the capital gains tax problem for UK beneficiaries.

migrants now pay 38% of personal income tax.

Inland Revenue has released a paper for consultation under the dry title Proposed Legislative Changes for Intermediaries. This doesn’t sound terribly exciting for the general public, but it’s actually quite important, because it looks at the role of tax agents and other intermediaries.

The expanding role of tax intermediaries

This has not been a very heavily regulated area and understandably, there’s been quite a lot of changes in the dynamic over the past 30 years since the Tax Administration Act was passed in 1994. That act specifically referenced tax agents, but other intermediaries have popped up in this space, such as those dealing with PAYE and tax pooling companies.

The purpose of the paper is to recognise that all these intermediaries have a crucial role in the tax system. And part of it is to set out clear rules as to who can be a tax agent or tax intermediary and how they will be regulated. This is crucial as tax agents and other intermediaries are given access to vital information.

Why register with a tax agent?

Now, the main intermediaries discussed in the paper are tax agents. Currently, there are around 5,000 tax agents registered with Inland Revenue. If you’re registered with a tax agent, apart from them having direct access to your information provided by Inland Revenue, a taxpayer also gets what we call extension of time arrangements.

This usually means that if you’ve registered with a tax agent, then the due date for filing a 2026 tax return is extended from 7th July 2026 to 31st March 2027. (And yes, many tax agents will see clients coming in on the 30th or 31st of March 2027 asking for their 2026 tax returns to be done.)

And the other benefit, and arguably much more important, in terms of cash flow, is that you get an extra two months to pay your terminal tax. Generally, terminal tax payments for the 31st March 2026 tax year will usually be due on 7th February 2027. But if you have a tax agent, that’s extended until 7th April 2027.

In addition, tax agents can communicate directly with Inland Revenue on behalf of clients and as part of this are given access to taxpayers’ personal details. However, it’s presently pretty easy to become a tax agent. Currently, you can apply to be a tax agent if you have 10 or more clients for whom tax returns are required to be filed. Now in this paper, Inland Revenue acknowledged it had been a bit uneasy about that particular rule because it’s quite possible that a person may be able to find 10 family members or friends as clients and then apply to be a tax agent. Coupled with the ability to access sensitive information, the opportunity for a tax agent to commit fraud is obviously a risk

Christchurch’s Andy Dufresne

One of the more memorable cases of gaming the system involved Carl Peterson, a sort of lesser Andy Dufresne from The Shawshank Redemption. Way back in the early 2010s, Peterson was in Christchurch prison and began helping other inmates with filing their tax returns and obtaining legitimate tax refunds.

Peterson realised he was onto a good thing, so he successfully registered as a tax agent whilst still in prison. He went on to make fraudulent claims for non-existent taxpayers totalling $50,000. Anyway, it rebounded on him because, apparently, gang members within the prison found out and put him under pressure. Finally, these frauds were discovered, and he got another year added to the 11-year sentence he was then serving.

The point is that the system still remains loose around who could be a tax agent. Peterson was caught and sentenced in 2013, so Inland Revenue has obviously had some concerns for some time, but it’s now finally taking action.

Tightening the rules

The paper proposes a number of changes. There will be three new categories of intermediaries: digital services providers, data consumers and a category of bookkeepers. The Commissioner of Inland Revenue will be given more discretion to disallow someone from being a nominated personal tax intermediary. The current 10-client rule for becoming a tax agent or a bookkeeper will be replaced with a requirement to be a member of an approved professional body.

Currently Inland Revenue recognises some professional bodies as “Approved Advisor Groups” on the grounds that their members must:

have a significant function of giving advice on the operation and effect of tax laws

be subject to a professional code of conduct in giving the advice, and

be subject to a disciplinary process that enforces compliance with the code of conduct.

The organisations that currently have Approved Advisor Group status are:

Accountants and Tax Agents Institute of New Zealand

CPA Australia

Chartered Accountants Australia and New Zealand

Institute of Certified New Zealand Bookkeepers

New Zealand Qualified Bookkeepers Association.

The plan is that any future tax agents after the relevant legislation is passed should be a member of one of these groups. Although this initiative is mostly of administrative interest, aimed at improving the running of the tax system, it is one which should have benefits for the wider tax community.

Trusts and United Kingdom resident beneficiaries

An area in which I am increasingly involved, and ironically takes me back to my UK roots, is in relation to distributions made by New Zealand trusts to UK resident beneficiaries. A common theme is that these trusts were established for asset protection purposes 20 to 30 years ago when the settlors were in business. The settlors are now either retired or winding down their activity.

One of the things about New Zealand is that we have a very fluid population, with significant numbers moving emigrating, immigrating or returning from their OE. (More on that below.)

For many doing their OE, the assumption is they will return to New Zealand, but people decide to stay, change their plans etc. For example, I initially arrived here on holiday and basically never left. And the same happens to people who go to Australia or the UK. They meet someone or land an extremely good job, their career takes off and the next thing you know, they’ve been overseas for some time.

The great wealth transfer

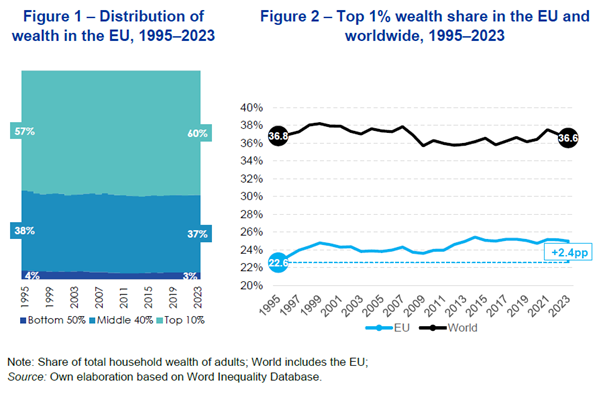

At the same time, we have the Baby Boomers and Generation X, the two richest generations in history, who are now starting to shuffle off this mortal coil. This means there’s a great transfer of wealth involving trillions of dollars happening. We referenced this in our last episode when discussing the EU and its paper on wealth taxes.

