This year’s annual tax bill, the Taxation (Annual Rates for 2025–26, Compliance Simplification, and Remedial Measures) Bill (“the Bill”) was released at the tail end of August. The Bill’s release coincided with the New Zealand Law Society’s 2025 Tax Conference, which was a happy coincidence – unless you were one of the presenters affected and had to frantically rewrite your paper.

The Conference began with a short message from Minister of Revenue Simon Watts who highlighted the key measures in the Bill such as those relating to the Foreign Investment Fund regime, digital nomads, employee share schemes as well as the exemption for households selling electricity into the grid.

FBT reforms delayed

On the other hand, the Bill was also noteworthy for what it didn’t include. In particular there are no proposals for Fringe Benefit Tax reform, which had been highly anticipated. According to the Minister, “FBT reforms are going to need more time.” This appears to have been in response to fierce lobbying from Federated Farmers over the very vexed question of the application of FBT to twin cab utes and vehicles generally.

The other area not included was the taxation of charities and not-for-profits and in particular the question of donor-controlled charities. This was less of a surprise because the Government backed away from changes earlier this year.

Digital Nomads

The Bill includes measures to improve or clarify the tax of New Zealand visitors and in particular so-called digital nomads. These follow on from announcements made in January allowing visitors on non-work visas to work remotely. The tax changes are designed to

“…address issues that may be discouraging visitors from staying in New Zealand for longer periods of time while maintaining the integrity of the underlying international tax rules.”

Effective 1st April 2026 the Bill will allow certain visitors to New Zealand, called non-resident visitors, to be present in New Zealand for up to 275 days in a given 18-month period without becoming a New Zealand tax resident. They have to be here lawfully and not undertake work for a New Zealand employer or client.

The proposals would also deal with the questions around exempting the non-resident employer from New Zealand employment related obligations, such as PAYE and FBT. Crucially, because this has become a very important question in this area, Also, and this is pretty important because of the greater ease of working remotely, the activities of a non-resident visitor are disregarded when determining whether a foreign entity has established a permanent establishment in New Zealand.

Similarly, if the visiting person is a director of a non-resident company, then as long as they meet the other conditions, the centre of management of or direct control of the non-resident company will not be considered to have moved to New Zealand for tax residence purposes.

These are welcome proposals which clarifies a grey area. That said I think it’s time that Income Tax Act had a specific clause which gave the Commissioner of Inland Revenue discretion to exclude from the “days present” count days where a person has been unavoidably detained in New Zealand due to sickness or, for example, another pandemic.

Inland Revenue granted itself that discretion during COVID back in 2020, but actually there was no such provision in the Income Tax Act, which would have allowed it to do so. My view is it should have that discretion so it can deal with unique circumstances.

Foreign Investment Fund regime changes

The Bill includes the final details around the changes to the Foreign Investment Fund (“FIF”) regime which have been foreshadowed for some time. Under the Bill eligible migrants can elect into the “Revenue Account Method” which will tax FIF interests on a realisation basis.

The main person eligible will be those who are in overseas companies’ employment share schemes where the regular valuations required under the FIF regime aren’t easily obtainable because the company is unlisted. The other main group are American citizens who continue to be subject to US taxes, even though they are no longer resident in the USA.

Under the Revenue Account Method eligible FIF interests together with any dividends received would be taxable on a realisation basis. However, only 70% of any gains or losses will be reported and subject to tax. Assuming a taxpayer’s marginal tax rate is 39% this works out to be an effective 27.3% tax rate. I thought the Government might go with the highest prescribed investor rate, which would have been 28%.

This measure takes effect retrospectively from 1st April 2025. On the whole I think it’s a welcome move although there will be grumblings that the capital gains discount should have been higher.

Employee share scheme changes

The Bill allows unlisted companies to elect into a regime where the tax liability for employees who receive shares or share options as part of an employee share scheme can generally be deferred until a liquidity event, such as the sale of shares.

That obviously makes sense in terms of the point at which you can value the shares and the employee who is doing a lot of work there will have the ability to raise the funds to cover their tax liability.

Controversial provision repealed

The Bill repeals the controversial section 17GB of the Tax Administration Act 1994 introduced in 2020 by the last Labour government. Section 17GB allowed the Commissioner of Inland Revenue to collect information for purposes relating to the development of policy for the improvement or reform of the tax system. This section was then used to carry out the high wealth individual research project, which was highly controversial.

The section’s repeal isn’t universally applauded. John Cuthbertson, the head of tax for Chartered Accountants Australia and New Zealand (“CAANZ”) suggested it was useful for Inland Revenue to have such data gathering powers to help develop tax policy.so long as the powers are judiciously used and managed. I sparked a lively LinkedIn discussion after I commented in support of John’s comments as I don’t believe we get enough data and information on our tax system, certainly compared with other jurisdictions.

In the discussion it emerged that according to the accompanying Regulatory Impact Statement (“RIS”) Inland Revenue undertook targeted consultation with eight key stakeholders in September 2024. This consultation included “stakeholders from the private sector, public interest groups, as well as academics.” This is pretty standard as part of the Generic Tax Policy Process. However, John Cuthbertson revealed CAANZ was NOT part of that consultation, which is very surprising. I’m now quite intrigued to know who exactly was consulted in that group. (Interestingly, according to the RIS Inland Revenue’s preference was for retention of section 17GB but restrict the use of information collected to the development of policy.)

Privacy Commissioner disapproves of proposed ministerial-level information sharing agreements

One of the counterpoints to section 17GB was the potential invasion of privacy, which is fair enough. It’s therefore ironic to see the Bill’s proposal to enable the Commissioner of Inland Revenue to disclose information to another government agency pursuant to a ministerial-level agreement. These would by-pass the existing Approved Information Sharing Agreements.

The new ministerial-level agreements enable the Minister of Revenue and the Minister in charge of the other agency the power to agree to the disclosure of information to determine entitlement or eligibility for government assistance, for the detection, investigation, prosecution or punishment, or suspected or actual crimes punishable by terms of imprisonment or two years or more, or to remove the financial benefit of crime.

On the face of it this seems reasonable, but according to the accompanying RIS the Privacy Commissioner raised the following concerns:

“The Privacy Commissioner has concerns as it relates to the proposed changes to enable and earn revenue to disclose tax information to other government agencies. He believes the disapplication of principles 10 and 11 of the Privacy Act in the proposal is unjustified. The privacy commissioner is. Is of the view that there are existing mechanisms to facilitate the sharing of the types of information Inland Revenue are proposing, including Approved Information Sharing Agreements under the Privacy Act 2020 and the board information sharing provisions available under section 18F of the Tax Administration Act 1994.”

The measure will probably go through as proposed but it will be interesting to see if any amendments are made following submissions on the Bill (which are now open until 23rd October).

Do we really need a Capital Gains Tax?

At the NZLS Tax Conference there was a very entertaining session on the issue of a capital gains tax (“CGT”) presented by Joanne Hodge and Geof Nightingale. Joanne and Geof were both members of the last Tax Working Group the big controversy of which was its recommendation for “a broad extension of the taxation of capital gains“. However, Joanne was of part a minority group alongside Robin Oliver and Kirk Hope of Business New Zealand, who did not support the recommendation.

Joanne and Geof’s opposing positions made for a very lively session. Geof remains of the view that it is needed not only as a revenue raiser but for addressing inequality and the question of economic efficiency. Joanne is more of a sceptic about CGT. She’s concerned in part mainly about the economic inefficiencies that can result from a CGT and also considers that the costs of doing so relative to the revenue raised means that perhaps it’s not really worthwhile.

This was a key factor for Joanne together with Robin Oliver and Kirk Hope to that was what drove her, and the other two minority opinions to dissent from the proposal for a comprehensive CGT. But always keep in mind that the entire Tax Working Group agreed “that there should be an extension of the taxation of capital gains from residential rental investment properties.”

Addressing the fiscal shortfall

In making the argument for a CGT Geof picked up matters we’ve raised in previous podcasts (and in Inland Revenue’s draft Long-Term Insight Briefing) about the coming fiscal shortfall which needs to be addressed. He described the outlook as “dire” and that we cannot outgrow these fiscal projections.

Joanne took a different approach. In her view the correct question is really “how comprehensively should we tax capital gains?” Although she’s opposed to a comprehensive capital gains tax because of the complexity involved, she’s NOT opposed to broadening the net. For example, she raised a question about private equity venture capital and how many people involved in capital raises are treating shares on non-taxable capital account when in fact they should be taxed on sale because they acquired the shares with a purpose or intent of sale. In Joanne’s view better enforcement will deal with a lot of issues and raise tax revenue.

