Inland Revenue has released an interesting technical decision summary in relation to the use of look-through companies. Look-through companies replaced the former qualifying and loss attributing qualifying companies with effect from 1st April 2011. They’ve therefore been around for some time, but great care is needed when using them.

The basic precept of a look-through company is a company which elects to be a look-through company for tax purposes. The company is still a separate corporate entity for all legal purposes, but for tax purposes, it’s rather like a limited partnership. Its losses and income will flow through to its shareholders. One of the key things to be in order to qualify for the look-through company status is you have to have five or fewer look-through shareholders.

Better ask Saul?

That was one of the questions at the heart of this application in this Technical Decision Summary. The company wanting to elect to be a look-through company applied to Inland Revenue for a ruling. There was quite an involved structure with three shareholder trusts with each trust benefiting the respective settlor together with a combination of their spouses, children, children’s spouses, grandchildren and other family trusts. The company had a subsidiary which was to be liquidated following the election and there was also a charity in the mix that was receiving distributions from on of the shareholding trusts.

One of the questions put to Inland Revenue in this application was whether the company qualified to make the election. There was also a question about what would be the treatment of the capital gain that arose on the liquidation of a subsidiary. All of this is highly technical, but it does highlight one of the major concerns many of us have had with the look-through company regime in that it is rife with little pitfalls. A very sensible approach was taken here by the parties involved to apply for a private ruling which was approved.

Inland Revenue said that there are only three look-through counted owners, so the company would meet the requirement of five or fewer shareholders. Each shareholding trust could make distributions to companies so a question was if a distribution went to a beneficiary company, could that compromise the status? Inland Revenue advised no and also accepted that if a subsidiary was liquated any capital gain which arose would still be available for distribution as a capital gain later.

This is quite a unique set of circumstances, but I raised it to show the great care that’s needed in dealing with look-through companies. Because if you get the timing wrong or you get the rules wrong, the election doesn’t apply and that can have quite severe tax consequences. It pays to tread carefully when making look-through company elections.

More on contractors and withholding taxes

Last week I spoke with Matthew Seddon, one of the finalists for this year’s Tax Policy Charitable Trust’s Scholarship Prize.

Readers raised a couple of questions: firstly, what happens when New Zealand companies offshore their work; and secondly wouldn’t it be simpler to make all contractors register for GST?

It so happens there is a set of rules that would apply withholding tax to payments that are made to offshore contractors, known as non-resident contractors tax. But the key point there is that the contractor must have actually performed the services in New Zealand. So, if an IT person flies into New Zealand as part of a project because they’re carrying out the services in New Zealand, non-resident contractors tax will apply even if the person is not tax resident in New Zealand. By the way, I’m sure this happened when Inland Revenue was going through its big Business Transformation project

The non-resident contractor’s regime has been around for quite some time. It was set up during the late 70s as part of the Think Big projects when the Government realised a lot of non-residents were working in New Zealand, but we had no mechanisms for capturing some of that tax revenue. So, the non-resident contractors tax regime was established, and it works pretty well.

Where all the work is done remotely then withholding will not apply because there is no New Zealand source as the services aren’t being performed in New Zealand but overseas. Under general tax principles, the taxing point therefore is in the offshore country. Overlaying these non-resident contractor rules are double tax agreements, so it’s another area where people can trip up very easily,

As for making contractors be compulsorily GST registered, this was something Matthew and I did discuss. I think the next stage in the evolution of GST is pretty much making business to business transactions zero-rated. This would simplify administration and compliance. So thank you to the questioners, Hamish, SolarDB and Kiwis, much appreciated.

“It was twenty years ago today…”

And finally, it’s actually been 20 years this week since I started Baucher Consulting. Back then I started with a single client, and I worked from home. Now there are three of us at the moment and we have offices in Takapuna. Change is constant in tax and it’s actually one of the attractions of your career. You really don’t know what challenges you will meet in the course of the day or week. And that keeps you on your feet.

I’ve been working in tax for 40 years and even now there’s always something that turns up and makes you think “Oh, I hadn’t come across that before.” It’s a great, intellectually stimulating challenge. And you’re always having to think on your feet sometimes very, very rapidly. Such as when you’re in the middle of a meeting with Inland Revenue who suddenly fires in a question you weren’t expecting. I’ve had a few of those over the years.

“Don’t look back in anger…”

Looking back over the past 20 years it’s interesting to look back and think how much has changed and yet in some ways how little has actually changed. Back in in August 2004 the top marginal income tax rate was 39% which kicked in at $60,000. The corporate income tax rate was 33% and the trustee rate was also 33%.

As we know the corporate income tax rate is now 28% which reflects the worldwide trend we discussed recently of falling corporate income tax. rates. We’re back up to a top 39% rate, but this time on income over $180,000. And as of 1st April this year the trustee tax rate is 39% for most trusts.

In August 2004 Michael Cullen, who was also the Minister of Finance, was the Minister of Revenue. Following the 2005 General Election he was replaced by Peter Dunne, who began his second stint as Revenue Minister after a brief period in 1996. Peter Dunne actually has the distinction of being the longest serving Minister of Revenue in New Zealand History. He held the post from 2005 right through until June 2013 when he was replaced by Todd McClay. Over the past 20 years, there have been nine Ministers of Revenue, including Sir Michael and Peter Dunne.

“The Minister reads his papers”

Quite a few ministers had quite interesting tax related careers prior to becoming MPs. Judith Collins, for example, Minister of Revenue between 2016 and 2017 was a former tax partner at the law firm Simpson Grierson. Barbara Edmonds, who was briefly Minister of Revenue last year between July and November, was previously an Inland Revenue official and then later attached to the Minister of Revenue’s office. And the current Minister of Revenue, Simon Watts, started his career as a tax consultant with Deloitte.

Fortunately, I’ve got to meet many of these ministers and their officials. I remember one Inland Revenue official remarking to me “The Minister reads his papers. Not every minister does.” Now I think all the ministers I have encountered in office read their papers. I think it’s particularly true of Simon Watts, who has impressed me this year where a couple of times I’ve come across some at conferences where he’s very clearly been across the brief and the massive amount of detail involved.

Back in 2004 David Butler was halfway through his period as Commissioner of Inland Revenue. He was succeeded in 2007 by the genial Canadian Bob Russell, who lasted until 2012. His replacement was Naomi Ferguson, one of the longest serving Commissioners of Inland Revenue in recent years. Naomi oversaw the Inland Revenue’s critically important Business Transformation project which upgraded Inland Revenue’s computer system.

Business Transformation was brought in on time and under budget, although the recent Performance Improvement Review highlighted some concerns about the reliance on a single supplier. Business Transformation was just in time to cope with the COVID pandemic. As officials told me without it Inland Revenue would not have been able to handle the demands that were placed on it as a result of the pandemic.

Sir Michael Cullen – the tax reformer

Looking back over the major changes in tax, as I mentioned, Sir Michael Cullen was both Minister of Revenue and Minister of Finance when Baucher Consulting started. I think he deserves to be recognised as one of New Zealand’s most significant finance ministers in modern times. He’s probably second only to Roger Douglas in that regard.

His tax initiatives included Working for Families in 2005, but the critical ones would be the setting up of the New Zealand Superannuation Fund in 2003 and most importantly, KiwiSaver which started in 2007. KiwiSaver’s start coincided with the introduction of the portfolio investment entity or PIE tax regime and the very controversial Foreign Investment Fund (FIF) regime, which took effect from 1st April 2007. A couple of weeks back we discussed the FIF regime its impact for some migrants. All of these were significant achievements which changed the tax landscape.

