Terry Baucher crunches the numbers around corporate tax and says anybody expecting the Tax Working Group to suggest a cut in the tax is going to be disappointed

Anyone who thinks the Tax Working Group will suggest a cut in company income tax in its interim report due to be released next month is going to be disappointed. Recently released papers prepared for the TWG concluded a cut was “unlikely to be in New Zealand’s best interests.”

The papers also contain some fascinating data about the size and profitability, or otherwise, of various industry sectors.

To cut or not to cut

At 28% New Zealand’s company tax rate was the 10th highest in the OECD in 2017. It is also above the unweighted OECD average of 24.9% for the same year. However, this doesn’t take into account the imputation regime which means the final tax rate for New Zealand tax resident investors is the shareholder’s marginal tax rate. As a result of the imputation regime the effective tax rate for New Zealand resident shareholders is the sixth lowest in the OECD.

Unless a company tax rate cut was accompanied by a reduction in personal income tax rates, the main benefit for New Zealand resident investors would be the opportunity to accumulate income taxed at a lower rate before distribution at which point it would be taxed at personal income tax rates. According to Inland Revenue the existing five percentage points gap between the company tax rate and top individual tax rate has encouraged “a variety of arrangements that…allow taxpayers to avoid the intended taxation of dividends on the distribution of income or assets from companies to their shareholders”. (As the same paper later notes some of these “integrity issues would be reduced if a capital gains tax were introduced.”)

These integrity issues plus additional complexity are also cited as reasons against a lower tax rate for small businesses. In addition, officials consider a small business tax rate is likely to reduce overall productivity, a long-standing problem for New Zealand. There is also the possibility that a small business tax rate might act as a disincentive to growth for businesses, a criticism the Fraser Insitute in Canada raised of a recent Canadian government proposal.

Nevertheless, New Zealand’s comparative position within the OECD is likely to worsen following the dramatic cut in the United States corporate tax rate from 35% to 21% with effect from this year. A cut in company tax rates is sometimes suggested so that New Zealand can remain “competitive”, so at first sight it seems likely pressure for a corporate tax cut may increase as company tax rates fall internationally.

Conversely, one of the key arguments against a company tax cut was the issue of “location-specific economic rents.” Economic rents are the returns over and above those required for investment in New Zealand to take place. As the paper notes these returns are “likely to be larger in a geographically isolated market like New Zealand where supply of certain goods and services is likely to require a physical presence in New Zealand.” In short, such returns can be taxed without discouraging investment as New Zealand’s location means investment remains viable despite taxation. In other words, if overseas investors are making a return with a 28% company tax rate, there is no need to incentivise them to invest with a lower tax rate. In fact as officials noted doing so would not be in New Zealand’s interests as more of the benefit would flow to non-residents.

Another revealing insight was that there appears to be little correlation between a cut in company tax and an increase in foreign direct investment (FDI). Despite a cut in the company tax rate from 33% to 30% in 2008 and then to 28% with effect from 1 April 2011, there was no surge of FDI into New Zealand either absolutely, or relative to Australia as the following graph illustrates:

There may have been other factors at play but as officials noted “it should at least cause us to question any assumptions that company tax cuts are likely to be a silver bullet for increasing the level of FDI into New Zealand.”

A narrow base?

Separate from the issue of company tax rates, another background paper analysed the effective tax rates for companies. Although results were advised as “indicative only” the paper threw up some interesting and at the same time potentially alarming statistics.

The analysis focused on “significant enterprises” (groups of entities with annual consolidated turnover greater than $80 million) over the 2013 to 2016 tax years. Apparently, there are only about 500 such enterprises in New Zealand and between them they are responsible for about 51% of the total income tax paid by companies ($12.6 billion for the year ended 30 June 2017). Furthermore some 20% of these enterprises have either a tax or accounting loss and therefore did not have effective tax rates calculated for the purposes of the paper.

