- Rachel Reeves, the first ever female Chancellor of the Exchequer delivers a UK Autumn Budget with potentially significant implications for many Kiwis and Britons who have migrated to New Zealand.

- Meanwhile Inland Revenue’s crackdown on tax evasion continues.

The UK finance minister is officially called the Chancellor of the Exchequer, a post which is more than 800 years old, and until this year it had never been held by a woman. So, when Rachel Reeves, the Labour Chancellor of the Exchequer delivered her maiden budget speech last Wednesday night, she made history as the first woman Chancellor in British history.

There was quite a lot to consider in this UK Budget, as people were watching to see how the new government would respond to the challenges it inherited. British budgets, unlike ours, coincide with the release of a Finance Bill and tax measures there’s always a lot of tax matters to consider beyond the headline measures.

The headline measures

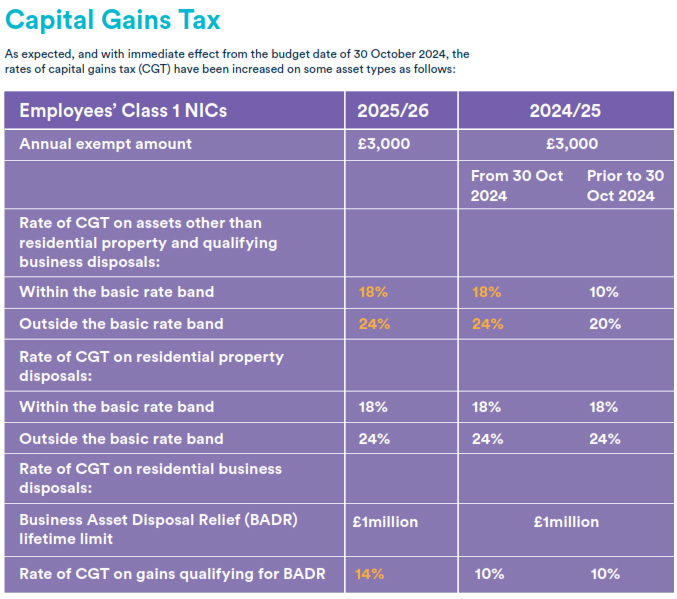

Most notably, there was an increase in Employer National Insurance Contributions (a Social Security tax) by 1.2 percentage points to 15% with immediate effect. There are also immediate tax rises for capital gains tax, but the top rate for capital gains tax still was capped at 24% for both property and non-property assets. Which as some commentators said is still lower than countries with which the UK compares itself. It’s quite interesting to see that comment about 24%, because one of the key points of our discussion around capital gains taxes here is what rate would apply? It’s therefore interesting to have an international comparison.

Beyond the headlines

It’s always interesting to dig around in other countries’ budgets and see what they do in certain areas. For example, the UK doesn’t have an imputation credit system, but there are lower rates of tax applied to dividends, even for those on the highest income. There’s also a savings allowance, which exempts certain amounts of investment income. It’s currently £1,000 for basic rate taxpayers (taxable income up to £37,700) and £500 for the higher rate taxpayers. The UK basic rate of tax is 20% and we have two rates lower than that so this savings allowance is not necessarily a measure we might want to copy here.

Twin cab utes and fringe benefits – an example to follow?

There’s apparently some uncertainty around the fringe benefit taxation treatment of twin cab utes which the Budget clarified. Where they have a payload of one tonne or more such vehicles are not there to be treated as cars for benefit in kind purposes unless they were acquired prior to 6th April 2025.

On Fringe Benefit Tax, the benefit value is calculated as a percentage of the vehicle’s list price when the car was first registered which is similar to our treatment. However, the percentage used is determined by the vehicle’s carbon dioxide emissions, or its range if it’s an electric vehicle. These percentages are set to increase steadily over the next three years as part of the range of tax increases announced. Inland Revenue is presently reviewing FBT and as is well known tax can act as a disincentive. If we want to incentivise a transition to a lower emissions economy, maybe we should be looking at how the UK applies FBT to vehicles.

UK pension tax free lump sum unchanged

There’s always lots of rumours before a Budget which I’ve seen sometimes used as a means to get people to buy new products or make tax driven decisions in fear of change. One of the rumours before this budget was that there were going to be changes to the taxation of pensions and in particular to the 25% tax free lump sum. That hasn’t happened, but remember, our rules are completely different. Just because 25% of the pension can be withdrawn tax free in the UK, that doesn’t mean the same rules apply here.

The big changes

But the main reason I was paying particular attention to this UK budget was because we finally got more detail around the two announcements made in the March Budget – the new foreign and income gains regime and the end of the non-domicile regime and the changes to inheritance tax. These are both measures which have significant impact for New Zealanders, who are either going to the UK or have returned to the UK, but also for UK expats who have migrated here.

New foreign income and gains regime

The foreign income gains (FIGS) regime is very similar to our transitional resident’s exemption in that a new tax resident’s foreign income and capital gains will be tax exempt for the first four UK tax years that they are resident in the UK. It’s not like our 48-month exemption period, it is tied to the UK tax year, which remember runs from 6th April to 5th April. (Perhaps reflecting that some of this stuff does date back 800 years or more, there’s no intention to change that tax year end).

What has also been clarified is that individuals who have previously elected to be taxed on the remittance basis, which meant their non-UK sourced income investment income was not taxable, can now be allowed to take advantage of a so-called temporary repatriation facility. This will last for three years, and they will be able to nominate and remit their non-UK income and gains from years when they were within the remittance basis and take advantage of lower tax rates. Initially 12% for the first two years ending 5th April 2026 and 2027, and then 15% for the year ended 5th April 2028.

