Tax cuts delivered, but watch out student loan borrowers.

After what seems to have been an interminable dance of the seven veils, all has been revealed and we now know the final shape of the Government’s tax package. Nicola Willis has delivered on National’s manifesto and increased thresholds as promised.

That was unsurprising, although there’s a twist in that these changes will take effect from 31 July, four weeks later than expected. The delay is to enable payroll providers to update their systems.

The big surprise for me is the decision to increase the threshold for the Independent Earner Tax Credit (IETC) to $70,000. As I said in my Budget preview, I expected this to be cut to help pay for, or even increase, the threshold adjustments. Speaking on Breakfast TV, I expressed the hope that any threshold adjustments would focus on the group around the threshold where the tax rate jumps from 17.5% to 30%. The lift in that threshold to $53,500 together with the extension of the IETC will help, but more needs to be done in my view.

Giving with one hand, taking with the other…

The Government has also increased the in-work tax credit (IWTC) by $50 per fortnight, which is welcome. However, its effect will be mitigated by the fact that the $42,700 annual family income threshold above which the IWTC will be abated at a rate of 27 cents per dollar remains unchanged. The threshold has not been increased since 1 July 2018 which means that families with income above the threshold face an effective marginal tax rate of at least 46.1% (17.5% plus 27% abatement plus 1.6% ACC Earner Levy) which is higher than that of the Minister of Finance. It remains remarkable to me that this issue has been allowed to continue for so long, but when I raised the issue with the Minister of Finance her response was “I utterly reject the question”. (There were quite a few other questions also rejected with varying degrees of utterly).

Increased Inland Revenue funding

As also promised by New Zealand First in its manifesto, the Budget proposes an additional $29 million annually for increased compliance activities. Interestingly, the specific appropriation for investigation, audit and litigation activities will be increased from $106.2 million to $165.4 million. The Appropriation for Services to manage debt and unfiled returns will also rise from $83.5 million for the June 2024 year to $105.7 million in the coming year. Both increases indicate we should expect to see a significant rise in Inland Revenue investigation and debt management activity.

Student loans

Unlike my prediction about the IETC, my speculation that there would be some increases here was correct. The Government proposes increasing the interest rate on student loan debt payable by overseas based borrowers from 3.9% to 4.9% from 1 April 2025. Furthermore, the late payment interest for both overseas AND New Zealand based borrowers will increase by 1 percentage point.

However, as previously discussed, the amount of student loan debt has steadily increased and only 26% of overseas-based borrowers are making repayments. The Budget Appropriations include a provision for debt impairment of $633 million (up from $539 million) for the coming year.

As noted above Inland Revenue is boosting its compliance activities for student loan overseas-based borrowers, “including those returning to or visiting New Zealand”. We can therefore expect to see a few defaulters being detained at airports. It will be interesting to see if such moves result in significantly increased repayments.

Waste disposal levy changes

Elsewhere, the Government proposes increasing the level of Waste Disposal Levy but at a lower rate than initiated by the previous Government. It’s anticipated the Levy will raise a total of $1.195 billion over four years to 2027/28 which is split 50:50 with local government. The Government proposes amending the Waste Minimisation Act 2008 to expand the range of activities the levy can be used for, such as restoring freshwater catchments. This sort of recycling of environmental levies is to be supported but perhaps the split between local and central government should be shifted in favour of local government.

Calling Inland Revenue?

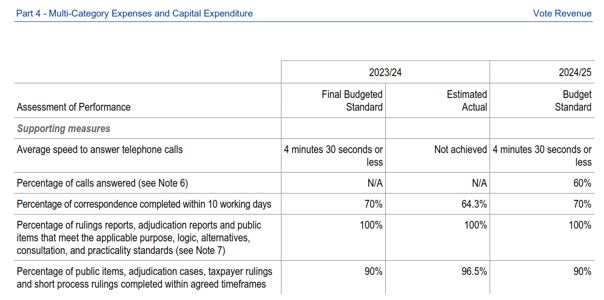

Wading through the detail of the Appropriation Estimates often reveals some interesting nuggets. The Vote Revenue Estimates included the following details about Inland Revenue’s expected performance when answering calls and responding to correspondence. It will be no surprise to many to note that the standard of answering calls within 4 ½ minutes was not met. Going forward Inland Revenue expects to answer 60% of all calls so I will check in next year to see how it performed.

Now what?

Having delivered on its campaign promises what next for the Government’s tax policy? The Finance Minister referenced the ACT Party’s proposals to flatten the tax scale but made no commitment as to when that might happen.

Willis also acknowledged Treasury’s advice of a structural deficit of about 1.5% of GDP (roughly $6 billion). This can only be addressed by spending cuts or tax increases and the expectation at present is for spending cuts to meet that gap. That means any future threshold adjustments are off the table, including the possibility of automatic indexation at some point. For the moment the Finance Minister will be happy to take the credit for the changes announced today. Let’s just hope it doesn’t take another 14 years for the next revisions.

This week a preview of what tax measures might be in Thursday’s Budget. What could Finance Minister Nicola Willis do to cover the cost of the tax threshold adjustments and where might Inland Revenue get additional funding for investigations and enforcement?

Also the UK election and the latest fallout from the ATO’s raid on Exclusive Brethren related businesses.

Before we preview next Thursday’s Budget a quick note on a couple of other interesting developments this week. The announcement of the UK General Election on 4th July will further delay details around the replacement of the current remittance basis of taxation. You may recall this was originally announced in the UK’s Spring Budget on 6th March. The proposal was for the remittance basis to be replaced by something similar to our Transitional Resident’s Exemption.

We were meant to have seen draft legislation by now, together with consultation on the related inheritance tax implications of the proposed change. But neither of those had materialised by the time the Election was called. We therefore remain in limbo as to what will be happening, although we do understand that the Labour Party, currently odds-on favourite to win the election, is broadly in favour of the new rules. As always, we’ll keep you up to date on when further developments arise, but in the meantime, anyone potentially affected should continue to plan on the basis that the existing remittance basis rules will remain in force.

Fallout from the ATO’s investigation into the Exclusive Brethren

In early April, I covered the Australian Tax Office’s (ATO) no notice raid on the offices of businesses related to the Exclusive Brethren. This week, the accounting firm Universal Business Team Australia or UBTA which is controlled by the exclusive Brethren, advised its clients that its accounting division would close with immediate effect. The same announcement said that UBT’s UK and New Zealand operations will continue unaffected for the moment.

As I said at the time of the initial ATO raids it would be interesting to see whether Inland Revenue will initiate a similar investigation of the Exclusive Brethren’s New Zealand related operations. It has to be said that closing down the accounting operation indicates that something fairly serious has been identified by the ATO. But no doubt we’ll find out more in the coming months.

A much anticipated Budget

Thursday is Budget Day. This will be my 14th Budget lockup and I’m looking forward to it as I always do. But this year is probably one of the most anticipated budgets in in a long time. There are two reasons for that. On the one hand, many people are very keen to finally discover the size of the proposed tax cuts and how they will personally benefit. On the other hand it’s a pretty anxious time for civil servants and a myriad of agencies and organisations waiting to see how the accompanying budget cuts will affect them.