Not one but two tax working groups

We’ve also had two tax working groups. The first one was the Victoria University of Wellington Tax Working Group 2009 – 2010, led by Bob Buckle of VUW. The second and much better resourced group sat between 2018 and 2019, chaired by Sir Michael Cullen. It is one of the highlights of my business career to date that I was invited to write a paper for that tax working group on whether there should be a separate tax ombudsman and a tax advocate for smaller taxpayers. My view was and remains, yes to both. In fact, it was one of the proposals that was picked up for further work by Inland Revenue’s tax policy division. But then something called COVID turned up. So those proposals are now way down the back-burner

In 2018 I also had the very good fortune to be a member of the Government’s Small Business Council. That was a great learning experience and very much a professional highlight. It also built networks which enabled me to have direct contact with Stuart Nash who was both Minister of Revenue and Minister of Small Business during the pandemic, when what became the Small Business Cashflow Scheme was being devised. Incidentally that’s an initiative I think should be picked up and expanded by the Government.

A tax switch and sneaky fiscal drag

October 2010 saw a major change to the tax system with the top income tax rate dropping from 39% to 33% as part of a tax switch with the GST rate increasing from 12.5 to 15%. That was the last time until the 31st July just gone that the tax thresholds were increased. I’ve said it before and I will keep saying it, I think it is unacceptable how successive Ministers of Finance of both parties have been allowed to get away with not regularly increasing tax thresholds.

Starting in 2010, I started writing for interest.co.nz and I’d like to take the opportunity to thank the publisher, David Chaston and managing editor Gareth Vaughan for their patience and their support through these past years. From that start I got to meet Dr Deborah Russell, who’s now the Honourable Deborah Russell MP, former associate of Minister of Revenue and our collaboration resulted in the publication in 2018 of the BWB text in 2017 Tax and Fairness, a huge personal and professional highlight.

Bright-line test and capital gains

Another significant tax milestone was on 1st October 2015 and the introduction of the bright-line test. It originally only applied to sales within two years of acquisition but during the last Labour government the period was increased to first five and then ten years. The bright-line test is significant because it recognised that having a tax provision which taxed on the basis of a person’s intention – was the property acquired for the purpose or intent of sale – was largely unenforceable.

No capital gains tax…for now

The last Labour government of course turned down the Cullen Tax Working Group’s proposed capital gains tax. However, that issue isn’t going to go away, in my view. Partly to redress that decision Labour then introduced the controversial and deeply unpopular interest limitation rules in October 2021. I could see the theory behind these rules, but I thought they were overcomplicated. Personally, if I was addressing the issue of interest deductibility, I would have gone with adapting the existing thin capitalisation regime. This has been in place since 1995 and therefore is well established.

With regards to interest limitation rules, it’s worth remembering, as I noted a couple of weeks back when talking about the OECD’s corporate tax statistics, there are over 100 interest limitation rules currently in existence around the world. So, the issue of over generous interest deductions is not one solely focused on residential property. Contrary to many of the claims made that the interest limitation rule that was a breach of business practice it’s actually quite a standard feature as the thin capitalisation rules demonstrate.

Podcasting since 2019…

Amazingly, this podcast started five years ago in 2019 with my first guest Jenée Tibshraeny then of interest.co.nz but now with the New Zealand Herald. I’d like to thank all my guests who have appeared over the years. The podcast is approaching its 250th episode. It’s something I enjoy which seems well received and it’s actually pretty handy for keeping abreast of developments.

One other professional highlight was providing data to the Finance and Expenditure Committee and Inland Revenue about the instances of over taxation of backdated ACC lump sums. Subsequent discussions with Inland Revenue led to legislative change which took effect at the start of this tax year.

A big thank you

But most of all, I’d like to thank the people who have helped me prosper over the past 20 years, starting with my wife Tina without whose endless support and patience none of this would have been possible. My colleagues here at Baucher Consulting, Judith, Eric, Darren, and Trent, my business coach Bruce Ross. David Chaston and Gareth Vaughan at interest.co.nz, my colleagues of the Accountants and Tax Agents Institute of New Zealand, where I was honoured to be on the board between 2010 and 2016. The many friends have made along the way and of course, my clients.

So, thank you all very much it’s been a fascinating 20 years. As I said change is a constant and there’s a lot more to come. I think we’re going to see big changes with the tax system as we try to fund the challenges ahead of climate change and the changing population. And as always, we will bring you those developments as they happen.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Matthew Seddon suggests imposing withholding taxes on organisations that engage independent contractors, including through electronic marketplaces

My guest this week is Matthew Seddon. Matthew is a lawyer at Bell Gully and one of the four finalists for this year’s Tax Policy Charitable Trusts Scholarship competition. He has suggested extending the withholding tax regime to include more independent contractors. Kia Ora Matthew, welcome to the podcast. Thank you for joining us. So how did you get into this and where did your proposal come from?

Matthew Seddon Hi, Terry, thanks for inviting me onto your podcast. It’s great to be here. The Tax Policy Scholarship provides young tax professionals with the ability to set out a proposal for a significant reform in the New Zealand tax system. My proposal is to extend PAYE withholding to independent contractors engaged by persons with an existing PAYE withholding obligation, i.e. employers, and also to those independent contractors engaged through an electronic marketplace.

TB Those electronic marketplaces try and match buyers and service providers. You picked up on something from the Tax Working Group in this space, is that right?

Matthew Seddon Yes, the Tax Working Group in 2018 had identified the rise of self-employed independent contractors as the most likely and most significant challenge facing the integrity and sustainability of the New Zealand tax system. The Tax Working Group’s final report had noted that withholding taxes should be extended as far as practicable in order to ensure greater levels of compliance. Furthermore, the Government’s recent focus on increased compliance activities is another reason which prompted me into this proposal.

TB Yes, because Inland Revenue got $29 million a year. I think they were saying they’re expecting a $700 million return on that. Is that right?

Matthew Seddon Yes, the $29 million I think is over each year and I think $116 million is set across for the four-year period. So their expectation is to raise $702 million over a four-year period from those increased compliance activities. Inland Revenue has also been stating recently that they’re going to focus on taxpayers who have not been complying with their tax obligations. Especially in the hidden economy.

TB Like I was saying the other week, the hibernating bear has woken up and it’s hungry and it’s making moves. Yes, I mean just picking up on that, the Performance Improvement Review recently released on Inland Revenue was quite interesting in its discussion around the tax gap, which the Tax Working Group fenced around a little but didn’t really go into specifics. But this is the area, right on scope of the tax gap, isn’t it?

A billion dollar gap?

Matthew Seddon Indeed, and Terry, just for listeners to understand, the tax gap is the difference between what Inland Revenue should receive in taxes if all taxpayers are fully compliant with their obligations compared to what tax they actually receive. The Tax Working Group had received some research that was commissioned by Inland Revenue on the tax gap for independent contractors, and that research indicated that independent contractors were under reporting their taxable income by about 20% on average. This was resulting in a loss of revenue of $850 million a year.

TB And that’s in 2018 dollars. So now we’re talking potentially over a billion dollars per year.

Matthew Seddon Exactly.

TB Well, if I was Nicola Willis, I’d be very interested in that because that’s a quarter of a percent of GDP. It’s actually a significant number now. So how does your proposal work?

Matthew Seddon So my proposal looks at imposing withholding taxes on organisations which engage significant numbers of independent contractors. For example, a large number of independent contractors operate through electronic marketplaces. A lot of employers engage independent contractors. So it’s by centralising the withholding obligation and imposing it on employers and electronic marketplaces instead of the numerous independent contractors underneath, that provides Inland Revenue with a greater ability to receive those taxes rather than having to chase independent contractors individually.

TB Yes. So I mean we have an extensive withholding tax regime. It’s something that’s I think has always been taken for granted, but we don’t realise actually how very comprehensive it is. But when you look back on it, the sort of sphagnum moss collectors, charges for directors’ fees is a 33% rate I believe. But these withholding tax obligations aren’t updated frequently or as frequently as you might imagine. As the Tax Working Group pointed out, we’ve seen a big growth in this sector. You’re saying we’ve got these existing mechanisms in place and should extend it to this particular group. Is there going to be a de minimis or is it going to be for anyone who’s already got a PAYE obligations or who has employees?

Matthew Seddon That’s right, Terry. So, the starting point is that if you’re an employee, your employer withholds PAYE. If you’re an independent contractor, generally you deal with your own tax obligations. What you’re referencing there about sphagnum moss collectors and directors’ fees are schedular payments and that imposes an obligation to withhold on the payer of those payments. My proposal would be to extend that schedule and the schedular payments regime to include those employers and electronic marketplaces that engage the independent contractors.

