The United Nations Conference on Climate Change, COP 28, has just wrapped up in Dubai. The current Minister of Revenue, Simon Watts, is also the Minister of Climate Change so he attended the conference on behalf of the Government. There has been a lot of debate about how far COP28 has moved change forward although an agreement was finally reached on beginning a phase out of fossil fuels.

Now, coincidentally, or maybe not, as COP 28 was ongoing, the Climate Commission released its final advice to inform the Government’s plan to meet Aotearoa New Zealand’s greenhouse gas reduction goal for 2026–2030.

Briefly, the report says that the Government needs to take active steps to encourage change by removing barriers and supporting investment that cuts climate pollution. The Commission’s analysis is the country has made progress, but it is not on track to meet its climate goals for the end of this decade. In the Commission’s view, that means that we will be missing out on benefits like new jobs, a more resilient economy and healthier communities.

In all there are 27 recommendations which are focused on areas where the Commission sees there are critical gaps in action or where efforts need to be strengthened or accelerated. A couple of these are encouraging households and business to switch to electric vehicles and making it easier for more people to choose public or active transport. Key thing here which I think everybody would agree with, is sorting out the roles of the Emissions Trading Scheme and forests in achieving these objectives.

The paper, all 193 pages of it, does refer to tax being one of the tools to be used. For example,

“To support the transition to a low emissions economy, incentives need to be designed to overcome near-term capital constraints to businesses shifting their existing assets and processes to low emissions alternatives. To support this, the Government could explore amending components of the tax system (for example, adjusting depreciation schedules and rates for eligible projects).”

Overall, the Commission has no specific tax suggestions beyond such general suggestions.

Replacing the Ute Tax – a UK suggestion

As it happens, this week the Government repealed what it called the Ute tax and with it the current clean car discount scheme, which seems at odds with the report of the Climate Commission. In the Government’s Coalition Agreements, there was a proposal from ACT for “Work to replace fuel excise taxes with electronic road user charging for all vehicles, starting with electric vehicles.”

Now that also seems at first sight to be contrary to the Climate Commission’s recommendations for reducing emissions. But this week I came across a major report on the UK economy called “Ending stagnation. A new economic strategy for Britain”. This has been produced by The Economy 2030 Inquiry.

The TL:DR (too long: didn’t read) of this 293-page report is that Britain is in a far bigger mess than we might appreciate, and Brexit has done nothing to improve its position. The report has a whole heap of recommendations, including, inevitably, suggestions around changing the tax system which is what attracted my initial interest. I’m always interested to see what’s going on around the world and what goes on in Britain affects quite a large number of people here, either expat Brits or Kiwis who have family in the UK. I have several cases on the go at the moment involving UK New Zealand tax matters.

The report suggests one of the major challenges the UK economy faces is a transition to Net Zero. Which is also a challenge we face. As part of this the report makes the following suggestion:

“Our tax system also needs to keep pace with net zero transition. To ensure the burden of motoring taxes does not fall on poorer households yet to switch to electric vehicles, a 6 pence per mile charge (equivalent to fuel duty), should be introduced for [electric vehicles].”

Viewed in this context and stepping back from the emotions around the repeal of the Clean Car Discount, ACT’s proposal makes sense. Encouraging people to take up EVs is what we want to do long term. But that doesn’t mean those people should have a free pass indefinitely. EVs will soon be subject to road user charges which would be similar to this UK proposal. Therefore charging EVs some form of charge is not unreasonable.

My philosophy around environmental taxes is that the revenue from any such fund raising measures should not go into the general pool of taxation, but instead be ring fenced and applied for environmental measures. In this case my belief is those funds could be used to assist people to swap out older cars into newer cars. Those newer cars may still use fossil fuels, but they will be more fuel efficient, and that’s a worthwhile goal because it does reduce the motoring burden and emissions.

Time for a land tax and “mild increases” in tax revenues?

Incidentally the Economy2030 inquiry report specifically references our post 1984 economic transformation and how we dealt with the change involved in major economic reforms. Given Britain is pretty much in a huge hole and needs to change dramatically, the report looks at how we managed our transition post 1984. As part of that, a separate paper was prepared for the Inquiry by the former Reserve Bank of New Zealand Chair Arthur Grimes.

Incidentally, and in what’s becoming something of a trend for the new Government, Mr. Grimes’ paper makes suggestions contrary to the Government’s actions and intentions. Specifically, around tax breaks for owner-occupied rental housing, his report notes the current policies “increase wealth inequity.” He also believes a “mild increase in tax revenues will eventually be needed”. His suggestion is for “broadening the range of taxes to include a land tax, the most efficient and (vertically) equitable tax available to the Government, should be considered.” I can hear Raf Manji and the members of TOP cheering at this.

Anyway, there’s a lot to read in Arthur Grimes’ paper. I think it’s a good summary of what we went through and how our experience is relevant for other economies.

