more feedback on Inland Revenue’s long-term insights briefing

an interesting Technical Decision Summary on cryptoassets

A fairly regular topic in podcasts and public domain generally, has been the tax treatment of charities. When the Government announced its tax and social policy work programme last month it included a review of the tax treatment of charities.

Last Tuesday, the Finance Minister Nicola Willis revealed more details around what was happening, explaining that there would be announcements in next year’s budget, to be delivered in May 2025.

“What essentially we’re doing is looking to see if there are any loopholes that are being exploited that would allow entities that are structured as charities to avoid tax they should otherwise pay”

More tolls on the way

Ms Willis commented it would not be right to rule out any new tax revenue streams or levies in this current Parliamentary term, adding “The truth is, I will be looking at revenue from tolls, and there could be tweaks to the charity tax regime. You can expect me to make announcements at the Budget” On the theme of toll revenue on Friday, the Government announced three new highways being built in the North Island would all be tolled.

Sir Michael Cullen’s biggest surprise

I recall discussing the role of charities with the late Sir Michael Cullen, when he was Chair of the last Tax Working Group. When I asked him what the biggest surprise of his time on the TWG had been, he replied it was been the extent of the charitable sector and its relative importance. The Finance Minister picked up on this commenting “what we’re weighing up here is on the one hand, in reality, New Zealand Charities play a massive role in our communities and many of them fundraise, contribute significantly to their communities and they face a lower tax burden because we all appreciate that.” She then went on to add.

On the other hand, wherever you have omissions from the tax regime, there will be some who structure their affairs to limit their liability. Who might, for example, be building up funds that aren’t going to charitable purposes, that are building up their own coffers. That’s one of the issues we’re looking at. There are a number of details here. What I want to work through carefully is not punishing the good while going trying to go after the bad.

Apparently the Finance Minister specifically mentioned Best Start and Sanitarium as examples of trading entities that are structured as charities which could impacted by the changes.

What did the last Tax Working Group say?

It’s worth looking back at what the last Tax Working Group said in its section on charities. It recommended the Government periodically review the charitable sectors use of what would otherwise be tax revenue, and to verify that intended social outcomes are being achieved.

In relation to the likes of Best Start and Sanitarium, the TWG noted “the income tax exemption for charitable entities’ trading operations was perceived by some submitters to provide an unfair advantage over commercial entities trading operations”. That is a common analysis that I see.

But the Tax Working Group hit the nail on the head when it went on to say “the underlying issue is the extent to which charitable entities are accumulating surpluses rather than distributing or applying those surpluses for the benefit of their charitable activities.”

This has been a long-standing issue and a sore point for some commercial operators which has been on Inland Revenue’s radar for some time. It will be interesting to see what comes out of this review and whether in fact there are some very targeted measures restricting the ability to qualify for the charitable exemption. But I suspect what it will come down to is how exactly the funds are being applied.

How much is at stake?

Another news report estimated that perhaps up to $2 billion of profit in the charitable sector may not be subject to tax. This estimated was based on the Charity Services latest annual report which noted charities had for the year ended 30 June 2024 total income of $27.34 billion with expenditure of $25.28 billion, leaving a difference of approximately $2 billion unaccounted for. Theoretically that income could have been taxed at 28% or $560 million. Which is not to be sniffed at, given the Finance Mnister’s repeated concerns about the state of the books. What counter-action comes out of the Inland Revenue review will be revealed in next year’s Budget.

Inland Revenue’s proposed long-term insight briefing under fire

Moving on, last week I covered Inland Revenue’s feedback and summary of submissions it received on its proposed long-term insights briefing (LTIB). Inland Revenue was proposing to explore what the structure of the tax system would be suitable for the future, and it published the submissions that it had received on the matter. This included, as I said, a rather entertaining but bold (as you might expect) submission by Sir Roger Douglas,

Subsequently Business Desk published a story on Monday under the rather excitable headline “Corporate tax group tells Inland Revenue to stay in its lane over the long-term briefing” (paywalled) .The gist of the story was that Inland Revenue was under fire from the Corporate Taxpayers Group for having suggested that it should undertake such a review without a proper mandate. According to the CTG’s submission Inland Revenue “could be viewed as suggesting this next LTIB process would be a review of the “broad structure” of the New Zealand tax system and its future suitability. That seems to require a general review of all aspects of the tax system along the lines of the 2019 (Cullen) Tax Working Group Report.”

Such reviews are often undertaken specifically at the request of a government, often after a change of government such as the 2001 MacLeod tax review, the 2010 Victoria University Wellington review and in 2019, the last Tax Working Group.

Inland Revenue’s unique role

The truth is always a little bit more nuanced than what the CTG were apparently saying. A point that hasn’t been picked up is that this actually shows one of the problems around Inland Revenue not only being the Government’s main revenue gathering agency and responsible for the administration of the tax system, but it also is the lead policy advisor on tax. Treasury has a tax policy group, but it’s significantly smaller in scale. This is unusual by global standards because typically tax policy sits within the equivalent of treasury.

In my view it’s unfair to be singling out Inland Revenue for undertaking a periodic review. It’s been five years since the last Tax Working Group, and a lot has happened since then. Let’s remember we’ve had a pandemic, and we’ve also got a major war going on in Ukraine. The global environment has changed dramatically since 2019, and I would actually expect government agencies like Treasury to be looking periodically at the shape of the tax system. This is a key purpose of long term insights briefings.

Treasury has its own long-term insights briefing on the fiscal position, which I’ve referred to repeatedly, which has implications for tax policy. I think the criticisms are slightly unfair, and the headline probably a bit excitable, although the Business Desk notes that Deloitte were also slightly critical of the proposal.

Corporate Taxpayers Group’s suggestions

When you actually look at the CTG’s submission, it’s more nuanced. The CTG suggests

“a more focused approach than attempting another general tax review. The environmental scan seems to suggest that the officials’ concern with the existing tax system is its possible inflexibility.”

The CTG submissions makes the very worthwhile comment that an official exercise here should be taking a sort of lead role in educating the public, and to some extent politicians, about the issues that are ahead and the options available for change. The suggestion is the focus should be on future revenue flexibility and then a question as to how governments might wish to apply the tax system to meet redistribution objectives (distributional flexibility). Against this background:

“Officials have an important role to play in such political processes. They should provide the best possible advice and objective manner matters. What are the best economic estimated economic costs of different tax bases? How would any proposal to meet distribution objectives increase these costs? The political process can then trade off measures to meet distributional objectives with the economic costs this would incur.”

The CTG suggests Inland Revenue’s proposed long-term insight briefing should consider at what is known from New Zealand and overseas studies of the dead weight costs or tax revenue generally on a particular tax basis.

I think this is a perfectly reasonable response by the CTG. You might say well of course they would say that because they represent some of the largest taxpayers in the country. So perhaps they’ve got a bit of self-interest on the matter. But the point is there are economic costs of taxing or not taxing particular sources of income and those costs need to be considered in the scope of any stand-alone review.

An interesting tax issue involving crypto assets

Finally, this week, there was an interesting issue raised in one of Inland Revenue’s latest Technical Decision Summaries. These are anonymised issues that Inland Revenue’ Tax Counsel Office (TCO) has come across either as a result of a dispute that’s between the taxpayer and Inland Revenue, or as here involving a taxpayer who has made an application for a ruling as to the correct treatment of a transaction.

Technical Decision Summaries can provide useful guidance, but they are always highly fact specific. In this case the taxpayer was a natural person who qualified to be a transitional resident because he was looking to return to New Zealand after more than 10 years of non-residency.

The question he asked was would he be a transitional resident in relation to crypto assets held in overseas centralised exchanges as well as decentralised exchanges.

Would the sale of those crypto assets therefore be exempt under the transitional residence exempt?

