After all, taxes are what we pay to get, maintain and keep a civilised society

A war, inflation, a proposed Tax Principles Act, dramatic U-turns and the Trusstastrophe. 2022 has been quite the year and I’m certain I’m not the only one whose predictions finished up wide of the mark.

Back in January, I saw three main themes for the year. Firstly, the ongoing response to COVID 19 and what new fiscal support will be offered. As part of this, the question of inequality and the taxation of capital would be on the agenda. Secondly, international tax reform and progress in the deal announced in October 2021. And finally, with Inland Revenue, how it was going to administer the tax system in the future.

Well, on the first there was a new COVID support package announced shortly afterwards in February, which ran through until May. However, although COVID is still very much around, the Government’s focus has rapidly shifted to dealing with a cost-of-living crisis in part, the result of COVID 19 and supply chain issues and the spike in oil prices after Russia invaded Ukraine.

By the way, as for financial support for COVID, only the Leave Support Payment Scheme, which pays $600 per week, remains available

Now, this is the year the details of the international tax deal announced in October 2021 were meant to be worked out, so everything would then be ready for implementation next year. Instead, it ran into a series of obstacles which has delayed this implementation until 2024 at least. Fortunately, however, this week a key obstacle has been removed, after first Hungary and then, following some last-minute shenanigans, Poland, dropped their objections to the deal. This enabled the EU to unanimously agree to implement Pillar two of the OECD proposals. This will impose the minimum corporate tax rate of 15%, which will apply to all national and domestic groups with combined annual turnover at least €750 million.

Overall, although progress is being made, it is at a slower pace than was expected back in 2021, and I would expect that will still continue to be the case next year. In fact reading the tax press, some are beginning to wonder if it will ever happen. But we will see.

Inland Revenue and the Cost of Living payments

After completing its Business Transformation programme, I expected Inland Revenue to turn its attention back to how the tax system is run. And certainly, at the start of the year there was a quite a bit of activity in this area with a particularly useful paper prepared by business New Zealand on the matter. However, the topic dropped off the radar in the wake of the cost-of-living crisis, which somewhat ironically then put the spotlight on how Inland Revenue operates.

In May’s Budget the Government announced a Cost of Living payment of $350 to be paid in three monthly instalments starting on 1st of August. To say there were a few teething issues would be one of the understatements of the year. Although mistakes were inevitable, given that were potentially over 2.1 million recipients, right from the outset, Inland Revenue seemed to be struggling to manage the delivery of the payments.

As has been reported, quite significant numbers of ineligible recipients and a large number of whom were outside New Zealand, had received payments incorrectly. And Inland Revenue also acknowledged there had been a systemic problem in respect of one group of 12,000 recipients.

Inland Revenue does now appear to have got on top of the issue of identifying the correct recipients of the payments. By the time the third payment was made on 1st October, the number of payments, compared with the first instalment in August had reduced by 96,000.

Inland Revenue now calculates that between 70 and 80,000 people may have incorrectly received a cost of payment and has now begun contacting this group about those payments.

Given payments were expected be made to 2.1 million people, some mistakes were inevitable. It is however, of concern that there were systemic issues identified. It’s arguably more problematic that Inland Revenue required by its own estimate, 750 staff, almost 20% of its current staff, to process those payments. This, combined with persistent rumours about now frequent overtime indicates potentially serious under-resourcing issues at Inland Revenue and that is something we will be keeping an eye on going forward.

The Cost of Living payment was one of the few surprises in May’s Budget. Grant Robertson chose again to do nothing about increasing thresholds, which, although tax rates were changed on 1st October 2010, the actual thresholds at which those tax rates apply, haven’t actually been adjusted since 1st October 2008. The theory behind the Cost of Living payments were that they were more targeted than raising the thresholds. But as we’ve just discussed, administrative errors by Inland Revenue meant that the payments attracted more controversy than anticipated.

Politics trumps tax policy, again

That said, the controversy around the Cost of Living payments paled beside the reaction to a proposal in the August tax bill to raise GST on management fees paid by KiwiSaver funds. On the face of it this was a routine tax measure designed to tidy up what was an unclear tax treatment and would not have taken effect until 1st April 2026. But it was expected to realise an estimated $225 million a year and then a political storm erupted once the accompanying Regulatory Impact Statement revealed that on the assumption the increase in GST would be fully passed on to KiwiSaver fund members, KiwiSaver balances would be reduced by an estimated $103 billion by 2070.

The Government rapidly decided to retreat, and the offending proposals were withdrawn inside 24 hours, which is a quite unprecedented move. It is one of the clear cases of politics trumping tax policy because once the dust has settled, the issue the matter was trying to resolve is still to be addressed. I suspect that whoever tries again might think about addressing criticism by using the funds raised to either restore the fee subsidy of $40, which was withdrawn in 2009, or adopting one of the Tax Working Group’s proposals for minimising the effect of tax on KiwiSaver funds of low-income earners.

The Trusstastrophe

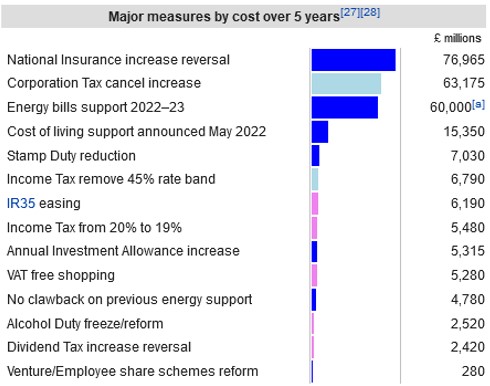

That controversy and U-turn was, quite frankly, nothing compared with what might politely be described as the Trusstastrophe (I’ve seen ruder descriptions) which happened barely a month later in the UK. To recap new Prime Minister Liz Truss and her Chancellor of the Exchequer, (finance minister) Kwasi Kwarteng decided to go for broke with a bold tax cutting mini-Budget in September. This proposed significant tax cuts, primarily the reversal of a proposed corporation tax increase and the removal of the 45% tax rate on the income tax rate. This provoked a massive run on the Pound and more worryingly in the gilt markets, the UK Government’s bond market.

Within four weeks, no fewer than seven of the tax cutting proposals were gone and shortly afterwards so too were Kwarteng and Truss to become footnotes in history. Truss becoming the shortest serving prime minister in British history. (Remarkably, Kwarteng is only the second shortest Chancellorship in history, after Iain Macleod who died in office after just 30 days).

What Kwarteng proposed

What eventually transpired

But if that was all great fun to watch from this side of the world, Truss and Kwarteng’s dramatic fall actually had a knock-on effect here. Arguably the most controversial proposal was the withdrawal of the highest 45% income tax rate band, it highlighted how a disproportionate amount of the proposed tax cuts would have gone to relatively few people. In the wake of the fallout, National here felt compelled to announce it wouldn’t go ahead with its proposed abolition of the 39% tax rate in its first term if it forms the Government after next year’s election.

There was also something else amidst the mayhem which didn’t attract a lot of attention. There were no attempts at all by Truss and Kwarteng to reduce capital gains tax or inheritance tax. In fact, Kwarteng’s successor as Chancellor Jeremy Hunt, has actually increased the tax on capital gains by reducing the annual tax-free allowance from its current £12,300 steadily to £3,000. This is an interesting insight into the relative states of the tax systems in the UK and here. The UK system even when being managed by bold tax cutters left alone the taxation of capital. Whereas as we know here, the taxation of capital is a perennial problem.

A Tax Principles Act?

It was in part to this issue that David Parker, the Minister of Revenue made a very interesting speech in April in which he proposed a Tax Principles Act across by which the system could be judged, regardless of the Government in charge. It’s well worth reading again the proposals, but we have not seen anything regarding the proposed bill which at the time he suggested would be coming out this year. Given how the Government reacted to the GST on management fees issue, I think it’s probably likely we won’t see this at all until next year, if Labour is re-elected and forms the next Government.

A constant theme of this podcast is around taxation of capital, because there’s a lot going on in the world in this space. As we just mentioned, the UK despite bold tax cuts, wasn’t prepared to make changes to the taxation of capital. Over in Ireland, the Irish Government asked a Commission on Taxation and Welfare to report on the Irish tax and welfare systems. Its final report published in September, made 116 recommendations, one of which was that the overall yield from wealth and capital taxes, including property, land, capital acquisitions and capital gains taxes should increase materially as a proportion of overall tax revenues.