The deductibility of staff retention payments

Inland Revenue released an interesting Technical Decision Summary about payments made to retain key staff as part of a sale of a company. What happened was the company was being readied for sale and as part of this process the company entered into retention agreements with key staff. These were variations to their current employment agreements which entitled the key staff to bonus payments calculated by reference to their salaries.

And the idea was to incentivise these key employees to remain with the company to enable the ongoing smooth running of the company during the sale process. The payments were made prior to completion of the sale and were conditional on the employees remaining continuously employed by the company on the relevant payment dates.

The company in this case considered a portion of the retention payments were capital and therefore non-deductible because they were part of a capital transaction being the sale of the business. The case finished up before the Tax Counsel Office and its Adjudication Unit which decided that in fact the retention payments could be deductible in full as the capital limitation did not apply.

This is a very fact specific case which is often the case with Technical Decision Summaries. However, they do give insights into how Inland Revenue might approach a particular case. Bear in mind each is very heavily contingent on the facts. Nevertheless this is an interesting one which turned out to be a good result for the taxpayer.

HM Revenue & Customs One – ChatGPT Nil

On the other hand, it did not go well for one Mrs Harber over in the UK who in her appeal against various HM Revenue and Customs (HMRC) assessments used ChatGPT as part of her research.

She then presented these “cases” in evidence.

Unfortunately for Mrs Harber none of these cases were real, ChatGPT in its enthusiasm had just simply dreamed them up, and Mrs. Harber hadn’t realised this.

In fact, she asked the tribunal how it could be confident that the cases relied on by HMRC were genuine. The tribunal pointed out that HMRC had provided the full copy of each of those judgments and not merely simply a summary as she had done, and the judgments were also available on publicly accessible websites. Mrs. Harber had not been aware of those websites.

She obviously lost the case, but the Tribunal generally took her approach as more of misunderstanding her obligations so did not penalise over heavily in terms of costs, awards. But it is an interesting commentary on the perils of making use of ChatGPT and the need to have discernment.

WorkRide FBT exemption update

Last week I discussed the WorkRide Product Ruling Inland Revenue had issued which would give an FBT exemption to employers providing E scooters, E bikes and the like. I originally stated there’s a cost limit of $4,000.

Subsequently a couple of people contacted me and asked if that limit was correct. It’s not. I was actually referencing a submission I’d made to the Finance and Expenditure Committee proposing a FBT exemption. In fact, the limit will be set by regulation, but that limit has not yet been passed nearly nine months after the relevant legislation was passed. It’s expected by the way the limit will be higher than the $4,000 sum I mentioned. My apologies for the confusion.

What’s the character of the year?

Finally, what is the character of this year? It turns out that in Japan it is a tradition to decide the character (kanji) of the year in mid-December. Over in England, Professor Rita de la Feria the chair of tax law at the University of Leeds, heard from a student that the kanji for 2023 has just been announced and it is 税, or “tax”.

On that bombshell, that’s all for this week. Next week in our final podcast for 2023 we’ll be reporting on the Half Year Economic and Fiscal Update and the accompanying Mini-Budget.

Until then, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Coalition Government is not proposing to reduce the top rate of income tax from 39% in the near future. It’s therefore probably no coincidence Inland Revenue announced it has started contacting taxpayers it has already identified who appear to be “diverting their income and benefiting from their different tax rate”. Inland Revenue has suggested to tax agents to contact it if they think their clients might be affected and has actually given a specific e-mail address for tax agents to do so.

Prior to when the tax rate was increased to 39% in 2021, Inland Revenue released a Revenue Alert RA 21/01 on diverting personal services income. This Revenue Alert did was to pick up what had happened the previous time we had had a 39% tax rate and the famous, or infamous, depending on your point of view, Penny Hooper decisions. Those cases involved two surgeons who each provided their personal services through a company which was in turn owned by a family trust. Although they were each paid a salary, the salaries were not considered commercially realistic, and the Supreme Court ruled the arrangements represented tax avoidance.

The structures used in Penny Hooper are still commonly used today and with the big rate differential between the company tax rate of 28% and the top personal tax rate of 39% there is obviously a quite a heavy incentive to adopt structures to minimise the impact of tax.

Inland Revenue has been looking at these types of structures for some time. Last year it put out some proposals for “countering” abuse which received a fair bit of pushback when it proposed expanding the ambit of the so-called 80% one supplier rule. The effect of this expansion would have meant that a lot of smaller professional services firms would have been caught with more income subject to the individual personal tax rate.

Inland Revenue backed off on those proposals. However judging by what has been said by the new Minister of Finance Nicola Willis about the state of the Government’s books, combined with the fact that National’s proposed foreign buyer’s tax isn’t happening, means that the funding of National’s proposed tax relief package is rather tight to put it mildly. Against this backdrop I would not be at all surprised to see Inland Revenue reactivate those proposals from last year and push them forward again

I also expect that the increase in the trustee rate tax rate to 39% from 1 April which was included in a bill of the previous government, and which has just been reintroduced, will go through. It would be consistent to do so when considered as a base protection measure to ensure the integrity of the top personal tax rate of 39% is maintained. Whether there will be some form of de minimis exemption we will have to wait and see.

