Inland Revenue releases three special reports regarding the changes to the platform economy rules, the 39% trustee tax rate and the new 12% offshore gambling duty

Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don’t, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

Apparently, tax debt is high in the construction sector and there’s also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

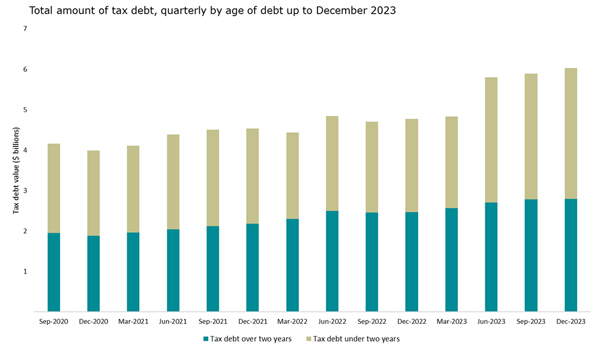

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over two years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

ADVERTISING

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it’s going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we’re going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators

Under the new rules, so-called online marketplace operators such as Airbnb, Uber and Bookabach will charge GST on all bookings made through them. However, the person who actually provides the ride or the accommodation may not be GST registered. This is where the flat-rate credit scheme comes into effect as the following example illustrates:

The full report is 68 pages so there’s plenty more to dive into.

Special report on 39% trustee rate

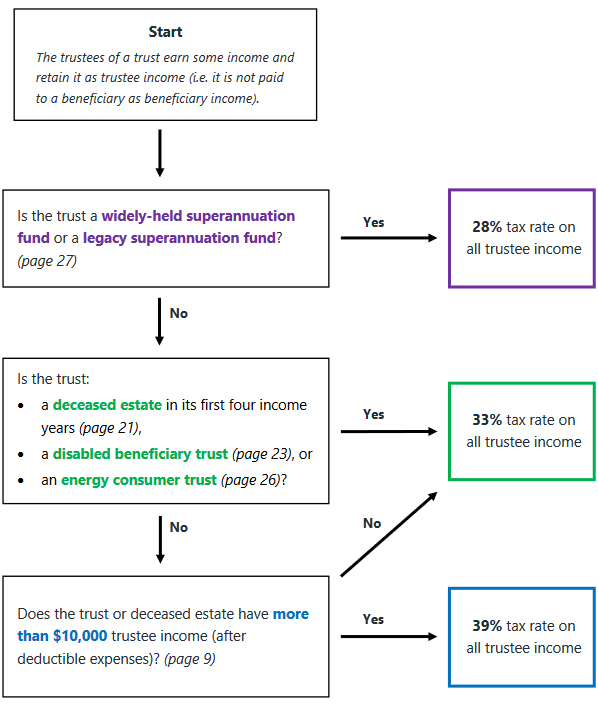

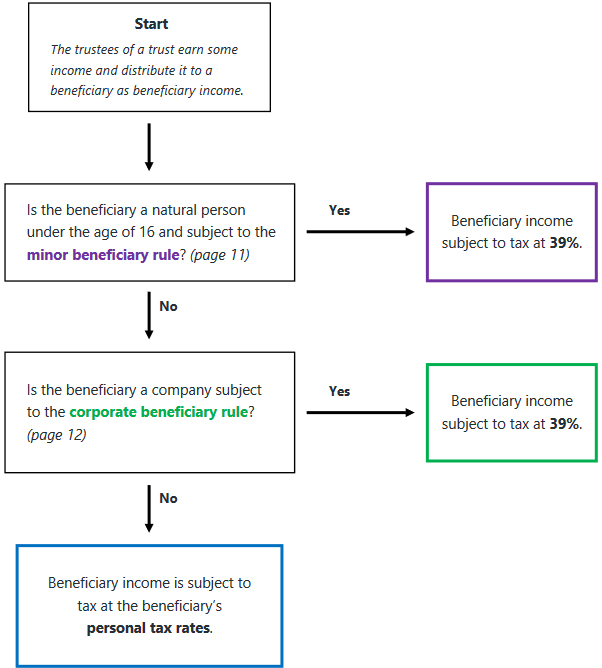

One of the other reports that was issued is on the application of the trustee rate of 39%. Basically, trustee income is the net income of the trust, which has not been distributed to beneficiaries. The 30-page report explains the basic provisions about “beneficiary income” and “trustee income” together with a couple of useful flow charts.

Trustee income flowchart

Beneficiary income flowchart

The report references the minor beneficiary rule which applies where the beneficiary is a natural person under the age of 16. In such a case only $1,000 of income per year can be distributed to that person as beneficiary income and be taxed at that person’s marginal tax rate, presumably below 39%. Under the new rules, any beneficiary income in excess of $1,000 paid to a minor would be taxed at 39%.

Overall, this is useful guidance. Just remember the $10,000 threshold is all or nothing: if trustee income is $10,000 or less, the trustee tax rate that applies is 33%, but if it’s $10,001 then it’s 39% on everything.

The third report is on the proposed offshore gambling duty, which takes effect from 1st of July and will apply to online gambling provided by offshore operators to New Zealand residents.

The bright-line test and tax evasion – a couple of useful real-life case studies

Finally, this week a couple of interesting Technical Decision Summaries from Inland Revenue. Technical Decision Summaries are anonymised summaries of some interesting cases that Inland Revenue’s Tax Counsel Office has encountered either through tax disputes and investigations or applications for binding rulings.

The first one, TDS 24/06, is an application for a ruling regarding whether the bright-line test or section CB 14 of the Income Tax Act would apply. The facts are complicated but involve three sections of land currently owned by the ruling applicant.

The applicant had initially acquired one section outright before his spouse and another co-owner acquired interests as tenants in common. Over time, the applicants proportion of the ownership changed until at the time his spouse died the property was held 50% as tenants in common with his late spouse. The second section was owned 50% each as tenants in common with his late spouse. After her death her 50% interest had passed to him under her will. The third section was owned by the applicant and his late spouse as joint tenants. Following her death, her interest was automatically transmitted to him.

The ruling applicant was concerned about the treatment of future sales. Would the bright-line test apply or failing that, would section CB 14? This section is a little used provision and applies where there’s been a disposal within 10 years of acquisition and during that time there’s been a 20% more increase in value of the land thanks to a change in zoning, or removal of restrictions.

The Tax Counsel Office concluded neither the bright-line test nor section CB 14 would apply. This is obviously a good result for the taxpayer but it’s actually also a good example, of how you can apply for a ruling to get Inland Revenue’s interpretation on a tax issue. You don’t necessarily have to follow it, but if you don’t, you better have good reasons for not doing so.

