It’s not often in tax that you can genuinely say a bombshell has dropped, but last Thursday at 4:00pm Inland Revenue released one such bombshell for consultation, the somewhat innocuous sounding Improving taxation of loans made by companies to shareholders. “Improving” is doing a lot of heavy lifting there.

The basic position is Inland Revenue plans to completely change the current tax treatment because, as a handy information sheet released alongside the main issues paper points out:

Our current rules mean shareholders who borrow from their company can pay less tax compared with other taxpayers who are fully taxed on their salary, wages and dividends or profits they earn as a sole trader or partnership.

The problem

The current position is this; if a shareholder borrows money from a company, it’s not treated as a dividend or income but is subject to interest. The company can either charge interest at an agreed market rate, or if the loan (or shareholder current account) is either below market rate or is interest free, the company is liable to pay interest calculated using the fringe benefit tax prescribed rate of interest, currently 6.67%.

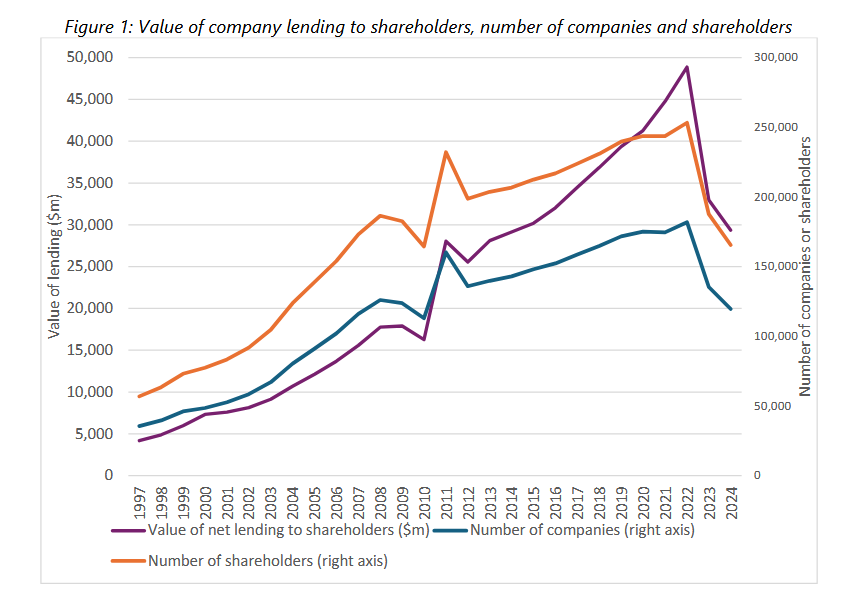

What has happened is that the amount owed by shareholders has built up over time, and the numbers are quite surprising. According to chapter 3 of the issues paper – paragraph 3.3 onwards – for the year ended 31 March 2024, approximately 119,000 companies (that’s about 16% of the 730,000 total companies in New Zealand) were owed a total of nearly $29 billion by about 165,000 shareholders who are either natural persons or trustees. As the paper notes:

For context, these companies reported $8 billion of taxable income in that same period, so the loan balances were over 3.5 times their annual income.

The average amount loaned by these companies to the shareholders was over $245,000 per company, or over $177,000 per shareholders.

A $19 billion impact of the increase in the trustee tax rate?

In fact, the amounts owed were even larger. According to Inland Revenue the amount of shareholder loans made to natural person and trustee shareholders peaked in the year end 31 March 2022, when about 182,000 companies recorded loans totalling $48.8 billion. The drop in nearly $19 billion between 2022 and 2024 appears mainly due to the increase in the trustee tax rate to 39% from 1st April 2024. Companies took the opportunity to pay dividends to trustee shareholders prior to the increase in the tax rate.

Large numbers are involved here.

A $12 billion problem

The sheer volume of the loans is staggering. If you want to get an idea of how big a potential loss of revenue the present rules represent, if the total of outstanding loans at 31st March 2024 had instead represented income paid to a shareholder or a shareholder employee (that is, someone who’s an employee and a shareholder in the company) and had been taxed at the highest marginal rate of 39%, about $12 billion of tax would have been payable.

A long-standing and fast-growing problem

The volume of outstanding shareholder loans is a considerable headache that has built up over time. Paragraph 3.7 of the paper notes that the annual growth in loans to shareholders has been approximately 8.7% per annum over the period 1997 to 2023. That surpasses the average growth in economic activity over the same period when nominal GDP growth on average was 5.4% per annum.

So which companies are lending?

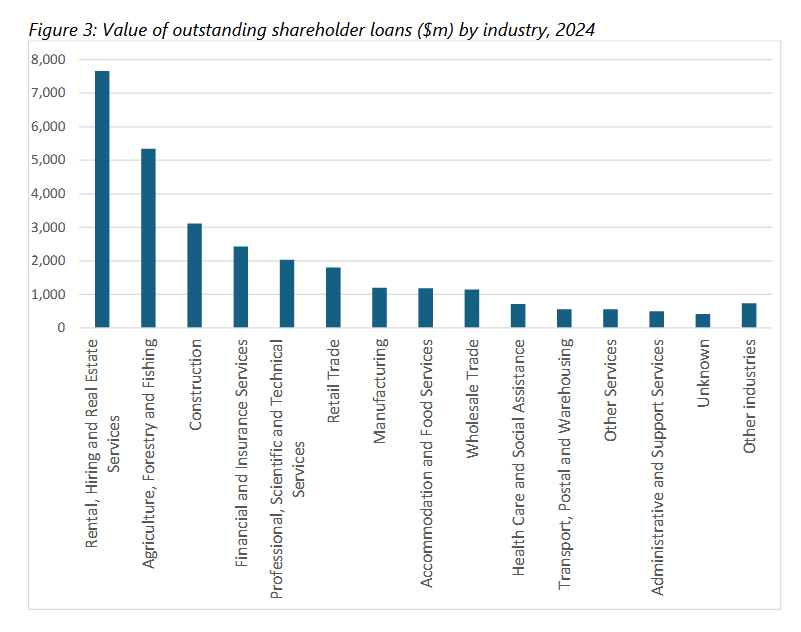

There’s an interesting analysis of what type of companies have been doing the lending. The biggest single group is the rental, hiring and real estate services sector who are responsible for about $7.5 billion of of that $29 billion. Then they’re closely followed by agriculture, forestry and fishing, which is about $5.2 billion, and then construction, which is just over $3.1 billion. These three sectors between them have nearly 55% of all total borrowing outstanding at 31st of March 2024.

Liquidations and other removals

There’s also another group of companies which I think would be of extremely great concern to Inland Revenue, and that’s companies with outstanding shareholder loans that have been liquidated or otherwise removed from the Companies Register.

Inland Revenue has analysed the approximately 184,000 such companies that were removed from the Companies Register between 1st April 2019 through to early 2025. The data suggests about 27,000 of those companies, nearly 15%, were owed money by their shareholders at the time they were removed based on the assumption that the shareholders at the time of removal were either individuals or trustees. In total those companies were owed approximately $2.3 billion, or about $85,000 per company. Further analysis shows about 15,000 of that group that were removed, were just simply struck off because they hadn’t filed their annual returns. This group was owed nearly $935 million or $55,000 per company.

Another 10,000 companies with shareholder loans went through the formal request for removal process. At the time of formal removal this group was owed $923 million or $92,300 per company.

Finally, 2,000 of companies with shareholder advances were put into liquidation process, and they owed over $426 million or $213,000 per company. For this group it’s quite possible the liquidator would have attempted to make a claim against shareholders with debts.

This group is of particular interest to Inland Revenue because it’s reasonably likely they had outstanding GST and PAYE debts. The shareholders in this group probably drew out loans for personal use which were effectively not taxed but the company later was liquidated owing GST and PAYE.