Overall the unweighted average tax rate for those profitable enterprises was 28%, or exactly in line with the company tax rate. However, once adjusted for the relative size of the enterprises, the weighted average rate fell to 20%. That in itself masked substantial variations between industries. 21 industries had effective unweighted company tax rates of less than 25%. In particular, the unweighted average effective company tax rate for the insurance and superannuation fund, residential care services, and motion picture and sound recording activities industries was 16%. Remarkably, 38% of the enterprises within these three industries were making a tax loss even though only 11% reported an accounting loss.

To help explain the variation in effective tax rates, the paper then reviewed the major tax adjustments in the 2015/16 tax year. Based on a sample of large enterprises which had approximately $13 billion in net taxable income for the year, the three most significant adjustments which decreased taxable income relative to accounting profit were untaxed realised capital gains amounting to $2.2 billion, unrealised valuation gains ($1.3 billion) and untaxed overseas dividends of $1 billion.

Conversely, those adjustments which increased taxable income included non-deductible accounting write-downs ($1.1 billion), non-deductible capital losses from sales of fixed assets ($600 million) and other non-deductible expenditure such as goodwill write-offs ($280 million).

The paper also looked at the untaxed capital gains for small and medium companies over the same four tax years. It found the average yearly value of untaxed capital gains was $2.2 billion with companies within the rental, hiring and real estate services averaging gains of $763 million each year. The research also noted that the following four industries had particularly high proportions of untaxed realised gains when compared with the accounting profits of the industry:

Accommodation and food services (64%)

Agriculture (53%)

Rental, hiring and real estate services (40%)

Financial and insurance services (27%)

In something of a throwaway comment the paper remarked that “the majority of small and medium enterprise are in a loss position”. Given the number of small businesses in New Zealand it’s not reassuring to hear that many are in loss.

What does all this mean? Quite apart from reducing the likelihood of a company tax rate cut, the analysis shows the relative importance of untaxed capital gains to several industries. After noting “the primary cause of under-taxation is untaxed capital gains, both realised and unrealised” officials then asked the TWG “Does this information affect the Group’s views on business and company tax”. We’ll know the answer next month when the TWG’s interim report is relased but defenders of the status quo on the taxation of capital gains are likely to have their work cut out.

Terry Baucher crunches all the tax news in the Budget, and says going into the 2020 election is when we might see changes in tax thresholds

With any major tax initiatives all kicked over to the Tax Working Group for review, unsurprisingly the Budget made no changes to existing tax rates and thresholds.

No increases in thresholds results in extra tax revenue through the effect of ‘fiscal drag’ whereby individuals pay more tax as their earnings ‘drag’ them into higher tax brackets.

For the year to 30 June 2018 the fiscal drag effect is calculated as $276 million. By 30 June 2022, when the total tax take is predicted to rise by almost 25% to over $103 billion, it will be $398 million.

At some stage thresholds, which have not been increased since 2010, will need to be adjusted, but for the moment the government, like its predecessor, is happy to collect the additional revenue.

Two significant tax changes were announced prior to the Budget. The major initiative is the ring-fencing of residential property losses. From 2020 it will no longer be possible to offset losses against other income. Instead the losses must be carried forward for future use. The additional tax collected as a result of this change is $125 million for the June 2021 year rising to $190 million for the June 2022 year.

The other change – and one likely to affect more taxpayers – is the introduction of GST on low-value imported goods from 1 October 2019. The current estimate is for this measure to raise $218 million between 1 October 2019 and 30 June 2022.

In the meantime, Inland Revenue will get a further $31.3 million of funding over the next four years to boost compliance. $23.5 million of this is specifically targeted at ensuring outstanding company tax returns are filed.

Another $3 million is to analyse the potential for improved tax compliance in ‘specific industries’ through better third-party reporting and withholding taxes. This is probably aimed at contractors not currently covered by the PAYE rules.

Overall, Inland Revenue expects to recover approximately an additional $239 million over the four years to 30 June 2022 from enhanced compliance activities.