Obviously, with children and grandchildren overseas, grandparents and parents want to make distributions to those descendants. And this is where they hit a major hurdle, which is often exacerbated because New Zealand does not have a capital gains tax.

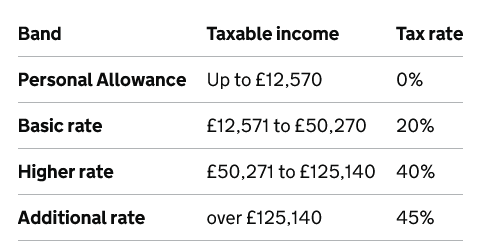

The UK would classify the typical New Zealand trust as a non-resident trust for UK tax purposes. Any distribution of income (as calculated for UK purposes) will be taxed at the beneficiary’s marginal tax rate (potentially 45%). This is relatively uncontroversial. Helpfully, distributions of accumulated income to other beneficiaries, including those not UK tax resident can be taken into account when determining what proportion of a distribution represents income for UK tax purposes.

UK income tax rates

It’s in relation to distributions of capital gains (as calculated for UK capital gains tax purposes) that matters get really problematic. Unlike distributions of income, the total historic gains of New Zealand discretionary trusts are taken into account when calculating what proportion of a distribution to UK resident beneficiaries is taxable.

Take for example, a New Zealand trust which has, since its settlement, realised one million dollars of (non-taxable) capital gains. These gains have been distributed in full to New Zealand resident beneficiaries.

The trustees now wish to make a distribution to the UK resident beneficiary. The hope is that with all the income and gains of the trust distributed to New Zealand resident beneficiaries, the distribution to the UK resident beneficiary would be tax free for UK tax purposes. Unfortunately for the UK beneficiary, that will not be the case.

Are those capital gains really tax free?

Firstly, the fact that the capital gains are tax-free for New Zealand is ignored. These were capital gains that would have been taxable in the UK. Furthermore, any capital gains that may have been distributed to any non-UK tax resident beneficiaries are ignored for UK tax purposes.

Consequently, any distribution of the trust’s million dollars of capital gains to the extent it wasn’t income that year would not be treated as tax-free capital, but as a distribution of capital gains, probably taxable at up to 24%.

This is an increasingly common scenario I’m encountering. In one case, the trust in question was settled in 1972. Just to compound matters, if the capital gains (for UK purposes) can’t be identified, the distribution will most likely be deemed to be income and therefore taxable at up to 45%.

This scenario should prompt the advisors for the baby boomer generation in particular, who have reached retirement age, to think carefully about the role of the family trust for them. In particular, what they want to do about overseas-based beneficiaries. Because in essence, they could be passing tax liabilities down the line.

Beware the “hotchpot clause”

Now you might say, well, that’s the overseas beneficiaries’ problem. They’ve made their bed; they lie in it. One Jersey court has basically said the same thing. But there may be some issues if the trust deed includes a “Hotchpot clause”, which basically tries to equalise things between beneficiaries. In this case the overseas beneficiaries’ tax bill becomes a big problem for the trustees.

It’s an issue for careful consideration. But it’s also an example of the golden rule – if there’s a cross-border transaction (and the size of the transaction doesn’t really matter), you need to seek advice. It’s likely you’re probably walking into a minefield either for the trustees or for the beneficiary.

Immigration and tax

The issue of immigration has hit the headlines after ACT proposed some tougher restrictions around migrants, including a $6 per day infrastructure charge for migrants who come in on short-term work visas. One of the things that stands out about New Zealand is the extraordinarily high proportion of the population who, like myself, were born overseas. According to the 2023 Census for the whole country it’s 28.8% and a quite astonishing 42.9% in Auckland where I’m based.

Now we immigrants are an increasingly important part of the economy not least because we pay a lot of tax. Just how much in proportion to our population base is something that hasn’t been generally considered until Treasury prepared a couple of Analytical Notes as part of its 2025 Long-term Fiscal Statement He Tirohanga Mokopuna. The first Analytical Note, AN 25/10 Transnationalism over the Life Course of New Zealand Birth Citizens, was published last October. The second Analytical Note AN 26/02 Transnationalism and tax payments among the foreign-born, was released in late March. This is an extremely interesting paper which examines the tax paid on personal income, primarily through PAYE.

“Foreign-born people increasingly pay more tax than their population share would suggest”

Analytical Note 26/02 reveals how the income tax paid by foreign-born persons has risen faster than their population share. In 2000 foreign-born people represented 24% of the population which matched their share of individual income tax on market income. However, by the tax year ending March 2024, the foreign-born made up 32% of the population but now paid 38% of the tax.

As the Executive Summary noted “The central finding of this paper is the simplest. In aggregate, the foreign-born are becoming increasingly important for the country’s tax base.”

This conclusion should perhaps give all the politicians happy to raise immigration for short-term electoral gains pause for thought. They might well be literally biting the hand that feeds some of their would-be voters.

The two Analytical Notes are worth reading for their insights into our economy and should be part of any reasoned debate about migration and a long-term population strategy. I’m not confident we will see such a debate during this year’s Election campaign.

