Scrutiny Week highlights issues of taxation of Big Tech companies.

There’s an election in November, and it is increasingly clear tax is going to be one of the big topics according to a recent Herald on Sunday editorial. One of the tax issues was highlighted by Jenée Tibshraeny in her column about criticism of the Inland Revenue and the Minister of Revenue’s approach to the taxation of tech companies during Parliament’s Scrutiny Week.

The Herald on Sunday’s leader was written with the Green Party’s tax policy in mind. Meanwhile, the Labour Party has previously announced that it will introduce a capital gains tax on residential and commercial properties, but it has also reiterated that it does not agree with the Green Party’s suggestion for a wealth tax.

Chlöe Swarbrick goes on the attack

None of this is a surprise to see in an election year. But it’s interesting to see that Chlöe Swarbrick, the co-leader of the Green Party, foreshadow part of the Green Party’s tax policy during Scrutiny Week. She took the Minister of Revenue, Simon Watts, and Commissioner of Inland Revenue, Peter Mersi, to task about the transfer practices of the large tech companies, the likes of Google, Uber, Apple, Oracle, etc. In particular, the large fees service fees that these companies paid to offshore associates.

Swarbrick also hammered away at Inland Revenue about leaving the tech companies alone but hitting small businesses hard over tax debts. A lose-lose situation for Inland Revenue there, by the by, but still an interesting political point to make.

What about royalty withholding taxes?

What was interesting to me about the Green Party’s questioning during Parliamentary Scrutiny Week was this question of royalty withholding taxes. The Minister and Commissioner were both asked why Inland Revenue did not appear to be pursuing the question of whether some component of the service fees paid offshore represented a royalty and therefore subject to what we call non-resident withholding tax (NRWT). The rate of NRWT applicable depends on the country to which the payments are being made. If it’s to the US, it’s 5%, to countries such as the Netherlands it’s I10%.

This was an issue picked up and examined in some length by Tax Justice Aotearoa in their Big Tech Little Tax report last year. It cited the example of Google New Zealand, which appeared to earn revenues in the year ended 31 December 2024 of $1.139 billion, but paid service fees of $1.052 billion to the Singapore related party, leaving an operating profit of just over $29 million. Service fees represented 92% of Google’s Google New Zealand’s earnings and similar numbers have been observed in the case of other tech companies such as Oracle.

Big Tech Little Tax 2026 update

In the same week, Tax Justice Aotearoa and the Better Taxes for a Better Future campaign have released an update of their Big Tech Little Tax report, which includes the latest results for the year ended 31st December 2025. Just to stick with Google New Zealand its December 2025 results showed revenues of $1.259 billion and service fees of $1.166 billion, again around about 92% of total revenue.

The update looked at Amazon Web Services and also Uber’s trading companies, Portier New Zealand Ltd (UberEats) and Rasier New Zealand Ltd (Uber Rides). Both companies paid substantial service fees offshore. Interestingly the authors think Facebook New Zealand is using a slightly different model to Google New Zealand because reported revenue of just under $175 million for December 2025 seems low given there are two million users in New Zealand.

A potential $600 million leakage?

Apart from Amazon Web Services, Facebook, Google and Uber the report includes updates for Microsoft New Zealand, Oracle, SAP New Zealand and Samsung. It estimates that if royalty withholding tax was applied to the estimated $11.4 billion of service fees paid overseas over a five-year period the NRWT payable would have been $634 million.

The original Big Tech. Little Tax report and its 2026 update were prepared by Nick Miller, a highly qualified former transfer pricing specialist at Inland Revenue and HM Revenue and Customs. The update also considered what would be the corporate income tax payable if these tech companies actually had a 5% return on sales. (Facebook’s return on sales in 2025 was 2.2% and Microsoft’s five-year trend shows a drift downwards to 4%). Based on the available data this could represent another $102 million over the 2021-2025 five-year period.

How did the Government respond?

In response to Chlöe Swarbrick the Minister of Revenue, Simon Watts, said the Government wanted to work within the Organisation of Economic Cooperation and Development Pillar Two Framework to find a lasting solution. But to all intents and purposes, the Pillar Two minimum global tax of 15% is essentially dead in the water following Donald Trump’s re-election as President of the United States.

There is also politics at play as I think the Government is not too keen to pick a fight with the United States tech companies and therefore attract the ire of President Trump. But notwithstanding that, applying the treaty royalty withholding tax rules might seem a more supportable action to take. If you’re talking about $600 million over 5 years, it’s not an unsubstantial sum of money.

A winning Green tax policy?

Politics aside it was an interesting exchange between the Green Party and the Minister of Revenue. It’s perhaps no surprise to see the Green Party’s tax package include a promise to enforce the current rules relating to withholding taxes and on these service fees and give Inland Revenue the funding to do so.

Politics and elections aside this is something I think Inland Revenue may push ahead with regardless of who forms the government after the Election. All tax jurisdictions around the world are starting to look very seriously at this question of transfer pricing and service fees going offshore. Across in Australia the Australian Tax Office tried to apply an embedded royalty argument in the PepsiCo case.

Managing tax debt – a lose-lose situation?

Moving on, Inland Revenue was also questioned during Scrutiny Week about its management of tax debt. As I said earlier, this is a bit of a lose-lose situation because it’s always going to be under pressure whether its approach is considered too hard or too soft.

As part of its campaign to collect debt, Inland Revenue has advised that it has started making pre-recorded calls or voicemail messages to taxpayers with overdue debt or late tax payments and returns. Inland Revenue by law must maintain the integrity of the tax system and as part of this it must pursue debt.

Lessons from Australia’s Robodebt scandal

That said, I’m not a fan of these automated calls as they can ignore existing arrangements in place which just upsets clients who think the matter is in hand. There is also the Australian experience with the so-called “Robodebt” scandal, which ultimately ended up with a Royal Commission and over A$2 billion legal settlement. I’m very interested to know what advice ministers have received regarding the Robodebt scandal in relation to the proposal to increase the use of AI by government agencies.

The problem with increasing the use of AI and going down the path of further automation is that tax has a lot of discretion around its administration, which is not specifically outlined in legislation and sometimes even internal administrative practice. There is always the issue of keeping taxpayers onside. Push too hard and you could see a Robodebt type scandal or taxpayers pushing back over priorities by asking “Why are you picking on me and leaving Oracle [for example] alone?”

Calling in Baycorp

Inland Revenue therefore has something of a dilemma around debt collection. But it still has a job to do to collect an enormous amount of tax debt. In addition to the automated calls, Inland Revenue is advising debtors may with tax debt which has been overdue for more than six months be contacted by Baycorp, which it has engaged as a third party debt collection agency.

