Various Treasury Briefings to Incoming Ministers have been released in the past week including that for the incoming Finance Minister. The slide pack discussing the Economic and Fiscal Context has attracted some attention because it discussed the option of introducing more taxes on capital.

Prepared on 24th November, the Briefing sets out

“Treasury’s view on New Zealand’s economic and fiscal context, including some of the key policy issues you will likely grapple with. It’s intended to provide context for subsequent, more detailed conversations between you and the Treasury.”

The summary section has a really fascinating slide not just about this podcast’s focus, tax and the fiscal outlook for the country, but about the Treasury’s snapshot of the present state of the New Zealand economy and the challenges ahead. And the summary gets straight to the point, “a substantial fiscal consolidation is required to bring revenue and expenses back into balance and support fiscal sustainability.”

The Briefing discusses the state of the economy and how a clear economic and fiscal strategy will create a strong base for growth. Although fairly routine in some ways it’s very well worth a read.

Fiscal pressures are building…

But what has caught people’s eyes are references in the Briefing to the fiscal pressures that are building. Now I’ve talked about this previously, and in particular He Tirohanga Mokopuna the statement on the long-term fiscal position from 2021. Incidentally, the 2016 precursor of that 2021 statement heavily influenced the last Tax Working group in its decision to propose a capital gains tax.

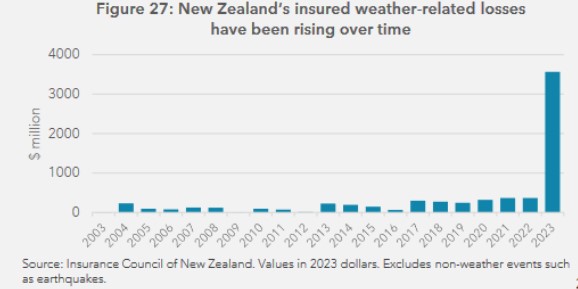

As the Briefing notes fiscal pressures are building. Gross New Zealand Superannuation costs have increased from 4.6% of GDP in 2011/12 to 5% of GDP in 2022/2023 and are forecast to rise to 5.4% in 2026/27. Then there’s the issue of weather-related events such as Cyclone Gabrielle which are increasing in intensity. The Briefing includes this really chilling quote

“In addition, New Zealand is exposed to a very high level of risk from its natural environment. Lloyds, the insurance marketplace, assesses New Zealand as having the second highest risk of annual losses in the world, behind Bangladesh and ahead of Japan.”

There’s also this interesting graph which shows the extent to which insurance claims have been increasing in recent years.

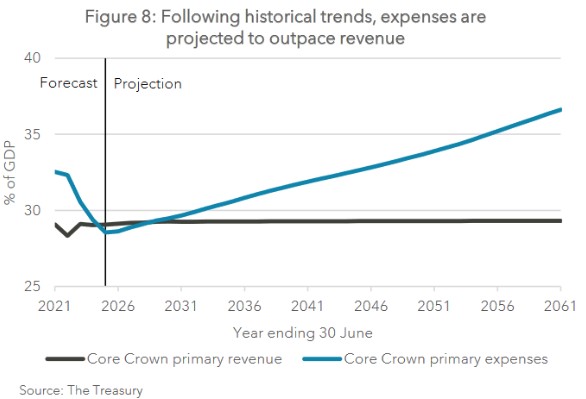

The Briefing references 2021’s He Tirohanga Mokopuna I just mentioned noting it

“…illustrated that at historic rates and policy settings, New Zealand’s core Crown expenditure will significantly outpace revenue over coming decades (Figure 8). The most significant spending pressures come from a combination of healthcare and NZ Superannuation.”

Core Crown expenditure was at a multi-decade high in response to the COVID pandemic, but is now outstripping the rise in revenue, even though core Crown tax revenue has been rising as a percentage of GDP since 2012/13. Treasury forecasts tax revenue will increase to 30% of GDP by 2026/27 on an unchanged policy. However, after stripping out one-off expenditures Treasury calculates the government is currently running a structural operating balance before gains and losses deficit of around 2% of GDP, which is roughly $8 billion.