Fiddling the books and getting found out

On the other hand, TDS 24/07 involved suppressed cash sales, GST and income tax evasion and shortfall penalties. The taxpayer carried on a restaurant business which was registered for income tax and GST. Inland Revenue’s Customer Compliance Services (CCS) investigated the company and formed the view that there was fraudulent activity going on. There was suppression of cash sales, and the taxpayer was under returning GST and income tax.

CCS reassessed the taxpayer’s GST and income tax returns for the relevant periods and they increased the taxable revenue for suppressed cash sales based on analysis of point of sale data, the taxpayer’s bank statements and industry benchmarking.

Industry benchmarking – an underused tool?

Just on industry benchmarking, I think Inland Revenue ought to be much more public about its data here and warn taxpayers there are benchmarks against which it will measure your business. It has done so in the past, but I think the combination of Business Transformation and then the pandemic interrupted progress in this space.

What people should remember is, Inland Revenue has some of the best data available anywhere about measuring industry benchmarking. I believe it should be making this much more public so that it can serve as an early warning shot for businesses that think they can suppress income. Everyone loses when this happens. Gresham’s law about bad money driving out the good is very applicable here, because businesses which are not tax compliant are undercutting those businesses which are following the rules. This is not a healthy situation as it leads to considerable frustration and anger and if not dealt with, will just simply encourage more of the same behaviour.

Tax evasion? Have a 150% shortfall penalty

In this particular case, the taxpayer’s fraud was identified, and GST and income tax reassessments followed. In addition, Inland Revenue also imposed tax evasion shortfall penalties, which are 150% of the tax involved. These evasion shortfall penalties were reduced by 50% for previous good behaviour, but that’s still represents a penalty of 75% of the tax and GST evaded.

Unsurprisingly, the taxpayer counter-filed a Notice of Proposed Adjustment under the formal dispute process, and the dispute ended up with the Adjudication Unit, which is run by the Tax Counsel Office as part of the formal dispute process. The Adjudication Unit did not accept the taxpayer’s counter arguments, including an attempt to claim an income tax and GST input tax deduction for the cost of fresh produce purchased with cash. The problem was there was no supporting evidence for this claim, so the Adjudication Unit probably found it easy to reject it. The Adjudication Unit ruled not only was the tax due, but the penalties were also correctly imposed.

Get ready for more Inland Revenue action

Circling back to our first story, this TDS illustrates what lies ahead for those in the construction industry who have been suppressing income. As I said, I do think Inland Revenue should make everyone more aware of its benchmarking data which would be a warning for would be tax evaders. It’s pretty clear from the announcement about the construction industry that Inland Revenue is gearing up for many campaigns targeting debt arrears and clamping down on tax evasion in particular industries. As always, we will keep you updated as to developments in those areas as they happen.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

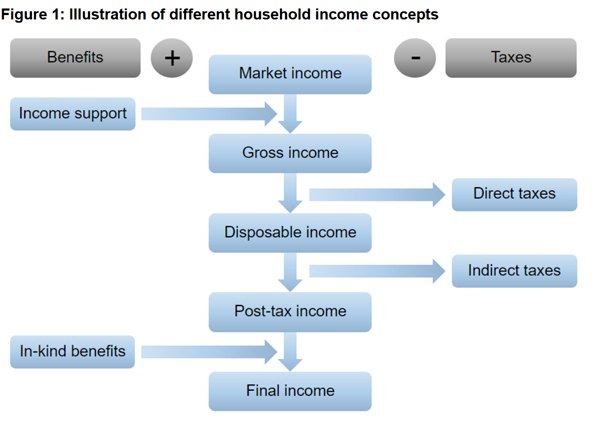

Treasury Analytical Note examines the effects of taxes and benefits for the 2018-19 tax year

The Australian Tax Office gets heavy with the Exclusive Brethren – will Inland Revenue follow suit?

Understandably the start of the new tax year on 1st April and the increase in interest deductibility for residential investment property to 80% was generally greeted by residential property investors with enthusiasm. Users of apps such as Airbnb and Uber, on the other hand, were less enthusiastic because the provisions relating to GST on listed services also took effect on 1st April. It has become clear that this change has caused some confusion and led indirectly to price rises.

Now GST on listed services refers to online marketplace operators who “facilitate the sale of listed service”. This is the so-called “Apps Tax”, which National promised to repeal when it was campaigning in last year’s election but then decided to keep it because it needed the money to make up for the loss of its overseas buyers tax.

These rules apply to the likes of Airbnb, Uber, Ola, and Bookabach which facilitate the sale of related the services. They now have to collect and return GST when the relevant service is performed, provided or received in New Zealand. It doesn’t matter whether or not the seller, the actual person doing the providing of the Uber or Airbnb, is GST registered. (For those already GST registered the change will have little effect).

Confusion and an unnecessary price increase?

However, a significant number of those providing the Uber or Airbnb, are not GST registered because the total services they provide annually are below the GST registration threshold of $60,000. But the introduction of the apps tax has prompted some of these non-registered persons to effectively increase their prices 15% to take account of the GST charge. However, this overlooks that though as part of the changes those non-GST registered persons can expect a 8.5% rebate under the flat-rate credit regime scheme.

What happens here is the offshore marketplace (Uber or Airbnb) will collect 15% GST on the booking but then pass 8.5% of that to the persons actually providing the Uber or Airbnb. But as an article in The Press notes, it appears many people now think they are GST registered and have effectively increased their prices by 15%. As Robyn Walker of Deloitte said, there definitely appears to be some confusion around hosts about this law change, and probably many don’t fully appreciate that they’re getting this 8.5% rebate.

As GST specialist Allan Bullot of Deloitte, noted there is a lot of confusion with Airbnb. It’s a complicated area, and something Airbnb providers are very careful about is registering for GST because of the fear they might have to pay GST if they sell the property to someone who’s not GST registered. In which case they effectively had to pay GST on the capital gain.

It appears what we’re seeing here is that those who have been brought into the new flat rate credit scheme haven’t yet quite worked out how the new rules will work for them. I would expect things to settle down in time and maybe Inland Revenue might put out more guidance. But it would appear that some providers are getting an accidental windfall at this point, although the increase is taxable for income tax purposes. Anyway, watch this space to see how this plays out and whether there’s some tweaking to the rules as this scheme beds in.