Tax deductibility when letting a room to a flatmate

Moving on, Inland Revenue has also released this week an interesting Question We’ve Been Asked which will be relevant to a number of people. QBWA 23/08 explains when a person can claim deductions for expenditure occurred in deriving rental income when that person rents a room in their home to a flatmate.

The amount of expenditure which will be deductible will be determined by apportioning between the private use portion of living in the house and the income earning proportion. Basically, you can apportion based on the relative proportions of physical space: if 20% of the house is being rented therefore 20% of the associated expenditure would be deductible.

The QWBA also covers off the application of other rules. For example, the interest limitation rules which we have been discussing quite frequently recently, these do not apply if the land is used predominantly for the person’s main home.

Similarly, the residential ring-fencing rule will also not apply if more than 50% of the land is used for most of the income year by the person as their main home. In theory if a homeowner had one flatmate and somehow it turns out there was a rental loss, possibly because of high interest payments, such a loss could offset against the home-owner’s other income.

Finally, the complex mixed-use asset rules shouldn’t apply either, because the house is unlikely to be left vacant for the required period of at least 63 days in a year. Even if the mixed-use asset criteria are satisfied the QWBA thinks the exclusion for long term rental property is likely to apply.

The QWBA also notes that in general the fact the person rents out a room in in their home to a flat mate while living in it should not stop the home being the person’s main home. Overall, this is an interesting QWBA even if only applicable in very specific circumstances. I think given the way interest rates have risen and the large mortgages some people have had to take on to get into the housing market makes it of more relevance appears at first sight.

WorkRide FBT exemption

Another bit of good news this week is the release of a Product Ruling in relation to provision of self-powered or low-powered commuting vehicles to employees of WorkRide’s customers.

Under the WorkRide scheme it enters into agreements with employers under which the employees of WorkRide’s customers agree to a temporary reduction in salary in return for a temporary lease of an electric bike/electric scooter and the opportunity to own the bike/scooter at the end of the lease period.

Under the ruling so long as the limits of the cost of the equipment being provided to an employee are not exceeded then the employer is not liable for Fringe Benefit Tax (FBT) on the value of the bike/scooter provided. The employer can claim the GST charged on the leasing of the equipment to it by WorkRide. The amount of the salary sacrifice agreed between the employer and the participating employee cannot exceed the amount of the service fee charged by WorkRide. The amount of salary sacrifice does represent a taxable supply for GST purposes.

It will be interesting to see how many people take up the exemption which certainly should be attractive to those working in inner city areas.

$1.4 billion of interest deductions claimed for 2021-22 tax year

Finally, this week, coming back to interest deductions, tax guru and former podcast guest John Cantin posted on LinkedIn earlier this week an Inland Revenue response to an OIA request he had made regarding the amount of interest deductions claimed by residential property investors in the 2021-22 tax year together with the amount of rental losses “ring-fenced”.

In summary,140,660 taxpayers claimed interest deductions totalling just over $1.4 billion. 47,490 of these had $663.9 million of rental losses ring fenced after deducting 563.9 million. Therefore 93,170 taxpayers claimed interest deductions totalling $845.6 million, which were allowed in in full. This means about a third of all taxpayers (33.7%) had their interest deduction effectively limited and this amounted to about 40% of the total interest deductions.

We don’t know the exact fiscal effect, that’s dependent on each taxpayer’s marginal tax rate. Assuming an average 20% rate, the cost would be $169 million and on a 33% tax rate $279 million per annum.

These figures are for the first tax year in which the restrictions kicked in, which was 25% non-deductible from 1st October 2021. The first full year of restrictions is for the year ended 31 March 2023. But the data for that year won’t be available until after March next year when the filing period for 2023 tax returns is over. You can still see there’s quite some significant numbers here around the impact of restricting interest deductions and therefore the cost of removing those restrictions.

Incidentally on this I’d be very interested to see what happens going forward for investors buying properties which don’t qualify as new builds. At present such investors aren’t to claim interest deductions and that was a deliberate policy decision by the Labour government. Could the new Coalition Government change that rule to allow interest deductions subject to the interest limitation rules for the relevant period. We shall see, and as always, we will bring that news when and if it happens.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

More details have emerged about the Coalition’s tax plans with a surprising twist that changes to interest deductibility for residential property investors have effectively been backdated to 1st April this year. Like many others when I was discussing this last week, I assumed that the reference to 2023/24 was to the Government’s financial year ending 30 June 2024 and the increase to 60% deductibility would kick in from 1st April 2024. (National’s own workings released during the Election use a 30 June year-end).

But this week the ACT Party clarified the increase in deductibility to 60% is in effect for the current income year, ending on 31st March 2024. So effectively, it’s backdated to the start of the year on 1st April. That caused a wee bit of a stir, because something of this nature hasn’t been done in a while. I can’t recall a new government coming in and announcing a tax measure effectively having a retrospective effect.