But the Briefing notes the problem with tightening expenditure at this time in response to this structural deficit is the demographic change now occurring. This increases the fiscal pressure to deal with an ageing population, including increasing superannuation costs and demand for health services.

A heavy reliance on personal tax

Treasury notes one option would be to increase revenue at which point a government will need to consider a capital gains tax. Because as the Briefing comments “New Zealand relies more heavily on personal tax compared with most OECD countries”. The reason for this is that many other OECD countries have significant Social Security taxes, and they’re used to pay for the likes of New Zealand Superannuation. We don’t have that. We have a very clean system, but because we don’t have Social Security, we rely more on income tax and GST.

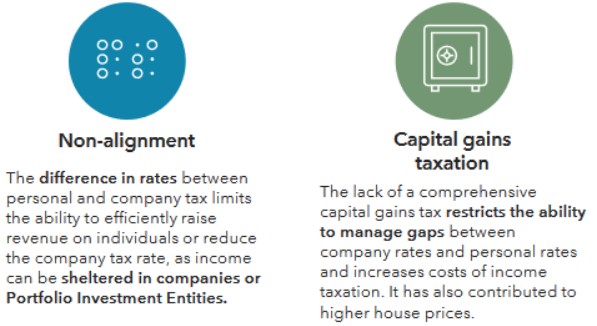

Constraints on the tax system – including the lack of a capital gains tax

On the state of the tax system Treasury’s Briefing comments

“However, there are constraints on our personal tax system which are creating increasing pressures and constraining our options for reform. These constraints arise due to the difference between our personal and company tax rates, and the lack of taxes on capital and capital gains. These limit options to raise revenue alter the mix of taxes or make changes that would meet distributional and economic objectives.”

The comment that the lack of capital gains taxation “has also contributed to higher house prices” will be disputed by some, but it’s interesting to see Treasury come out and say it.

Overall Treasury sums up that “At a high-level there are several options to support a return to surplus while delivering priorities” including:

“Increasing revenue through structural reforms of the tax system policy changes to increase revenue or letting fiscal drag continue to increase revenue raised through personal income tax.”

We’ve talked about fiscal drag ad nauseam and last week I referenced the draft report produced under the Tax Principles Act which showed how fiscal drag increases average tax rates over time. We think the Government is still committed to increasing the current income tax thresholds, whether they will index them regularly for inflation is another matter.

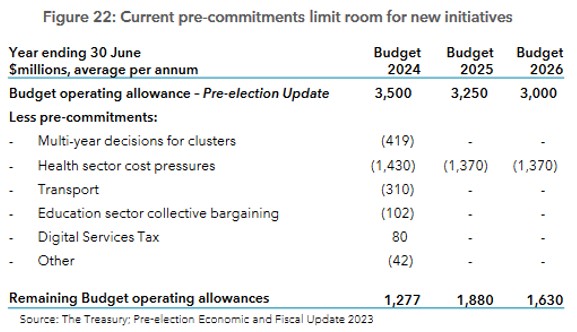

As always, these briefings contain a wealth of little detail. They’re fascinating, really, one little detail that hasn’t picked up by many was on page 19. This was discussing the Budget 2024 operating allowance, which was set at $3.5 billion. The Briefing discusses the existing pre-commitments and included in those pre-commits is revenue of $80 million from a Digital Services Tax.

This seems a little bit optimistic because I understood the DST wasn’t actually being introduced although it possibly reflects the effect of the expected changes in the international tax base. Either way it’s a little detail I was a bit surprised to see. However, $80 million in the context of $3.5 billion operating allowance and over $130 billion annual Government expenditure it’s a drop in the ocean. Still, it’s interesting to see it there.

Inland Revenue consultation on charities’ business income exemption

Mentioning tax working groups, I remember asking the late Sir Michael Cullen the chair of the last Tax Working Group whether there was anything that surprised him. He replied that it was the extent of the charitable sector what was going on there. This is something I see fairly frequently in comments on these transcripts, it seems to be a bit of a sore point that certain charities have a business income exemption (By the way, thank you to everyone who comments, I do read them even if I don’t always respond).

Inland Revenue have just released a 46-page consultation document on to what extent is business income a charitable entity derives exempt from tax. As has become the habit and it’s very welcome, it’s accompanied by a useful little five-page fact sheet on the matter.