There’s some more details about the Research and Development tax incentive which will involve $1 billion over four years. Eligible businesses spending more than $100,000 annually on R&D will get a rebate of 12.5 cents for every dollar of R&D spend.

In a nod to the Deputy Prime Minister’s love of racing the bloodstock tax rules will change to allow deductions to be claimed for the “costs of high-quality horses acquired with the intention to breed.” A snip at $4.8 million over the next four years.

Migrants can expect to pay another $113 million in fees over the next four years, and the Immigration Levy is expected to raise another $44.7 million over the same period.

The relative narrowness of our tax base, the implications of the gig economy and technological change, and the international pressure for lower corporate income tax rates to name a few. For me three areas stand out: the scale and potential impact of demographic changes underway; the potential role of environmental taxes; and the taxation of capital and savings.

But my biggest initial impression is how the decision to exclude consideration of taxing the family home, or the land underneath it from the TWG’s terms of reference, hangs over the paper like Banquo’s Ghost.

A demographic timebomb?

My first major conclusion from the Submissions Background Paper is how much the coming fiscal pressures of an ageing population really need to be kept front and centre when considering changes to the tax system.

The paper begins by setting out key risks and challenges for the tax system over the next 30 years or so. A key baseline is the Government’s fiscal objective of maintaining taxation at the historical level of 30% of GDP over time. At the same time the paper identifies the pressure of changing demographics and an ageing population. For example, for the current year to 30 June 2018 New Zealand Superannuation is expected to cost $13.7 billion, “more than all other benefit payments combined”.

As a result of these pressures, the paper projects the Government will have a primary deficit of 1.2% of GDP by 2030 (about $3.4 billion based on current GDP), rising to 4% of GDP in 2045 or $11.4 billion based on current GDP. Very clearly then as the paper warns;

“If the Government is to continue providing healthcare and superannuation at current levels, then the level of taxation will need to increase, or spending on other transfers or publicly provided goods and services will need to fall.”

Against this backdrop the work of the TWG and the recommendations it will make are hugely important. Change is coming and therefore the tax system needs to be ready for that.

Taxing the environment

The environment is hugely important to the New Zealand economy whether it is liveable or for our two largest export earners agriculture and tourism. New Zealand is committed to reducing net emissions 30% below 2005 levels by 2030 so the Background Submissions Paper suggests;

“Using the tax system to ensure that consumers and producers face the costs of emissions and other environmental harm could be one way we can meet our international obligations.”

The paper also notes that New Zealand had “the second highest level of carbon emissions in the OECD per dollar of GDP in 2017”, an alarming statistic which suggests action is needed sooner rather than later if we are to maintain the idea of being clean and green.

At present environmental taxes such as petrol excise duties and waste levies amount to approximately 4.2% of total tax revenue, or about 1.3% of GDP. This puts New Zealand at the low end compared with other OECD countries. For example, almost 15% of Denmark’s total tax revenue is made up of environmental taxes and these represent just over 4% of GDP. Across the Ditch, Australian environmental taxes are just over 2% of GDP, representing 8% of all taxation.

A recent OECD paper noted that in 2015, outside of road transport, 81% of emissions were untaxed. The report concluded tax rates were below the low-end estimate of climate costs (€30 per tonne of CO2) for 97% of emissions. New Zealand at €0.48 per tonne of CO2, was sixth from bottom of the 42 countries surveyed.

There would therefore appear to be significant opportunity for shifting some part of the tax burden onto environmental taxes. However, as both the Background Submissions Paper and the OECD notes many environmental taxes are “poorly designed and targeted.”

Wealth inequality and savings

The TWG’s terms of reference may have excluded taxing either capital gains from the family home or the land underneath the family home, but considering the taxation of savings is within its remit. So too is the issue of inequality and the Background Submissions Paper has a wealth (pun intended) of charts illustrating the issue of income and wealth inequality. (See Figures 12-19 between pages 33 and 38 of the report).