She made a very interesting point that all blocks of land should have their own IRD number which would help with better enforcement. I think it’s a really good idea.

A matter of faith?

Joanne does raise valid concerns about the complexities that are involved in a CGT. Amusingly she and Geof also referred to an informal comment from Professor Len Burman an American CGT specialist to the 2010 Tax Working Group (of which Geof was also a member). Professor Burman suggested that you can do all the analysis on capital gains tax that you want, but in the end, whether you support it or not becomes analogous to religion, a matter of faith.

It’s an interesting proposition; I worked for 10 years in a system with CGT prior to arriving in New Zealand so the arguments around whether or not it should exist simply never arose in my professional career until I came here. So perhaps I am a believer in that regard, but it’s worth noting this year is 60 years since the UK introduced capital gains tax, 40 years since Australia introduced its CGT, Canada has had one since 1972 and South Africa since 2001. As is well known, the absence of a CGT makes New Zealand an outlier. The debate over a CGT will continue to rage, and no doubt we will bring you more commentary on future developments.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

calls for capital gains tax to help solve housing affordability.

Earlier this year, the popular Auckland Cafe chain Little and Friday closed its final store in Ponsonby. That was a great personal disappointment for me as its food was wonderful, although my waistline is probably all the better for its closure.

It has now emerged that at the time of its closure, the owners owed $640,000 in tax and the company has now been put into liquidation owing creditors over $1.4 million.

This obviously puts a different complexion on the closure, and it also prompted an interesting debate amongst my tax agent colleagues, with quite a few pointing out the inconsistencies that they see in Inland Revenue’s debt management. One took particular exception to the news, commenting how he had been grilled over a relatively small adjustment, less than three figures, and yet somehow Little and Friday had been allowed to build up unpaid GST and PAYE totalling $640,000.

Focusing on the wrong target?

Another tax agent noted that he had received a call regarding a client being overdue in making their small business cashflow scheme repayments. The amount outstanding was $18,000, but as the tax agent pointed out, the client also owed several hundred thousand dollars in relation to unpaid GST and income tax. The agent was therefore rather puzzled as to why Inland Revenue seemed to prioritise the small business cashflow scheme arrears. Several other tax agents weighed in with similar points about such inconsistencies.

Now, debt management is a core role for Inland Revenue. That goes without saying. But it is also an issue where there are clearly strains emerging. We’ve talked previously about what’s been going on with the student loan scheme, where substantial amounts of debt are allowed to build up over enormously long periods of time.

My attention has been drawn to a case where the student loan borrower left more than 20 years ago and was eventually contacted by Inland Revenue demanding over $200,000 of accumulated interest and penalties. Like Little and Friday, and other cases noted above, the unanswered question is “How did Inland Revenue manage to let it get to that stage?”

Earlier intervention needed?

When looking at Inland Revenue’s management of its debt portfolio two concerns arise – its approach seems inconsistent and it doesn’t intervene soon enough.

Inland Revenue has enormous tools at its disposal. It can put companies into liquidation and that’s actually what happened with Little and Friday. But it doesn’t want to do that all the time. It will sometimes hesitate before doing anything, for perfectly reasonable circumstances. But there does come a point where it is probably better for all concerned that the Inland Revenue moves sooner and doesn’t allow the debt to build up.

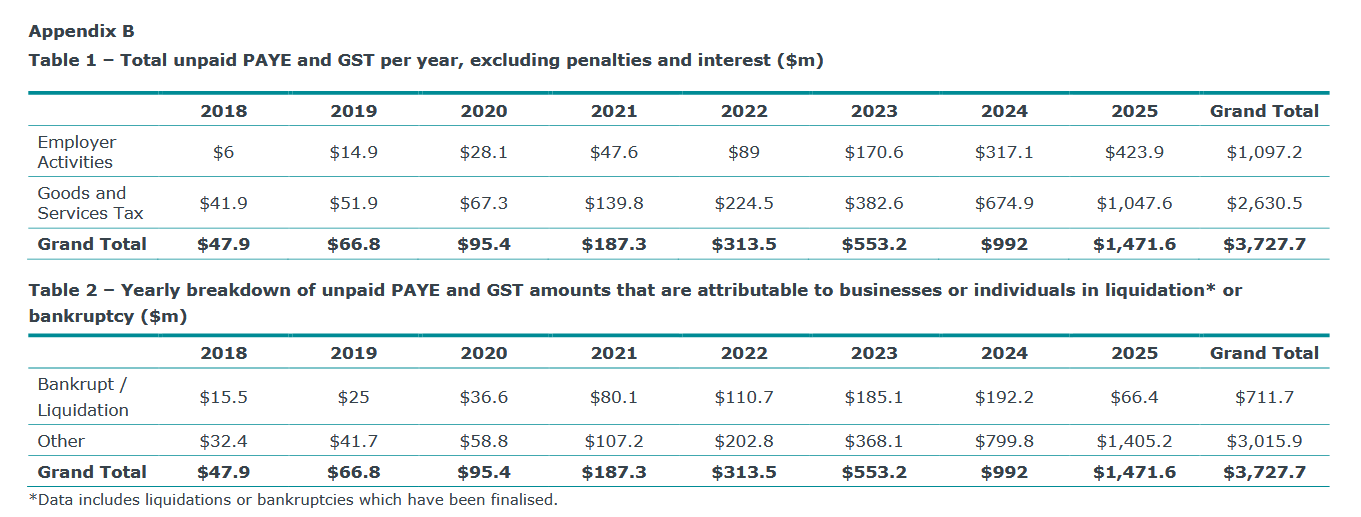

Now Little and Friday is not an unusual circumstance. While preparing for this podcast I came across an Official Information Act request about debt dating from June this year, and the number being reported was frankly horrifying. According to this report, as of 31st of March 2025, the total amount of unpaid PAYE and GST, excluding penalties and interest, stands at $3.727 billion.

As can be seen $711.7 million of that $3.7 billion represents businesses or individuals going into liquidation. The rest is simply outstanding debt which Inland Revenue is hoping to obviously try and recover. But the amount of debt it is writing off is starting to increase, as is the amount of debt that it deems non-collectible. According to this OIA report the non-collectible amount as of 31st of March 2025 is expected to be $1.1 billion dollars.

Then there’s a very interesting industry breakdown of how that amount of debt has accumulated.

The sectors hardest hit in that are our construction which has $347.2 million of unpaid debt as of March 2025. accommodation and food services, i.e. cafes like Little and Friday owe $130.6 million, manufacturing $93.7 million and professional, scientific and technical services have also accelerated remarkably $131.7 million. Even rental hiring and real estate services, which you would regard as relatively strong industries, has unpaid GST and PAYE of $179.9 million as of 31st March this year.

Across the whole of the economy, these numbers are piling up and it presents a huge problem for Inland Revenue, and by extension for the Government as to how is it going to manage this issue.

Unfairly targeting student loan defaulters?

A very real threat for people owing student loans who are not meeting their obligations is being arrested at the border. But none owe $600,000 of tax. In theory, someone owing that amount of unpaid GST and PAYE could be freely entering and leaving the country without customs making a move against them.

On the other hand, someone owing $100,000 of student loan debt, which is sizeable, yes, could enter the country and be arrested. I wonder why such an inconsistent approach applies.

To be fair Inland Revenue is working through the overdue debt issue and taking enforcement action. This week it reported how an accountant, Luke Daniel Rivers, also known as Mai Qu was jailed for six years over a $1.7 million COVID-19 fraud. He made false claims over wage subsidies in the small business cash flow scheme.

Now quite correctly Inland Revenue and the Ministry of Social Development have pursued that. But at the same time, we have these other businesses falling over, owing very substantial sums of money, and it appears almost as if the defaulters are able to walk away without consequences, to the frustration of myself and other tax agents.

What about MBIE?

One other thing of note in this area are the potential breaches under the Companies Act 1993. In some cases, you’d have to say there there’s a strong argument that businesses racking up hundreds of thousands of dollars of tax debt are in breach of their Companies Act obligations, which could lead to action by the Ministry of Business, Innovation and Employment.

The economy is under strain and tax debt is rising. Sometimes really bad luck hits a business or person. Small businesses can get hit particularly hard if a key person falls ill. Tax debt may just be down to sheer bad luck, the wrong thing happening at the wrong time.