The main business income exemption is in section CW 42 of the Income Tax Act 2007. There’s a related section CW 41 treating non-business income as exempt for charities.

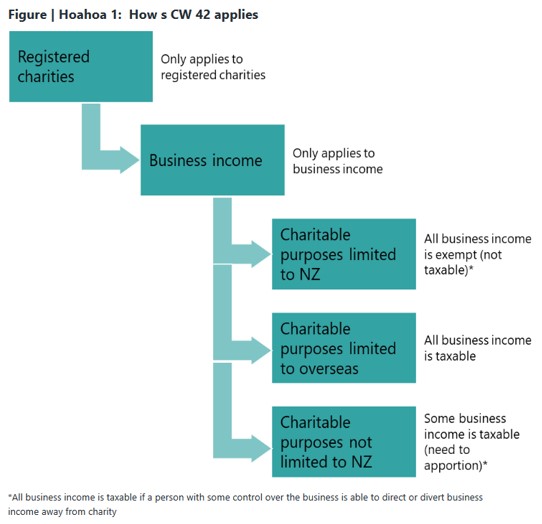

But this particular draft interpretation statement is consulting on what constitutes business income and to the extent to which it will be exempt. How the exemption applies is set out in a very handy flow chart produced in the in the fact sheet.

OK.

In summary, if the charity’s charitable purposes are limited to New Zealand, then all its business income is exempt. But if the charitable purposes are limited to overseas, then all business income is taxable. If it so happens that the charitable purposes aren’t limited to New Zealand, so charitable services are provided both in New Zealand and overseas, then there’s a need to apportion.

The interpretation statement runs through with some good examples what meets the criteria to be business income. It also considers how a charity would about apportioning between business and non-business income and services in and outside New Zealand. Much of this is relatively routine and it’s been standard practice for some time.

I think the thing that concerned the last tax working group, and which prompted the late Sir Michael Cullen’s comment is that there isn’t necessarily a follow through on whether a charity which may meet all these criteria is actually applying its spending to the community. A charity may have an exemption; therefore, they’re not paying income tax. Excellent. But are they applying funds for charitable purposes? If so that’s all well and good. That’s what we want to see. But what if that’s not happening? This is when issues arise about charitable exemptions when the funds are being accumulated and not distributed. That’s a whole topic for another time.

CSI Inland Revenue?

And finally, a little story just came out this week regarding Gordon Kenneth Morris, a Waikato sharemilker, who fraudulently claimed COVID support money which he then spent on online gambling. After he was caught, he was sentenced to nine months home detention.

What happened was he submitted fraudulent applications for the Small Business Cashflow Scheme and also for Resurgence Support Payments. He received a total of $27,200 from the Small Business Cashflow Scheme. But his application for $8,800 in Resurgence Support Payments was declined.

When Inland Revenue investigated it found Morris had also filed false GST and income tax returns and in the period between 1st April 2018 and 20th October 2020, he and his wife had spent over $336,000 on online casinos.

It’s a bit of a tragic case, but it’s also a good introduction for my guest next week, Tracy Lloyd from Inland Revenue, who is Service Leader Compliance Strategy and Innovation. We will be discussing how Inland Revenue detects fraudsters such as Mr Morris.

That’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue guidance on the new 39% trustee rate

Briefing the Minister

Tax credits or threshold adjustments?

The Finance Minister signed off 2023 rather like a Shortland Street season finale, leaving us all guessing as to the exact extent of the proposed tax cut package and when it might apply. We were told at the Half Year Economic Fiscal Update Mini-Budget on 20th December we could expect more details shortly. But now it’s February and we’re no wiser. It now appears likely we’ll have to wait until the Budget in May for full details.

A 39% trustee tax rate?

On the other hand, the business of government carries on and we will know early next month whether the coalition government will proceed with increasing the trustee tax rate to 39%. That’s when the Finance and Expenditure Committee reports back on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the annual tax bill currently before Parliament which proposed the increase to 39%. It must be passed by 31st March.

The FEC heard oral submissions last week, and I note that (previous podcast guest) John Cantin thinks it’s most likely that the tax rate will go ahead. This is even though such evidence as we’ve seen suggests that a 39% tax rate for trusts probably represents over taxation of many trusts once the wider family context is considered.