Lessons from Bill English

Former Prime Minister Bill English, who’s been advising the current government, delivered eight budgets during his time as finance minister and it would be surprising if Nicola Willis had not absorbed a few lessons from his experiences. Clearly what she would love to do is match what English did in 2010, when he masterminded a so-called tax switch. This cut the top personal income tax rate from 38% to 33%, together with a reduction in the corporation income tax rate to 28%. But at the same time, he increased GST from 12.5% to 15%. As former Labour Minister of Revenue David Parker ruefully admitted it was a masterpiece of political campaigning and delivery.

But Bill English was also a master of slipping in some quiet and relatively unnoticed tax increases. There was a controversy in 2012 about the removal of an old measure which primarily affected paper boys. But one which was turned out to be very significant was the reintroduction of employer superannuation contribution withholding tax on employer KiwiSaver contributions in 2011. That’s now worth almost $2 billion a year according to Inland Revenue’s annual report to June 2023

Bill English, and to be fair, Grant Robertson, were both happy to allow fiscal drag to increase the tax take, hence the fact that tax thresholds have not been adjusted since 2010. Tax cuts were a key promise of the National Party and the ACT Party and the key delivery in this budget will be increasing income tax thresholds. These are certainly one of the tax measures we know will happen. We also know that there will be increased funding for Inland Revenue for investigations as that was included in the coalition agreement with New Zealand First.

What did National promise?

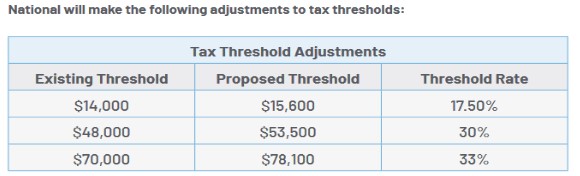

On the tax threshold adjustments, National’s promises in its election manifesto were fairly modest.

As long-standing listeners to the podcast will know, I think the $48,000 threshold is highly problematic.

Steven Joyce and the Independent Earner Tax Credit

Now it’s worth noting and remembering back in 2017, then Finance Minister Stephen Joyce proposed quite a significant family incomes package, including threshold adjustments, for the 17.5% and 30% rates. As part of the measures to pay for those increases, he proposed cancelling the Independent Earner Tax Credit (IETC). This is a tax credit worth up to $520 a year for people earning between $24,000 and $48,000. One of the rationales given by Joyce for cancelling the IETC was that only 30% of those people who could claim it actually did so.

Here’s where it gets quite interesting. According to the Tax Expenditure Statement (tax expenditure statements estimate the cost of a specific tax relief) released at the time of the 2017 Budget, the estimated cost of the IETC for the year ended 31 March 2017 was about $223 million. The Tax Expenditure Statements released in last year’s budget estimates the value of the IETC for the year ended 31 March 2023 to be $174 million. According to Treasury the amount of IETC claimed “has fallen by 9.5% over the past two years.

The Independent Earner Tax Credit to be abolished?

My first big prediction is therefore that the tax threshold adjustments, the IETC, will be abolished, which would free up $174 million. As I said, it would be interesting to see where the emphasis of those threshold adjustments will fall. I’d like to see them focus around that $48,000 mark.

By the way, Steven Joyce would have increased the threshold where the 17.5% rate kicks in from $14,000 to $22,000 and the threshold at which the rate increases to 30% would have been increased to $52,000. Inflation has really devalued those thresholds, so it will be interesting to see what comes out on Thursday relative to what was proposed in 2017.

What Inland Revenue investigation activities will get funded?

Now the other thing that definitely is going to happen is increased investigations and enforcement funding for Inland Revenue. I expect there to be a reasonably substantial increase. At present in the Appropriations to June 2024, there’s $133.8 million of funding for investigations. Just to put some things in context, in Steven Joyce’s 2017 Budget, the Appropriates for investigations for the year to June 2018 was $173.7 million. Inflation adjusted that would now be close to about $200 million. However, I doubt whether Inland Revenue presently has the capacity to use what would effectively be in a 50% boost in funding. (As an aside, the reduction of investigation staff funding since 2018, has been a matter of some controversy – were too many skilled people let go just to make the numbers balance?)

A fringe benefit tax review?

Whatever additional funding is provided I expect to see tied to specific initiatives. One of those will be in relation to fringe benefit tax (FBT) which has just been in the news. Inland Revenue’s Stewardship Review of FBT in 2022 has clearly caught the Minister of Revenue, Simon Watts’ attention, because he’s mentioned it in a couple of speeches. We also know through an Official Information Act release that he has received advice on his options for review. These are either a once over lightly approach or a more fundamental review. Inland Revenue prefers the latter approach. As previously mentioned, FBT has been around for a long time and it’s long overdue for serious review. Expect the Budget to contain funding for that review.

Dealing with the hidden economy and organised crime

There will also be substantial funding given for an initiative into the hidden economy. Minister Watts has received advice on Inland Revenue’s role in defeating organised crime which includes money laundering and tax evasion. Increasing funding here would not only tick the box for the Coalition agreement with New Zealand First, but also with the Coalition Government’s wish to get tough on crime and the gangs.

Cracking down on Student Loan debt

I also expect to see a fairly substantial amount of funding given to addressing the question of student loan debt which currently stands at over $9 billion. There’s a particular problem with overseas based borrowers, many of whom are in default either because Inland Revenue doesn’t know where they are, or they’re simply ignoring any requests for payment.

At the moment, Inland Revenue’s record with overseas defaulters is not terribly impressive. According to Inland Revenue’s annual report for the June 2023 year, it received just 108 payments totalling $16,421 from 18 overseas based student loan defaulters.

You can therefore expect a crackdown. Not only will there be increased funding to track down defaulters (including greater use of the existing agreement with Australia), I expect the Government will make it very clear that the already existing powers to detain student loan defaulters at the border will be enforced. Expect to hear more stories about that.

More Student Loan changes?

I also wonder whether the student loan repayment rate may be increased. One of Bill English’s sneaky tax measures was back in April 2013 when he increased the repayment rate from 10% to 12%. Another increase would mean student loan borrowers would have one of the highest effective marginal tax rates because this 12% or whatever it might be, is on top of their PAYE deductions.

Alternatively, the Government might introduce a nominal interest charge on student loan debt, or they could increase the minimum amounts of repayments required by overseas borrowers. Re-introducing interest on student loans would be a controversial measure. But my view is, if you’re going to have controversy around tax, you do it in your first budget.

What about GST on fund management fees?

If Nicola Willis is considering measures which could help claw back the cost of threshold adjustments GST on management services to managed funds is one which I think might come back onto the table. You may recall when the Labour Government introduced this proposal in August 2022 it withdrew the bill within 24 hours in the face of some ferocious pushback, which also included the fairly creative use of some long term fiscal impacts as to the potential impact on KiwiSaver funds.

That measure would have done two things. It would have clarified the treatment, which is currently very ad-hoc, but it would also, and this is where Finance Minister Nicola Willis, will be paying attention, have been worth about $225 million a year from 1st April 2026. So don’t be surprised if it’s reintroduced again to help pay for the tax threshold adjustments and as part of a “rebalancing.”

Could Cash PIEs be in the firing line?