But overall, Inland Revenue looks to be struggling, for want of a better word, managing the portfolio. Even allowing for maybe getting better resources to manage this, there’s still the question of an inconsistent approach that I and other tax agents have noted. So, there’s a lot of going on in this space.

I expect the Commissioner of Inland Revenue is reporting very frequently to the Minister of Revenue on this issue and any new initiatives to address these concerns. The most important thing would be to get the economy going again and hopefully some of these businesses are able to trade their way out. But we’ll have to wait and see.

Capital gains tax to deal with housing affordability?

Now, in recent weeks, there’s been quite a lot of chatter around Inland Revenue’s long-term insights briefing, which has talked about the need to perhaps expand the tax base. Last week we discussed how CPA Australia called for a capital gains tax.

This week at the Government’s Building Nations 2025 Infrastructure Summit on Wednesday 6 August, Group Chief Economist and Head of Research for ANZ Richard Yetsenga discussed the question of what he described as runaway house prices in Auckland, Australia and New Zealand. He said that we should look seriously at introducing a capital gains tax as a means of addressing house price affordability. In his view, if this issue is not resolved, “I think it’s going to eat us alive. It’s our biggest intergenerational issue.”

Mr Yetsenga was speaking after addresses from the Finance Minister, Nicola Willis, and Transport Minister and Housing Minister Chris Bishop. In response he suggested looking at both the supply and demand issues of the tax system, which in his view, was one of most effective ways available to influence economic activity.

That’s something I would agree with. What we don’t tax is as important as what we do tax. I think the fact that we don’t have a capital gains tax has resulted in major distortions for our economy. This was something which the recent International Monetary Fund report on our poor productivity mentioned. It’s very interesting to see all the constant chatter on the topic of capital gains taxation.

How many people return overseas income?

Finally, Inland Revenue proactively publishes any Official Information Act (OIA) requests that it receives. These often include some very interesting data such as the breakdown of debt I discussed earlier.

The question was rather oddly phrased because the requester asked “Do you know if/believe there high compliance with NZ tax rules for NZers working overseas?” Inland Revenue’s response was basically this is actually not a request for information, it’s more for an opinion so we aren’t answering that.

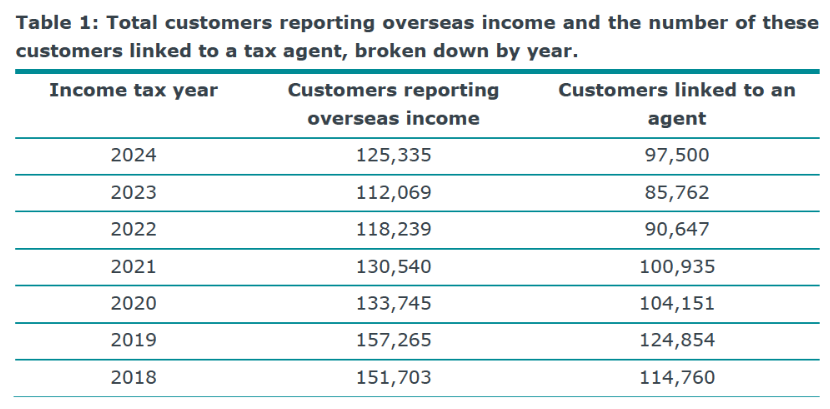

The request then asked for specific data about taxpayers reporting overseas income, and also the split between taxpayers who reported it and those taxpayers with tax agents who report it. Inland Revenue provided the following breakdown for the 2018 to 2024 tax years. (The final due date for filing tax returns for the 2024 tax year is 31st March 2025 so 2024 is the latest year for which complete details are available).

What caught my eye about this data is that the numbers have fallen since the 2019 year. In 2018, 151,703 taxpayers reported overseas income, of which 114,760 were linked to a tax agent. After an increase in the 2019 year the numbers reporting income decline each year until the 2024 year when it rises from 112,069 to 125,335.

I find it quite surprising, given the international mobility of our labour, that fewer people appear to be reporting overseas income when we have a lot more migrants arriving.

I suspect it’s possibly piqued Inland Revenue’s interest, because I’ve had some clients requesting assistance after they have been contacted by Inland Revenue which has received information under the Common Reporting Standards of Automatic Exchange of Information. It will be interesting to see how that number of taxpayers reporting overseas income tracks.

By the way, this OIA also references the Common Reporting Standard, confirming in response to a question it “receives financial account information automatically from the Australian Tax Office under the Common Reporting Standard. This information is matched to taxpayer accounts and risk assessments.”

This ought to be well known and, as noted above, maybe we might see an increase in the numbers reporting overseas income.

Happy Twenty-first!

Now finally this week, according to LinkedIn, Baucher Consulting is 21 years old today. So Happy Birthday to me. It’s been and continues to be an amazing journey and who knows what the future will bring. In the meantime, thank you all for all the messages of support.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

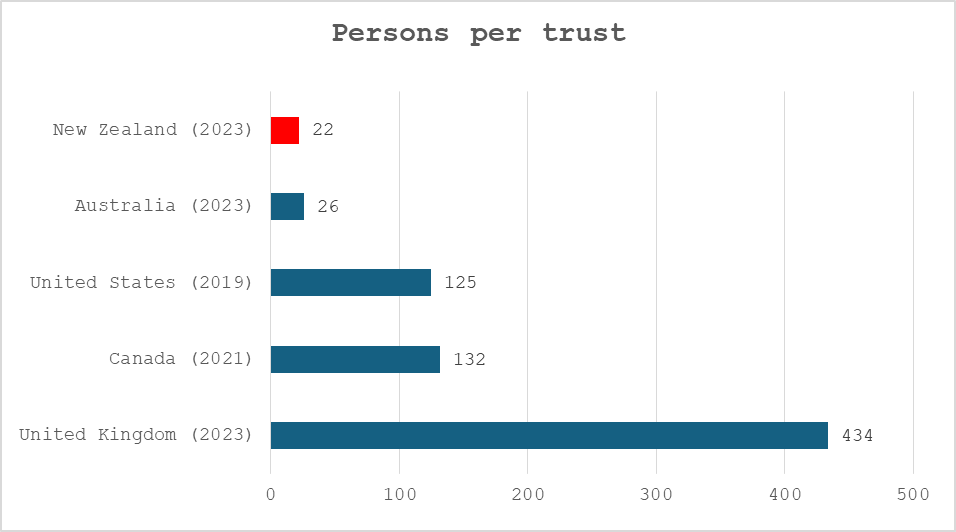

New Zealand has an extraordinarily high number of trusts relative to its population. We don’t actually have official numbers on the number of trusts in the country but estimates range as high as 600,000. Inland Revenue’s recent trust disclosures data notes that as of 31st March 2023 it had 412,000 trusts with IRD numbers. Not all of them have to file tax returns but to put it in context that number of 412,000 represents one trust for every 12 people in the country. By comparison, based on UK tax return filing statistics filed for the same period, there is one trust in the UK for every 434 people.

(Prepared by author using latest available official tax return statistics)

So, there are a significant number of trusts in New Zealand. And that means unintended consequences are lurking for the settlors, trustees and beneficiaries of these trusts. One I would consider is a well-known issue is that for Australian tax purposes, a trust is deemed resident if any trustee is tax resident in Australia. A common pre-migration planning tactic for people moving from here to Australia is to ensure that they resign any trusteeships.

Watch out for Australian resident executors

By the way, this trust residency rule also applies to executors. I’ve frequently advised clients that they need to update their wills and if they have an Australian executor, they need to remove that person or consider alternatives.

Got an Australian resident trustee? Get ready to pay Australian capital gains tax even if it is your main home.

The implications of having an Australian resident trustee are frankly messy, to put it mildly. For Australian tax purposes a trust is deemed tax resident in Australia if ANY trustee is tax resident in Australia. This potentially makes the trust subject to Australian capital gains tax with the Australian resident trustee responsible for collecting the tax on any capital gain derived by the trust.

As an Australian resident trust any capital gain will be calculated under Australian tax law. This applies regardless of the fact that we don’t have a general capital gains tax. The issue that’s emerged in several cases that I’m dealing with relates to property has been sold by a trust and the disposal was not taxable for New Zealand because either the bright-line test didn’t apply or in some cases the property was actually the main home of one of the trust beneficiaries.

Australia has an exemption from capital gains tax for the main home, but and this is a huge but, this exemption does NOT apply to main homes held in trust.