As part of the FIGS regime there are also changes to what’s called the Overseas Workday Relief. This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties determined on “a just and reasonable basis”. This is quite a significant one for expats and for companies that have very highly paid and skilled employees and has been greeted with general enthusiasm by by those impacted.

Inheritance Tax

Potentially the biggest change though, is in relation to inheritance tax (IHT). This applies to all assets situated in the UK or all assets situated anywhere, if the person is domiciled within the UK. There’s a nil rate band of £325,000, above which 40% will apply (these rates and thresholds have been frozen until 2030). IHT has a potentially significant impact because under the present rules, someone tax resident outside the UK could still be within the IHT net because they are still deemed to be domiciled in the UK. I’ve had to deal with one or two of these instances.

There’s also a pretty nasty trap for someone like me who might have left the UK a long time ago and adopted a new domicile of choice outside the UK. At present if I ever became tax resident again in the UK, our domicile would immediately revert to the UK. Therefore, working or living for prolonged periods of time in the UK was actually potentially highly tax disadvantageous from an IHT perspective.

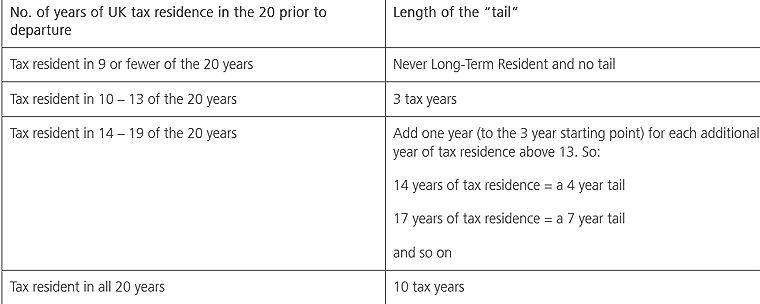

All this will be replaced now by a residence-based regime. The tests for whether non-UK assets are subject to IHT will now be whether the individual has been tax resident in the UK for at least 10 out of the last 20 tax years immediately preceding the tax year in which the chargeable event, most typically death, but can also be a lifetime transfer into a trust, happens.

There’s also a tail on how long a person is in scope if they’ve been non-resident during a period. For example, if someone had been UK tax resident for between 10 and 13 years, they remain in scope for IHT for three years post departure.

(Courtesy Burges Salmon)

Implications for New Zealand residents

What this change means for a lot of British expats resident here is they’ve got to think again about what their IHT obligations could be. By the way, our double tax agreement with the UK does not cover IHT. The UK has the right to charge IHT on assets situated in the UK, that’s not surprising. However, it potentially also has got a long reach if HM Revenue & Customs determine someone resident here is subject to IHT.

IHT and trusts

One of the other IHT changes is to the taxation of trusts used to hold assets outside the scope of IHT, so-called excluded property trusts. If I understand it right, starting from 6th April 2025, if a settlor dies and they’re within the scope of IHT, assets settled by them into what was previously an excluded property trust are now within IHT. This is a major change and I’m investigating it further given we make very extensive use of trusts. I’ve been dealing with quite a few clients who have UK connections year and it’s been really revealing to see how complex the taxation of trusts is from the UK perspective. It’s good to see some clarity around the new rules, but as I say, it’s a significant budget in many ways, and there could be quite major consequences for more people based here than they might anticipate.

Meanwhile, Inland Revenue’s crackdown continues

Moving on, Inland Revenue continues its crackdown when it announced on Thursday that it’s making unannounced visits to hundreds of businesses who it believes are not meeting all their tax obligations as employers.

According to Inland Revenue, they receive about 7000 anonymous tip offs each year. It has said “the volume of tip offs has grown over previous years indicating an increased sense of frustration by the community in general, businesses who are not doing the right thing.”

Inland Revenue’s analysis shows that the tax risks overwhelmingly relate to taking cash for personal use without reporting sales and or paying employees in cash.

Based on this Inland Revenue is making unannounced visits to over 300 employers whose practices it will closely examine. I’ve seen this happen with a few clients under investigation. Inland Revenue staff will go to a café or business and just watch to see what’s happening. They may buy something, but they will certainly sit and observe and see who uses the till, how everything is recorded and from there they will draw the relevant conclusions.

The consequences of being investigated

As an example of what happens to taxpayers who have not been compliant, the director of an asbestos removal and labour hire company has been jailed for three years in what the judge called serious offending and the worst of its kind to come before the Christchurch District Court in the last 20 years. The director, Melanie Jill Tatana, also known as Melanie Jill Smith, was jailed for three years for what was described as wilful diversion of funds.

Her company employed around 60 people, and between April 2019 and September 2022 had been required to deduct PAYE on 63 occasions but failed to pay the full amounts totalling $1.6 million. Tatana was therefore charged with 63 counts of aiding and abetting to knowingly take PAYE from workers’ wages and not pay it on to Inland Revenue. Instead, more than $800,000 had been diverted for her personal use.

One of the more encouraging things from my perspective about this case is that this offending has all been pretty recent and Inland Revenue tracked it down within a couple of years. I’ve seen cases where the offending has been four or five years.

I still think 63 occasions of nonpayment is a little generous, but bear in mind that Inland Revenue did take the the foot off the throttle around pushing hard on on companies and businesses because of COVID. That amnesty or less stringent approach is now over and it’s back to business. And Tatana won’t be the first to find out about Inland Revenue’s hardline approach.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.