The change accelerates the restoration of full interest deductibility. It means that from 1st April 2024, interest deductibility will rise to 80% and then will be fully 100% deductible from 1st April 2025. So, within the next 16 or so months, it will be restored to full deductibility. However, as CTU Chief Economist Craig Renney pointed out this acceleration adds another $900 million over the forecast period to the cost of restoring interest deductibility.

Changes to provisional tax?

One of the practical implications of the change is an interesting debate around what action landlords who are provisional taxpayers should take. Such landlords would have paid the first instalment on 28th August. This would have been done based on either 110% of the residual income tax for the 2022 tax year, or 105% of the residual income tax for the 2023 tax year. In both cases, the interest deductibility proportion was higher, so the change might not have an effect. On the other hand, interest rates were lower in both years, particularly in 2022.

What I think you’ll almost certainly see is taxpayers will be keen to understand the impact of the change and how it will affect their provisional tax. My general view would be to pay on 15th January as normal, but then have a really close look before the final instalment on 7th May next year when you should have a fairly good idea of your likely tax liability for the year.

Still there are options to perhaps consider reducing the next amount of provisional tax. And some will take advantage of that. Of course, the risk comes that you may have to pay use of money interest at 10.93%. Although tax pooling can help with that.

What else is now clear?

The release of the Government’s 100 day, 49 point action plan makes clear the Auckland Regional fuel tax is to be abolished and increases to the fuel excise duty will not go ahead. No surprises there as National campaigned on these initiatives. The Clean Car Discount is set to go by the end of this year.

A $900 million bigger hole

As I mentioned earlier, one of the fallouts of the change in the timing of the restoration of full interest deductibility for residential property is an extra blow out by $900 million dollars. One of the apparent means of meeting that gap is the rollback of smokefree legislation, which was set to be world leading. Ironically, several countries seem to have decided to follow our previous example.

The smokefree changes have caused quite a stir. Bernard Hickey in his daily substack The Kaka said that Treasury had estimated that using a 3% discount, smoke free legislation would cut public health costs by $5.25 billion. But that’s now being kicked down the road.

We’ll know more about progress on other measures to fill this gap when the Half Year Economic Fiscal Update, and the promised Mini-Budget are announced on 13th December.

Time to legalise and tax marijuana? The Colorado example.

But if we are looking at the question of raising taxes, or essentially getting more tax revenue from tobacco excise duty, then I’m going to pick up a point that I’ve had for some time and ask why not legalise and tax marijuana. Now, yes, there was a referendum which voted against that. But referendums are not binding on governments. I also think there are second order benefits of legalisation including putting a hole in organised crime’s finances.

At present 24 states in the United States of America have now legalised or decriminalised marijuana. One of those is Colorado, which has a population of just over five million, more or less identical to Aotearoa New Zealand.

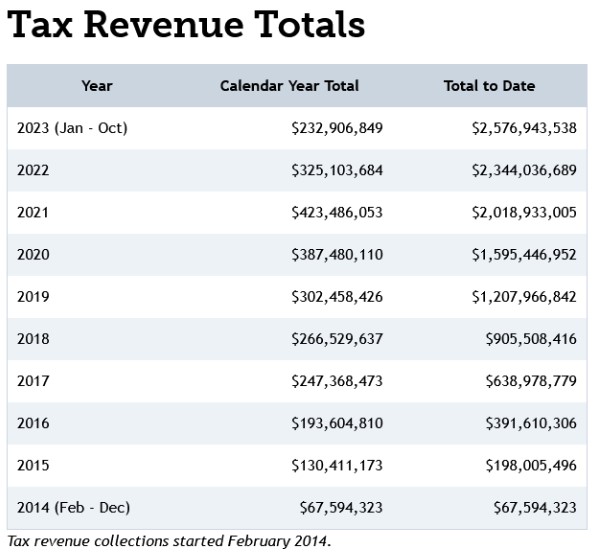

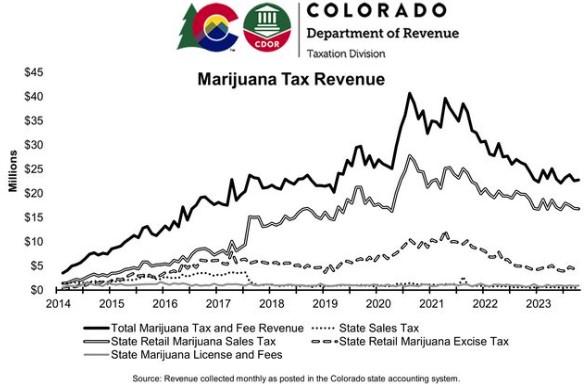

Colorado legalised marijuana in 2014 and have been taxing it since then. The taxes comprise the state sales tax (2.9%) on marijuana sold in stores, the state retail marijuana sales tax (15%) on retail marijuana sold in stores, and the state retail marijuana excise tax (15%) on wholesale sales/transfers of retail marijuana. In addition, Colorado also has fee revenue coming in from licensing and application fees.