Now the reason why I was looking at employers in particular and the reason why I would not have a de minimis, is because employers have the systems and software in place that pay their existing employees and they also make those payments to independent contractors. So the software and systems should only require minor modification and configuration to be able to deal with withholding on payments to those independent contractors. The independent contractors that are engaged by employers and electronic marketplaces. It wouldn’t be all of those independent contractors that are subject to the withholding. It would only be those independent contractors who are principally providing services to the employer or the electronic marketplace such that they are functionally equivalent to employees.

TB Yeah, that’s a really interesting point there because often you find that someone walks out the door on Friday is contracting back on Monday. So this question of functionally acting as an employee – is that going to be a requirement, do you think? Would it perhaps just be extended if a person is providing personal services to a company, would that perhaps be a stronger approach? I think so rather than try to get to a definition that they’re doing the same as if they were an employee because all the employment lawyers listening will be twitching on that one because there is a big case going through the courts at the moment, I believe on that matter.

Matthew Seddon It’s essentially to look at who is providing services to the employer or the electronic marketplace. It’s designed to carve out people who are genuinely supplying goods to an employer or an electronic marketplace. So, you don’t have an overreach of withholding obligations. You could imagine if withholding was made on all payments to independent contractors, it would lead to chaos. There would be withholding on every single payment that’s made by an employer.

Furthermore, proposals to extend withholding to all independent contractors have a significant downside in the fact that you’d be requiring, for example, home owners to withhold tax and pay that to Inland Revenue for a painter that was engaged to paint their house. So this proposal is designed to narrow the focus to the independent contractors who are providing services to employers and electronic marketplaces.

TB That makes perfect sense. It’s a huge area though. But as I said, the scope of this with downsizing that’s been going on through Ministries, for example, this exactly is happening, as I said, some people are probably coming out on Friday as employees and coming back contracting with a different role on the Monday. A flat 20% rate, was that what you are thinking?

Matthew Seddon Yes. The default rate would be 20%. This is in recognition of the fact that independent contractors can claim deductions for income tax purposes. It also aligns with the current voluntary schedular payments regime that already exists.

TB Yes, the voluntary schedular payments regime. So right now, if you were contracting to an employer, you could say take 20% off and the employer or rather the contracting company could do that?

Matthew Seddon Yes, there is a mechanism whereby both parties can agree to undertake a withholding. The one thing I would note about my proposal is that it is simply the default rate of 20%. There is an existing regime for schedular payments which provides that an independent contractor can notify the payer of their name, IRD number and an elected rate no less than 10%. The independent contractor can essentially toggle the rate to reflect their effective tax rates so that they they’re not overpaying tax throughout the year. And they’re not underpaying as well, so that they can get a correct tax outcome by the end of the year.

TB Yes. Our pay-as-you-earn-system is more flexible than it was, but there’s scope for improvement there. I think real time payments are the next step in the evolution of our tax system. Something just popped into my mind. If I recall correctly, if a company is providing hiring, hiring contractors, they have a withholding tax obligation automatically. Is that correct?

Matthew Seddon The labour hire rules in the schedular payments regime, I think it’s a 20% rate.

TB Yes, 20%. And it wouldn’t matter, say a contractor was working individually or through a company. Generally speaking, you can under the schedular payments rules, generally speaking, if you’re working through a company, the payer doesn’t have to withhold tax. What do you think? Would you change that here?

Matthew Seddon I think there’s a company exemption in the schedular payments regime which looks through certain companies. So, I think that could also fit in with this proposal.

TB Because mainly the fact someone’s running through a company doesn’t mean that they’re actually completely up to date with their obligations, as week after week Inland Revenue tells us what’s going on. And the other thing that you touched on in there was about the fact that as contractors, they have the ability to claim deductions. I think this is where the paper prepared for the Tax Working Group was saying basically that it seems given comparable levels of income there is this gap of about 20% and they identified that on the basis that self-employed or contractors appear to have 20% more discretionary spending than their employee counterparts.

How would you counter that? I know as a small business, when you are dealing with small businesses, people are very keen to claim everything they can, and they don’t always tell you what they’ve claimed or they’re not always as straight up or as accurate as we would all like in this space. I’ve wondered whether we should have standard deductions. What’s your view on that? I know in the UK they did that for self-employed individual. Any thoughts on that particular idea?

Matthew Seddon My proposal primarily focuses on the withholding obligation, that is on the income side of the equation, so by being able to report and withhold on these payments, Inland Revenue is going to see exactly what these independent contractors are earning.

I guess to the extent that independent contractors are claiming sizable amounts of deductions relative to their industry peers. It would allow Inland Revenue to go and look and audit those independent contractors. On the deduction side, it’s something that I have thought about. I know in the GST rules for listed services there are flat rate credits for non-GST registered persons. So, there could be a similar flat rate deduction for independent contractors to align themselves across the board.

TB I deal with quite a number of American clients and their tax returns have what they call a standard deduction of $12,000. But you don’t have to claim that, you can go for what they call itemised deductions which presumably you do so on the basis that you’ve got more to claim.

It just crossed my mind that one of the things coming out of the Performance Improvement Review of Inland Revenue which we discussed a couple of weeks back, they talked about the tax gap, and I think they also talked about making one of its objectives to make the tax system easier and simpler and particularly for small businesses micro businesses. Your proposal basically is in that space, isn’t it? And it does have that benefit.

Matthew Seddon Exactly. It provides greater levels of compliance for those small businesses, those independent contractors. There’s going to be less need for them to engage accountants and third-party providers. There’s going to be less engagement with the provisional tax system. That’s going to be a much simpler experience for those independent contractors. My proposal also recognises that there will be some costs imposed on employers and electronic marketplaces. But by leveraging off the existing PAYE rules and schedular payments rules, it is designed to minimise those compliance costs as much as possible requiring them to just modify and configure their software and systems.

I think it’s important as well to notice that prior to any implementation of this proposal, there should be a sufficient period of time in which engagement can take place between Inland Revenue and these payroll software providers. I know this has recently taken place for the personal tax cut changes which had effect from 31 July.

TB That’s actually quite critical, and wider consultation is always welcomed in this space. Something just came to mind. I mean, obviously what we’re talking about here, this could be a measure that helps to close the tax gap and raise revenue, which is great from Inland Revenue’s perspective and for Treasury, but it’s actually as I see it, and what I find attractive about this is that it’s also a benefit to contractors.

I deal a lot with small businesses here and you know, managing their tax isn’t always easy and everyone is not as diligent about managing their tax as they should be. I’m a big believer in making payments regularly, and in this case, withholding payments seems to me would contribute quite a bit to that. That was something you had that in mind when you were looking at the proposal weren’t you, because that’s one of the judging criteria of the competition.

Matthew Seddon Exactly, minimising compliance costs for taxpayers and also minimising administration costs for Inland Revenue as well.

I think independent contractors, while they might have the benefit of the time value of money by only making provisional tax payments three times a year, as they currently have no withholding may allow them to have less tax obligations in the first place, as it’s all dealt with by their employer or the electronic marketplace and really allows them to focus on doing what they do best, and that’s running their own business.

TB Yeah, I’d endorse that approach. I do recommend to a lot of my clients, they run businesses, they’re shareholder-employees, we don’t often use the shareholder-employee regime and I tell them, go through the pay-as-you-earn system making your payments regularly, so you keep on top of your tax payments. That’s one of the things, as I mentioned a minute or two ago, I like about the more frequently people make their tax payments, they’re going to be more compliant, get up to date and they will have less stress about it. It’s one of the things about managing small businesses. There’s a lot to deal with and there’s not much that you can actually do, there’s an irreducible minimum you’re dealing with at times and withholding payments helps in that space.

Slightly related topic, what about GST? Now it’s not directly in scope, but to me, I think this is the next frontier of tax could be compulsory zero-rating which would be easy for both the employer or the contracting company and the contractor. What’s your thoughts on that?