Bringing New Zealand into line with other countries

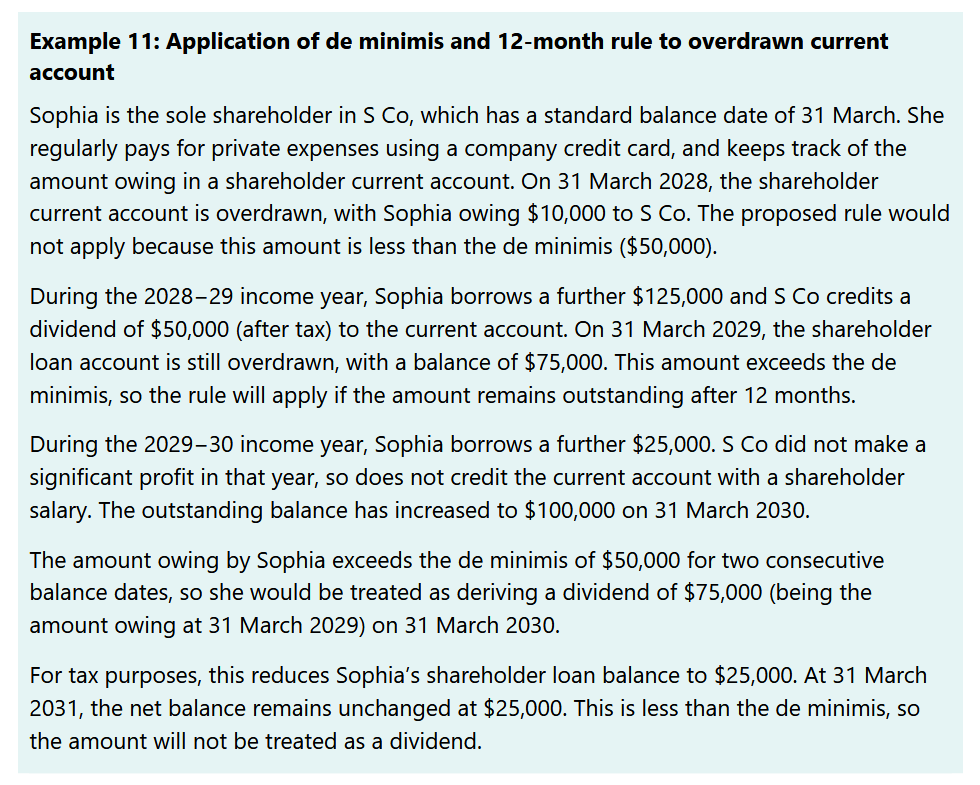

Inland Revenue’s main proposal is that as of 4th December, when the paper was released, if a shareholder loan has not been repaid within a set period, any outstanding balance above a threshold at the end of that period will be treated as a dividend and taxed accordingly. The repayment period will probably be 12 months which is the maximum time allowed for filing the company’s tax return if it is linked to a tax agent. The suggested threshold is $50,000, subject to consultation. With some reservations, Inland Revenue would permit imputation credits to be attached to any dividends deemed to arise under the proposal.

As the paper notes this change would bring New Zealand into line with most of our comparable jurisdictions. If you look at the treatment of shareholder advances across Canada, Australia, the UK and Norway, all take the approach that shareholder advances will be treated as income unless they’re repaid within a certain period. Inland Revenue’s proposed regime would be closest to that of Canada.

This proposal represents a huge change and one which is likely to have significant revenue effect. Exactly how much isn’t specified. At a guess it’s probably going to run to hundreds of millions, perhaps. It will be interesting to see exactly what happens because there’s going to be a displacement activity. Companies will either start paying out higher dividends or increased salaries to avoid the charge. Either way the Government’s tax take will increase.

Not yet enacted but effectively in force

It’s important to remember that Inland Revenue is open to consultation on its proposal so there’s going to be some fine tuning. Whatever the final form agreed, it will apply to all loans to shareholders made on or after 4th December. In other words, although the legislation is not yet in place, it is now in force. Accordingly, I recommend companies should create new accounting ledgers to record all activity from 4th December 2025 separately from any existing shareholder loans as only “new” loans will be subject to the new rules.

What about existing loans?

Inland Revenue proposes the outstanding loan balances, an estimated $29 billion as of 31st March 2024, will not be required to be repaid. This is a pretty good outcome because requiring loan repayments would be a huge shock to the economy particularly for small and medium enterprises, where shareholder advances are commonly in place.

Treatment of capital gains

Shareholder advances often arise after a company realises a substantial capital gain and shareholders therefore want to access the proceeds. I’ve seen examples where the shareholders have withdrawn the tax-free gains from the sale of an investment property for example often before the accountant even knows what’s going on. (This probably explains why the rental, hiring and real estate services sector has such a large amount of shareholder advances).

The problem is that capital gains even if they are tax-free, can only be distributed when the company is being liquidated. It may be interesting to see if Inland Revenue decides to allow some leniency in calculation of the loans for such advances on the basis that they would not be taxable if those gains had arisen in the hands of the shareholders directly. Inland Revenue’s starting position is that it “does not consider that an exception should be included for loans funded out of capital gain amounts” but it’s open to submissions on this point.

Treatment of shareholder loans on company’s cessation

In relation to companies which are removed from the Companies Register with outstanding loans to shareholders, the paper proposes that the amount of the outstanding loan is deemed to be income of the borrower. This will apply regardless of the reason for removal from the Companies Register. It would therefore apply if the company is struck off for not filing its annual Companies Office return (a fairly frequent event).

Furthermore, this measure would also apply from 4th December 2025. This is considered “necessary to minimise integrity concerns and structuring opportunities that could otherwise arise.” Although any legislation would effectively be retrospective Inland Revenue notes the proposal “does not result in an amount being subject to tax that would not be income under the current law.” It’s very hard to disagree with this proposal, given that some companies may have accumulated PAYE and GST debts.

Time for a closer look? When 5% of companies are owed 55% of all debt

A group of companies which might find themselves under future scrutiny are those that have substantial amounts of loans. This is arguably one of the most interesting and perhaps surprising part of the paper. According to Inland Revenue there were about 5,500 companies that had outstanding loan balances of more than $1million. Approximately 55% of the total value of outstanding loans, or nearly $16 billion was owed to those companies. In sum 5% of all companies with shareholder advances were owed 55% of the total outstanding debt.

Then within that group, there’s 540 companies that had outstanding loan balances of more than $5 million. In fact, that group alone had 22% of the value of all shareholder loans, roughly about $7 billion, even though they represented just 0.5% of all companies.

The present proposal is that there will be no requirement to repay those loans. However, I still think that Inland Review might take a closer look as to exactly what’s going on with these companies because, as the paper notes, there does seem to have been some substitution of loans for income using the prescribed rate of interest rules to sort of bypass or to minimise the tax payable on the withdrawals.

Incidentally, there was a proposal in a draft I saw that the prescribed rate of interest, currently 6.67%, would be increased substantially to nearer credit card rates, i.e. nearly 20%. That has been dropped presumably after a fair amount of pushback.

A significant but logical change

In conclusion these proposals will significantly impact the small-medium enterprise sector. As Bernard Hickey pointed out, when we discussed the proposals on the Hoon just after the paper’s release, this group is very much part of the Government’s current voting base. It will therefore be interesting to see what happens during consultation.

The Organisation for Economic Cooperation and Development (OECD)had a paper in 2024 which looked at the question of small/medium enterprises and tax arbitrage in the sector. The proposals represent a significant change. But they are also logical when you look at what happens in comparative countries.

As previously noted affected companies need to take action now because whatever the final shape or form of the proposal comes out, it’s effective from 4th December. The paper’s open for consultation until 5th February. Sharpen up your pens and get your thinking caps on as to how you see this will work and what you want to see in terms of repayment period and a threshold. Inland Revenue has proposed $50,000, but they may be open to suggestions on that.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue’s updated draft interpretation statement on the deductibility of repairs and maintenance expenditure has a controversial take on the treatment of leaky buildings.