According to Inland Revenue’s press release, this is intended to encourage earlier engagements on overdue debt, improved compliance outcomes and reduce the risk of debt escalating. All perfectly reasonable objectives in my mind. I just think the one concern that the Revenue has to be careful about, is with the increasing prevalence of phone and e-mail scams is how does it get cut through and connect with defaulters.

To me, a key objective for Inland Revenue with debt management is earlier intervention. If a taxpayer has missed a couple of GST and/or PAYE payments it should act immediately rather than let debt pile up.

Inland Revenue is torn between trying to enforce the law, collect the debt and also keep showing that it is acting equitably and preserving the integrity and people’s perception of the integrity of the tax system. Not an easy task, to be fair.

2026 home office and kilometre rates confirmed

Finally, a couple of Inland Revenue updates. The square meterage rate that may be claimed for home office use for the 2026 income year has been set at $57.30 per square metre, which is up from the previous rate of $55.60 in the 2025 income year. This square metre rate is based on the average cost of utilities and housing for the average New Zealand household. Taxpayers may in addition claim a proportional mortgage interest and rates or rent based on the percentage of floor area of the property used for business purposes.

Separately, Inland Revenue has also published the kilometre rates for the 2026 income year.

These kilometre rates are published annually after the end of the relevant tax year. But Inland Revenue also noted it’s considering publishing some further guidance on kilometre rates for the current tax year to 31 March 2027 because of the dramatic increases in fuel prices. In the meantime, taxpayers can use these 2026 rates as a reasonable estimate of the employee cost of using their private vehicle for business purposes for the current tax year.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[My apologies for my recent silence – I am presently recovering from RSV but hope to restore regular service shortly].

Scrutiny Week highlights issues of taxation of Big Tech companies

The last couple of weeks or so I’ve been talking about the changes to the threshold for the application of the Foreign Investment Fund (FIF) rules with effect from 1st April this year. The change means that if the cost of your foreign investment funds, typically overseas shares is less than $100,000, you do not need to enter the FIF regime. Instead, you only need to return dividends, and, if you’re a share trader, any capital gains. Notwithstanding the new threshold a taxpayer can continue to elect to opt into the FIF regime.

The new threshold drew some interesting commentary in the media with some noting the change seems to favour the wealthy. The Minister of Revenue, Simon Watts, rejected that assertion by saying that he would not see people holding $100,000 or less of shares as wealthy.

So who holds FIFs?

Many of our clients have investments within the FIF regime. and the majority of them acquired those interests when they were either working overseas on an OE or before they migrated here. In many cases, they’re professionals who took advantage of tax-preferred schemes, such as the United Kingdom’s Individual Savings Accounts, or maybe acquired shares through employee share ownership plans.

It’s also worth noting that many overseas jurisdictions have considerably deeper capital markets than here, so investing on the stock market is perhaps more common, although the advent of KiwiSaver and Sharesies has made a huge difference.

The FIF regime – a quasi-wealth tax

When I’m looking at this issue, it’s not so much whether $100,000 of overseas investments can be considered wealthy although someone holding that level certainly would be above average wealth, but rather how the clients see the FIF regime. It’s very unique compared with how overseas Jurisdictions particularly in how it taxes on an unrealised basis. This makes it very much like a wealth tax. In fact, that’s how I describe it to overseas clients and advisors, most of whom come from jurisdictions with capital gains tax regime which mostly work on a realised basis.

I believe there’s a considerable amount of non-compliance with the FIF regime. We regularly file voluntary disclosures of FIF income for clients, mainly because clients are completely unaware of its scope and operation until something triggers it. They may come across something or in some cases Inland Revenue catches up with them and asks a few pertinent questions.

A welcome increase

Against that background, the increase in the minimum threshold to $100,000 to me is welcome. I think the expansion of the FIF revenue account method for unlisted shares is also welcome because it aligns with a laypersons concept of how a capital gains tax regime operates.

Anyone who has migrated here from Australia, the United Kingdom or the United States, will have encountered capital gains taxes. And one of the things about capital gains tax is a realisation is a potential taxable event. My observation is that most people when they’re thinking about tax and how systems work, it’s really around money flows. If money comes in, they think that might be a taxable event – if they receive an inheritance, for example. But more importantly, if they are selling stocks or overseas properties, there’s an awareness it could have tax consequences.

Is a Capital Gains Tax too complex?

A frequent counterargument to a capital gains tax is its complexity. My response to that is the FIF regime is complex and as I said above, its unrealised basis of taxation counter intuitive. Alongside that consider the bright-line test, the treatment of commercial property, then associated property transactions for those dealing in land or builders, etc together with other carve-outs for farmers and main homes. In short, the existing tax treatment system is complicated. And that’s before we get to the financial arrangements regime.

I’ve always been of the view that perverse as it may seem to opponents, a capital gains tax regime would probably simplify matters for many people. Now, that’s not to say there’s always devil in the detail. We talk about that all the time. But I think in terms of understanding where people think they may have compliance, a CGT scheme is much more understandable than the foreign investment fund regime.

What to get GST for its fortieth birthday? An Inland Revenue issues paper.

Moving on, Inland Revenue has issued an officials issue paper for consultation on current GST issues, just in time for the introduction of GST’s 40th birthday on 1st October. GST is a very important tax for the Government because of its broad base and relatively low rate compared to other jurisdictions. This makes it an extremely efficient tax gatherer. For example, the Budget projected GST revenue of $33.1 billion for the year to 30th June 2027. To put that in context this is expected to be just over 22% of the total forecast government revenue for the year.

GST is not a simple tax though; this is perhaps one of those common misconceptions about it because of its broad reach. Like all taxes there are interesting and complex issues on the boundaries and with its operation. As paragraph 1.2 notes

“While the GST system generally works well, a number of issues have been identified where the legislation produces outcomes that do not reflect the underlying policy or intent or where technical changes could improve the way the system operates. Addressing these issues would improve the certainty, efficiency, integrity and fairness of the GST rules.”

Eight issues under review

The paper reviews eight topics it thinks may merit further consideration. It starts with the question of the definition of dwellings and commercial dwellings, which is quite important for GST purposes because commercial dwellings, if a person is in long-term accommodation, GST applies at 60% of the standard 15% rate, or effectively 9%. Inland Revenue’s question is whether the definitions of what represents “commercial dwellings” can be improved?

This might seem a little arcane, but commercial dwellings definition could impact emergency housing and student accommodation. You can see why it’s relevant.

Chapter 3 reviews the issue of electricity being exported to the grid from residential premises and what happens if the surplus being exported to the grid is made from a GST registered person. Again, quite a technical issue, but it’s something that’s going to happen more often. Bear in mind that income tax changes have been made to treat those proceeds or offsets as not being taxable for income tax purposes.

Chapter 4 reviews some GST cross-border issues in relation to non-residents suppliers who are usually making supplies to GST registered entities in New Zealand and the practical effects of requiring registration in certain circumstances.