Treasury analyses the effects of tax and income

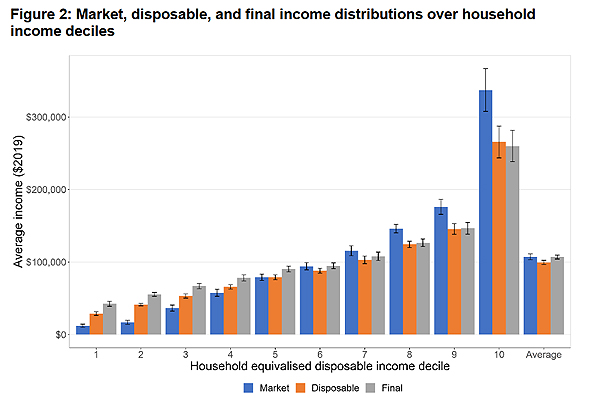

Moving on, just before the end of the tax year, Treasury produced an interesting Analytical Note on the effects of taxes and benefits on household incomes in tax year 2018 – 2019. This is interesting in a number of ways because frequently when people are talking about the effective tax burden, they look at the impact of direct taxation on a person’s pre-tax income.

Some have pointed out this is not really a true measure of a person’s net tax burden. They’re referring to the effect of transfers that people might receive from government in the form of Working for Families or New Zealand Super, but also the indirect transfers such as education and healthcare.

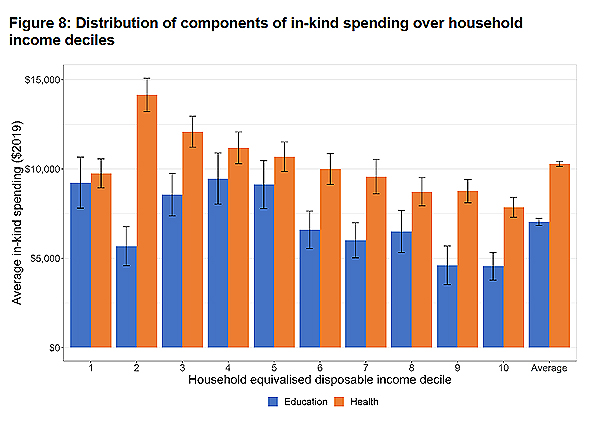

This paper tries to examine that for the 2018-19 tax year and what it does is calculate a household’s “final income” which represents net income after direct and indirect taxes and then adds an estimate of the government spending on health and education services received in kind.

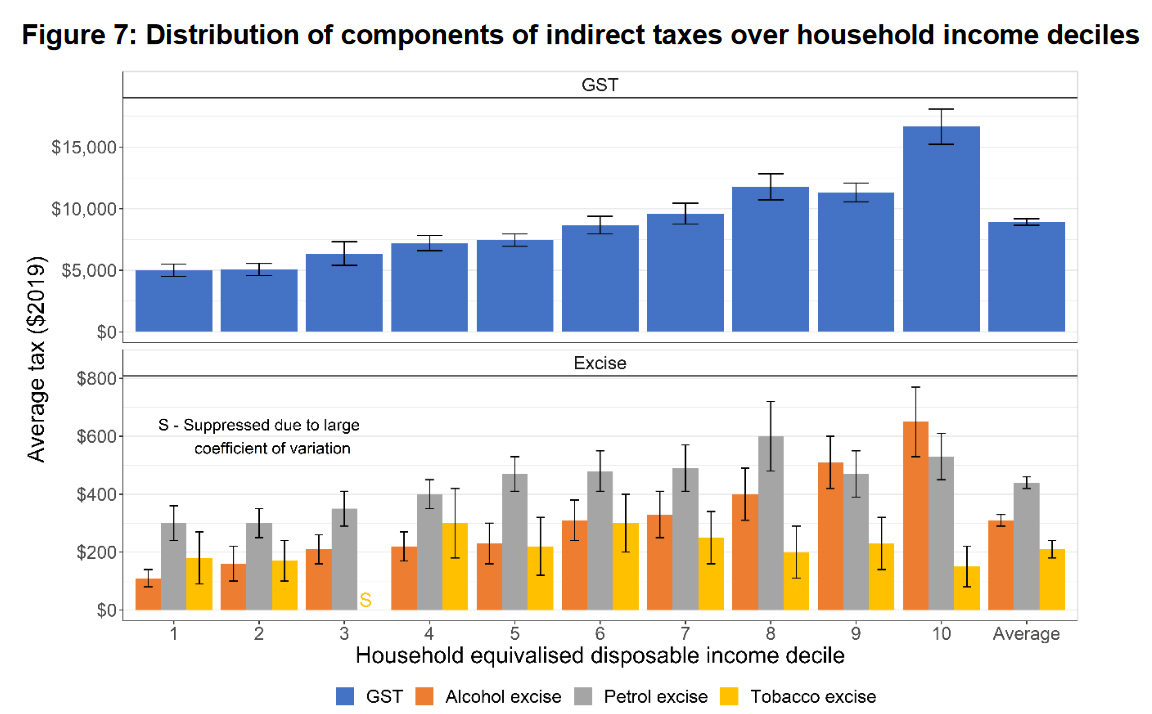

As the paper notes basically when you just look at disposable income, that is market income plus transfers, such as Working for Families credits or New Zealand Super, these are incomes are generally lower than market incomes on average over the population of New Zealand, and fairly unequally distributed. However, once you bring in indirect taxes and in kind benefit payments to get final incomes as defined, these are significantly more equally distributed than disposable incomes and close to market incomes when averaged over all households.

Yes, but what about Gini?

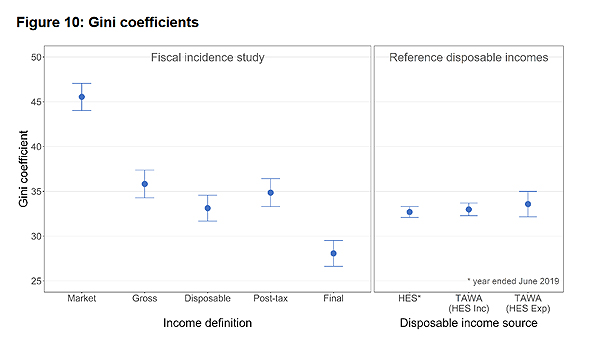

The Note also considers the Gini coefficient. This is the measure of inequality, where the higher the number, the more inequality society is. The Gini coefficient starts at 45.6 ± 1.5, and that drops to 35.8 once you bring in income support payments. Once you include consumption taxes and the benefits in kind such as health and education you end up with a Gini coefficient of 28.1 which is considerably lower and indicative of a much more equal society.