Potentially the most controversial measure, though, would be to tackle the question of the prescribed investor rate (PIR) on portfolio investment entities (PIEs). Currently the highest PIR for a PIE is 28%, which means there’s an 11-percentage point difference between the top maximum prescribed investor rate and the top personal tax rate, (and also now since 1st April, the trustee tax rate). This has helped the development of what are called Cash PIEs, which are largely invested in term deposits/money markets. If the funds had been directly invested in term deposits held with banks, the interest would be taxed normally up to 39%. But because they’re in PIEs, that’s capped at 28%.

Inland Revenue has increasing concerns about this mismatch between the corporate income tax rate of 28% and the top marginal rate of 39% and it tried unsuccessfully back in 2022 to introduce some measures around this issue. If it was going to make a start on addressing these issues, I think you could see a proposal to income of Cash PIEs taxed at 39%. The Government might even try to make all PIEs except KiwiSaver funds subject to ordinary tax rates. Such a move would be hugely controversial, but it would probably also raise a fair bit of cash as well.

Anyway, we’ll find out on Thursday. As usual, I’ll be in the lock up and you’ll be able to hear our view on this year’s Budget just after 2PM.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

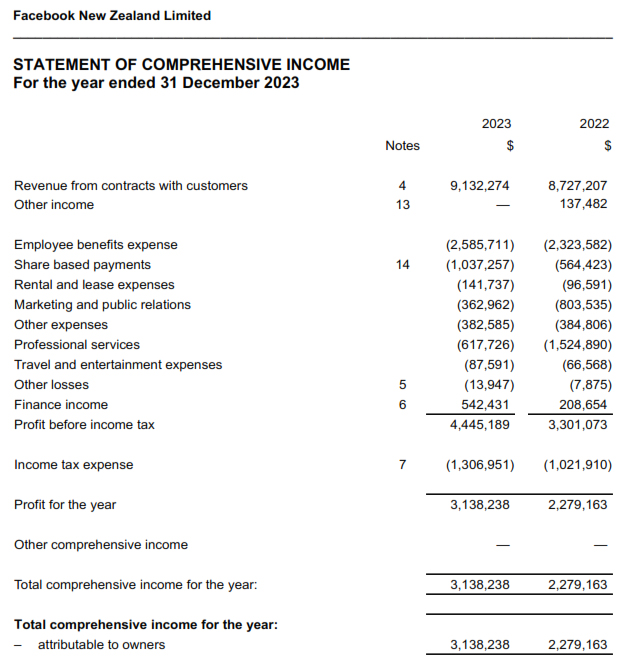

Facebook New Zealand’s 2023 results show the scale of the advertising revenue going offshore.

Treasury’s blunt warning ahead of the Coalition Government’s December Mini-Budget.

The Australian budget was announced last Tuesday evening and although comparisons with Australia are not always constructive, there are several points of interest, not just in terms of how the tax systems operate, but also about initiatives which could replicated here.

The Treasurer is predicting a surplus for the period to June 2025, but after that, apparently things get a bit tougher. A little bit like Aotearoa-New Zealand in that regard. The key point with an election coming up, is the “Stage Three” tax cuts take effect from 1 July. As is well known and has been the subject of some commentary over time, Australia has a tax-free threshold of A$18,200. That threshold isn’t changing, but what is happening is that the tax rate for the next bracket between $18,200 and $45,000 is dropping from 19% to 16%. The big change is in the next tax bracket where the rate drops from 32.5% to 30% for income from A$45,000 all the way up to A$135,000 Australian. Quite apart from the rate change the bracket has been extended from A$120,000 to A$135,000. The 37% bracket remains in place and applies for income between A$135,000 and A$190,000. Over $190,000 the top rate of 45% kicks in.

We had record migration last year and a lot of those people are heading to Australia and no doubt these tax measures will make it more attractive. I’m in the camp that you can’t ever compete on tax cuts because there’s always someone better able to reduce tax rates further. Right now that’s Australia.

One of the interesting comments I’ve heard about the Australian budget, is that the Australian Treasury forecasts, are frequently incorrect sometimes resulting in unexpected surpluses. Apparently, the Australian Treasury consistently under-estimates forecast inflation and the iron ore price, which since Australia is such a huge minerals exporter, is quite critical. Generally, the Australian economy tends to perform better than Australian Treasury predictions.

Another strong Australian corporate tax result

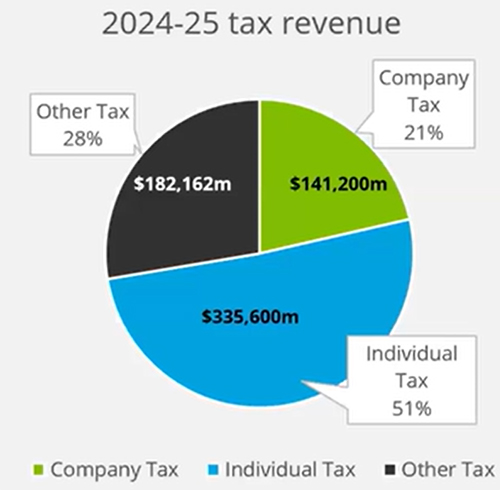

Furthermore, as the Australian economy is performing so well, the Australian company tax take is now a significant proportion of the total tax revenue. For the coming year to June 2025 it’s predicted to be A$141.2. billion or just over 21%.

(Deloitte Australia)

That’s a substantial sum by world standards. For comparison, in the UK (a near comparatively sized economy) the proportion of the tax take that comes from companies is usually between 7% and 10%. We are also a country with a fairly high corporate tax take. In the year to June 2023, it was 16.1% of total tax revenue. However, one of the reasons the Government’s books are deteriorating is the decline in the company tax take which is expected to fall to 15.6% of the total tax revenue this year.

Australian cost of living initiatives

There were also a number of other direct cost of living initiatives, including a $300 energy bill rebate to all Australian households. Eligible small businesses will get a $325 rebate during the coming year to June 2025. The Australian Government will also provide A$1.9 billion Australian over five years to increase the Commonwealth Rent Assistance maximum rates by 10%. (This would appear to be the Australian equivalent of the Accommodation Supplement).

Over here we don’t know whether the Budget in two weeks’ time will contain specific cost of living responses similar to these Australian initiatives but that appears highly unlikely. Based on what we’ve heard so far, the Government is relying on the individual tax threshold adjustments to sort of deliver cost of living relief.

Beefing up the ATO

Australia has a capital gains tax and some changes are proposed around the application of capital gains tax to non-residents. These are intended to ensure from 1 July 2025 that foreign residents are caught within the rules in relation to disposals of land. That’s something people tend to forget, that non-residents are taxable on disposals of Australian property and these proposed rules are intended to strengthen that compliance.

Another thing of note, which I think we will see something similar in our budget, is increased funding for various Australian Tax Office (the ATO) compliance programmes. The ATO has currently got three such programmes on the go, covering personal income tax, the shadow economy and tax avoidance (Tax Avoidance Taskforce). The Budget announced a new initiative countering fraud. In terms of dollar returns on these programmes, they range between four to one for the funding of the personal income tax down to a little two to one for the Tax Avoidance Taskforce.

Small businesses and ABUMS

The other thing that I think people would love to see here is the Instant Asset Write Off. This is where small businesses can purchase an asset up to $20,000 in value and claim an instant write off. This programme has been extended for another year. Apparently one of the reasons it has been extended is that the legislation which would have terminated that programme hasn’t yet been passed. Australian governments have a habit of announcing measures and then not getting around to passing the relevant legislation resulting in something with the delightful acronym ABUMS – Announced But Unacted Measures.