As I said, these are very highly fact specific, and the ruling that came back was he would qualify as a transitional resident so long as he met various conditions and yes, the amounts derived from the sale of crypto assets during the transitional residence exemption, which typically lasts at least 48 months, would not be deemed to have a source in New Zealand.

As part of the analysis, the technical decision summary looked at what we call the source rules in section YD 4 of the Income Tax Act 2007. Would this be income from a business wholly or partly carried on in New Zealand? Are the contracts wholly or partly performed in New Zealand, or is this disposal of property situated in New Zealand?

The TCO concluded that none of those would apply and therefore because the crypto assets being traded or sold through the offshore centralised exchanges and decentralised exchanges, any gains would qualify for the transitional residence exemption. This is an issue I’ve seen discussed previously, although I’ve not directly advised on it, so it’s interesting to get some Inland Revenue commentary. But as I said, although Technical Decision Summaries are useful, bear in mind these are always highly fact specific, so be very careful in deciding if one might apply to your circumstances.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

One of the unseen revolutions in international tax over the last decade has been the adoption of the automatic exchange of financial account information. Also known as the Common Reporting Standards https://www.ird.govt.nz/crs this was developed by the Organisation of Economic Cooperation and Development, the OECD, in conjunction with G20 countries. It requires the automatic exchange of information on financial accounts – which is bank accounts, other investments held by taxpayers outside their jurisdiction. Financial institutions are required to provide information on such accounts to their respective tax authority which then sends that information to the jurisdiction in which that taxpayer is resident.

This project began in 2017. For the latest year, the tax authorities from 111 jurisdictions have automatically been exchanging information on financial accounts. And as I said, it’s a very broad range of investments, not just bank accounts. It’s all forms of investments. By and large, the public is pretty unaware of what’s happening here even though the numbers are significant.

€130 billion in tax interest and penalties so far

According to the latest peer reviewfrom the OECD, information from over 134 million financial accounts was exchanged automatically in 2023, and that covered total assets of almost €12 trillion. As a result, over €130 billion in tax interest and penalties have been raised by the jurisdictions through various voluntary disclosure programmes and other offshore compliance programmes.

Now the interesting thing here is that as a consequence of the introduction of the CRS, financial investments held in international finance centres or tax havens have decreased by 20% since the introduction of CRS in 2017. That’s a significant change. It means investments are moving into jurisdictions where they will be taxed. Over the long term that’s going to be quite significant for increased tax revenue around the world.

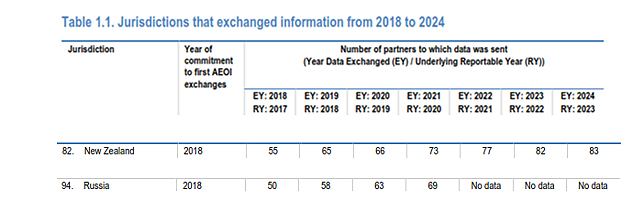

The full OECD report, which also discusses methodologies, runs to 248 pages, but the bulk of what people will be interested in is covered in the first chapter. Table 1.1. gives a summary of how many jurisdictions have been exchanging information, starting in 2018. According to the latest report the time of this report, 118 jurisdictions including New Zealand have started exchanging information.

Now the interesting thing to notice is the steady growth in the number of partners to which data has been sent. For example, the tax haven Anguilla in 2017 sent data to four countries but by 2023, it’s up to 67. The Cayman Islands, another key tax have sent data to 83 jurisdictions.

CRS and New Zealand

New Zealand began swapping data in 2018 when it sent information to 55 partners. For the latest year that’s grown to 83. Based on the early data exchanges Inland Revenue began a review programme in late 2019 which was then interrupted by COVID. However, it has now resumed its review programme, and I have one case at the moment which involves the taxpayer making the relevant disclosures after Inland Revenue enquiries based on data received through CRS. They won’t be the only one.

I was rather amused to see that Russia began exchanging data in 2018 when it sent data to 50 jurisdictions. But for the last three years no data is available. Wonder what’s happened there.

By the way the United States is not part of the CRS. That’s because it has something called the Foreign Account Tax Compliance Act, which basically was the model on which the current global CRS was built, and so it reports data separately.

How much data is Inland Revenue sharing?

I’ve tried unsuccessfully to obtain more detailed information on the data exchanges using the Official Information Act (the data exchanges are outside the OIA because of international treaty obligations which is fair enough). Notwithstanding this the impression I have is there are some huge numbers involved.

You have been warned…

What people should be aware of is that there’s a massive amount of data being circulated by tax authorities around the world right now. Many people may be oblivious to what’s going on. The likelihood is if you have an overseas financial account and you haven’t declared it for whatever reason, then it is quite likely that you will soon be asked a few questions about that by Inland Revenue.

Speaking about Inland Revenue, earlier this year they asked for consultation on their proposed long-term insight briefing (LITB). To quickly recap, LITBs are

“…future focused think pieces that government departments produce every three years. They provide information on long term trends, risks and opportunities that could affect New Zealand in the future, and policy options for responding to these matters. Their purpose is to help us collectively think about and plan for the future. They are developed independently of ministers and are not current policy.”

Back in August Inland Revenue proposed that its next long term insight briefing will explore what would be a suitable structure of the tax system for the future, and invited submissions by early October.

Inland Revenue has now published a summary of those submissions. In total, there were 35 submissions from 12 groups and 23 individuals. Most submissions were generally supportive of the topic. The rest, either suggested something completely different or were either ambivalent about it or did not actually specify whether they supported the project or not.

Seven themes in feedback

Inland Revenue’s picked out seven themes that came through from those submissions. Firstly, the fiscal pressures arising from superannuation and healthcare are a key trend and that’s one of the reasons behind Inland Revenue wanting to do a long term insight briefing on this topic. Most agreed with that, but several also added the question of increasing fiscal pressures arising from climate change.

My belief is its climate change that’s going to be the trigger point around changes to the tax system because that’s happening right now. And as damage from the floods grows and costs and insurers look increasingly wary about insurance, people will be looking to the Government for support.

The second theme was keeping flexibility in the tax system. In its submission EY commented

“We agree improvements to system flexibility should be the focus for this LTIB. In particular, working through options for system integrity in the context of tax rate increases is in our view, important.”

The devil is in the detail

A third theme was the analysis needs to consider policy design details and looking at first principles. Chartered Accountants of Australia and New Zealand made the comment that “Sometimes it is the detail that can make things unworkable. The framework should consider the merits of expanded tax bases with different design parameters”.

Another theme – and this is something I think I would endorse – the analysis needs to consider the tax and transfer system interaction. There were a few submissions pushing very strongly on that point.

A fifth theme proposed considering corrective taxes. The Young International Fiscal Association Network suggested that environmental taxes would fit well with Inland Revenue’s proposed topic because of the long term environmental trends.

The impact of technology

Another theme was the question of technological change and how that will affect the sustainability of tax bases. Earlier this year an IMF report on the impact of artificial intelligence suggested changes to tax systems could be needed.

Some submitters emphasised that it was important to consider how the tax system impacts a wider range of social outcomes. These included Doctor Andrew Coleman who was broadly in support of what was in the proposed LTIB. He suggested that they need to look at a wider range of retirement savings reforms, which would be no surprise to anyone who listened to the podcast with Gareth Vaughan and myself earlier this year. Several other submissions suggested how tax system could support productivity.

Finally, there were suggestions about considering progressive consumption taxes, which hasn’t really been looked at in any detail in New Zealand.

How Inland Revenue will proceed

Following this feedback Inland Revenue has said the LTIB will discuss the arguments for lower taxes on savings and the question of the tax treatment of retirement savings as part of a discussion about social security taxes. This is an interesting development because as the consultation noted generally, most jurisdictions have social security taxes which represent somewhere around 25% of total tax revenue. Whereas we don’t have them at all. This was a point Dr Coleman made in the podcast so it’s good to see Inland Revenue will be looking at that.