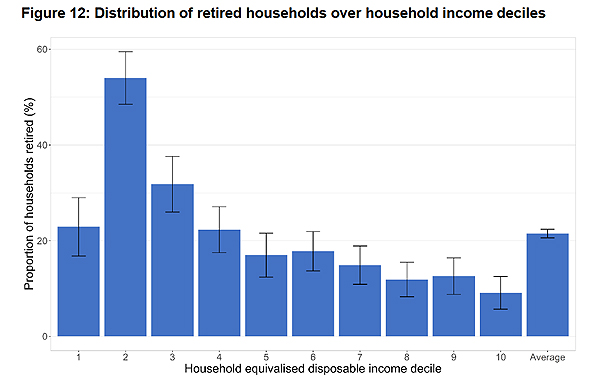

What the Treasury analysis did was to take 66% of all core Crown tax revenue and 68% of core Crown expenditure and allocated that to New Zealand households. Although the effect is approximately neutral as the note describes the effect is unevenly distributed. Households in the bottom five “equivalised disposable income deciles” received on average more in government services than they paid in taxes, whereas the opposite is true for houses in the top four deciles.

The second decile is the one where there’s a large amount of support happening. This is because there’s a fairly high concentration of New Zealand super recipients in that second docile.

The Note also considers “retired households”, where one of the people in the household is receiving New Zealand super.

“Drink yourself more bliss”

I was amused to see in the analysis of indirect taxes a comment about the average alcohol excise amounts increasing reasonably steady with each decile household equivalent. In other words, the richer the decile, the more they drink. That is a crude summary but it did amuse me.

As I noted, the Treasury analysis covers GST and the effect of economic benefits in kind. There was some commentary at the time of last year’s High Wealth Individual report that it wasn’t really quite fair because it didn’t take into account what the impact of GST and government benefits in kind. This is interesting to see, and I definitely recommend having a read of the note which is a reasonably easy read.

The Australian Tax Office raids the Exclusive Brethren’s business operations

And finally this week, a story coming out of Australia caught my eye about the Australian Tax Office (“the ATO”) raiding multiple premises associated with the global headquarters of Universal Business Team (UBT) on March 19th. UBT is a Sydney registered company that provides services and advicee to about 3000 exclusive Brethren owned businesses in 19 countries.

ATO investigators also apparently raided the head offices of a number of Brethren run companies, including OneSchool Global. In what would also be the standard procedure here, they confiscated phones, computers, documents and other materials. This was done as part of what the ATO call a “no notice raid”. Inland Revenue can do such raids as well, but the point is, it’s not done very often, and the fact that this has happened is extremely intriguing to see.

One of the things that I see frequently pop up in the comments of these transcripts, are questions/ pushback about charities having an exemption from tax on their business profits. It’s more complicated than that, but it’s there’s an obvious tension there. (Again thank you to all those who contribute, your comments are read even if I don’t always respond).

On this point I recall a discussion I had with the late Michael Cullen when he was chairing the last tax working group. During a roadshow event I asked him if there was anything which had surprised him during his role. He replied that he had been surprised by the scale of the charitable sector. He and the group had some concerns about whether in fact, all the charitable donations were being used for charity. In particular whether donations made under an exemption to an exempt business were in fact being used for a charitable purpose. The Tax Working Group’s final report noted:

“80. …the income tax exemption for charitable entities’ trading operations was perceived by some submitters to provide an unfair advantage over commercial entities’ trading operations.

81. notes, however, that the underlying issue is the extent to which charitable entities are accumulating surpluses rather than distributing or applying those surpluses for the benefit of their charitable activities.”

The Sunday Star Times asked Inland Revenue to comment on the ATO’s action but Inland Revenue just dropped a dead bat on it. But I would think, as the Sunday Star Times said, any information relating to New Zealand businesses that came into the ATO’s hands would proactively be passed on under the Convention on Mutual Administration Assistance and Tax Matters, part of the double tax agreement between Australia and New Zealand.

The scale of information exchange which goes on between tax authorities is very largely unknown, but it’s probably one of the most revolutionary changes to the tax landscape which has happened in the last five to 10 years. I don’t think we’ve yet seen anything like the impact that it will have.

Will Inland Revenue follow suit?

In summary the ATO clearly feels that it’s justified in launching a “No notice raid”. The question is whether Inland Revenue is considering something similar or is it just going to sit back and watch carefully? We don’t know, it won’t say, but you can be sure that it will be watching very closely to see what findings that come out of the ATO raid. If it does get anything interesting from the ATO, expect to see something similar happen here.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week, Inland Revenue published a reminder aimed at tax agents that clients must have a taxable activity in order to be registered for GST.

The notice said if your client is filing regular GST refund returns with expenses consistently more than their income, it may suggest they are not carrying out a taxable activity or have errors in their GST returns.

Inland Revenue then notes that clients “may receive a letter if they have filed regular GST refund returns from registration.” Tax agents are advised to “please review the refund returns filed and if required take any necessary action”. Inland Revenue then add that letters may be sent to clients who have been filing regular GST refund returns in the last 36 months.

If anyone receives such a letter their response will be expected to include one or more of the following:

a description of the taxable activity or activities undertaken and an explanation for the regular GST refunds.

A voluntary disclosure to correct any errors in the GST returns,

Cancellation of the GST registration if they are no longer carrying out a taxable activity. The final GST return should be filed with the required adjustments.

Inland Revenue are clearly about to run a campaign on this issue. Based on Inland Revenue’s statistics during the year ended 31st March 2023 there were just under 100,000 GST registered persons with nil turnover. (About the same number as have turnover exceeding $1 million). There’s another 160,000 or so who have a GST turnover of between $1 and $60,000.

According to Inland Revenue the net GST refund paid to GST registered persons with turnover below $60,000 has increased from $463 million in the March 2001 year to $1.473 billion in the March 2023 year.

Clearly Inland Revenue has looked at this and thought “How genuine are some of these GST registrations?” It will probably be looking at some of the lifestyle blocks that I’ve encountered with some grazing income, but the expenses of running outweigh the grazing income. Inland Revenue looks to be gearing up for a campaign to review those such clients in some detail. We’ll track to see what happens on this and give you updates as and when information emerges

When is a subdivision project a “taxable activity” for GST purposes?

Moving on and still on the matter of GST, and actually on the question of carrying on a taxable activity, Inland Revenue has just released a draft Question We’ve Been Asked (QWBA) for consultation on when is a subdivision project a taxable activity for GST purposes.

Following the 1995 Court of Appeal decision in Newman, Inland Revenue had issued a Policy Statement on this issue.

Under the Policy Statement whether a subdivision project is a taxable activity for GST purposes depends on the facts of each case. Determining this takes into consideration factors such as the scale of a subdivision, the level of development, work time and effort involved, the amount of financial investment and the commerciality of the transaction. Based on this the general view was if a person carried out a subdivision involving three or four sections, it was likely to not represent a taxable activity for GST purposes.