Ominously, the paper comments that over the past three decades the “inequality-reducing power of the tax and transfer system on market income inequality has steadily declined”. Furthermore, the inequality-reducing power of the tax-benefit system is now below the OECD average.

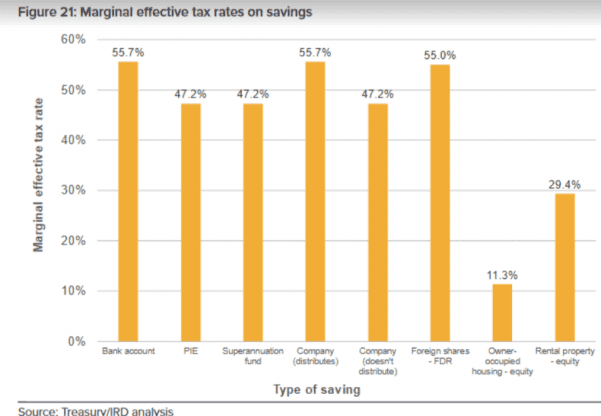

Tied into the issue of inequality is the taxation of household savings. It’s here that the impact of the terms of reference loom largest. After assuming a risk-free rate of return of 3%, inflation of 2% and a 33% tax rate to determine a marginal effective tax rate, the Background Submissions Paper then applied this to calculate the marginal effective tax rates of various asset classes. Its conclusion: “owner-occupied and rental housing is undertaxed relative to other assets.” The extent of the under-taxation is starkly illustrated by Figure 21 (reproduced below).

At 55.7% the marginal effective tax rate on bank savings is almost five times that of the 11.3% rate applicable for owner-occupied housing equity and nearly double the 29.4% rate for rental property.

The Reserve Bank estimated the value of housing as at 30 September 2017 to be over $1 trillion. Even excluding residential rental property (perhaps a third of the total), this is a huge amount of capital to be left essentially untaxed. The holders of that property are mostly older and wealthier, a growing number of which are receiving New Zealand Superannuation. As Andrew Coleman noted last year, changes to the tax system in the late 1980s established a huge incentive in favour of housing. This created an inter-generational timebomb which will need to be defused at some point.

Much of the immediate debate on the Background Submissions paper has been about the efficacy and impact of a capital gains tax, but there’s been little discussion about the ongoing fiscal impact of continuing to exclude maybe $700 billion of capital from taxation with potentially very adverse outcomes for future generations.

Overall the Submissions Background Paper includes plenty of thought-provoking material to consider. The paper also underlines what was apparent from the outset; excluding the taxation of the family home created a big hole at the heart of the review.

Whatever the final recommendations of the TWG are for addressing the future sustainability of the tax system there’s a danger it will be found as Macbeth warned after killing Duncan to “have scotched the snake, not killed it”. Only time will tell.

Terry Baucher on Google, tractors, tax evasion, cashless society, taxing CO2 emissions, the Swiss cryptocurrency town, really big tax cuts, sugar tax, Nigeria’s census & more

Today’s Top 10 is a guest post from Terry Baucher, an Auckland-based tax specialist and head of Baucher Consulting.

We welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

If you’re interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

1) What’s a tractor in Australia got to do with Google?

“NZ strikes blow for global tax clampdown as Google shifts policy” was the headline in the Financial Times after Google revealed to Parliament’s Finance and Expenditure Select Committee it was going to change how it booked its revenue from New Zealand.

“We intend to shift our business model from this past approach, such that customers will enter into contracts with our New Zealand entity, which will generate revenue from NZ advertising customers, and pay taxes in line with its role in the transaction.”

So, will this mean more tax for New Zealand? Not necessarily because although the advertising revenue will no longer be booked in Singapore, Google New Zealand might still be charged for the right to use Google’s intellectual property.

Intellectual property and the right to use intellectual property is embedded in many more household objects than just smartphones. For example, farmers in Nebraska are demanding the passage of a law to enable them to carry out repairs to tractors which now contain millions of lines of software code.

Australian farmers are increasingly concerned that they may not be able carry out their own repairs on tractors purchased from America.