On that note, that’s it for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and any requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Monday 4th May – it has been edited for brevity and clarity]

This year we have regularly discussed Inland Revenue’s increased activities in the crypto asset investor space including the introduction of the Crypto-Asset Reporting Framework (CARF). In our view Inland Revenue is increasingly aggressive with its activities in this space.

$36 billion and counting

The latest demonstration of this focus is a media release “reminding investors of crypto-assets that they need to get tax compliant now, so they don’t end up with an expensive surprise down the line.”

The media release includes several interesting stats which reveals why Inland Revenue is paying so much attention to this area. According to Inland Revenue it “has identified 355,000 unique crypto-asset users in New Zealand undertaking around 57 million transactions with a value of $36 billion.”

Now, all those numbers are very surprising. Inland Revenue doesn’t specify the period involved, but the fact that there’s 355,000 crypto investors, basically one in fifteen of the population, is something that probably surprises a lot of people. The volume of transactions is again fairly extensive, but the sheer value is quite extraordinary.

Naturally Inland Revenue, particularly with the government finances under pressure, will be very keen to make sure all these investors are following the rules correctly. We’re therefore seeing some fairly aggressive enquires, and there are a number of significant crypto related cases we know are before the courts which, by Inland Revenue’s own account, involve tens of millions of dollars.

You are not invisible…

This bulletin sets out Inland Revenue’s approach. It reminds people that CARF is now in force and Inland Revenue will match information received from CARF to tax returns and follow up on any discrepancies. The bulletin also observes

“…despite popular thinking, people are not invisible on the blockchain, and we have the tools and the analytical capabilities to identify and expose crypto asset activities.”

Reinforcing a development I reported recently, the bulletin continues:

“A first batch of letters has now been sent to people who would normally have their tax assessed automatically and who Inland Revenue knows have traded on one or more crypto asset exchanges.”

This is highly unusual. As people may be aware Inland Revenue is about to start its annual automatic assessment process, which between now and the end of June will process the year-end tax for over two million taxpayers churning out refunds or assessments of unpaid tax.

What this letter is pointing out is, that many people who are crypto asset investors are also salary earners subject to PAYE and therefore normally do not have any reporting obligations and they might think they’ve slipped through the cracks. This letter makes it clear to such persons that the auto assessment process will not apply to them. Inland Revenue has information about their crypto activities which they will need to report.

What to do if you receive such a letter?

A lot of people may be shocked when they look at their myIR accounts or open their mail to see such a letter. It may well be the first time they’re had to engage directly with Inland Revenue. You’re basically being asked to complete and file a tax return. I suggest that anyone who receives these letters should talk to a tax advisor and make sure you meet the obligations.

Do not put your head in the sand. In the present space we’re seeing quite a bit of what you might describe as more forceful efforts by Inland Revenue across all activities – investigations as well enforcement debt collection.

This latest media advisory letter for affected crypto asset investors is part of this new landscape.

Fiscal drag, the tax system’s “dirty little secret”

Marc Daalder of Newsroom has published a story about the effect of inflation on the amount of additional tax that’s been paid over the last 16 years. As I told Marc this is one the tax system’s dirty little secrets.

Marc’s story refers to a report prepared in December 2025 by Inland Revenue for the Minister of Finance, Nicola Willis and the Minister of Revenue, Simon Watts. The report was part of the commitment made in the National-New Zealand First Coalition Agreement to “…assess the impact inflation has had on the average tax rates faced by income earners.”

This brief report provides information on the inflation since 2010 when we last had a major reset of tax rates. Between then and the 2024 Budget nothing was done in terms of adjusting thresholds or tax rates other than introducing a new 39% tax rate on income over $180,000 in 2021.

What is fiscal drag

Fiscal drag is what happens when thresholds are not automatically indexed to inflation. Income growth even if just for inflation only can result in more income being taxed in higher tax brackets and therefore increase average tax rates. The analysis focuses on individuals rather than families and solely considers taxable income. The report considers the increase in average tax rates due to inflation across the various income distributions and the amount of additional revenue from this increase in average tax rates and the distribution of individuals impacted by these higher tax rates.

The report concludes, unsurprisingly, that fiscal drag has increased average tax rates and therefore tax revenue since 2010. Annual inflation measured by the Consumer Price Index between 2010 up until 2024, i.e. the period, the 14-year period in which tax thresholds did not increase averaged approximately 2.5% per annum.

Average tax rate rose by 2.55 percentage points

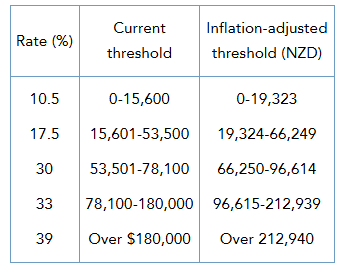

The Inland Revenue report includes a table showing the inflation-adjusted thresholds for the 2010-2024 period. (The 39% threshold introduced in 2021 has also been inflation adjusted).

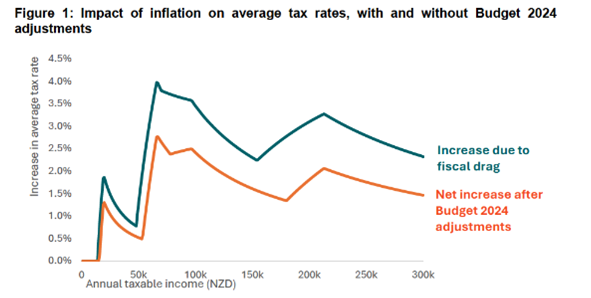

According to the report overall fiscal drag has increased the average tax rate by approximately 2.55 percentage points without the Budget 2024 adjustments and 1.65 percentage points when including them.