And this is one of the areas we think New Zealand is out of sync with global trends. But the politics are very difficult. It’s easy to say what’s needed as a tax consultant, but politicians want to be re-elected and they have to deal with the political fallout. But whenever I do address this topic, it always provokes a lively discussion.

Top Five most read transcripts

It’s interesting to look at what are the most read transcripts and most listened posts and try and pick a common theme. They’re actually surprisingly different. By far the most read transcript for the year was when I discussed an interpretation statement on the application of land sale rules to co-ownership changes and changes of trustees. Interestingly, this was one of the top five most listened podcasts.

The Budget special was the second most read transcript for the year. At number three was when I discussed extended reporting requirements for trusts. (In that episode I also warned about the risks of mis-understanding the UK’s remittance basis rules after then Chancellor, and now Prime Minister Rishi Sunak became embroiled in a scandal).

The consistent theme emerging is about the taxation of property/wealth and that’s the case for the fourth and fifth most read transcripts. The fourth-place transcript covered a Reserve Bank of New Zealand’s Analytical Note on the housing market in an international context. The RBNZ note compared our housing market with several other developed markets and suggested that favourable tax settings have not helped the housing crisis.

In the fifth-place transcript I looked at the question of wealth and windfall taxes. Certainly, the comment section gets pretty lively whenever I make a suggestion that maybe we do need to change tax settings around the taxation of capital, such as introducing the fair economic return that Associate Professor Susan St John and I have been talking about for some time.

Top podcast tracks

With podcast listeners the top five is slightly different. The most listened to podcast for the year involved the proposed income insurance scheme, which has slipped under the radar although it’s still progressing in the background. Housing and countering tax avoidance was also in the top five podcast tracks for the year but only the episode covering the changes in ownership appeared in both top five lists.

Time for a more open discussion on tax?

As I said, whenever we deal with the taxation of housing, that pushes a few buttons which is sometimes amusing to see, but inevitable. But debates about what we tax aren’t going to go away. We’re going to see them more so next year being an election year. I do think we need to be asking a lot more about why we’re raising the tax – this point frequently comes up in the comments to a transcript.

This is important because one of the things that is emerging is the longer-term trends for the tax-take relative to the demands and pressures on it, such as rising superannuation costs. Those aren’t being very publicly discussed, but they’re very clearly being pointed out in Treasury’s report on Wellbeing and particularly in He Tirohanga Mokopuna 2021, its combined Statement on the Long-Term Fiscal Position and Long-Term Insights Briefing. But the Government doesn’t really want to talk about capital gains taxes at all. When Inland Revenue was preparing its Long-Term Insights Briefing it was specifically told not to consider the impact of capital gains tax.

I think politicians have deliberately, if understandably proscribed debate on the matter. But the fact is those debates aren’t going to go away. Tax systems evolve over time and these issues are going to need to be discussed because ultimately if “taxes are what we pay for a civilised society”[1], they also meet the demands of the economy and society at that time. If tax doesn’t change or adapt to meet those needs we have future problems brewing.

And on that note, that’s all for this week and for 2022. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you to all my listeners and readers and for all the feedback I greatly appreciate it even if we don’t always agree.

Until next year kia pai te Kirihimete, have a great Christmas!

Vivien Lei introduces her award winning tax reform idea to introduce weighting factors into environmental tax loads, ensuring the full costs are brought into business decisions and nudging behaviour away from polluting outcomes

This week, I’m joined by Vivien Lei, this year’s winner of the Tax Policy Charity Scholarship. Vivien, and other entrants were invited to propose significant reforms to our current tax system or analyse potential weaknesses and unintended consequences from existing laws and propose changes to address them.

Topics for consideration were environmental taxation, tax administration or the powers granted to the Commissioner of Inland Revenue to collect information for tax policy purposes. Vivien won with her proposal to change Aotearoa-New Zealand’s environmental practises with impacts weighted taxation.

Kia ora Vivien, congratulations and welcome to the podcast. How do you feel after all that?

Vivien Lei Kia ora and thank you for inviting me, Terry. It’s great to be here.

Yes, the competition was an amazing experience. You know, we don’t normally have many opportunities to really think about kinds of policy and different things that we could achieve in the future. So, this was a great opportunity for someone young to kind of test the waters, think creatively. And yes, it’s been great to have the support of everyone so far.

Vivien (centre) with the other finalists and members of the Tax Policy Charity judging panel and Deborah Russell MP Parliamentary Under-Secretary for Revenue

Terry Baucher How did you land on this idea of weighted impact? What was the genesis of the idea behind that?

VL The competition had three themes and I was immediately drawn to the environment one. I think a lot about the world that we will be leaving for our future generations, because realistically our current trajectory is not sustainable.

I think my non-tax experience has been a key inspiration. Before I started in tax, I was an entrepreneur. I spent six years building and growing early-stage start-ups and social enterprises from scratch, and I assisted with some researchers at the University of Auckland as well, looking at social enterprise ecosystems and impact measurement.

And the other part of my background is I’m also currently Finance Leader of the charitable Fisher Paykel Healthcare Foundation. So, I’m really privileged to have insight into the impact that the board and my foundation lead, interact with, and fund.

Through all of this, I’ve learnt so much from people and the social impact and not for profit sectors, and this experience really underscored for me how important it is to measure impact. So, you can check that you’re having the intended effects and articulate how what you’re doing links to the outcomes you’re aiming to achieve.

And I think others are realising this too. That’s why we’re seeing all these environmental reporting and evolving accounting standards. And I had in my mind that there’s an opportunity here for tax to proactively adapt alongside them and not fall behind.

But if we want to do something about our environment, you really need bold actions and innovation. And I think New Zealand prides itself on innovation and there are some amazing minds out there who could help us tackle this massive issue. My thinking has never been about a sin tax. It’s all about how we can make sure the full costs of people’s activities are clear and then incentivise a significant change in behaviours and norms towards positive environmental outcomes. So that’s kind of how my thinking landed on the impact weighting.

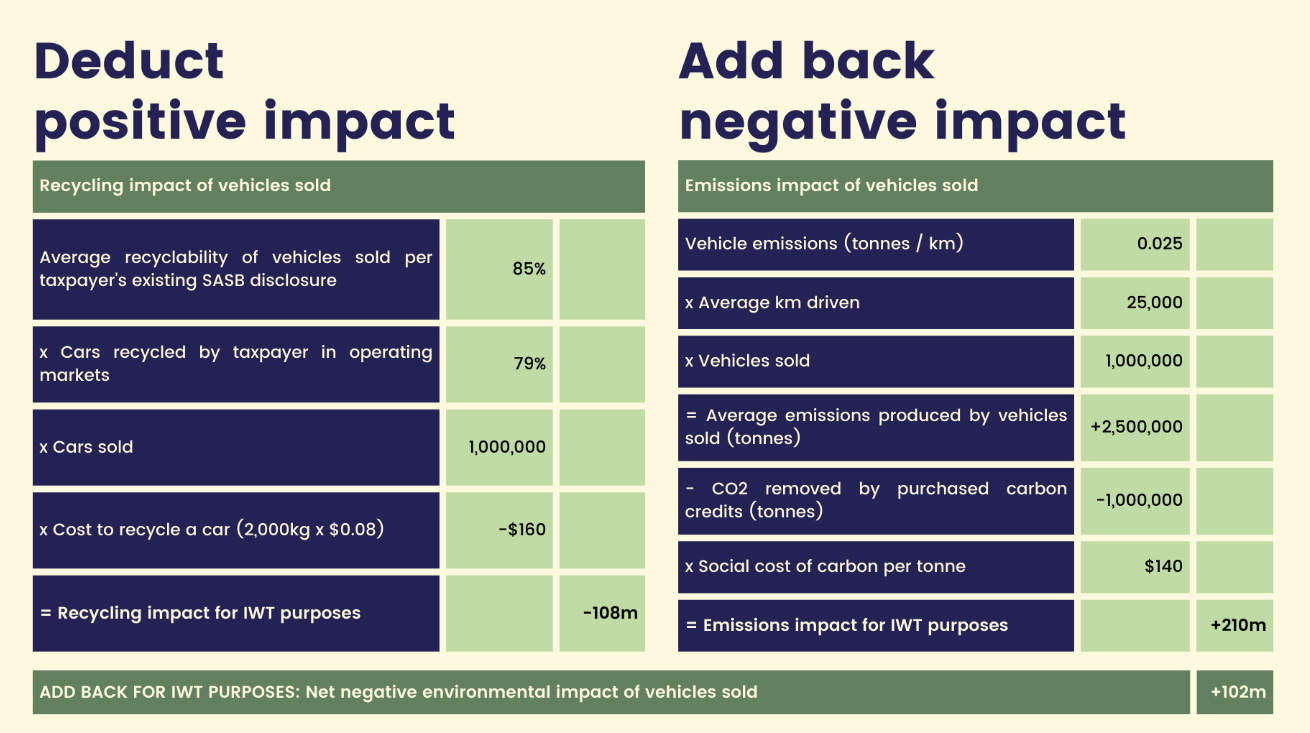

TB It’s fantastic and fascinating to hear about your background before you got into tax, unlike some poor sad nerd like me who went from university into a tax career. But to me, as we both know, tax has an interesting behavioural impact on that. Your paper points out we have the sixth highest emissions per person in the world and there’s just a little detail about negative environmental impacts like the Rena grounding. It cost the government $46 million, but we only ever got $27 million back from the ship owners and insurers.