“If you buy a tractor, you buy a tractor and it’s yours. And the big companies are now trying to say if you buy a tractor, it’s not yours.

How long before Australian and New Zealand farmers may have to follow the lead of farmers in Nebraska and demand the ”right to repair” tractors?

2) Tax evasion.

Two tradies were recently jailed for each evading nearly $1 million in tax.

The tax department said Hamilton plasterer Paul Andrew Mills was sentenced on February 9 to two years and one month prison.

Auckland builder Hamish Paul Aegerter received a sentence of two years and seven months on Friday

“WILSON, a 64-year-old male from Chapel Hill Queensland falsified nine BAS to obtain $217,134 in refunds he was not entitled to. Documents provided at audit were determined to be false. He was convicted on two charges and sentenced to 36 months jail with a non-parole period of 12 months.”

“The director of a Gloucester security services company, who stole almost half a million pounds in tax, has been jailed for three years after an investigation by HM Revenue and Customs.”

It’s tempting given New Zealand’s ranking as the least corrupt country in the world to think tax evasion is a relatively minor matter.

In fact, as Treasury admitted in 2013: “There are no reliable estimates of the size of the tax gap in New Zealand.”

The same report then went on:

“A reasonable general order of magnitude for the tax gap across OECD countries would be 5 to 20 percent of total tax collections.18 This implies a tax gap for New Zealand of around $3-11bn. We expect New Zealand to be at the lower end of this general range owing to our general broad-base, low-rate tax settings, significant reliance on indirect taxes, and low levels of corruption – all things that are thought to be correlated with a smaller tax gap”.

This seems a naïve attitude but even at the lower end of the scale $3 billion of additional tax is not chump change.

And between 2010 and 2015, the number of cash payments in shops almost halved, from 39% to 20%.

At the same time, electronic payments have surged. Ninety-five per cent of Swedes have access to a debit or credit card, and made an average of 290 card payments a year in 2015. That’s well above the EU average, at 104 card payments per year.

“In Sweden companies can refuse to accept cash payments. This approach is already being used by some restaurants, public transportation and hotels. In Sweden the use of cash is decreasing, and approximately 80 % of all transactions are made electronically, including through new techniques such as smartphones and contactless payment methods. An app developed by banks in Sweden facilitates money transfers between private persons and make payments to companies, which has increased in use from 76 000 transactions in 2012 to 76 million transactions in 2015” (page 23).

As part of an anti-tax evasion programme, Sweden requires that sales must be registered in a cash register connected to a fiscal control unit. The immediate revenue effect once the requirements were introduced was a 5% increase in the reported revenues. This resulted in increased tax revenues of at least SEK 3 billion (€320 million) per annum as a result of reduced tax evasion. Something for Inland Revenue to consider?

4) Tax year end approaches.

The end of the 2017-18 tax year is fast approaching. The 31st of March is also the due date for tax agents to file clients’ tax returns for the March 2017 year. The pressure will ramp up on tax agents to meet the deadline.

In the UK, the deadline for filing 2016-17 tax returns was 31st January. According to HM Revenue and Customs a record 10.7 million “customers” filed before the due date with 92.5% of these completed online. As HMRC noted, it got a bit frantic towards the end.

There were 758,707 people who completed their return on the last day before the deadline and the most popular hour for customers to hit submit was from 4pm to 5pm on 31 January with 60,596 returns received (1,010 per minute, 17 per second).

Thousands of customers avoided any penalties at the last minute as 30,348 customers completed their returns from 11pm to 11:59pm yesterday.

The penalties for late filing can accumulate quickly so naturally people were quick to offer excuses including the following gems:

I couldn’t file my return on time as my wife has been seeing aliens and won’t let me enter the house.

I’ve been far too busy touring the country with my one-man play.

My ex-wife left my tax return upstairs, but I suffer from vertigo and can’t go upstairs to retrieve it.

My business doesn’t really do anything.

I spilt coffee on it.