No to considering financial transaction taxes

As part of managing the whole scope of the LTIB Inland Revenue believes it “could reduce the discussion of some tax bases are less likely to be subject of significant public discussion such as financial transaction taxes.” This makes sense. Financial transaction taxes or Tobin Taxes are something that pop up in discussions about tax reform. I’m ambivalent about whether in fact they will achieve what people make out for them. I think they would add complexity and they would drive all sorts of different behaviour.

They’re not going to do a full review of the interaction of the tax and transfer system. And to be fair to Inland Revenue, I think that would be an entire long-term insight briefing of itself. But their chapter on consumption taxes discussed using transfers to offset GST rate increase somewhat similar to what Andrew Paynter proposed last week. (Just to repeat Andrew’s proposal is his alone and does not reflect any Inland Revenue policy). According to Inland Revenue the tax regimes chapters “will largely focus on how to make our main tax bases more flexible to rate changes, including considering options to support system coherence and integrity.”

Providing an analytical base

In summary Inland Revenue’s intention

“…is to provide an analytical base to provide further consideration of these issues in the future. For example, our focus on tax bases is on understanding the relative costs of taxing different underlying factors and what the overlaps and differences are in those tax bases. Our focus on tax regimes is on exploring how to make our tax based main tax bases more flexible to rate changes without undermining equity or efficiency goals.”

All of this seems perfectly reasonable to me.

From here there will be a future opportunity to provide feedback when Inland Revenue releases a draft of its briefing for public consultation in early 2025. It will then be finalised and given to Parliament in mid-to-late 2025.

Sir Roger Douglas’s radical proposals

Inland Revenue have also published all the submissions, from those who gave permission to do so, adding up to 175 pages of submissions, from individuals and organisations alike. It’s interesting to dip in and see what is being suggested on the topics. Sir Roger Douglas was one of the submitters and as you might expect, the old warrior is still looking for something radical.

Part of his proposal is a tax-free threshold of $62,000. But the trade-off is most of that gets put into retirement and health accounts. With the proposed retirement account, he’s probably reflecting the thinking of Andrew Coleman about the need for the current generation to start saving in earnest because of the various pressures coming towards us. Can’t say I agree fully with Sir Roger’s proposal but full marks for boldness.

Feedback on Andrew Paynter’s proposal

And finally, this week, to pick up a little bit from last week’s podcast with Andrew Paynter and his proposal to increase GST by 2.5% points to 17.5%, but then with a rebate for low- and middle-income earners. The transcript has been very well read and generated a phenomenal number of comments, over 150 at last count, and I thank all the readers and commenters for that.

What about the self-employed?

One commenter asked a question which we didn’t cover off during the podcast; how would Andrew’s proposal apply to the self-employed? The answer is it would use something similar to the provisional tax system. A person’s income would be uplifted from last year and if you’re in the range then you qualify for the proposed payments.

Last week Tax Management New Zealand and the Young International Fiscal Association network ran a joint presentation for the two winners, Andrew and Matthew to come and present their proposals. If you recall, Matthew proposed expanding the withholding tax regime to contractors. Andrew and Matthew both made excellent presentations to a very engaged crowd, and I can see why the judges had a difficult time splitting the pair. So well done again.

Left-to-right Matthew Seddon, Terry Baucher and Andrew Paynter

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

My guest this week is Andrew Paynter, a policy advisor at Inland Revenue and co-winner with Matthew Seddon of this year’s Tax Policy Charitable Trust Scholarship. The Tax Policy Charitable Trust was established by founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa.

Andrew Paynter’s proposal is to increase the rate of GST to 17.5% and introduce a GST refund tax credit for low-and middle-income individuals.

I should make it clear here that everything in Andrew Paynter’s proposal and what is in this podcast represents his views and not those of Inland Revenue. Kia ora Andrew Paynter, congratulations on your win and welcome to the podcast. Thank you for joining us.

Andrew Paynter Thank you. That’s very kind. And yes, it’s great to be here and I’m really excited to have a chat with you.

TB Me too, it is a very interesting proposal. And so how do you land on choosing this? There is a pretty free rein in choosing topics for the scholarship. But what drew you to this particular proposal? .

The background

Andrew Paynter Yes, sure. For me, something I’ve been interested in ever since I’ve worked in the tax space is the New Zealand Crown’s long term fiscal position. And we know from the New Zealand Treasury’s most recent long-term insights briefingHe Tirohanga Mokopuna 2021 that as we look into the future, the Crown is going to be spending at quite a higher rate than it is getting revenue.

And for me, I think that puts New Zealand in quite a weak position to manage its daily societal needs. But also to manage future disasters, pandemics and economic shocks. And we know that these things are going to happen more often and probably at a greater severity than they have in the past. So that was sort of my starting point. I guess that was the thing I was interested in, and I wanted to try and develop some form of solution to that.

TB Yes, I mean, this is something long-time listeners to the podcast keep hearing me banging on about Treasury’s statement on the long term fiscal position. I also note in its briefing to the new Finance Minister, Treasury says there is a structural deficit of 2.4% of GDP. So we have a fiscal gap already, according to Treasury. I mean people talk about reducing expenditure, but that will only take you so far, particularly when expenditure is going up faster than you can reduce it, to be blunt. So why did you land on GST?

Why increase GST?

Andrew Paynter I think there’s quite a few reasons that I landed on GST. I guess the two main points are about finding a revenue raiser that embodies good taxation principles.

And then the second part is trying to find a revenue raiser that I think has better impacts than other revenue raisers, particularly in relation to effectiveness and efficiency.

So, on that first point, embodying good taxation principles. It’s really important that any revenue raisers that we choose are aligned with broad-based low rate, and that’s ensuring that we maintain f broad-based low rate at an entire tax system level, and at a regime level.

Of course, when we look across the New Zealand tax system, I think we can all agree that one regime in particular stands out as being super broad-based and that’s GST. We know GST has few exemptions and exclusions, but it also has the highest value added tax revenue ratio score in the OECD by quite some margin.

TB Yes, that’s quite a stat. In fact I think only Chile raises a higher proportion of tax from GST than ourselves?

Andrew Paynter I’m not entirely sure if that’s correct, but I do know for the revenue ratio score, I think Luxembourg has the second highest score in the OECD. But we outscore Luxembourg by quite some mark. And I think we have double the OECD average in New Zealand. So, it’s quite a difference.

GST – the broad base, low rate exemplar

TB That’s taxing everything. It’s as you say, it’s the exemplar in the system of the broad-based low rate. Even if you’re you’re proposing to raise it to 17.5%, even then, that would still be below the OECD average, isn’t that right?

Andrew Paynter Yes. The OECD average rate is 19.2%, so 17.5% is still nearly 2% below the average.

TB How much would that raise? This is the thing the politicians say. OK, how much would we get if we increased it by 2.5 percentage points. What’s the potential take?

Andrew Paynter Yes, I think obviously it depends on a huge raft of dynamic factors like inflation and consumption patterns. If the rate was applied in the 2023 tax year it would have raised an additional $4 billion in revenue. So that gives like a proxy for what’s possible.

TB Wow. I mean, that’s one percentage point of GDP. So that is a significant amount. But the question is, as I said, why GST? There’s a lot of debate around capital taxation as well, wealth taxes, capital gains tax and occasionally, not so much though, estate duty/death duties/inheritance tax. In your paper, you talk about GST being a one-off taxation on the wealthy. Can you elaborate on this?