Chapter 5 considers the issue of correcting errors and inaccuracies. Apparently, our legislative framework is a little less coherent in this approach than overseas jurisdictions. There are also some inconsistencies with other legislation. For example, generally speaking, refunds for more than four years ago are not permitted for income tax purposes. However, in some GST cases, it’s possible to make claims going back eight years. Understandably, Inland Revenue wants to resolve that discrepancy.

Chapter 6 is mostly technical and discusses a range of miscellaneous changes including claiming GST on pre-registration expenses and whether a group GST registration should have a separate IRD number rather than the IRD number of the group representative?

Modernising the GST Act

Chapter 7 is something I’d probably have put first, and that is modernising the Goods and Services Tax Act 1985 which is now over 40 years old. A lot of amendments have been passed in that time so it’s not easy to follow.

The issues paper asks whether there should be a complete rewrite as was done with the Income Tax Act? It concludes it’s not necessary partly because Inland Revenue doesn’t presently have the resources for what would be a fairly major move. I agree with that conclusion.

On the other hand, reordering the act and tidying it up and presenting it in a more cohesive manner is something I think should be done. For example, section 20 deals with the “Calculation of tax payable” and currently runs to more than 35 subsections. I believe restructuring and renumbering the act would be strongly supported by tax specialists.

GST and international business events

Chapter 8 has an interesting review about the GST treatment of business events such as conferences and conventions supplied non-resident businesses. This is an issue raised by parts of the tourism industry. The paper suggests this is perhaps a zero-sum game in that a non-resident business could register for GST and reclaim some of the input tax on business event services. Apparently, Singapore and Australia have specific GST rules for business event services and the paper canvasses whether similar rules could apply here.

International developments and improving GST administration

Chapter 9 considers international developments in GST/VAT administration. This primarily considers digital reporting tools and improving administration of the tax such as the use of e-invoicing. The paper notes that when looking at what’s happening in the rest of the world in digital reporting, we may have slipped behind in terms of efficiencies noting “developments suggest that New Zealand’s current approach is more cautious than some comparable jurisdictions.” Should New Zealand follow the lead of countries such as Singapore and the United Kingdom?

This chapter considers an interesting point from Australia where if someone is defaulting on their GST returns, they are moved from reporting quarterly to reporting monthly as a means of improving debt collection. The view is increased reporting means better debt intervention. We already have bi-monthly reporting as the standard and monthly reporting is also available. (As an aside I think quarterly reporting as in Australia and the UK would be helpful).

I understand the thinking, but I think it’s better for Inland Revenue’s own systems to be picking up GST defaults much sooner, say if two successive GST returns are in default. I think you don’t need legislative changes to enable this, rather Inland Revenue should use the tools it already has,

What about GST on fees to managed funds?

Overall, there’s quite a lot to consider in this paper. I am surprised to see that the question of GST on fees charged to managed funds is not included. Back in September 2022, the last Labour government introduced a proposal to apply GST on such fees. This was to clarify the ad hoc approach which meant newer entrants to the market were paying GST, but older market operators were not.

The proposal provoked a storm of protest resulting in the Government backing down very rapidly, within 24 hours on the proposal, instead leaving it to Inland Revenue to ‘review’. In terms of major issues, I would have thought this was probably quite a significant issue because the numbers were quite large (an estimated $225 million annually), but it’s not included (and therefore it must be assumed the present treatment is acceptable).

Inland Revenue is seeking consultation on 56 questions across the various topics and submissions are now open until 29th June.

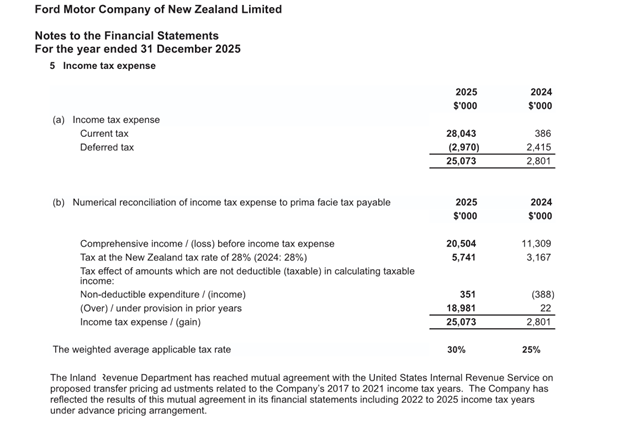

Ford forks out $18 million in back tax

Finally, this week, we frequently discuss the question of transfer pricing and overseas payments made by New Zealand subsidiaries of overseas companies. to tax havens or tax favoured jurisdictions and the effect on the tax base. Most of the time we are thinking perhaps of Google and the over one billion dollars in service fees paid to Singapore.

It’s therefore interesting to see Thomas Manch of Business Deskreport that Ford Motor Company of New Zealand Limited’s 31st December 2025 financial statements included a comment regarding settlement of a transfer pricing dispute with Inland Revenue. Note 5 to the accounts (see below) records an under provision of tax in prior years of just under $19 million. The result was Ford Motor Company’s tax bill for the year went up from $2.8 million for the year ended 31 December 2024 to just over $25 million for the year ended 31 December 2025.

It’s tempting to be cynical and think Inland Revenue is not paying a lot of attention to transfer pricing, but clearly this is a matter that has been in some dispute for quite some time as the adjustments go back to the year ended 31st December 2017. This also shows that these disputes can take some time to settle. Inland Revenue will be happy with this win, and it will be interesting to see what other disputes may be going on.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

I’ve talked before about how one of the frustrations of the Budget Lock-up is that detailed commentary on any tax measures is never made available during the Lock-up. A Treasury official told me during this year’s lock-up this is the protocol because the legislation has not been introduced into Parliament. This is one of those arcane points of order which may make Parliamentary sense but is a bit of a frustration. Because as we all know, the devil is in the detail.

It turned out that there were quite a few devils in it after the Budget Lock-up ended and the relevant tax bills and other initiatives were released. It’s quite interesting to compare what we saw during the Lock-up in terms of the announcements or the media release of the Revenue Minister, Minister Simon Watts, with what actually emerged after 2:00pm on the day.

Donations tax credit change

The Budget announced a maximum donation cap of $100,000 per person per tax year as a means of managing “expenditure control”. This was a surprise but makes sense when you look at the pattern of what National finance ministers have done in past budgets. Bill English and Steven Joyce were always looking for opportunities to remove or limit tax concession to balance the books. The biggest single example of this approach was in 2012 when employer contributions to KiwiSaver schemes became subject to Employer Contribution Superannuation Tax. That’s now worth probably close to $2 billion a year. In hindsight, it’s fairly obvious changes to the donations tax credit would perfectly fit with that pattern.

It’s interesting to look at the Regulatory Impact Statement (RIS) that accompanied the announcement. What emerged was a reminder that the removal of the cap on donations only happened in 2008. So, the present position is relatively new and has only been around for 18 years.