Under the Generic Tax Policy Process (“GTPP”) “Inland Revenue is primarily responsible for the detailed design, implementation and review of tax policy.” As part of the GTPP Inland Revenue in conjunction with the Minister of Revenue will periodically release Work Programmes reflecting the Government’s current priorities.

The latest, or “refreshed” Work Programme as the Minister of Revenue Simon Watts put it, was released on 29th October. According to the Minister “The refreshed work programme is about removing regulatory barriers and delivering a stable, predictable tax environment that directly supports growth and opportunity.”

Four key workstreams

There are four workstreams in the Work Programme:

Attracting and retaining capital and talent to make New Zealand a better place to invest capital, work and do business. The intention here is to minimise biases on economic decisions, reduce international tax barriers and rewarding effort and individuals’ investment in their own skills.

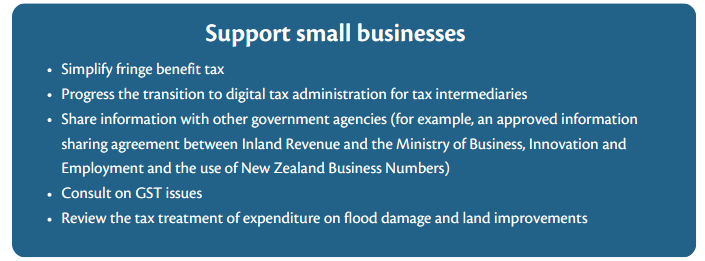

Supporting small businesses, primarily by reducing compliance costs and making tax treatment simpler and fairer.

Simplification and integrity of the tax system, again by reducing compliance costs across the board for all taxpayers but also protecting “against tax avoidance and evasion to maintain a simple, stable and predictable tax system.” Simplification is the easier part the harder part is making sure that the system operates as is intended and that taxpayers are compliant and are seen to be compliant.

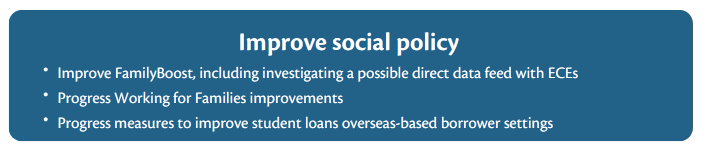

Finally, improve social policy which is described as “improving the delivery of income support payments administered through the tax system and increasing work incentives.” I have some doubts about how some of the other initiatives we’ve recently seen will actually work.

Remedial legislation

In addition, as the two-page summary of the Work Programme notes, “the remedial programme plays an important part in maintaining the tax system.” The current tax bill going through Parliament contains 43 remedial amendments covering matters such as investment boost, employee share schemes, GST, FBT and KiwiSaver, as well as what’s called termed a further 24 maintenance amendments. (Worth remembering further items may be added as the Bill progresses. Although submissions on the Bill have closed, it is possible for the government to introduce further provisions to an existing tax Bill.

Supporting small businesses

There’s nothing terribly unusual in the Work Programme, quite a bit of which is in the current tax bill going through Parliament. In the small business workstream it’s interesting to see simplifying fringe benefit tax listed, as that got kicked down the road. Sharing information with other government agencies is one of the more controversial measures in the Bill but it’s good to see proposals to consult on GST issues and review the tax treatment of expenditure and flood damage and land improvements.

Revising provisional tax for small businesses?

But I was intrigued to see the Minister of Revenue in the accompanying press release make the following comment.

“We are also working with intermediaries to reduce compliance costs and make tax treatment simpler and fairer. Inland Revenue is currently exploring a more flexible approach to income tax payments for sole traders and small businesses and plans to consult on this on the first part of next year.”

That’s actually good to hear because I think it’s time for a thorough review of the provisional tax system, which is not terribly friendly towards small businesses in my view. Currently, for taxpayers with the standard 31st March year-end payments are due on 28th August, 15th January and 7th May. The 15th January payment falls at a particularly awkward time for small businesses because many are on holiday at that time.

(The current timing of provisional tax payments was largely for the convenience of larger companies, many of which do not have a 31 March balance date so do not face this issue. I still find it astonishing that in a country where 96% of businesses are small businesses, landing a major tax payment in the middle of the summer holidays seems quite bizarre.)

Anyway, according to the Minister, we’re going to see something in this area in the New Year which I fully welcome.

Changes to FamilyBoost but no review of abatement thresholds and rates?

In relation to the social policy initiatives, in here they’re talking about improving FamilyBoost, including investigating a possible direct data feed with early childhood education centres.

In terms of improving Working for Families it’s not clear what’s involved but I consider a real look at the thresholds and abatements is really critical here. As a Treasury paper earlier this year noted, 30% of solo parent families have an effective marginal tax rate of above 50%. We also have the proposals to remove Jobseeker benefit for 18- and 19-year-olds living at home where the annual family income exceeds $65,529. This move if implemented would result in an effective marginal tax rate of over 1.34 million percent, a very clear disincentive to work.

So there’s lots of work to be done in the social policy space in my view. It will be interesting to see what emerges over time and of course, we’ll bring you those developments in due course.

Are repairs to leaky buildings deductible?

Moving on, as we recently discussed with John Cuthbertson of Chartered Accounts Australia and New Zealand, Inland Revenue’s Tax Counsel Office regularly releases draft guidance for consultation about particular aspects of the tax system. As John explained a major part of his team’s role is reviewing and responding to these draft guidance releases.

I expect he and his team are going to pay particular attention to the draft interpretation statement on the income tax deductibility of repairs and maintenance expenditure. Now, this is updating the Commissioner’s guidance from 2012 on the topic Interpretation Statement IS 12/03 which is widely used and often referenced in other guidance.

All or nothing, the impact of withdrawing depreciation for buildings

As the draft guidance notes, since depreciation is no longer allowed for buildings, it is now more important to correctly characterise repairs and maintenance expenditure. The withdrawal of depreciation means repair and maintenance expenditure is a bit of an all or nothing matter. It’s either going to be deductible or it’s not deductible and there’s no depreciation either, so the stakes are higher.

According to the introduction, the Commissioner’s interpretation has not changed since 2012, and this guidance has been updated to reflect recent legal developments, improve clarity and reflect a more modern format. The full interpretation statement itself runs to 81 pages but there’s also a handy summary fact sheet which at seven pages, is a lot more digestible.

What about leaky buildings?

Despite the Commissioner not changing his interpretation, one of the areas I think is going to provoke some controversy is in relation to the treatment of leaky buildings. To be fair, this is a complicated area, and enormous amounts have been spent in dealing with remediating leaky buildings since the crisis first emerged in the 1990s. I think it would have been better for Inland Revenue to have issued separate guidance on the treatment of leaky buildings expenditure because the numbers are very big.

It’s worth citing out at length what Inland Revenue says about the issue, because it’s sure to provoke controversy. Paragraph 193 of the guidance starts,

“Inherent defects are faults in an asset’s design, construction or manufacture that can subsequently cause a need for work to be carried out on the asset. This may be because the defect requires routine maintenance and repair work to be brought forward or because it results in additional required work or both. In New Zealand, an example of inherent defects in a repairs and maintenance context involves properties that have been referred to as called leaky buildings or leaky homes.”

It’s the next paragraph [194], which is the kicker as far as I’m concerned. It reads,

“As noted at paragraphs 100 to 102, the courts have considered a repair involves the restoration of a thing to a condition it formerly had without changing its character.

[So far, so uncontroversial].

In the case of leaky buildings, this raises the question of what is the asset’s relevant former condition. In the Commissioner’s view, this is likely to be the “as constructed” condition of the building, including the inherent defects in that construction. Therefore, works to remediate damage caused by the inherent defects that goes beyond restoring this original condition may not involve repairs if the building is improved or enhanced by removing the inherent defects. In that case, the nature of the work undertaken is more likely to be considered an improvement, the costs of which involve capital expenditure.” [my emphasis]

Paragraph 195 continues in the same vein.