So looking at it with an impact approach is a very neat way of doing so. I particularly like the point you picked up that if we can’t buy enough emissions offsets because everyone’s going to be doing that as well. It does come down to some hard decisions about how we measure it, manage it and reduce it is how I’d put it.

In here you said the approach you’ve taken is there are certain businesses that have a negative environmental impact, and they will obviously want to take steps to reduce that negative impact. And the way you phrase it, they get a credit, as I understand it, a credit for doing something positive. Negative impacts are obviously emissions. What would be some examples of positive impacts?

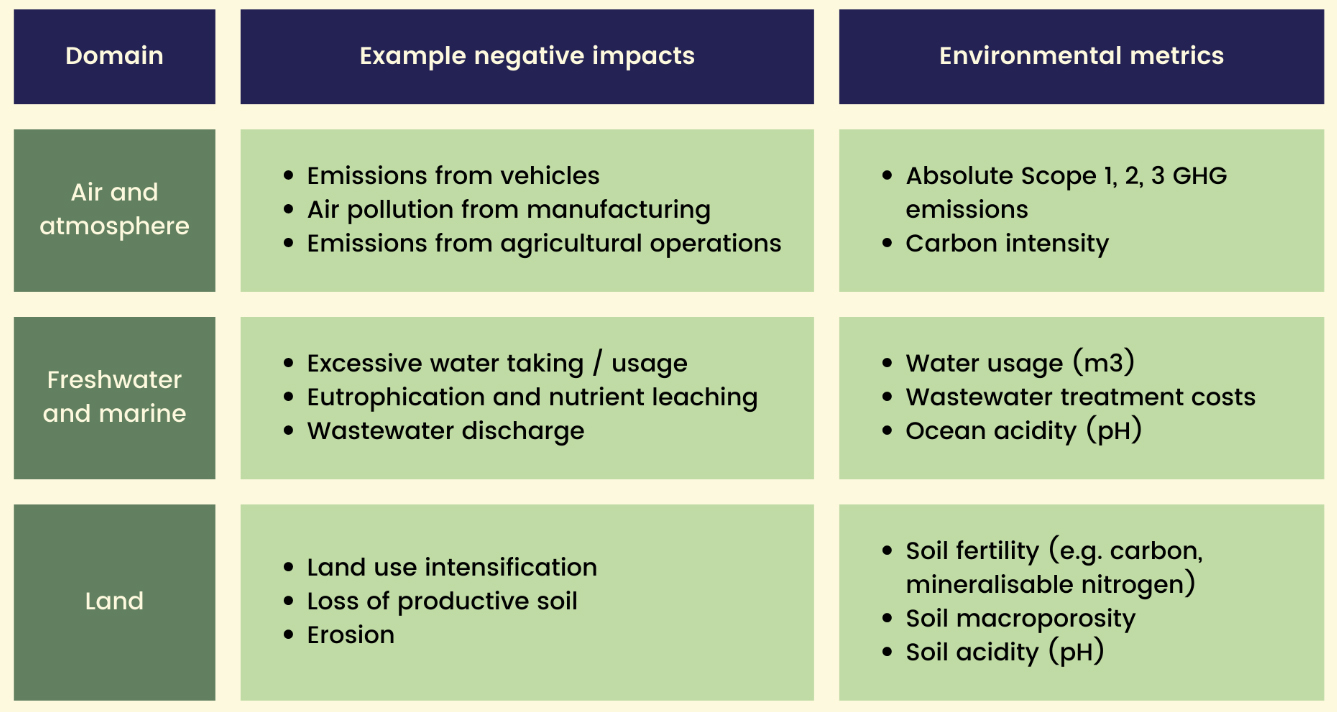

VL How it functions is organisations continue to be taxed at their standard tax rate, but then they’ll have a permanent adjustment in their statement of taxable income. And that net adjustment will take into account both the negative and the positive impact. What I suggest in my proposal is that we focus on three environmental impact domains, because there are a lot of different types of impacts.

And some of them it’s quite difficult for an individual actor I guess, to measure what their own impact is. So, what I suggested was air, for example, that’s kind of where the emissions is. But there would be other negative impacts now, other domains such as around freshwater, marine and land as well. So that’s kind of a negative impact side.

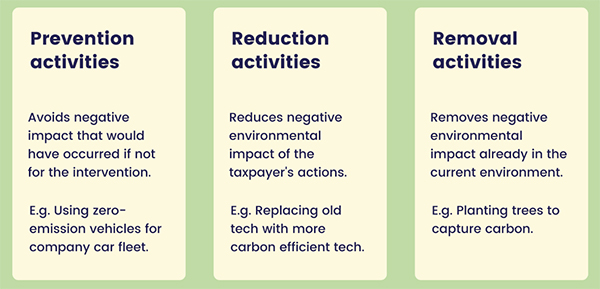

To answer your question on the positive impact. The way my framework sees it is there are broadly three types of activities that would be seen as having a positive impact, and those are namely prevention, reduction and removal activities. The names are probably quite self-explanatory, but you have activities that avoid negative impacts in the first place.

For example, if you just use EVs for your company fleet, then you have avoided having that kind of negative impact. You’ve got ones that reduce environmental impacts, having processes that are more carbon efficient, for example, and then removal as well.

For example, planting trees, or directly capturing emissions and storing them in geological reservoirs. So these are the three types of activities that I see would be seen as valid effectively for having a positive environmental impact.

TB That’s fantastic. And so, as you said, EVs are a classic example. You have an electric fleet, therefore no emissions, but equally switching away to more efficient ones. You went from ordinary car fleet to hybrids. You’ve also got a positive impact there. Further down the chain, you have some pretty old clunkers you’ve been running around on, and you replace them with newer ones. So they’re even more efficient. So again, each one of those has a positive impact. They’re all a slightly different way, one’s a gold-plated option. The other one’s less gold plated, but quite a realistic option.

Car fleets are getting more and more efficient. Something I know the UK and Ireland do is that they measure FBT on emissions. So obviously, electric fleet, no emissions. If you have a more efficient fleet, fewer emissions, lower FBT. It’s fascinating.

In your proposal, you pick up existing ideas about how to measure impact such as the Australasian Environmental Product Declarations. Would you explain a little bit more about how those work.

VL Yes. From my experience, both on the academic side, but also when I was running my own ventures, measuring your impact is really not straightforward. It’s an evolving kind of industry at the moment. I would say there’s no universally agreed methodology, but I think this might change because we are seeing the accounting standards start to develop in that area. From my point of view, I don’t want to reinvent the wheel. There are multiple recognised impact measurement methodologies and as long as you’re taking some sort of reasonable approach to measuring impact, I think that’s valid.

In my proposal, one of the frameworks I referenced was the environmental product declaration, and that’s quite good. That’s basically a third party that comes and verifies the lifecycle environmental impact of a product. And there are other kinds of frameworks as well.

So many large corporates will do their own sustainability disclosures. Some of them will have carbon accounting, for example, and then have those disclosures audited by a specific kind of carbon audit firm. And there are other voluntary standards as well. One that we talk about here at my current role at Fisher Paykel Healthcare is the GRI, which is a voluntary kind of global standard. But again, all these show that lots of organisations are thinking about “how do I report to my stakeholders the amount of my emissions or the amount of landfill waste we divert?” these are the kind of frameworks and existing measurements that impact weighted taxation, which leverage effectively.