“…no case for a fundamental review”

The proposal raises $19 million a year when it’s fully implemented starting from 1st April 2027. As I told 1News, I see the move as nothing more than kicking over the stones to find some extra money. As the RIS noted Inland Revenue had not carried out a comprehensive review of donation tax concessions and had not compared the merits of using the tax system to support philanthropy versus direct government funding such as grants. The RIS also noted that Inland Revenue’s “2023−24 stewardship review found that there was no case for a fundamental review of the donation tax credit and that it was largely fit for purpose.”

Instead, Inland Revenue considered the donation tax credit from an “integrity and expenditure control perspective” while balancing the need to support the sector.

Improving expenditure discipline

According to Inland Revenue, expenditure on the donation tax credit was growing at an average of 2.6% per annum, yet at the same time the number of individuals claiming credits was declining. According to the RIS “Reintroducing a lower maximum entitlement threshold would improve expenditure discipline.”

Three options had been considered; firstly, maintaining the status quo. Secondly lowering the credit rate to 25%, but with the cap remaining at taxable income. (Remember, you can never give more than your taxable income for a year). The third option which is what was adopted, was lowering the maximum donation amount. Interestingly three further options were considered here. The one that was introduced, $100,000, but they also looked at lowering it to $15,000 or $4,500.

Charities not unreasonably pointed out the change could mean less money for donors. But the information sheet subsequently published said that the change would probably affect 350 donor entitlements, or 0.1% of donors. In other words, a very targeted and measured approach.

Trust income allocations to tax exempt beneficiaries

As I said in my Budget lock-up briefing there were some good measures in relation to not-for-profits regarding increasing the threshold for reporting and income and removing the risk of members’ subscriptions being taxed.

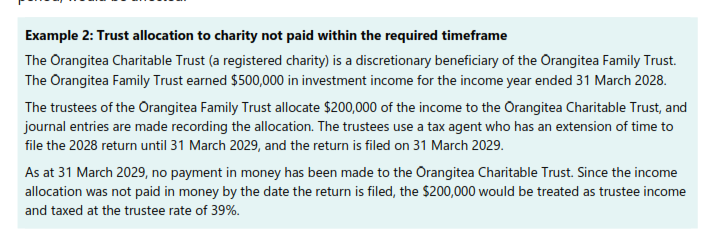

There was also an interesting change regarding trust income allocations to tax exempt beneficiaries. Now this is an adjunct to charitable donations and charity trusts as private trusts frequently have charities as beneficiaries to which they make donations which represent a deduction from trustee income.

The proposal is that private trusts which allocate beneficiary income to tax exempt beneficiaries will be required to pay the beneficiaries in money within a specified period in order for it to be tax exempt. If it’s not paid within that time, it will be taxed at the trustee rate as the following example illustrates:

This change is meant to counter a potential integrity risk when the beneficiary is tax exempt because the trust’s income receives a tax exemption despite not actually being paid to the charity and made available for charitable purposes.

This only applies to private trusts that allocate income to tax exempt beneficiaries. Apparently, there are 400 trusts that allocate income to tax exempt beneficiaries each year which surprised me. We’ve got over 200,000 trusts registered with the Inland Revenue and only 400 or so making use of this mechanic seems surprisingly small.

One other quirk is this change will apply from the start of the 2028-2029 income year. By contrast most of the other Budget measures announced will either have an immediate effect, from the start of the current 2026-2027 tax year, or from 1st April 2027 and the start of the next tax year.

Fringe benefit tax changes

There was also good news with fringe benefit tax changes. Again, this is legislation that will be published later this year, but it follows up from previous Inland Revenue consultation on fringe benefit tax.

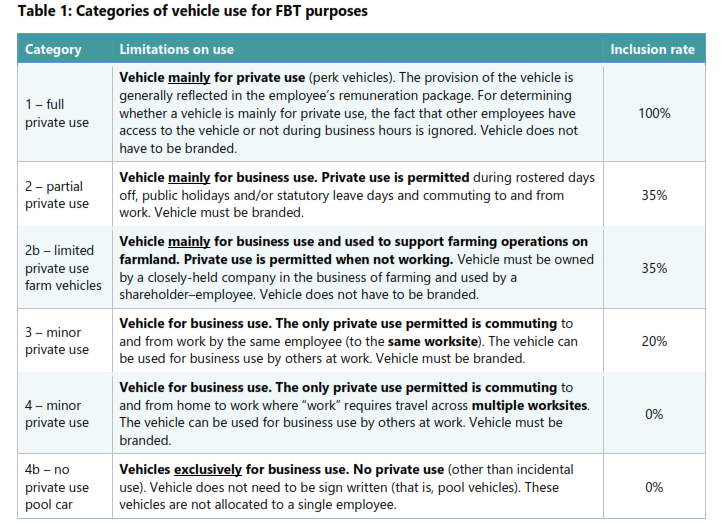

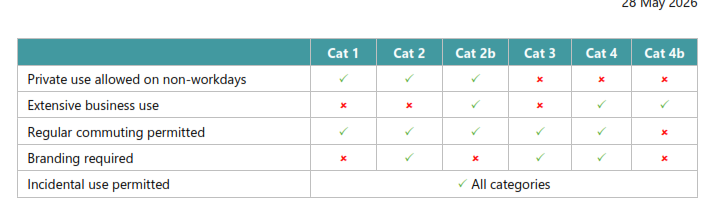

The main proposal is basically to simplify FBT for motor vehicles by implementing a “category approach.” Instead of counting the days in which a vehicle is available for employee use, the proposal would remove that entirely and instead require employers to choose a category based on the private use of the vehicle and use that rate when calculating their FBT viability.

There will be new rates for calculating the value of a vehicle for FBT purposes. Presently, the standard default rate is 20% annually or 5% quarterly. That will increase to 22.8% annually or 5.7% quarterly. For hybrid vehicles, it will be 19.6% annually or 4.9% quarterly, and an electric vehicle will be17% annually or 4.25% quarterly. So that would give more fuel-efficient vehicles a slight FBT advantage.

The idea behind this is to reduce compliance costs and hopefully also lower the FBT costs for some employers. It’s a good move in my view and will be in force from 1st April next year.

Foreign investment fund changes

Moving on, there were a couple of positive changes in the foreign investment fund (FIF) rules. Firstly, the cost threshold below which the FIF rules do not automatically apply was doubled to $100,000, the first increase since 2000. Taxpayers can still use the FIF regime even if the cost of their FIFs is below the threshold. Remember that dividends must still be returned if the FIF regime does not apply.

The other, somewhat unexpected, change allows all taxpayers to adopt the FIF Revenue Account Method (RAM) for unlisted securities. Previously, only new residents who arrived after 1 April 2024 could use the RAM. Furthermore, all New Zealand residents subject to double tax because of citizenship or the right to work in another country may also now use RAM for their listed shares, regardless of when they became tax resident. This will mainly apply to migrants from the United States.

