controversial Inland Revenue proposals for shareholder loans hit a major roadblock

The Finance and Expenditure Select Committee has reported back on the Taxation (Annual Rates for 2025-2026, Compliance, Simplification and Remedial Matters) Bill. This Bill contained measures in relation to changing the tax treatment of non-resident visitors who are working remotely while visiting New Zealand, introducing the new Revenue Account Method for calculating foreign investment fund income, plus the usual host of other amendments tidying up various issues.

The amendments to the tax treatment of New Zealand visitors are designed to encourage people to work here remotely without triggering too many adverse tax effects. One change proposed relates to disregarding the activities of a non-resident visitor present in New Zealand when determining whether a company is tax resident in New Zealand.

Watties, Heinz, tax and a Lions legend

This is a long-standing point and with Watties being in the news for all the wrong reasons, I recall an interesting point raised way back in the 1990s when Watties was acquired by Heinz, the international food manufacturing giant. Apparently, Tony O’Reilly, the former British Lion and then chairman of Heinz, was in the country at the time the deal was being finalised. Did this mean Heinz had a permanent establishment in New Zealand because key decision makers were here?

Tony O’Reilly in action against the All Blacks in 1959

That was a somewhat mischievous question. But it is an example of where key personnel being in a country may trigger unintended and adverse tax consequences. The Bill tidies up a number of issues relating to this as well as clarifying the treatment of remote working by non-residents.

No major changes to the Revenue Account Method proposal

When the bill was introduced, much fanfare was made of the proposed Foreign Investment Fund (FIF) Revenue Account Method. This allowed an eligible person’s FIFs to be taxed on a realised gains basis with a discount of 30% applied to the gain resulting in an highest effective tax rate of 27.3% (i.e. 70% of 39%).

This was seen as disappointingly high so many submissions on the Bill requested a higher discount to reduce the effective tax rate. These have all been knocked back on the basis that the maximum rate of 27.3% is broadly comparable to the 28% payable under the PIE regime.

But there are some minor mostly technical changes. For example, losses arising under the Revenue Account Method were initially to be ring-fenced and only available against future gains. Any such losses will now be available to offset against dividends from the same interests. So that’s a bit of a win.

And there is the ability also to allow taxpayers to sometimes use other method calculations which are required at present rather than and not lose their eligibility to apply the revenue account method to other interests. In other words, you can sort of split treatment on that. So generally, the rules are a progression, but I think you can read when you get into reading the fine printing, you sort of see the technical minutiae and issues that pop up because of the complexity involved.

There was an interesting, there’s also a proposal for essentially there’s a realisation tax on migration, and a point has now been clarified that If this happens, the calculation of any tax payable, because someone has used the revenue account method and then migrated out of New Zealand, they would use the market value of the interest at the time the person departs New Zealand, not the market value received when the interest is subsequently disposed of.

Quick example, a person leaves New Zealand when the market value of one of these interests is say, $500,000, subsequently sells it and realises the market value of $1,000,000. Any New Zealand tax payable will be based on the 500,000 being the market value at the time they left.

Don’t look the parents are squabbling…

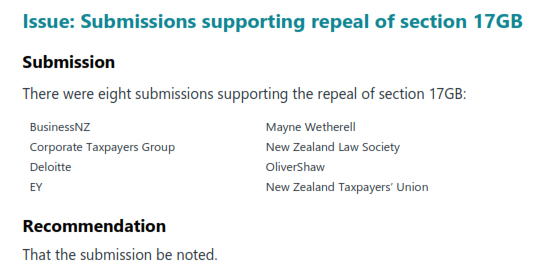

There was a nice little spat between the various parties on the committee over the proposal to repeal the Section 17GB of the Tax Administration Act 1994, which allows the Commissioner to collect information for the purpose relating to the development of policy for the improvement of the tax system. This was the measure introduced under the last Labour government, which was then used as the basis for finding the information for Inland Revenue’s controversial 2023 High Wealth Individual Review. Unsurprisingly Labour and the Greens opposed its repeal as did 202 submissions (including for the record Baucher Consulting, and the Chartered Accountants of Australia and New Zealand). Eight submissions supported the repeal.

Information sharing risks?

Labour was also opposed to the provision expanding the ability to allow Inland Revenue to share information about individual taxpayers with other government agencies more easily by way of Ministerial agreement. The Labour Party MPs made this very valid point,

“While Inland Revenue has strict rules about which employees may access information about individual taxpayers and it polices those rules rigorously, the same protocol may not apply in other agencies.”

Indeed, Inland Revenue, to the best of my recollection, has never had issues where someone has emailed out a spreadsheet full of confidential details which we’ve seen both the Ministry of Social Development and ACC to name a couple of culprits do. The Labour Party also noted “This is a significant change to the rules that protect the privacy of taxpayers’ information. We note the Office of the Privacy Commissioner has concerns about these proposals.” Despite this the provision is to go into effect.

Financial arrangements – three welcome surprises

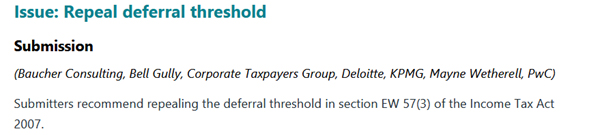

A big and welcome surprise relates to changes to the financial arrangements regime. Under the financial arrangements regime if certain thresholds are exceeded taxpayers must calculate income and expenditure on an accrual, or unrealised, basis rather than on a cash, or receipts, basis. These thresholds had not been increased since 1999, and the bill proposed to double them.

The regime also has a deferral threshold which means income and expenditure must be calculated on an accrual basis (unrealised) if the difference between calculating income on a cash (receipts) basis and the accrual basis exceeded $40,000 at any point. This applied regardless of whether a taxpayer’s total financial arrangements were under the $1 million threshold. Unsurprisingly, this deferral threshold frequently tripped up taxpayers (I even once saw advice from a Big Four firm which had overlooked its impact). I was one of several submissions recommending repeal of this threshold.

Inland Revenue has accepted our submission noting the deferral threshold

“…imposes a high compliance burden, requiring taxpayers to calculate income and expenditure on an accrual basis to compare it with a cash basis result and ensure that the difference is below a threshold. This is the same compliance burden that being a cash basis person is intended to avoid.”

This is an excellent result.

But wait, it gets better

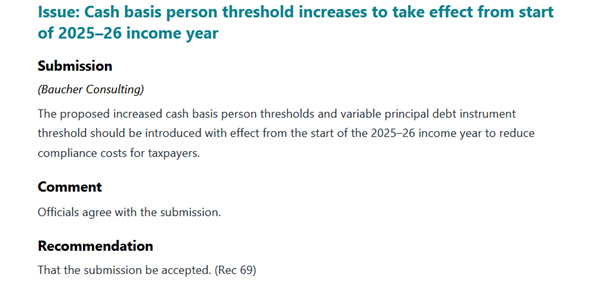

Under the Bill the increased thresholds were due to take effect from the start of the 2026-27 income year (1st April for most people). Adopting the principle of you don’t ask, you don’t get, I also submitted the threshold changes should be effective as of the start of current tax year (i.e. 1st April 2025). This would reduce compliance costs for the taxpayers, one of the key objectives of the Bill.

To my great surprise and delight, that was accepted as well, which is another excellent result.

But wait, there’s more…

KPMG made a very sensible submission that foreign currency loans used as mortgages over property should be removed from the financial arrangements rules and calculations. Exchange rate fluctuations can mean the deferral threshold is breached making any unrealised foreign exchange gains taxable. This once happened to one of my clients resulting in a tax bill of over $100,000.

Although Inland Revenue did not accept KPMG’s submission in full, it proposed instead “limiting the effect of foreign exchange fluctuations for the absolute value threshold”. This would be achieved by testing the absolute value threshold (now $2 million) is tested using the principal amount converted at a set date, for example, the first day of the financial arrangement, and ignoring subsequent foreign exchange fluctuations. If the principal amount changes for non-foreign exchange rate, reasons i.e. increases or decreases in borrowing, the financial arrangement should be reassessed for the threshold.