How GST represents a one-off tax on the wealthy

Andrew Paynter Two interesting parts to that really. I was again looking to this future fiscal deficit and trying to think of revenue raisers that suited that future context. And one thing that we know is underpinning part of the deficit (obviously it’s not the whole thing, but part of it) is having this ageing population. And so, is there a way to leverage revenue from an ageing population? Of course, as the population gets older, a higher percentage of the population is earning less taxable income, but they are consuming often more than the means of their income as they’re drawing down on savings. So, increasing the rate of GST becomes in a way an effective one-off taxation on all the current and future wealth that exists in New Zealand so long as that wealth is then consumed in New Zealand on taxable supplies.

TB So if the ageing population skips off to spend its money overseas that is outside the GST net. But the likelihood is, as you say, they’ll consume more and more of it in New Zealand effectively because their income has declined.

Andrew Paynter Yes.

TB This means the GST relative to what their income as a proportion of the total tax they might pay, will rise on under this measure. Yes, so interesting analysis there but we don’t have a lot of evidence.

Andrew Paynter That’s correct, yes.

TB Maybe we don’t have as much statistical evidence as we would like. The empirical evidence to talk about, the behavioural impacts of this. But GST’s not really subject to the same behavioural impacts as other taxes, because you can either spend it in New Zealand or spend it offshore. And as we said, your opportunity to do that has become limited because physically you may not be able to travel, or it becomes too expensive to travel.

Andrew Paynter Yes, that’s right. Some interesting analysis is that when you do increase GST or just a VAT or consumption tax in general you do get potential behavioural responses. You know, substitution effects, price elasticity responses, etc. But some of the academic analysis I found was that when you introduce a rate increase alongside a compensation measure, those behavioural responses are often quite muted. So you don’t actually get the same response that you would if you just did a GST rate increase by itself. And obviously, this proposal does have a compensation measure aspect to it.

What about inflation?

TB Yes, we’ll come to that in a minute. One of the other things that may come into play around a GST increase, is it’s potentially inflationary. How do you deal with that effect, how have you calculated that potential effect and how long would it last?

Andrew Paynter It’s quite interesting. I think we have some precedent in New Zealand that we can look to. For the 2010 GST rate increase, the government of the day had modelled that the inflationary response would be about 2% immediately after the introduction of the new rate. That was reflecting an immediate 2.5% price increase on all taxable suppliers, and then some form of future and lagged response on non-taxable supplies like rents, but those are a lot harder to quantify.

So, you certainly do get a significant inflationary impact, but I think that because the Reserve Bank has the discretion to look through temporary inflation shocks in the way that it sets its monetary policy, in theory it shouldn’t have very significant economic consequences. And again, I think, we can look back to 2010 and see that.

TB Yes, we want to avoid that horrible double whammy – prices have gone up and then interest rates go up, that is a real nasty spiral.

Andrew Paynter Yes, that’s right.

TB And as we mentioned before, GST is as incredibly efficient tax. Businesses were collecting it and everything fell into place very smoothly. I’ve been around long enough to remember that after the 2010 increase things fell into place pretty smoothly.

But the big downside though for GST, (and the last Tax Working Group touched on this) and the taking GST off food was a partial response, is that GST is actually a regressive tax. Particularly for the lower- and middle-income earners. And the second part of your proposal deals with that. What are you proposing there?

Ensuring equity through a targeted GST refund tax credit

Andrew Paynter As we noted before, the inflationary impacts of a GST rate increase means that businesses are passing on the full cost of the GST rate increase to final consumers.

And so that means prices are going to immediately increase relative to incomes. That’s obviously a problem. We have relatively high levels of inequality in New Zealand, so low to middle income New Zealanders don’t necessarily have the means needed to absorb that price impact.

Then on top of that, as you mentioned, GST is regressive. I know it’s argued that it’s not necessarily regressive over an entire lifetime, but I think the fact that it’s regressive, at least at a point in someone’s life, it can impact on their economic position, which can then have lifelong implications on them economically. To address that I’m proposing that a targeted GST refund tax credit should be introduced to offset that impact.

TB How would that work?

Andrew Paynter It’s a very good question. We were touching on it in a conversation we were having off-air earlier, with all social policy initiatives when you’re choosing a compensation measure or when you’re just designing that compensation measure, it’s all about trade-offs and deciding on what values and objectives you value more than others and what you’re trying to achieve.

We can discuss the design parameters for the credit in a second, and I’m sure we will. But I guess I just wanted to highlight that this is just one way to do it. It’s not necessarily the only way and it’s not necessarily the only “right” way to do it. It really depends on what you’re trying to achieve.

TB Because there’s quite a bit of interest around this sort of mechanism around the world, isn’t it? The IMF released a working paper in April just as you were writing your initial proposal. But that was completely different. And that was a refund that comes through as point-of-sale credit. You mentioned in your paper that Canada has been doing it.

Andrew Paynter Yes, that’s right.

TB So, similar to what you’re doing?

Andrew Paynter Yes. As you said, the IMF compensation measure is completely different to a tax credit like I’ve proposed. Whereas Canada’s example is a tax credit, as they call it, the GST/HST refund tax credit but the design parameters reflect the realities of the governmental and tax systems in Canada so it’s quite complicated.

Although we could look to these examples for some inspiration, I think that the parameters that we select for the New Zealand context should be rooted in the realities of our government structures, and also our transfer system and our tax system.

Resolving the problem with abatements and marginal tax rates

TB You note in the paper that transfer payments have been sliding lower relative to median incomes over time. Then what you’re driving at is that one alternative might be “let’s increase the alternative transfer payment”. But they all come with heaps of abatements as you point out.

I was reviewing Inland Revenue’s annual report before today’s podcast and a stat that jumped out at me on this point was that only 22% of people receiving Working For Families credits do not have an abatement. That threshold is $42,700, which means 78% are being abated, and that’s at 27.5%.

So, you want to avoid that because it just increases this whole problem of effective marginal rates. How do you intend to do that? You’re taking what they call a fiscal cliff approach. Is that right?

Andrew Paynter Yes. Part of the design of the credit that I’m proposing is to use a cliff face approach. As you touched on, abatement is where your entitlement, whatever that may be, is decreased by a specified percentage for each dollar you earn over whatever the threshold is.

So, when you compare that to a cliff-face approach (which is where your entitlement just ends once you hit the threshold) you don’t get the same impact on effective marginal tax rates.

You still get work incentive impacts, but those are a lot sharper and shorter. So given as you say, there’s lots of interacting abatement payments in the New Zealand context, for those reasons I’m proposing that the credit utilise the cliff face approach.

TB Yes, you’ve also said it’s to be individual, so it’s not calculated like Working for Families on a collective family unit. It’s on an individual basis because the evidence shows you wouldn’t be getting much potential abuse of the credit. Why an individual credit rather than a family credit?

Andrew Paynter It’s various factors. I think one point is again touching on that Canadian example. In Canada, I believe you can file as a family or as a couple. Whereas in New Zealand, all of our filing is individualised. The administrative realities are that unless you’re in a regime like Working for Families, you don’t necessarily have those connections within the tax system to your partner.

Individualising the credit therefore aligns with the individualised nature of New Zealand’s tax system. It means that you don’t need information from your partner in order to get the credit. Which means that you can automate it because you don’t have to have an application process that says, this person’s my partner and this is their income. On top of that I was looking at the Household Economic Survey and it really looks like consumption patterns don’t vary greatly between one person household consumption data versus two person households. Consumption is quite an individualised thing.

TB That’s encouraging, because the simpler this is, the better in my view.

Andrew Paynter 100% agree.

What’s the threshold?