There are also changes regarding the attributable FIF income method, which is beneficial for any shareholders who used to hold 10% or more of a foreign company. The rules regarding eligibility for the 10-year FIF exemption in the case of corporate migration (for example to the United States as part of a capital raise) will be clarified.

What’s particularly helpful about these changes is that they are effective as of 1st April 2026, i.e. they’ll have an impact this tax year. We’ll see more detail when this year’s tax bill is released in August/September.

Financial arrangements regime proposals

There are changes to the financial arrangements regime aimed at migrants. The proposal is to allow some taxpayers to reduce their exposure for unrealised exchange gains and losses by allowing them to calculate their income in a foreign currency instead of in New Zealand dollars. There will be a new calculation method for financial arrangements acquired for the purposes of meeting the Active Investor Plus visa requirements.

These changes have been made because the financial arrangements regime has proved problematic for migrants in a number of ways. Although helpful, I think the changes highlight that the financial arrangements regime is well overdue for a complete review – the last was carried out in 1998.

Banks in the firing line

A big surprise in the Budget was the introduction of a prudential levy on the finance sector which will be administered by the Reserve Bank. This is a tax increase in all but name. The interesting thing is, although it’s supposed to be a cost recovery mechanism, the accompanying media release commented “The levy will be paid to the Reserve Bank, with the revenue returned to the Government through an increased dividend.” This seems more than just a cost recovery exercise.

There was also a potentially significant thin capitalisation proposal aimed at the banks. The thin capitalisations rules apply to overseas controlled companies under which interest deductions are only allowable in full if their debt/asset ratio is 60% or less. If the debt to asset ratio exceeds 60%, then interest deductions get limited.

Now in the case of banking groups, the debt/asset threshold is set much lower. Since 2012, it has been 6% for foreign-owned groups. The Government proposes to increase this threshold to 12% for groups that include a “domestically systematically important bank”, which I’d say would be the big four Australian-owned banks, and 11% for all other banking groups.

The idea is to protect New Zealand’s tax base by limiting the amount of cross-border related party debt a banking group can take on for tax purposes and therefore limiting interest deductions in New Zealand. This is a fairly significant change for the banks expected to raise $45.2 million over the four year forecast period and together with the prudential levy won’t be welcomed by the banks. The levy and thin capitalisation changes are effective from 1st April next year. It will be interesting to see the pushback on these changes.

Budget tax bill passes

As noted, the detailed legislation for these various changes will be included in the annual tax bill due in August/September. In the meantime, the tax bill including the cap on individual donations introduced with the Budget has now been passed.

The bill also included the measure deeming a dividend to arise on any outstanding amount owed by a shareholder to a company six months after the company is removed from the Companies Register. This applies from 4th December 2025 the date Inland Revenue published its controversial paper on the taxation of company loans to shareholders. The accompanying RIS noted that in the case of companies going to liquidation, the average outstanding loan balance was around $213,000 per company. The measure is expected to raise $146 million (net of impairments) over the four year forecast period.

Double tax agreement with the United Kingdom updated

Finally, just a quick note that the double tax agreement with the United Kingdom has been updated and a new one was signed in at the start of the month week. This will replace the existing double tax agreement which entered into force in 1984.

The new agreement is designed to “better support cross-border trade and investment between the two countries and includes key anti-abuse provisions developed by the OECD to prevent base erosion and profit shifting”. It will come into force shortly once the relevant Order in Council is passed. Expect to see more updated agreements as we have some very old double tax agreements in place. The United States is another one dating from the 1980s.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

The first clue there might be some potentially significant tax changes in the Budget was when Inland Revenue announced on Wednesday afternoon it would be holding a post-Budget briefing. This is unusual and prompted some last-minute speculation much of which turned out to be wide of the mark.

The main tax headline is the changes to the taxation of charities and not-for-profits. The good news for smaller organisations is that the amount of net income they can earn tax free each year is increased from $1,000 to $10,000. There will also be legislative clarifications to ensure membership subscriptions and levies received by not-for-profits remain non-taxable. This will be a huge relief for such organisations after Inland Revenue had indicated it thought subscriptions could be taxable.

The trade-off is capping eligible donations at $100,000 per person per year. However, in certain circumstances donors will be able to claim donation tax credit refunds during the year rather than wait until the end of the tax year.

Tackling the issue of shareholder loans

Last December Inland Revenue dropped a bombshell with proposed changes to the taxation of company loans to shareholders. In March the Government then beat a retreat after the proposal generated pushback from various sources including the ACT Party and New Zealand First. Work did continue on the issue of the treatment of outstanding shareholder loans when a company goes into liquidation owing tax.

The Budget includes legislation to make clear that a tax charge will arise if a shareholder owes money if a company goes into liquidation or is otherwise removed from the Companies Register. The amount of any outstanding loans will be taxed as income. My understanding is that the measure will have effect from 4th December 2025 as originally proposed and is expected to raise $152 million over the period to 2029-30.

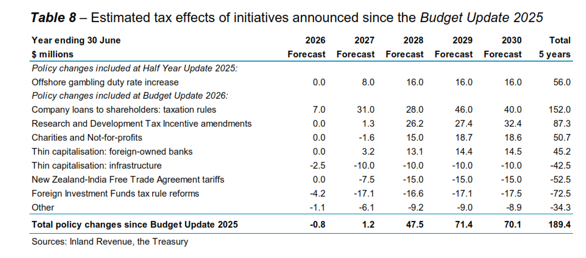

There are changes to the Research and Development Tax Incentive, some to enable in-year payments and others to expand the range of R&D expenditure mining businesses can claim (cheers Shane!). But there is a reduction in the cap on non-internal software for R&D from $25 million to $3 million. This means overall the Government will gain $87.3 million over the forecast period.

Foreign Investment Fund changes

The Foreign Investment Fund (FIF) revenue account method introduced in last year’s Budget and targeted at migrants has now been extended to include New Zealand residents who are invested in unlisted overseas shares. Such investors will now have the option to be taxed on realised gains instead. Furthermore, the FIF de-minimis threshold will double to $100,000, a welcome move for many small investors. (Arguably, it also reflects the widespread non-compliance in this asset class).

Overall, the expected return on the specific tax initiatives is $189.4 million over the five years to 30th June 2030 per the table below.