“With leaky buildings, an improvement is highly likely to incur. The removal of an inherent defect is likely to be a legal requirement imposed on work done to remediate damage in a leaky building so it meets current building standards. It is also likely that work required involves replacing original materials used in constructing significant and integral parts of the building with superior materials.”

That’s a hell of a couple of paragraphs in my view, because this interpretation would appear to rule out claiming deductions for large portions of any expenditure on leaky buildings and remediation.

I see where Inland Revenue are going with this, but a counter argument is that the building was built or purchased to be used as a building, and it was unfit for purpose in the first place. How is it an improvement to make it fit for purpose, because, basically, properly constructed buildings shouldn’t leak in the first place? That’s perhaps oversimplifying the argument, but Inland Revenue have adopted an unduly strict interpretation which is not likely to be welcomed.

As I said, you can see where Inland Revenue are coming from, but you can also see that investors have a building that’s not fit for purpose and requires remedial expenditure. In some cases, they are able to continue to use the building at some reduced capacity. But based on this draft guidance they are unable to get a deduction for those repairs to get it to the standard to which it originally should have been at all times. Furthermore, because depreciation is no longer available for commercial buildings, this becomes an all or nothing issue.

As an aside its’s quite possible that the original builders or constructors of these defective buildings will face lawsuits and they may be to pay compensation or carry out remedial work in which case the building owner is not out of pocket. However, many leaky building owners face the problem of having to expend a substantial amount of expenditure, not get a deduction for it and not be able to claim depreciation. I therefore foresee quite a bit of pushback on this guidance.

We’ll have to wait and see for developments. Notwithstanding that, I also think this is perhaps such a vital matter it should be left to Parliament to determine the appropriate treatment. Watch this space.

[This is an edited transcript of the episode released on 3rd November 2025]

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

My guest this week is John Cuthbertson, FCA from Chartered Accountants Australia and New Zealand, (CAANZ). Since 2017, John has led the New Zealand tax team responsible for engaging with Inland Revenue, Treasury, Government and Opposition MPs on tax law reform, policy settings and administration. He joins us today to discuss CAANZ’s public role in advocacy, the Generic Tax Policy Process, and the new tax bill released last month and how to make effective submissions. Welcome, John. Thank you for joining us.

John Thank you for having me, Terry.

TB Not at all. Been a pleasure to bring you on. I’ve been looking to do so for some time. So, tell us a little bit about your specific role with CAANZ, the size of your team and how it plays out.

CAANZ’s tax advocacy team & role

John We’re a perfectly formed small team, TB. We have 2.3 full-time equivalents in terms of senior tax advocacy roles, which basically means that my three staff work part-time. And with that, there’s myself and a member knowledge specialist who’s responsible for our newsletters and our digital side of things. We amplify what we do or work with our tax advisory group, which is broadly put together from a cross-section of chartered accountants in New Zealand, from public practice through to commerce and academia. And they work closely with us for the various submissions we put out each year. We do advocate in the public interest, which really means free from sectorial bias and what’s good for New Zealand Inc, what’s good for the taxpayers, but also at a higher level, what’s good for the tax system as a whole.

TB You would be constantly talking with Inland Revenue and policy officials on a number of things at any one time, generally. Would that be the case?

John We have regular meetings. We meet on a fortnightly basis for a half hour catch up, if you like. But we’re not just advocating on the tax policy that is coming through. We also submit on all of the draft public rulings, and we look at the various documents that come out for taxpayers to complete each year. We’re providing input into all of that. We did 60 submissions in the year ended 30 June, just gone. That’s a huge commitment.

TB So much stuff is pushed out by Inland Revenue, I can’t possibly cover it in the podcast. I pick up stuff with those major interpretation statements, at least one or two a month, and then basically smaller rulings, et cetera. So the volume of work your team works through is phenomenal.

John Yes, last week alone, we had five submissions due on Friday.

Submissions on tax bills

TB So you’re doing submissions, and you’ve talked earlier about that process in relation to rulings, interpretation statements. But then every so often, twice a year, we get a big tax bill that’s dropped on us sometimes. What happens then? Because we’ve got the current one, the Taxation (Annual Rates for 2025-26 Compliance, Simplification, and Remedial Measures) Bill.

And this is obviously where your team will be very busy now because submissions are due by October 23rd. And am I right in thinking you’ll make a written submission, which will be quite substantial, over 100 pages? I think that’s not uncommon, but you’ll also appear in front of the Finance and Expenditure Committee to talk through particular points.

John Yes. We definitely do a written submission and it’s not uncommon for our submissions to get to about 160 pages. And that submission, we’re somewhat unique in that we submit on virtually the whole of the bill. There’ll be areas where we can’t add any value to, we recognise that, but we generally try to submit on the majority of the bill. And the reason we do that is because it sort of sets it up as, it sounds a bit rude, the sort of centrepiece submission in a way. In the sense that that’s what the committee use because we summarise the main clauses of the bill, and then what we do is we put forward our view and backup for it in terms of a set out.

Officials and MPs can use our submission as sort of a non-biased opinion on the bill if you like, so that they’ve got a document, and we purposely set it out so that they can print it off and write their notes between the margins. We’ve left all that space for them because that’s what they told us they wanted.

Appearing before the Finance and Expenditure Committee

That’s the written process. And then usually within about a week of the bill being due, the written submission, you then appear before the Finance and Expenditure Committee. That’s at your option, but we always take that option. And then you get between 10 and 15 minutes, just like any other submitter, to make your points.

So usually when we go along to that phase, we’re very selective. And by that stage, having gone for a massive submission process, there’ll be four or five key issues that stand out for their own reasons. And we will pick two of those areas and take that to the committee on the day. And we’re usually one of the first to submit, so that’s quite nice. And then we get to go through, and they’ll ask questions. And then if you’re really unlucky, they’ll ask questions about things you haven’t actually talked about, which can get a lot more complicated.

But it’s a very good process. And to be fair, you don’t want surprises coming up at that stage because it’s sort of too late. You really want most of the things to be known. And the time against the select committee, ideally, it would be a no surprises basis. But unfortunately, there are often things that need to be dealt with.

What about Amendment Papers?

TB So, for example, let’s say something unusual happens between now and October, they may drop in an Amendment Paper [previously a Supplementary Order Paper]? These can be controversial because sometimes they come in, and no one’s had a chance to submit on them. These Amendments tend to find themselves getting amended further on down the track because they haven’t gone through that consultation process. Or am I being unfair on the process?

John I think it depends on the amendment, TB, and the problem you have is there’s a huge variation in what those amendments can be. In some cases, the amendment that gets put in later simply because they ran out of runway for the bill, which has to be completed by a certain time. But they’ve still done the majority of the work, and they do the extra work to bring it in. And it depends when it comes in on the process of the readings of the bills as to how much public scrutiny it does get.

A clarification or a change in the law?

If it comes in at the very end, then it gets no scrutiny. But if it comes in slightly earlier, there will be scrutiny. I’m more concerned about the things they call clarifications, because quite often they’re not. Clarifications can often be a change in the law. That’s probably what more concerns me, but you’re right. We would always try, and people can actually put a supplementary submission in if they want to, a written submission and see how that goes. It might not always be accepted, but you’ve got that option and sometimes they will allow for that automatically. That will be stated that you can submit on this point and require a new due date, but certainly if something has come in late and it’s controversial or it’s not what we would want, then definitely that’d be one of the topics we would raise in our oral submission.

The problem with the 2020 trust disclosure rules

Now, if I go to the trust disclosures one, which is a pet hate of ours to be honest with you, that had all the hallmarks, TB, of coming in late as a pre-Christmas present, under urgency, without public consultation. And came with the 39% rate also introduced the same way for when that all came through.

And it’s never good to put something like that into primary legislation because it’s very hard to alter and fix in a quick and meaningful way. And it just went way over the top. And what I mean by that, my personal preference would have been that they’d had a census to get the information gaps that they had and fill it in that way first and then have a lot lesser regime in terms of information you want to keep on an ongoing basis.