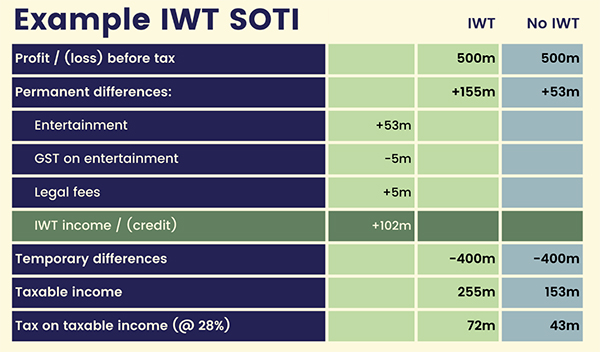

TB Working through an example, you’ve got your statement of taxable income. So, you start with your profit or loss before tax, and you would make your standard tax adjustments? Then you make the impact weighted adjustment which is basically an add-back or a deduction and it’s a permanent difference, isn’t it? There’s no timing around this. I think that’s a strength, actually, because if there was a timing difference, you’d see manipulation straightaway.

VL Yes, and it gets complicated quite fast. Yes, just one off. I see it as permanently increasing for most people, their tax payable, eventually in the long term, as people do more and more positive impacts activities. Then it might turn into a deduction effectively.

TB You’ve prepared an example in here. We’ve got a profit before tax, $500 million, add back permanent differences which would be entertainment $53 million, the GST on entertainment – people often forget that by the way, there’s a whole other podcast I could also do on that. Non-deductible legal fees and then the IWT, the impact weighted Income or credit, which in this case is $102 million.

And then you have the temporary timing differences of $400 million. The net taxable income is $255 million, which the tax on that at 28%, is $72 million. And the difference is effectively without the impact weighted taxation, the taxable income would have been $153 million.

So the impact here for this particular company is an extra $102 million of income at 28%, which today is just over $28 million. Which is, I’d say, a very positive incentive for them to take steps.

A quick question in terms of what happens with the revenue that’s raised there. How do you see that being deployed? As hypothecated or just into the general pool? Over time it would hopefully sink to nothing.

VL I think that’s right. I didn’t have a firm view on this, to be honest. I see potential either way and I think it’s probably more flexible for the government for it to go into a general pool, because there’s opportunities here. You could either, for example, take it to environmental R&D kind of initiatives, or you could take it to the cleanup kind of budget as well.

I don’t really have a view on this. I think for me, we have a relatively low environmental tax take in New Zealand. And as you mentioned before, these negative environmental impacts are effectively being subsidised by us. The Government is paying for it. We need to reprice these activities effectively and this increased tax take just reflects effectively the cost of the activity that these organisations are undertaking. And how that money then gets distributed just depends on what the appetite is really. But long term you’re right, it should go down and part of that will probably involve quite a bit of investment and innovation to do more positive impact activities. We probably don’t even know what they look like right now but could make a significant difference in the future.

TB Yes, I totally agree. Your paper, by the way, has some nice little anecdotes. I mentioned the one about the Rena, but here you’re talking about American Airlines, for example. That if it actually had to account for its environmental costs, they would be US$4.8 billion. And airlines are notoriously non-profitable anyway, so that would be the end of that.

And the other thing is emissions prices in New Zealand for our transport emissions would need to be nearly three times the current price to meet our agreements. So what you’re saying is that new taxes are never popular, but we’re not actually pricing the costs of what we do anyway and we should do. Once you do that, it’s interesting to see what incentives come out of that. Am I paraphrasing that correctly?

VL Yes, that’s absolutely right. And I think part of it is the environmental costs are clear to see at the moment as well. It’s very difficult and that’s why this measurement piece is so key. But I think if an organisation isn’t fully paying those environmental costs, they’re not realising the full cost of their activities.

There’s less of a disincentive for them to stop doing activities with the negative impact. And there’s flow on effects as well. All the stakeholders of the organisation like customers, for example, aren’t getting a clear picture either of what the cost of, let’s say this product is.

So, I think that’s really the thinking around this. “Let’s have a clear picture of what the cost of that activity is.” And you’re right, this does add an incentive to think is there something I could be doing differently to have a positive impact, rather than continuously having negative environmental externalities?

TB We’re starting to see that. What was it last week – the American court wanting to suspend the import of fish caught from the Maui catchment area. It’s something of a concern I have, because although we are much more than an agricultural economy, food exports are tied to our green image. And so, courts taking action like that is potentially quite alarming for food producers and others.

Obviously you’d want to try and mitigate that possibility. And as you say, the current approach of certain industries buying emission offsets just isn’t driving enough change. I think what you’re saying here, to repeat a point, is that you’re building on existing ideas. This is nothing particularly new. As you said, there is already environmental impact standards. So, it wouldn’t be one that every company could come up with.

I imagine for example, as part of the reporting, you’d tell Inland Revenue, these are the environmental impact standards we have adopted, and so long as Inland Revenue say, well, those are approved, that’s fine. That would be how it would work, I imagine?

VL Yes, absolutely. I think it’s all about not adding more compliance if possible. So, if there are already methods where organisations are measuring impact or reporting on it within their financial statements then those should be used. So there are various New Zealand organisations doing integrated reporting and we hear a bit about impact weighted accounting.

Last year as well New Zealand became the first country to require certain financial organisations to make climate related disclosures and I think we’ll see the first of those in 2024. I think off the back of all these we are seeing people doing this reporting anyway. And that’s about how can we link the tax payable to that reporting so that organisations are not just merely disclosing what’s happening but actually have some skin in the game to proactively take action about the impact they’re having so far and how to improve it.

I think using existing standards helps with that, and in the future, we saw in New Zealand for example, that the financial organisations have a set standard now and I think probably over the next few years we will see those standards expand for other organisations and industries. And as they do that, there is an opportunity here for tax to really adapt alongside them and not just wait for the full standards to be implemented before we think about how does tax fit in with this? I think as the accounting standards go on this journey of understanding what this will look like, so too should tax.

TB Yes, tax change is quite interesting. Take the shape of the New Zealand tax system. The other day I looked at 1949 to see what’s in our tax take then. There was even an “Amusement tax”, for example. And then compare that with our system now, and you can see how it evolves over time which is what should be happening. Tax can in some ways lead that change we desire.

So, I’m looking at this proposal and thinking, “Oh my God, I’m a small one-man business. How is this is going to apply to me?” But you’re saying initially it would be larger organisations to begin with. What would be the break point, the cutoff point, so to speak? And would that be a sinking lid, as more and more people came into it as the system bedded in.

VL Yes. I think the initial scope for implementation is voluntary at the start, especially until accounting standards mandate disclosures. That will give people time to work through how this regime would work. And yes, I see large organisations first, consistent with an IFRS accounting definition. https://www.xrb.govt.nz/standards/accounting-standards/

And the reason for that was large organisations are probably some of the biggest contributors to the environmental impacts just due to their scale and size. They’re most likely to be doing some sort of voluntary measurement or reporting already and their actions will have a significant positive impact because of their scale and size. So that’s why I picked large organisations first.

I do think that we have to balance the complexity of measuring environmental impact versus the likely costs that the government would have to subsidise without impact weighted taxation. So, for a smaller organisation, I guess there could be a lot of complexity, especially in these early stages when we’re all trying to figure out how this works. That’s quite difficult.

I do think though, that the impact measurement capability will improve and become more commonplace long term. It would be appropriate to widen the scope in the future. And there is a lot of support out there for all kinds of small and medium sized organisations as well.

I know Sustainable Business Network has been coming out with toolkits aimed at SMEs to help them with impact measurement and reporting. So, as we evolve this and see how the first kind of adopters respond to this regime, and in many years to come, we will be ready for small and medium sized organisations to participate in Impact Weighted Taxation.

And for some of them this could be a huge opportunity as they are realising that customers are interested, and prefer positive environmental impacts, and that could be quite helpful to their business from a customer point of view. And if it also helps their business from a tax point of view, that’s very nice as well that there’s synergies there. I think that might be what it will look like long term.

TB I would say that for some they might find we’ve got a competitive advantage here because we are a low carbon emitter, we’re just a low carbon industry or business, and we’ll jump in on this. By the way what is the definition of “large”?

VL The amounts were updated earlier this year. It’s either total assets in excess of $66 million or turnover exceeding $33 million.

TB So similar to the company’s office reporting standards. That’s still a reasonably sized proportion of businesses in New Zealand. Several thousand businesses could be within that.