I tend to agree with John that the rate increase will go ahead, in part because it is a base protection measure as it aligns the trustee rate with the top individual tax rate. But also, the Government will probably be grateful for some additional revenue to counterbalance the lost revenue from the proposed tax threshold adjustments. That said, I know a number of submissions proposed that some sort of de minimis threshold is introduced, and the rate of 39% will only apply on the excess.

Inland Revenue’s view on tax planning for the new 39% rate

Meantime, and rather helpfully, Inland Revenue released last Friday some high-level guidance about how it might perceive taxpayer transactions and structural changes ahead of a rate change. General Article GA 24/01 proposed increase in the trustee tax rate to 39% has been released in response to requests since the rate was proposed for guidance on how Inland Revenue might perceive some transactions.

GA 24/01 contains several examples of possible transactions and how Inland Revenue would view the transaction. The first example is a company owned by a trust which changes its dividend paying policy. Inland Revenue considers a company is entitled to change its dividend paying policy and while taking into account the funding needs of shareholders and applicable tax rates, it “is unlikely without more (such as artificial or contrived features) to be tax avoidance.”

The example then notes Inland Revenue might have concerns if the company could pay a dividend by crediting shareholder current accounts, but “objectively has no real ability to pay those credit balances if it was to be liquidated.” In other words, the company tries to pay a dividend ahead of the trustee rate increase but doesn’t have the funds to pay the dividends in cash in full.

Another example is of a trustee choosing to wind up a trust. Again, GA 24/01 suggests such a step is “unlikely without more (such as artificial or contrived features) to be tax avoidance.” GA 24/01 also looks at the question of trustees investing in Portfolio Investment Entities instead of other available investment options. The advantage here is that the maximum rate applicable to Portfolio Investment Entities is 28% Again, Inland Revenue concludes such a step is unlikely without artificial or contrived features to be tax avoidance.

That said, Inland Revenue is going to continue to gather information on trusts and something it has said would be of concern to it is where income is allocated to a beneficiary taxed at a lower rate, and then instead of actually being paid out or being fully available to the beneficiary, is resettled back on the trust. In effect, the beneficiary has not benefited from the distribution.

The allocation of income to a beneficiary, where the beneficiary actually doesn’t know of an allocation or has no expectation of receiving the income together with replacing dividend income with loans “in an artificial manner”, are other alternatives which would concern Inland Revenue if there’s no real commercial reality behind the arrangement. And then artificially altering the timing, ie: bringing forward or deferring any taxable deductible payment, particularly it’s linked to existing contractual terms or practise for the date of payment.

These are just a number of scenarios which might play out. And clearly Inland Revenue’s watching. As I said, we really won’t know what the state of play will be until early next month when the FEC reports back, and when it does, we’ll let you know. But as I said, the expectation I have is we should see that tax rate increase.

The Tax Principles Act may be gone but its first draft report lives on

Moving on, one of the first things the coalition government did was repeal the controversial Tax Principles Act. Nevertheless, the draft report that was due to be produced under the Tax Principles Act has been proactively released and it makes for some interesting reading.

The report gives a background as to why it’s being prepared, its reporting obligations, and it explains what are the tax principles that were measured. These were included in the Act – efficiency, horizontal equity, vertical equity, revenue integrity, compliance and administration costs, flexibility and adaptability and certainty and predictability. Incidentally, a lack of certainty and predictability was one of the objections that was made about the Tax Principles Act because didn’t go through the full generic tax policy process.

Inland Revenue was required to assess the principles, against four measurements:

Income distribution and income tax paid;

Distribution of exemptions from tax and of lower rates of taxation;

Perceptions of integrity of the tax system, and

Compliance with the law by taxpayers.