11% of trusts return 81% of the income

They’ve had a number of years of this now and we use their own data they collected from the first year of the trust disclosure information to go to the select committee when they were putting the trustee rate up to 39%. Because their own data showed in the end that there was only 11% of trusts that earned more than $180,000 in this country as total trustee income. But the dichotomy was that those 11% actually earned 81% of total trust income.

TB Wow.

John And when you went through the numbers underneath that, there was a very significant number of trusts that earned very little income, nowhere near $100,000 or $80,000. Some of them were just $1,000 or $2,000 when you think about it. And that very small percentage, and this is how we got to that scenario, having a small trust exemption in terms of the trustee rate at 33%, which we pushed for very hard.

We think the rules as they’ve stood, and they’ve been gradually reduced, are still too harsh on the smaller trusts because even though they’ve got reduced disclosure requirements, they’re still disclosure requirements and still quite onerous to do. We would like now to see those smaller trusts removed completely and just look very closely at the information you need from the larger trusts.

Because we had a whole mismatch there on the way through of information around distributions and deemed distributions and deemed settlements. And some of them it was just going to the family bach for a holiday, it was in a trust scenario, and you had the option of valuing that at market value or nil. Most people would have taken nil. But once you start mixing numbers and characterisations up like that, you get some meaningless data. I’m not sure what you got out of that. And I think they just didn’t know what they wanted and asked for too much.

Impact of the Trusts Act 2019

TB Yes, that was a problem. That’s picking up an earlier point, that one-size-fits-all. Yes, the trust disclosure rules were very onerous. The new rules did coincide with the Trusts Act 2019 coming into force which requires more disclosure going on then, but my view would be, “What’s the baseline that’s required under the Trusts Act 2019?” And that ought to be acceptable within certain parameters, unless you define a large trust and say it’s income is X or assets worth Y and work around that rather than the approach we got.

John The problem though Terry, with the rules that they brought in was that they weren’t quite linked with the trust.

So you were asking for things that weren’t already in existence and people had to then create extra costs to combine things or strip things apart like land and buildings. Now they’ve realised that, they’ve simplified that to allowing you to present it in the way you normally present it.

The problem we see though, is whilst it looks good that this is being repealed from our perspective, when you read the fine print, and it’s always in the detail, it says because they think that they’ve got their general powers to collect the same sort of information and it’s up to the Commissioner now to decide what information they need on a go-forward basis. So, if you saw one of our recent press releases, it was more around a plea to Inland Revenue to be sensible about what they need be mindful of . And I think there’s a huge dichotomy here between that small trust, big trust scenario when you look at where all the income’s been earned. And the problem’s different now too, because we’ve got a trustee rate of 39% and a top marginal tax rate of 39%. Presumably that’s taken some of the heat out of what the fear was in the first place and why they needed the information.

Tips for a good written submission?

TB In terms of tips for submitters, what would you say from your experience? Because obviously, you’ve probably got the best guides on how to submit. All submissions pick out key points and use your 10 min that you get wisely. But on a written submission, what would you say would be a good way of approaching it?

John Look, there’s one key bit of advice I’d give, and you can take this how you like, but I think a lot of submitters are guilty of focusing on the negative. They’ll come out and say “We absolutely hate this thing. You should not do it. What the hell were you thinking?”

But that’s all they say and they don’t offer anything. I think what is really powerful is if you can come along and say “look, we don’t like this for X, Y, and Z reasons. We think there’s a better way of doing it or achieving what you want to achieve. And by the way, this is what it could look like.” If you can put up alternative scenarios, that’s what we went to the select committee with on that 39% trustee rate.

We came out and said well, we’ve got this data now from you. We had an Official Information Act request. We gave them a two-page summary and when presented on it and we did that in advance. So, I think for submitters the idea is not just to have a rant. I think for some people it’s cathartic, but it doesn’t achieve anything other than getting it off your chest.

The reality is having your eyes open, be measured and objective. It’s not a personal affront. What you’re trying to do is be seen to be sensible and have objective ideas. Set out what you see wrong with it, that’s fine, but then offer up an alternative, that’s the most powerful thing you could do. And you may not have an alternative necessarily, but you don’t have to have all the technical detail to say how this will work, because that’s their job to put together at the end of the day. If you can help them, that’s fine. If you’ve just got a genesis of an idea which says, well, could it be done another way, which would involve this and this? That’s all you have to do. You don’t have to give them the answer. All you have to do is point out that it’s in need of a solution and that’s possibly what it could look like.

TB Well, I think on that note, that seems a good place to leave it. My guest this week has been John Cuthbertson, FCA of the Tax Leader of Chartered Accountants, Australia and New Zealand. John, it’s been fantastic to have you on talking about your role, The Generic Tax Policy Process and submissions. And thank you for your insights on the new tax bill. Really great pleasure to finally have you as a guest. Thank you so much.

John Well, thank you for having me, TB. It’s been a been a pleasure.

TB That’s all for this week, I’m TB Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Organisation for Economic Cooperation and Development (the OECD) has just published its Tax Policy Reforms 2025. The report is intended to provide comparative information on tax reforms across countries and the latest tax reform trends.

This year’s edition focuses on tax reforms introduced or announced during the 2024 calendar year in 86 jurisdictions. This broad scope makes it such a fascinating report as it gives insights and very interesting data on what trends the OECD are seeing and how other countries are adapting their tax systems to particular challenges.

Key trends

The first conclusion was that after 2023 marked a turning point away from the broad tax relief measures seen during the pandemic and the subsequent period of inflation, 2024 solidified that trend with a mix of rate increases and targeted tax support across all major tax types.

“High levels of debt coupled with the significant emerging spending needs relating to climate change, ageing and in some countries, increased defence spending has meant that jurisdictions of all income levels have adopted strategies to mobilise more revenues.”

Rising cost of climate change

In short, we’re not alone in realising that we’ve got issues coming down the path. I do find it interesting that while the debate in New Zealand has focused on the increasing costs of superannuation and health care, the OECD executive summary references climate change first. Although we definitely face future issues around changing demographics with rising superannuation costs and related health care costs, the immediate expenses in relation to climate change are arriving now.

Widespread tax and social security increases and base-broadening

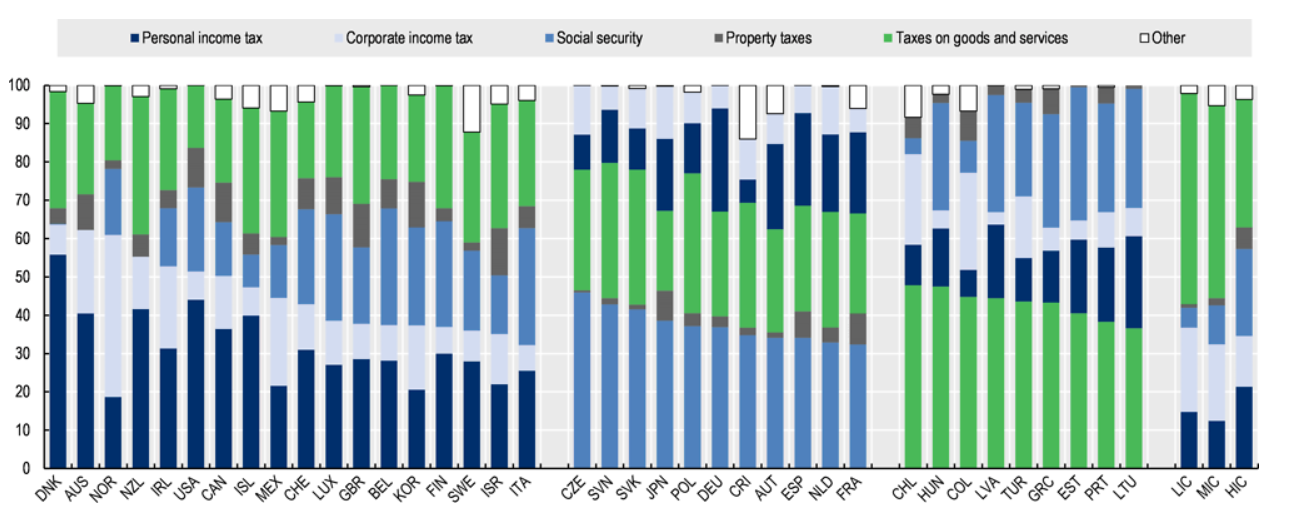

According to the OECD, during 2024 more jurisdictions raised their top personal income tax and capital income tax rates than in previous years, “often to generate revenue or enhanced tax progressivity.” This also applied with social security taxes, another area where our system is a bit of an outlier. Almost all other OECD jurisdictions do have such taxes where they represent upwards of 25% of the total tax take.

