- Renting rooms to flatmates

- Provisional tax

At the end of last week, the Government announced a surprise tax measure for North Island businesses hit by recent flood damage. The measure means that they will not have to pay tax on insurance or compensation they might receive for any damaged buildings or plant or equipment.

As the Revenue Minister David Parker pointed out, generally speaking such payments are treated as taxable income. Recognising another tax bill is the last thing any businesses affected by the floods needs, the Government has decided to adopt a measure which was used previously following the Canterbury earthquakes and the Hurunui-Kaikoura earthquakes. It essentially allows a deferral of the tax on the compensation payments received to replace damaged or lost buildings and plants and equipment.

What happens is instead of a depreciation recovery (income) happening because you’ve received a payout, there’s a rollover relief which will defer the recognition of that income on the basis that there is a commitment to rebuild or replace the destroyed buildings or plant. There is a key difference here as to the measures used previously for the earthquakes, and that is there is no requirement for any replacement buildings to be located in the same region. This is because in some cases managed retreat is now being considered. For example, where a building which is in the Hawkes Bay has been destroyed or severely damaged by Cyclone Gabrielle, the business owner may decide to relocate to a different region. In this case the rollover relief would apply an exemption.

This is a good measure to see. The formal legislation will be introduced shortly probably around the time of the Budget, I might imagine, along with the other budget measures.

What happens if you rent a room to a flatmate?

Moving on, Inland Revenue has released an interesting draft Questions We’ve Been Asked consultation on how the bright-line test might apply to where a person rents out a room in their home to a flatmate. Alongside that there’s another Draft Questions We’ve Been Asked relating to the extent to which a person can claim deductions for expenditure incurred in deriving the rental income, when they’ve rented a room to in their home to a flatmate.

As always, there’s a bit of detail in these, but in summary, in relation to claiming deductions or costs incurred in renting a room out to a flatmate, the draft consultation concludes that deductions can be claimed to the extent that they’re incurred in deriving gross income. The rental income will be assessable and the amount of expenditure needs to be apportioned between private use living in the house and income earning use, rental income from a flatmate.

The draft consultation suggests that apportionment, based on the use of physical space, is a reasonable basis on which to determine what represents an income earning component of expenditure and therefore calculating the deduction available.

Interestingly, the interest limitation rule will not apply, if the land is used predominantly for the person’s main home. Similarly the residential ring fencing rule won’t apply if more than 50% of the land is used for most of the income made by the person as their main home.

The general rule here is that it’s a matter of fact, whether the dwelling is the person’s main home. You must consider all the circumstances. But the fact that you are renting out a room in, in your home to a flatmate while you are living there will not preclude the home being the person’s main home. And on that basis, the interest limitation and residential ring-fencing rules should not apply.

Which leads on to the second question as to whether then the bright-line test might apply. If so, would a person who is living in a home and rents out a room to a flatmate, qualify for the main home exclusion.

This draft consultation concludes that, yes, that person should qualify for the main home exclusion. Again, whether it’s a home is a matter of fact, and you consider where the person resides and has a fixed presence. Just a reminder, though, that there is a slight twist in for land acquired between 29th March 2018 and 26th March 2021. The main home exclusion applies where for most of the days in that bright-line period, the land is mainly used as a residence by the person.

But there may be situations where that in fact is actually incidental to the main purpose of carrying on rental activity. I think one of the questions there would be if you are starting to rent out more than one room if say there are four bedrooms and you’re renting three out. The question might then start to arise as to whether the main home exemption would be available. Anyway, it’s good to see some guidance on this as this question no doubt is going to pop up from time to time.

It’s provisional tax payment time

Monday is the due date for payment of the final instalment of Provisional tax for the March 2023 income year. The key thing to keep in mind here is if you think your residual income tax for the year to 31st March 2023 is going to exceed $60,000, then you need to make the full payment on Monday. Otherwise, use of money interest will apply on the unpaid provisional tax.

Incidentally, the interest rate on tax paid late rises to 10.39% with effect from Tuesday. Also, bear in mind, in some cases, you may also face late payment penalties, an initial 1% on the tax paid late. And then if it’s not paid in full within seven days, a further 4% is levied. Use of money interest continues to apply on top of these penalties. So, paying your tax late is an expensive proposition.

I’ve been dealing with Provisional tax for almost 30 years now, and it’s still something that confuses me from time to time. But the key point to always keep in mind about the latest iterations of these rules is that if your residual income tax is going to exceed $60,000 for a tax year then you need to pay the liability in full on the third provisional instalment date.

