- And issues draft guidance on the taxation of share investments and tax

- The Olympics, a cautionary tale involving Snoop Dogg

Earlier this year in June, we talked about Inland Revenue’s releasing insights from its first round of a hidden economy campaign focused on smaller liquor outlets around the country. It noted that in this first stage, compliance staff had made 220 unannounced visits nationwide, looking for signs of issues such as income suppression, unreported sales and non-registered staffs. And it noted that although most of the businesses had their tax affairs in order, unfortunately some hadn’t.

That was described as a deliberate light touch campaign. And Inland Revenue said at the end of that release that more unannounced visits to businesses will be made as it steps up its compliance work

Well, last week we saw the second stage of that, where it announced that from 14th of August it will be sending letters to taxpayers in the liquor industry selected for a possible visit. This time Inland Revenue community compliance teams will be visiting liquor store businesses, including independent and franchise liquor retailers, across most locations. But this does not include bars or hospitality venues. I’d surmise they’ve got a separate plan for that group of taxpayers.

These teams will be looking at income suppression, record keeping practises – including when using cash – and employer obligations. All it’s said is that they will be issuing letters as of 14th of August, which meant they started going out last week. So, if you’ve been selected for one of these visits, I suggest you review your practises to see what areas could possibly be at risk. And certainly talk to your accountant or tax agent if you have one.

This isn’t surprising, Inland Revenue foreshadowed this in June. Remember they got an extra $116. million over four years in the budget to ramp up their compliance activity. This is merely the tip of the iceberg.

Inland Revenue’s harder line

What I and other tax agents are also noticing elsewhere, is that Inland Revenue has certainly adopted, let’s say, a harder edge in its approach. We’re now getting requests for information in situations where previously that didn’t happen, and I’ve heard one or two somewhat unsettling stories of borderline bullying of taxpayers.

I’m all in favour of ramping up compliance, but it’s always worth remembering that any tax system, even one as remarkably compliant as ours is, does depend on the goodwill of the taxed to enable its smooth operation. And I would just hope that Inland Revenue would keep that in mind. Because sometimes dropping a heavy hammer on those who’ve made innocent mistakes doesn’t actually achieve very much for the wider perceptions of the integrity of the tax system.

But that said, there’s nothing really surprising in this Inland Revenue campaign. And I expect I’ll be talking more about new investigation initiatives in other areas over the coming months.

Taxing share investments – what are the rules?

Moving on, an area where we spend quite a lot of work advising clients on is the question of share investments, particularly in relation to offshore shares. Although the Foreign Investment Fund regime in its current iteration, has been in place for a very long time, nearly 17 years in fact, it’s probably not as well-known as Inland Revenue perhaps might expect.

I think what I sometimes see in this space is that people coming from other jurisdictions which have a capital gains tax regime, pretty much assume it’s much the same approach here. So, it’s helpful that Inland Revenue last week released some draft guidance on the taxation of share investments for consultation.

The draft guidance runs to 43 pages including some detailed appendices and as always, there are a couple of helpful fact sheets attached. One explains when the FIF rules apply, and the other one summarises the general treatment of share investments.

The draft Interpretation Statement covers what happens when an investor is investing in shares, what liability do they have for dividends, share sales and how these rules interact with the Foreign Investment Fund rules.

Interestingly the guidance refers to share lending arrangements and foreign currency accounts.

“the statement focuses on investments who use online investment plan platforms, although the principles in this statement apply more widely to other share forms of share investments by individuals such as through brokers”.

This tells me that Inland Revenue have been collecting data through the Common Reporting Standards (CRS) on the Automatic Exchange of Information. Just before COVID arrived Inland Revenue had begun marrying up the data that they started receiving in 2018 and 2019 under CRS. Based on this it had started to ask questions of taxpayers, who they knew through the CRS information, had some form of offshore investment, but did not appear to have included that in their tax return.

So, I suspect this is another development in what I just talked about a few minutes ago – Inland Revenue ramping up its compliance activities.

Which set of rules?

Now, as the guidance and the fact sheets explain, there are two treatments at play here. The Foreign Investment Fund regime generally applies to all shares outside Australasia. And not to get into too much detail about that, just always be careful that some listed stocks in Australia do actually represent FIF interests. Shares outside the FIF regime such as those listed either on the New Zealand Stock Exchange or on the Australian Stock Exchange are subject to the “ordinary rules”.

The guidance explains when the ordinary rules will apply and when the Foreign Investment Fund rules will apply. And one of the things that it picks up on is what is the tax treatment where a taxpayer has realised gains from the disposal of shares? The general rule under section CB4 of the Income Tax Act 2007 is that those amounts from selling shares are taxable, where the shares were acquired for the “dominant purpose of disposal or were part of a share dealing business or profit-making scheme.”

Determining the dominant purpose

Now deciding what an investor’s “dominant purpose” is done at the time the shares are acquired. The investor’s stated purpose is tested against a combination of objective factors. And it’s often the case, that an investor may have one purpose or more than one purpose, or not even really any clear purpose when buying shares.