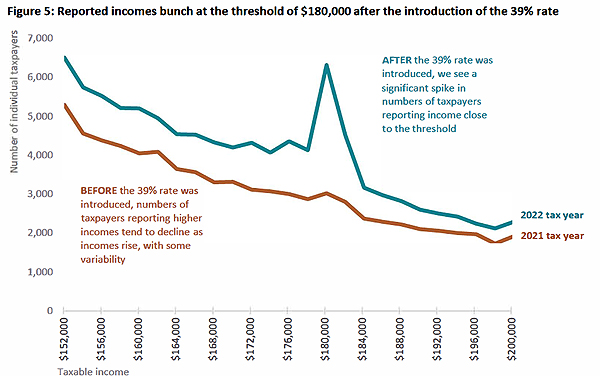

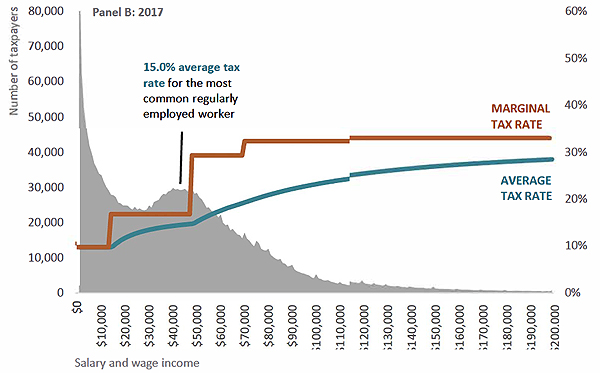

The report has lots of interesting graphs including the taxable income distribution for individuals for the 2022 tax year which shows a wee spike around the $180,000 mark.

I think that’s rather revealing even if there are apparently only 4,000 individuals involved. But still for those taxpayers you may need to have a good explanation of what’s going on.

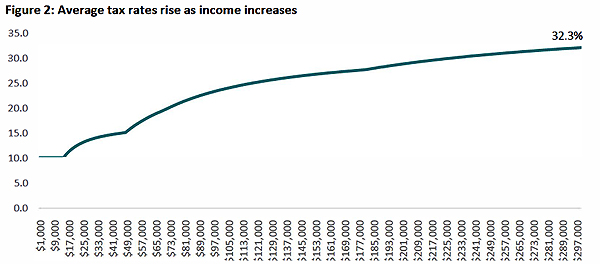

There’s a graph showing how average tax rates rise as income rises. This graph tops out at $300,000, by which point the average tax rate has risen to 32.3% for someone of that income.

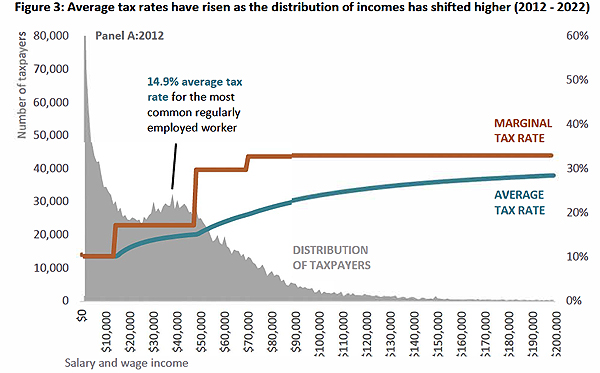

But what I thought was quite interesting were the graphs looking at the average tax rates from 2012 to 2022. In particular the graphs illustrated the effect of inflation combined with the non-adjustment of thresholds. That’s an issue I’ve talked about frequently and threshold adjustments we think will be at the core of the Government’s proposed tax relief package expected to be rolled out later this year.

The report notes between 2012 and 2017, the average tax rate for the most common regularly employed worker increased by 0.1 percentage points. Not too bad. But from 2017 to 2022 it increased by 1.2 percentage points. That’s quite a more significant example. Overall, in the period between 2012 and 2017 it rises from 14.9% to 15% and then rose between 2017 and 2022 to 16.2%.

This is the fiscal drag (or bracket creep) I discussed with Susan Edmunds of Stuff. It’s been an issue for quite some time. As wages rise faster, they drag persons on average incomes into a higher tax bracket. It will be interesting to see how the Government addresses it, and I’ll talk about that in a few minutes.

There’s plenty of other material to consider. There’s an interesting stat that the top decile of taxable income earners paid 44% of personal income tax. The report notes that the same group earned 33% of total income and suggests this is a better indicator of progressivity in the tax system than the fact that 44% of tax is paid by the top decile.