The danger scenario

The danger scenario is a typical New Zealand complying trust with an Australian resident trustee. The trust sells a New Zealand situated property and then looks to distribute the gain. Even if that gain is distributed only to New Zealand resident beneficiaries, under Australian legislation, the Australian trustee is liable for the tax on that gain. Conceptually, it seems inconceivable that the sale of a New Zealand property distributed to New Zealand residents is taxable in Australia but it’s the interpretation the Australian Tax Office has adopted because at least one trustee is an Australian tax resident.

Well, what about the double tax agreement?

What can be done about this? Well in some cases, if there are only Australian resident trustees, then to use a technical term you are frankly stuffed. But more often than not, the majority of trustees are New Zealand tax residents. In this case you might be able to apply the clauses within the double tax agreement between Australia and New Zealand (the DTA) dealing with residency.

The problem is that the current DTA following the modifications made in 2017 to adopt the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS (the MLI), doesn’t have an easy process for resolving this matter. Generally, you can apply the relevant double tax agreement to determine the place of effective management for non-individuals.

For example, a trust might have five trustees with only one in Australia and the remaining four trustees plus the settlor and this is the group which carries out the management of the trust. Accordingly, the place of effective management is in New Zealand. Australia therefore gets no taxing rights in relation to any disposals of non-Australian situated property. (Keep in mind that even if this scenario plays out, if a distribution is made to an Australian resident beneficiary who does not qualify for the Australian temporary resident exemption, the distribution is still taxable in Australia).

However, at present under the modified DTA, trustees wanting certainly will actually have to make an application to Inland Revenue through the mutual agreement process to ask them to consult with the Australian Tax Office and resolve the matter of residency.

A helpful United Kingdom court case?

Coincidentally, Howarth v HMRC [2025] EWCA Civ 822 an interesting UK Court of Appeal decision on the issue of place of effective management for a trust has just been released. The case involved a widely marketed tax avoidance scheme known as a “round the world” scheme, which was designed to avoid UK capital gains tax (CGT).

Under the scheme the trust’s Jersey based trustees held shares in a UK incorporated company. The Jersey trustees resigned in favour of a Mauritius resident trustee company who then sold the shares. Following the sale the Mauritian trustees resigned in favour of UK resident trustees. At the time the shares were sold, the trust would be deemed tax resident in Mauritius, a jurisdiction which, very conveniently, does not tax capital gains.

When the Court of Appeal considered the issue of the trust’s place of effective management it concluded the trustees in Mauritius were following a predetermined single plan set out by the UK settlors of the trust. The Mauritian trustees were “playing their parts in a script which had been written by others”. The Court of Appeal therefore upheld two lower court decisions (the equivalents of the Taxation Review Authority) that the place of effective management of the corporate trustee was in the UK.

It’s quite useful to see courts talking about the residency of trusts because double tax agreements don’t specifically refer to trusts but “non-individuals”. As a UK Court of Appeal decision, it represents a good precedent. Incidentally it’s expected if the case goes up to the UK Supreme Court, it will probably still rule the same way.

I think Haworth v HMRC could be useful for any trustees who find themselves dealing with the complications of an Australian resident trustee and they wish to ensure any Australian tax is limited only to gains actually distributed to an Australian resident.

CPA Australia calls for a capital gains tax

Still in relation to capital gains tax, as previously discussed Inland Revenue has a long-term insights briefing currently out for consultation. (Submissions are open until 1st September). The briefing discusses how we need to look at ways we could expand the base tax base to meet coming financial demands mostly around superannuation, health and in my view, climate change.

This week CPA Australia, the accountancy body which represents over 3000 accountants here in New Zealand, has called for a rethink of the tax system, including consideration of an introduction of capital gains tax (CGT). The organisation agreed with Inland Revenue; there are many pressures on the New Zealand tax system particularly around ageing demographics. CPA Australia felt the absence of a capital gains tax puts pressure on other taxes. I agree with that analysis, and I also think that’s tied to the question of productivity and diversion of our scarce capital into lower return assets, mainly residential property investment.

It’s interesting to see the CPA Australia come out in favour of a CGT. It suggests that a CGT should only apply to assets acquired after a certain date. In other words, assets held prior to the introduction of that date would be exempt. This is what Australia did when it introduced CGT, coming up 40 years ago next month.

Follow Australia? “Yeah, nah.”

Interestingly, when the last Tax Working Group considered CGT, it got advice from Australia which recommended not to follow the Australian approach and instead go for what’s sometimes known as the valuation day approach. This would base CGT on the valuation of assets on the date of introduction. CPA Australia rightly point out there are compliance problems with that approach but like so much of the stuff we encounter in the tax world, other countries have met and dealt with these issues, so they are not unique or insurmountable.

More on the abatement web

Last week I discussed a substack from Ganesh Ahirao, former head of the Productivity Commission analysing what I called The Dirty Secret of the New Zealand tax system – that very high effective marginal tax rates apply, sometimes over 70%, to people on very modest incomes.

Ganesh has written a follow up this week providing further examples illustrating how people trapped on low-income or benefits, who are trying to work their way out of the system, as they are encouraged to do so, are hit very quickly by very high marginal tax rates.

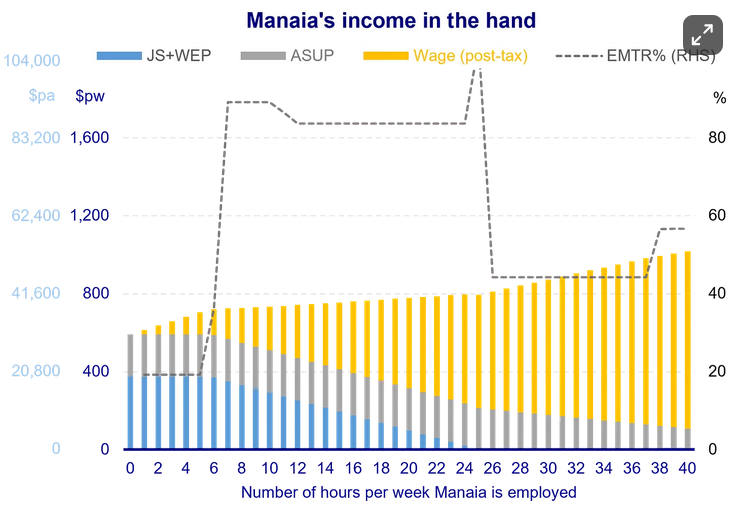

For example, Manaia is single with no children, no student loan, paying immediate rent of $415 a week for a one-bedroom flat. Manaia is eligible for Jobseeker Support alongside the Winter Energy Payment and Accommodation supplement for a total of $592 per week before tax. Six hours employment at the living wage will raise her weekly pre-tax income to $700 but above that threshold, she starts losing her Jobseeker Support at a rate of $0.70 on the dollar. Her effective marginal tax rate jumps above 80% plus.

As Ganesh details, many low-income earners seeking support even one as widespread as Working for Families face similar situations.

These graphs illustrate Ganesh’s argument which I fully endorse, is we have allowed a huge problem to develop over the last 30-40 years through constant tinkering with the benefits system and swapping universality for a more “targeted” approach. The result is a horrendously complex position which really needs cut through and reform.

I support that and make no apologies for bringing the story up. It is something we should be discussing more frequently and asking our politicians to fix. We can’t be saying to people we need you to work if you’re a beneficiary and then promptly hitting them with 80% marginal tax rates. That is unrealistic and unfair.

The meaning of ‘payment’ for GST purposes

And finally, this week, Inland Revenue has released a valuable draft interpretation statement for consultation on the meaning of payment for GST purposes. When a payment is made is crucial for determining the GST time of supply, the tax period for which you may return output tax. It’s also relevant when an input tax deduction can be claimed and particularly in relation to secondhand goods input tax deductions which are only available when a payment is made.

This draft interpretation statement (only 22 pages) will replace a couple of previous Inland Revenue guidance items, which are actually over 30 years old. The principles involved haven’t changed, but it’s still useful to see the advice consolidated in an updated interpretation statement.

The draft considers typical examples of what constitutes payment. Obviously, cash or bank transfers are payments, but what about if there is an offset or some vendor finance. For example, payment could be made by setting off against an existing debt owed by the supplier to the recipient. Accounting entries can count, but you have to have the evidence to support them, and obviously payment of a deposit represents a payment (and can trigger some GST time of supply issues in relation to the sale and purchase of a property), Overall a very useful guidance.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Every industry has a dirty secret which is known to its practitioners but is not generally known by a wider audience. In my view the New Zealand tax system’s dirty secret is how high effective marginal tax rates most impact our lowest earners.