Matthew Seddon Yeah, that’s right. It’s not directly included in my proposal, but I think when thinking holistically about the tax obligations of these independent contractors and how they can be automated as much as possible. GST is obviously another area to consider. I think zero-rating, there might be some scope for that. It would mean there’s less obligations on the independent contractor and would not be required to return the GST amount and they’d still be able to claim some GST credits.

The alternative I was thinking about was potentially having the carve out for employment apply to these independent contractors who are functionally equivalent to employees. You should ideally end up with a scenario where if you’ve got an employee and an independent contractor sitting across from the table from one another at their employers’ offices, they should be treated as similarly as possible so that there’s horizontal equity between the two.

TB So what’s next for you? 1500 words was your initial proposal. So now you’ve got the 4000 words which means you’re in the money, you’re going to come away with a medal of some sort. As they say, it’s always good to make the medal rounds. So it’s in mid-October sometime. You’ve got to finalise your entry and what’s involved in that?

Matthew Seddon The final oral presentation is in October and our 4000-word submission is due in September. The 4000 words is essentially branching out and expanding on our initial 1500-word proposal. The 1500-word proposal was a teaser to the judges to set out what the concept was and how it met the relevant judging criteria. The 4000 words will expand on this initial idea.

TB It’s not many though, 4000 words, really when you think about it and then obviously your oral presentation, you’ll be in front of several gurus of tax. That would be interesting, I’d say.

Matthew Seddon Indeed, it will be interesting to hear the judge’s comments and questions in person.

TB Well, I’m sure you’re looking forward to it. I am. I think it’s a very interesting proposal. It sounds mundane, but it’s actually quite important. Thank you very much, Matthew Seddon. Thank you for coming along. Good luck for October for this scholarship, we’ll watch with interest.

Matthew Seddon Thanks Terry.

TB And on that note, that’s all for this week. We’d like to thank Matthew Seddon again for joining us and wish him all the best for the scholarship. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week, as part of its continuing drive to increase compliance, Inland Revenue released an updated property tax decision tool.

What this does is help people work out when a property might be taxable under any of the land taxing rules, including the bright-line test. It’s been updated to take account of the bright-line test changes which took effect on 1st July this year.

The growing issue of helping families into housing – what are the tax implications?

Generally speaking, since 1st July, the bright-line test only applies where the end date for sale as determined under the rules is within two years of when the property was deemed to have been acquired. The aim of the tool is to work through all the various scenarios that might apply. So that’s something worthwhile, and I think we’re going to see more of people wanting to make more use of this because of a developing trend around shared home ownership where people who are not necessarily couples are coming together to purchase properties. There are also families wanting to help elderly parents.

We’re seeing some very interesting scenarios develop as a result. One of those scenarios was the subject of last week’s Mary Holm’s column for the New Zealand Herald.

“We’ve bought my wife’s parents’ house. They had a small mortgage on it, with no income, just super, coming in. They didn’t have enough money to keep paying the mortgage, hence they were going to start a reverse mortgage to keep things afloat.

If they sold the house they would’ve struggled to get into a retirement village and stay near family etc. So we bought the house so they don’t ever have to leave – so let’s say they will be there for at least another 10 years.

They pay us $750 rent per week. We took out a 30-year $800,000 mortgage, with just the interest on it at $1977 a fortnight, so we are topping up mortgage payments as the rent does not cover it. We also pay the rates, insurance and any maintenance costs.

How do we treat this in terms of any possible tax or claims as such?”

Mary asked Inland Revenue and me for comment. Notwithstanding that a net loss was foreseeable, my advice was you never always know what the full story is as there may be a detail which for whatever reason, the correspondent has overlooked. The basic approach I took was you should report it. Inland Revenue were much of the same view but noted that any excess deductions would be ring fenced.

As I mentioned to Mary, I think we’re going to see a lot more of this. Because they’re coming from both ends of the generational spectrum. In this case we’ve got the elderly parents wanting to stay near family and then at the other end, young people trying to get on the housing ladder.

Is shared home ownership an answer to housing affordability?

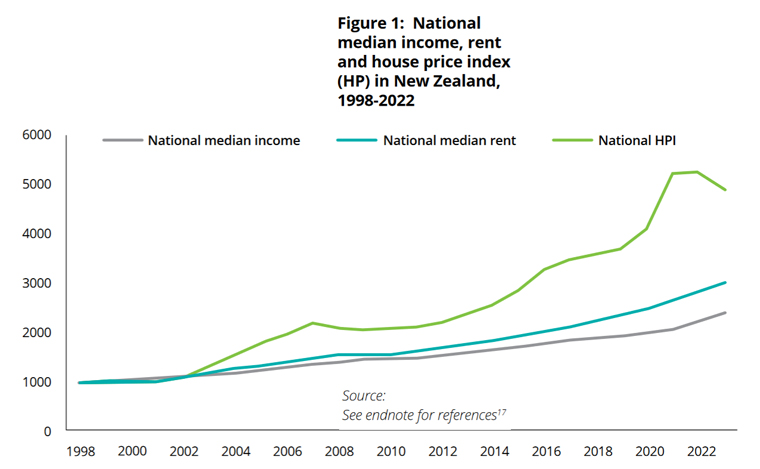

Over the last 20 years or so I’ve seen the practice develop quite rapidly of parents, grandparents and other relatives helping their children or grandchildren get their foot on the property ladder. This was the subject of an interesting report on shared home ownership released by Westpac called Next Step Forward. The report notes that the housing market is increasingly difficult, and “the home ownership dream is increasingly out of reach for some New Zealanders”. The report’s analysis is that shared home ownership will become increasingly common and how might that develop.

The report describes the housing market as “distorted”. To give you some idea of the scale of the problem, the report notes “As of February 2024, the median house price was 6.8 times the median income compared to 5.4 times in 2004 and roughly 2.3 times in 1984.” So over 40 years, the median house price relative to median income has practically trebled.

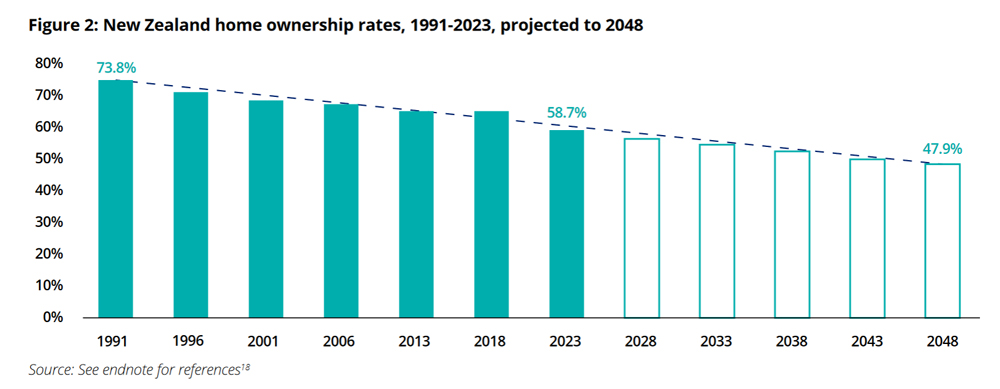

The report also notes that home ownership rates in New Zealand have been declining steadily since peaking in 1991 at 73.8%. They’re down to 58.7%, so a 15 percentage point drop over 30 years is pretty substantial. But the report projects that within 25 years, the proportion of homeowners will have dropped to 47.9%. (The report notes the outlook is even worse for Māori and Pacific peoples, where the home ownership rate is lower, at 47% and 35%, respectively, as of 2023).

What are we going to do about this? Well, as the report suggests shared home ownership is going to become more common. This in turn is going to trigger all sorts of tax issues. Which is why something like Inland Revenue’s property tax tool is handy. The report, incidentally, doesn’t really discuss tax other than mentioning tax free capital gains do play a part in people’s investment decisions and may have an impact on the housing market

There’s no real short answer to this issue. Raising incomes would be one thing, freezing or slowing the rate of house prices would be another, and building more homes would be a vital third factor. Pulling all this together is a huge problem and each solution comes with secondary effects.