The arguments will rage around the progressivity and fairness, David Seymour of the Act Party for one has been talking about this area. Overall, there’s a lot to consider in the report. Interestingly, in the note to Cabinet regarding the repeal of the Tax Principles Act, the new Minister of Revenue Simon Watts suggested that much of this data could be made separately available, perhaps as part of Inland Revenue’s annual report. I hope we do see that, because for some time I’ve felt that the discussion around bracket creep, fiscal drag and thresholds has been sort of sidelined because governments have been not too keen to discuss it in great detail.

Briefing the Minister

Mentioning the new Minister of Revenue Simon Watts, another report released last Friday was the Briefing to the Incoming Minister. I think some of the data that’s been included in this draft report under the Tax Principles Act, would normally go into the Briefing for Incoming Minister.

What I found interesting in the Briefing was Inland Revenue’s discussion around where it’s at and the effect of the completion of the Business Transformation Programme which has allowed it to “deliver significant cost savings”. For example, the Briefing notes the amount of revenue collected for the year ended 30 June 2023 grew by 62.5% compared with the year ended 30 June 2016, the last full year before transformation began. Over the same period, the number of Inland Revenue full-time equivalents reduced by 29%.

There’s been a lot of talk about government cuts for the public sector, but I think the Briefing subtly, or not too subtly, you might say, raises a good question – if an organisation has managed to reduce its headcount by 29% and its funding is not tracked with inflation since 2017, which appears to be the measure for the basis of these public spending cuts, why would you add further cuts?

My view would be, and I think I wouldn’t be alone in thinking this amongst tax practitioners, is that Inland Revenue is under a bit of strain. We know it probably needs to boost its investigations efforts. So why it should be on the chopping block when it’s already done much of what any government would want it to do – more with less. But we’ll see how that plays out.

I thought the amount of commentary in the Briefing around the question of funding this point was quite interesting. It notes that for the year, to June 2024, the department gets about $800 million a year. And at October 31st 2023 its workforce was 4,231. Whereas back in June 2016 it was 5,662. And by the way, the report also notes the department has planned for taking a $13.9 million reduction for the year to June 2025, which was announced by the previous government in August 2023.

According to the Briefing funding would be running around about $700 million going forward, but then adds something the government should probably pay attention to.

“Our primary cost pressures in out years will be remuneration and inflationary cost pressures on technology as a service contracts, accommodation, leases and other operating costs. We are currently developing options for meeting these costs and we’ll report back to you on these matters.”

I know speaking as an employer and along with other colleagues, finding staff is difficult at the moment, so that puts pressure on salaries, obviously. And Inland Revenue is not immune to that because it needs to pay near market rates to attract good quality people, because as the gamekeeper, so to speak, it needs to match the poachers on the other side. Like so much in the year ahead it will be interesting to see how the Minister settles in and what happens with Inland Revenue’s funding.

The shape of things to come – tax credits or threshold adjustments?

And finally, coming back to what lies ahead, as I mentioned at the start, the Half Year Economic Forecast Update left us none the wiser as to the nature of the threshold adjustments, which we think are going to happen. In that gap. David Seymour of ACT has come forward and talked about the ACT policy, which is to simplify the tax rate structure down from the current five rates down to three, with a top rate of 33%. This is moving back to the rate structure which applied from 1989 through to 2008. Basically, until 1 April 2000 (when the 39% rate was introduced) there were two main rates with a tax credit adjustment for low-income earners.

David Seymour talked about tax credits similar to the existing Independent Earner Tax Credit. But as I told RNZ while the concept’s not uncommon, there’s still the issue we discussed earlier. What about adjustments for inflation and keeping the true value of that, otherwise lower rate/ lower income earners will face higher effective marginal tax rates.

There’s also a certain complexity with tax credits. The thing about applying thresholds across the board to everybody, it’s pretty straightforward. Whereas with tax credits, if there’s a claim process that’s involved, not everybody will claim that. It introduces a bit of complexity at the bottom end, which Inland Revenue’s Business Transformation was determined to do the opposite in order to try and make it as easier for most taxpayers to comply.

As mentioned, we have the independent earned tax credit, but it starts cutting out at $44,000 and then drops out at $48,000 once income crosses that threshold. We’ll have to wait to see what happens and in the meantime there will be plenty of debate ahead. We will bring all of those developments to you as usual.

In the meantime, that’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.