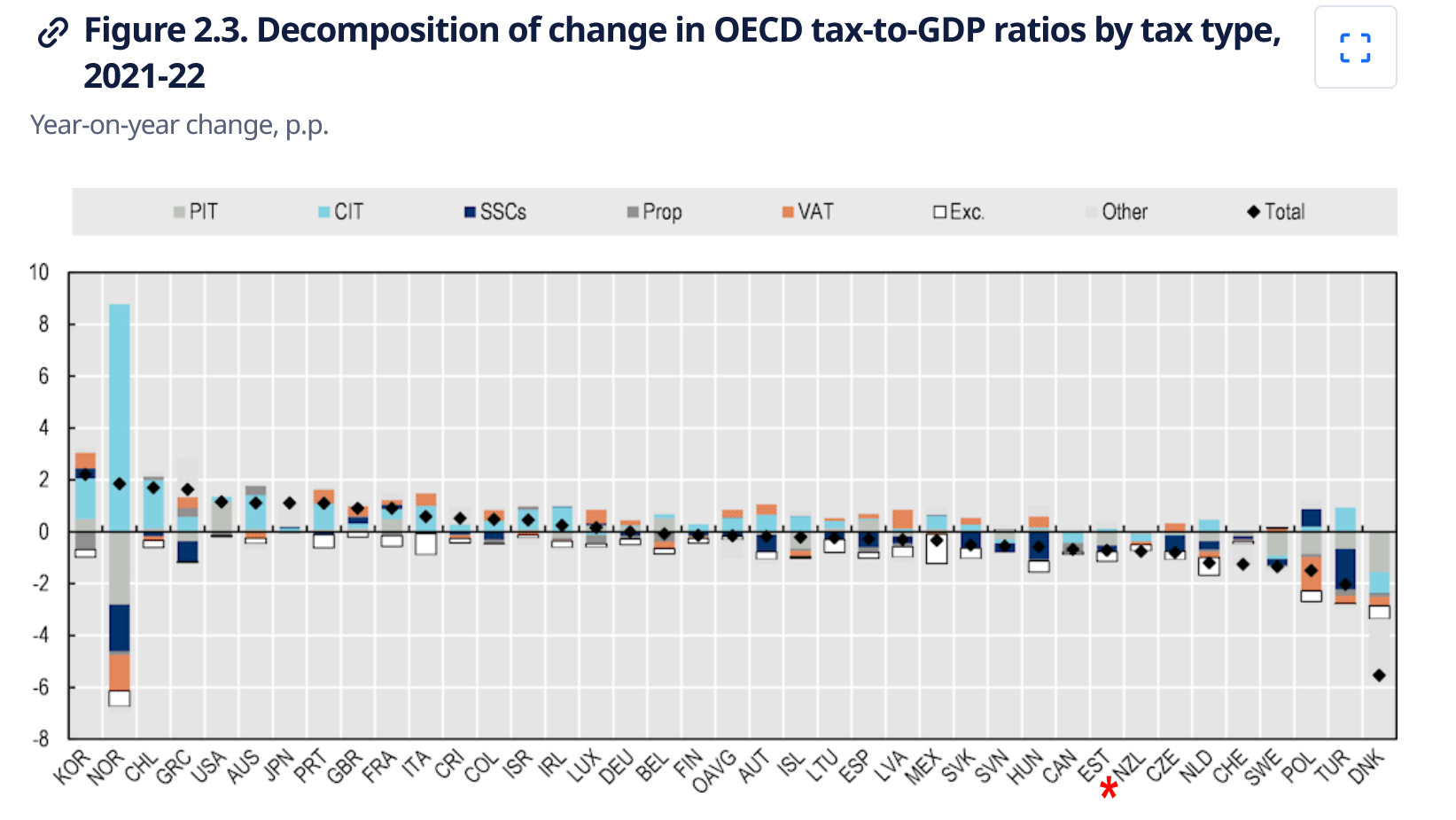

“From 2020 to 2021, the tax-to-GDP ratio rose in 85 economies with available data for 2021, fell in 38, and stayed the same in one. In more than half of these economies, the change in the tax-to-GDP ratio was under one percentage point, whereas 22 economies saw shifts greater than two percentage points in their tax-to-GDP ratio.”