International tax deal in trouble?

Moving on, an equally complicated scenario and one we’ve been covering for several years, is the question of the taxation of multinationals. Back in 2021, the OCED/G20 declared a breakthrough international tax deal over the taxation of the largest multinationals in the world. The deal proposed a Two-Pillar solution over the question of taxing rights. Ultimately this is where the idea of a minimum corporate tax rate of 15% emerged.

Agreeing in principle was one thing, but the negotiations have been going on since then and increasingly it seems to be that they’re running into difficulty. A key 30th June deadline has now passed, and it appears that some governments are starting to lose patience with the whole process.

One of the ideas behind the agreement was to head off the implementation of digital services taxes (DSTs). As part of the process these DSTs were put on hold by several jurisdictions, including the UK, Austria, India and others. In the meantime, as negotiations have dragged on, other countries such as Canada have said “Well, we’ve had enough of this, we’re going to go ahead and impose a digital services tax.”

Meantime, the United States whose companies such as Alphabet and Meta are at the heart of the issue have threatened retaliatory tariffs on countries imposing DSTs. Nobody wants a trade war, but someone has to blink in terms of getting a deal past this impasse. So, they’re continuing to negotiate, even though the deadline theoretically has expired.

Time to go back to first principles?

On the other hand, as Will Morris, PWC’s Global Tax Leader points out in this short video. Maybe we should just go back to first principles instead of trying to hammer out a deal through the existing Pillar 1 process which some consider is not really fit for purpose.

It’s not a bad idea but it would delay further progress in the matter, and I think that’s where governments who’ve got elections to win may not be prepared to wait much longer. I think generally the public is a bit antsy about the question of corporate taxation. As I noted last week, when we looked at the OECD’s latest corporate tax statistics, statutory corporation tax rates have pretty much stabilised after 20 years of falling.

However, there are still substantial gaps in public finances as a result of first the Global Financial Crisis, then the pandemic and increasingly we’re having to deal with the impact of climate change as well. When the insurers are leaving the market, who picks up the tab? In my view, that’s going to be we the taxpayers.

There will be pressure to get some sort of deal across the line, but I also think although we may see corporate tax rates elsewhere in the world rise, I think with our 28% rate, we haven’t really got much room for manoeuvre for an increase at this point.

A place where talent does not want to live?

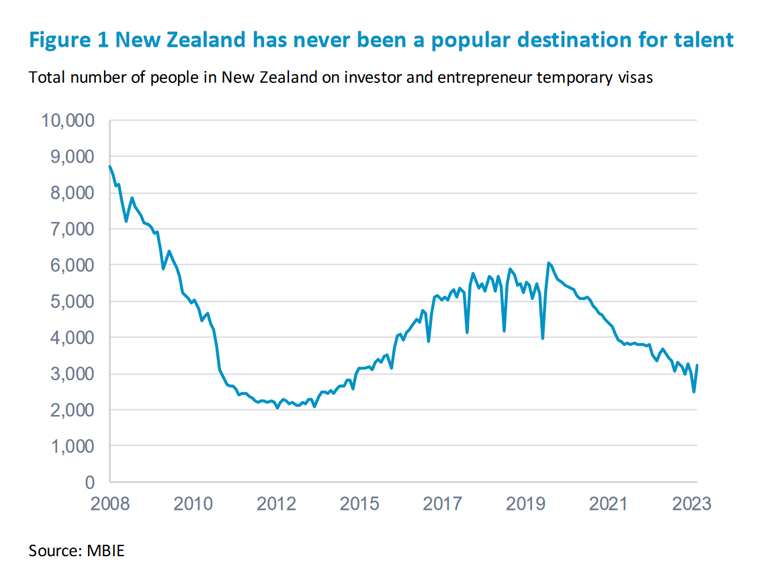

Finally, the New Zealand Institute of Economic Research released a fascinating report on Thursday. Provocatively titled The place where talent does not want to live, it looks at the question of New Zealand’s immigration policy and how that sits alongside our international tax regime.

The report was prepared for the American Chamber of Commerce in New Zealand, the Auckland Business Chamber, the Edmund Hillary Fellowship and the NZUS Council. It’s a fascinating document because it pulls together points, we don’t always hear discussed when we’re looking at immigration policy, how does our tax system interact with that policy?

The report notes that conceptually, we have developed tax rules which make sense in a tax context. However, they lead to wider issues once they start operating in a broader context. In particular the report really focuses on the Foreign Investment Fund (FIF) regime which it considers disadvantages many investors who come here hoping to use their skills and their capital to help build the economy and the tech sector in particular.

I’ve seen comments on this topic previously from entrepreneurs, and it’s easy perhaps to be cynical and say, “Well, they’re speaking out of self-interest” but 40 years of tax experience also tells me that behavioural responses to tax are very observable and policymakers should pay attention to such responses.

An in-depth examination of the Foreign Investment Fund regime

What makes this report particularly interesting are the authors, Julie Fry and Peter Wilson. Julie is a dual New Zealand and U.S. citizen who in her bio notes that “her location and financial decisions have been impacted by the tax rules covered in the report.” Peter was Manager of International Tax at the New Zealand Treasury from 1990 to 1997 and then Director of Tax Policy from 1998 to 2002. As such “He was responsible for advising the government on many of the tax issues contained in this report.” Consequently, outside of anything prepared for a tax working group, this report is one of the most in-depth examinations we’ve seen of our international tax regime and FIF regime.

The report notes that although we have a fairly open flow of migrants, “New Zealand has never been a particularly popular destination for talented people”. (Interestingly, we have no data on how long people on the various investor and entrepreneur visas stay).

As the report notes there’s a competition for global talent and New Zealand is not attracting as many as we would like. We should therefore be thinking hard about the implications of this.

The report hones in on the FIF regime as being a particular problem for many investors because of the way that it taxes unrealised gains. This creates a problem of a funding gap where an investor is expected to pay tax on an investment which very often isn’t producing cash because as a growth company cash is being reinvested. (By the way, this is often a common argument against wealth taxes).

As the report notes, “New Zealand’s tax rules were not designed with the idea of welcoming globally mobile talent in mind.” For example, as Inland Revenue’s interpretation statement on residency makes clear it’s deliberate policy to make it’s easy to be deemed tax residency in New Zealand, and hard to lose. This has long term flow implications because as the report points out, people who would perhaps want to commit to New Zealand are reluctant to do so because of the tax consequences of doing so.

Chapter Three is the very, very interesting section of the report as it explains the development of our current international tax regime and the rationale for the various FIF regimes and their design. The overall objective was to protect the tax base, but they didn’t really think about what was happening with migrants. As Ruth Richardson and Wyatt Creech then the respective Minister of Finance and Minister of Revenue explained in 1991:

“The objective of the FIF regime, where it applies, is to levy the same tax on the income earned by the FIF on behalf of the resident as would be levied if the fund were a New Zealand company. Because the FIF is resident offshore with no effective connection with New Zealand, the only way of levying the tax is on the New Zealand holder.”

This is conceptually correct from a tax perspective but as the report keeps pointing out, it doesn’t really take into account what happens with migrants who made investment decisions long before they arrived in New Zealand only to find their accumulated savings are being taxed here under the FIF regime. I have a similar problem with the taxation of foreign superannuation schemes. Although the tax treatment conceptually ties in with our system, it seems to me we are effectively taxing the importation of capital and this paper is basically saying the same thing in relation to FIF.

How much tax does the FIF regime raise?

Section 3.5.1 on page 26 of the report has an interesting analysis of how much revenue the FIF regime raises. Because our tax reporting statistics aren’t very detailed, the answer is we don’t really know. The report concludes

“The high-level finding is that the level of overseas investment is small compared to total financial assets at the national level. Portfolio foreign investment is, in some years, one-thousandth of domestic investments. This suggests that the current FIF tax base is likely only to make a minor contribution to direct revenue.”