Overall, there was some interesting stuff in the Australian Budget including another measure I’m going to talk about next, which I also wonder whether we might see applied here.

Facebook’s results

Moving on, Facebook has now released its New Zealand financial statements for the year to 31 December 2023, and these are bound to generate some controversy. The official income reported for the year was $9.1 million and the profit before tax was $4.4 million, resulting in income tax of $1.3 million.

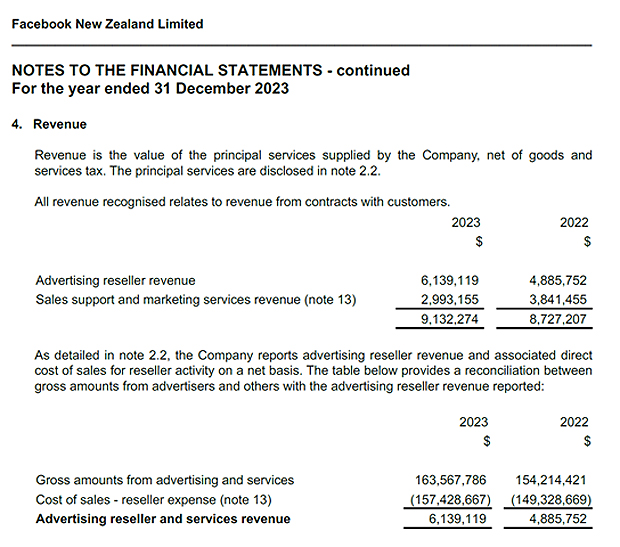

Like Google New Zealand details of the payments to related parties is the very interesting section to look at, together with the statement of cash flows because these give you a better clue of what the scale of Facebook’s activities within New Zealand are. Note 4 to the financial statements, which explains the revenue, sets out what is happening. “The company reports advertising reseller revenue and associated direct cost of sales for reseller activity on a net basis” This note explains that the gross amounts it received in the year to December 2023 from advertising and services was $163,567,786 and then a reseller expense was $157,428,667.

So, although Facebook is reporting income for income tax purposes of $9.1 million, the real scenario is that the revenue that’s passing through it, is substantially higher.

Another Australian example to follow?

Now it so happens there’s a case going through Australia at the moment involving what they call an embedded royalty. Basically the Australian Tax Office took a case against drinks company Coca-Cola in relation to what it perceived as an embedded royalty (and therefore subject to withholding tax) in payments for the right to brew Coca-Cola in Australia.

The Australian budget has a number of what’s termed Intangibles Integrity Measures. One of those it appears is a new provision, effective from 1 July 2026, where it applies a penalty to taxpayers who are part of a group with more than $1 billion in global turnover annually, that are found to have mischaracterised or undervalued royalty payments to which royalty withholding tax would otherwise fly.

Now that’s two years away from implementation, but it’s clearly a shot across the bow of companies such as Facebook or Meta, and Alphabet, the owner of Google, about these reseller services expense. So that’s something to watch how this develops.

And I just wonder whether we might see something similar here, because significant sums of money coming from advertising, are going overseas, and, as I’ve mentioned before, that has had a detrimental impact on our media landscape that it’s basically been starved of cash as a consequence. So, watch this space.

Treasury’s warning on structural reform

Finally, this week there was a budget information release from Treasury of papers relating to the Government’s mini budget in December. And one of the papers titled Implementing the fiscal strategy has attracted quite a great bit of interest.

In the paper Treasury sets out in fairly blunt terms that there is a requirement or need for structural reform of the tax system. The key paragraphs are 24,25 and 26. Paragraph 24 notes

“Structural reform of the tax system is the most effective way to ensure it is flexible and capable of raising additional revenue sustainably… Such reform would need to recognise that while revenue raising is the primary purpose of the tax system, its distributional and economic objectives are also important.”

Plenty of wry smiles here for those who listened to the Titans of Tax expand on this very point.

The problem with fiscal drag

Paragraph 25 then discusses the importance of fiscal drag

“Since 2010, fiscal drag…has played an important role in enabling successive governments to use the tax system to meet their revenue objectives. This has placed increased pressure on the tax system’s other objectives. If you wish to offset or end fiscal drag, through adjustment of personal income tax rates and thresholds the fiscal headroom which needs to be created will further increase”.

In other words, if you want to end fiscal drag, you really do need to rebalance and reshape the tax system,

I’ve seen some commentary that this was blunter advice than was provided to the previous government. I don’t actually subscribe to that view because in my view Treasury’s 2021 long-term fiscal insights briefing He Tirohanga Mokopuna was pretty clear that a fiscal crunch was coming. I just think that because there’s been a change in government, what Treasury has done here is taken the rather softly, softly approach in He Tirohanga Mokopuna and just made it very blunt so the new Government knows from the offset that there are challenges ahead. And to be fair to Finance Minister Nicola Willis and the Prime Minister, they have not denied that. But what they propose to do about it, of course, we’ll have to wait and see.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

And I reflect on 40 years in tax – what’s changed or not changed.

The Finance Minister Nicola Willis made the first of what is going to be a series of pre-Budget speeches to the Hutt Valley Chamber of Commerce, and in it she dropped a few clues as to the likely contents of the Budget.

In particular, she announced that the Budget’s “tax relief package will increase the take home pay of 83% of New Zealanders over the age of 15 and 94% of households.”

In case you’re wondering who is in the unlucky 17%, these are taxpayers with annual income currently below $14,000 or with no income at all. They therefore would not benefit from any increase in tax thresholds. According to Inland Revenue in the year to March 2022, there were over 800,000 taxpayers whose income is been between $1.00 and $14,000. There were another 210,000 or so who had no income at all during the 2022 tax year.

14 long years?

In her speech Nicola Willis noted that New Zealanders have not seen any changes to personal income tax rates and thresholds for 14 years. “Unlike most developed countries, New Zealand has made no adjustments to tax brackets to compensate for rampant inflation.” However, having highlighted this point, there wasn’t a commitment in her speech to regular indexation of thresholds, which is how we got 14 years without changes. I’ll have more commentary on that a little later.

The Finance Minister talked about “tax relief aimed at middle and lower-income workers” which is interesting because it hints that maybe threshold adjustments might be focused most on those earning below $70,000. The threshold which I think is most problematic, and Geof Nightingale, Sir Rob McLeod and Robin Oliver all agreed with this, is at $48,000 where the tax rate goes from 17.5% to 30%. There doesn’t appear to be any plans to adjust the tax rates there, but whether there is a bigger proportional increase around that threshold relative to the other thresholds, we’ll have to wait and see. We know by the way that the $180,0000 threshold at which the 39% tax rate kicks in is not likely to be increased.

The OECD joins the call for a capital gains tax

The Finance Minister’s speech came hot on the heels of the latest Organisation for Economic Cooperation and Development (OECD) Economic Survey on New Zealand, released on Monday. The big headline here from a tax perspective that the OECD joined the IMF in recommending a capital gains tax. What was interesting here is that when the IMF made this suggestion, Nicola Willis, dismissed it with a snippy comment following in the footsteps of her predecessor Sir Michael Cullen. This time around, there was no such snippy dismissal.