Colorado’s Department of Revenue publishes monthly marijuana tax reports, and between February 2014 and October this year it has collected over US$2.5 billion from marijuana taxes. That’s over NZ$4 billion.

However, whether you are taxing smoking or marijuana, long term, the revenue should decline to nil, because ultimately we want people to not smoke because of the health order benefits. You can see this in Colorado’s marijuana tax revenue which rises quite steadily initially but then since mid-2021, it has started to fall away. This is probably the second order effects of people stopping smoking altogether.

But anyway, on average, the tax take is settling down to about US$300 million a year which is roughly $500 million New Zealand dollars. That’s actually a not insubstantial amount of revenue.

So that’s the Colorado example. I’m not going to say it’s going to happen here under the new Government. But you never know. Henry Kissinger died yesterday, and the relevance of that is that he was the one who coined the phrase “Only Nixon could go to China” which opened the door to a US rapprochement with China.

The phrase means bold leadership could surprise people by doing the unexpected. Bear in mind, back in 2015, John Key and Bill English surprised everyone by introducing the bright-line test. The point by referencing Kissinger and Nixon, two of the nastier people of the 20th Century, is that a bold and welcome change of direction can come from an unexpected source.

Revision of the bright-line test – when?

Speaking of the bright-line test, it isn’t specifically mentioned in the 49-point first 100 days action plan the Government announced on Thursday. I imagine we’ll get the timeline for revision at the Half Year Economic Fiscal Update.

“Overlooked” some income? The clock never stops ticking for Inland Revenue

This week Inland Revenue released five Technical Decision Summaries with a common theme relating to disputes over omitted income and penalties. To recap, Technical Decision Summaries are anonymised summaries of adjudication decisions made by a unit within Inland Revenue’s Tax Counsel Office as part of the formal dispute process between Inland Revenue and taxpayers.

The facts vary slightly in each summary, but all involve some form of income diversion/suppression which was picked up by an Inland Revenue review. For example in TDS 23/18 the taxpayer was the sole director and shareholder of Company B which carried on a retail business. The taxpayer also held 49% of the shares in Company A which operated a retail business. Y, who was married to the taxpayer, was Company A’s sole director and held the remaining 51% of its shares. The Taxpayer was also a settlor, trustee, and beneficiary of a Trust which was involved in property investment. (This is a fairly common structure in my experience.)

The Taxpayer filed income tax returns showing wages from which PAYE had been deducted and shareholder salary from Company B and income from the Trust. But on review by Inland Revenue, it appeared that money from Company B had been deposited into the taxpayer and his wife’s personal accounts partner and then used to pay personal expenses and to fund a property major purchase made by another company. These deposits had not been declared as income.

Inland Revenue proposed taxing this income and included a shortfall penalty for tax evasion. The shortfall penalty for tax evasion is 150% of the tax that’s been evaded, although in this case it will be reduced by 50% because of previous good behaviour.

What is also of note here and the other four Technical Decision Summaries is that the four-year time bar period for many tax returns had passed in respect to some of the years in dispute. (Generally, Inland Revenue can’t increase an assessment if it’s more than four years after the end of the tax year in which the relevant return was filed). The taxpayers tried to rely on the time bar rule but Inland Revenue argued it did not apply because of tax evasion and omission of income.

And that is how it panned out. The Tax Counsel Office’s Adjudication Unit ruled there is assessable income and the time bar provision is not applicable because of tax evasion and/or omission of income. Accordingly, the shortfall penalties also applied.

As I mentioned the other Technical Decisions Summaries involved similar issues and had similar outcomes. In TDS 23/16, there was a further problem for the taxpayer in that they were trying to make a subvention payment, to offset losses. And that was also turned down because of a lack of common shareholding.

There are some good lessons from these summaries, primarily if you don’t declare income, don’t try and rely on the time bar to stop Inland Revenue looking at earlier years. As the summaries make apparent it’s very clear Inland Revenue has the power under sections 108 and 108A of the Tax Administration Act 1994 to assess older years that would normally be time barred. In such circumstances, shortfall penalties for tax evasion will almost always apply.

“A really good idea”

As I mentioned last week one of the things that was surprising about the Coalition’s tax policies is the additional resources for Inland Revenue’s audit and investigation activities. On TVNZ’s Q+A last Sunday Minister of Finance Nicola Willis said that she welcomed the proposal which she thought “was a really good idea.”

We’ll only know exactly how much extra funding Inland Revenue is going to get in the Budget next May. But for the moment, you can expect Inland Revenue to be cranking up its investigation activity, and you can expect to see a lot more shortfall penalties kicking in.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

When the shape and tax policies of the new Coalition Government were announced one of the first surprises for me was the appointment of Simon Watts, the National MP for North Shore, as Minister of Revenue. I was surprised by this because Andrew Bayly has been National’s Spokesperson for Revenue for the past four years.