VL Absolutely. Much like implementing other tax regimes, you’d first trial it with a few of them. For example, for the R&D tax credit regime Fisher Paykel Healthcare was one of the first to trial that. So that’s probably the key in the initial implementation, voluntary, choosing a select group if needed before you have all large organisations participate. For these kinds of things, it’s key to try it out and see how the details work. I’ve just started some of the thinking here, but I’m sure there will be many other things to work through as well because these kinds of regimes are not simple.

TB But they are necessary, the key point you make is we move to a circular economy. You estimate moving to a circular economy within Auckland alone would be worth $8 billion by 2030, which isn’t that far off. These decades roll round very quickly. This is coming towards us much more quickly. Steps and initiatives like this are what we need. We’ve got to try everything.

VL That’s right. The circular economy is probably a concept we’ve talked about quite a lot recently because everyone’s realising, we need to change our practises hugely. And the way we’re going to do that is to design all the waste out.

We’ve got to make sure everything can be reused, recycled, reprocessed for as long as they can be before they reach the end of their life. Technology can really help us with this as well in terms of figuring out what happens to all these materials. There is an opportunity here for tax to incentivise that as well, so that we effectively accelerate our actions towards that.

TB There’s no doubt, as we both know, tax has a very interesting behavioural impact on people. And as I said, I think for smaller businesses that may have opportunities where they could essentially be in credit, they will take it up, and other businesses that realise we have a problem here will take action appropriately.

And to borrow a phrase I’ve heard about the All Blacks, sometimes we think we need a big bang. We need to just find something that captures emissions and that’s the end of it. But actually, a lot of 1% adjustments will get us there. And I definitely think your proposal is one of those 1% adjustments.

VL Absolutely. It’s about incentivising all the small actions, every little bit counts. That just reflects the reality that every little thing we’re doing will help the environment and that is ultimately going to benefit our economy.

You reference the clean, green image that we so value here at Aotearoa. And a lot of our industries, agriculture, fisheries, these are all very closely linked to our environment. So being able to incentivise things towards us, this is going to help our long-term economy as well.

TB Well, that seems a great point to leave it there. Thank you so much Vivien, for coming on. And congratulations again on what is a fascinating paper, I’m looking forward to seeing more of this and dealing with it myself.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time ka pai te wiki – have a great week.

Inland Revenue about to target 80,000 over incorrect Cost of Living Payments

What about a tax-free threshold?

Last week I discussed some of the submissions made on the latest tax bill and in particular the implications for persons providing accommodation through Airbnb or ride sharing via Uber or a similar app. Reading the comments to the transcript it appeared to me there is some confusion around these proposals. So, this week I thought I’d look at these proposals in a little bit more detail as I didn’t actually cover off the Taxation Annual Rates for 2022-23 Platform Economy and Remedial Matters) Bill (No 2) to give its full title at the time of its (re-)introduction.

The key part of the Bill is the platform economy sometimes also known as the digital marketplace. Now there are two parts to the proposals that are contained in the bill. The first, and what I think is relatively uncontroversial, is the implementation of an OECD Information and reporting exchange framework. This would require New Zealand based digital platforms to provide Inland Revenue with information annually about how much users of those platforms had received from relevant activities.

Inland Revenue would then use that information as part of its administration in the tax system. In other words, checking to see that people who receive payments have returned those payments. It would also share the information with foreign tax authorities where that information related to non-residents. This is intended to take effect from 1st January 2024.

Although this is still to be passed into law, earlier this week New Zealand was part of a group of 22 jurisdictions who signed a multilateral competent authority agreement for the automatic exchange of information under the OECD Model Rules for Reporting by Digital Platforms.

So that process is proceeding even as the legislation is passing through Parliament.

As I said, I think this is relatively uncontroversial. It is supported by the likes of the Chartered Accountants Australia and New Zealand. Interestingly, however, BusinessNZ was less enthusiastic about the proposals although I think it’s largely concerned about compliance costs.

It requested a delay in the introduction of the OECD based and reporting exchange framework, which isn’t going to happen because we’ve already signed the agreement to say we’re going to deliver it.

BusinessNZ also asked for Inland Revenue to undertake a quote, “clearer cost benefit analysis to ensure there was a clear understanding of the likely net benefit of the platform economy changes on the New Zealand economy”. That’s a little bit surprising but probably reflects BusinessNZ’s concerns about compliance costs.

However, it’s the second part of the proposal which generated most of the criticism and pushback from submitters that I referred to last week. The Bill proposes that the current GST rules on electronic marketplaces which apply to remote services and certain imported goods now be extended to “listed services”, which would include supplies of accommodation through Airbnb and other booking services, ride-sharing, beverage and food delivery services and services that are closely related with these services. These changes are intended to take effect from 1st April 2024. There’s a bit of lead time but it’s not that far off.

What these proposals are intended to address is an issue where some of the services provided would normally be subject to GST. But because they’re being passed through these electronic marketplaces, apps, that’s not necessarily happening. And a concern of Inland Revenue and the Government is …

“Ïf this was to continue, it could have adverse consequences for the long-term sustainability of the GST system and place traditional suppliers of these services who are charging and returning GST at a competitive disadvantage. It could also undermine New Zealand’s broad based GST system.”

You may recall that the Hospitality Association was one of those that supported the changes because of this risk.

What the bill does to address these concerns is require operators of electronic marketplaces such as Airbnb, Uber and the likes to become the deemed supplier of or for GST purposes where they authorised the charge for the supply of listed services to a recipient.

What will happen is the person who actually provides the services (what’s termed “the underlying supplier”, such as the driver or someone providing accommodation to Airbnb), would be deemed to have made a supply to the operator within the market electronic marketplace, i.e. Airbnb, Uber or other rideshare operator. That particular supply would be zero rated for GST purposes so that the underlying supplier wouldn’t be paying GST directly, but instead it would be the operator of the electronic marketplace who would be deemed to be supplier and making supplies of listed services of 15%.

Example 4: Listed services performed, provided, or received in New Zealand Charlotte is based overseas and is looking for accommodation in New Zealand for an upcoming holiday. She uses an electronic marketplace to book accommodation in a bach in Queenstown. Under the proposed amendments, as the accommodation provided through the electronic marketplace is in New Zealand, the marketplace operator would be treated as the supplier of the accommodation and would need to account for GST.

Now where the person who actually supplies the accommodation to Charlotte is registered for GST, then the transactions between them and the marketplace provider would be zero-rate for GST purposes.

But if that person wasn’t GST registered, there’s going to be something termed a flat rate credit scheme which requires the app or marketplace operator to pass on as a credit, a proportion of the consideration charged for listed services.

Example 8: Basic operation of the flat-rate credit scheme for marketplace operators Henry provides taxable accommodation through an electronic marketplace where the marketplace operator is responsible for collecting and returning GST on these supplies. Henry notifies the operator of the electronic marketplace that he is not a registered person for the purposes of the GST Act. Charlotte books accommodation that Henry provides through the electronic marketplace for $200 plus GST for the stay. The marketplace operator collects GST of $30 on the supply of the taxable accommodation that they are treated as making to Charlotte. Knowing that Henry is not a registered person, under the proposed amendments, the marketplace operator applies the flat-rate credit scheme and calculates: GST of $30 at 15% of the value of the supply, and the input tax deduction of $17 for the flat-rate credit at 8.5% of the value of the supply. The marketplace operator would be required to deduct input tax of $17 from the $30 of GST payable to Inland Revenue and pass on the $17 to the underlying supplier as a flat-rate credit. The marketplace operator would pay the remaining $13 to Inland Revenue, and this would be the net GST collected on the supply of the accommodation.

This example illustrates where I think BusinessNZ and some of the other submitters have a case about the potential complexities and compliance issues.

Notwithstanding these issues the critical point from Inland Revenue and the Government’s perspective is the proposals put everyone on a level playing field as far as GST is concerned. We will probably end up with more people registering for GST.

The net effect of this, according to the accompanying Regulatory Impact Statement, was about an extra $47 million in GST annually, but I’ve seen estimates that could run as high as $100 million. There is undoubtedly some complexity coming into the system, but I am of the view that in terms of business impact I don’t believe it’s going to be quite as harmful as submitters suggested. I think other factors like the state of the world economy are more important in that case. But we’ll watch to see how what happens with the submissions process.

The expected errors emerge

Moving on, we’ve covered in the past the controversial Cost of Living payments. It emerged this week as part of the annual review of Inland Revenue by Parliament’s Finance and Expenditure Committee that it considers between 70 and 80,000 people may have been incorrectly paid some or all of that $350 Cost of Living payment.