Most people will think the greatest increases in average tax rates will be for people on higher income. But listeners who have heard me bang on about this topic for many years will know the greatest impact is in fact lower down the income scale than most might think.

In fact, the biggest single increase is for individuals earning between $70,000 and $90,000 in 2024.This is because this group had a greater share of their income shifted into the 30% bracket because of the 12.5 percentage points jump in tax rate from the lower 17.5% bracket. According to the report the threshold for the 30% rate which was $48,000 in 2010 should have risen to $66,249 by 2024, over $18,000 higher.

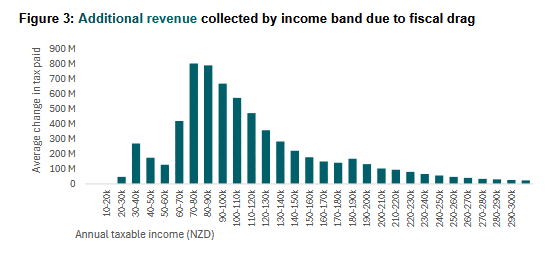

Consequently, the additional tax revenue collected by fiscal drag in annual taxable income reported is nearly $2 billion for people earning between $60,000 and $90,000.

Even taking account of the 2025 Budget changes, the report estimates fiscal drag’s additional revenue increased tax revenue by approximately one percentage point of GDP or over $4 billion annually. This number is higher than I had expected.

Don’t expect any changes in the Budget

It will be interesting to see if there’s any fallout from this report. The fiscal pressures for the government are such that there is no chance of any threshold increases happening in this year’s Budget. In fact, I don’t think a new government of any hue will be in a position to introduce increases any time soon.

European Commission report on wealth taxes.

Last episode we spoke with Tax Justice Aotearoa, who had published their tax policy statement for a fairer, more transparent tax system. Coincidentally, this was released at the same time as a monster report published by the European Commission Wealth taxation including net wealth, capital and exit taxes.

The report itself has two volumes and runs to over 450 pages which I am still digesting but fortunately there’s a 17-page executive summary. The foreword to the executive summary notes:

“The report is set against a backdrop of rising concern about the distribution of wealth in Europe, the erosion of taxes on wealth and wealth transfers over recent decades, and renewed fiscal needs in the wake of multiple crises. Over the past three decades, private wealth in the EU has grown substantially and has become more concentrated among households at the top of the wealth distribution.”

What is concerning the EU is that the top 1% in the EU have increased their share of total household wealth faster than their counterparts globally.

“This trend is notable because global top-wealth shares have stabilised in recent years while the EU continues to witness an upward drift. These patterns underscore the broader economic context for the present study. Wealth concentration is becoming a structural feature of the European economic landscape, raising questions about how existing tax frameworks can ensure fairness.”

A question of fairness

The European Commission echoes what Tax Justice Aotearoa and other tax fairness advocates are saying. If the tax system is building in unfairness, then what are the downside risks of perceived unfairness? If wealth is not being taxed relative to income, what are the social impacts of that?

The report contains some very interesting analysis, for example it notes that the very wealthiest, the top 0.01% in the EU have grown less rapidly than their peers in some non-EU countries. This apparently reflects a smaller role for high-growth firms and more redistributive systems. “These features temper the emergence of extreme fortunes, even as the top 1% continue to pull away from the rest.”

The available evidence here also points to the wealth gap between the richest 1% and the rest increasing substantially.

What is a wealth tax

The report analyses all wealth-related taxes such as net wealth taxes, recurrent taxes on unrealised capital gains which are a response to the “distortions created by realisation-based capital taxation” (our Financial Arrangements regime is an example of such a tax). Non-recurrent realised capital gains tax – which is the “classic” capital gains tax which arises only on a realisation event.

The report notes, unsurprisingly, that non-recurrent taxes on realised capital gains form a core component of capital income taxation in all EU member states, although their design varies substantially. The report notes the empirical evidence indicates that higher capital gains taxes can reinforce lock-in, (i.e. holding on to assets to avoid a tax charge) and capital gains tax cuts might have positive impacts on certain investment transactions.

The report notes, and this is also an issue, if not THE issue in our tax system, the central limitation of the various EU capital gains tax regimes s incomplete coverage. Unrealised gains are heavily concentrated among high wealth households, and realisation-based systems enable strategic timing of sales.

There’s a section on inheritance and gift taxes, noting that their share of tax revenue and private house increased in a number of European countries, and large inheritance is very important in the formation of very high net wealth, including among billionaires. In other words, billionaires are inheriting or being created by inheritances, which may be not as ideal.

Apparently, 17 member states and some other European countries have inheritance or estate taxes. The report notes

“Looking forward, simulations suggest that the revenue potential of inheritance taxation is likely to grow further as the volume of bequests increases with the “great wealth transfer” from older to younger cohorts.”

This is referring to the transfer of wealth now happening as the two richest generations in history, the Baby Boomers and Generation X, are now starting to pass away leading to a great wealth transfer of trillions of dollars to their descendants. Naturally, tax authorities and politicians are seeing this huge wealth transfer and thinking, ‘we might want some of that to meet rising costs of superannuation and ageing’. Similarly, taxpayers will take steps to mitigate the effects of taxation

Behavioural responses to wealth taxes

The report comments that “Behavioural responses and institutional design are central to understanding the performance of inheritance and gift taxes” The empirical evidence points to strong incentives for tax planning. For example, the UK’s Inheritance Tax applies at 40% to estates worth more than £500,000. That concentrates the mind wonderfully so there’s a lot of Inheritance Tax planning as a consequence. Conventional economic theory has tax as a deadweight cost and inhibitor of activity

On the other hand, according to the report the tax effects on wealth accumulation, labour supply and entrepreneurship appear generally modest.