The effective marginal tax rate (EMTR) is the highest rate of tax that is applied to the very last dollar that you earn. This also takes into consideration abatements or clawbacks which apply. Now for most persons, the natural assumption would be if the highest income tax rate is 39%, then the highest EMTR would be 39%. That’s a fairly logical, quite understandable and mostly correct approach.

How your EMTR can be above the maximum income tax rate

But, “mostly” is doing a lot of lifting because in certain instances a person’s EMTR can be above the highest tax rate. This is usually where a tax relief is withdrawn, or abatements apply. One example of where tax reliefs will be withdrawn is the Independent Earner Tax Credit, which is available to taxpayers who are not receiving New Zealand superannuation or Working for Families and have annual income between $24,000 and $70,000.

However, between $66,000 and the upper $70,000 threshold, it starts to get clawed back at a rate of 13%. This means that although the personal income tax rate for income between $66,000 and $70,000 is 30%, the effect of the clawback means a person’s EMTR within that income range is actually 43%.

The most common example that impacts most people are the interlocking layers of abatements that apply when someone is claiming a tax credit or benefit. The most notable example, which we’ve discussed quite frequently, is Working for Families. These tax credits are abated at a rate of 27.5 cents on the dollar, where a family’s income exceeds $42,700. (Respectively 28 cents and $44,900 from 1st April 2026).

Abatements also apply in relation to Accommodation Supplement and Jobseeker and the combination of all these results in people on modest incomes having extremely high EMTRs.

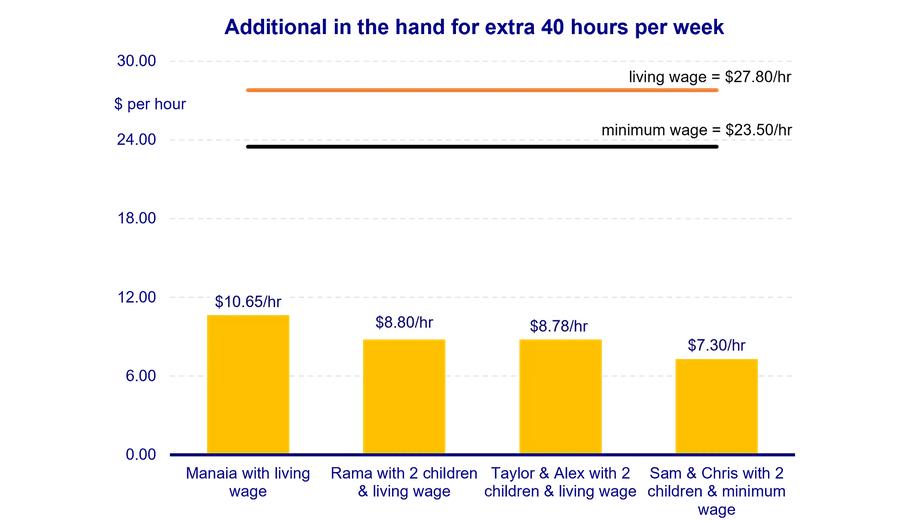

Working 40 hours a week for an additional $6.07 per hour

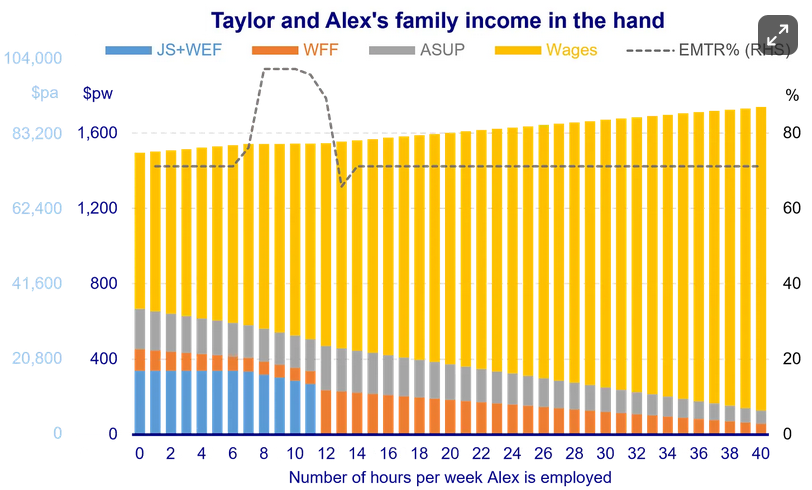

Ganesh Ahirao (Ganesh Nana), the last head of the recently disestablished Productivity Commission, has put together an illustration of how this Gordian Knot of abatements and benefits affects the family of Alex and Taylor and their two children.

The relevant facts are that Taylor is employed full-time at $25 per hour. So the family income is $1000 gross per week which, after deductions for income tax and ACC, is $829 per week net.

The family rent a two-bedroom house in Island Bay, paying the median rent for the suburb of $625 per week. This means that, after rent, the family has $204.30 per week to meet all other non-rent living costs and expenses. They’re therefore claiming additional assistance. Alex can claim Jobseeker Support there’s also Working for Families credits and Accommodation Supplement available.

However, as Ganesh illustrates, if Alex and Taylor do make a claim, they can find themselves trapped in nightmarish web of overlapping, interlocking benefits where the level of abatements can be dependent on what other assistance they’re receiving. Complicating matters is the requirement for anyone like Alex claiming Jobseeker Support to accept employment.

How to lose 71.2% in tax and abatements on the minimum wage

If Alex takes five hours at the minimum wage of $23.50 per hour (i.e. $117.50 per week) this won’t affect his Jobseeker Support because he’s allowed to earn up to $160 per week before abatement. His earnings will be subject to tax and ACC but crucially they also have an impact on the Working for Families and Accommodation Supplement because the family income is above the abatement thresholds.

The abatements and tax on $117.50 total $83.62 leaving net cash in hand of $33.88, or an EMTR of 71.2% – more than double the official income tax rate of 30% (31.67% once 1.67% ACC earner levy is added).

Remember this 71.2% EMTR is for a family earning a little bit under $60,000 a year, $1200 a week. As Ganesh’s analysis illustrates their EMTR can get even higher.

A well-known problem, at least amongst the experts

Earlier this year I discussed a paper prepared by Treasury which examined this issue of how the tax and transfer system affects financial incentives to work. In the paper Treasury noted that most New Zealanders have EMTRs below 50% with only 6% experiencing EMTRs over 50%.

The Treasury paper noted families with children are more likely to face higher EMTRs. Single parent families are particularly hard hit, with 30% of single parent families having EMTRs greater than 50%, and in some cases higher than 100%.

The lesson from the Treasury paper, and Ganesha’s substack, is that over time we have built a complicated, interlocking and confused system of means tested benefits.

We also have a not unreasonable expectation that people receiving benefits should attempt to work. However, the EMTRs of 70% or even more resulting from the abatements applied by means testing may make the actual return for any additional hours minimal.

In such situations, and faced with such disincentives, why would people work extra hours? What Ganesh’s substack hammers home is the need to be step back and have a real think about what we are trying to do with our work and benefits system and the interaction between tax and benefits.

Inconsistent approach

This problem has also been recently highlighted by the changes to the FamilyBoost initiative where the Government is reducing the abatement rates and increasing the abatement thresholds with effect from 1st October because the initiative – a key election promise – wasn’t reaching as many people as expected.

FamilyBoost is now available for families earning up to $229,100, well above the low threshold impacting families like Alex and Taylor. Understandably this has led to questions as to whether such families should be receiving assistance. Which is perhaps a bit rough, because raising children is not cheap.

A long-standing issue ignored for too long

In my view the Government is sending wildly opposite messages here. In many cases, the abatement thresholds have not been increased with inflation for some time. Therefore, with the rise in cost of living and rent in particular, people on lower incomes are struggling to keep up.

This is leading to more applications for supplementary assistance, which then feeds this spiral of higher EMTRs applying. It’s time for someone to grasp the nettle and say, “Well, this is really not achieving very much. Let’s go away and rethink it.”

Strange bedfellows?

Now, in the strange story basket this week is one where the Green Party and the Taxpayers Union have found common ground.

This curious tale is a byproduct of the local government election in Wellington. Two Green Party candidates running there are proposing a change to the taxation rating system. Instead of taxing properties on their total value, including improvements, the Green party candidates want to base rates solely on the value of the underlying land.