According to the new Commissioner of Inland Revenue, Peter Mersi at least 12,000 people were incorrectly paid the first tranche of $116.67 because of a “coding error”. Apparently, all these people had a negative portfolio investment entity balance, and as it was the only income they had they weren’t actually eligible. But somehow this wasn’t picked up in time.

And then, as been previously discussed, payments were made to others who had left the country but hadn’t apparently updated their details according to Inland Revenue.

Since the first payments went out on 1st August, Inland Revenue has been checking people’s eligibility and as a result, the number of payments made has fallen as they remove what they consider ineligible persons. The first payments on 1st August were made to 1,480,000 people. The second tranche on 1st September went to 1,422,000, and the final payments on 1st October went to 1,384,000. So over the time of the payments, 96,000 fewer people received a payment for the third instalment compared with the first instalment.

So far, 177 people have returned payments and Inland Revenue is about to contact up to 80,000 about potential overpayments.

Separately, there’s another 75,000 who haven’t received any of these payments, even though they aren’t eligible. And the reason they haven’t done so is they’ve yet to supply Inland Revenue with bank account number details.

Now, as I’ve said previously, I thought mistakes were inevitable given the scale of what was happening. I was more concerned about systemic coding issues where there seem to be groups of people that shouldn’t been receiving payments were reported as having received payments. And Inland Revenue has now acknowledged that one of those groups was this group with negative portfolio investment entity income.

I was also concerned about the fact that Inland Revenue estimated it would need somewhere between 750 and 1,000 staff to process the exercise. This bears out a concern I have about Inland Revenue being under resourced. I’m hearing stories that there’s a lot of overtime being carried out by Inland Revenue staff which indicates there’s still a potential staff resourcing issue. No doubt we will hear more about these payments, and we’ll update you on future developments.

Tax-free thresholds and where bracket creep hurts most

I’ve talked previously about a tax-free threshold. And this week, I and other several other tax advisers spoke to Susan Edmunds at Stuff about the idea.

Tax free thresholds are common overseas. Australia has an exemption for the first A$18,200. Britain has a personal allowance of £12,570 and France has an exemption of €10,225. But here in New Zealand as is well known, every dollar is taxed. And partly as a result of the cost-of-living crisis questions have been raised as to whether it’s time to change.

The Tax Working Group did quite a bit of work in this space and it’s my view, as I expressed to Susan, the time’s probably come for small exemption. I was thinking of in the order of $5,000, which was also the number the Tax Working Group landed on.

But the downside is such tax-free thresholds are expensive. For example if you were to exempt the first $14,000 of income, which is currently taxed at 10.5%, would cost $4.7 billion a year. So, there’s a significant trade-off involved.

And there’s another issue that the Tax Working Group identified, which is that a significant proportion of that benefit could also go to secondary income earners in households which were above the median income. Is that something we actually want?

Deloitte partner Robyn Walker talking to Susan Edmunds made the points ‘What are we trying to address here? Is a tax-free threshold the best tool to do so?’ I entirely agree with this. For example, if we’re talking about the cost-of-living, then maybe controversial or not, it may make more sense to consider specific payments, such as happened with the Cost of Living payment.

Robyn also discussed the idea with RNZ’s The Panel. One of the things she mentioned is that there’s a tool on the Treasury website where you can do your own modelling and calculate the effect of different changes to tax rates and you can see the cost of making changes to rates and thresholds.

But discussions around a tax-free threshold and changes to thresholds aren’t going to go away. And a particular point, both Robyn, myself and others keep making is that there’s a lot of pressure on the group earning between $48,000 and $70,000 where the tax rate jumps from 17.5% to 30%. In our view this is the group that probably needs most relief and where politicians should be focused on improvements.

The politicians are undoubtedly working in the background on this issue. National’s got its plan which is to index the thresholds. What Labour has got in the works, we don’t know, but I’m pretty certain they’re planning something.

A winning idea

Finally this week, congratulations to Vivien Lei, who is this year’s winner of the Tax Policy Charitable Trust Scholarship Award. Vivien is currently Group Tax Advisor with Fisher Paykel Healthcare. Her winning proposal was how to change New Zealand’s environmental practices by introducing an impact weighted tax regime. Under this model, organisations would be taxed on their net positive or negative impact on the environment. A very interesting proposal.

Now we’ve had past winner Nigel Jemson on the podcast and I’m very pleased to say that Vivien will be joining us before the end of the year to talk about her submission.

Thousands here could be potentially subject to UK Inheritance Tax.

Airbnb and Uber are not happy about a GST law change.

GST for all its complexities, is the best example of the Broad Base Low-Rate tax principle, a single rate of 15% applied broadly. However, one of the ongoing controversies with GST is around its application to food and other basic necessities. New Zealand’s approach is at odds with many other countries, such as Australia or the UK, where food is not subject to GST (or VAT, as the UK calls it).

Frequently we see commentary that it would be a good move to help lower income earners by removing GST on food. This has been suggested as a response to the current cost of living crisis. I am opposed to such moves and many GST specialists are also in the same camp. Firstly, I don’t think this move is effective as proponents believe, and secondly, if the issue being addressed is low income, then it is better, in my view, to give more income to that target group rather than using a tax measure which would benefit more people, including some who we probably think don’t need assistance.

A report released yesterday in the UK regarding the impact of the withdrawal of the so-called tampon tax bears out these concerns of myself and other GST specialists about introducing GST exemptions. In the UK, VAT of 5% used to apply to tampons and other menstrual products until January 2021, when it was abolished. Prior to its abolition, VAT specialists predicted that the full benefit of abolition would not be reflected in lower prices. And a report by Tax Policy Associates bears this fear out. According to the report, at least 80% of the savings from the tax savings was retained by retailers. In fact the report questions whether any of the benefit of the removal of VAT ever passed through to lower prices.

Professor Rita de la Feria the chair of tax law at the University of Leeds was one of those who warned beforehand of this likely outcome. Commenting on the report she noted this was not only predictable but predicted. In her view “we have to stop confusing policy aim with policy instrument and we also need to stop using tax policy instruments to signal we care about the policy aim.”

Those are wise words and should be kept in mind next time you hear calls for tax changes for ostensibly very sensible reasons. In tax, even with well-meaning policy, there are always unintended consequences and tax is not always the most appropriate mechanism. Sometimes direct action, such as giving payments to those affected, or supplying tampons for free is the best approach.

How UK tax law applies to NZ residents

Staying in the UK, next week the latest Chancellor of the Exchequer, Jeremy Hunt, Grant Robertson’s equivalent, will be presenting the Autumn Statement. He is expected to introduce a number of tax changes and tax increases in an effort to try and restore the UK’s finances. Hunt, incidentally, is the fourth chancellor this year, whereas Grant Robertson is only the fourth New Zealand finance minister this century. So that gives you a measure of just how much upheaval has been going on up there.

I regularly advise New Zealanders and migrants from the UK about UK tax matters. Frequently there are ongoing issues for them and inevitably complexities creep in.

Based on my experience, there are probably thousands of New Zealanders and family trusts who may unwittingly have UK tax obligations. There are also former residents from the UK who are now living here who misunderstand the relationship between the UK and New Zealand tax treatments of investments. So here’s a quick summary of those people who may be affected by UK tax and the differing tax rules between New Zealand and the UK.

Firstly, if you have property in the UK, then UK capital gains tax will apply to any disposals. There are strict timelines about reporting those disposals which are unrealistic in my view, but they still apply. CGT will apply even though the disposal might not be taxable for New Zealand purposes. By the way, the bright line test does apply to overseas property.

If you were renting a property out in the UK then you must report that income both in the UK and in New Zealand. However, for New Zealand purposes, any UK tax paid will be given as a credit against your New Zealand tax payable.

As should be well-known transfers of, or withdrawals from UK pension schemes are subject to New Zealand income tax. I don’t agree with that policy but it’s the law. In addition, if you are receiving a pension from the UK then the UK pension scheme should not be deducting any PAYE. You will need to apply to H.M. Revenue and Customs through Inland Revenue to get any refund of any such tax deducted. By the way, Inland Revenue will not give you a credit for any tax deducted, it wants the tax paid here. That’s the procedure under the double tax treaty and you’ll have to go and get the PAYE back off HMRC, which can be a very frustrating experience, believe me.

But potentially the most significant tax that will apply, which is also the least known, is Inheritance Tax. Inheritance Tax applies firstly to any assets situated in the UK. So, if a New Zealander who worked over in London, bought an investment property there before moving back here, that property is in the UK Inheritance Tax net.