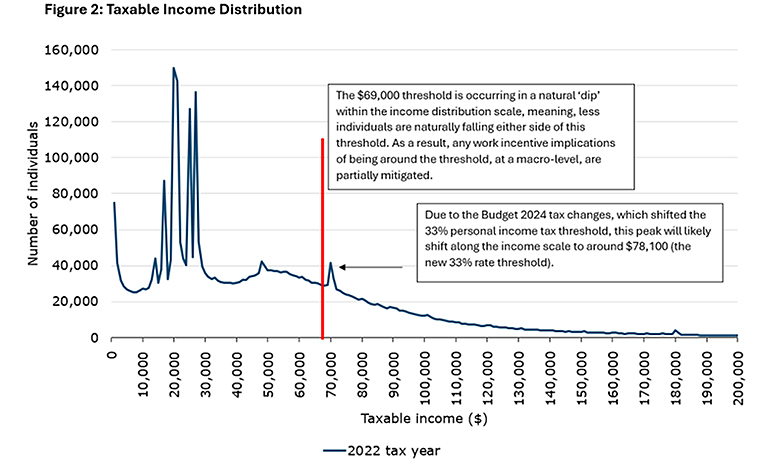

TB And so, the threshold you were talking about would be about $69,000.

Andrew Paynter Yes, I’m proposing that the threshold for the payment is $69,000, which is the median income from salary and wages. Obviously, it can be quite hard to define what we mean by low to middle income. But I think choosing this middle point makes sense for this notion of low to middle income.

You have less people naturally falling in that $69,000 space comparative to other parts of the income scale. And that means that those work incentive impacts that we talked about, are affecting less people, which I think is quite important from a macroeconomic perspective when compared to other parts of the income scale where you could put the threshold.

TB Yes, we see distortions around thresholds all the time. It’s quite blatant actually. You can see spikes in your graph at $70,000 and then $48,000. Don’t know what they have to do with it other than threshold increases.

Andrew Paynter Yes. That’s right.

How frequently?

TB This credit though, it would be payable quarterly. Is that correct?

Andrew Paynter Yes, I’ve chosen a quarterly model for paying and that quarterly model is full and final and that was to balance a few factors. It was to ensure that people are actually getting the credit close to the point in which they’re incurring the increase in GST, versus if you did a year, you might incur some form of increased cost towards the start of the year and you’re waiting quite a significant amount of time to get the payment. And again, given that this is targeted at low- or middle-income individuals, that sum of money is quite important.

Also, if you had a shorter time period, such as a week, it might be a bit more administratively difficult. For example, it’s hard to know how much people are actually getting paid as if a weekly model was chosen people’s pay periods might not align with that.

Having a quarterly full and final model also means that there’s a low demand for reassessments and that’s going to be important from an administrative perspective for Inland Revenue. Also, debt situations are avoided because you’re doing a lagged income model and that means people don’t have to guess what their income is going to be.

TB I think that’s incredibly important because when you see the stats, the debt’s building up. I mentioned earlier about the abatement issues for Working for Families and you say it’s full and final. So, in the quarter a person earns below the threshold, they get that payment and then for the next three quarters, they’re well above that.

But there’s no requirements to say, for example, they’re total income for the year was $80,000. But for the first quarter, they were within that $69,000, but that’s they received a final payment then and that’s it. No going back. No “backsies” from Inland Revenue to go back and re-assess.

Andrew Paynter Yes, that’s right.

TB And because as you say, the cliff face approach takes care of that because they get cut off, but hopefully their earnings have risen enough to mitigate the impact of the inflationary increase in GST.

Andrew Paynter Yes, that’s right.

TB I’m all for keeping it as simple as possible, otherwise the system gets bogged down with a lot of resources chasing relatively small sums of money. I think there are mechanisms to deal with that, and that’s the other part in here.

You’ve set out some different things you’re basically trying to automate as much as possible within Inland Revenue’s existing processes.

Definition of income?

Andrew Paynter Yes. Again, having the credit individualised as we touched on earlier, means you don’t need partner information. I also propose that the credit is based on a definition of taxable income, not something of a broader like economic income, which agencies like the Ministry for Social Development use for benefit payments. Inland Revenue already holds taxable income information in the course of its usual tax activities.

And then because it’s individualised and you don’t need partner information, it should in theory just be this really automated process where you know, me as an individual earns salary and wages and as long as I’m under the threshold for the quarter, as long as Inland Revenue has my bank account information, I will just get the payment.

TB I like that approach. Obviously you’ve got great feedback because you’ve won. But what feedback have you received from that? Is there a potential that your proposal might be taken further? Did Nicola Willis come up and say “ “Come and have a word with me I like this.”

Andrew Paynter Obviously everyone’s been very kind and very supportive, but whatever happens with my proposal, I’ve simply just come up with the idea. I’m obviously proud of my idea and all the work I put into it, and I have simply just put the idea out into the world.

TB That’s fantastic. Any final thoughts on what’s next?

Andrew Paynter What’s next? I’m not sure. A bit of relaxing I think. I guess one thing I would just say is if there’s any younger tax professionals listening to the podcasts or want to be tax professionals, it’s a really awesome competition and it’s a great opportunity to tackle some form of issue that you’re passionate about.

You’ve got the time and the space to develop a solution that you really care about and then you get to have it tested by leaders in the tax space. And I think that’s a really cool opportunity. So I heavily encourage anyone who meets the eligibility criteria to apply.

TB I thought the standard this year was extremely high and I’m very grateful to yourself, Matthew, Matthew and Claudia for all coming on and talking about your proposals

I think that seems to be a good point to leave it here. My guest this week has been Andrew Paynter, co-winner of this year’s Tax Policy Charitable Trust Scholarship, and we’ve been talking about his proposal to increase GST and have a refundable tax credit.

Andrew, it’s been a great privilege talking to you about that. Congratulations again. Have a well-deserved rest and onwards and upwards. I’ll watch with interest.

Andrew Paynter Thanks, TB. I really appreciate it. Thank you for having me on. It’s been great.

TB Not at all. Thank you. And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

more on Inland Revenue’s crackdown on student loan debt

and why we might need to pay more tax

At an event for the Young International Fiscal Association, the Revenue Minister, Simon Watts announced the Government’s Tax and Social Policy Work Programme. These work programmes are a working document updated frequently so that after a change of government they reflect the new government’s priorities in tax policy and social policy areas.

According to the speech made by the Revenue Minister, the work programme under the current government is designed to support rebuilding of the economy and improve fiscal sustainability by simplifying tax, reducing compliance costs and addressing integrity risks.

There are six areas of priorities going forward: economic growth and productivity, modernising the tax system, social policy, the integrity of the tax system, strengthening international connections and other agency work.