A bit late for my client perhaps but still a good result. The three change are also good examples of the Generic Tax Policy Process in action resulting in sensible law changes.

Controversial shareholder loan proposal halted

Moving on, late last year, Inland Revenue dropped what I described as a bombshell, with a consultation proposal for significant changes to the treatment of shareholder loans. Inland Revenue proposed that shareholder loans above a certain threshold would instead be treated as dividends, similar to the treatment for Australian and UK taxation purposes.

These proposals have hit a major roadblock with opposition from Winston Peters and New Zealand First together with the ACT Party. The end result is that the proposals as put forward in December will not be proceeding. Instead, Inland Revenue will continue to review the issue of the treatment of outstanding shareholder loans when a company goes into liquidation owing tax.

The proposals were quite controversial but the same time there was something of a tacit acceptance that yes, perhaps something needed to change. Simultaneously, there were concerns that Inland Revenue was perhaps muddling two issues. One of the issues was that companies that went under often sometimes owed substantial sums by shareholders, and in some cases, this meant Inland Revenue was missing out because funds were paid to shareholders instead.

John Cantin, former guest of the podcast, and also the independent advisor to the Finance and Expenditure Committee on the current tax bill has made public his submission to Inland Revenue on the shareholder loan proposals. His view is that more information is needed on the interaction between outstanding shareholder loans and company failures and the composition of the tax debt of such companies. If it is mostly GST and PAYE? Then yes, maybe that is something to be considered. He also thought there was merit in looking at changing the tax treatment of what happens on liquidation.

The upshot is we’ll be going back for round two of consultation. It’ll be interesting to see what comes out of this. Like John I think changes around what happens when a company is put into liquidation are sensible and also around keeping records of what we call available capital distribution amounts and available subscribed capital.

Property flippers – what about the tax impact?

And finally, an interesting story from RNZ about a complaint to the Real Estate Authority about a rise in so-called ‘property flippers’ making six-figure returns from unwitting vendors. Property data firm Cotality has noted a rise in significant rise in what’s called contemporaneous sales, with the number happening last year was almost double the total for 2024.

In a contemporaneous settlement, a property flipper makes a purchase offer with a long settlement period and then finds another buyer to purchase the property on the same day the property flipper has to settle their purchase. If it all goes to plan the property flipper makes a quick gain.

According to iFindProperty co-founder Maree Tassell who has complained to the Real Estate Authority about the practice:

“It’s quite common that there are some deals out there where people are making over $100,000-plus on contemporaneous settlements, getting a property under contract. The poor old vendor, and even often the vendor’s agents will think ‘oh this is a real purchaser’. …It’s quite deceptive to the vendors and quite deceptive sometimes to the agents.”

Although tax isn’t actually discussed in this story, these transactions would be considered a taxable trading activity even if they are not specifically within the bright-line test rules. It’s the sort of activity Inland Revenue should be watching with great interest. Property flippers should therefore beware, you may be making a quick buck, but Inland Revenue will be tracking these transactions. If you are not declaring the income, then you could find yourself with a big please explain somewhere down the line.

And on that note, that’s all for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

We’re racing towards the end of the current tax year. And naturally, at this time of year, tax advisors will be planning ahead and considering what elections we might need to make before 31st March, whether to bring forward taxable income into this year or, if we can, defer taxable income into a later tax year because we are aware that in that new year a lower tax rate will apply.

Right now, I’m discussing these timing options with a number of clients who are thinking about transferring or withdrawing funds from their UK pension schemes. Such transfers/withdrawals are taxable under the foreign superannuation scheme transfer provisions in Section CF3 of the Income Tax Act 2007.

Long-term followers will know that I am not a fan of this regime, but it’s now been in place since 2013. One of my major criticisms with the regime is that it triggers a tax liability for the transferor, even though that person may not be able to access the funds in the scheme to pay the tax. This wasn’t really grasped by most of the industry until after the reforms were put in place.

The Scheme Pays solution

Subsequently, there’s been a long period of consultation between industry specialists and Inland Revenue, and then between Inland Revenue and HM Revenue and Customs (HMRC) to find an answer to this issue. Fortunately, and finally, that answer has now been found and will become effective from 1st April. It’s known as the ‘Scheme Pays’ option, under which the transferring scheme, the receiving scheme (which for UK purposes is known as a qualifying recognised overseas pension scheme or QROPS) will pay the tax on behalf of the transferor, the transfer scheme withdrawal tax.

The benefit of the Scheme Pays option is twofold. Firstly, the tax may be paid from the funds that are transferred. The problem that had existed previously was that HMRC could have treated a withdrawal to pay the tax as an ‘unauthorised withdrawal’ for UK tax purposes, which could come with a 55% tax charge on it. Working through a solution which was mutually acceptable to HMRC and Inland Revenue took some time.

Secondly because a QROPS is a portfolio investment entity the tax rate payable is capped at 28%. The option that now becomes available for people considering a transfer into a QROPS is If they do so, they will pay tax at 28%, which if they’re a higher rate taxpayer – 39% – is a very attractive option.

When to transfer?

The issue now under consideration is whether a person transfers a scheme before 1st April, be taxed at the usual personal tax rates and is therefore responsible for meeting the tax personally. Alternatively, defer the transfer until on or after 1st April and into a QROPS. The deferral will increase the amount of taxable income, but the trade-off is a flat 28% tax charge. There are some clients where that’s an extremely attractive option, and we’re talking about saving tens of thousands of dollars as a result.

There is an argument, in my view, that the tax rate for all transfers like this should have been 28% or linked to the top prescribed investor rate all along, because basically part of the rationale for this regime is countering people getting a benefit from investing offshore.

The transfer scheme withdrawal tax

The individual making the transfer is still liable for determining the taxable amount of the transfer. For example, if it’s $100,000, the receiving QROPS will withhold 28% or $28,000 from the amount transferred and pay it to Inland Revenue. The transferring taxpayer has got 10 working days from the point at which the funds reach the scheme to ask the scheme to pay the tax (‘Transfer Scheme Withdrawal Tax’) on your behalf.

The taxpayer can calculate the taxable amount using either the ‘Schedule Method’, or the ‘Formula method’ if it is available. For many people who are transferring defined benefit schemes, such as UK teachers’ pensions or UK police pensions, they must use the Schedule Method.

It may have taken a long time to resolve but the Scheme Pays option is a good alternative. As I said, it has the potential to save thousands of dollars for some taxpayers. So if you’re considering transferring your UK pension you should get in touch with your local tax advisor.

Changes to banking taxation ahead?

Moving on, in my last podcast I mentioned in passing that the Minister of Finance had made comments about a potential banking review. Subsequently there’s been a couple of stories in the New Zealand Herald and Business Desk on this matter, in particular, Inland Revenue are preparing a consultation document entitled Changes to Tax Rules for Foreign-Owned New Zealand Banking Groups.

the document outlines a series of technical proposals aimed at improving the integrity of the tax system. Apparently, the changes would affect offshore banks that have branches in New Zealand (about 6% of the banking sector by assets according to 2024 figures) rather than locally incorporated banks with which the vast bulk of Kiwi households and businesses engage. While the proposed changes could see banks pay a bit more tax, they aren’t aimed at generating material amounts of additional tax revenue for the Crown.

Although it’s interesting to see this issue under consultation, it represents one of the group of technical issues that Inland Revenue is always mulling over particularly because being the banking sector, there’s possibly quite some large sums involved.

A banking levy surprise in the Budget?

Dileepa Fonseka in Business Desk wondered, whether in fact, there might be some form of banking levy introduced as part of the budget on 28th May. He considered whether such a levy could possibly be tied to the recently established Depositor Compensation Scheme (DCS).

Dileepa notes that in Europe, 17 countries and the United Kingdom have introduced bank levies or financial stability contributions in the years following the Global Financial Crisis. Many were levied on the liabilities banks carry rather than profits and are designed to ensure financial stability and to cover the cost of insuring bank deposits.

It’s possible anything which taxes banks more might be a bit of a vote winner, even if, as experts note, there’s a chance that such levies might ultimately be passed through to customers. Dileepa also makes an interesting comparison with a similar levy which was a surprise sprung by Scott Morrison in 2017 when he was the Australian Treasurer (Finance Minister).