According to the OECD, social security contribution rate “increases remained widespread and amid rising health and ageing-relating spending”. Meanwhile social security base broadening measures included focused on increasing maximum contribution thresholds and expanding the range of covered income, whereas based narrowing measures targeted specific types of workers or sectors to stimulate labour force participation.

ACC increases

Although we don’t have a general social security tax New Zealand is noted as one of the countries increasing their social security contribution rates during 2024. What the OECD is referring to here is ACC, where levies were increased by 5% with further increases set to occur in the next two years. These increases were announced in late 2024 and in case you missed the detail they are as follows:

Year

Levy rate (GST inclusive)

1 April 2027 to 31 March 20281 April 2026 to 31 March 20271 April 2025 to 31 March 20261 April 2024 to 31 March 2025

$1.83 per $100$1.75 per $100$1.67 per $100$1.60 per $100

It’s likely many haven’t noticed these changes because they are deducted through PAYE, so they are one of those unknown tax increases (like bracket creep) which happen without many realising.

Plenty happening with GST/VAT

I found the section on Value Added Tax (VAT) or GST one of the most interesting. As the OECD notes the use of reduced VAT rates/exemptions as a policy instrument remained widespread in 2024.

“In almost all jurisdictions, governments apply reduced VAT rates or exemptions, most often intended to reduce the tax burden on essential products such as food, healthcare, education and housing. Reduced VAT rates were also used as a means of supporting certain sectors, such as sports, tourism, culture and agriculture.”

In addition, many jurisdictions continued to use targeted temporary VAT rate reductions as a tool to cushion price increases on specific products or as part of support measures in response to natural disasters. (An interesting idea but probably not practical here).

By contrast to the single all-inclusive 15% GST rate applicable here there’s a lot of tinkering that goes on in other countries around applying zero-rating. For example, the UK extended zero-rating on menstrual products to include reusable period underwear. Over in Ireland, it reduced the VAT rate on the supply and installation of heat pumps from 23% to 9%. Ireland also extended zero rating on the supply and installation of solar panels for private dwellings to include schools.

As we discuss below GST/VAT is an efficient revenue raiser which is why Estonia raised its VAT rate from 20% to 22% to help rebalance its general budget. Similarly, Singapore has been gradually increasing its VAT rate. On the other hand, ten countries increased their VAT registration thresholds to support small enterprises.

Inflation and GST/VAT

The report notes Luxembourg previously lowered their standard rate of VAT to 16% to help deal with inflationary pressures. In 2024 the rate was raised back to 17%. I’ve often thought because it directly affects spending, VAT/GST is something that could be used to better target dealing with inflation rather than through interest rates.

Overall, it’s interesting to see the very active use of GST/VAT for public policy purposes

Going against the trend

Many jurisdictions increased taxes on tobacco, alcohol and sugar sweetened beverages, although we are noted as going against the trend in relation to heated tobacco products. By contrast sixteen countries including Canada, Ireland, Spain and the United Kingdom, implemented or announced increased taxes on tobacco products to improve public health and raise revenue.

Fuel excise taxes and expanding carbon taxes

Another notable shift according to the report was the move away from temporary fuel tax reliefs towards increases in fuel excise taxes. For the second consecutive year, high-income countries, and we are included in that list, “continued to strengthen explicit carbon pricing…with several increasing carbon tax rates or expanding their scope to include new sectors such as international shipping and agriculture.”

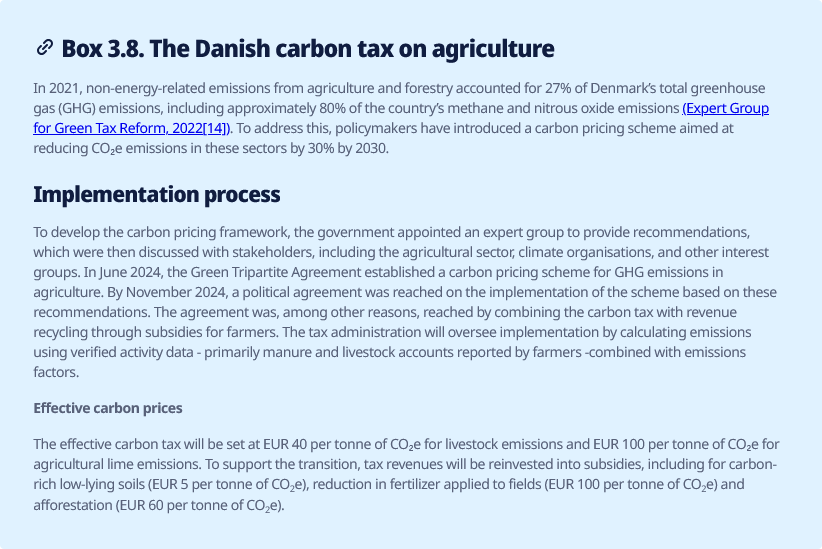

A carbon tax on agriculture – the Danish example

Something which will probably horrify farmers is Denmark’s carbon tax on agriculture aimed at reducing CO2 emissions from agriculture and forestry by 30% by 2030.

The Danes propose recycling the tax revenue into subsidies, including for carbon rich, low lying soils, reduction in fertiliser applied to fields and afforestation. I consider environmental taxes have a big role to play in climate adaptation, but my firm view is they are recycled to mitigate the effect of transition to a lower carbon economy.

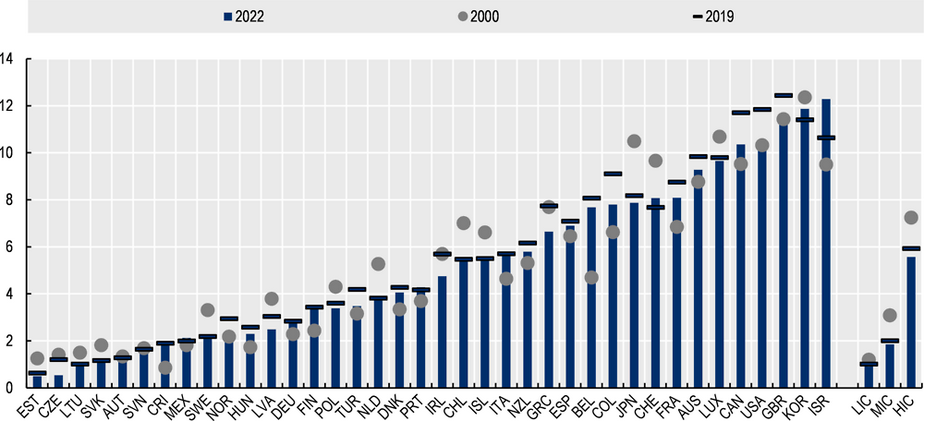

Corporation tax trends

In 2024 more jurisdictions increased corporation tax rates than reduced them for the second consecutive year. It therefore seems the long-running downward trend in corporate income tax rates has halted or is reversing. That said, the OECD noted “many governments continue to prioritise support for investment”, such as the Investment Boost in this year’s budget. Governments continue to offer tax incentives for investments, particularly in research and development, clean technologies and strategic sectors.