During that time, he has built up knowledge and background in this area. And I know that colleagues who have met him believe he understands the issues involved in the portfolio. So, it is a surprise to see Andrew overlooked for this portfolio. Obviously, there are reasons behind that, but it still means that Simon Watts will be picking up a portfolio with little background knowledge on how Inland Revenue has been operating. But no doubt he’ll get up to speed quickly. It will be interesting to see what’s in the Inland Revenue and Treasury Briefings to Incoming Minister. And we’ll report on that when those briefings are released in due course.

No foreign buyer’s tax but plenty of “buffer” still

In terms of the headlines about what what’s happened, it is no surprise to hear that the foreign buyers’ tax proposed by National is off the table. That was obviously a precondition of getting New Zealand First on board. The coalition is “committed to delivering tax relief” with increases to tax thresholds from 1st July 2024.

But beyond that, it’s not clear what’s to happen. National’s agreement with Act confirms “…no ongoing commitment to income tax changes, including threshold adjustments beyond those to be delivered in 2024.” Furthermore, the two parties recognise “that details of [National’s] Fiscal Plan may be subject to amendment in response to significant new information or events.”

The agreement with New Zealand First refers to letting “Kiwis keep more of what they earn with tax relief of up to $100 per fortnight for an average income per household and a Family Boost childcare tax credit of up to $150 per fortnight.”

At the press conference following the signing of the Coalition agreement the incoming Prime Minister Luxon, said in response to the cancellation of the foreign buyer’s tax that National believes there is a “buffer” available to allow the proposed tax threshold adjustments to happen next July. They actually have a buffer around the finances.

Interestingly, when you go through both coalition documents there is no reference to “budget surplus” in either document. But there is a commitment to restore fiscal responsibility and deliver value for money. So, what does that mean? It could be that the Coalition might be prepared to allow deficits to run longer than was previously said. Otherwise, there’s no mention of how the gap created by the lack of the foreign buyer’s tax will be met. We might get a clearer idea with the mini-Budget which is going to be part of the Half Year Economic Fiscal Update to be released in mid-December.

Accelerated restoration of mortgage interest deductibility

National campaigned on a phased restoration of full mortgage interest deductibility for residential rental properties. That timeline will be accelerated under the agreement with Act. From 1st April 2024, it’s going to be 60%, then 80% from 1st April 2025 and 100% from 1st April 2026.

The agreement with Act includes the repeal of the Clean Car Discount and a commitment to

“Ensure the concepts of Act’s income tax policy considered as a pathway to delivering National’s promised tax relief subject to no earner being worse off than they would be under National’s plan.”

A couple of New Zealand First surprises

There are a couple of interesting initiatives in the New Zealand First agreement neither of which were part of their election policies.

The first is “By or before 2026, assess the impact inflation has had on the average tax rates phased by income earners.” This is an implicit acknowledgment of the impact of not increasing income tax thresholds since 2010. We should actually get a measure of the consequential effect of fiscal drag. I wonder if this initiative would include Working for Families’ abatement level. However, there’s no commitment to take action on the findings.

More funding for Inland Revenue investigation

More importantly, and already incoming Minister of Finance Nicola Willis has included the impact of this in the “buffer”, the Coalition Government will “increase funding for IRD tax audits to urgently expand the IRD tax audit capacity, minimise taxation losses due to insufficient IRD oversight, and to ensure greater integrity and fairness in our tax system.”

How this will be achieved, is going to be very interesting to see. Obviously, it should mean an increase in resources for Inland Revenue. Exactly how much we probably won’t see the full details until the full year’s Budget next May. Still, this is a surprise, including the fact that it has got sign off from Act as well, who are generally committed to lower taxes. (Incidentally, Inland Revenue ought to be safe from Act’s proposal to reduce the public sector headcount by reference to a 2017 baseline, because its staffing level has fallen from 5,519 in June 2017 to 4,130 in June 2023).

Sharing GST with Councils?

The agreement with Act contains a couple of other proposals of varying interest. Firstly, the new Government will not progress the development and delivery of National’s manifesto commitment to a “Taxpayer’s Receipt” for taxpayers. Although minor it’s interesting that Act didn’t want that.

On the other hand, in terms of local government financing, there’s a couple of things here which I think are really interesting and potentially significant. Firstly, they are to consider sharing a portion of GST collected on new residential builds bills with councils. This is part of Act’s commitment to wanting to expand development and housing, that it thinks there should be more revenue sharing going on councils. I agree we should be looking at how councils fund themselves because my view is the current model is unsustainable, particularly for very small councils. A shake up in this area is well overdue and sharing GST receipts is one option going forward.

Road user charging & a congestion charge for Auckland?

The Act agreement calls for work to replace the fuel excise taxes with electronic road user charging for all vehicles starting with electric vehicles, which are currently exempt from road user charges. Does this mean the Auckland regional fuel tax isn’t to be repealed until this new system is in place? The agreements are not clear on this point. [It appears that unless a specific National policy is covered by one or both the agreements it remains National policy. This would appear to include the reduction in the Bright-line test timeframe to two years].

During the election campaign Auckland Mayor Wayne Brown asked if the Auckland regional fuel tax goes how was Auckland going to fund that gap.