Jordan Williams, the executive director of the Taxpayers Union, came out and endorsed this approach on the basis that the current system effectively penalises developments by taxing improvements.

Meanwhile the Green Party candidates are looking to target what they see as land banking, where people are just simply sitting on land, not paying rates. The move is intended to encourage the land to be used for productive purposes, whether it’s more housing or alternative commercial developments.

It’s interesting to see very opposite political bedfellows come together on this point. It’s probably a once in a Blue (or Green) Moon but certainly it’s an example where a principled tax approach can result in a common approach from what appear at first sight to be some unlikely bedfellows.

Is that a business you’re carrying on? New Inland Revenue guidance

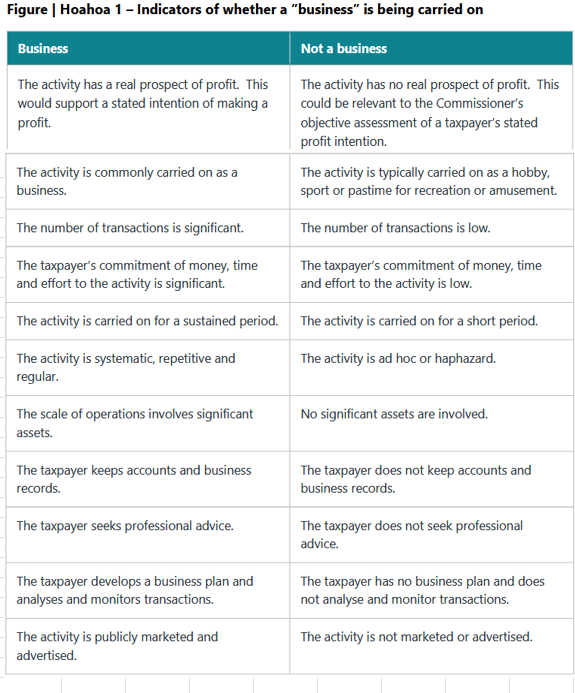

Inland Revenue has released a draft interpretation statement for consultation on the important issue of when and whether a taxpayer is carrying on a “business” for income tax purposes.

As the draft interpretation statement notes:

“It is important to understand if you are carrying on a business, and when that business is being carried on, because carrying on a business is a requirement of many provisions in the Income Tax Act 2007. In particular, an amount that a person derives from a business is included in a person’s income for tax purposes and the person is allowed a deduction for expenditure incurred in carrying on that business.”

This draft statement is part of a project whereby Inland Revenue is modernising and updating its previous guidance, which in this particular case goes back to 1971. Unless otherwise stated these updates are not changing any previous interpretation.

The leading decision in this area is Grieve v CIR (1984) 6 NZTC 61,682 (CA). In Grieve the court ruled that deciding whether a taxpayer is in business involves a two-fold inquiry as to the nature of the activities carried on and the intention of the taxpayer in engaging in those activities.

The draft statement (which runs to 46 pages including references) discusses these relevant factors in depth but it also has a useful summary.

Overall, this is a useful guide to a commonly asked question.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

the first ever sentencing for possession of tax evasion tools.

Inland Revenue’s draft long-term insights briefing currently out for consultation has generated quite a bit of debate. The paper discusses the future shape of the system and how to fund the rising cost of superannuation and related health costs.

Sir Roger Douglas has now entered the chat as he, together with Professor Robert MacCulloch of Auckland University, have released a paper titled How to change the welfare state from a taxation to a savings-based model. In some typically bold thinking from Sir Roger, the proposal is to dramatically change the tax system, and instead of trying to raise additional tax to meet these costs, take a completely different approach.

A tax cut or something else?

Sir Roger and Professor MacCulloch suggestion is for the first $60,000 of income to be tax free. Based on current tax rates, that’s at least a $10,000 tax cut for everyone with income of at least $60,000. Instead, those taxes would be directed into mandatory savings accounts for health, pensions and other risk cover. These would then be supplemented by employer contributions (effectively a social security tax, although not specifically described as such) with the trade-off for these contributions being a cut to the corporate income tax rate.

They’ve released a short paper outlining their proposal (there’s also a more detailed paper that Sir Roger and Professor MacCulloch produced in 2020). The paper starts with an analysis of the forthcoming rise in health and superannuation costs and the need to take a long-term view on addressing this issue. Sir Roger and Professor MacCulloch take the view that the conventional approach, raising taxes to meet these costs isn’t going to cut it. Something more dramatic is needed.

Taking the axe to corporate welfare

In addition to the proposed mandatory savings accounts, Sir Roger and Professor MacCulloch propose cuts to what they call corporate welfare and grants to high earners. The cuts include the removal of screen production grants, ending accelerated depreciation allowances for industries such as forestry, fishing and bloodstock, withdrawing winter energy payments to wealthy households and KiwiSaver subsidies to higher earners. They also propose ending the “favourable tax treatment to owners of rental housing” but this isn’t defined. I’d be very intrigued to know more about what exactly they’re driving at there. All up Sir Roger and Professor MacCulloch suggest these could save over $12 billion annually.

Yeah, but…

This is quite a radical proposal which would be quite a shock to the system, and I’d be very interested to see what other economists think of it. One hurdle I see is with the proposals aimed at introducing competition into the provision of health services. This is a perennial problem for our economy. We are just 5.2 million people and 2,000 kilometres away from the nearest neighbour. Competition in that context is always going to be difficult but it’s an issue we need to address, not just in this context but across the economy as a whole, because I think it’s a major problem for our economy.

Overall, you can never say that Sir Roger Douglas would die wondering. As a RNZ report noted it’s a bold plan and I recommend reading the summary paper. Bear in mind some of what it proposes in terms of removing subsidies such as the Government’s KiwiSaver contribution for high-income employees are now actually happening.

What about increasing GST?

On a more conventional approach Inland Revenue’s briefing paper includes a discussion about the implications of raising GST from 15% to 18%. Last Thursday I spoke with Wallace Chapman of RNZ’s The Panel about this proposal.

The Inland Revenue briefing paper notes the suggested GST increase could raise $5.5 billion of tax annually. This is because, as I explained to Wallace and his panellists, GST is an enormously efficient tax. It does meet the classic broad based low-rate approach. You broaden the basis as widely as possible so you can have as low rate as possible. Furthermore, because we have no exemptions, our GST is enormously efficient. So really if you were thinking of increasing taxes your first point of call would be to raise GST.

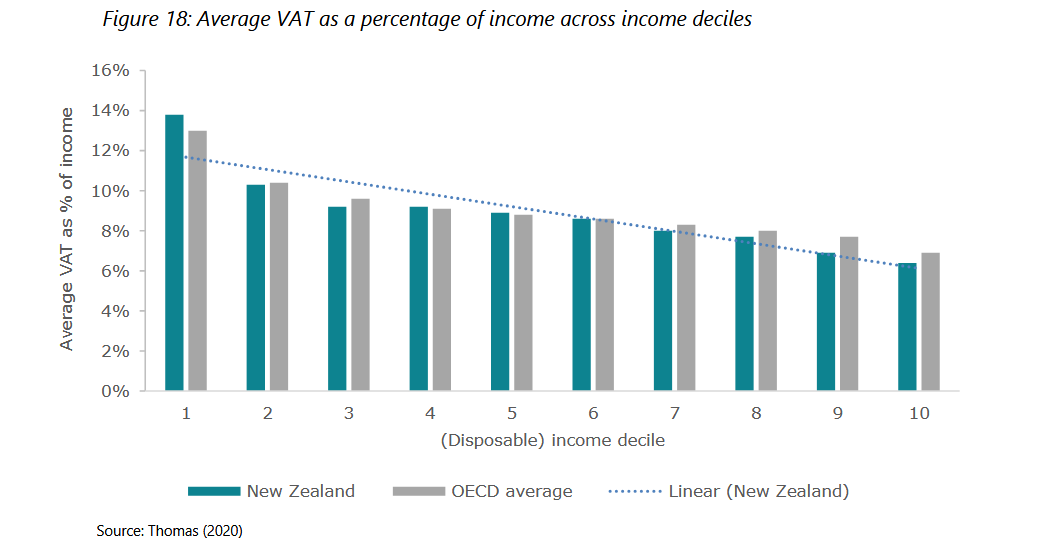

A regressive tax

The problem is though, as Inland Revenue pointed out and as Holly Bennett, one of Wallace’s guests immediately jumped on, GST is a regressive tax. There’s quite an interesting analysis of this in the Inland Revenue briefing paper. The paper notes that GST or VAT (value added tax) is regressive relative to income.