The onus is on the investor to prove that their dominant purpose for buying shares was to dispose of them, or conversely, not dispose of them. The guidance notes an investor only has to prove that disposal was not their dominant purpose. They do not have to prove an alternative dominant purpose.

Generally speaking, share sales will not be taxable if an investor can show that the shares were bought with the dominant purpose of receiving dividend income, receiving voting interests, or other rights provided by shares or a long-term investment growth in assets or portfolio diversification. Other than situations “Where at the time of acquisition this is planned to be achieved through sale.”

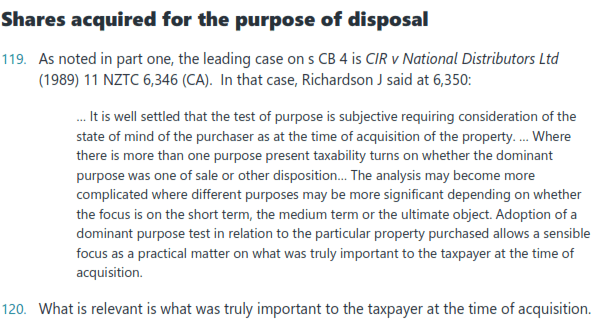

The appendix here has some interesting commentary from case law, most notably is the Court of Appeal decision CIR v National Distributors. Inland Revenue had lost in the High Court but appealed, and their appeal was upheld two to one in the Court of Appeal, with Justice Richardson giving the main judgement.

The taxpayer National Distributors had made eight purchases and sales of shares over a two-year period. The shares were held between eight months and three years with an average of 19 months before sale. The dividend yields were inconsistent and ranged from less than 3% to over 11% year, depending on the shares. Overall, the dividend yield was 6.5% per year compared with 25%-year from gains on sales.

Richardson noted that share purchases fell into two categories. Some were purchased for family reasons, but the second group were held to have been acquired, on the facts, for the purpose of sale. The taxpayer did not in the court’s view establish that there was no dominant purpose of sale.

In summary another useful interpretation statement and fact sheets. It’s good to see Inland Revenue putting some general guides and clarifying the point around when someone is subject to the Foreign Investment Fund regime, and when the ordinary rules will apply.

Tax and the Olympics

And finally, this week congratulations again to our Olympians for their fantastic achievements. I greatly enjoyed the Olympics as I’m sure everyone did. Not just because of the great performances by so many New Zealand athletes, but also just the sheer spectacle of watching the best in their sport.

One of the more entertaining parts of the Olympics was that the American TV channel NBC sent across rapper and record producer Snoop Dogg to provide commentary on the Olympics. Some of what he got up to was quite hilarious, check out him dressed up for a dressage event for example.

All good fun but the sharp-eyed Andy Bubb, Special Counsel, Tax Disputes at the Australian law firm Clayton Utz has pointed out that Snoop Dogg has possibly ended up with a fairly hefty French tax liability.

Apparently, he was paid USD 500,000 a day for his work, and what Andy Bubb has noted, is that under Article 17 of the double tax agreement between France and America, France has the right to tax the earnings of an entertainer or sportsperson where the activities are carried out in France. Now you can’t divert the income to an entity under the tax treaty because that’s overruled as well. As France’s top marginal tax rate is 45% the multimillion dollar question arises did Snoop Dogg’s advisors deal with all the ramifications of his entertaining and well-paid gig at the Olympics?

Never mind Snoop Dogg, what about Hamish?

Now, being a nerd, I took a look at the double tax agreement between New Zealand and France and yes, a similar clause is in there for artists and athletes. Accordingly, if you are competing in France and you are paid, you will be taxed. And this might actually be of relevance for Hamish Kerr because as I understand it, the track and field gold medallists each got US$50,000. France might be looking to take a cut of that.

But there is an exception in Article 17 of the treaty where any payment made to an artist, or an athlete will only be taxed in the jurisdiction where that athlete is resident – New Zealand – if those activities (carried out in France at the Olympics) are supported substantially by public funds from New Zealand.

I’m guessing most of our Olympians are heavily supported by public funding which should mean that any payments that our athletes receive for winning medals, or in relation to their activities in Paris, are only taxable in New Zealand thanks to this exemption under the double tax agreement. It would be interesting to see what comes with this. (It’s also worth noting that although the International Olympic Committee earns billions from the Olympics, the majority of the athletes receive nothing for their efforts).

I thought it was an entertaining wee story, but it also highlights a common issue and something that people perhaps don’t appreciate. That artists and entertainers have some of the most complex tax planning issues of any individual, certainly outside the hyper wealthy and multinationals. That’s because when they trade, carry out gigs in various jurisdictions, they are potentially triggering tax liabilities in every country in which they perform. But in this particular case, although Snoop Dogg may have a tax problem, I’m hopeful that no such problem will be encountered by Hamish Kerr for his winnings.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.