“Available studies suggest that inheritance taxation can be designed in a way that preserves its progressivity and revenue potential without triggering large real economic distortions, provided that enforcement is effective and legal avoidance channels are curtailed.”

This whole section probably merits a podcast of its own.

The mobility effect of wealth taxes and Australia

The report also covers a set of taxes referred to as “exit taxes”, which if a person migrates may trigger a tax charge on exiting the country. (America applies one such tax to anyone renouncing its citizenship). According to the European Commission, broader research on mobility suggests that high wealth relocations are rare and movements are more influenced by preferential regimes in destination countries than by exit taxation itself.

I agree with that analysis. The biggest concern I have about introducing a wealth tax in New Zealand is this mobility effect. That’s because Australia has an extremely favourable regime, the Temporary Residents regime. My worry would be that people would migrate to Australia, because as long as they don’t become Australian citizens, then non-Australian based investment income and capital gains should remain outside the Australian tax net practically indefinitely. (By contrast our Transitional Resident exemption is time limited). The capital flight risk is one which has to be analysed because investors and migrants do look closely at preferential tax regimes.

Overall, this is a fascinating report, and it reflects growing interest worldwide in wealth taxation. The issues identified in the report as a cause of concern about the long-term effect on social coherence of extreme wealth accumulation are relevant here and this report will add to that debate.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

beware the hidden traps of the financial arrangements regime.

Recently, we’ve been discussing Inland Revenue’s increasingly aggressive, in our view, activities in dealing with crypto asset investors. You may recall that one tax agent has reported that clients with unfiled but not yet due 2025 tax returns received warning letters from Inland Revenue in effect saying, ‘You may not have yet filed your return, but we know you’ve got crypto-asset income, and we expect to see it in your return.’

To add to this increased activity, Inland Revenue has adopted the international Crypto Asset Reporting Framework, or CARF from 1st April. This is an extension of the Organisation for Economic Cooperation and Development’s Common Reporting Standard on the Automatic Exchange of Information (AEOI).

Reporting crypto asset service providers

From 1st April CARF will apply to what are termed New Zealand-based ‘Reporting Crypto Asset Service Providers’. These are basically any individual or entity who are carrying out the exchange or conversion of crypto assets on behalf of users as a business. This includes acting as a counterparty, intermediary or provide a trading platform. It does not include an individual entity who is only holding wallets or is trading crypto assets on their own benefit.

These Reporting Crypto Assets Service Providers must collect and report specified information about their users and transactions. This is then reported each year to Inland Revenue each 30th June. The first reporting date will be 30th June 2027 covering the period from 1st April 2026 to 31st March 2027. That information will then be shared with other jurisdictions as happens currently with AEOI.

The unknown network of information sharing

Inland Revenue obviously will also use what data it receives through CARF and the AEOI to match with New Zealand resident taxpayers. CARF is another example of something many appear unaware of, which is the massive amount of information that Inland Revenue gathers and has access to, and how it also shares that information with other jurisdictions. Those jurisdictions will in turn also be sharing similar types of information with Inland Revenue.

Inland Revenue is being very aggressive in the crypto-asset space. Its basic position regarding crypto-assets appears to be that all crypto is trading income and will be taxed accordingly although circumstances will vary. The one thing all crypto-asset investors should be aware of is that it is more likely than not, that Inland Revenue has data relating to your transactions. So pleading ignorance of the rules is not going to work.

More on the financial arrangements regime

Moving on, we’ve greeted with some relief the recent back-dated increase in thresholds for about the financial arrangements regime. The change should hopefully mean a lot of taxpayers are now what’s termed “cash basis holders”, so they’re not potentially subject to exchange rate fluctuations and therefore being taxed on unrealised income when the cash flows don’t match.

The issue with the financial arrangements regime is that it is extremely broad which an interesting new Inland Revenue Technical Decision Summary TDS 26/03 illustrates. The taxpayer in question applied for a private ruling in relation to the potential application of the financial arrangements regime to a transaction relating to the sale and purchase of land.

The arrangement in question was for the sale and purchase of land. The sales were structured as a staged subdivision with settlement and payment for each lot occurring in eight stages over eight years. The sale and purchase agreement included what’s known as a lowest price clause, under which the agreed price for the purchase of each subdivision was the lowest price for tax purposes under section EW 32(3) of the Income Tax Act 2007.

Does deemed interest income arise with a staged subdivision?

The issue TDS 26/03 considered was whether the consideration payable under the sale and purchase agreement was in fact the lowest price, and whether there was any financial arrangement income in the form of deemed interest under the agreement. In other words, the price component have included an interest component because eight payments would be received over a period of eight years. In such a context, it’s not hard to see why the persons putting this arrangement together were a bit concerned about potentially being caught under the financial arrangements regime.

Inland Revenue did indeed conclude the agreement was a financial arrangement which is hardly surprising given the eight-year period proposed. What about the lowest price clause, which basically said this is the price we would have paid at market value. This argument was accepted by Inland Revenue’s Tax Counsel Office. Yes, the sale and purchase agreement was a financial arrangement, but the value of the land was the purchase price as agreed, and therefore there was no financial arrangement income or loss for the purposes of the financial arrangement regime.