It’s interesting to see the stories circulating in this space. We’ll get more details on the Inland Revenue consultation when it is publicly released, and we’ll discuss it then. Meantime, as I said in the first podcast of the year, we could expect to see a bit of electioneering around a potential bank levy.

Foreign Investment Funds and transitional residents

Finally, this week, there’s an interesting Inland Revenue Technical Decision Summary, TDS 26/01, regarding the opening value of foreign investment funds. It relates to a transitional resident, a person who has either not previously been resident in New Zealand or has been non-resident for at least ten years. Transitional residents generally are eligible for a 48-month exemption from New Zealand income tax on their overseas investment income. But what happens when that exemption period expires?

The taxpayer in the TDS also requested a 31st December balance date, which had been approved by Commissioner. In other words, without saying so specifically, this client is probably an American who must file US tax returns to 31st December. And as the TDS notes, a 31st March balance date means there are high compliance costs because the person has to calculate income for US tax purposes to 31st December and then for our purposes to 31st March.

The taxpayer’s last day of his transitional residence exemption period was actually 31st December 2024. He requested a change of balance date for his tax year from 31st March to 31st December to align with his US filing period. Inland Revenue agreed to the request which means that balance date could be used for calculating hi FIF income. Which is good because that is very handy for many American clients, because of the dual reporting they have to do.

But the other point is that the TDS agreed the opening value for each FIF interest for the purposes of the income year ending 31st December 2025 would be nil, not the value as of 31st December 2024. That means that when applying the fair dividend rate, which is 5% of the opening value and any quick sales adjustments, the opening value would be NIL. Therefore, for the year to 31st December 2025, only the quick sales adjustment calculation will apply in relation to the FIF interests acquired and disposed of during that tax year.

This is an interesting little summary. It confirms a point that some of us had thought was the case, that clients required to file American tax returns could switch to a 31st December year end to help ease compliance. The taxpayer still has to request a change but this TDS indicates Inland Revenue should accept the request.

Still on foreign investment funds, we should hear this week about the final form of the proposed change, allowing taxpayers required to file US tax returns to adopt a quasi-capital gains tax or “revenue account” approach to their foreign investment fund interests, i.e. being taxed on a realisation basis. The Finance and Expenditure Committee is due to report back on 10th March on the Bill and we’ll bring you that news next week.

And on that note, that’s all for this week, I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

Welcome to 2026. It’s early in the year, but the main drivers for the tax year seem already set. With $9.3 billion of tax interest and penalties outstanding as of 30th June 2025 Inland Revenue’s crackdown on debt will continue. It will also ramp up its investigation activities, with holders of crypto-assets under particular scrutiny.

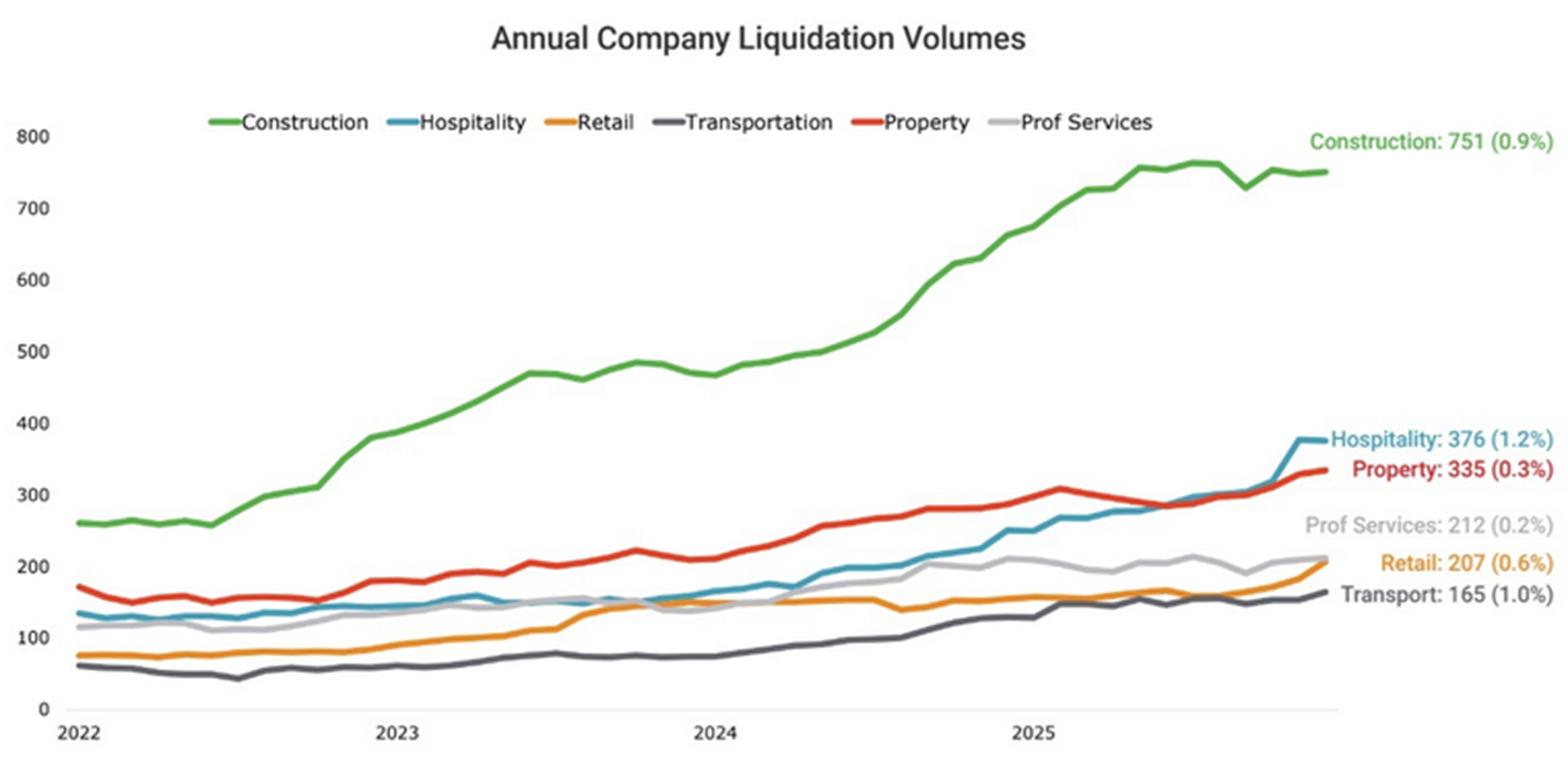

Inland Revenue is working hard to get the overdue tax debt down. However, the economy isn’t in great shape, with a recent story pointing out that liquidations have been the highest since the global financial crisis in 2008-2010. The construction sector in particular is struggling.

If you are behind with tax debt contact Inland Revenue

I cannot stress this enough, if you are in trouble with your tax debt, the first and best thing you should do, is to approach Inland Revenue. So long as you are realistic and open with, you will probably find it is prepared to work with you on an instalment plan. And in some cases where the debt is relatively small, say under $20,000, you can set up your own instalment plan, or your tax agent can help you do it.

The key thing is you have got to make the initial approach because Inland Revenue’s attitude hardens if it feels that a tax debtor is not making realistic attempts to address the scenario.

The 80:20 rule in reverse

An interesting feature about the composition of tax debt is that although the bulk of tax is paid by the very largest companies in the form of PAYE, GST, and company income tax, the majority of tax debt comes from SMEs, micro-businesses and individuals. As of 30th June 2025, over 527,000 taxpayers owed tax. For many of those small businesses, the owners are under enormous stress and it’s difficult to address the issue of tax debt. Perhaps surprisingly, my experience has been that many clients are relieved when they eventually do contact Inland Revenue as it’s often not as bad as feared and a plan is now in place.

Don’t expect the Election to change anything

We can also expect to see Inland Revenue ramping up activities. I would not be surprised if this year’s Budget has more funds for investigation and debt collection activities on top of the $35 million per annum boost it received in last year’s Budget. And by the way, this will be something that will remain the same even if there’s a change in government after the Election. Inland Revenue will still be expected to crank up its enforcement activities.