The report notes there are continuing wide disparities in corporate income tax (CIT) revenue across countries particularly between low-income countries where CIT represented 22% of revenue in 2022 compared with 13.3% in high-income countries. At 13.69% we’re slightly above the OECD high-income average but quite some way below Australia’s 21.814% in 2022.

According to the OECD the average combined rate was 21.1% in 2024, which is down from 28% in 2000. Three countries (Austria, Luxembourg and Portugal) cut corporate tax rates in 2024, but five, Chechnya, Iceland, Slovenia, the Slovak Republic and Lithuania all increased their corporate tax rates.

Small business measures

The report discusses the wide range of incentives for small and medium sized enterprises (SMEs), which is very interesting to see. Several jurisdictions have specific incentives or tax rates for SMEs with the look-through company and shareholder-employee regimes being the closest comparison.

The report noted in relation to research and development incentives that “on average SMEs benefited from higher tax incentives due to the preferential tax treatment specifically aimed at smaller firms.” As noted above we typically don’t have such measures but arguably if you want to lift New Zealand’s productivity, specific incentives for SMEs is perhaps something worth considering.

Property tax reforms

This section covering property taxation includes not just real property, but also capital taxes. Here the trend was predominantly focused on rate cuts and base narrowing measures. These measures were designed to make housing more affordable, simplify property tax systems and encourage investments. Where property tax increases did occur, “they were primarily driven by the need to raise revenue and address equity or fairness concerns.”

According to the OECD property taxes continue to make up a relatively small share of total tax revenues in most countries, although significantly more important in high-income countries where they averaged 5.6% of total tax revenues in 2022. (Perhaps surprisingly, New Zealand sits at this average).

As always, a fascinating report to review with plenty of detail and policies to consider. Well worth a read.

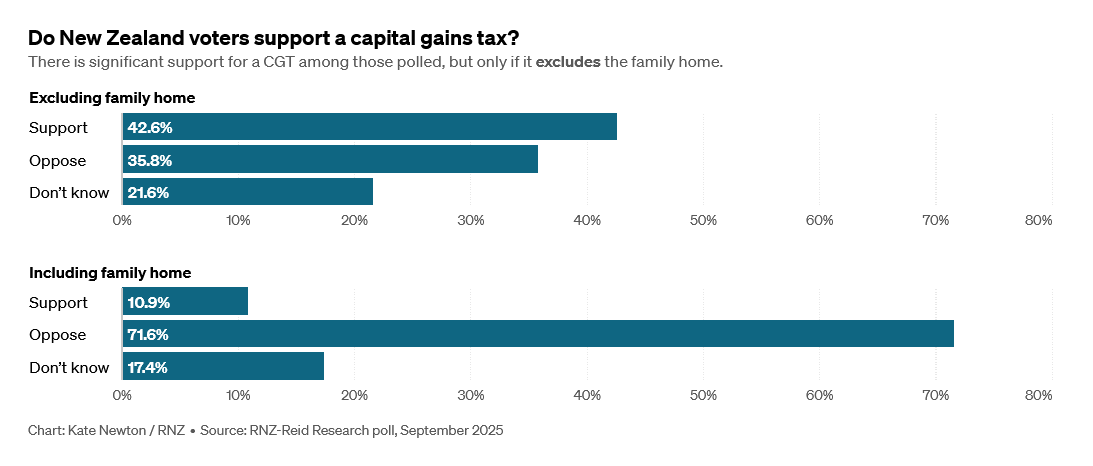

Yeah, nah, definitely maybe – what do the public think about capital gains tax?

Moving on, a recently released RNZ-Reid Research poll gives an indication where the public stands on capital gains tax. The headline summary is a plurality support it, so long as it doesn’t include the family home.

Of interest here is the relatively narrow plurality in favour and the over 20% “Don’t knows.” So very much up for debate it appears.

Happy 40th Birthday, Australia’s CGT

Saturday 20th September was the 40th anniversary of Australia introducing its CGT. When considering a CGT, we have 40 years of evidence from our closest neighbour as a counterfactual. If a CGT was as dire an issue a problem for our economy as its opponents often suggest, then we should be richer than Australia and have higher productivity. However, the objective evidence points the other way. That’s not to say that introducing CGT will immediately improve our productivity, but it should mean that more capital is deployed more effectively.

Yes, Australia’s CGT comes with great complexity, but that complexity is all around the world. On the issue of complexity, I think it’s also a relativity point. If Australia, which is our closest peer economy has it and we don’t, then this is where relative efficiencies come into play. Are we more efficient and productive than those economies because we don’t have that complexity? My view is the evidence is our productivity is already falling behind so arguing CGT inhibits efficiency and productivity is not necessarily true. If other countries consider they need to have a CGT for a variety of reasons beyond simple revenue raising, then that is something we should factor into our thinking.

Professor Keen is a very interesting gentleman who is a former Deputy Director of the Fiscal Affairs Department at the International Monetary Fund (the IMF). During his time with the IMF, he led missions to over forty countries, so he has a great breadth of experience. Currently, he is Ushioda Fellow at the University of Tokyo.

I attended the presentation he made to the Tax Policy Charitable Trust in Auckland which was followed by a panel discussion with Aaron Quintal (Tax Partner, EY), Robyn Walker (Tax Partner, Deloitte) and Kelly Eckhold (Chief Economist, Westpac). As you’d expect it was a fascinating event.

If you think our ageing challenge is big, at least we’re not Japan

Professor Keen began by praising Inland Revenue’s long-term insights briefing, for actually considering the coming demographic fiscal issues. Japan where he now resides also has an ageing population and its demographics are horrific. Furthermore, its government debt to GDP ratio is over 200%. Japan is facing major issues but, in his view, the Japanese policymakers just weren’t willing to engage on the topic, whereas we were.

Professor Keen thought our tax system on the whole has an underlying logic to it. He particularly liked our GST system for its comprehensiveness “Don’t touch it, it’s fantastic.” In relation to the topic of CGT Professor Keen noted that it could complete our comprehensive income tax framework. He suggested that any CGT adopted should be inclusive with exclusions as an approach, rather than where we are at the moment, where it’s exclusive with inclusions (and there are more inclusions than many realise). Most comparable jurisdictions have already implemented a CGT regime along the lines suggested. I did get the impression he was surprised at how much of an argument went on around the topic.

GST at 22%?

In the following panel discussion GST was seen as the area where if we are going to raise additional revenue then GST must rise. Professor Keen noted that if we were to increase GST to the average European rate which is nearly 22%, that would raise 4.5% of GDP, a huge sum of money which would go a long way to resolving future funding issues.

The big “But” to raising GST is mitigating its effect on lower income earners. We have an issue with this already in our system as I’ve discussed previously. We would need to bring in much greater targeted relief for those most adversely affected by an increase in GST.

Professor Keen noted that Inland Revenue’s view was that GST could go up to 17.5%, but any higher may hit potentially significant public pushback. This is interesting when you think about European rates of 25% and higher.

It was a very interesting presentation by Professor Keen. It’s always good to get an international perspective on our system. We get a favourable tick basically because we have a very good GST system, a reasonably solid basis of policy making and we are trying to address these coming fiscal pressures.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

a new report on how the tech companies minimise their tax.

and tax agents rate Inland Revenue.

Recently we discussed the Taxation (Annual Rates for 2025−26, Compliance Simplification, and Remedial Measures) Bill which coincided happily with the New Zealand Law Society’s annual tax conference.

Making compliance with the financial arrangements regime easier

Amidst all the excitement, I overlooked a fairly critical measure in relation to the financial arrangements regime. As regular readers will know, the financial arrangements regime is highly complex, and little known to the average taxpayer. A major issue with the regime is that once certain thresholds are breached unrealised gains and losses must be included in taxable income, i.e. on an accrual basis.