Denmark saw the most significant drop of 5.5 percentage points, with New Zealand’s tax-to-GDP ratio falling by three-quarters of a percentage point, well above the OECD average fall of .147 percentage points. (Norway’s dramatic corporate income tax take increase of 8.775% is the result of “extraordinary profits in the energy sector”.)

Composition of tax base

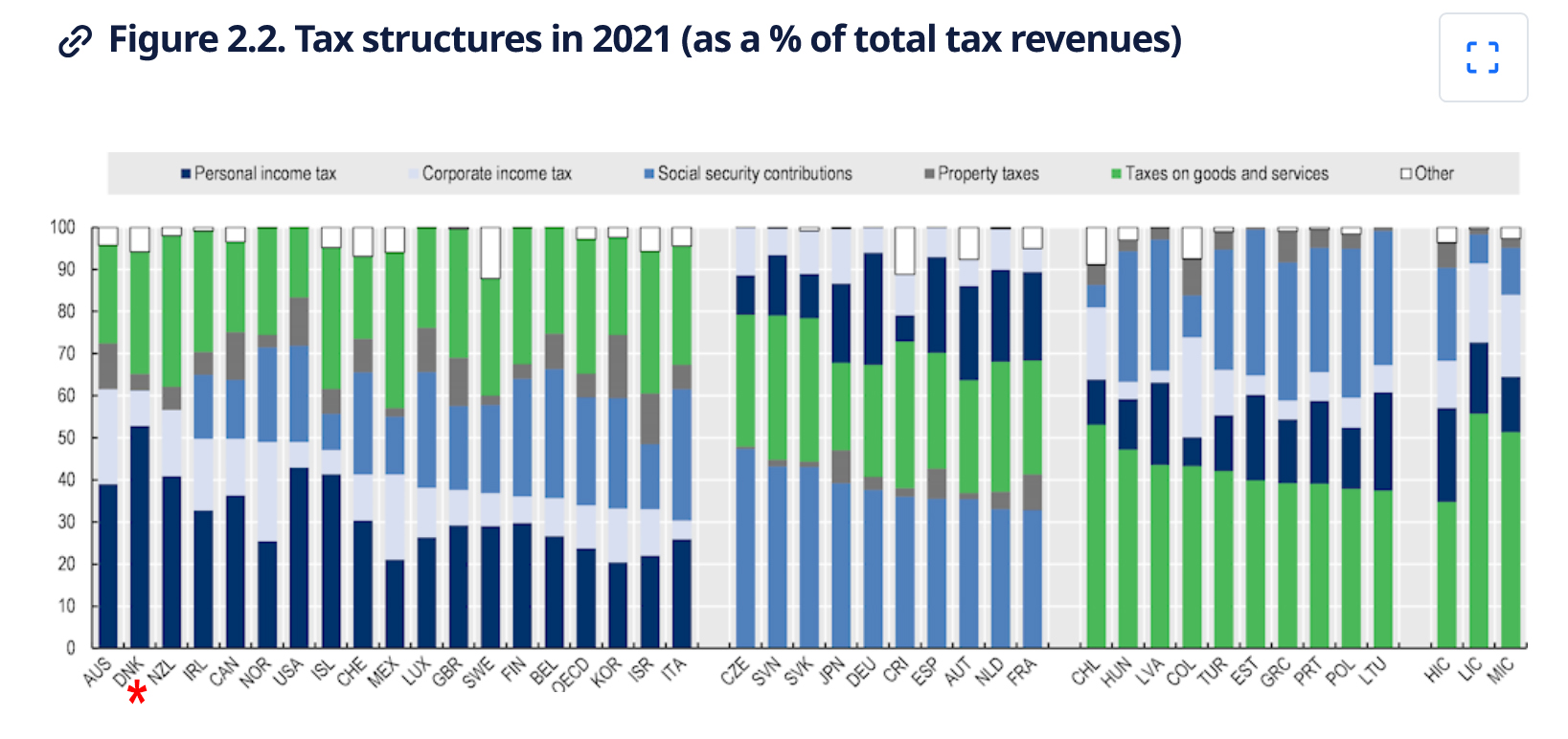

With regards to the composition of tax, 18 OECD countries (including New Zealand) primarily generate their revenues from income taxes, including both corporate and personal taxes. Ten OECD countries relied most heavily on Social Security contributions, and another 10 derived the majority of the revenues from consumption taxes, including VAT, (GST). Notably, taxes on property and payroll taxes contributed less significantly to the overall tax revenue mix in OECD countries during 2021.