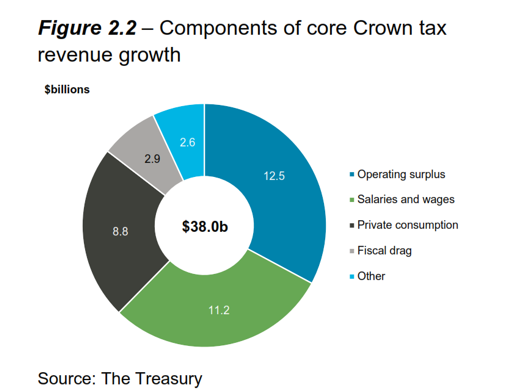

Fiscal drag – helping balance the books, again

The Budget predicts that total tax revenue will rise by $38 billion over the period to 30th June 2030. $2.9 billion or 7.6% of this represents fiscal drag. This is where growth in salaries means average tax rates for individuals increase as they cross tax thresholds which have not been increased since 2024. Fiscal drag is a long-standing tactic which helps balance the books without attracting too much attention. We were given no indication of any increase in tax thresholds.

A tax by any other name… the new prudential levy on financial industry

Beforehand I expected some increases to various levies to help balance the books. Like fiscal drag it’s a well-worn path to raise revenue without directly increasing income tax or GST. The new prudential levy on the financial industry was not on my horizon, particularly since at $209 million over the four years to 2029-30 it’s the biggest single fund-raising initiative in the Budget. The levy will be paid to the Reserve Bank, but the expectation is that the revenue will flow through to the Government “through an increased dividend.” In other words, the levy is more than the cost recovery described in the Budget documents. It will be interesting to see how the banks respond to this.

Incentivising house building

David Seymour had floated the suggestion that councils be allowed to retain part of the GST collected on sales of new homes. That hasn’t happened, but instead from 1 April 2027 councils will receive payments for consenting new homes. The incentive payment starts at 0.25 per of the national average consent value for the first additional one percent of existing dwellings consented. This rises to 1.25 percent of the national average consent value where more than two percent of existing dwellings are consented.

This all sounds good but I do wonder if it might cause a short-term hiccup as it is arguably in councils’ self-interest to delay issuing consents until after 1 April 2027 when the payments start.

More Inland Revenue funding for litigation and compliance but less for front line services?

The headline announcement is that following on from prior years, Inland Revenue has been given an extra $15 million per year to boost debt compliance. However, when you drill down into the Vote Revenue Appropriations a different picture emerges.

Inland Revenue have not been excluded from the agencies subject to cuts. To meet those targets its total appropriation for the 2026-27 year has been cut by just over $15 million to $771 million. This includes the effect of the additional $15 million boost. This implies nearly $30 million of cuts from the 2025-26 year.

Services to manage debt and unfiled returns take the brunt of this hit with a reduction by over $20 million from the prior year. Services to Ministers and to assist and inform customers to get it right from the start – probably the main public-facing part of Inland Revenue, falls by $3.5 million. This seems at odds with maximising revenue collection and I am personally highly sceptical that AI systems will be able to take up the slack as apparently expected. Expect telephone hold times to lengthen.

On the other hand, the appropriation for undertaking investigation, audit and litigation activities rises by $10.1 million to over $146 million. This reflects increased investigation activity we are seeing and also will fund court cases several of which relate to crypto-asset taxation involving “tens of millions of dollars.”

Overall, this was a much more interesting Budget from a tax perspective than I anticipated. As usual there’s a lot of devils in the detail, some welcome and others not so welcome.

The Organisation for Economic Co-operation and Development (OECD) recently released its 2026 Economic Survey of New Zealand. The OECD, like the International Monetary Fund (IMF), carry out regular reviews and this is a fairly detailed report running to over 140 pages, which you would expect, given the OECD has a significant economic database to work with.

The OECD was cautiously optimistic about the state of the NZ economy but noted that GDP growth was slower than in many OECD countries. Ongoing fiscal consolidation was needed, but the Middle East conflict may require more “targeted support”. It recommended ensuring “strong accountability through transparency of the [RBNZ’s] Monetary Policy Committee decision making”. Other recommendations included harnessing digital tools to improve health system performance and for a more affordable, secure and sustainable electricity system (which, in the long term, does not include LNG in the OECD’s view).

Not all recommendations made by the OECD or the IMF are greeted with enthusiasm by the government of the day. The Prime Minister reacted very strongly to warnings about the Government’s LNG proposals, calling the OECD’s report “a load of rubbish”.

Unlocking capital markets to drive growth

It’s Chapter 4 of the survey, which I found most interesting and relevant, as it included a discussion of our tax settings relating to the taxation of savings. This section was written by Dr David Haugh, the head of the New Zealand (and Finland) desk, together with his colleagues Kyongjun Kwak and Carl Magnus Magnusson. Dr Haugh is actually a New Zealander who started his career with the Treasury before joining the OECD. That means he has a good background knowledge of New Zealand and our challenges.

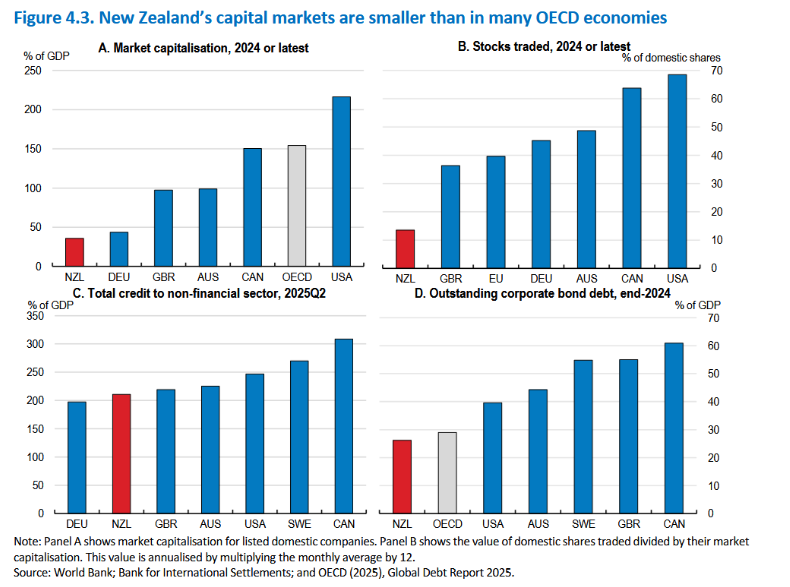

The background summary is that our capital markets remain “shallow by international standards, constraining long-term investment, innovation and productivity growth”. The survey notes that the NZX has seen no major domestic initial public offerings since 2021. That’s apparently part of a worldwide trend, as many firms that might otherwise have gone to market have instead opted for a private or trade sale. A classic example would be Fonterra’s recent sale of its global consumer and associated businesses, Mainland Group, to Lactalis.