The report actually is quite sobering reading, not just around the tax side of it, but just generally about what it has to say about certain aspects of the New Zealand economy. Education was specifically mentioned as a point where attention needs to be focused on improving standards and therefore flowing through to greater productivity across the economy.

The OECD agreed with the Government’s proposed fiscal approach trying to squeeze spending and keep it under control. It had some criticisms about how budget operating allowances have been allowed to increase in recent years without any real explanation.

The OECD supports the broad-base, low rate approach, a capital gains tax, and tax reliefs for pension saving

But it also made the point that “any tax cuts should be fully funded by offsetting revenue or expenditure measures”, before going on to add “raising revenues should first be achieved through broadening the tax base and reducing distortions before raising rates of existing taxes.” That very much endorses the broad-base, low-rate approach Sir Rob MacLeod in particular espoused in a recent podcast.

No surprises there, but the report continues:

“There is a need to reduce distortions to household choice of asset allocation. Shares, land and owner-occupied residential property are tax favoured. Most capital gains from shares, owner-occupied residential property and land are not taxed. To ensure the tax system is not overly distorting, saving and supporting broader growth, capital gains taxation reform should be done as part of a wider review of tax settings for saving. New Zealand’s tax settings remain an outlier in some respects in international comparison, and notably in offering no tax deduction for contributions and in taxing the returns pensions funds earned while they’re invested and prior to withdrawal at progressive rates, this likely distorts saving away from private pension saving.”

Robin Oliver made the point about over-investment in housing, but as mentioned last week Dr Andrew Coleman picked up on how our taxations of savings is unusual by world standards,

There’s a lot to digest in this 150-page report which is only available online. It’s probably no surprise that expanding the capital gains tax base is not likely to be very high on the agenda of the Coalition Government at the moment. But there’s plenty of food for thought in the report.

One of the other points of interest, and there has been some commentary about this, is the suggestion for an Independent Fiscal Institution, basically, a policy costing unit. The OECD picked up that there had been no independent costings of policies in the run up to last year’s election. This is something that could be done by an Independent Fiscal Institution. Some work was done on this under the last government and Nicola Willis seems open to revisiting the issue.

Following the Irish example?

The OECD survey suggested the Irish Fiscal Advisory Council (IFAC) https://www.fiscalcouncil.ie/as a model that could could be followed. Given Ireland has a similar population this seems a good idea. Personally, I think we ought to look very closely at countries of comparable size to ourselves. The IFAC has been mandated to independently assess the government’s fiscal stance and budgetary forecasts and monitor compliance with budgetary rules. As I mentioned earlier the OECD thinks that we need to review our budget rules.

According to the OECD survey about 80% of OECD have some form of Independent Fiscal Institution. The Congressional Budget Office in the United States which has 270 staff is a very well-known example. Over in Australia, the Parliamentary Budget Office, with 45 staff has this role. The Canadians have a similar Parliamentary Budget Office and over in the UK they have the Office for Budget Responsibility. There’s plenty of examples around the world to consider and it would be encouraging if we heard something in the Budget about this.

Small businesses and statistics

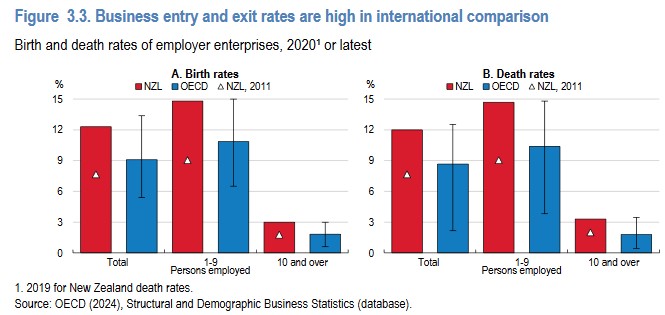

The OECD survey, noted that the business entry and exit rates are higher in international comparison although this means “business dynamism is vibrant” the OECE also noted that the “high share of the population working in micro, small and medium enterprises…hints at a difficulty for these firms to grow into larger businesses.”

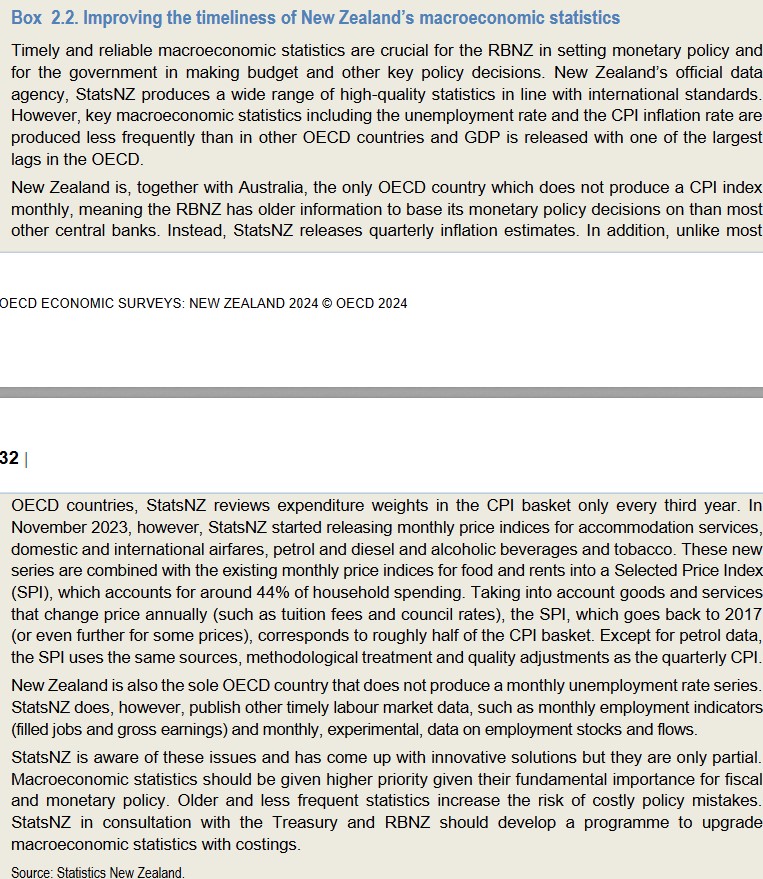

One other thing I thought was very interesting was commentary around improving the timeliness of New Zealand’s macroeconomic statistics. I’ve long thought it was a weakness that we don’t see monthly GDP or inflation data, but I wasn’t aware we were, like Australia, very much in the minority within the OECD in not producing a monthly CPI index. As the OECD noted “Older and less frequent statistics increase the risk of costly policy mistakes”. I wonder what the OECD would have made of the news that all Stats NZ staff were offered voluntary redundancy?

Don’t look back in anger? Forty years in tax

This week, it is 40 years since I started working in tax. They say the past is a different country, we did things differently there and that’s true, but one thing that hasn’t changed over my time in the past 40 years is the behavioural impact of tax. When I started working in the UK, the top rate of income tax was 60% and I saw people very incentivised to make sure that they’re claiming all the possible deductions, maximising pension deductions and the like. The top rate in the UK now is 45%, but you still see the same behavioural impact.