Drilling into the detail

Part 3, of the report looks at the detail of the tax policy reforms adopted during 2023. This part has an introduction, then looks at five separate categories of taxes beginning with personal income tax and Social Security contributions, followed by corporate income tax and other corporate taxes, taxes on goods and services, environmentally related taxes and finally taxes on property.

As I mentioned previously, there was “a marked increase in the number of jurisdictions that broadened their Social Security contribution bases and raised rates”. Generally speaking, for high income countries personal income tax and social security contributions represent 49% of total tax revenue. Across the OECD personal income tax represented 24% and social security contributions 26% on average.

Here about 40% of all tax revenue comes from personal income tax. That’s one of the higher proportions around. Around the globe there was a bit of tinkering around personal income tax reforms mainly targeting lower income earners. This is an area where I think we need to focus any future reforms.

We have just (partly) adjusted thresholds for inflation and interestingly, I see that during 2023 quite a few jurisdictions did increase thresholds for inflation. For example, Austria updated its automatic inflation adjustment mechanism to counteract inflation, pushing workers into higher brackets. Meanwhile Australia increased its threshold for its Medicare levy to ensure low income households continue to be exempt, given that inflation has led to higher normal wages.

Corporate income tax rates are on the rise

Substantially more corporate income tax rate increases and decreases were announced or legislated by jurisdictions in 2023. Six jurisdictions increased their corporate tax,four of those did so by at least two percentage points. Türkiye increased all its corporate tax rates by five percentage points.

Whenever there are discussions about reforming our tax system, the issue of reducing our corporate tax rates will come up. With a 28% rate we are at the higher end of the corporate tax rate scale. There is potentially some scope, but as economist Cameron Bagrie has noted any such decrease needs to be part of a broader range of changes.

An example of such a change was the introduction of a general capital gains tax by Malaysia for all companies, limited liability partnerships, cooperatives and trusts from 2024.

Picking out of the details something which I know businesses here would look at with a certain amount of envy is more generous depreciation allowances. The UK, for example, has permanent full expensing for main rate capital assets as it’s called and a 50% first year allowance for special rate assets. Australia has also increased its thresholds for effectively fully expensing items for small businesses. Around the world there’s a whole range of incentives for R&D and environmental initiatives.

We have just limited the limits for residential interest deductions but it’s interesting to see that Italy abolished its allowance for corporate equity provision. Meantime Canada has new restrictions on net interest and financing expenditure claimed by companies and trusts.

Taxes on goods and services (VAT/GST)