28 years on, it’s not unreasonable for Inland Revenue to come back and look at the matter again. In the draft QWBA the Commissioner considers most of these factors are still relevant when considering whether a subdivision is a taxable activity. However, the draft clarifies and, in some respects, differs from the previous Policy Statement.

According to the draft QWBA in determining whether a subdivision represents a GST taxable activity “the most relevant factor will generally be whether the activity is carried on continuously or regularly. This Question We’ve Been Asked focuses on this factor.”

Following on from this, paragraph 29 of the draft states,

“Generally, the Commissioner considers the level of development work involved in the construction and sale of a single house or other residential dwelling as part of a subdivision is not on its own enough for an activity to be considered carried on continuously or regularly.”

On the other hand, the construction and sale of multiple residential dwellings or a large commercial building is more likely to be continuous or regular. This is an interesting change in tone since 1995. But also, when you think about it, the change reflects how generally speaking, it has become easier to subdivide. Certainly, in Auckland if not necessarily everywhere, it has become easier to subdivide.

Clearly, Inland Revenue is seeing a lot of activity in this space. And the question is then arising, well, at what point does a simple subdivision become a GST taxable activity? Hence this updated QWBA.

As I mentioned a few minutes ago, there was always a sort of general conclusion from Newman that maybe three or four lots carved off would not be a taxable activity. But as the draft notes, there’s no specific number of lots created that determines whether a taxable activity exists. Our case law indicates that where a subdivision activity involves the creation and sale of multiple lots, it MAY be a taxable activity. But it doesn’t necessarily mean a subdivision involving creation and sale of multiple lots will always be a continuous activity because, for example, a subdivision is so straightforward that the number of lots sold is not significant, but it does in revenue.

But…a single section could be a taxable activity

Paragraph 32 of the draft notes although an activity leading to the supply of only one section will not usually be considered an activity carried on continuously or regularly, “this does not mean an activity leading to one supply can never be a taxable activity”. It could be that if other factors are sufficiently present, such as the scale of the subdivision or the level of development work. This will be this will indicate the activity is continuous, even if it leads to only one supply. For example, the construction and sale of a single commercial building on subdivided land would be an activity carried on continuously and regularly.

Changes from previous policy

The previous policy referred to the commerciality of the project as a factor but Inland Revenue have now decided that commerciality is no longer significant. In addition, there was an example in the previous Policy Statement where the construction and sale of a tea shop on subdivided land would represent a taxable activity. However, this draft QWBA now considers that building a tea shop would not normally involve more activity at work than that involved in constructing a residential building and therefore would not meet the criteria to be a taxable activity.

No GST, but what about income tax?

The draft also adds a reminder that although it is focused on GST, even if a subdivision activity is not a taxable activity for GST purposes, the resulting sale may still be subject to income tax. This might perhaps be under the bright line test. But there are other provisions that specifically deal with subdivisions carried out within ten years of acquisition. A useful reminder that although a transaction might not be within the GST net, it could well still be subject to income tax.

A few examples

There are some good examples at the end of the draft QWBA. It’s just worth repeating again that the material being put out by Inland Revenue is much more accessible than it was in previous years. The draft contains a good example about a basic subdivision then, which would not be a taxable activity because it’s not carried on continuously and regularly.

Example four illustrates the GST issues where a subdivision is part of an existing taxable activity. Now this is a question that does pop up quite regularly in my experience. In this case, Loammi and Marissa are GST registered as a partnership with a taxable activity of residential property development. They buy dilapidated houses and renovate them to sell for a profit.

In this example they realise they could make a larger profit on a particular piece of land by subdividing before sale. And therefore, even though the subdivision and sale would not be a taxable activity on its own, in this case the sale of the subdivided land is a taxable supply because it was done in the course of furtherance of their existing taxable activity

Overall, this draft QWBA is probably a good warning for anyone considering subdividing property, maybe carving off two, three or four sections, and thinking that that would not represent a GST taxable activity. This view is no longer so clear cut. Like much of tax it’s fact dependent. It’s also another good example where it pays to get good advice beforehand, otherwise a nasty GST surprise could be awaiting.

Foreign Investment Funds – a welcome change of heart from Inland Revenue

Finally, a few weeks back I discussed an interesting Inland Revenue Technical Decision Summary about which methodologies must be used to calculate income under the Foreign Investment Fund (FIF) regime. Under the FIF regime individuals and trusts may switch between the fair dividend rate, which applies a flat 5% to the opening value of a persons FIFs or the comparative value, which looks at the gains, losses and income during the year.

However Inland Revenue had suggested this could not happen where people were making voluntary disclosures of FIF income for prior tax years, something I see quite frequently. Inland Revenue’s proposal was this ability to change methodologies was not available and all taxpayers making voluntary disclosures would be required to adopt the fair dividend rate.

This prompted a fair bit of pushback from quite a number of advisors, including myself. I’m pleased to say that Inland Revenue has now issued an updated draft QWBA on this matter. The updated QWBA notes the Commissioner accepts that taxpayers have a choice of methods to calculate income, even if they fail to declare the income in a tax return and later file a voluntary disclosure or fail to file a tax return by the due date and later provide one including the FIF income.

This updated QWBA is another example of the Generic Tax Policy Process working with Inland Revenue taking on board feedback from advisers. It’s a good result for taxpayers. I was concerned that if Inland Revenue adopted a harsh approach on this, then people would just simply stay in the undergrowth and hope that Inland Revenue never noticed them. And that’s not good for the tax system at all, where you’ve got people who are become compliant and feel that they are unfairly penalised for doing so. Meanwhile other non-compliant persons see this and decide to just take a chance on not being caught in the first place. This is never a wise approach in my view.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

An Australian case highlights the problems around removing GST from food, and as the Government’s financial statements for the year ended 30th June 2023 are released, instead of our tax cuts do we actually need more tax?

Last week I mentioned the retirement of Geof Nightingale and I also surmised that it wouldn’t be long before we heard from him again. And sure enough, this week he popped up on Mike Hosking breakfast show talking about the various tax policies on offer. After a tongue in cheek confession that this had all given him a bit of a headache, Geof then made the very wise suggestion that perhaps it is time to establish an independent fiscal costings unit so that during an election campaign the claims of the various parties can be scrutinised impartially.

As Geof noted, this is actually something the Labour Party proposed in the run up to the 2014 election. Now, given the claims, counterclaims and accusations this week about exactly how many families would gain the maximum benefit from National’s tax proposals, maybe this is something which should be looked at again. On the other hand, someone else has also suggested perhaps we can refer them for false advertising? Probably a bit too late for that really.