Out with the old, in with the new

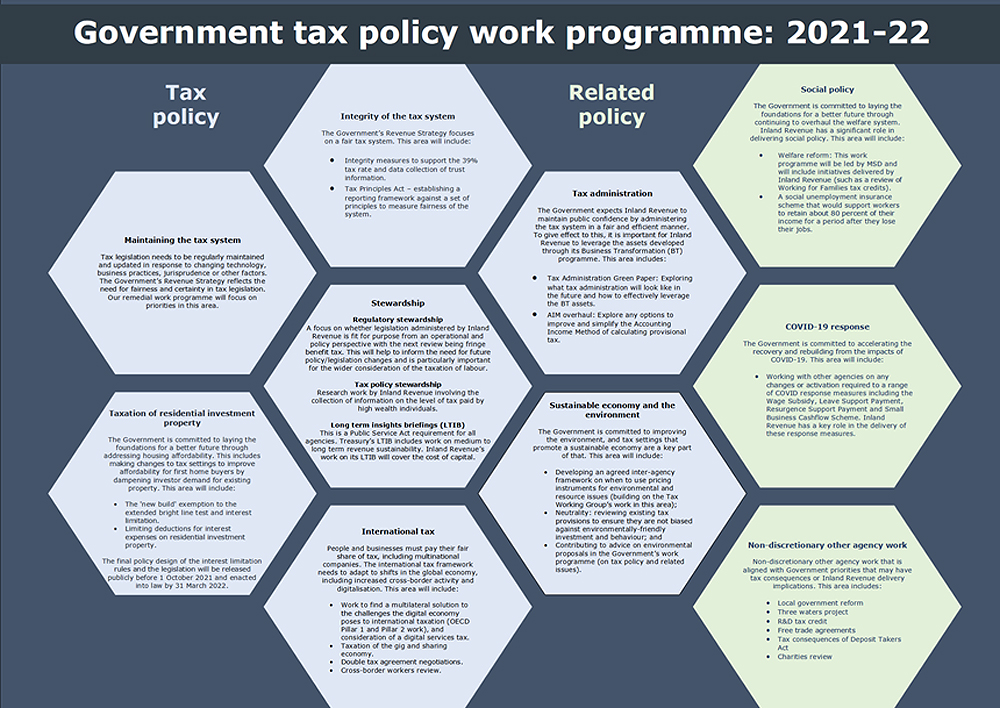

It’s interesting to have a look at what changes have been made since the programme was last officially updated back in 2021-22.

There under the Labour Government, there were 10 work streams of tax policy and related policy matters some of which overlap with the updated programme. Social policy integrity of the tax system, maintaining the tax system were all part of the 2021-2022 work programme and they’ll be part of every work programme going forward.

On the other hand, the COVID-19 response and the taxation of residential investment property were two major areas back in 2021-22 which are no longer there. As is well known the current government when it came in repealed all the work in relation to changes to the taxation of residential investment property.

Tax policy changes already happening

Drilling into the latest workstreams, some of them are already underway such as improvements to employee share schemes, implementation of the Crypto-asset Reporting Framework, simplification of the Approved Issuer Levy reporting including allowing retrospective registration and changes to inward pension transfers. All these are in the current tax bill before the House.

The other interesting things they’ve added in here, which we’ll watch with some interest, are exploring compliance cost reductions, including improving tax compliance with small businesses. Now you recall last week in my review of Inland Revenue’s annual report one of the areas Inland Revenue felt that business transformation hadn’t delivered as much as had been hoped for, was in reducing compliance costs for small businesses.

I totally support what Inland Revenue are doing, but the issue that they’ve run up against is that sometimes it has to accept the trade-off between good tax policy and the risk of tax seepage around the margins. If a policy allows a deduction or other benefit for taxpayers such as SMEs that meet certain criteria, you get certain deductions, Inland Revenue is always concerned about people exploiting that. The question that arises is does the wish to reduce compliance costs outweigh the risk that some of those measures might be abused?

A place where talent wants to live?

An interesting one that caught my eye was their plan to review the Foreign Investment Fund rules. This is something that was mentioned in passing by the Minister of Revenue at the recent New Zealand Law Society Tax Conference. This looks to address the issues raised by the report The place where talent does not want to live in relation to the problems the Foreign Investment Fund regime causes for investors migrating here.

Another interesting one is reviewing the thin capitalisation rules for infrastructure. That’s almost certainly tied up to the desire to have public/private partnerships help build infrastructure in the country. What it would almost certainly mean is that the current thin capitalisation rules (which basically limit interest deductions for international multi-nationals, which have more than 60% debt asset ratio) would almost certainly be relaxed.

In terms of other agency work Inland Revenue is considering, is an improved information sharing agreement with the Ministry of Business and Innovation and Employment, student loans, the question of final year fees free and overseas based borrower settings, the highly topical Treaty of Waitangi settlement, Local Water Done Well and supporting the all-of-Government response to organised crime. (Organised crime often represents tax evasion so it will always fall in the ambit of Inland Revenue).

Changes to the taxation of the Super Fund?

A big work programme, probably in terms of modernising the tax system, would be exempting the New Zealand Superannuation Fund from income tax. This would be quite significant as the New Zealand Superannuation Fund probably contributes $1 billion a year in company income tax. On the other hand, the Government will probably then be able to dial back completely its contributions to the scheme. In other words, the fund would now be expected to be self-funding going forward, which is quite possible now it’s reached a near critical mass of at least $70 billion in value.

The document’s fairly light on detail, just a one pager, but it gives you an insight as to where the priorities are right now. There are no real big surprises and we’ll watch and bring developments as these policies mature and are brought to fruition.

Student loan debt – Inland Revenue ups the ante

Moving on, last week I talked at some length about Inland Revenue’s actions around the collection of student loan debt and it so happened that yesterday Inland Revenue’s Marketing and Communications Group Manager Andrew Stott appeared on RNZ’s 9:00am to Noon with Catherine Ryan. They discussed what Inland Revenue is doing with its extra $116 million of funding over the next four years. This Includes an additional $4 million for recovering overdue student loan debt.

Quite a lot of interesting commentary came out of this interview. One of the first surprises was that many young people going overseas don’t know that their student loan debt, once they leave the country, starts to accrue interest. Therefore, they get behind surprisingly quickly. As is known, only 29% of overseas based borrowers are making repayments at the moment, and the student loan debt is now up to $2.37 billion, $2.2 billion of which is owed by overseas borrowers. A substantial number of whom are based in Australia.

So that’s now obviously a focus both operationally and in the latest work programme. I’m particularly interested to know more about what is planned in the overseas based borrower settings. What does Inland Revenue consider it needs to improve its ability to collect debt under the student loan scheme?

Inland Revenue has been allocated $4 million in funding to get cracking on recovering debt and it’s expected to produce a four to one return this year, which is expected to rise to eight to one next year. It will meet those targets pretty comfortably I’d say. Apparently in the first quarter of its new financial year – 1st July to 30th September this year it’s already collected $60 million in overdue debt up 50% from last year.

A surprising statistic

I guess the big surprise that came out of the interview was when Mr. Stott noticed that most of the debt is owed by people in their 40s or 50s who had never got round to repaying Inland Revenue. These people had been much younger when they went overseas with student loan debt which then accumulated as interest and penalties were added. This does beg the question that if people went overseas in their 20s and we’re now chasing them in their 40s and 50s, what was Inland Revenue doing in between?

As I said in last week’s podcast, relying on late payment and interest charges for enforcement just doesn’t work. We know from research in other areas when a person’s debt blows out (and probably the threshold is as low as $10,000), people will put their head in the sand and not take action because the matter feels too big to manage. Mr Stott mentioned that there’s several debts running into tens of thousands. I have seen one where it’s over $100,000. The average debt owed is about $17,000, but it’s the old overseas debtors, obviously larger debts, that Inland Revenue is going to be targeting.

As part of this it is talking to anyone who returns to New Zealand who has a debt of at least $1,000. They can now identify such persons thanks to the information sharing that goes on between New Zealand Customs and Inland Revenue.

Inland Revenue also have the ability to detain/prevent someone from leaving until they have a conversation about payment of debt. According to Mr Stott the group being targeted are those who have persistently not engaged with Inland Revenue. They have not responded to Inland Revenue at all. They’ve simply just said now go away, I’m not going to talk to you and ignored them. They will be fined and will find themselves having an extra stay at the airport just prior to departure.

Deducting debts from overseas salaries?

Inland Revenue has the ability to issue deduction notices requiring amounts to be withheld from payments to Inland Revenue debtors. (According to an Official Information Act response I got from Inland Revenue, it issued over 42,000 such notices in the year ended 30th June 2024).

Mr Stott was asked whether it could do the same in Australia? Can Inland Revenue ask the Australian Tax Office (ATO) to issue the equivalent to a deduction notice so that an employee working in Australia has part of their salary deducted to pay student loan debt. The answer is yes it can, but it’s not easily done. It’s termed a “garnishee order” in Australia and requires a court order. Consequently, Inland Revenue hasn’t really used such orders.