For comparison in 1984 the top rate in New Zealand was officially 60% but a further 10% surcharge had been introduced in 1982 by Sir Robert Muldoon, the Prime Minister and Finance Minister at the time. The top rate was therefore 66% which applied to income above $64,000. Based on CPI since then that’s the equivalent of roughly $260,000 now. According to the Inland Revenue date for the March 2022 income year, just over 42,400 taxpayers earned more than $260,000. That’s a little bit under 1% of all taxpayers. But they had a substantial amount of income between them, close to $20 billion and therefore paid a sizeable amount of tax nearly $7 billion in total.

The effects of forty years of inflation – how New Zealand taxpayers appear to have lost out compared to their UK counterparts

In terms of inflation, it’s quite interesting to look back at the tax rates and the income bands which applied. In 1984 the lowest rate was 20% on the first $6,000 of income. That $6,000 in 1984 dollars would now be $24,350 so in terms of inflation adjustments, even when we see the current 10.5% tax threshold move from $14,000 to maybe $16,000 in the Budget you can see that maybe New Zealanders have been losing out. Consequently, because we aren’t adjusting thresholds regularly, fiscal drag means that inflation has affected the ordinary working New Zealanders quite substantially.

That becomes clearer when you swap notes with what’s gone on in the UK with the tax thresholds there over the same period. The UK has a tax-free personal allowance which Was £2,005 back in 1984 when I started working. It’s now £12,570, but if it had just kept in place in place with inflation, it would be only £6,300. In other words, the value of the tax-free personal allowance has doubled in the past 40 years.

Interestingly, the tax threshold after which the higher tax rates kick in was £15,400 back in 1984. Inflation adjusted that would £48,300 compared with the £50,000 where it actually takes effect. There is an additional rate of 45% in the UK on income over £100,000. Back in 1984 the highest 60% tax rate kicked in at £38,100 inflation adjusted that would be £120,000 now.

What you see looking at these numbers is broadly speaking average earners in the UK have been less affected by fiscal drag and inflation than New Zealand workers have been. And that is something that I think I’d like to see changed here for the better and we should be having regular inflationary adjustments as is required by the UK tax law. I think such a move would tie into the better fiscal discipline suggested by the OECD.

The behavioural impact of no capital gains tax

I’ve now worked for over 30 years in New Zealand, but I still remember my shock when I realised there wasn’t a general capital gains tax here. When I consider the behavioural impact of taxation, that’s where you see it apply most where people will be looking to turn something that could be taxable at 39% into a non-taxable gain. And so, there’s a distortionary effect there.

And just to circle back to discussions we’ve had previously on the podcast and what the OECD have just said, there is a tremendous amount of value in the broad-based low-rate approach. It’s not perfect, but one of the things it does deal with is this question of behavioural impact and distorting behaviour chasing tax benefits. My personal view is the absence of a general capital gains tax has had an effect on our productivity. If it’s better in investment returns to invest in residential property in which the returns are largely tax free, than investing in a business or in shares that are taxed, such as overseas shares under the Foreign Investment Fund regime, then that diverts investment into less productive assets. Whether that’s for the benefit of the wider economy as a whole, well, that is a matter for ongoing debate. My view is it’s not.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A quiet week in the tax world – but is this the calm before the storm of this year’s Budget?

The latest OECD report on taxing wages shows the tax wedge rising in most countries including New Zealand.

It’s been a quiet week in the tax world, which, to be honest, is quite welcome. But there’s also a growing sense of a calm before the storm, that being the Coalition government’s first Budget on 30th May, I’ll offer up some speculation as to what I think will be in the budget closer to the time, but one thing we do know will be expected to happen, is adjustments to the flat tax thresholds, which as listeners will well be aware of, have not actually been adjusted since October 2010.

It so happened last week the Organisation for Economic Cooperation and Development (the OECD) released Taxing Wages 2024, its annual Taxing Wages report. This is a fascinating document which looks across the composition of wages and provides details of taxes paid on wages. This year, it’s also focusing on fiscal incentives for second earners in the OECD and how tax policy might contribute to gender outcome gaps and labour out market outcomes. It’s a big report which runs to 679 pages and is only available online.

Taxes are increasing thanks to inflation

One of the things that comes out of the Executive Summary was that in the words of the report tax systems in the OECD are not fully adjusting to inflation. Consequently,

“The average tax wedge for all eight household types covered in this report increased in the majority of countries between 2022. And 2023 driven in most cases by higher income tax. For the second consecutive year, more post tax incomes at the average wage level declined across the majority of all OECD countries now.”

The tax wedge is described as the difference between the labour costs to an employer and the corresponding net take home pay of the employee. It represents the sum of the total personal income tax and Social Security contributions paid by employees and employers. Less any cash benefits that the employee might receive.

New Zealand has consistently scored well in this measure because we don’t have Social Security taxes and we’ll talk a little bit more about that later. But notwithstanding that, the average take home wage for New Zealand employees has been declining over the past few years.

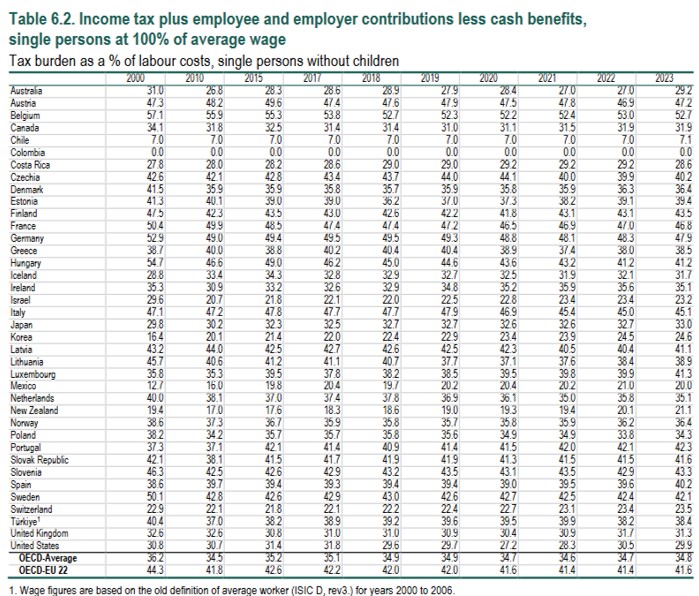

The report has an appendix showing the evolution of effective tax rates on labour since 2000 with a number of separate measurements based on single persons, single parents, or married couple with two children. It looks at what the tax wedge for each group is based on 67% of average wage, 100% of average wage and 167% of the average wage.

Now, whatever measure you take, you can see that the tax burden for New Zealand employees has been rising steadily since 2010, but you can see it start to accelerate in the last three to four years. So, for a single person at 167% of the average wage, their tax burden has gone from 23.9% in 2017 to 25.8% in 2024. Now you might think 2 percentage points isn’t much, but it becomes more noticeable as it accumulates over time. For a single person at 100% of the average wage the tax burden has gone from 18.3% to 21.1% over the same period.

This OECD report reinforces what we’ve been saying for some time that tax adjustments to the thresholds are long overdue. Now those who listened in to last week’s podcast with Sir Rob, Rob McLeod, Robin Oliver and Geof Nightingale will have noted pretty much everyone was of the view that the threshold where the 30% tax rate kicks in, that’s $48,000 was a major problem in our tax system. Geof was particularly insistent on this point. This OECD data reinforces that point. So, it will be interesting to see what moves are made in that space in the Budget at the end of the month.