Not self-employed? You might still have to pay provisional tax

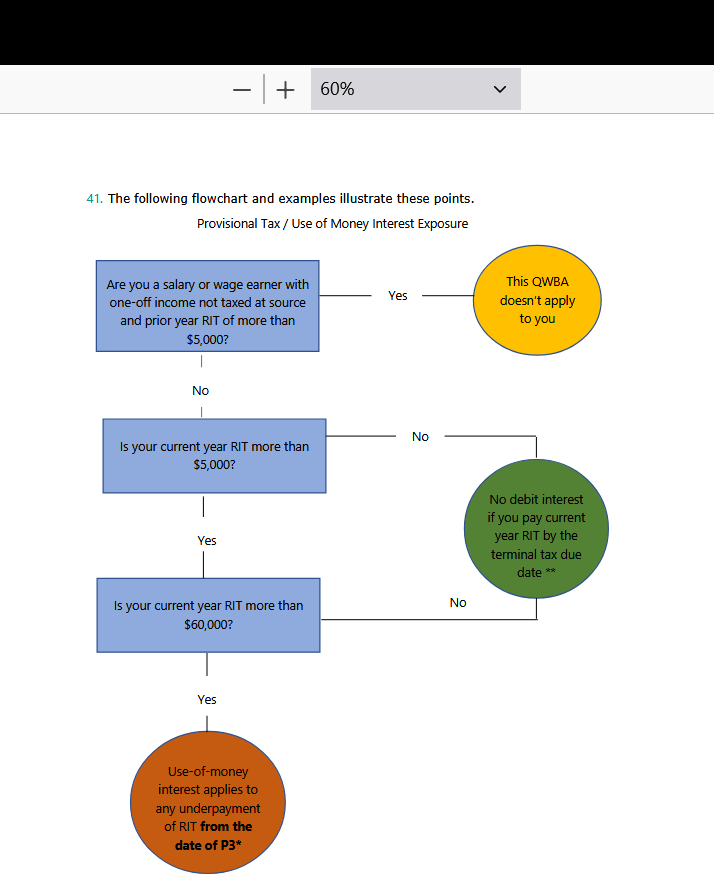

Usefully, Inland Revenue have released a Question We’ve Been Asked QB 23/05 on the impact of provisional tax for salary and wage earners who receive a one-off amount of income without tax deducted.

For example, this sort of income could be the gain from the exercise of shares granted under an employee share scheme, or from the transfer of a pension from overseas or a gain from a sale subject to tax under the bright-line test.

The general provisional tax rules are if your prior year residual income tax was less than $5,000, then this question you’ve been asked doesn’t apply. However, if it it’s more than $5,000, then you will be liable to pay terminal tax. No interest will run on that tax if it’s paid by the terminal tax due date, which is typically the 7th February following the end of the tax year for those without a tax agent, or the following 7th April for those with a tax agent.

As always in tax there’s a but, and the big but is what I mentioned a few minutes ago. What happens if your residual income tax exceeds more than $60,000? Then use of money interest at 10.39% will apply to any underpayment from the date of the third instalment, typically 7th May.

This is a really critical point if you have an untaxed gain such as those I mentioned, a gain under the bright-line test, transfer of a foreign superannuation scheme or as a result of exercising shares under an employee share scheme, and your tax liability exceeds $60,000, then you’re into the provisional tax payment regime straightaway and you have pay the tax in full on the third instalment date, typically 7th May, or this year, Monday 8th May.

Provisional tax does trip up a lot of people and but generally speaking, unless you’ve made a big gain, in which case you probably should have the funds available (or at least I’d hope so), you’ve got until the terminal tax date to meet those requirements.

One thing you need to do, by the way, if you are a salary earner and you have realised one of these untaxed gains, you should notify Inland Revenue as soon as possible before it starts its auto calculation assessment process. Otherwise, what might happen then is that they calculate you may be due a refund. They will make that refund and then you will have to repay the refund and the correct amount of provisional tax.

More feedback on taxing wealth

And finally, the controversy continues to around the Inland Revenue High Wealth Individual Research Project and the various related reports such as the Sapere report. There’s some fairly interesting commentary flying around on the topic. I thought Damien Venuto in the New Zealand Herald was on point when he said whether we like it or not, there is a reckoning coming around how we deal with tax.

The DomPost has an article by Susan Edmunds, which wasn’t online at the time of the podcast, talking about what was happening here and getting the views of Robyn Walker of Deloitte. Previous podcast guest John Cantin, as always, has some very insightful commentary. I think John makes an interesting comment about how the Sapere report and some other commentary brings in the question of benefits paid to taxpayers to provide an overall economic view. And he thinks that rather confuses the matter.

We don’t tax unrealised gains? Think again.

I want to repeat a point I made last week in the podcast and on RNZ’s The Panel. We currently do tax unrealised gains. The Foreign Investment Fund regime is the very best example of that. The taxation of pension transfers is another. When someone transfers an overseas pension to New Zealand, they’re not always realising it. In some cases, people are taxed on the value of the pension transfer but they can’t access it until they reach age 55. So that’s not really a realised gain. There are the financial arrangements rules which tax unrealised foreign exchange gains and losses. Overseas, estate taxes in essence tax unrealised gains. So, the concept is not unusual.

I remember looking at the various commentary reports from the 1980s and early 1990s when New Zealand was overhauling its tax system. There was a real debate going on around whether it was practical to have an accrual-based capital gains system. Wisely, the reports concluded that much as that might be economically accurate, it simply was practically impossible. Wealth taxes, quasi do that in a way, but a capital gains tax on an unrealised basis is, to all intents and purposes, a non-starter.

So, the debate will continue, and we’ll see a lot of politicking around that. Like Damien Venuto I’d like to see some hard answers on this from politicians about how they are going to address the issues of demography, demographic change and climate change.

And on that bombshell, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.