The Act agreement has a specific commitment to “Work with Auckland Council to implement time of use road charging to reduce congestion and improve tight travel time reliability.” Again, that’s something that Mayor Wayne Brown has mentioned recently. And maybe it’s tied into that question of a replacement for the regional fuel tax.

A public health levy?

Also of interest in the Act Coalition Agreement is a reference in its immigration policy introducing “a five-year renewable parent category visa, conditional on covering healthcare costs, with consideration for public health care levy.” It’s not clear whether this levy refers to those people coming in under that immigration category or a wider public health care levy. It doesn’t appear to be a commitment in Act’s election promises.

39% trustee rate

The Agreements are silent on whether the outgoing Labour Government’s intention to increase the trustee tax rate to 39% will be implemented. This is part of an existing tax bill which lapsed when the last Parliament rose. This particular bill must be reintroduced because it includes setting the annual income tax rates, which must be passed each year to enable the funding of the government. This initial silence implies that that the increase in the 39% Trustee tax rate is going to remain. We’ll have to wait and see but we’ll probably get more specific information when the Half-Year Economic Fiscal Update is released next month.

(This is an edited transcript of part of the Podcast recorded on Friday 24th November)

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

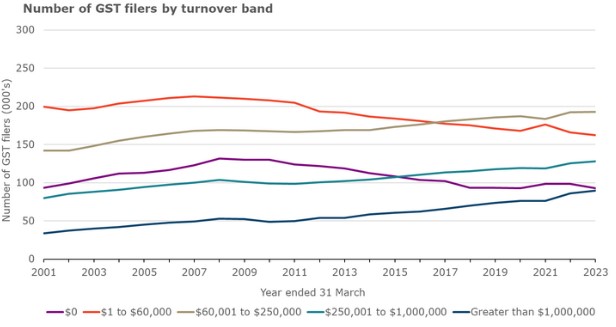

This week, Inland Revenue published a reminder aimed at tax agents that clients must have a taxable activity in order to be registered for GST.

The notice said if your client is filing regular GST refund returns with expenses consistently more than their income, it may suggest they are not carrying out a taxable activity or have errors in their GST returns.

Inland Revenue then notes that clients “may receive a letter if they have filed regular GST refund returns from registration.” Tax agents are advised to “please review the refund returns filed and if required take any necessary action”. Inland Revenue then add that letters may be sent to clients who have been filing regular GST refund returns in the last 36 months.

If anyone receives such a letter their response will be expected to include one or more of the following:

a description of the taxable activity or activities undertaken and an explanation for the regular GST refunds.

A voluntary disclosure to correct any errors in the GST returns,

Cancellation of the GST registration if they are no longer carrying out a taxable activity. The final GST return should be filed with the required adjustments.

Inland Revenue are clearly about to run a campaign on this issue. Based on Inland Revenue’s statistics during the year ended 31st March 2023 there were just under 100,000 GST registered persons with nil turnover. (About the same number as have turnover exceeding $1 million). There’s another 160,000 or so who have a GST turnover of between $1 and $60,000.

According to Inland Revenue the net GST refund paid to GST registered persons with turnover below $60,000 has increased from $463 million in the March 2001 year to $1.473 billion in the March 2023 year.

Clearly Inland Revenue has looked at this and thought “How genuine are some of these GST registrations?” It will probably be looking at some of the lifestyle blocks that I’ve encountered with some grazing income, but the expenses of running outweigh the grazing income. Inland Revenue looks to be gearing up for a campaign to review those such clients in some detail. We’ll track to see what happens on this and give you updates as and when information emerges

When is a subdivision project a “taxable activity” for GST purposes?

Moving on and still on the matter of GST, and actually on the question of carrying on a taxable activity, Inland Revenue has just released a draft Question We’ve Been Asked (QWBA) for consultation on when is a subdivision project a taxable activity for GST purposes.

Following the 1995 Court of Appeal decision in Newman, Inland Revenue had issued a Policy Statement on this issue.

Under the Policy Statement whether a subdivision project is a taxable activity for GST purposes depends on the facts of each case. Determining this takes into consideration factors such as the scale of a subdivision, the level of development, work time and effort involved, the amount of financial investment and the commerciality of the transaction. Based on this the general view was if a person carried out a subdivision involving three or four sections, it was likely to not represent a taxable activity for GST purposes.

28 years on, it’s not unreasonable for Inland Revenue to come back and look at the matter again. In the draft QWBA the Commissioner considers most of these factors are still relevant when considering whether a subdivision is a taxable activity. However, the draft clarifies and, in some respects, differs from the previous Policy Statement.

According to the draft QWBA in determining whether a subdivision represents a GST taxable activity “the most relevant factor will generally be whether the activity is carried on continuously or regularly. This Question We’ve Been Asked focuses on this factor.”

Following on from this, paragraph 29 of the draft states,

“Generally, the Commissioner considers the level of development work involved in the construction and sale of a single house or other residential dwelling as part of a subdivision is not on its own enough for an activity to be considered carried on continuously or regularly.”