Secondly Inheritance Tax also applies on a global basis to all assets wherever they’re situated if you are “domiciled” or deemed to be domiciled in the UK. Domicile is a complicated concept which I am not going to get into now. But basically, pretty much anyone born in the UK who’s migrated here in the last ten years or so probably still is domiciled for UK tax purposes. If you were a Kiwi and you spent more than 15 years in the UK, you may also be deemed to be domiciled in the UK. If so, Inheritance Tax applies at a rate of 40% on all assets over the first £325,000. (The price of New Zealand property means that this threshold is comfortably exceeded).

In my experience, many migrants and returning Kiwis are completely unaware of the potential impact of Inheritance Tax. For example, UK Inheritance Tax law does not recognise de facto relationships (apparently much to the relief of several politicians a partner in a London law firm once told me). I once dealt with a scenario where the New Zealand resident survivor of an unmarried couple had to pay over £50,000 of Inheritance Tax on her share of a jointly owned New Zealand property after her Scottish partner’s death.

Finally, the UK has a trust register which arrived in the wake of anti-money laundering legislation and its use has been greatly expanded. Any trust which has property in the UK must register. Furthermore, any trust which has a UK source of income such as bank interest must register if it has beneficiaries, including discretionary beneficiaries who are resident in the UK. This is a common scenario I’ve seen. It appears this registration requirement applies even if no distributions have ever been made to the UK situated beneficiaries. There’s some controversy about that particular provision because it appears New Zealand trusts may even have to file UK tax returns even if all the UK income is being distributed to New Zealand beneficiaries.

So that’s a quick summary of some of the UK tax issues which I commonly encounter. I’ll look to update this summary next week if there are any developments from the Chancellor’s Autumn Statement. Now is maybe time to have a look at your position to see if, in fact, you might potentially have a UK tax issue. And also keep in mind that Inland Revenue is currently running an initiative where it is checking on people’s potential tax obligations from their overseas investments.

“We want to remain tax-free”

Finally, this week and back to GST, Airbnb made a submission to Parliament’s Financial Expenditure Select Committee complaining about the proposal for it to charge GST on all accommodation bookings made through its platform.

In its submission, it warned this would stifle the country’s economic recovery and cost the economy up to $500 million a year.

Now this measure was introduced in the Taxation (Annual Rates for 2022-23, Platform Economy, and Remedial Matters) Bill (No 2). Airbnb along with Uber, also affected by the new proposals, unsurprisingly, think the law changes are unfair. On the other hand, the Hospitality Association was amongst those submitting in favour of the change. Chief executive Julie White said a third of its membership consists of commercial accommodation providers adding “and a consistent frustration of theirs is a lack of level playing field when it comes to services like Airbnb”.

The comments from Uber and Airbnb are unsurprising to me. But what I did find of interest about the bill was there have been quite a considerable number of submissions made 820 so far, and quite a few from individuals who would be affected. To quote one, “this law change will result in fewer bookings to me and significantly impact my retirement plans. This will have the additional impact of higher costs of vacations for New Zealand families who are largely for larger families and cannot afford to stay in a hotel.”

Another submitter thought “This action will have a huge negative impact on a new form of tourism at a very personal, localised level.” I’m personally not sure that the impact will be quite as dramatic as those submitters suggest, but it is interesting to see the reaction to what might be seen as a relatively straightforward GST proposal.

As is often the case, many other submitters took the opportunity to push for other changes, such as several suggesting for the removal of FBT on the provision e-bikes to employees.

There was also criticism of the complexity of the interest,limitation and bright-line test rules. One submitter noted that the commentary to the bill had more than 28 pages devoted to remedial provisions for this legislation, and he concluded correctly, in my view, “it is simply not appropriate to expect most landlords to be able to apply the detail of tax law of this complexity.”

Incidentally, the same submitter suggested that because the interest limitation measures had been introduced partly in response to rising house prices, now house prices were falling logically the interest limitation measures should be repealed. It’s a fair point, and he wasn’t the only one to make it. But somehow I can’t see that happening. To leave off where we came in this is another situation where the policy aim and policy instruments have got confused.

New rules about Provisional Tax when you haven’t previously been a provisional taxpayer

Late last week, the OECD released its fourth edition of its corporate tax statistics. These are becoming pretty essential reading about the corporate tax world. They’re particularly important because as the introduction to the report says, “the database is intended to assist in the study of corporate tax policy and expand the quality and range of data available for the analysis of the impact of base erosion and profit shifting” (the BEPS initiative).

This latest edition has information about corporate tax revenues and trends over the past 20 years. But it also looks beyond headline tax rates at the effective corporate income tax rates. There are particularly interesting sections on R&D tax incentives and on the anonymised and aggregated statistics collected via the country-by-country reporting, which is something that came out of the BEPS initiative. These are an absolute gold-mine for corporate tax statistics.

The primary data analysed here is for the year ended 31st December 2019. The average corporate tax revenues as a share of total tax revenues in that year was 15%, compared with 12.6% in in 2000. And similarly, the average corporate tax revenues as a percentage of GDP have risen from 2.6% in 2000 to 3.1%.

How does Aotearoa New Zealand stack up and compare to those general measures? Well, as a share of total tax revenues and corporate tax revenue in 2019 it was 12.4% of the total, which is below the overall average of 15% but above the OECD average of 9.6%. However, Aotearoa is still well below the Asian Pacific average of just over 18%.

On the other hand, as a share of percentage of GDP, at 3.9% it’s well above the OECD average of 2.98% and the Asia Pacific average of 3.26%.

Quite an interesting dichotomy there, it could be said that corporate tax take is quite low. But when you look at it in the context of as a percentage of GDP, it seems relatively strong.

The report notes on corporate income tax rates that they had have fallen considerably for most jurisdictions since 2000. 97 jurisdictions, for example, had lower tax rates in 2022 than in 2000. Another 14 had the same, but only six including China have a higher rate.

On average, these rates have been declining. The average combined rate across the 117 jurisdictions covered is now 20% compared to 28% in 2000. Our current 28% is near the top of the pile. Australia is also quite high up with its 30% rate, although that is about to reduce. In 2000, the percentage of jurisdictions where the statutory corporate tax rates were greater than or equal to 20% was 85%. For this year, it’s down to 60%.

But as I’ve said in the past elsewhere and the report notes, the trend has been starting to reverse. The infamous Trussonomics budget was going to reverse corporate tax. Increases proposed for next year. In the wake of that complete disaster those tax increases have been reinstated. And that’s quite a significant change in direction.

The report also examines what is the effective average tax rate across the jurisdictions. This is seen to be a much more accurate tax policy indicator than statutory tax rates. For 2021 the average effective average tax rate across the 77 jurisdictions covered is 20.2% which is 1.2 percentage points lower than the average statutory tax rate of 21.4% for the same year.

Here in Aotearoa-New Zealand, the statutory effective statutory tax rate is 27.1%, which is not far short of our statutory rate of 28%. And that reflects the lack of distortions and special incentives we have in our tax system. In fact, when you examine effective marginal tax rates, we’re in the top ten of all countries at 20.1%. By comparison with many other jurisdictions, such as Finland, which was in the news this week, its effective marginal rate is 15%. Also in the top 10 are Australia with a rate of 16.9% and Japan at 17.2%. Incidentally, Argentina has the top effective marginal tax rate of 29.2%.

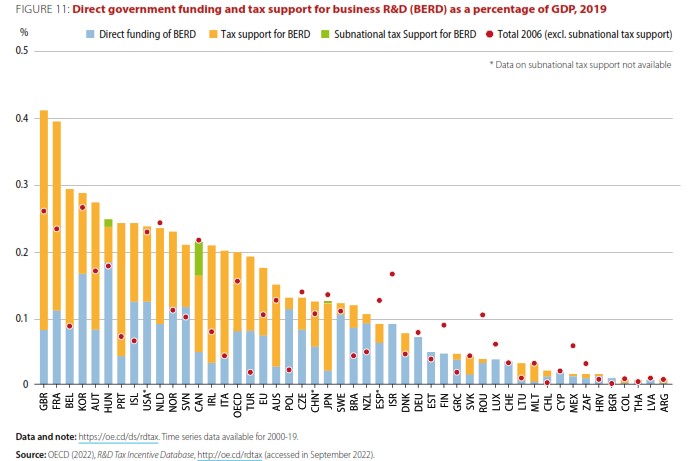

The database looks at tax incentives for research and development, and the total of direct government funding and tax support for business R&D as a percentage of GDP in 2019. Across the OECD it was 0.2%. Aotearoa-New Zealand is well down the field at just over 0.1%. What I thought was quite interesting is more than 80% of it comes from direct funding from the government. A very small proportion, barely 20% of that 0.1% is for tax support and that’s actually amongst the lowest across all the OECD.