Cryptoasset investors targeted

On investigations, I’m hearing noises that transfer pricing reviews are increasing, but a key focus area is cryptoassets. Inland Revenue noted in its last annual report that it had several cases going through its dispute process, which involved “tens of millions of dollars”. It seems to be taking a fairly aggressive approach.

A client has shown me a letter where Inland Revenue have said, “if you do not make a voluntary disclosure or contact me directly, I will assume that you have deliberately failed to correctly declare your cryptoasset income.”

The tone of this letter was really quite surprising to me. Generally speaking, when Inland Revenue is considering investigations and audits, it is never as aggressive as that. More often the questions/letters that come in are along the lines of “Are you sure about that? Maybe you might want to check and come back to us.” Whatever Inland Revenue’s tone cryptoasset investors and traders should expect enquiries.

Wrapping, bridging, lending, borrowing and staking cryptoassets

Still on crypto, Inland Revenue has released a 30 pages issues paper for discussion setting out its view on the income tax treatment of wrapping, bridging, lending, borrowing, and staking cryptoassets, or decentralised finance (DeFi) transactions.

The basic position Inland Revenue has adopted with crypto is that it is property, and therefore the general rules apply that the disposals of crypto will be taxable if they were acquired for a main purpose of disposal or as part of a profit-making activity.

The paper refers to increases in crypto arising from DeFi transactions as “rewards”. Inland Revenue’s view is these are money’s worth and usually taxable when received. The analogy would be these rewards are like a dividend or an interest payment and should therefore be taxed. Submissions on the paper are open until 12th March.

Expect some crypto related court decisions

Last November I discussed the Technical Discussion Summary TDS 25/23 on the taxation of cryptoassets. As previously noted, Inland Revenue is currently involved with several similar cases involving “tens of millions of tax” so I expect some cases to appear in the courts this year perhaps either before the Taxation Review Authority, or the High Court.

As an aside it’s worth noting one of the interesting (and I don’t think it’s entirely healthy to be frank) issues with our tax system at present is that we don’t actually get an awful lot of tax cases coming through, partly because the dispute process is designed to try and resolve most issues before they get to court.

But I do wonder if it’s gone too far the other way. Supreme Court Justice Susan Glazebrook has publicly remarked on the decline in tax cases in the courts. Is that entirely healthy, given that tax is a fairly litigious topic? It is a little surprising when you step back and reflect that we don’t see many tax cases coming through. That said, I expect we will see some crypto related cases this year.

International tax – America goes its own way

Moving on, the year has been quite frantic with international developments. One of the features of the new second Trump administration is its withdrawal from many international agreements, and it has also made it very clear that it will view unfavourably what it regards as discriminatory tax practices.

As a result, the international two-pillar agreement that the OECD/G20 been working on for close to a decade now has hit a big speed bump, with the Americans making it very clear they don’t believe or consider that its multinationals (we’re talking particularly the tech companies) should be subject to those rules.

Now the end result of that is that there’s been a development called the side-by-side package which the OECD released in early January. l It’s convoluted as always with international tax, but at the moment, there’s only one country that qualifies for the side-by-side system, and you’ll not be surprised to hear that’s the United States. Basically, the idea is to allow Pillar Two to continue to coexist with the American tax regime and in theory deliver comparable minimum tax outcomes. In theory everyone is still progressing towards the 15% minimum corporate income tax rate globally.

Incidentally, the Pillar Two rules were effective for 2025 from a New Zealand perspective which means some multinationals may be subject to these rules. As I mentioned earlier, there’s been reports coming out from the Big Four that more transfer pricing reviews are happening. Anyway, we’ll keep our eyes on what’s going on in the global tax space. We expect to see more developments in that area. And it’d be interesting to see how Inland Revenue approaches its audit work in relation in this space.

“What’s in a name? That which we call a rose by any other name would smell as sweet”

Finally, it’s an election year and tax seems set to play a major part of the debate this year. So far Labour has proposed a capital gains tax on residential properties (excluding the family home) and commercial properties.

Meanwhile, echoing Juliet’s question in Romeo and Juliet, a sharp debate broke out last week, in relation to the Government’s gas levy to help pay for the proposed LNG facility in New Plymouth. Is it a tax or “just” a levy? We can expect to see more of this verbal jousting in the months ahead of the election.

Last week, the Finance Minister Nicola Willis was one of the speakers at a two-day economic forum at Waikato University. Interestingly, she brought up the question of tax policy, which is often a matter that’s debated at tax conferences although usually it’s the Revenue Minister discussing the topic.

The Finance Minister hasn’t exactly gone outside her lane because tax is a key part of her portfolio, but it is unusual to see her discuss it publicly.

She noted “tax policy certainty needs to span successive governments.” And that’s very true. The issue she was driving was a hope that Labour would support the Investment Boost package that was renounced as part of last year’s budget.

Investment Boost is an interesting initiative, one of what we call accelerated depreciation, which the OECD suggests we should be doing if we want to boost productivity. It’s an interesting mix of reactions to it, mostly positive.

I’ve had clients who are in the business financing sector report that it hasn’t had the booster effect that they were expecting.

So anyway, the Finance Minister was saying she hopes that Labour in the interests of consistent tax policy would keep Investment Boost. That remains to be seen. It’s an election year and to possibly; to borrow a rugby phrase, she’s getting her retaliation in first.

A bank taxation review?

In her speech the Finance Minister also raised the question of whether the four main big Australian-owned banks are paying enough tax. This seems a classic example of Bettridge’s law of headlines, that is, any headline that ends in a question mark can be answered by the word no. There’s a great deal of commentary around how much tax is paid by the big four banks and whether it is appropriate. They seem to have higher margins than their Australian parents and a higher margin compared with many other countries.

Australian introduced its Major Bank Levy in 2017 and there has been a long-running bank levy in the UK. Infamously, as the Green Party pointed out, Margaret Thatcher introduced a bank levy on excessive profits in the early 1980s. Anyway what the Finance Minister has apparently put on the radar is some form of review of the tax treatment or what’s happening with the tax and the big four banks. It will be interesting to see what comes out of the review.

Budget date announced

Finally, this year’s Budget will be on Thursday 28th May, a little later than I anticipated. We’ve been told it won’t be a “lolly scramble”, but being an election year, I expect we may see some surprise announcements.

Meanwhile the main themes for the year are set, more Inland Revenue debt recovery and investigation activity, an international tax picture in flux and finally because of the forthcoming election we’re going to be hearing a lot about tax. Whatever eventuates we will keep you up to date with developments.

And on that note, that’s all for this week, I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

Earlier last year, Inland Revenue conducted a policy consultation on tax matters relating to charities and not-for-profit sector. At the time, there was a fair bit of speculation that there would be changes announced in the May budget in relation to the taxation of charities and in particular what was seen perceived to be the unfair tax advantage given to charities which owned businesses.

That actually didn’t play out, but instead Inland Revenue pushed forward with consultation on the taxation of mutual transactions of associations or not-for-profits, including clubs and societies. Behind the scenes it began targeted consultation in November with around 50 persons and organisations who had provided feedback on the previous consultations. This consultation covered donor-controlled charities, membership subscriptions, and other matters.

A Christmas surprise?

On 15th December, just before Christmas, Inland Revenue then released what it called a ‘Targeted policy consultation’. This explained what had happened in November and that it was now seeking more feedback because of wider public interest in the issue. The thing was, though, the initial deadline for submissions was 24th December. However, Inland Revenue added it would be prepared to extend this submission deadline on request, but it plans to review all submissions by late January.

The surprise part of the consultation is in relation to membership subscriptions and related matters. The consultation makes clear that membership subscriptions charged by tax-exempt not-for-profits, such as the 29,000 registered charities and 19,000 amateur sports clubs, are not taxable currently and will not be taxed under the proposals out for consultation.

Are membership subscriptions taxable?