A good result for the taxpayer and a useful example about how the financial arrangements regime contains plenty of traps for the unwary.

And now in sports news…

Finally, this week, you may have forgotten, the Football World Cup to be held in Canada, Mexico and the United States is coming up. The All Whites have qualified for the first time since 2010 and their first opponent is Iran with the match to be played in Inglewood, California on 16th June. President Trump’s view is that Iran should not be there, but FIFA hasn’t really responded to this, so potentially the match may be moved to Canada or Mexico or even cancelled.

The All Whites versus the Internal Revenue Service?

Anyway, it has emerged in the last week or so that the venue is potentially the least of the problems for both Iran and the All Whites. This is because FIFA has failed to reach agreement with the United States Internal Revenue Service (the IRS), about a tax exemption relating to payments made to players and officials attending the World Cup.

Quite apart from their appearance fees, players and officials receive a daily living allowance or per diem. This was US$850 at the 2022 World Cup but because of the increase in the number of teams to 48 it has been reduced to US$600 (about NZ$1000) per day, for this year. I’ve been told there are literally huge bags of cash carried around as the daily disbursements are made to officials and players.

According to the Guardian report, no blanket exemption has been agreed with the IRS, and therefore those teams playing in the United States may be subject to federal, state, and city taxes on their tournament earnings and per diems.

When Qatari held the World Cup in 2022, it granted exemptions to all 32 attendees. As things stand Carlo Ancelotti, head coach of the Brazilian team, potentially could be taxed on his earnings in both Brazil and the US. The double tax agreement might give some relief and there should be a foreign tax credit available for any US taxes paid, but in summary it’s a bit of a mess.

But what about the double tax agreements?

There are a number of participating countries which will have double tax agreements with the United States. These typically include a whole range of clauses dealing with the issue of which country gets taxing rights in this scenario. The Guardian reports 18 countries have signed a formal double tax agreement with the United States, which would exempt their delegation from paying the federal taxes on the matter. Most of those are in Europe, but Australia, Egypt, Morocco, and South Africa are all reported as having a relevant double tax agreement.

New Zealand has a double tax agreement with the United States, but it is over 40 years old. I’m therefore not entirely sure that the agreement may cover the treatment of sporting participants. It’s therefore possible the All Whites players and officials will be subject to US federal taxes on their earnings and the daily living expenses I mentioned earlier.

A win-win for Iran and the All Whites?

You can be sure that the Iranians do not have a double tax agreement with the Americans. It will be interesting to see how this plays out. It might be that both the All Whites and Iran would be very happy to have the match moved outside the United States, not necessarily because of geopolitical matters, but simply because they get to keep more of their earnings.

And on that note, that’s all for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

The Government’s “targeted, timely and temporary” fuel relief package does as I thought it would, make use of the Working for Families tax system, but not to the extent that I had hoped. The proposal is to increase the In-Work Tax Credit (IWTC) by $50 a week. That will last for up to 12 months or sooner if until 91 octane falls below $3 a litre for four consecutive weeks.

The package will benefit 143,000 working families with children who will get receive the full $50 a week, with another 14,000 additional families getting a reduced payment, thanks to the impact of the abatement thresholds. First payments will be made on 7th April if people receive IWTC and Working for Families weekly, or 14th April if they’re paid fortnightly. The package is expected to cost $373 million if it runs for a full year will be counted against the Government’s operating balance for Budget 2026, which is coming up next month on 28th of May.

Whether it’s why broad enough is obviously a concern because prices are racing up particularly that of diesel which at my local Gull petrol station has risen 30 cents per litre this month alone to overtake 91 Octane petrol. There’s a lot of pressure on families out there.

The Lord giveth…and taketh

The start of the new tax year on 1st April also means a number of other changes took effect, some of which will take funds away from families. One of the more noticeable changes will be the increase in KiwiSaver contribution rates, which rise from 3% to 3.5% for both employers and employees. This happens automatically unless the employee applies for a temporary reduction to stay at 3% which can be for between 3 and 12 months. An employer is not required to increase their contributions if an employee requests a temporary reduction. According to an ASB survey perhaps 15% of employees planned to request a temporary pause on the increase to 3.5%.

ACC rates have also increased with the earner’s levy rising from 1.67% to 1.75% per $100 earned up to the maximum of $156,641 per annum. The minimum wage increases from $23.50 an hour to $23.95 an hour. But Best Start payments for babies born after 1st April will now be subject to abatement on annual family income over $79,000.

In my last podcast prior to the announcement of the fuel relief package, I suggested one option could be to increase abatement thresholds. It so happens the abatement threshold for Working for Families was increased, with effect from 1st April, from $42,700 to $44,900, the first increase since June 2018. However, in keeping with the theme of giving with one hand and taking with the other, the abatement rate also increased from 27 cents per dollar to 27.5 cents per dollar.

Relief package highlights abatement issue

The $44,900 income threshold is for a FAMILY’s income. Also keep in mind that someone working 40 hours at the new minimum wage of $23.95 per hour, has a total annual income of $49,816, which is nearly $5,000 above the new threshold.

The Government’s package here highlights an issue we’ve raised repeatedly now for several years about the interaction between low abatement thresholds leading to high effective marginal tax rates for persons on average and sometimes below average income.

The Government finds itself, giving with one hand, and then taking with the other. And the taking bit isn’t always noticed by the general public. The announcement of a $50 boost will go down well for those 143,000 families that are going to get it, very welcome indeed. But there’s the other 14,000 families who won’t be getting the full benefit, and a whole group that never got anything at all but still have increased transport costs.