And it seems to me that points to the concerns which are continually raised about productivity. If we’re not investing in R&D, should we be looking harder at why investment in R&D is so low and what can we do to boost it. Has the government been doing too much or not enough and what part of role businesses playing in that?

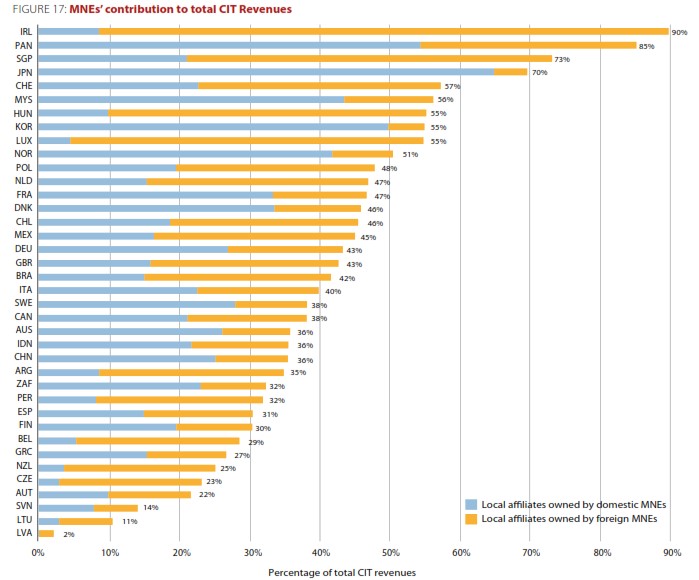

Another thing that caught my eye which I thought was potentially quite concerning was the contribution of multi-national enterprises (MNEs) to total corporation income tax revenues. At the top is Ireland where 90% of the corporate tax take comes from foreign multinational enterprises.

We’re near the bottom with 25% of total corporation tax revenues come from multinationals. So that’s a surprisingly low figure. But what I thought was particularly concerning was the breakdown of this. What the report does it splits the reporting between local affiliates owned by overseas MNEs and local affiliates owned by domestic multinationals. In our case the proportion from domestically owned multinationals is under 5% which appears to be amongst the lowest in the OECD. I think only the Czech Republic and Lithuania have a lower percentage. I wonder whether that points to a lack of diversity in expansion overseas in by our corporate sector.

Some of this information comes from aggregated Country-by-Country Report (CbCR) data which has been collected from almost 7,000 MNEs with turnover exceeding 750m Euros. The data analysed from 47 countries including ourselves indicates “evidence of misalignment between the location where the profits are reported and the location where economic activities occur”

For example, the median value of revenues per employee in jurisdictions with a corporate income tax (CIT) rate of zero is USD 2 million as compared to just USD 300,000 for jurisdictions with a CIT rate above zero. Moreover, in investment hubs, related party revenues account for 35% of total revenues, whereas the average share of related party revenues in high-, middle- and low-income jurisdictions is around 15%. “While these effects could reflect some commercial considerations, they are also likely to indicate the existence of BEPS.”

I think Inland Revenue and other tax authorities will be reviewing this data with interest. Anyway, lots to consider in these statistics, particularly about increasing R&D and the role of overseas export focused multinationals.

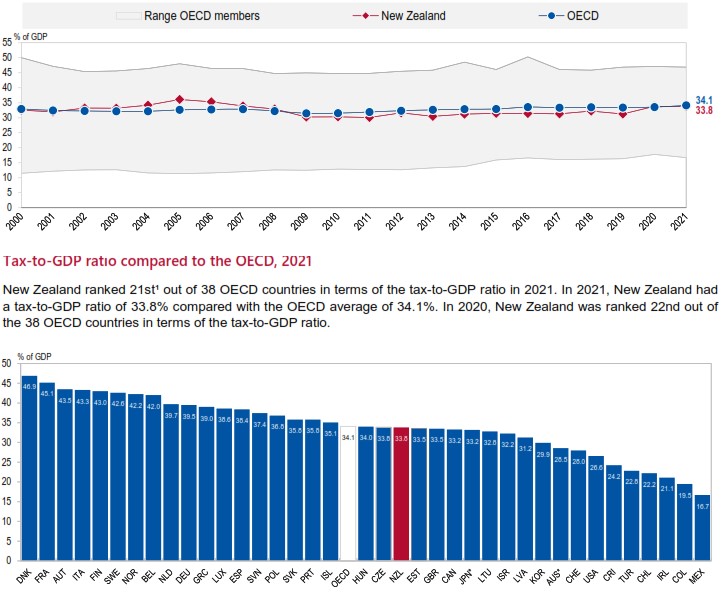

Coincidentally, on Wednesday the OECD also released its Revenue Statistics 2022 edition. This shows how tax revenues bounced back in 2021 as OECD economies recovered from the initial impact of the COVID-19 pandemic. In fact, the OECD average tax-to-GDP ratio rose by 0.6 percentage points in 2021, to 34.1%, the second-strongest year-on-year increase since 1990.

Tax-to-GDP ratios increased in 24 of the 36 OECD countries for which 2021 data on tax revenues was available, declined in 11 and remained unchanged in one. That one country was Aotearoa-New Zealand where the ratio staying at 33.8%, below the OECD average of 34.1% and ranks 21st out of 38 OECD countries.

What the Crown Accounts tax data reveals

It was a busy week for tax data as the Government published its financial statements for the four months to 31st October. The total tax receipts of $35.6 billion for the period is actually $122 million below forecast, which in the scheme of things doesn’t seem too bad. We are seeing fairly strong wage growth from PAYE or source deductions. The forecast was for $14.4 billion but in fact, it was $628 million above that at just over $15 billion. Company income tax was also $302 million above forecast.

However, GST at $9 billion was $945 million below forecast which is a very significant shortfall. Because of the Government extending its cuts to fuel excise duty and road user charges they were 30% lower than forecast, a shortfall of $185 million.

What does all this mean? Firstly, we can see the effect of fiscal drag, which we’ve talked about endlessly. That is the impact as people’s salaries increase and take them across the thresholds, most notably the $48,000 threshold where the tax rate jumps from 17.5% to 30%. We can still see the impact of that, and that’s a factor in the strong growth in PAYE receipts.

To give you an example of the overall effect, the PAYE receipts for the four months to 31st October 2021 were $13.3 billion. But in the four months just ended, these were $1.5 billion or 11% higher at $15 billion. So that’s the effect of fiscal drag which is an issue which isn’t going to go away before next year’s election so expect to see plenty of political posturing and manoeuvring around that issue.

When Bright-line taxes are payable – maybe surprises for some

And finally Inland Revenue have released a draft consultation on the question of provisional tax and the impact on salary of wage earners who receive a one-off amount of income without tax deducted. This scenario could arise where a salary earner realises a gain from the sale of a property subject to the bright-line test. Other instances include shares released under an employee share scheme or one I’ve seen quite frequently, the tax liability arising on the transfer of/or withdrawal from a foreign superannuation scheme.

Typically, when this happens because the taxpayer is on PAYE, they weren’t a provisional taxpayer in the previous tax year as their residual income tax, or RIT, was under $5,000 in the year prior to the receipt of the untaxed sum.

Under the draft consultation, if the tax on the untaxed income is over $5,000 the taxpayer will be deemed to be a provisional taxpayer. But, so long as the total amount of tax payable ends up as being less than $60,000 then the use of money interest exposure will be only start running from the terminal tax date, typically, this would be 7th February following the tax year end of 31st March. This is pretty reasonable and reasonably well understood.

The problem is, though, if the RIT is over $60,000 then the person is meant to pay the tax due on the third provisional tax instalment date, that is 7th of May following the tax year end. If not made, use of money interest starts to apply. Many people affected probably haven’t quite realised that’s when their tax liability is due rather than on the terminal tax date, so it’s good to get clarity on this.

It’s particularly important because Inland Revenue has just announced that use of money interest rates are to rise with effect from 17th January. The rate of underpaid tax will rise to 9.21% with the rate on overpaid tax also increasing to 2.31%. I have to say that that 6.9 percentage point gap is frankly a bit of a laugh, and at odds with some of the somewhat pointed comments made by the Government to banks about social licence and assisting customers during hard times.