But the question under consideration is around membership subscriptions for most not-for-profit organisations. Currently, the accepted treatment is that trading with members, such as conferences and sales of merchandise, are considered taxable income, but membership subscriptions were not as they were covered by the ‘mutuality principle’. However, Inland Revenue has drafted an operational statement “…indicating that it is likely to formally change its view and state that under current law many membership subscriptions would be taxable.” Needless to say, this would be an unwelcome surprise for quite a lot of groups. Although there may be a trade-off in that some other expenses which are currently not deductible may become deductible.

The consultation also suggests the current annual tax-free threshold of $1000 could be raised to $10,000. There are also suggestions to simplify the income tax filing requirements for taxable not-for-profits, but Inland Revenue also wants to require banks and other financial institutions to provide it with financial information for those not-for-profits who use the tax-free threshold.

This is a surprising and for many organisations unwelcome development estimated to raise perhaps $50 million annually. From what I’ve seen there’s no clear explanation given as to why Inland Revenue thinks the mutuality principle no longer applies in relation to the subscriptions. I imagine there will be quite some pushback on the membership subscription issue. It will be interesting to see how this plays out and what changes are announced in the 2026 Budget.

“Don’t look back in anger” – 2025 in review

Talking of Budgets, the 2025 budget on 22nd May contained a pleasant surprise with the announcement of the Investment Boost allowance. This enables businesses of any size to fully deduct 20% of the value of any new assets in the year of purchase. Interestingly, it also includes new commercial and industrial buildings and would also cover earthquake strengthening in some cases. Perhaps surprisingly, there was no cap put on the amount which could be claimed by a business.

The Investment Boost initiative is designed to boost investment and productivity, a theme in common with other tax initiatives, for example, proposals for digital nomads and changes to the Foreign Investment Fund regime included in the Taxation (Annual Rates for 2025−26, Compliance Simplification, and Remedial Measures) Bill currently before Parliament. It’s actually a on long-standing principle of our tax policy to enable investment in New Zealand and remove barriers to doing so.

The investment boost was a big surprise. Whether it’s had the hoped for impact is not clear yet. As everyone is well aware, economic activity was bumpy in 2025, but it could be that the groundwork has been laid for a stronger recovery this year.

Boosting Inland Revenue’s compliance activities

Another constant theme for the year, was more money in the 2025 Budget for Inland Revenue to boost its compliance activities. On top of the $116 million it was given over 4 years in the 2024 Budget it got another $35 million in the 2025 Budget. Consequently, 2025 saw great degree of investigative work by Inland Revenue. According to Inland Revenue’s 2025 Annual Report, it has achieved great returns from its increased compliance activities.

In addition to investigation and review work, Inland Revenue is also trying to close off what it considers loopholes and areas where there appears to be seepage in the tax system. The not-for-profits consultation we discussed earlier is one such example. However, arguably the biggest single example, and which was such a bolt from the blue, I called it a bombshell, was the recently announced consultation on the taxation of shareholder advances. It’s one of the most significant changes to the taxation of small businesses in recent years, potentially worth several hundred million of additional tax revenue annually. We’re therefore going to see a fair bit of lobbying and feedback about the proposals which are almost certain to be as part of the 2026 Budget and the annual tax bill. Watch that space.

Targeting crypto-assets

The taxation of crypt-assets is one specific area where Inland Revenue is currently very active. In November I discussed Technical Decision Summary TDS 25/23 where investors in crypto-assets lost the argument that gains were on capital account and therefore non-taxable. This case is probably the tip of the iceberg as according to Inland Revenue’s 2025 Annual Report “As at 30 June 2025, more than 150 customers were under review, with total tax at risk in the tens of millions.”

We’ll also see ongoing activity from Inland Revenue reviewing property transactions. Everyone tends to underestimate how much access to data Inland Revenue has and the information sharing which goes on with other Government agencies and tax authorities around the world. I’m sure I’m not the only tax agent seeing increasing numbers of inquiries from clients and Inland Revenue relating to investigations or reviews covering overseas income which may or may not have been declared properly.

Tax debt – a $9.3 billion problem

The other big area for Inland Revenue is managing the debt book, in late November I had a very interesting discussion with Tony Morris from Inland Revenue about how it is approaching the management of its debt book, which is over $9.3 billion and what steps are being taken to reduce this.

I’m seeing a much more forceful attitude from Inland Revenue around earlier interventions and debt collection. In some cases, that’s well merited. Other cases, I think it’s been a little ham-fisted. There’s also work to be done in managing companies which fall behind on GST and PAYE. Much earlier intervention is needed there. But one hopes that the extra money that Inland Revenue has received from the government will aid that. Getting the debt book under control is obviously very important for Inland Revenue and for the Government.

One area I think actually needs a fundamental redesign, is the question of student loans where only 30% of overseas-based debtors are making repayments at this point. Now, Inland Revenue does have the power in many double tax agreements to ask overseas authorities to intervene on its behalf, but it seems to have been a bit reluctant to do so. 2026 may see a change in this approach.

Overall, we can expect to see Inland Revenue gathering using all its available tools to collect the maximum amount of overdue debt and bring the debt book under control. That’s been a big theme in 2025 and it’s going to be a continuing theme this year.

The Trump effect

Internationally, the second Trump administration has caused all sorts of upheaval across the world order geopolitically, but also in the tax space where progress on the already grindingly slow Organisation for Economic Cooperation and Development/G20 multilateral tax proposals, the so-called Pillar 1 and Pillar 2 proposals, has basically ground to a halt.

The Trump administration made it clear early on it is hostile to what it considers unfair taxation and regulation. Its National Security Strategy released in November spelled it out bluntly.

(National Security Strategy of the United States of America, page 19)

Against this background it’s hardly surprising the Government in May decided to withdraw (“discharge”) the Digital Services Tax Bill.

Big Tech, Little Tax

The multilateral Pillar 1 and Pillar 2 deals seem dead in the water, but as the Tax Justice Aotearoa noted in their report, Big Tech, Little Tax that still leaves the problem of the tech companies’ apparently extensive use of transfer pricing methodologies to minimise their tax bills.

One of the examples the Tax Justice Aotearoa report considered was Oracle New Zealand, which according to its 2024 financials, earned revenue of $172.7 million, but paid licensing fees of $105.3 million to an Irish-related party company. It ultimately finished up with taxable income of just $5.3 million. It’s apparently paid royalties representing between one third and three-fifths of its total revenue. Oracle, incidentally, is currently undergoing an audit in Australia and there’s a related tax case going through the courts, which I expect Inland Revenue will be watching very closely.

And then there’s Microsoft, which earned revenue of $1.32 billion, but then paid over a billion dollars in purchases to another Irish located related party company.

The Digital Services Tax might have had some impact on this, but a more likely tool to try and recover additional tax would be to start applying non-resident withholding tax on the royalty element of any cross-border payment. The payments should remain deductible, but subject to a (typically) 5% withholding tax. Such an approach should be acceptable under most long-standing international agreements, but it will be interesting to see what pushback emerges if Inland Revenue adopts this approach.

Tax policy highlights the rising cost of demographic change

In the tax policy space in general, it’s been an interesting year with the Inland Revenue’s long-term insights briefing somewhat controversially looking at the question of the tax base. This was alongside Treasury’s He Tirohanga Mokopuna, statement on the long-term fiscal position which took a 40-year view of the Government’s fiscal position. A common theme was the demographic pressures on pension funding. Unsurprisingly that, together with the rising costs of climate change, was also a major theme the OECD’s review of tax policy in 2024.

Capital Gains Tax – a never-ending story?

The seemingly endless debate about capital gains tax continued through 2025. The International Monetary Fund paid its regular Article IV visit and suggested it might not be the worst thing in the world. The more interesting IMF report to me was about New Zealand productivity, where it directly suggested that the lack of a capital gains tax has meant excess capital has been gone into property rather than into productive investment, and it could be a factor in our low productivity. That’s not an unreasonable conclusion in my view.

Then we had the Labour Party finally announcing its somewhat limited capital gains tax proposal, which will apply to all residential investment and commercial property. That’s a little less bold than what Labour Party members wanted, but on the other hand is in line with our practice of incremental changes. It’s also pretty much in line with what the minority group on the last tax working group suggested, a comprehensive capital gains tax wasn’t needed, but expanding it into the taxation of residential property was certainly recommended.