According to the organisation of Economic Cooperation and Development (the OECD), the average GST to income ratio declines from 10.4% in Decile 2 to 6.9% in Decile 10. We follow a similar profile with our GST to income ratio declining from 10.3% in Decile 2 to 6.4% in Decile 10.

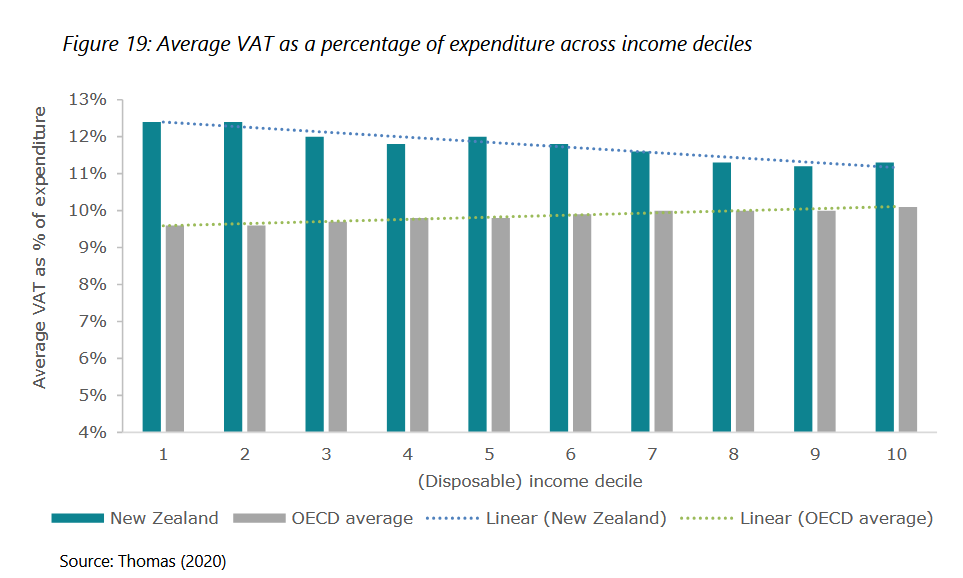

The Inland Revenue paper also considers the effect of GST relative to expenditure. In this instance GST or VAT is slightly progressive for most OECD countries because of the exemption of tax of necessities such as food and some sanitary products and various other Items which make up a very large proportion of the consumption basket of lower income households. However, our GST, because we don’t have any such exemptions, is mildly regressive.

Increasing poverty?

As Holly Bennet (one of Wallace’s panelists) was quick to also point out, an effect of GST increases is to increase the poverty headcount. According to Inland Revenue, based on the 2015/2016 Household Expenditure Survey GST “increased the imposition of GST in New Zealand increased the poverty headcount by 4.7%, the poverty gap by 1.7%, and the squared poverty gap by 0.8.” What’s worse is that the effect of those increases is higher than the OECD averages of 3.1%, 0.7%, and 0.3% respectively, again, because we have no exemptions.

The GST dilemma

So, raising GST results in the dilemma that it would raise a lot of revenue very quickly but hit lower income families harder. The suggestion in Inland Revenue’s paper is that there should be a compensation increase in welfare benefits for low-income families. They suggest that would probably cost maybe $440 million a year in total.

Readers and listeners may recall that last year a guest was Andrew Paynter, one of the Tax Policy Charitable Trusts co-winners. We discussed his proposal of raising GST to 17.5 % and introducing a GST refund tax credit for low- and middle-income earners.

Coincidentally or not, Andrew works for Inland Revenue, but there’s a worldwide trend looking at this particular issue. For example, the International Monetary Fund released a paper last year Designing a Progressive VAT which suggested a point of sale credit for low-income families. As the Inland Revenue paper notes Canada and Thailand have point of sales/refund credits for low-income earners.

Some form of capital taxation also needed

If you were adopting a conventional approach to addressing the rising expenditure gap, then raising GST is the most likely approach. My personal view is we also need to have some form of capital taxation because as I explained to the Panel, not only do we have rising health and superannuation costs, the cost of dealing with the impact of climate change, is rapidly accelerating.

This week Forsyths Barr and the Insurance Council released data that showed that over 40 years, the average annual cost of dealing with weather related events was $203 million. However, in the latest 10 years those costs had risen to $606 million annually and the five-year average is now $952 million per annum. Currently Tasman is spending $500,000 a day repairing its roads in the wake of the recent floods.

So climate change is having a huge impact now and there are a huge number of properties – 220,000 in total – presently worth over $180 billion, which are located within coastal inundation and inland flood zones. More than a quarter of those are in the Canterbury, Tasman, Gisborne, West Coast and Nelson regions. Those last four of which have all had severe weather events in the last year.

A quid pro quo

Protection against climate events will be another growing demand, particularly since for most people their property is their principal capital asset. This is where I think some form of capital taxation/capital gains tax is perhaps appropriate because if the Government and local councils are expected to spend more to protect capital assets, the quid pro quo must be that those capital assets become taxable.

Working for Families – a correction

Moving on, last week I talked about the changes to FamilyBoost and I noted that there had been no change to the threshold for Working for Families. That was actually incorrect. A kind reader from Inland Revenue pointed out that the Working for Families threshold will increase to $44,900 with effect from 1st of April next year its first increase since July 2018. Thanks for getting in touch and apologies for my error.

I’ll just simply add that on an inflation adjusted basis, that threshold should have gone up to something like $54,650 so it’s still way short of where it should be.

In any case the effect of the increase in the threshold from$42,700 to $44,900, which remember is for a family’s income, is mitigated by the increase in the abatement rate went up from 27.5 cents per $100 to 28 cents per $100.

Furthermore, the other point I made last week was about the focus of the FamilyBoost towards higher income families. That point doesn’t change just because the threshold for Working for Families has been (slightly) increased.

A New Zealand first

A recurrent theme this year is how Inland Revenue has increased its focus on chasing non-compliance. The latest example is the Auckland man who has become the first person in New Zealand to be convicted and sentenced for aiding and abetting his company’s possession of the electronic sales suppression tools.

Now these sales suppressions tools basically alter the Eftpos record so they’re very much about suppressing income and basically trying to defraud the taxpayer. In this case, Gurwinder Singh has been sentenced to seven months home detention on tax evasion charges, including the charge of aiding and abetting this company for possessing electronic sales suppression tools for the purpose of evading the assessment and payment of tax.

All up, Singh’s tax evasion amounted to $198,500. Apparently one of the things he was also doing was although he had four employees, including himself, he was only reporting PAYE returns for two staff. So, some obvious and not so obvious tax evasion was going on here. Anyway, this is the first time the new law in relation to electronic sales suppression tools has been applied. Would-be fraudsters have been warned.

The pitfalls of schedular payments

As often mentioned, Inland Revenue turns out vast amounts of very interesting and helpful material. Once such source are its Technical Decision Summaries about issues or rulings that Inland Revenue has encountered.

One TDS released this week is a private ruling in relation to the application of the schedular payment rules.

This involved a company wanting to make use of offshore personnel to act as directors in New Zealand. The question of interest here is a reminder that if you are making payments to overseas persons, they may, even if they are contractors, be subject to non-resident withholding taxes/schedular payments.

That’s why this one is useful. This ruling explained why those provisions would not apply. But typically, if they do apply then 15% withholding tax can be deducted which can come as a shock to some overseas persons. This is a useful ruling on a point which we often encounter but is one of those cases where I suspect the compliance isn’t always as diligent as it could be.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue releases submissions on the taxation of not-for-profits.

A major report on climate adaptation ducks a key issue.

Last week, it emerged that the Finance Minister, Nicola Willis has sought advice from Inland Revenue and Treasury on whether New Zealand’s major banks are paying enough tax.

According to a release on policy work being undertaken by Treasury and the Reserve Bank, the Finance Minister “and the Minister of Revenue have commissioned Inland Revenue to review whether income tax settings are applying correctly to banks for potential consideration at Budget 2026.”

This is a clear implication that some changes may be ahead, or are being considered for next year’s Budget, which coincidentally is also an election year.

“A wide range of options”

It appears Inland Revenue are considering, “a wide range of options.” What’s often brought up with banks is whether they have excessive levels of profits and therefore should be subject to a windfall tax.