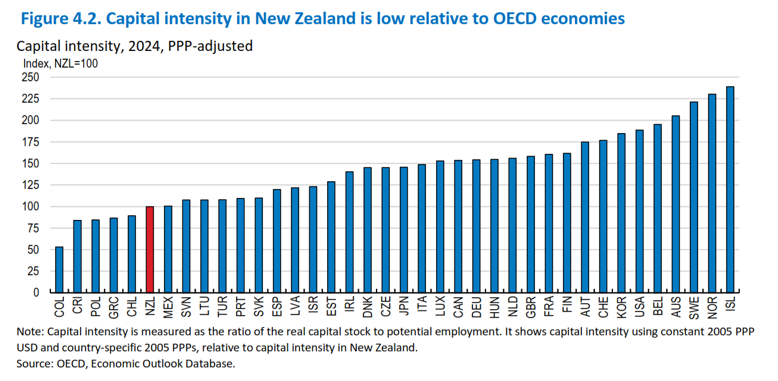

There are some pretty damning graphs illustrating the scale of the problem. Quite apart from smaller-than-average capital markets, ‘capital intensity’ or the ratio of real capital stock to potential employment is low relative to other OECD economies. In 2024, New Zealand’s capital intensity was just about 100%, whereas if you look at Israel, Norway and Australia, they’re all over 200%.

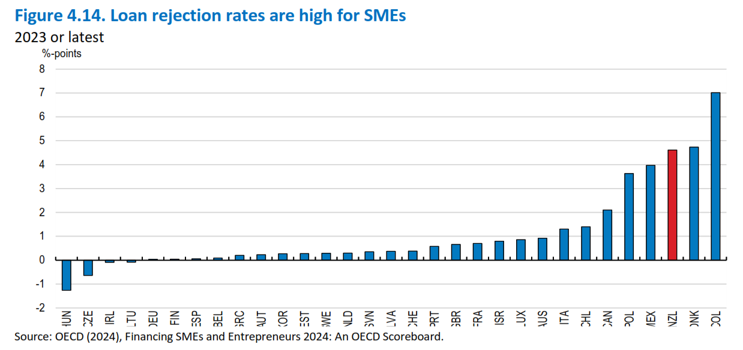

There’s also a sideswipe for the Australian banks, with the OECD saying “costly bank lending dominates, with OECD analysis of lending margins showing they’re about twice the international norm”. With the main banks preferring mortgage lending, SME loan rejection rates are high.

There’s a fairly blunt assessment of why our capital markets are underdeveloped – the decision in 1975 to cancel the Third Labour Government’s compulsory superannuation scheme:

“The decision to abolish the private pension saving schemes in 1975 and replaced it with a publicly funded universal pension at age 60, significantly hampered the development of New Zealand’s capital markets by reducing households’ incentives to accumulate private pensions, depriving capital markets of a key source of long-term domestic funding.” [page 98]

Developing public equity markets – the Swedish example

There’s a very interesting discussion about how Sweden “has developed one of the most dynamic and inclusive equity markets relative to its economic size in Europe and across the OECD.” A key element of this is the Investment Savings Account, or an ISK account. There are over 4 million ISK accounts, with half the adult population having an ISK. These have helped channel household investments into listed equities. Britain’s Individual Savings Account is a slightly similar product. The recommendation is that we consider introducing a non-retirement New Zealand Equity Savings Account.

Raising household savings through changes to KiwiSaver

The report notes our retirement savings are fairly inadequate by world standards. In September 2025, the value of funds under management in KiwiSaver was $141 billion or 32% of GDP. By comparison, in Australia, the assets under management exceeded A$3.6 trillion or 133% of GDP. Furthermore, the average Australian retirement pension plan value is NZ$130,000 or nearly five times greater than the average NZ$28,000 in New Zealand.

The survey notes that withdrawals are allowed to buy a first farm or first house, which, together with increasing withdrawals for hardship (these have doubled from $100 million a month in 2023 to $200 million a month in 2025), slows the accumulation of funds. The OECD questions the purpose of withdrawals for first farms or houses. It suggests that if the policy objective is to support low-income people into house ownership, then a separate instrument would be more effective. The OECD also recommends not creating any further exemptions.

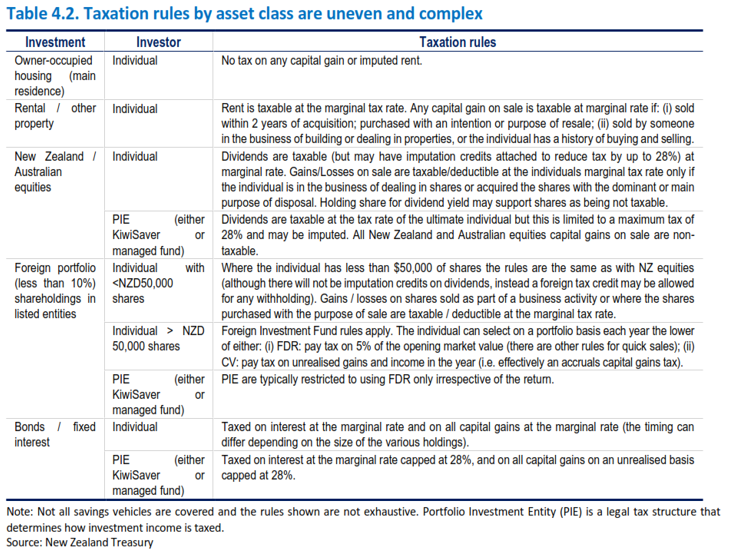

‘New Zealand’s taxation of capital income and savings is complex and uneven’

The survey then discusses the taxation of capital income and savings, which it describes as “complex and uneven, with housing taxed lightly relative to financial assets and especially pensions”. Our corporate income tax at 28% is noted to be amongst the highest in the OECD. Taken together, these settings:

“…distort household and firm investment decisions and suppress the accumulation of private pensions and other long-term financial savings, which is a critical issue not only for capital market developments but also for retirement income adequacy.”

In short, the way our tax system has distorted savings has had long-run consequences. This is something I’ve been saying for a long time and it’s also the view of the International Monetary Fund.

Increasing the accumulation of pension savings by reforming the taxation of savings

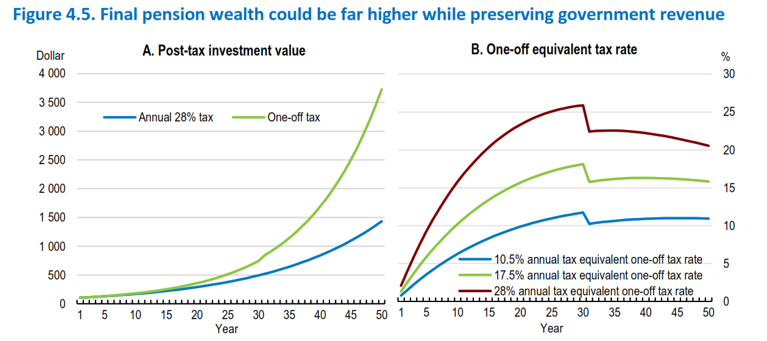

The OECD’s view is that the taxation of savings needs reform to allow greater accumulation of pension savings. The survey notes only seven of 38 OECD countries tax the investment income pension and only three, New Zealand, Australia and Türkiye, have a tax-tax exempt system (TTE). The most common system operated in about 17 out of 38 countries is an exempt tax, which is what you see in the UK and America, which allows the accumulation of more funds within the fund that eventually gets taxed as a pension.