Social security taxes – time for a rethink?

Moving on, thanks to everyone who’s commented or given feedback here and across the various social media platforms about last week’s podcast. It’s always great to have some engagement. I do read all the comments even if I don’t always respond.

There were some particularly interesting comments from Dr Andrew Coleman of the University of Otago about Social Security taxes and the absence of them in New Zealand. As he noted, New Zealand is an outlier in world terms in this respect.

Now, as I mentioned in the podcast, Social Security contributions were once quite a significant factor of the New Zealand tax system from the 1930s until the 1960s. But what happened over time was that the contributions weren’t hypothecated and applied only to Social Security payments, but in fact just became treated as part of taxation generally until in April 1964, the Social Security Fund was merged into the Consolidated Fund

Ultimately, the then Finance Minister Robert Muldoon decided in 1968 that separate Social Security contributions were no longer required and merged everything formally into income tax. Since then period, income tax has used to pay for Social Security such as welfare and superannuation.

That’s more than 50 years ago, but as Doctor Coleman pointed out many other countries have Social Security taxes. So, is that something we should consider in more detail? Well, I hope to explore that point in a separate podcast.

Sir Rob McLeod, Robin Oliver and Geof Nightingale on expanding the tax base

[In this part of the podcast I asked Sir Rob, Robin and Geof about the strains New Zealand’s Broad Base Low-Rate approach is experiencing and if a government wanted to raise how would it do so- through a wealth tax, capital gains tax, stamp duties or estate duties, whatever].

Sir Rob Mcleod (RM) Well, if I can kick off, I’m a huge fan of Broad Base Low-Rate (BBLR). I think it’s got a very simple thrust. It’s as much about pragmatism as it is about technical. I think we need to be careful in my experience with the debate and understanding that a Broad Base Low-Rate system is not one characterised by a myriad of taxes. Some people interpret a myriad of taxes as achieving breadth and therefore fitting with Broad Base Low-Rate. No, my definition of Broad Base Low-Rate is a few taxes with a broad reach. That’s where you get the simplicity. And the income tax and the GST covers most of GDP in the nation.

What does it not touch is the question to ask. You can talk about wealth tax and CGT, capital gains tax, but they’re actually part of the income tax. There’s an overlap between wealth tax, capital gains tax and the income tax. I don’t believe that that gap justifies the kind of emphasis that’s being given to wealth tax and CGT.

Sure, we’ve got some capital gains not taxed, most of them actually are taxed already in the system. The comprehensive capital gains tax I think in that sense is a bit of a misnomer because we do not have comprehensive taxation in the New Zealand system. And if you go and then put wealth taxes on, whether it be land or wealth in general, you are actually doubling up on the income tax. You’ve got an element of double tax in doing that and that takes us back to the starting point, that Broad Base Low-Rate is about identifying the gaps. And there’s bugger all gaps actually left by a broadly designed GST and income tax such as New Zealand has.

And when we go into the debates on specifics around the margins of that base, there are good reasons for arguing about why we shouldn’t have them. So that’s why I think BBLR is there. If you want to get more out of what we’ve got than the broad base of income tax and GST, you’ve got to justify it and you’ve got to start with what percentage of the GDP should be taxed in the first place. With balanced budgets, government spending equals taxation. With a balanced budget, which is kind of where the world wants to be these days.

So, I think recognise that the tax rate for the nation is government spending divided by GDP. And there’s a hell of a lot of benefit from there. So, if you want a tax cut, you’ve got to cut the government spending. It’s the only way to do it. Those various elements I think are very interconnected in the debate around Broad Base Low-Rates.

Geof Nightingale (GN) I think your question was where would you go to for another 1% of GDP? And I would agree with Rob that it feels to me that 30% of GDP or Government expenditure to GDP at roughly 30% has (that’s our long-run average, it spikes up and down for pandemics and earthquakes and recessions and things) that’s a constraint that I would be quite personally happy for our economy to operate against.

The question is then how you raise that revenue. And I totally support Broad Base Low-Rate. I think it’s effective in practise and 30 years of experience. I think the missing bit still there is our income tax is not as Broad Based as it should be, and I think we do need to extend it into further realised capital gains. So, whether you do that as a separate comprehensive capital gains tax like other countries, or you just change the definition of income, that’s a design feature.

Philosophically, it’s the same thing. It’s just how you get there. Taxing more income through realised capital gains, and then I would recycle that revenue into tax cuts, reductions, initially in the lower marginal rates because that’s where our problems come with high effective marginal tax rates in conjunction with welfare, which leads to productivity and incentives to work and all of that. So I would extend the taxation of capital, recycle the revenue and like Rob aim for 30% government expenditure over GDP.

TB Robin, you were part of the tax working group, you were one of the three dissenters in 2019. I that still your opinion?

Robin Oliver (RO) As Rob said and Geof echoed, it’s not a black and white issue. Do you tax capital gains or not? I mean, Michael Cullen kept on trying to make the point, talking about taxing capital income, not capital gains. Everybody ignored it, but he had a point that we do tax capital gains in certain cases and it’s all part of our income tax system and GST anyway. Are there holes in the system where you can efficiently raise more money at low cost? And the big hole, the gap in our system, it came out in the tax working group and all other reports is land.

We are a growing economy, growing population, land rises/increases systematically in value and that produces a lot of income and overall, we don’t tax it. You look at all the data, you know, higher wealth people, predominantly own land. Not all, but predominantly. So OK, should we be taxing land in one form or another? And I’ve got sympathy for that, but you’re going down to the workability. No government will ever tax home ownership. If it does, it will cease to be a government pretty quickly and someone sensible will come in and abolish that tax. So that’s a big hole in any land base. And then you’ve got issues about iwi and their relationship with land. You’ve got farmers.

We used to have a land tax. We had a comprehensive tax in the 1890s and we ended up with a tax just on Queen St commercial property. Everybody else got exemptions over time. I have some sympathy for taxing the increase in the value of land or land in some form which is not taxed now, but the housing, the home ownership stuff. You know, David Caygill, he proposed taxing homeowners. And he got told to back off.

I was working with him on capital gains tax proposal and we officials recommended including home ownership. And we were gobsmacked, totally bewildered when he accepted our recommendation. We expected him not to. And he went off to lose that next election, but probably not for that reason.

Workability matters. Home ownership is off the table. Our problem as a country is we take our savings, we invest it in land, we borrow from Australia, we invest in more land, bid up the price of land. We end up with the same amount of land as we began with – because that doesn’t increase – and heavily in debt to Australian banks. Solving that problem is not easy.

The problem with overinvestment in housing

TB Yes, it’s a behavioural impact. I had this conversation with an American client yesterday, who because of the fact they have to file U.S. tax returns, they’re subject to capital gains tax. But the FIF regime, he looked at that, and said, well, I can’t invest in stocks so I’m going to look at residential investment property here. That’s really a case of an unintended consequence of a tax.

On the family home, I fully grasp all of that, but is there an argument for saying that there is a limit? Because we build some of the biggest houses in the world. New Zealand houses – new houses, were until quite recently – are the third largest in the OECD. They were nearly getting on for close to 200 square metres.

RO We like our houses.