No doubt Inland Revenue will soon be receiving a few creative excuses. It would be good to know whether aliens are also at work in New Zealand.

5) Taxing CO2 emissions from road transport.

New OECD reports on the taxation of energy use make uncomfortable reading for New Zealanders.

Road transport is taxed relatively highly, but other negative side effects of fuel use in road transport (e.g. local air pollution, congestion), suggest that taxes are still too low in most countries. Fuel taxes dominate price signals, carbon taxes play almost no role.

According to the OECD New Zealand has the lowest rate of taxation on diesel at €1.3 per tonne of CO2. (Road user charges are not taken into consideration). By comparison the UK charges €299.9 per tonne of CO2. When it comes to taxing petrol New Zealand imposes €184.8 per tonne with the UK again the heaviest taxer at €353.4 per tonne. Russia doesn’t tax either diesel or petrol and the US has the third lowest rates of taxation at €21.8 per tonne for diesel and €19.1 per tonne for petrol.

Based on these numbers the taxation of CO2 emissions represents a huge challenge to the New Zealand economy. The greater use of environmental taxes is within the terms of reference of the government’s Tax Working Group. It will be interesting to see what conclusions it reaches.

6) Swiss banking goes crypto.

Investors in cryptocurrency got a rude awakening at the start of the year when what Nouriel Roubini called “The biggest bubble in human history” appeared to burst. The price of bitcoin fell from just under US$20,000 in mid-December to US$6,000 on February 6th. According to CoinMarketCap, the total market capitalisation of cryptocurrencies has fallen by more than half this year, to under $400bn.

However, the volatility of cryptocurrencies doesn’t seem to have deterred the Swiss town of Zug which has been quietly developing into a hub for crypto-services with the encouragement of the Swiss government.

The country should seek to become the “crypto-nation”, said the economy minister, Johann Schneider-Ammann, last month. Zug aims to be the capital of that nation.

To that end, Switzerland is maintaining loose rules for crypto-businesses, even as other countries are tightening theirs. An industry is developing to store tangible crypto-assets, such as the hard drives on which cryptographic keys are stored, offline in cold, dry, secret sites complete with rapid-response teams. Where better than a decommissioned military bunker in the Swiss Alps? In Zug, friendliness to crypto-currencies is in evidence all around. “Bitcoin accepted here” stickers adorn the city hall and several shops, including the wine merchant’s. In 2016 Zug became the first place in the world to accept bitcoin for some public services. Residents can get a blockchain-based digital identity.

It was the arrival of the Ethereum Foundation in 2013 which really kick-started Zug’s development. Regardless of the seemingly speculative nature of cryptocurrencies, it’s the potential application of blockchain technology at the core of Ethereum, which is attracting interest. As this E&Y report suggests blockchain technology could transform indirect tax such as GST “by securely establishing the what, where and when of transactions”.

Regulators around the world are struggling to keep up with the pace of developments in cryptocurrencies. My view is that blockchain technology means cryptocurrencies are here to stay. With that in mind, how about making New Zealand a “crypto-nation”? After all, the advantages of Zug as a hub are equally true of New Zealand, only we have better beaches and wines.

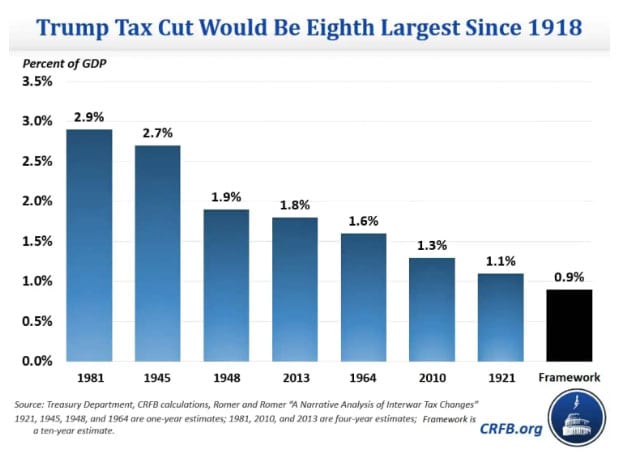

7) The biggest tax cut in (American) history?