The Working for Families abatement threshold is far too low which results in clawing back family income at a time when families need every cent possible, because this fuel shock is going to feed through to transport costs, obviously, and from there into the price of food.

An incredibly complicated system in need of reform

Over the past 30-odd years New Zealand has developed an incredibly complicated system of benefits where we’re giving with one hand, clawing back with another hand, and not looking at the overall impact of what we’re trying to achieve. I understand the question of abatement thresholds and its impact was actually discussed at the recent International Fiscal Association conference and my thanks to Robyn Walker of Deloitte for raising the issue for discussion.

But this is something I’m going to continue to raise. It would good to be hopeful we might see something in the coming Budget, but I wouldn’t hold out much hope for that because if something in this area was under serious consideration, it might have been included as part of this temporary package. But clearly, that’s not likely to happen, particularly since the threshold has just been increased.

Changes to thin capitalisation

The necessary legislation for the fuel relief package was included in the Taxation (Annual Rates for 2025–26, Compliance Simplification, and Remedial Measures) Bill we’ve been discussing in the past couple of podcasts. A number of other late amendments were also included in the Bill prior to it finally passing into law. A major change was in relation to the thin capitalisation regime in relation to infrastructure projects.

By way of background, overseas investors can choose to fund their New Zealand investments with equity or debt. If the investment is made via equity there’s no deduction available. However, if the investment is debt funded a deduction is normally available for any interest payable on the debt. Consequently, from a tax perspective debt financing is obviously preferable.

Back in 1995, New Zealand introduced some thin capitalisation (or thin cap) rules, which basically said for foreign-controlled home subsidiaries, the amount of tax-deductible debt would be limited to 60% of the net debt asset ratio for the New Zealand entity. (There’s some fluctuation allowed to this threshold depending on the worldwide group tax percentage for the total group of companies).

Thin cap rules are very common worldwide as a counter to excessive interest deductions, but it’s been recognised they can be a potential hindrance on infrastructure projects.

A targeted exemption

I understand discussions have been going on for some time with interested parties with suggestions that New Zealand follows Australia in introducing a specific thin cap exemption for infrastructure. The Government has therefore

“Agreed to a targeted exemption to the thin capitalisation rules specifically for infrastructure investment (including new infrastructure projects as well as existing infrastructure businesses), that aims to mitigate a potential impediment to foreign investments in New Zealand’s infrastructure under the existing rules.”

Under the amendment effective from the start of the 2026-27 tax year, any entity now electing into it will be able to deduct interest expenses on its full amount of debt, without a thin capitalisation adjustment so long as the debt is applied to the eligible infrastructure entity’s business or project, is from a genuine third party and does not have any equity-like features. The lender must only have recourse to the assets and income of the entity. Furthermore, the New Zealand entity still has to be capable of supporting the debt on a standalone basis without any further support from its investors.

This is a step forward and ties in with the Government’s overall plan to develop infrastructure and assist infrastructure projects. There’s been some discussion about the revenue loss risk on such an initiative, but equally we’re experiencing the risk of not building enough infrastructure in the first place. So maybe accepting there may be a risk around tax seepage is the right way forward.

Tax change for the New Zealand Superannuation Fund

The Bill also enables the New Zealand Superannuation Fund to pay its tax payments annually rather than through the provisional tax regime, as it currently does. This is designed to help its cash flow because as the country’s largest investor and taxpayer, it locks up a lot of capital in provisional tax payments, which if it gets wrong, can have quite severe use of money interest implications.

Using tax pooling to collect tax debt – another band-aid solution?

One other interesting change is a pilot extending the time limit to use tax pooling to satisfy income tax debt for the 2022-23 and 2023-24 income years. At present if you have not paid your tax in full for those years use of money interest (8.97% from 16th January this year) will be charged.

The proposal is to allow payments to be made using tax pooling (which has a lower effective interest rate) for those outstanding years until 1st of October 2027. This option is not allowable if the applicant has been bankrupted or is the subject of recovery proceedings for unpaid tax. The debtor must be up to date with their income tax and GST returns and with your GST and PAYE payments. (Inland Revenue does have some discretion to allow tax pooling if it considers it’s a one-off scenario, and it has accepted an application for financial relief under the Tax Administration Act).

This is an interesting idea to try, which could help with the over $9 billion of tax debt currently outstanding. However, I think it’s another example of perhaps putting a patch on or a Band-Aid on instead of rethinking the whole issue. At the moment late payment penalties AND use of money interest apply to late paid tax. In my view it should be either late payment penalties or use of money interest, but the combination of the two is a double whammy, which I don’t think is particularly effective and just aggravates clients.

Use of money interest is a vital tool, and I have no issues with it. We could argue that the rate is very high, but then it has to be because the Government doesn’t want to be treated as a banker of last resort. Nevertheless, I think reviewing the whole issue of late payment penalties, use of money interest, and how much of a factor they are with companies and individuals defaulting on their tax, would be a worthwhile exercise.

Inland Revenue myIR accounts under cyber-attack

Finally, Inland Revenue is always on the watch out for cyber security risks and so it’s introduced two-step verification when people are accessing their My IR accounts. This is to counter attempts by cyber criminals to hack into people’s My IR accounts.

Last month Inland Revenue noticed a significant increase in malicious attempts to log on with over 500,000 attempts made.

Unfortunately, around 300 MyIR accounts, which did not have two-step verification set up, were accessed. Inland Revenue has closed these accounts and they’re also monitoring another 900 accounts where a correct password was entered, but the two-factor authentication prevented access.