It seems to me that is something Inland Revenue really will need to look at closely, because if you’ve got 70% non-compliance and you’ve got an estimated 900,000 student loan debtors in Australia, it would be worthwhile establishing a process to enable garnishee orders to happen more frequently.

It may be that they have to ask the ATO to amend legislation, which would delay everything. But it would appear that they have the tools already, so it will be interesting to see if that’s employed more frequently.

Increased audit activity

The other thing Inland Revenue has ramped up is audit activities. It has apparently already launched 2,000 audits in the first quarter of its new financial year. This is up 50% on the previous year. Incidentally, 10% of those, are targeting the largest companies in the in the country.

As previously mentioned, Inland Revenue have recently targeted bottle stores and the construction industry. The next group of people that they’re going to be talking to now are vape stores, nail salons and hairdressers. Because in all cases they suspect cash income is not being declared, so these businesses will be the subject of unannounced visits.

The focus in Inland Revenue now is on enforcement and debt collection and there are more signs of it. So, I’ll repeat what I’ve said previously. If you have debt with Inland Revenue approach them to discuss it. You will find that if you take proactive action, it will be reasonable in most cases, unless you have a history of non-payment In which case good luck. Taking proactive action is the best approach, because tax debt is something you simply can’t put your head in the sand and hope it goes away. It won’t. Inland Revenue has got many more resources now, and the net is closing.

Why we might need to pay more tax

Finally, earlier in the week, I was one of several commentators Susan Edmunds of RNZ spoke to for a story on why we might need to pay more tax. Her story picked up the recent speech by the Treasury’s chief economic adviser Dominick Stephens which noted that the country appears to be running a fiscal deficit of 2.4% of GDP – that’s about $10 billion – and the pressure that’s building on demographic change, the ageing population, and rising healthcare costs. The article also referenced, Treasury’s 2021 Statement on the long term fiscal position He Tirohanga Mokopuna. I repeated that I think it is a matter of when, not if, the tax take has to rise when you put all these factors together.

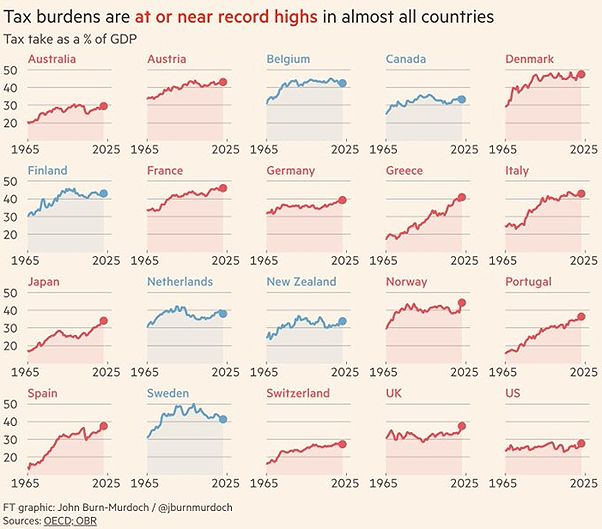

It’s also worth noting that the recent UK budget I covered a couple of weeks back increased taxes. Subsequently, the Financial Times had a very interesting graphic noting that tax burdens as a percentage of GDP for the last 50 years are at all-time highs in 14 of the 20 countries highlighted.

The pressure on tax revenues is a global problem, so we are not alone in trying to deal with these issues.

I think the break point, so to speak, will be the increasing cost of dealing with the damage as a result of extreme weather events. And I note that last week the Helen Clark Foundation released a report on the question of climate change and insurance premiums. My personal view is we need to get moving on this sooner rather than later, because that will help ease the transition.

Other jurisdictions we compare ourselves with, such as Australia and the UK, have a 45% top rate. And of course, in Europe the rates are much higher, still around 50% or so. I remain firmly committed to the broad-based low-rate approach, which means if we do broaden the base, we can hold tax rates down below these levels.

More tax, or less costs?

There was a nice to and fro in the comments on the LinkedIn post I put up with one commenter noting that we also need to reduce costs. Managing our expenses is part of what we have to do here, but if we’re talking about 2.4% of GDP, I think the pressures are too great for such a big gap to be easily closed just by better enforcement and cost management.

University of Auckland Professor in Economics Robert McCullough, thinks that this tax debate will define the next election in terms of “if we’ve got these expectations, how are we going to pay for everything?”

We shall see. And as always, we will bring you developments as they happen.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Rachel Reeves, the first ever female Chancellor of the Exchequer delivers a UK Autumn Budget with potentially significant implications for many Kiwis and Britons who have migrated to New Zealand.

Meanwhile Inland Revenue’s crackdown on tax evasion continues.

The UK finance minister is officially called the Chancellor of the Exchequer, a post which is more than 800 years old, and until this year it had never been held by a woman. So, when Rachel Reeves, the Labour Chancellor of the Exchequer delivered her maiden budget speech last Wednesday night, she made history as the first woman Chancellor in British history.

There was quite a lot to consider in this UK Budget, as people were watching to see how the new government would respond to the challenges it inherited. British budgets, unlike ours, coincide with the release of a Finance Bill and tax measures there’s always a lot of tax matters to consider beyond the headline measures.

The headline measures

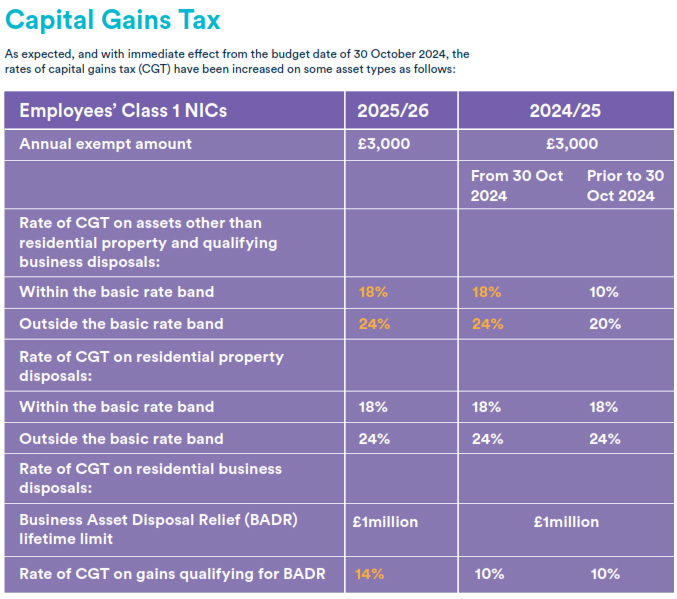

Most notably, there was an increase in Employer National Insurance Contributions (a Social Security tax) by 1.2 percentage points to 15% with immediate effect. There are also immediate tax rises for capital gains tax, but the top rate for capital gains tax still was capped at 24% for both property and non-property assets. Which as some commentators said is still lower than countries with which the UK compares itself. It’s quite interesting to see that comment about 24%, because one of the key points of our discussion around capital gains taxes here is what rate would apply? It’s therefore interesting to have an international comparison.

Beyond the headlines

It’s always interesting to dig around in other countries’ budgets and see what they do in certain areas. For example, the UK doesn’t have an imputation credit system, but there are lower rates of tax applied to dividends, even for those on the highest income. There’s also a savings allowance, which exempts certain amounts of investment income. It’s currently £1,000 for basic rate taxpayers (taxable income up to £37,700) and £500 for the higher rate taxpayers. The UK basic rate of tax is 20% and we have two rates lower than that so this savings allowance is not necessarily a measure we might want to copy here.

Twin cab utes and fringe benefits – an example to follow?