The Tax Policy Charitable Trust brought down former IMF Deputy Director Professor Michael (Mick) Keane for a couple of lectures, one of which was in Wellington at Treasury. He made the interesting observation that most tax jurisdictions which do have a capital gains tax, and remember we’re in the minority, approach it from the basis that everything is in unless it’s out. Presently, our approach is the flip side, everything is out unless it’s in but the problem is there’s a lot more in than people realise and so there’s seepage of potential review. In terms of conceptuality, I think his approach is to be preferred. Include everything and then carve out exemptions (such as the family home). That is what we see around the world as he noted.

Looking ahead as always, there will be a huge debate going on around what are the best tax settings for New Zealand as we head into the second half of this decade. With 2026 being an election year, we’re going to hear a lot about capital gains tax. I’m afraid non-tax geeks will probably be heartily sick of it by the end of the year.

Thank you

Finally, I’ve been very fortunate with the guests I’ve had this year, so thank you all, you’ve been most interesting and generous with your time. A special shout-out to Tony Morris of Inland Revenue for a fascinating discussion on where Inland Revenue is working in the debt space. (Transcript coming soon).

And on that note, that’s all for 2025, we’ll be back in late January to cover all the latest developments in tax as always. I’m Terry Baucher and thank you for reading and commenting. Please send me your feedback and requests for topics or guests. In the meantime, best wishes for 2026!

It’s not often in tax that you can genuinely say a bombshell has dropped, but last Thursday at 4:00pm Inland Revenue released one such bombshell for consultation, the somewhat innocuous sounding Improving taxation of loans made by companies to shareholders. “Improving” is doing a lot of heavy lifting there.

The basic position is Inland Revenue plans to completely change the current tax treatment because, as a handy information sheet released alongside the main issues paper points out:

Our current rules mean shareholders who borrow from their company can pay less tax compared with other taxpayers who are fully taxed on their salary, wages and dividends or profits they earn as a sole trader or partnership.

The problem

The current position is this; if a shareholder borrows money from a company, it’s not treated as a dividend or income but is subject to interest. The company can either charge interest at an agreed market rate, or if the loan (or shareholder current account) is either below market rate or is interest free, the company is liable to pay interest calculated using the fringe benefit tax prescribed rate of interest, currently 6.67%.

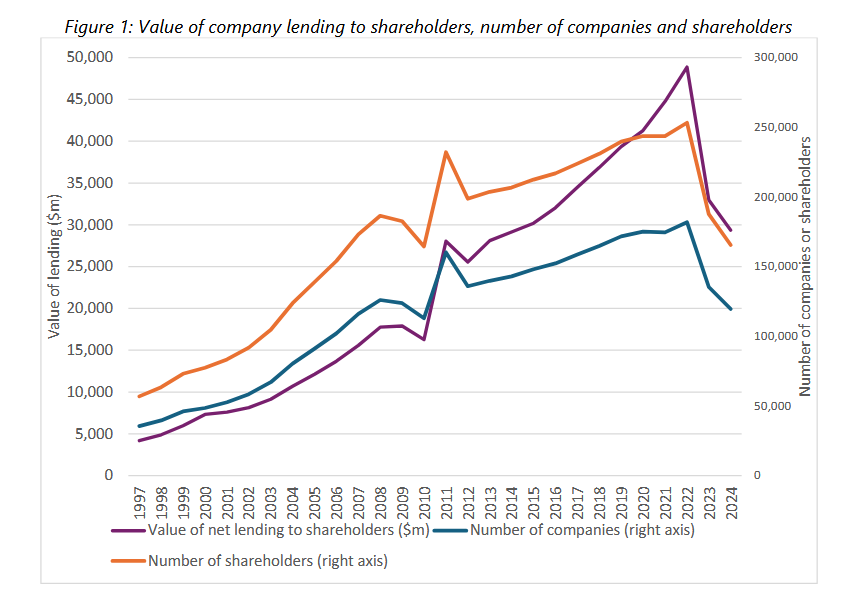

What has happened is that the amount owed by shareholders has built up over time, and the numbers are quite surprising. According to chapter 3 of the issues paper – paragraph 3.3 onwards – for the year ended 31 March 2024, approximately 119,000 companies (that’s about 16% of the 730,000 total companies in New Zealand) were owed a total of nearly $29 billion by about 165,000 shareholders who are either natural persons or trustees. As the paper notes:

For context, these companies reported $8 billion of taxable income in that same period, so the loan balances were over 3.5 times their annual income.

The average amount loaned by these companies to the shareholders was over $245,000 per company, or over $177,000 per shareholders.

A $19 billion impact of the increase in the trustee tax rate?

In fact, the amounts owed were even larger. According to Inland Revenue the amount of shareholder loans made to natural person and trustee shareholders peaked in the year end 31 March 2022, when about 182,000 companies recorded loans totalling $48.8 billion. The drop in nearly $19 billion between 2022 and 2024 appears mainly due to the increase in the trustee tax rate to 39% from 1st April 2024. Companies took the opportunity to pay dividends to trustee shareholders prior to the increase in the tax rate.

Large numbers are involved here.

A $12 billion problem

The sheer volume of the loans is staggering. If you want to get an idea of how big a potential loss of revenue the present rules represent, if the total of outstanding loans at 31st March 2024 had instead represented income paid to a shareholder or a shareholder employee (that is, someone who’s an employee and a shareholder in the company) and had been taxed at the highest marginal rate of 39%, about $12 billion of tax would have been payable.

A long-standing and fast-growing problem

The volume of outstanding shareholder loans is a considerable headache that has built up over time. Paragraph 3.7 of the paper notes that the annual growth in loans to shareholders has been approximately 8.7% per annum over the period 1997 to 2023. That surpasses the average growth in economic activity over the same period when nominal GDP growth on average was 5.4% per annum.

So which companies are lending?

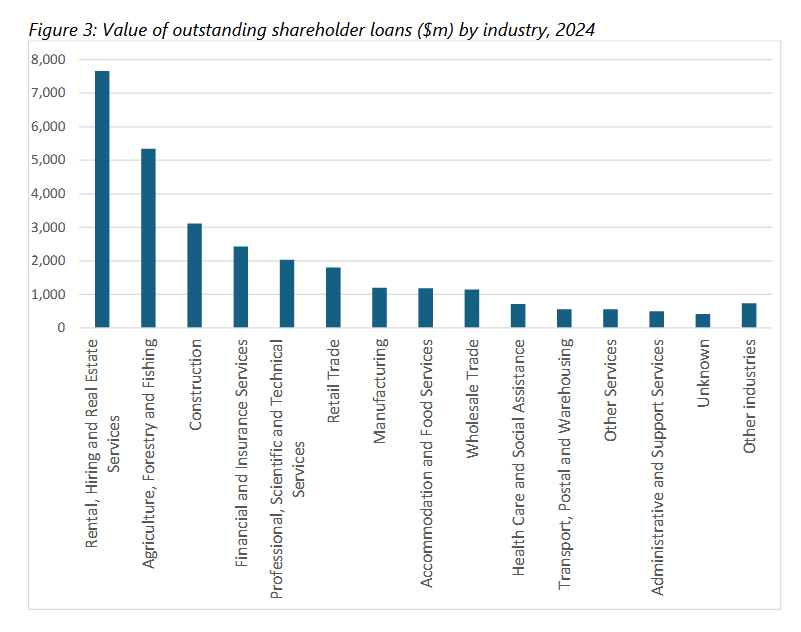

There’s an interesting analysis of what type of companies have been doing the lending. The biggest single group is the rental, hiring and real estate services sector who are responsible for about $7.5 billion of of that $29 billion. Then they’re closely followed by agriculture, forestry and fishing, which is about $5.2 billion, and then construction, which is just over $3.1 billion. These three sectors between them have nearly 55% of all total borrowing outstanding at 31st of March 2024.

Liquidations and other removals

There’s also another group of companies which I think would be of extremely great concern to Inland Revenue, and that’s companies with outstanding shareholder loans that have been liquidated or otherwise removed from the Companies Register.