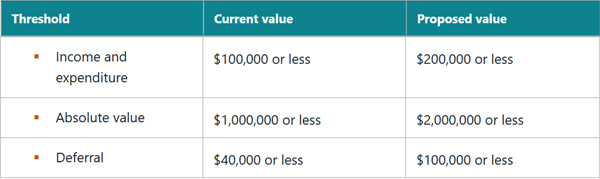

These thresholds have not been amended since 1999 which was the last time there was a serious review of the financial arrangements regime. It’s therefore very welcome news to see a proposal to significantly increase the three key thresholds allowing persons to be treated as a ““cash basis person” and therefore able to return income or expenditure from a financial arrangement on a cash (realised) rather than an accrual (unrealised) basis.

However, Robyn Walker of Deloitte has pointed out the continued existence of the deferral threshold remains problematic. At present, even if the other two thresholds are met, income may still have to be returned on an accrual basis if the difference between income and expenditure calculated on an accrual basis and that under the cash basis exceeds the deferral threshold. In other words, in order to comply with the cash basis method taxpayers are required to calculate and track income and expenditure under the accrual basis.

As Robyn notes the deferral threshold just needlessly complicates matters. (The anecdotal evidence is that its effect is often not realised). She is therefore campaigning for the repeal of the relevant provision requiring the deferral threshold calculation. I fully support her suggestion as bringing about a much-needed simplification. As an aside my personal preference would be for the new thresholds to have retrospective effect from 1st April 2025, rather than 1st April 2026 as proposed.

PepsiCo and Big Tech

One of the papers at the recent New Zealand Law Society tax conference reviewed the Australian PepsiCo case involving what’s called an “embedded royalty”. In this case the Australian Tax Office (“ATO”) said that a bottling agreement for concentrate agreement between PepsiCo and Schweppes Australia Pty Limited involved an embedded royalty and therefore withholding tax was due on a portion of the payments under the agreement.

The ATO won in the initial court case in March 2023, but on appeal and a majority of the Full Federal Court ruled in favour of the taxpayers in March 2024. The case then went to the High Court of Australia which has just ruled 3:2 in favour of Schweppes Australia/PepsiCo.

That would appear to be the end of the matter in Australia but as the paper and session at the New Zealand Law Society tax conference noted, the case remains of interest here. In particular, could our non-resident withholding tax and non-resident contractor’s tax rules apply to part of any payments made to an offshore related party by a New Zealand company.

The PepsiCo decision coincides with the release of a report from Tax Justice Aotearoa entitled Big Tech Little Tax – Tax minimisation in the technology sector. This report examines the publicly available records of the major tech companies in New Zealand to determine how much income tax they are paying and how they are structuring their affairs.

There’s a lot to pick apart in this report. It notes the Government has decided to withdraw the bill introducing a Digital Services Tax (DST) given the Trump administration’s plain declaration that any form of DST would be viewed unfavourably. Inland Revenue had estimated a DST would have been yielded perhaps $100 million in annual revenue.

Targeting the tech giants

The purpose of the paper (written by ex HMRC/Inland Revenue international tax specialist) is

“…to identify practical options to capture a greater proportion of income, including through the application of existing legislation. It argues, for example, that applying the 5% withholding tax stipulated in the New Zealand US double tax aggregation agreement to the service and licence fees of Google, Facebook, Amazon Web Services and Microsoft would have yielded withholding tax revenue of $130 million.”

The paper analyses the various types of fees paid by the New Zealand subsidiaries of companies like Google, Facebook, Amazon Web Services, and Microsoft, and explores whether some of these payments might, in substance, constitute royalties and therefore subject to non-resident withholding tax of 5%. This is where the PepsiCo case becomes particularly relevant, as it provides insight into how such payments might be classified.

The paper analyses the tax practices of the tech giants and their three primary models of tax minimisation: the service fee model, the inflated licence fee model, and the service company model. Facebook, Google and Amazon Web Services appear to use the service fee model involving substantial “service fees” to related offshore companies.

Oracle New Zealand and Microsoft New Zealand use the inflated licence fee model, under which the local subsidiary pays a large percentage of their revenue to offshore subsidiaries for the licensed use of certain intellectual property rights. According to the report in 2024:

“Oracle New Zealand earned revenue of $172.7m but paid licensing fees of $105.3m to an Irish related party, leaving taxable income of just $5.3m. In previous years, the company has disclosed royalties, which, at that time, made up between a third and three-fifths of total revenue.

Microsoft New Zealand earned revenue of $1.32bn but paid $1.075bn in “purchases” to an Irish related party, leaving taxable income of $62.8m.”

It so happens that Oracle in Australia is currently in the middle of litigation with the ATO regarding the sub-licensing of software and hardware from Oracle Ireland to Oracle Australia and whether these should be treated as a royalty. This is a major case as apparently at least 15 other multinationals are facing a similar dispute with the ATO. Inland Revenue (which tends to follow Australia’s lead on transfer pricing issues) will be watching with interest.

A lack of transparency

The paper also discusses MasterCard, Visa and Netflix where we really don’t know what’s going on because there is no publicly available information. At present all three companies meet the requirements to be exempt from publishing financial statements. The paper surmises the three companies utilise the service company model under which “the local subsidiary operates only as a marketing and support service to an overseas group company, while sales or service revenue is booked offshore.”

I agree with the paper’s recommendation that the Companies Act reporting requirements are changed “to require all local subsidiaries of overseas-headquartered companies to file accounts publicly.” The numbers are reportedly quite large for MasterCard and Visa; it’s the commission on $49.5 billion of credit card payments. In the case of Netflix, if it has 1.2 million subscribers in New Zealand then its expected subscription revenue should be approximately $250 million a year.

Overall it appears there is substantial potential profit shifting happening through the use of various fees, some of which could be subject to non-resident withholding tax. As noted above there is significant litigation happening in Australia on the issue and I don’t think the ATO is going to back off on the matter. I do wonder where Inland Revenue is on this and I expect that we will see more chatter and more discussion of this topic.

Tax agents survey results

Finally, what do tax agents think of Inland Revenue? Quite a few times it depends on what we receive in the morning mail and how our clients react. Joking aside Inland Revenue regularly surveys tax agents and it has just published its Tax Agents Voice of the Customer survey results for the just ended 2024/25 financial year.

According to Inland Revenue tax agents “continue to report strong satisfaction with our services. Some of these results are at their highest levels so far:

92% of tax agents are satisfied with their overall experience

95% found it easy to get what they needed, which is a significant improvement

88% trust Inland Revenue.”

Those are all fantastic numbers and very encouraging.

The benefits of answering the phone

Inland Revenue considers these results “reflect our improved responsiveness” which includes that “Over the past six months, many of you have noticed it’s now easier to talk to us on the phone.” Not being able to get through and speak with someone at Inland Revenue has been a sore point for many tax agents.

The reality is that although Inland Revenue would prefer tax agents and the general public interacted online with it, sometimes there is no substitute for a phone call. This is the swiftest way of sorting out any issues resulting from Inland Revenue not processing a transaction correctly. Often a tax agent will come under pressure from a client to resolve an issue swiftly. I think Inland Revenue doesn’t always appreciate that when it drops the ball, we as tax agent cop the flack for it because something we’ve said is going to happen hasn’t been done. It’s therefore encouraging that phone response times have improved.

Tax agent satisfaction with responsiveness on web messages is now 74% up from 70% for the year ended 30th June 2024. I think that’s too low it should be at least 80% in my view. To be fair I think Inland Revenue would want to reach this level too. Satisfaction with consistency of Inland Revenue’s advice was 76% for the year which is down from 79% for the 2024 year. As Inland Revenue notes consistency of advice is important but remains a challenge.

Outside of survey bodies such as the Accountants and Tax Agents Institute of New Zealand, the Chartered Accountants of Australia and New Zealand, and the New Zealand branch of CPA Australia all regularly discuss service delivery and operational matters with Inland Revenue officials. Overall, the survey is a pass mark for Inland Revenue, but areas for improvement remain and it’s good to see it acknowledging this.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.