There’s apparently some uncertainty around the fringe benefit taxation treatment of twin cab utes which the Budget clarified. Where they have a payload of one tonne or more such vehicles are not there to be treated as cars for benefit in kind purposes unless they were acquired prior to 6th April 2025.

On Fringe Benefit Tax, the benefit value is calculated as a percentage of the vehicle’s list price when the car was first registered which is similar to our treatment. However, the percentage used is determined by the vehicle’s carbon dioxide emissions, or its range if it’s an electric vehicle. These percentages are set to increase steadily over the next three years as part of the range of tax increases announced. Inland Revenue is presently reviewing FBT and as is well known tax can act as a disincentive. If we want to incentivise a transition to a lower emissions economy, maybe we should be looking at how the UK applies FBT to vehicles.

UK pension tax free lump sum unchanged

There’s always lots of rumours before a Budget which I’ve seen sometimes used as a means to get people to buy new products or make tax driven decisions in fear of change. One of the rumours before this budget was that there were going to be changes to the taxation of pensions and in particular to the 25% tax free lump sum. That hasn’t happened, but remember, our rules are completely different. Just because 25% of the pension can be withdrawn tax free in the UK, that doesn’t mean the same rules apply here.

The big changes

But the main reason I was paying particular attention to this UK budget was because we finally got more detail around the two announcements made in the March Budget – the new foreign and income gains regime and the end of the non-domicile regime and the changes to inheritance tax. These are both measures which have significant impact for New Zealanders, who are either going to the UK or have returned to the UK, but also for UK expats who have migrated here.

New foreign income and gains regime

The foreign income gains (FIGS) regime is very similar to our transitional resident’s exemption in that a new tax resident’s foreign income and capital gains will be tax exempt for the first four UK tax years that they are resident in the UK. It’s not like our 48-month exemption period, it is tied to the UK tax year, which remember runs from 6th April to 5th April. (Perhaps reflecting that some of this stuff does date back 800 years or more, there’s no intention to change that tax year end).

What has also been clarified is that individuals who have previously elected to be taxed on the remittance basis, which meant their non-UK sourced income investment income was not taxable, can now be allowed to take advantage of a so-called temporary repatriation facility. This will last for three years, and they will be able to nominate and remit their non-UK income and gains from years when they were within the remittance basis and take advantage of lower tax rates. Initially 12% for the first two years ending 5th April 2026 and 2027, and then 15% for the year ended 5th April 2028.

As part of the FIGS regime there are also changes to what’s called the Overseas Workday Relief. This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties determined on “a just and reasonable basis”. This is quite a significant one for expats and for companies that have very highly paid and skilled employees and has been greeted with general enthusiasm by by those impacted.

Inheritance Tax

Potentially the biggest change though, is in relation to inheritance tax (IHT). This applies to all assets situated in the UK or all assets situated anywhere, if the person is domiciled within the UK. There’s a nil rate band of £325,000, above which 40% will apply (these rates and thresholds have been frozen until 2030). IHT has a potentially significant impact because under the present rules, someone tax resident outside the UK could still be within the IHT net because they are still deemed to be domiciled in the UK. I’ve had to deal with one or two of these instances.

There’s also a pretty nasty trap for someone like me who might have left the UK a long time ago and adopted a new domicile of choice outside the UK. At present if I ever became tax resident again in the UK, our domicile would immediately revert to the UK. Therefore, working or living for prolonged periods of time in the UK was actually potentially highly tax disadvantageous from an IHT perspective.

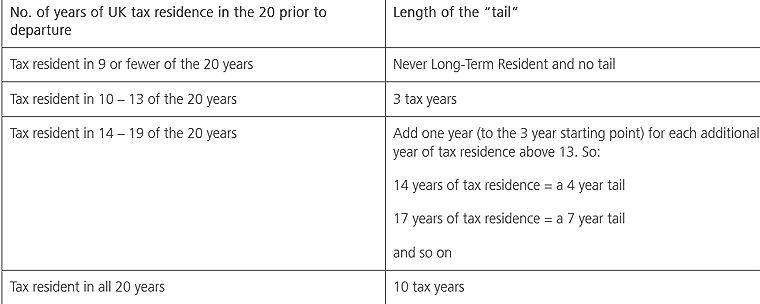

All this will be replaced now by a residence-based regime. The tests for whether non-UK assets are subject to IHT will now be whether the individual has been tax resident in the UK for at least 10 out of the last 20 tax years immediately preceding the tax year in which the chargeable event, most typically death, but can also be a lifetime transfer into a trust, happens.

There’s also a tail on how long a person is in scope if they’ve been non-resident during a period. For example, if someone had been UK tax resident for between 10 and 13 years, they remain in scope for IHT for three years post departure.

(Courtesy Burges Salmon)

Implications for New Zealand residents

What this change means for a lot of British expats resident here is they’ve got to think again about what their IHT obligations could be. By the way, our double tax agreement with the UK does not cover IHT. The UK has the right to charge IHT on assets situated in the UK, that’s not surprising. However, it potentially also has got a long reach if HM Revenue & Customs determine someone resident here is subject to IHT.

IHT and trusts

One of the other IHT changes is to the taxation of trusts used to hold assets outside the scope of IHT, so-called excluded property trusts. If I understand it right, starting from 6th April 2025, if a settlor dies and they’re within the scope of IHT, assets settled by them into what was previously an excluded property trust are now within IHT. This is a major change and I’m investigating it further given we make very extensive use of trusts. I’ve been dealing with quite a few clients who have UK connections year and it’s been really revealing to see how complex the taxation of trusts is from the UK perspective. It’s good to see some clarity around the new rules, but as I say, it’s a significant budget in many ways, and there could be quite major consequences for more people based here than they might anticipate.

Meanwhile, Inland Revenue’s crackdown continues

Moving on, Inland Revenue continues its crackdown when it announced on Thursday that it’s making unannounced visits to hundreds of businesses who it believes are not meeting all their tax obligations as employers.

According to Inland Revenue, they receive about 7000 anonymous tip offs each year. It has said “the volume of tip offs has grown over previous years indicating an increased sense of frustration by the community in general, businesses who are not doing the right thing.”

Inland Revenue’s analysis shows that the tax risks overwhelmingly relate to taking cash for personal use without reporting sales and or paying employees in cash.

Based on this Inland Revenue is making unannounced visits to over 300 employers whose practices it will closely examine. I’ve seen this happen with a few clients under investigation. Inland Revenue staff will go to a café or business and just watch to see what’s happening. They may buy something, but they will certainly sit and observe and see who uses the till, how everything is recorded and from there they will draw the relevant conclusions.

The consequences of being investigated

As an example of what happens to taxpayers who have not been compliant, the director of an asbestos removal and labour hire company has been jailed for three years in what the judge called serious offending and the worst of its kind to come before the Christchurch District Court in the last 20 years. The director, Melanie Jill Tatana, also known as Melanie Jill Smith, was jailed for three years for what was described as wilful diversion of funds.

Her company employed around 60 people, and between April 2019 and September 2022 had been required to deduct PAYE on 63 occasions but failed to pay the full amounts totalling $1.6 million. Tatana was therefore charged with 63 counts of aiding and abetting to knowingly take PAYE from workers’ wages and not pay it on to Inland Revenue. Instead, more than $800,000 had been diverted for her personal use.

One of the more encouraging things from my perspective about this case is that this offending has all been pretty recent and Inland Revenue tracked it down within a couple of years. I’ve seen cases where the offending has been four or five years.

I still think 63 occasions of nonpayment is a little generous, but bear in mind that Inland Revenue did take the the foot off the throttle around pushing hard on on companies and businesses because of COVID. That amnesty or less stringent approach is now over and it’s back to business. And Tatana won’t be the first to find out about Inland Revenue’s hardline approach.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.