Inland Revenue has analysed the approximately 184,000 such companies that were removed from the Companies Register between 1st April 2019 through to early 2025. The data suggests about 27,000 of those companies, nearly 15%, were owed money by their shareholders at the time they were removed based on the assumption that the shareholders at the time of removal were either individuals or trustees. In total those companies were owed approximately $2.3 billion, or about $85,000 per company. Further analysis shows about 15,000 of that group that were removed, were just simply struck off because they hadn’t filed their annual returns. This group was owed nearly $935 million or $55,000 per company.

Another 10,000 companies with shareholder loans went through the formal request for removal process. At the time of formal removal this group was owed $923 million or $92,300 per company.

Finally, 2,000 of companies with shareholder advances were put into liquidation process, and they owed over $426 million or $213,000 per company. For this group it’s quite possible the liquidator would have attempted to make a claim against shareholders with debts.

This group is of particular interest to Inland Revenue because it’s reasonably likely they had outstanding GST and PAYE debts. The shareholders in this group probably drew out loans for personal use which were effectively not taxed but the company later was liquidated owing GST and PAYE.

Bringing New Zealand into line with other countries

Inland Revenue’s main proposal is that as of 4th December, when the paper was released, if a shareholder loan has not been repaid within a set period, any outstanding balance above a threshold at the end of that period will be treated as a dividend and taxed accordingly. The repayment period will probably be 12 months which is the maximum time allowed for filing the company’s tax return if it is linked to a tax agent. The suggested threshold is $50,000, subject to consultation. With some reservations, Inland Revenue would permit imputation credits to be attached to any dividends deemed to arise under the proposal.

As the paper notes this change would bring New Zealand into line with most of our comparable jurisdictions. If you look at the treatment of shareholder advances across Canada, Australia, the UK and Norway, all take the approach that shareholder advances will be treated as income unless they’re repaid within a certain period. Inland Revenue’s proposed regime would be closest to that of Canada.

This proposal represents a huge change and one which is likely to have significant revenue effect. Exactly how much isn’t specified. At a guess it’s probably going to run to hundreds of millions, perhaps. It will be interesting to see exactly what happens because there’s going to be a displacement activity. Companies will either start paying out higher dividends or increased salaries to avoid the charge. Either way the Government’s tax take will increase.

Not yet enacted but effectively in force

It’s important to remember that Inland Revenue is open to consultation on its proposal so there’s going to be some fine tuning. Whatever the final form agreed, it will apply to all loans to shareholders made on or after 4th December. In other words, although the legislation is not yet in place, it is now in force. Accordingly, I recommend companies should create new accounting ledgers to record all activity from 4th December 2025 separately from any existing shareholder loans as only “new” loans will be subject to the new rules.

What about existing loans?

Inland Revenue proposes the outstanding loan balances, an estimated $29 billion as of 31st March 2024, will not be required to be repaid. This is a pretty good outcome because requiring loan repayments would be a huge shock to the economy particularly for small and medium enterprises, where shareholder advances are commonly in place.

Treatment of capital gains

Shareholder advances often arise after a company realises a substantial capital gain and shareholders therefore want to access the proceeds. I’ve seen examples where the shareholders have withdrawn the tax-free gains from the sale of an investment property for example often before the accountant even knows what’s going on. (This probably explains why the rental, hiring and real estate services sector has such a large amount of shareholder advances).

The problem is that capital gains even if they are tax-free, can only be distributed when the company is being liquidated. It may be interesting to see if Inland Revenue decides to allow some leniency in calculation of the loans for such advances on the basis that they would not be taxable if those gains had arisen in the hands of the shareholders directly. Inland Revenue’s starting position is that it “does not consider that an exception should be included for loans funded out of capital gain amounts” but it’s open to submissions on this point.

Treatment of shareholder loans on company’s cessation

In relation to companies which are removed from the Companies Register with outstanding loans to shareholders, the paper proposes that the amount of the outstanding loan is deemed to be income of the borrower. This will apply regardless of the reason for removal from the Companies Register. It would therefore apply if the company is struck off for not filing its annual Companies Office return (a fairly frequent event).

Furthermore, this measure would also apply from 4th December 2025. This is considered “necessary to minimise integrity concerns and structuring opportunities that could otherwise arise.” Although any legislation would effectively be retrospective Inland Revenue notes the proposal “does not result in an amount being subject to tax that would not be income under the current law.” It’s very hard to disagree with this proposal, given that some companies may have accumulated PAYE and GST debts.

Time for a closer look? When 5% of companies are owed 55% of all debt

A group of companies which might find themselves under future scrutiny are those that have substantial amounts of loans. This is arguably one of the most interesting and perhaps surprising part of the paper. According to Inland Revenue there were about 5,500 companies that had outstanding loan balances of more than $1million. Approximately 55% of the total value of outstanding loans, or nearly $16 billion was owed to those companies. In sum 5% of all companies with shareholder advances were owed 55% of the total outstanding debt.

Then within that group, there’s 540 companies that had outstanding loan balances of more than $5 million. In fact, that group alone had 22% of the value of all shareholder loans, roughly about $7 billion, even though they represented just 0.5% of all companies.

The present proposal is that there will be no requirement to repay those loans. However, I still think that Inland Review might take a closer look as to exactly what’s going on with these companies because, as the paper notes, there does seem to have been some substitution of loans for income using the prescribed rate of interest rules to sort of bypass or to minimise the tax payable on the withdrawals.

Incidentally, there was a proposal in a draft I saw that the prescribed rate of interest, currently 6.67%, would be increased substantially to nearer credit card rates, i.e. nearly 20%. That has been dropped presumably after a fair amount of pushback.

A significant but logical change

In conclusion these proposals will significantly impact the small-medium enterprise sector. As Bernard Hickey pointed out, when we discussed the proposals on the Hoon just after the paper’s release, this group is very much part of the Government’s current voting base. It will therefore be interesting to see what happens during consultation.

The Organisation for Economic Cooperation and Development (OECD)had a paper in 2024 which looked at the question of small/medium enterprises and tax arbitrage in the sector. The proposals represent a significant change. But they are also logical when you look at what happens in comparative countries.

As previously noted affected companies need to take action now because whatever the final shape or form of the proposal comes out, it’s effective from 4th December. The paper’s open for consultation until 5th February. Sharpen up your pens and get your thinking caps on as to how you see this will work and what you want to see in terms of repayment period and a threshold. Inland Revenue has proposed $50,000, but they may be open to suggestions on that.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue’s updated draft interpretation statement on the deductibility of repairs and maintenance expenditure has a controversial take on the treatment of leaky buildings.

Under the Generic Tax Policy Process (“GTPP”) “Inland Revenue is primarily responsible for the detailed design, implementation and review of tax policy.” As part of the GTPP Inland Revenue in conjunction with the Minister of Revenue will periodically release Work Programmes reflecting the Government’s current priorities.

The latest, or “refreshed” Work Programme as the Minister of Revenue Simon Watts put it, was released on 29th October. According to the Minister “The refreshed work programme is about removing regulatory barriers and delivering a stable, predictable tax environment that directly supports growth and opportunity.”

Four key workstreams

There are four workstreams in the Work Programme:

Attracting and retaining capital and talent to make New Zealand a better place to invest capital, work and do business. The intention here is to minimise biases on economic decisions, reduce international tax barriers and rewarding effort and individuals’ investment in their own skills.

Supporting small businesses, primarily by reducing compliance costs and making tax treatment simpler and fairer.

Simplification and integrity of the tax system, again by reducing compliance costs across the board for all taxpayers but also protecting “against tax avoidance and evasion to maintain a simple, stable and predictable tax system.” Simplification is the easier part the harder part is making sure that the system operates as is intended and that taxpayers are compliant and are seen to be compliant.

Finally, improve social policy which is described as “improving the delivery of income support payments administered through the tax system and increasing work incentives.” I have some doubts about how some of the other initiatives we’ve recently seen will actually work.