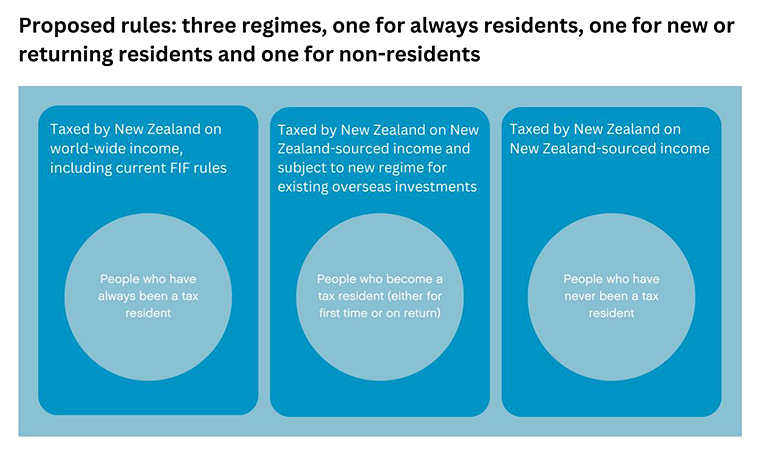

A suggested reform

The report concludes that in an international context where we were trying to attract the right talent, maybe we should be looking at the FIF regime. What it suggests is to separate the tax treatment of people who have always been tax resident from those of new and returning tax residents. The existing FIF rules would continue to be applied to those have always been New Zealand tax resident. Meantime a new regime should be designed for new and returning tax residents.

The report does touch on the question of a general capital gains tax regime (which could be an answer) but considers the development of a comprehensive CGT is a long term political consensus building project.

In discussions I’ve had with other colleagues on this matter we’ve noted how our American clients in particular are very affected by the current FIF regime. As American citizens they are required to continue to file American tax returns and are therefore subject to capital gains tax. This creates a mismatch between when they pay New Zealand income tax and the final US tax liability on realisation. Although the FIF regime creates foreign tax credits for US tax purposes, clients are frequently not able to utilise the foreign tax credits.

As people told the report authors this is extremely frustrating and there is no doubt that people are upping sticks and moving because of it. (I’ve also seen other clients switch into property investment instead).

Overall, this is a very interesting and highly recommended report considering the intersection of tax driven behaviour with wider economic issues.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The just concluded UK general election was the first general election held in July since 1945, when coincidentally the Labour Party also won by a landslide ending Sir Winston Churchill’s wartime prime ministership. Before he became Prime Minister again in 1951, Churchill started writing his monumental six volume history of the Second World War, the first volume of which was titled The Gathering Storm.

And if you’ll pardon the somewhat laboured analogy, this is very much what’s happening with Inland Revenue at the moment. There’s a very clear gathering storm approaching as Inland Revenue pulls together and beefs up its investigation resources. We saw signs of this a couple of weeks back with its commentary about targeting smaller liquor outlets. Now last Wednesday, an Inland Revenue media release announced it is “honing in on customers who are actively dealing in crypto assets but not declaring income from them in their tax returns.”

By way of background, back in 2020, Inland Revenue updated its guidance on the tax treatment of crypto assets. Clearly that was part of a plan to follow through and check on who was trading and investing in crypto but not reporting the income. However, first COVID and then the cost-of-living crisis got in in the way of Inland Revenue’s intentions to follow through up its guidance.

Targeting non-compliance

But those immediate crises have passed now, and it appears that Inland Revenue has been busy investigating potential non-compliance because according to the media release late last year, it wrote to “a group of high-risk customers and gave them the chance to fix any non-compliance issues before facing audit.” This is a standard tactic of Inland Revenue. It basically puts it out to taxpayers without being too specific that it is aware of potential non-compliance and “invites”, that is the terminology used, the taxpayers involved to come forward and make a voluntary disclosure. If the taxpayers do so, then the potential to be charged shortfall penalties is likely to be greatly reduced.

Following on from these “invitations”, the next stage if the taxpayers don’t come forward is directly targeted follow up action. This appears to have just happened, as Inland Revenue is saying it has “just sent another round of letters to those Inland Revenue believes are not complying.

According to Inland Revenue it has data which has enabled it to identify “227,000 unique crypto asset uses in New Zealand undertaking around 7 million transactions with a value of about $7.8 billion.” There’s a potentially sizable sum of tax on the line here.

Pay up, or else…

The media release continues with a rather veiled threat

“Cryptoasset values have reached new highs, so now is a good time for people to think seriously about tax on their crypto asset activity. The high value also means customers are well positioned to pay their tax for the 2024 tax year and earlier.”

In other words, Inland Revenue is saying as values have recovered that means taxpayers can’t plead poverty when it comes to paying the tax due on their profits.

The media release goes on to explain something that we’ve said frequently; Inland Revenue has more data available to it than people realise.

“We want customers and tax agents to know that we are stepping up our compliance activity for customers with cryptoassets. Despite popular thinking – people are not invisible on blockchain and we have the tools and analytics capabilities to identify and expose cryptoasset activities.”

So there it is, very clearly stated ‘We know more than you think we know and we are coming for you.’ Part of this, by the way, is that New Zealand and therefore Inland Revenue has signed up to the new Crypto-Asset Reporting Framework (CARF) recently developed by the Organisation for Economic Cooperation and Development. This is yet another example of the growing international cooperation on the exchange of information, a regular topic on this podcast.

Under CARF the first set of reporting is due to apply from the 2026/27 tax year which will lead through to increased tax revenue. In fact, according to the Budget, the expectation is that CARF will deliver $50 million of additional tax revenue in the June 2028 year..

That’s in the future. What’s happening right now is that Inland Revenue has used its existing network of information exchanges and data sharing almost certainly by tax treaty partners such as Australia, the UK and the US, to obtain data about transactions carried out by New Zealand based crypto-asset investors and traders. It’s now going to put the squeeze on those it considers non-compliant.

It’ll be interesting to see what comes out of it and we will watch with interest and bring you news of developments. In the meantime you have been warned and this is of course the latest sign of the gathering storm of Inland Revenue investigations.

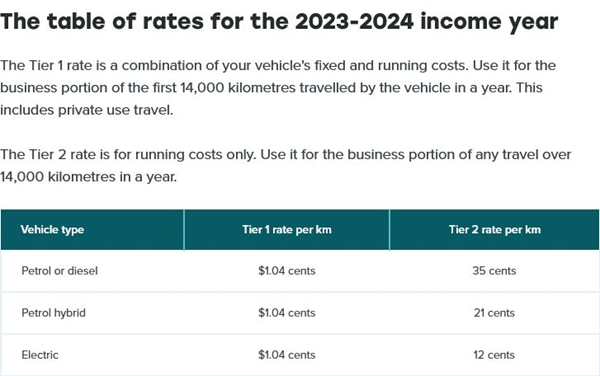

Inland Revenue kilometre rates for 2023-24

Moving on, Inland Revenue has just published its kilometre rates for the 2023-2024 income year. Unsurprisingly, given the recent rise in fuel prices, the so-called tier one rates show an increase in vehicle running costs that are allowable for the year. These rates may be used to calculate the deductible running costs for a vehicle.

Note that the Tier 1 rate of $1.04 for the first 14,000 kilometres applies to all vehicles whether petrol, diesel, hybrid or electric. The Tier 2 rates above the first 14,000 km DO vary between vehicle type.

This is good to know, but I do wonder whether it might be a bit more useful to have this sort of information earlier in the relevant tax year. Inland Revenue obviously wants to be accurate, but a different approach perhaps might be to adopt an interim rate and index that for inflation. Anyway, these are the rates that are now applicable for the 2023-24 tax year if you wish to claim the relevant deduction.

Are we raising enough tax?

And finally, this week, the Tax Policy Charitable Trust held an event on Thursday last night to announce its four finalists for this year’s Tax policy scholarship prize. The first half of the event was a panel discussion on New Zealand’s tax revenue sufficiency. Ably chaired by Geof Nightingale, a member of the last two Tax Working Groups, the four panellists that joined him were Talia Harvey and Matt Wooley, joint winners of the scholarship prize in 2017, Nigel Jemson, the winner in 2020 and Vivian Lei, the winner in 2022. You may recall Vivien, have previously been a guest on the podcast.