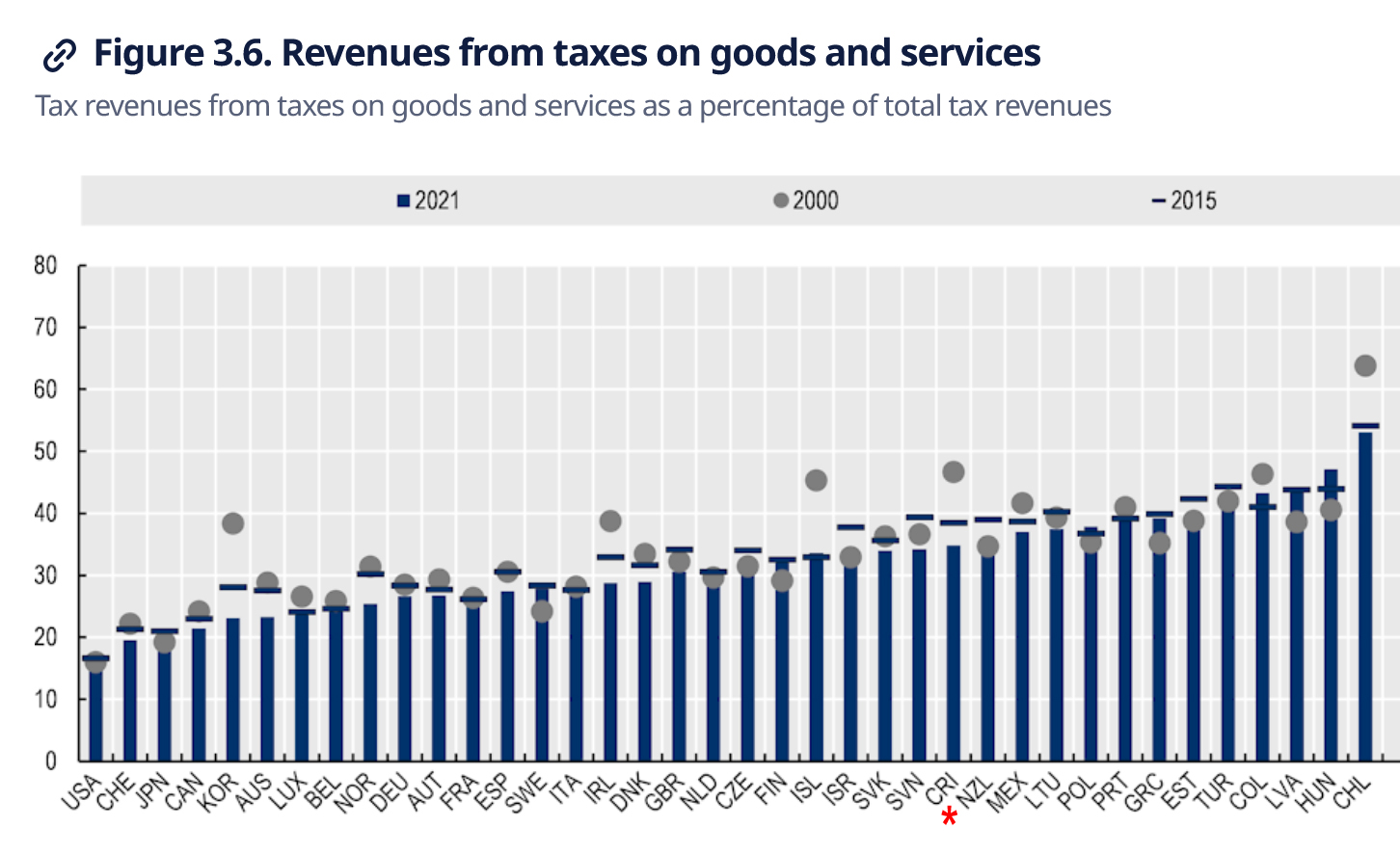

In the VAT/GST space, in terms of revenue from taxes on goods, although we have one of the most comprehensive GST systems in the world, New Zealand was only twelfth in the OECD for the percentage of tax revenue from goods and services as a percentage of total tax revenues. GST raises just over 30% of total tax revenue here, whereas Chile raises over 50%. This is quite interesting given how comprehensive our GST system is. It might mean that there is scope to expand the the rates of GST further. (Six countries including Estonia, Switzerland and Türkiye did so in 2023). But any government doing so should do so as part of a total tax switch package.

We discussed GST registration thresholds a couple of weeks back. During 2023 seven countries increased or planned to increase their VAT registration threshold. I was very interested to discover that Ireland has a split VAT registration threshold treatment: the registration threshold for the sale of goods is €80,000. But for the provision of services, it’s €40,000. I’ve not seen this split before. Meanwhile Brazil is undertaking the introduction of VAT/GST, which is a huge step forward.

A stable tax policy or just less tax activism?

There’s a lot to consider in this report more than can be easily covered here. Overall, it’s incredibly interesting to see what’s going on around the world. Many of the reforms discussed here involve threshold adjustments but there are plenty of new exemptions and incentives introduced. We generally don’t get into this space, that’s possibly a reflection of a very stable tax policy environment, but also perhaps a less activist philosophy by New Zealand governments which hope market incentives will work. Whatever, the approaches it’s interesting to see what’s going on around the world and I recommend having a look at this very interesting report.

ACC crackdown

Moving on, ACC has been in the news when it emerged that it has been chasing thousands of New Zealanders for levies on income they earned while working overseas.

According to the RNZ report, ACC sent 4,300 Levy invoices for the 2023 tax year to New Zealand tax residents who had declared foreign employment or service income in their tax return. The issue is that the person was often overseas at the time the income was earned and in some cases the the person has probably incorrectly reported the income in their return.

It’s an interesting issue and coincidentally, it so happens that I’ve just come across a couple of similar instances. My initial view is there seems to a bit of a mismatch between the relevant income tax legislation and the legislation within the Accident Compensation Act 2001. Watch this space on this one because I’m not sure the matter is entirely as cut and dried as ACC considers.