TB So could you say above two and a half million dollars or $5 million, the gain above that – some pro rata, we’re getting into technical details, but there is this thing that you’ve just espoused it perfectly, Robin. That at present we’re encouraged to invest in land and more land and borrow. So, there’s a loss of productivity, that 20% dead weight. There’s got to be a lot of lost productivity because capital is diverted into land rather than elsewhere.

RO The current group did look at something like that, although it was outside our terms of reference. We were not allowed to even consider the home or the land underneath the home or the sky above the. In terms of reference that we did look at that. The trouble is, a $2,000,000 house is not all that much in Auckland, as Michael Cullen kept on putting out, it was a hell of a lot in Whakatane.

TB There are 77,000 homes in Auckland worth more than $2,000,000, according to an OIA I got.

RO Probably one in Whakatane.

GN There’s a technical solution. If you were going to put all realised capital gains into the tax pot, you give every New Zealander a lifetime exemption, regardless of asset class or description, and that might be $5,000,000 or more, less but and that then shouldn’t distort behaviour. It’s arguably equitable and from a compliance and administration perspective, it would take probably 95% of us out of the of the loop.

RO And with that 95% of revenue.

GN Yes, well, maybe not because the assets are weighted towards the top. But anyway, the argument against that was always administrative. It’s very difficult to administer. But with current digitisation and things, I’m not sure those administration and compliance arguments – the integration of the land registers and share registers and things – as strong as it used to be. So, there are theoretical solutions there, but they’re hard to get to the public.

RO The idea of taxing the person with over $5 million has got a lot of appeal, but it’s not realistic. I always give the example of the idea you can freely tax all these very high wealth individual/ medium wealth individual people. Well, some of those are your medical specialists, your surgeon, your oncologist. And they can go to Australia.

You whack this $5,000,000 tax on their income over a lifetime and off they go to Sydney. So you’re sitting here in New Zealand, you’ve got cancer or something like that, and we’ve got a more equal society, but we have no treatment for cancer. Off to a hospice you go.

GN That might be the case with a wealth tax, but with an income tax I’m not convinced, Robin. I mean, Rob might be able to comment with direct experience of working in Australia. But labour and consumption taxes in Australia on high earners, medical professionals, they’re pretty tough compared to New Zealand. (TB 45% top rate plus 2% Medicare).I would have thought, but I don’t know what your experience is Rob.

RM it’s not just Australia, we’re becoming more global, aren’t we? So almost every country is a neighbour of one sort or another these days. The other thing is these people are incentivised to find these loopholes. And having lived, having operated and worked in Australia for six years, they’ve seen wealthy people find loopholes there too. So that that won’t go away.

TB It’s our job to find them, to be frank.

RM Yes.

RO The government legislates for them. You get tax free superannuation in Australia, or 15%. We’ve got to get away from this idea we can tax our wealth. Our problem is, as we’re next to Australia, is Australia becoming wealthier than we are. It’s attracting our nurses, our doctors, our policemen, our police persons and what have you through higher wages. We’ve got to increase our wage level and our productivity, and we don’t do that by sitting around and inventing new taxes.

TB But do we change the incidence of tax, so that capital gets diverted into more productive areas?

RO I give you the example of houses. I agree with that.

GN Our effective marginal tax rates, in those doctors, nurses and policemen, if you go across to Australia and look at those, yes, the incomes are definitely higher 30 or 40%. But I think there’s a tax dynamic in there as well for those people. Because we’re sweating our labour incomes, particularly in those low ends.

Robin has often said this, the worst tax rate we’ve got in New Zealand is the 30% rate at $48,000. Which is huge, it kicks in below the median income. So, I think there’s a tax dynamic in those migrations of doctors, nurses and police as well.

What about inheritance taxes?

TB The $48,000 threshold is a shocker. A final point on this housing. I think you’re right, politically a capital gains that incorporates the family home is impossible. You’re not even a one term government with that. But does that perhaps point to the need – and this is where the IMF come in – is that maybe that’s picked up through an inheritance tax at a separate point. Inheritance taxes, estate duty used to be quite significant. It was 5% of government revenue way back when in 1949, and they were one of the first taxes we introduced here. But they’ve declined over time around the world, but now there seems to be particularly with this, the wealthiest generation in history – and I think all of us are members of the Boomers – are starting to pass away, and there’s a huge transfer of wealth about to happen. And governments are looking at that.

RM Can I bring the conversation back to where I was about what percentage of GDP should tax be.

Because we are straight into, in essence, the tapestry of taxes. And what lurks underneath the motive for that conversation is really redistribution. Because a lot of the motive in the conversation that we’re having is about getting feathers off particular geese, and about certain thresholds and the rest of it.

The starting point ultimately is what does the country need by way of revenue as a percentage of GDP now? Now, if you’re arguing that actually New Zealand’s got a big problem of injustice or inequity because the rich are basically getting away with it, is a bit of a different to back from where we came from and earlier on in our conversation. Geof, to be fair, has identified redistribution as a goal. So he’s been consistent in that regard.

But I think this demonstrates why it’s so important to first of all ask yourself what you’re trying to do with your tax system, and if it is about revenue and getting a particular percentage of the GDP, then I think that these debates about estate duty and wealth tax and land tax are red herrings.

The 1% of GDP, for example, Geof, that you’ve mentioned in the question we’re asked to consider through a new tax, does not undermine my general principle of the broad reach and impact of GST and income tax. In fact, you guys (Robin and Geof) were both on the Cullen Review and you actually, in the report that came out, compared a 1% increase in GST with the capital gains tax and it kind of blew it away. That demonstrates my point that the Broad Base reach of GST and income tax can do everything that you’re trying to get out of these, peripheral and miscellaneous taxes. The only thing that’s left standing as to why you want to do it, is redistribution.

RO I’m OK with that, obviously. But getting on to death duties, estate duties, they have an interesting history. Other countries have them. People have different ideas about bequests and motivation. You know, how important it is to give money to the children. You’ve got Warren Buffett, who honestly gave each of his children 10 million and that’s it. Well, 10 million seems like a nice little nest egg, but in Warren Buffett’s terms, that’s just rounding. Bugger all in bequest terms, Other people will die for it. Literally, they will fight. It is enormously powerful. They will do anything to avoid death duties.

When we used to have them, that was the area of massive tax planning. It was the beginning of it all – avoiding death duties was a massive industry. And you think it’d be easy to do. Well, you’ve got to have gift duties as well, otherwise people just give it away to the kids. And you end up with Inland Revenue, as it used to do, roaring around, stamping every gift that’s made in the country, every Christmas and what have you, and determining they’re not subject to gift duty.

Massive amounts of bureaucracy involved. They are not easy taxes and I’ll just finish with the history of the end of death duties in New Zealand.

It started off with Australia. Death duties were limited to the state governments. When Queensland got rid of its death duties Victoria and New South Wales and the rest of Australia followed suit. We followed thereafter. Because anybody was going to go to the country which didn’t have it.

Death duties have got some appeal to people, I understand the issues. It’s very appealing when people don’t have any bequest, motive to actually tax a windfall gain. The only reason they are working, building their business is for the children and grandchildren. These people will react massively to its reintroduction.

[This is an edited part of the full podcast which readers are encouraged to download and listen to at the link at the top of this page.]

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.