L-R Matt Woolley, Geof Nightingale, Vivien Lei, Talia Harvey and Nigel Jemson

Now, this was a fascinating panel discussion conducted under Chatham House rules, focusing on the scale of fiscal challenges for the next few decades and how could we meet those? Does this mean for example, some new taxes might be required such as capital gains tax? What about boosting Inland Revenue’s investigation efforts? And then on the spending side of the equation what do we do about rising health care and superannuation costs? Do we perhaps increase the age for eligibility or (re)introduce some forms of mean testing for New Zealand Superannuation? All these points were raised for discussion.

The panel discussed ‘the tax gap’, the gap between what we think the tax collection should be and what’s not being collected. There’s a lot of work to be done in this space, because we really don’t have a clear handle on the extent of this particular issue. Some work carried out several years ago by Inland Revenue suggested that when you look at the consumption patterns between self-employed persons and employees, there might be as much as a 20% gap. In other words, self-employed people appear to have about 20% higher levels of consumption than employees on ostensibly similar levels of income. This is a topic which actually might be worth a podcast episode in itself.

And the finalists are…

It was then followed by the announcement of the four finalists of this year’s Tax Policy Charitable Trust scholarship prize. Every two years the Tax Policy Charitable Trust invites young professionals (anyone under 35 on 1 January 2024) to submit proposals for review, improving any aspect of New Zealand’s tax system. Entrants submit a 1500 word overview proposal on any part of the tax system from which the judges choose four finalists will be selected to go through for the final main scholarship prize, which is worth $10,000.

Submissions are judged for their creativity, original thinking and sound and reasoned research and analysis. In addition the judges take the following factors into consideration:

Impact on the New Zealand economy, including GDP and business growth.

Social (including distributional equity) and environmental acceptability.

Feasibility of introduction, including political and public acceptability.

Impact on simplicity of tax system.

Ease of administration by taxpayers and Inland Revenue, or other relevant government agencies, and impact on compliance costs.

This year, there were 17 entrants and the four finalists chosen are

Matthew Handford, who proposes an Independent Tax Law Commission aimed at improving the Generic Tax Policy Process, or GTPP. The GTPP is a cornerstone of tax policy and is internationally well regarded, but it’s now 30 years old, so is due a reconsideration. I look forward to hearing more about Matthew’s proposal.

Claudia Siriwardena, who is suggesting a simplified FBT regime for small and medium enterprises. This gets a big tick from me, and I’m very interested in hearing more about this one.

Matthew Seddon, who proposes extending the independent contractor withholding tax regime. Mathew’s suggestion picks up the point just raised about the tax gap and deals with it by improving compliance. Again, another interesting proposal.

Finally, Andrew Paynter who is putting forward a proposal to increase the GST rate from GST but also tackle the regressivity of GST with a rebate for low and middle income earners. I’ve seen some international papers on this particular topic, so I’m very, very interested to hear more about what Andrew’s proposing here.

My intention is to get all four scholarship finalists on the podcast to talk about their ideas before the winner is announced in October, so stay tuned for developments. In the meantime, congratulations to Matthew, Claudia, Matthew and Andrew and to everyone else who entered. No doubt there were some interesting ideas put forward that did make the cut this time, but overall, it’s a great sign of the healthy state of tax policy debate in New Zealand.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Originally loaded to Soundcloud 6 July 2024. On interest.co.nz 8 July 2024).

It was a busy week in tax with Inland Revenue releasing guidance in relation to a couple of commonly encountered scenarios. The first is QB 24/04When is a subdivision project a taxable activity for GST purposes?

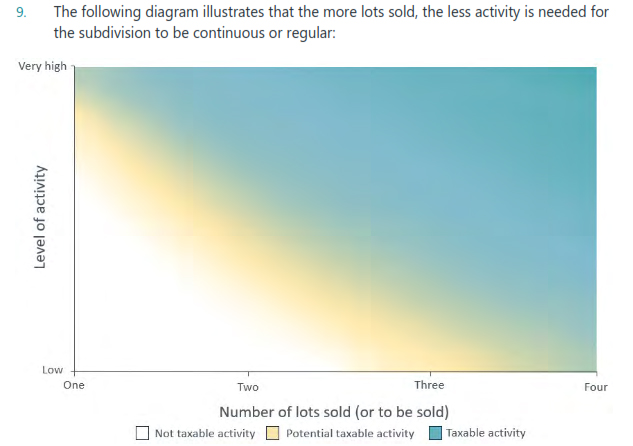

This covers the frequently discussed and very important issue of what is the GST treatment when you are subdividing land into two or more plots? The standard position about GST is that you must register if you’re carrying on a taxable activity and the value of those supplies exceeds the registration threshold of $60,000.

What’s a taxable activity?

Clearly many subdivisions will exceed that $60,000 threshold when they are sold so what represents a taxable activity? In order for a taxable activity to exist it must be carried on continuously or regularly. Therefore, it follows that for a subdivision to be continuous or regular, it usually needs to involve the sale of more than one lot. A subdivision which only involved one sale would usually be regarded as a one-off activity because it does not meet this threshold of continuous or regular.

Notwithstanding that the Inland Revenue guidance points out that some subdivisions which only led to one sale may in fact be continuous and regular. But that would only be if the level of activity involved was very high. Now, like so much of tax, it’s this comes down to the question of the facts of a particular case. Very high in this context might be something like construction and sale of a large office block, or more likely, because more often than not we’re talking about subdivisions of residential land, an apartment block.

The guidance continues the more subdivision plots are divided, the more likely it is to be deemed as being continuous or regular. Following the Newman decision way back in 1995, if a subdivision leads to the sale of four or more lots, that’s typically taken as the benchmark for determining that the continuously or regularly is happening and there is a taxable activity.

On the other hand, what happens when there are two or three lots? Then you have to consider the level of the activity relative to the number of lots being sold in order to determine whether or not this activity is continuous or regular. Therefore, you’d look at the level of development work, the time and effort involved, the level of financial investment and the level of repetition. This last point is probably most critical. If you’re repeating the process multiple times, this is more likely to fall into the continuously or regularly category. But as the guidance notes, everything is fact dependent.

On the other hand, the factors that are not so relevant are whether or not the subdivision is commercial. It doesn’t matter whether the subdivision has a “commercial” flavour or you are subdividing your own land to downsize. Anything done without an intention to sell the resulting land is not relevant. For example, if you build a house on a subdivided lot with the intention of living in it, but later change your mind and decide to sell, work done before you change your mind is not relevant.

Overall, this is useful guidance which comes with a helpful accompanying fact sheet. Keep in mind that the GST treatment is not tied to the income tax treatment. Your project might not be a GST taxable activity, but it could well be subject to the bright-line test or any of the other land taxation rules.

Another common issue – loans to shareholders

Moving on, the other topic, on which Inland Revenue has released useful guidance is a draft interpretation statement on the income tax position in relation to overdrawn shareholder loan account balances (sometimes called shareholder current accounts). Now, as anyone who works with small businesses will tell you this is actually a pretty common scenario. Despite this, the income tax position is not always as well understood as it should be.

In my experience, overdrawn shareholder current account balances typically arise in two scenarios. Firstly, where the owner or shareholder is taking out more in drawings than they’re being paid as a shareholder or employee or any other form of payment. This is a fairly common scenario.

The other instance is where the company has realised the substantial capital gain and shareholders extract the cash without waiting to consider the tax implications of doing so. Often in those situations, advisers don’t find out until maybe months afterwards. At that point it can become quite difficult to unwind the tax consequences because the numbers involved are quite substantial.