Inland Revenue responds to social media criticisms

A couple of weeks back, we covered criticism of Inland Revenue for providing the details of hundreds and thousands of taxpayers to social media platforms. It had done so as part of various marketing campaigns targeting people who owed taxes and Student Loan debt in particular.

Inland Revenue has now responded by putting up a dedicated page on its website, referring to customer audience lists.

In its words “social media is just one channel we use to reach customers. It is very effective at reaching people where they are.” As I said in the podcast Inland Revenue’s dilemma is it has to go to where the people are which is on the social media websites. In order to reach out to them it’s going to have to provide certain data. To reassure people the new page explains how it uses custom audience lists and what data is provided.

They do upload a list of identifiers such as name and e-mail addresses, which is then ‘hashed’ within Inland Revenue’s browser before being uploaded to the social media platform. This is where I think the tech specialists have raised concerns that the hash technique is not as secure as Inland Revenue thinks.

Australia – the Lucky Country again

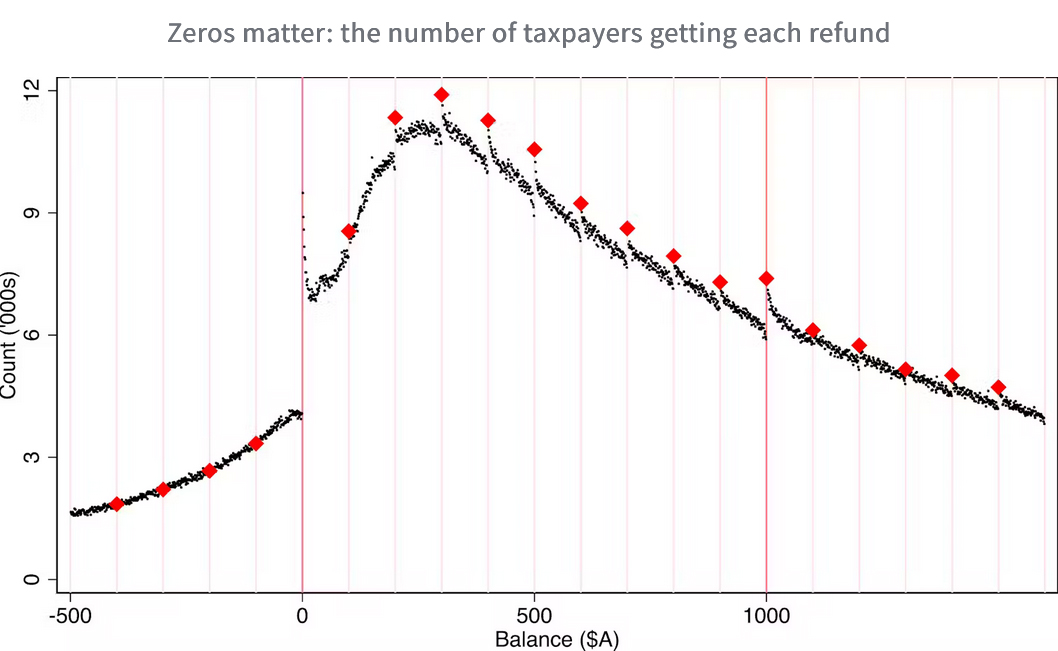

And finally, an interesting story from Australia about tax refunds. A research team at the Australian National University’s Tax and Transfer Policy Institute discovered a “striking” number of returns generating round number refunds (basically any digit ending in zero). The unit examined 27 years of de-identified individual tax files and found far more refunds of exactly $1,000 than of $999 or $995.

The unit concluded these returns are more likely to be driven by efforts to evade and minimise tax and are costly for the Australian Tax Office to audit such as work related expense deductions. Unlike New Zealanders, Australians can claim deductions on their tax returns. Somewhat concerning to me as a professional is that zeros in tax returns prepared by agents were twice as common as those prepared by taxpayers.

What this article is driving at is that some of the complexity of the Australian system results in the system getting gamed. Back in February you may recall Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue was a guest on the podcast. Based on our discussion and my own observation I would have confidence that Inland Revenue would not get caught out the same way thanks to the Business Transformation programme. As Tracy recounted, Inland Revenue can track live changes and they can see people just trying to square the return off to what they regard as an acceptable number.

Anyway, it’s an interesting story. It shows the differences between our tax system and that of Australia, but it does seem a little rich that not only can you earn more in Australia, but you get bigger refunds.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.