Remedial legislation

In addition, as the two-page summary of the Work Programme notes, “the remedial programme plays an important part in maintaining the tax system.” The current tax bill going through Parliament contains 43 remedial amendments covering matters such as investment boost, employee share schemes, GST, FBT and KiwiSaver, as well as what’s called termed a further 24 maintenance amendments. (Worth remembering further items may be added as the Bill progresses. Although submissions on the Bill have closed, it is possible for the government to introduce further provisions to an existing tax Bill.

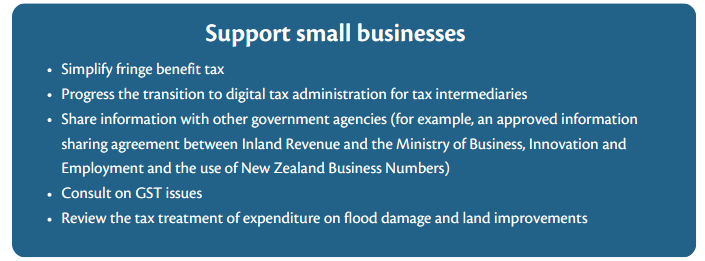

Supporting small businesses

There’s nothing terribly unusual in the Work Programme, quite a bit of which is in the current tax bill going through Parliament. In the small business workstream it’s interesting to see simplifying fringe benefit tax listed, as that got kicked down the road. Sharing information with other government agencies is one of the more controversial measures in the Bill but it’s good to see proposals to consult on GST issues and review the tax treatment of expenditure and flood damage and land improvements.

Revising provisional tax for small businesses?

But I was intrigued to see the Minister of Revenue in the accompanying press release make the following comment.

“We are also working with intermediaries to reduce compliance costs and make tax treatment simpler and fairer. Inland Revenue is currently exploring a more flexible approach to income tax payments for sole traders and small businesses and plans to consult on this on the first part of next year.”

That’s actually good to hear because I think it’s time for a thorough review of the provisional tax system, which is not terribly friendly towards small businesses in my view. Currently, for taxpayers with the standard 31st March year-end payments are due on 28th August, 15th January and 7th May. The 15th January payment falls at a particularly awkward time for small businesses because many are on holiday at that time.

(The current timing of provisional tax payments was largely for the convenience of larger companies, many of which do not have a 31 March balance date so do not face this issue. I still find it astonishing that in a country where 96% of businesses are small businesses, landing a major tax payment in the middle of the summer holidays seems quite bizarre.)

Anyway, according to the Minister, we’re going to see something in this area in the New Year which I fully welcome.

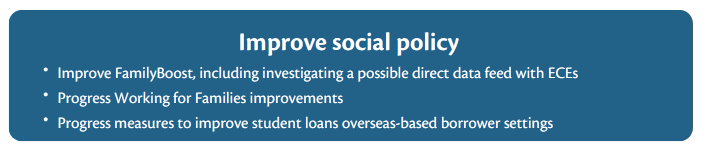

Changes to FamilyBoost but no review of abatement thresholds and rates?

In relation to the social policy initiatives, in here they’re talking about improving FamilyBoost, including investigating a possible direct data feed with early childhood education centres.

In terms of improving Working for Families it’s not clear what’s involved but I consider a real look at the thresholds and abatements is really critical here. As a Treasury paper earlier this year noted, 30% of solo parent families have an effective marginal tax rate of above 50%. We also have the proposals to remove Jobseeker benefit for 18- and 19-year-olds living at home where the annual family income exceeds $65,529. This move if implemented would result in an effective marginal tax rate of over 1.34 million percent, a very clear disincentive to work.

So there’s lots of work to be done in the social policy space in my view. It will be interesting to see what emerges over time and of course, we’ll bring you those developments in due course.

Are repairs to leaky buildings deductible?

Moving on, as we recently discussed with John Cuthbertson of Chartered Accounts Australia and New Zealand, Inland Revenue’s Tax Counsel Office regularly releases draft guidance for consultation about particular aspects of the tax system. As John explained a major part of his team’s role is reviewing and responding to these draft guidance releases.

I expect he and his team are going to pay particular attention to the draft interpretation statement on the income tax deductibility of repairs and maintenance expenditure. Now, this is updating the Commissioner’s guidance from 2012 on the topic Interpretation Statement IS 12/03 which is widely used and often referenced in other guidance.

All or nothing, the impact of withdrawing depreciation for buildings

As the draft guidance notes, since depreciation is no longer allowed for buildings, it is now more important to correctly characterise repairs and maintenance expenditure. The withdrawal of depreciation means repair and maintenance expenditure is a bit of an all or nothing matter. It’s either going to be deductible or it’s not deductible and there’s no depreciation either, so the stakes are higher.

According to the introduction, the Commissioner’s interpretation has not changed since 2012, and this guidance has been updated to reflect recent legal developments, improve clarity and reflect a more modern format. The full interpretation statement itself runs to 81 pages but there’s also a handy summary fact sheet which at seven pages, is a lot more digestible.

What about leaky buildings?

Despite the Commissioner not changing his interpretation, one of the areas I think is going to provoke some controversy is in relation to the treatment of leaky buildings. To be fair, this is a complicated area, and enormous amounts have been spent in dealing with remediating leaky buildings since the crisis first emerged in the 1990s. I think it would have been better for Inland Revenue to have issued separate guidance on the treatment of leaky buildings expenditure because the numbers are very big.

It’s worth citing out at length what Inland Revenue says about the issue, because it’s sure to provoke controversy. Paragraph 193 of the guidance starts,

“Inherent defects are faults in an asset’s design, construction or manufacture that can subsequently cause a need for work to be carried out on the asset. This may be because the defect requires routine maintenance and repair work to be brought forward or because it results in additional required work or both. In New Zealand, an example of inherent defects in a repairs and maintenance context involves properties that have been referred to as called leaky buildings or leaky homes.”

It’s the next paragraph [194], which is the kicker as far as I’m concerned. It reads,

“As noted at paragraphs 100 to 102, the courts have considered a repair involves the restoration of a thing to a condition it formerly had without changing its character.

[So far, so uncontroversial].

In the case of leaky buildings, this raises the question of what is the asset’s relevant former condition. In the Commissioner’s view, this is likely to be the “as constructed” condition of the building, including the inherent defects in that construction. Therefore, works to remediate damage caused by the inherent defects that goes beyond restoring this original condition may not involve repairs if the building is improved or enhanced by removing the inherent defects. In that case, the nature of the work undertaken is more likely to be considered an improvement, the costs of which involve capital expenditure.” [my emphasis]

Paragraph 195 continues in the same vein.

“With leaky buildings, an improvement is highly likely to incur. The removal of an inherent defect is likely to be a legal requirement imposed on work done to remediate damage in a leaky building so it meets current building standards. It is also likely that work required involves replacing original materials used in constructing significant and integral parts of the building with superior materials.”

That’s a hell of a couple of paragraphs in my view, because this interpretation would appear to rule out claiming deductions for large portions of any expenditure on leaky buildings and remediation.

I see where Inland Revenue are going with this, but a counter argument is that the building was built or purchased to be used as a building, and it was unfit for purpose in the first place. How is it an improvement to make it fit for purpose, because, basically, properly constructed buildings shouldn’t leak in the first place? That’s perhaps oversimplifying the argument, but Inland Revenue have adopted an unduly strict interpretation which is not likely to be welcomed.

As I said, you can see where Inland Revenue are coming from, but you can also see that investors have a building that’s not fit for purpose and requires remedial expenditure. In some cases, they are able to continue to use the building at some reduced capacity. But based on this draft guidance they are unable to get a deduction for those repairs to get it to the standard to which it originally should have been at all times. Furthermore, because depreciation is no longer available for commercial buildings, this becomes an all or nothing issue.

As an aside its’s quite possible that the original builders or constructors of these defective buildings will face lawsuits and they may be to pay compensation or carry out remedial work in which case the building owner is not out of pocket. However, many leaky building owners face the problem of having to expend a substantial amount of expenditure, not get a deduction for it and not be able to claim depreciation. I therefore foresee quite a bit of pushback on this guidance.

We’ll have to wait and see for developments. Notwithstanding that, I also think this is perhaps such a vital matter it should be left to Parliament to determine the appropriate treatment. Watch this space.

[This is an edited transcript of the episode released on 3rd November 2025]

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.