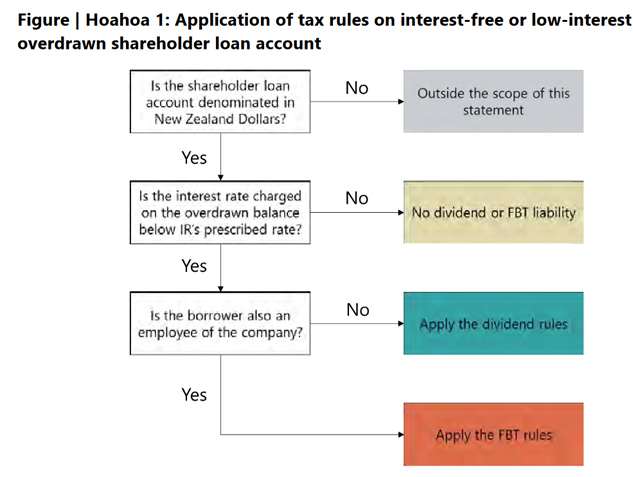

It’s therefore good to have Inland Revenue guidance and this comprehensive interpretation statement runs to 41 pages begins with the summary of the basic rules. A dividend is deemed to arise for a shareholder if they are paying little or low interest on an overdrawn shareholder loan account.

The amount of a dividend on an interest free or low interest loan typically represents the difference between a benchmark interest rate that should be charged and the amount of actual interest rate occurring on the loan. Benchmark for this purpose is Inland Revenue’s prescribed rate of interest, which since 1 October 2023 has been 8.41%.

A dividend can also arise where the loan has been advanced to an associated person of the shareholder. This can lead to some quite involved tracing of shareholdings and related calculations about percentage of shareholdings. This is necessary to determine if there is an association and whether that associated company is part of the same 100% owned group and therefore potentially eligible for the exemption on intra-group dividends. This is another area where I’ve encountered situations where this associated person issue hasn’t been picked up.

Incidentally, it’s worth noting, by the way, that although for New Zealand tax purposes, the amount of the dividend is the amount of interest that should have been charged in Australia and the UK, the amount of the dividend is deemed to be the full amount of the advance made. This might be something we might see Inland Revenue take a look at as it’s something that has occasionally come up in discussions with officials.

Loans to shareholder-employees

Were the shareholder is also an employee of the company, then the low or interest free loan is not treated as a dividend but is instead subject to fringe benefit tax. The amount of the benefit is the difference between the interest paid and the prescribed rate of interest. Something to note here is that the shareholder-employee doesn’t solely mean someone within the provisional tax regime, but it also includes shareholders who are employees and whose salary are subject to PAYE There’s a couple of useful flow charts to help people determine who might be captured by these rules.

The draft interpretation statement also notes that typically interest paid by a shareholder on an overdrawn current account is generally not deductible. This is because usually the drawings are often applied for private or domestic purposes, and so there’s no link to an income earning process. However, in some cases the money might have been withdrawn to invest in a residential property or some other income producing asset, in which case the interest would become deductible, if all the other deductibility criteria can be met.

One other key point to note is what happens if a shareholder is no longer required to repay the overdrawn balance, because the company forgives or remits the debt in some way. In this case the full amount of the loan will be deemed to arise either as a dividend or under the financial arrangements regime. In either case the shareholder will usually be taxed on the amount that’s been remitted.

The interpretation statement also covers scenarios when resident withholding tax might need to be deducted and interest therefore be reported as investment income. This would be somewhat unusual, but the interpretation statement explains when it might happen.

Overall, this is an important and useful document setting out the rules pretty clearly on a topic which as I noted is frequently encountered amongst small businesses but isn’t always as policed or managed as effectively as it should be. It’s also accompanied by a more digestible 8 page fact sheet. Consultation is open until 2nd August.

A blueprint for taxing billionaires?

One of the interesting things going on around the world in the tax policy area now is something of a trend amongst international organisations such as the International Monetary Fund (IMF), the Organisation for Economic Cooperation and Development (OECD) for releasing papers for discussion on the taxation of capital and wealth.

The latest such paper A blueprint for a coordinated minimum effective taxation standard for ultra-high-net-worth individuals was commissioned by the Brazilian G20 presidency earlier this year. The report was written by the French economist, Gabriel Zucman, a protégé of Thomas Piketty. It proposes a framework the approximately 3,000 or so billionaires in the world to pay at least 2% of their wealth in individual income tax or wealth taxes each year.

Zucman’s report notes there been a vast improvement in international tax cooperation since the mid-2010s, particularly with the Common Reporting Standard on the Automatic Exchange of Information which commenced in 2017. He also pointed to the recent agreement hammered out by the OECD for a minimum tax of 15% on large multinationals. (It’s worth noting though that agreement has yet to be fully implemented as progress has slowed recently).

Zucman correctly points to this growing international cooperation and exchange of information as laying the baseline for further international cooperation in the form of what he terms a common minimum standard, ensuring an effective taxation of ultra-high net worth individuals. According to Zucman this “would support domestic policies to bolster tax progressivity by reducing incentives for the wealthiest individuals to engage in tax avoidance and by curtailing the forces of tax competition.” This would target the tax havens where much of this wealth is sheltered.

The paper estimates that a 2% tax on those 3,000 billionaires could realise between US$200 and US$250 billion U.S. dollars in revenue annually. If it was extended to those worth more than $100 million, that could generate another US$100 to US$140 billion per annum. These tax revenues would be collected from “economic actors who are both very wealthy and undertaxed today”. Those affected might not agree with this assessment that they’re presently under taxed.

The paper is realistic enough to note that there are real challenges with the proposals, such as how to value the wealth, ensure effective taxation if some jurisdictions don’t agree to implement it, and of course compliance by taxpayers. It’s a bold proposal which has attracted a lot of attention although I’m sceptical about the potential level of revenue which could be raised. We really don’t have a very detailed understanding of the composition of the wealth and where it is held of the very wealthy. That’s an issue which would need to be addressed. And as I mentioned, there are serious issues around valuations and informed enforcement, which Zucman acknowledges.

Starting a conversation?

But for me, the most interesting thing to me about this whole proposal, it’s the latest. As I said, it’s the latest in the line of papers coming out of the likes of the G20, the OECD, the IMF, the World Bank, all of whom are basically saying that we are not taxing wealth sufficiently and we need to do something about that to address inequality. As Zucman himself puts it in the Foreword of the report

“The goal of this blueprint is to offer a basis for political discussions – to start a conversation not to end it. It is for citizens to decide through democratic deliberation and the vote how taxation should be carried out.”

In other words, he is repeating my old precept that tax is politics.

My personal view is we need to have a broader discussion around the taxation of capital. One of the points to emerge from the current debate going on over replacing the Cook Strait ferries is that the new ferries represented just 21% of the total cost of Project iReX. The other 79% represented the cost of upgrading the supporting infrastructure not just for the larger ferries but also to make it climate change and earthquake resilient for the next 100 years.

Even if we dialled back the futureproofing to, say, 50 years, we’re still talking about significant sums of investment. We’re also still left with the key point of how will we pay for the vast amount of infrastructure that we will need to upgrade to deal with the continuing impact of climate change. In my view our politicians have not yet seriously engaged with us on this issue.

Meanwhile in the UK…

And finally, this week a quick note on the UK election which is next Thursday. The likelihood is that the opposition Labour Party is heading for a massive win. One of their key tax proposals is the abolition of the remittance basis or non-dom tax regime.

But not every voter has understood exactly what that means. As Labour candidate Karl Turner recounted to the Guardian

“We met a guy who said he was going to vote Labour but wouldn’t now because he had just heard that we were taxing condoms,”

“I said, ‘condoms?’ ‘Yeah,’ he said: ‘I just heard on that [pointing to the TV] that you are taxing condoms, and I’m not having it. You’re not getting my vote.’ It was Terence [Turner’s parliamentary assistant] here who worked it out.

“‘We’re taxing non-doms, not condoms,’ I said. ‘Oh,’ he said. ‘Like the prime minister’s wife? Ah.’ He calls out: ‘Margaret: they’re taxing non-doms, not condoms.’”

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Loaded to Soundcloud 30 June 2024. Appeared interest.co.nz 1 July 2024).