The critical disadvantage of our TTE system is that it penalises the accumulation of long-term financial retirement assets, sharply reducing compounding returns relative to the exempt-exempt-tax systems used by many other countries, such as the UK and the United States.

The OECD bluntly concludes:

“The TTE system for financial savings combined with light taxation of housing in New Zealand… makes the overall system one of the most housing-biased tax systems in the OECD. This bias has been capitalised into higher house prices, larger new dwellings, lower ownership rates amongst younger cohorts, and a worsening of New Zealand’s net international asset position, reflecting reduced domestic financial capital available for firms.”

The OECD notes that because pension savings compound over 40 years or so, lowering the tax burden on returns “substantially increases long-run private wealth accumulation”. So, does that mean switching to the common exempt-exempt-tax approach? Not quite. An argument against such tax incentives, and one I share, is that the benefit of such savings is mostly captured by the wealthy who would be saving anyway, and tax incentives don’t lead to significantly increased savings. Another issue with tax incentives is, as Finance Minister Nicola Willis pointed out, they are extremely expensive.

Auto-enrolment and KiwiSaver

According to the OECD, many of these concerns are indirectly addressed by an auto-enrolment system, i.e. everyone would be in KiwiSaver and therefore automatically contributing and saving. UK evidence is that within such auto-enrolment schemes, savings do not fall or rise in response to tax incentives and other private savings are not reduced to offset the diversion into tax-preferred schemes. Furthermore, the strongest benefit of such a change would be for low and middle-income households, who have limited discretionary savings anyway.

Removing or reducing tax on KiwiSaver returns would operate primarily by allowing greater compounding and unchanged contribution patterns, generating substantial increases in total retirement wealth. In other words, directing the incentives there towards the lower-income earner is an approach I fully support.

The survey includes an example illustrating that if this approach is adopted and coupled with a withdrawal tax, the post-tax pension value is twice as large by age 65 compared with the current annual taxation approach.

Overall, there’s plenty of food for thought in this survey. We’ve had a long period of stable policy settings in relation to savings, but we have problems with productivity and access to capital for start-up companies. New Zealand actually has a fairly vibrant tech sector, but as this paper notes, a lot of small tech companies go overseas to get funding because they can’t get it here. I’ve advised on a few such situations, and I’m always surprised the investment capital isn’t readily available here. This OECD survey should therefore provoke plenty of debate amongst politicians and analysts alike, but I fear it will get drowned out by the noise around the coming general election.

The latest National Climate Change Risk Assessment is not a pretty read

More or less simultaneously with the OECD report release, the Climate Change Commission released its National Climate Change Risk Assessment (NCCRA) for 2026. This is the first one that’s been produced since 2020 and is not pretty reading. It identifies the 10 significant risk areas “where focused action would make the biggest difference.” In short, this means increased infrastructure spending, particularly in relation to water infrastructure. The NCCRA warns that without immediate action, water infrastructure could be the “first climate risk to reach an extreme severity level within the next 25 years”.

The regularity of natural disasters has been increasing. According to the NCCRA stat, about 97% of the estimated $33 billion of government expenditure on natural hazards since 2010 was spent on responding to and recovering from disasters, with only 3%, i.e. a billion dollars, spent on risk reduction.

What happens when the insurers withdraw cover?

Whether or not you accept what’s driving climate change, it is happening. The NCCRA notes that 556,000 buildings with a combined replacement value of $235 billion are currently exposed to inland flooding. Insurance premiums are rapidly rising, leading the OECD’s economic survey to note “climate-change-induced rises in insurance premiums make inflation control more difficult”.

Quite apart from rising insurance premiums, my concern is that at some point, the insurers are going to dictate what happens with such properties. If the insurers start withdrawing cover, and that’s now coming into general discussion, people will look to the government to help because if they can’t get insurance on their properties, the banks won’t lend against that. This also ties into what the OECD was saying about the high dependency on property ownership for savings.

The NCCRA notes that if we keep allowing the current pattern to continue, of simply accepting damage will happen and then repairing it afterwards, this will drain funds away from core services such as health and education. Over the past 15 years, we’ve spent on average $2 billion a year, or roughly 0.5% of GDP, on climate mitigation and recovery, and things are only getting worse.

All this comes back to a long-standing argument I’ve been making here on the podcast and elsewhere: that climate change is going to drive changes in our tax system by way of having to increase revenue to fund these changes. There’s been plenty of debate about the long-term fiscal sustainability of New Zealand superannuation, but the impact of climate change is an immediate and growing problem.

This is a long-term issue where you really do hope that all the major parties in Parliament accept the need to address this and move accordingly. But as we’ve seen with the superannuation debate, that’s not likely to happen.

The Australian Budget

Finally, across the ditch, the Australian Budget was handed down on Tuesday, 12th May. There had been a lot of speculation beforehand that there would be changes to ‘negative gearing’ and the taxation of capital gains. This speculation was correct, but the extent of the changes has taken people by surprise.

Negative gearing is what the Australians call the ability to offset losses from residential property investment against other income. With immediate effect, any new investors will now only be able to offset losses from purchases of ‘new builds’. (Rather like our previous interest limitation rules.) Taxpayers with existing rental properties will still be able to offset their losses against other income. In other words, they will not be subject to what we term ‘loss ring fencing’.

The capital gains tax surprise

Presently, Australia grants a 50% discount on the amount of a capital gain for individuals, trusts and partnerships if the asset in question has been owned for more than 12 months.

This 50% discount will no longer apply for any gains realised on or after 1st July 2027. Instead, there will be a cost-based indexation, i.e. based on retail price, which was the rule between 1985 (when Australia introduced capital gains tax) and 1999. There will also be a minimum 30% tax rate on capital gains.

This is a significant change, and it’s expected to result in a rise in payable capital gains tax. Pre-Budget speculation focused on gains from residential property investment, but this change will apply to all asset classes.

A potential silver lining?

Now, the interesting thing if you’re a New Zealand resident and you’ve got a property investment in Australia, this change may be beneficial. At present, New Zealand tax residents are subject to Australian capital gains tax on disposals of Australian-situated property, but because they are not Australian tax residents, they do not get the 50% discount. (Australia is frequently quite sneaky in how it taxes non-residents.)

This change may mean that New Zealand investors subject to Australian capital gains tax on Australian properties may actually be better off. We’ll need to see the details on that, but it’s perhaps a silver lining for everyone.

On that note, that’s it for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and tell you and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Friday 15th May – it has been edited for brevity and clarity]