On the passing of The Tax Cuts and Jobs Act 2017, President Trump declared “It will be the biggest tax decrease, or tax cut, in the history of our country.” Is that so? Not according to several sources including the United States Treasury Department.

The largest tax cuts in American history were President Reagan’s Economic Recovery Act 1981, which cut taxes by 2.89% of GDP (the top rate fell from 70% to 50%). By the same measure President Trump’s cuts would the eighth largest since 1918.

It would therefore appear the President’s claim was wrong. Bigly. (Sorry, not sorry).

But what would be the biggest tax cuts in New Zealand history? Tax rates and thresholds have been remarkably stable over the past 30 years and there have been few genuine tax cutting budgets. (The Budget 2010 income tax cuts were offset by an increase in GST). There were some tax reductions in 1996 and 1998, but for radical income tax cuts those in the mid-1980s when the top rate fell from 66% to 33% are the most radical.

8) “Sugar, sugar, oh honey, honey…”

”Sugar, rum and tobacco are commodities which are nowhere necessaries of life…which are…objects of almost universal consumption, and which are therefore extremely proper subjects of taxation.”

Thus spake Adam Smith, yes THAT Adam Smith, in The Wealth of Nations. However, as the recent spat between health advocates and NZIER demonstrated, taxing sugar is a controversial move.

Although Health Minister David Clark said the government had no immediate plans for a sugar tax, the merits, or otherwise, of such a tax are within the remit of the Tax Working Group to consider.

Meantime, the United Kingdom is introducing a Soft Drinks Industry Levy on 6th April. The levy applies at a rate of 18 pence per litre to drinks containing at least 5 grams of sugar per 100 millilitres. It increases to 24 pence per litre if the sugar content is 8 or more grams of sugar per 100 millilitres. The SDIL is expected to raise £520 million per annum to be spent on increasing the funding of sport in primary schools. Both proponents and opponents of sugar taxes will be watching to see if it achieves its health objectives. Watch this space.

9) Census.

Next Tuesday is Census Day, the 34th in New Zealand since 1851. It will be the first digital census, barring a major IT malfunction such as happened in Australia in 2016 it should pass off without note.

The refusal of the government to accept population census of 1962 prompted the 1963 population census which critics claimed were arrived at by negotiation rather than enumeration. The result was contested at the Supreme Court which ruled that it lacked jurisdiction over the administrative functions of the Federal Government.

The 1973 Census conducted between November 25 and December 2 was not published on the ground of deliberate falsification of the census figures for political and /or ethnic advantages.

Tuesday’s Census will be nowhere near as fraught as Nigeria, but it will be interesting to see how central and local government act on the data gathered.

10) A playlist for preparing your tax return.

Right now, if you ring Inland Revenue and find yourself on hold, there’s a good chance you’ll hear Coconut Rough’s 1983 hit Sierra Leone. In fact, you’ll probably hear it a lot. For the past few weeks some fault, or just plain sadism, has meant that Inland Revenue’s hold music has put Sierra Leone on continuous loop.

It could be worse, though, The Beatles Taxman for instance:

“Let me tell you how it will be

There’s one for you, nineteen for me

‘Cause I’m the taxman, yeah, I’m the taxman”

Here are a couple of collections of music to prepare your tax return by:

Unsurprisingly the Beatles’ Taxman, Pink Floyd’s Money and Abba’s Money, Money, Money feature in both soundtracks. There’s no sign of Blondie’s One Way or Another (its opening lyrics are surely Inland Revenue’s mission statement “One way or another, I’m gonna find ya’, I’m gonna get ya’, get ya’, get ya’, get ya”).

Sierra Leone isn’t anywhere to be heard either. Mercifully.

6) Swiss banking goes crypto.

6) Swiss banking goes crypto.