Removing GST on food – a legislative headache in the making?

Moving on, the multi-party debate on Thursday night on TV1 threw up several moments of light relief, including when the leaders were asked to comment on National’s foreign buyer tax policy and Labour’s proposal to remove GST from fresh and frozen fruit and vegetables. None of the leaders thought much of either policy.

This prompted moderator Jack Tame to challenge Winston Peters, noting that New Zealand First’s manifesto proposed the removal of GST from food. (For the record, the Greens and Te Pati Māori both propose to go further than Labour on this point). It turned out, however, that New Zealand First had literally just updated their manifesto, dropping the original proposal and instead proposing it would “secure a select committee inquiry into GST off basic fresh foods. We must examine if this would deliver real benefits for taxpayers before legislating for it.”

Maybe New Zealand First’s change of tack on this topic was prompted by a recent Australian tax case. In this case the court ruled that a series of frozen food products were subject to GST and could not be zero rated (or “GST-free”, in Australia’s somewhat peculiar GST terminology). In brief, what happened was that Simplot was marketing six frozen food products such as a fried rice or pasta product, each of which contained a combination of vegetables and seasonings, as well as grains, pasta and/or egg.

The case turned on around what constitutes a kind of food marketed as a prepared meal. If they were food, as Simplot argued, then no GST applied. However, if they were if they represented a kind of “food marketed as a prepared meal but not including soup as per Australia’s GST legislation“, then it would have been subject to GST.

After an exhaustive analysis, including examining the packaging and advertising, Justice Hespe ruled GST applied. But it appears that she was none too happy with the whole process and the legislation. She remarked in paragraph 141 of her judgement

“The legislative scheme with its arbitrary exemptions is not productive of cohesive outcomes. It has left the Court in the unsatisfactory position of having to determine whether to assign novel food products to a category drafted on the premise of unarticulated preconceptions and notions of a “prepared meal”. It may be doubted whether this is a satisfactory basis on which taxation liabilities ought to be determined.”

Now that’s probably justice speak for “You have got to be kidding that we have to do this every time.” But they represent pretty wise words of warning for future drafters of any New Zealand legislation removing GST from food.

More tax, not less?

As mentioned at the beginning, a key part of the election campaign has been the various tax proposals on offer, and particularly promises of tax relief in the form of tax cuts or threshold adjustments. Each of the parties, with the exception of Labour, have something on this. But in Stuff economist and previous podcast guest Shamubeel Eaqub said of both Labour and National that they were, “pretending somehow we don’t have long term big, long term issues that we need to deal with and time is running out.” He continued, “In terms of reaching surplus they are all saying getting back to surplus is important but how do you do it while giving tax cuts and spending on things we’ve already promised ourselves?”

I echoed his comments in part by saying that I didn’t believe the politicians of the two main parties are “being serious enough about funding what’s ahead.” And I noted that it was the coming challenges in terms of the ageing population and in particular related health care and superannuation costs that had prompted the last Tax Working Group to propose a capital gains tax.

Several other commentators weighed in as well, and I’d recommend reading in particular what I thought was some fairly insightful commentary from Gareth Kiernan, the Chief Forecaster at Infometrics. He noted something that’s been a theme of this podcast for some time, that New Zealanders are already paying significantly more tax due to the issue of bracket creep because income tax thresholds had not been adjusted since 2010. Governments had benefited from inflation moving people into higher tax brackets.

But in his opinion, this policy,

“It reduces discipline on government spending and muddies the tax and welfare decision for voters. It would be more appropriate for tax thresholds to be indexed to incomes or inflation, so that if any government wanted to alter the income tax rates or thresholds, they would need to articulate the reasons for their policy.”

He also went on to note,

“..in the current environment, one might argue that there needs to be more investment in infrastructure, and more funding for healthcare, and therefore taxes need to go up to pay for that. Alternatively, one might argue that there has been considerable expansion in government spending in recent years with few results to show for it, so spending needs to be reined in and taxes can be cut to go alongside that change.”

Now, I posted a link to this story on LinkedIn and it provoked a lively debate. A couple of people came back straight away with the reasonable assertions if we cut out wasteful expenditure and enforce the tax legislation, we would have sufficient income and that we may not necessarily get a better economy or better outcomes for people by increasing tax.

What is the state of the Government’s finances?

Now, the question of how much the Government spends is quite relevant in this particular example, because this week and providing some context, the Government’s financial statements for the year ended 30th June 2023 were released.

Tax revenue was up +$3.9 billion on June 2022 to a total of $111.7 billion. But that’s actually about $3 billion less than what was projected in the Budget in May. And the main reason for that fall is that corporate tax income at just under $18 billion, is -$2.4 billion below forecast, although higher withholding taxes on interest and dividend income has somewhat compensated for that fall. The GST take was bang on with what was projected at the Budget ($28.13 billion)

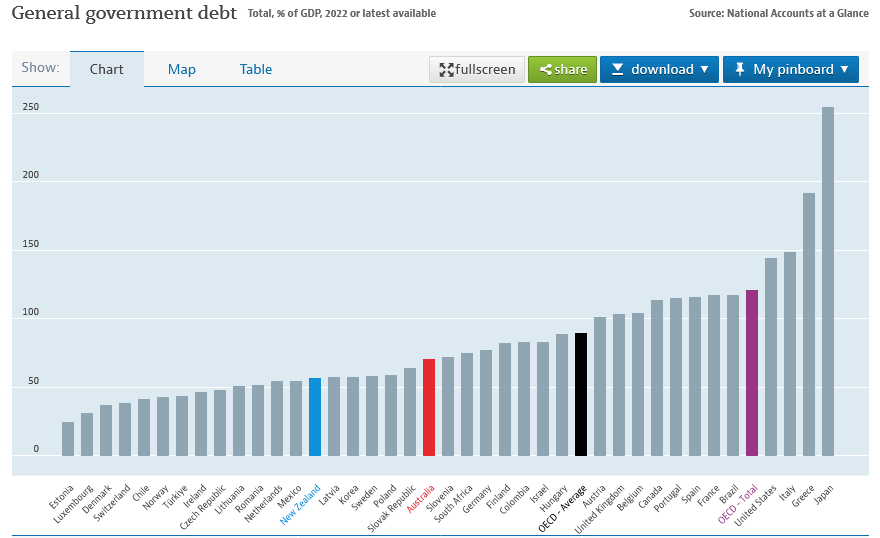

Ultimately the Government overall had an operating deficit before gains and losses of $9.4 billion. There’s been a lot of debate about government spending and core Crown expenses as a proportion of GDP were 32.2% of GDP, which is down from 34.5% in the June 2022 year. And the reason for that is the end of the COVID 19 restrictions and support that was given. Net debt is 18% of GDP, which is incredibly low by world standards.