On the other hand, the construction and sale of multiple residential dwellings or a large commercial building is more likely to be continuous or regular. This is an interesting change in tone since 1995. But also, when you think about it, the change reflects how generally speaking, it has become easier to subdivide. Certainly, in Auckland if not necessarily everywhere, it has become easier to subdivide.

Clearly, Inland Revenue is seeing a lot of activity in this space. And the question is then arising, well, at what point does a simple subdivision become a GST taxable activity? Hence this updated QWBA.

As I mentioned a few minutes ago, there was always a sort of general conclusion from Newman that maybe three or four lots carved off would not be a taxable activity. But as the draft notes, there’s no specific number of lots created that determines whether a taxable activity exists. Our case law indicates that where a subdivision activity involves the creation and sale of multiple lots, it MAY be a taxable activity. But it doesn’t necessarily mean a subdivision involving creation and sale of multiple lots will always be a continuous activity because, for example, a subdivision is so straightforward that the number of lots sold is not significant, but it does in revenue.

But…a single section could be a taxable activity

Paragraph 32 of the draft notes although an activity leading to the supply of only one section will not usually be considered an activity carried on continuously or regularly, “this does not mean an activity leading to one supply can never be a taxable activity”. It could be that if other factors are sufficiently present, such as the scale of the subdivision or the level of development work. This will be this will indicate the activity is continuous, even if it leads to only one supply. For example, the construction and sale of a single commercial building on subdivided land would be an activity carried on continuously and regularly.

Changes from previous policy

The previous policy referred to the commerciality of the project as a factor but Inland Revenue have now decided that commerciality is no longer significant. In addition, there was an example in the previous Policy Statement where the construction and sale of a tea shop on subdivided land would represent a taxable activity. However, this draft QWBA now considers that building a tea shop would not normally involve more activity at work than that involved in constructing a residential building and therefore would not meet the criteria to be a taxable activity.

No GST, but what about income tax?

The draft also adds a reminder that although it is focused on GST, even if a subdivision activity is not a taxable activity for GST purposes, the resulting sale may still be subject to income tax. This might perhaps be under the bright line test. But there are other provisions that specifically deal with subdivisions carried out within ten years of acquisition. A useful reminder that although a transaction might not be within the GST net, it could well still be subject to income tax.

A few examples

There are some good examples at the end of the draft QWBA. It’s just worth repeating again that the material being put out by Inland Revenue is much more accessible than it was in previous years. The draft contains a good example about a basic subdivision then, which would not be a taxable activity because it’s not carried on continuously and regularly.

Example four illustrates the GST issues where a subdivision is part of an existing taxable activity. Now this is a question that does pop up quite regularly in my experience. In this case, Loammi and Marissa are GST registered as a partnership with a taxable activity of residential property development. They buy dilapidated houses and renovate them to sell for a profit.

In this example they realise they could make a larger profit on a particular piece of land by subdividing before sale. And therefore, even though the subdivision and sale would not be a taxable activity on its own, in this case the sale of the subdivided land is a taxable supply because it was done in the course of furtherance of their existing taxable activity

Overall, this draft QWBA is probably a good warning for anyone considering subdividing property, maybe carving off two, three or four sections, and thinking that that would not represent a GST taxable activity. This view is no longer so clear cut. Like much of tax it’s fact dependent. It’s also another good example where it pays to get good advice beforehand, otherwise a nasty GST surprise could be awaiting.

Foreign Investment Funds – a welcome change of heart from Inland Revenue

Finally, a few weeks back I discussed an interesting Inland Revenue Technical Decision Summary about which methodologies must be used to calculate income under the Foreign Investment Fund (FIF) regime. Under the FIF regime individuals and trusts may switch between the fair dividend rate, which applies a flat 5% to the opening value of a persons FIFs or the comparative value, which looks at the gains, losses and income during the year.

However Inland Revenue had suggested this could not happen where people were making voluntary disclosures of FIF income for prior tax years, something I see quite frequently. Inland Revenue’s proposal was this ability to change methodologies was not available and all taxpayers making voluntary disclosures would be required to adopt the fair dividend rate.

This prompted a fair bit of pushback from quite a number of advisors, including myself. I’m pleased to say that Inland Revenue has now issued an updated draft QWBA on this matter. The updated QWBA notes the Commissioner accepts that taxpayers have a choice of methods to calculate income, even if they fail to declare the income in a tax return and later file a voluntary disclosure or fail to file a tax return by the due date and later provide one including the FIF income.

This updated QWBA is another example of the Generic Tax Policy Process working with Inland Revenue taking on board feedback from advisers. It’s a good result for taxpayers. I was concerned that if Inland Revenue adopted a harsh approach on this, then people would just simply stay in the undergrowth and hope that Inland Revenue never noticed them. And that’s not good for the tax system at all, where you’ve got people who are become compliant and feel that they are unfairly penalised for doing so. Meanwhile other non-compliant persons see this and decide to just take a chance on not being caught in the first place. This is never a wise approach in my view.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.