The debate around excess profits and windfall taxes frequently arises. As the Greens rather ironically pointed out, Margaret Thatcher introduced a surcharge for banks in the early 1980s, when the monetarist policy that the British Thatcher government had adopted meant that increases in interest rates would naturally flow through to higher profits for the banks.

Thatcher, together with Chancellor of the Exchequer (Finance Minister) Geoffrey Howe took the view that as the banks were profiting from monetarism they should pay additional tax as a result. However, windfall taxes are highly problematic in terms of defining.

Clearly it would be perhaps appropriate to align settings with Australia. An alternative therefore might be to adopt the Australian bank levy.

A 0.6% levy on banks with liabilities over A$100 billion has been in place since 2017 and there have been calls to increase it. If you’re aligning the treatment of the big four banks with what their parents are subject to in Australia, then politically you have probably removed one objection to any such surcharge.

Another area which could be considered are the thin capitalisation rules. That is, the level of debt that banks would be allowed to carry and still claim deductions.

The general rule is that if the debt/asset threshold exceeds 60% then interest restrictions are put in place.

There is a lot going on in this space around the world. Last year the OECD’s corporate tax statistics report said that there are now over 100 interest limitation rules in place, which is up from 67 jurisdictions having such rules in 2019.

Obviously, the Government considers there is some scope for tweaking the tax rules, but this is a political matter and ACT leader David Seymour has already put the kibosh on that. Whether that means the Government will not proceed, or that it reaches out to see if it can get cross party support on any proposals, we’ll have to wait and see. This is an interesting development which we will watch with some interest.

FamilyBoost scheme changes

The Finance Minister also announced on Monday that there would be changes to the FamilyBoost scheme which gives eligible families a rebate on fees paid to early childhood education centres. Take up has not been anywhere near as high as was expected or promoted when the proposal was made.

In recognition of this, the Government decided to revamp the scheme and has lifted the threshold for maximum eligible income from $45,000 per quarter to $57,286 per quarter. In other words, from $180,000 per annum to $229,000 annual household income.

The amount that can be increased has gone from 25% to 40%, up to a maximum of $1,560 per quarter. There’s also a reduction in the abatement rate from 9.75% to 7% for household income over $35,000 per quarter.

The intention is that these changes will come into effect for childhood education costs incurred in the current quarter from 1st July to 30th September onwards. Legislation will come be coming through on this.

As the tireless Craig Renney, Chief Economist for the Council of Trade Unions, has noted, this change is very generous and is weighted towards higher income families.

What about Working for Families?

Looking at the increased abatement thresholds coupled with reduced abatement rate, I do not understand why the Government has done nothing in relation to increasing the abatement threshold for Working for Families, which still remains at $42,700 for total family income.

Although there were changes in this year’s Budget (including an increase in the abatement rate to 28%) this threshold has not been changed since 1st of July 2018, seven years ago now.

The Government is sending mixed messages. Both measures – Working for Families and FamilyBoost – help working families, but it appears only high-end families have the issues of abatements and the impact of high effective marginal tax rates addressed.

There would probably be greater cost involved in lifting thresholds and/or reducing abatement rates for Working for Families, but whoever said politicians would be consistent in their approach?

To me the changes create a weird scenario. But FamilyBoost was a Government election commitment, so it’s understandable the Government is trying to make it more accessible.

Inland Revenue releases submissions

At the start of this year there was a lot going on in relation to the not-for-profit sector, with many thinking the Government was looking to change the tax treatment of this sector and in particular the exemption from business taxation for businesses run by charities.

It subsequently backed away from that although the issue of the taxation of mutual transactions of associations, clubs and societies is still under review.

Last Monday (it was a busy old day) Inland Revenue proactively released the submissions it received on the issues paper Taxation and the Not-for-profit Sector it sent out for consultation in February. It received 826 submissions, which is quite a number, and it has published all these submissions where permission has been given. It’s also produced a four-page summary of the common themes in the submission.

One was that consultation needed more time, which I totally agree with. Others felt the Government was looking at the wrong end of the issue in that not-for-profits provide a net benefit, not a net cost for the Government, because they save government expenditure.

Another was that the issues paper lacked clarity about what was the problem to be addressed, with many submissions suggesting the focus should be on the bad actors. All good points in my view.

What about the charity business exemption?

On the charity business income exemption, there were differing views as to whether in fact charities had a competitive advantage.

Economists generally agreed with Inland Revenue‘s view that no advantage existed. But other submitters disagreed. There were questions about the complexity of defining the issue at stake, with some submitters skeptical about how much revenue could be raised.

There were also suggestions that maybe a minimum distribution rule could be a more effective policy response.

There was a mixed response on the issue of donor-controlled charities. As usual, some acknowledged there were concerns on this, but others thought again that the existing regime was rigorous enough and any changes would impose increased compliance costs.

On the vexed issue of not-for-profits and friendly society transactions, the view was that these should be removed from the system and member subscription should remain non-taxable.

In relation to a de-minimis tax free threshold “There was near universal support from those that submitted on the mutuality topic that the $1000 income tax deduction was too low and should be increased.”

Overall interesting to see these responses. As noted above, consultation has just closed on the application of the mutuality principle to transactions of associations, clubs and societies. There has been strong pushback on this as well so it will be interesting to see what emerges.

This is a group that’s been put together to give the Government some guidance on developing a framework for dealing with climate adaptation. It’s a short report, only 16 pages and well worth the read.

The report’s opening paragraphs dive right in:

“The group considers there to be an urgent need to change the way New Zealand adapts to climate change. New Zealand is already experiencing the impacts of climate change, but it is currently underprepared. This is leading to larger and more frequent recovery costs, unmanaged financial strain and disproportionate impacts on some groups.

Climate change will continue to bring substantial financial costs for the country. Failing to act or delaying decisions will not avoid or reduce costs that New Zealand governments, businesses and individuals face.”

That’s an on the nose and in my view accurate summary of the position we face. As I’m recording this podcast the Nelson/Tasman region is under a state of emergency for yet another storm that is expected to hit in the next few hours. This is just the latest experience of the “impacts of climate change. Achieving “a consistent approach”

The report considers that “New Zealand needs a consistent approach to decision making that is well informed about the risks.” To achieve this approach, it suggests there are three key areas which need to change.

Firstly – New Zealanders need to have fair warning about the way natural hazards could impact them, so they can make informed decisions too.

Secondly – New Zealand should take “the broadest interpretation of a ‘beneficiary pays’ approach to funding the increased investment and risk reduction because of climate change. This would mean that those who benefit most from these investments contribute more.”

Finally, people and markets should adjust over time to a change in climate. The adjustment is already happening. Insurers have been raising premiums and making it clear that there are areas where the insurance risk is greater than they are comfortable with.

The question that the report raises is the length of this transition period beyond which “people should not expect buyouts”. In its view

“The Group acknowledges there is no right answer to how long a transition should take. However, the Group considers that a transition period of 20 years would appropriately balance the need to spread costs with creating the right incentives to act.”

Who pays?

However, the report is pretty silent about the meaning and extent of what it refers to as “financial assistance” which, it suggests, does not continue beyond the transition period. Neither of the words ‘tax’ or ‘levy’ appear in the report and in my view, that’s kicking the can down the road.

The report is right to highlight the scale and urgency of climate adaptation, but it should have gone further and said, “we need to prepare for this, we suggest that it’s going to need either higher taxation or a climate levy.”

By doing so, the issue comes up for discussion. Instead, it has rather ducked that point.

This has drawn criticism from a climate policy expert, Professor Jonathan Boston, who said phasing out government assistance for climate adaptation and property buyouts would be “morally bankrupt.”

Although he agrees we should not be creating incentives for people to stay in risky areas, he feels that a 20-year transition period is not long enough, and ongoing government support will be needed. I agree with both those points.

The costs of climate change are happening now

The issue of how governments manage rising superannuation and health costs is important. But I think the more immediate financial impact we have to address is climate adaptation.

And unfortunately this report, although it clearly spells out the risks that we’re facing and the need to develop a framework to respond, ducks the key question of “who’s going to pay for this, and how do we finance that transition?”

As I have said repeatedly, this is going to involve some form of tax increase or specific levy.

The cost of climate adaptation is an issue where we really do need all the politicians to put party politics aside and address the longer-term issues – that climate adaptation will involve huge costs which presently falls on local councils who are in no position to fund the burden.

It is going to require central government support, in the form of specific tax or levy.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day and best wishes to everyone in Nelson/Tasman, or anywhere else affected by the bad weather.