And actually, here’s something we’ve I’ve mentioned before, but perhaps isn’t really known is that we are currently one of the few countries, according to our financials where the Government has positive net worth.

The government has net wealth of about 46% of GDP, whereas some countries such including Australia, which surprises me, are actually negative. Obviously, the big standout here is Norway, thanks to its trillion-dollar sovereign wealth fund.

The OCED measures of debt is slightly different, but general government debt is still below the OECD average. But like the commentators who are thinking we should be looking at our spending, I’m of the view we need to be investing in our infrastructure beyond roads.

But one of the things that puzzles me and it’s always brought up about government spending, it seems, is that somehow $55 million was spent on a proposed cycleway across the Auckland Harbour Bridge, which never eventuated. And then there’s a significant amount of money that’s gone into mental health, but yet doesn’t seem to have found its way to the frontline. So, I definitely agree with the view that there’s questions to be asked about the quality of our spending and how effectively it’s deployed is the quality of our public service able to deliver on what’s required? It may mean the answer is a combination that we do need more funding, but also we may actually need to invest in the capacity of bureaucrats to actually deliver.

The climate change bills arrive for Auckland ratepayers and us all

But the key point I want to come back to about the costs ahead which we’re not hearing enough about from the two main parties, is how are we going to manage the impact of climate change? This week, remember, Auckland Council has just signed off on the process of what’s to happen with a buyout of 700 properties that were red stickered following the January and February floods. That’s going to cost a total of $774 million, $387 million of which is going to come from the government.

Of note here and it’s something quite a few people have raised a red flag about, is that although insured Category 3 property owners will receive 95% of the the pre-flood market value, those who were uninsured will receive 80%. This raises the issue of moral hazard – if that’s what’s going to happen why bother insuring.

This is a big issue that I think we have to discuss: how are we going to fund all of this? Then if we are going to be in a scenario where we have to be buying out property owners, is buying out uninsured people fair for the those who have insured themselves? Is this approach a fair cost both to the people in the affected local government area and those generally in the wider population, because that’s who’s funding these buyouts.

In my view this is going to be a bigger issue because, I want to repeat again, we have so much of our wealth tied up in property, and yet property is the asset class that is most exposed to the effects of climate change. We’ve had Auckland with 700 homes, and over on the East Coast there’s another 400 homes, I believe, where this buy out process is underway.

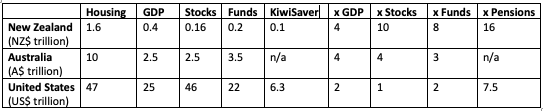

If we are going to be assisting property owners, and I believe we should, is the quid pro quo that the level of taxation on property rises? Bernard Hickey had some interesting stats in his daily Substack The Kākā around how much of our wealth relative to the country’s GDP is committed to housing. A total of $1.6 trillion, or four times our GDP, is committed to housing. But more importantly, although that’s not so out of line with other countries, it dwarfs our other investments

This royally skewed set of incentives is why our housing market is worth NZ$1.6 trillion, which is four times our GDP (NZ$400 billion), 10 times the value of our listed companies (NZX total market value of $160 billion), eight times larger than our total managed funds sector ($200 billion including NZ Super Fund and ACC) and 16 times larger than our only-very-marginally-incentivised household pension funds (Kiwisaver at $100 billion). For comparison, Australia’s housing market is worth the same four times GDP, but is worth four times stocks, three times and funds under management. In the United States, its housing market is worth twice GDP, once the stock market, twice funds under management and 7.5 times its comparable ‘subsidised’ household pensions market, which is known as 401k in America, rather than KiwiSaver.

Bernard believes, and I agree having looked at it when researching Tax and Fairness this overinvestment is a by-product of our tax settings. Therefore, if we change those tax settings around the incentive to invest in property that may change two things. One, we invest in more productive assets. And two, we raise the revenue to help deal with the coming crisis around climate change.

Will the Election change the discussion?

But at the moment it has to be said that funding the cost of climate change is not part of the two major parties’ discussions around tax, but who knows? My view is the debate around tax policy and our tax settings isn’t going to end with the Election next Saturday, it’s going to continue beyond that. In my view these issues around funding climate change will accelerate. If we can come to some form of multi-party accord on this, I think it will be better for us. But tax is politics, so don’t be holding out too much hope for agreement soon.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

At last week’s International Fiscal Association’s Trans-Tasman conference, a lot of the discussion among New Zealand advisors outside of the seminar rooms was around the state of tax policy. There is a growing concern that a more active government with interventions and proposals such as the proposed zero rating of GST on fruit and frozen and fresh fruit and vegetables is undermining the Generic Tax Policy Process which has been in place for nearly 30 years.

Like many practitioners, I’ve been involved with the GTPP at various stages. It is well-regarded internationally and has operated since 1994. It is intended to ensure

“better, more effective tax policy development through early consideration of key policy elements and trade-offs of proposals, such as their revenue impact, compliance and administrative costs, and economic and social objectives. Another feature of the process is that it builds external consultation and feedback into the policy development process, providing opportunities for public comment at several stages.”

However, the concern is emerging that against this well-established background more recent measures such as the Tax Principles Bill, or the legislation that enabled Inland Revenue to carry out its high wealth individual research project, have happened outside the GTPP framework. The proposed GST zero rating of fresh and frozen fruit and vegetables could be another example. These developments are unsettling the previously predictable process for working through and discussing tax proposals.

I’m of the view that tax is fundamentally about politics and politicians will always make political calls. The GTPP is intended to minimise the effect of that and give more predictable tax policy outcomes. But you can’t eliminate it entirely and this dichotomy between efficient tax policy process and politics will always be there.

There is also the question raised in an interesting story this week by BusinessDesk (paywalled) in reference to the work of the Corporate Taxpayers Group (CTG) about when consultation ends and lobbying begins. The CTG includes the main corporate taxpayers such as Fonterra and the four big banks. The New Zealand Superannuation Fund, the largest single taxpayer in the country, is also a member.

The CTG meets regularly at the offices of Deloitte (more frequently than I had imagined) as the story outlines, and there is an annual membership fee which is to pay for the secretariat, which will make submissions to Parliament and to Inland Revenue.

But when does this move from consultation to lobbying. Very difficult to say. I don’t see it as lobbying although I do appreciate the risks that might be involved in that. But having been involved in the process and been in meetings with CTG representatives, Inland Revenue officials, I don’t believe that’s the case.

But as I said, I can understand why some might be concerned by this. It comes back to a key part of any democracy, and that’s transparency. But on the whole, as I said, I think New Zealand’s been very well-served by the GTPP. And I know that internationally it’s very well regarded because it has got a stability of process to it.

I think one of the issues that’s causing raising concern is because left wing governments are likely to more interventionist. But I do think this situation is exacerbated at the moment because the strain of the boundary between capital and revenue, and our general under taxation of capital, the lack of a capital gains tax, wealth, tax, death duties, are putting strains on the system. And so, politicians are trying to find shortcuts to try and deal with this issue and the need for more revenue. You can dispute how much is needed. But when I look at the state of roads and hospitals and you see the growing bill for climate change, my view is and it’s also the view of Treasury, as I pointed out a number of times, and its Long Term Insights Briefing He Tirohanga Mokopuna we need more revenue.

A whole lot of hissing

So, there are strains emerging and it’s impacting the GTPP, which makes tax advisers understandably a little unsettled about how well that process will continue. As Louis XIV’s finance minister Jean-Baptiste Colbert said in probably one of the most famous maxims about taxation: “The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing.” That was true in the 17th Century and remains true today. And there is quite a lot of hissing going on at the moment.

The GTPP in operation – consulting on trading stock

Moving on and still on to the topic of consultation and an example of the GDP in operation. Inland Revenue has released a paper for consultation on the treatment of trading stock disposed of below market value.

At present, whenever trading stock is given away, or disposed of for below market value it’s deemed to have been disposed of at market value. The reason for that rule is reasonably solid. It’s to counter potential tax avoidance where the stock is given away or may be used for private consumption by a business owner or sold at a deep discount to associated persons. In some cases, it could apply for a particular industry, exchanges of stock could take place at cost or less. All of those generate benefits in terms of the under taxation of revenue. So that’s why that rule exists.

But there have been instances where businesses have wanted to give away stock and make donations for charitable purposes, and that’s when this rule becomes problematic because they can’t effectively do so. Over time the practice has developed for granting temporary emergency relief in some situations as a work-around.

In 2004 a permanent override was put in place with donations to farming, agricultural and fishing businesses during what is termed an adverse event. And there have been a large number of those weather-related adverse events either for drought or like we’ve experienced this year, flooding.

Between 2010 and 2012, there was a temporary override for 18 months in response to the Canterbury earthquakes. And then again, starting in March 2020, a temporary override was put in place for four years in response to COVID 19.

That override will end on 31st March next year, and the object of this consultation paper, is to propose a more permanent solution rather than using ad hoc solutions whenever we encounter a particular scenario such as COVID or earthquakes.

The consultation paper runs to 29 pages and includes a useful appendix which summarises all the potential summary policy options and how they may play out. Overall, this is a good example of the Generic Tax Policy Process in operation. Consultation on the paper is now open and closes on 6th September.

Managing retreat & how to pay for it.

As just mentioned, temporary emergency relief from the usual stock donation rules has been granted for a number of reasons, including this year, the flooding in January and February and the impact of Cyclone Gabrielle. A constant theme of this podcast is the question of environmental taxation and the need to address the longer-term question of how we going to pay for these climate related events.

Earlier this week a Government expert working group released its report on the question of what’s termed managed retreat.

The report, which clocks in at 284 pages, is very comprehensive and raises a number of potential scenarios and alternative measures that could be needed. One of which, as the excellent Newsroom story covering the report notes, is conditional powers to basically force people to leave particular areas that are under threat.

Being a tax podcast the question we are most concerned about with environmental and climate change impacts is how we are going to pay for it. The report has two key proposals E65 and E66.

But consider this, we have currently 700 homes which have been rendered uninhabitable following the flooding in January and February. And there’s another 10,000 homes that require flood protection. The Government has said it will split the costs over the uninhabitable homes with local councils affected. But, as far as I can tell, neither the councils nor the Government have really fully funded for these costs of maybe a cool billion or so this year and maybe every year and rising. So, it is an issue that needs to be addressed.

The report has some interesting discussion around what happened in Canterbury in relation to the earthquakes and then the first and I emphasise, first, example of managed retreat, from the Bay of Plenty settlement of Matatā

The report says, however we decide to fund this, the funding should not be subject to the usual vicissitudes of the annual budget round because that would mean it would lead deferment and dangerous delay. When it comes to kicking a football down the road, the politicians, as we know, are better than the Football Ferns at kicking it a long way out of trouble. Or so they think, but the issue still remains. I totally agree, therefore, with the report’s recommendation that there has to be a permanent funding solution.

I maintain that if we are going to do something around the lines of environmental taxation, the funds that are allocated to it should be hypothecated, and certainly not form part of the consolidated fund because we’ll then have politicians tempted to raid those funds. We’ve seen this in the recent Auckland Budget Council, by the way, where reserves built up for environmental purposes were used for other purposes.

In terms of holding politicians to account, I think we need to be asking a lot more questions about them on this matter because this is going to affect us all. We’ve had a miserable winter with extensive flooding and the ground is sodden. What happens when the next big floods come along, who pays for the clean-up?

No longer friends with Russia…

At the International Fiscal Association Trans-Tasman conference last week, we spent a lot of time discussing double tax agreements. It so happens, Russia has decided to suspend its double tax agreements with 38 countries, which it considers are now ‘unfriendly’ in the wake of the invasion of Ukraine. New Zealand is on that list. So that probably means that for someone in Russia trying to claim tax relief from under the double taxation between New Zealand and Russia, they’re out of luck and they’re probably going to be facing higher tax bills as a consequence.

TikTok and GST fraud

And finally, just on the topic du jour this week of GST, there’s an absolutely extraordinary story coming out of Australia about how social media influencers on TikTok encouraged at least 56,000 people to take part in a A$1.6 billion tax fraud scheme. Apparently these TikTok influencers explained how to get fraudulent GST refunds. The scam involved obtaining an Australian Business Number, then filing Business Activity Statements (the equivalent of GST returns) and claiming false GST refunds. In some cases, there were attempts to claim refunds of up to A$100,000.

The Australian Tax Office apparently is still grappling with the sheer size of the scandal. There’s a story in the Australian Financial Review about a Victorian woman who managed to stay out of jail, after repeated attempts to try and get A$115,000 fake GST refunds for a dog grooming business that had been set up more than a decade ago but had been largely dormant until 2020 before she attempted to pull this scam.

Fascinating story which will be interesting to see how it plays out. To me it lends support to the suggestion that we should look seriously at zero rating transactions between GST registered businesses. It should be a means of stopping such attempted frauds. Obviously, if that proposal is taken forward, it should go through the proper Generic Tax Policy Process consultation.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.