Always be alert that your My IR account contains highly sensitive data. This includes, dates of birth, addresses, details of your bank account, and your earnings. It’s good to know that Inland Revenue is watching closing. Sometimes two-step verification can seem like a pain in the backside, but it’s a vital tool. And with over 500,000 attempts to hack in one month, there’s a serious issue that Inland Revenue has to guard against.

And on that note, that’s all for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics of guests. Until next time, kia pai tō rā. Have a great day.

(This is an amalgamated transcript of the 23rd March and 3rd April podcast episodes. It has been edited for brevity and clarity).

controversial Inland Revenue proposals for shareholder loans hit a major roadblock

The Finance and Expenditure Select Committee has reported back on the Taxation (Annual Rates for 2025-2026, Compliance, Simplification and Remedial Matters) Bill. This Bill contained measures in relation to changing the tax treatment of non-resident visitors who are working remotely while visiting New Zealand, introducing the new Revenue Account Method for calculating foreign investment fund income, plus the usual host of other amendments tidying up various issues.

The amendments to the tax treatment of New Zealand visitors are designed to encourage people to work here remotely without triggering too many adverse tax effects. One change proposed relates to disregarding the activities of a non-resident visitor present in New Zealand when determining whether a company is tax resident in New Zealand.

Watties, Heinz, tax and a Lions legend

This is a long-standing point and with Watties being in the news for all the wrong reasons, I recall an interesting point raised way back in the 1990s when Watties was acquired by Heinz, the international food manufacturing giant. Apparently, Tony O’Reilly, the former British Lion and then chairman of Heinz, was in the country at the time the deal was being finalised. Did this mean Heinz had a permanent establishment in New Zealand because key decision makers were here?

Tony O’Reilly in action against the All Blacks in 1959

That was a somewhat mischievous question. But it is an example of where key personnel being in a country may trigger unintended and adverse tax consequences. The Bill tidies up a number of issues relating to this as well as clarifying the treatment of remote working by non-residents.

No major changes to the Revenue Account Method proposal

When the bill was introduced, much fanfare was made of the proposed Foreign Investment Fund (FIF) Revenue Account Method. This allowed an eligible person’s FIFs to be taxed on a realised gains basis with a discount of 30% applied to the gain resulting in an highest effective tax rate of 27.3% (i.e. 70% of 39%).

This was seen as disappointingly high so many submissions on the Bill requested a higher discount to reduce the effective tax rate. These have all been knocked back on the basis that the maximum rate of 27.3% is broadly comparable to the 28% payable under the PIE regime.

But there are some minor mostly technical changes. For example, losses arising under the Revenue Account Method were initially to be ring-fenced and only available against future gains. Any such losses will now be available to offset against dividends from the same interests. So that’s a bit of a win.

And there is the ability also to allow taxpayers to sometimes use other method calculations which are required at present rather than and not lose their eligibility to apply the revenue account method to other interests. In other words, you can sort of split treatment on that. So generally, the rules are a progression, but I think you can read when you get into reading the fine printing, you sort of see the technical minutiae and issues that pop up because of the complexity involved.

There was an interesting, there’s also a proposal for essentially there’s a realisation tax on migration, and a point has now been clarified that If this happens, the calculation of any tax payable, because someone has used the revenue account method and then migrated out of New Zealand, they would use the market value of the interest at the time the person departs New Zealand, not the market value received when the interest is subsequently disposed of.

Quick example, a person leaves New Zealand when the market value of one of these interests is say, $500,000, subsequently sells it and realises the market value of $1,000,000. Any New Zealand tax payable will be based on the 500,000 being the market value at the time they left.

Don’t look the parents are squabbling…

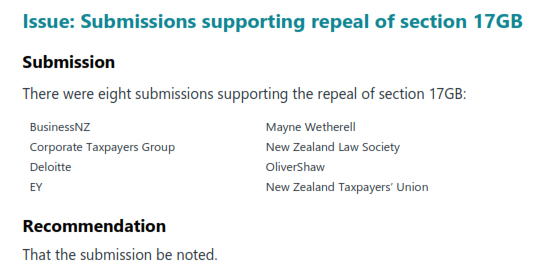

There was a nice little spat between the various parties on the committee over the proposal to repeal the Section 17GB of the Tax Administration Act 1994, which allows the Commissioner to collect information for the purpose relating to the development of policy for the improvement of the tax system. This was the measure introduced under the last Labour government, which was then used as the basis for finding the information for Inland Revenue’s controversial 2023 High Wealth Individual Review. Unsurprisingly Labour and the Greens opposed its repeal as did 202 submissions (including for the record Baucher Consulting, and the Chartered Accountants of Australia and New Zealand). Eight submissions supported the repeal.

Information sharing risks?

Labour was also opposed to the provision expanding the ability to allow Inland Revenue to share information about individual taxpayers with other government agencies more easily by way of Ministerial agreement. The Labour Party MPs made this very valid point,

“While Inland Revenue has strict rules about which employees may access information about individual taxpayers and it polices those rules rigorously, the same protocol may not apply in other agencies.”

Indeed, Inland Revenue, to the best of my recollection, has never had issues where someone has emailed out a spreadsheet full of confidential details which we’ve seen both the Ministry of Social Development and ACC to name a couple of culprits do. The Labour Party also noted “This is a significant change to the rules that protect the privacy of taxpayers’ information. We note the Office of the Privacy Commissioner has concerns about these proposals.” Despite this the provision is to go into effect.

Financial arrangements – three welcome surprises

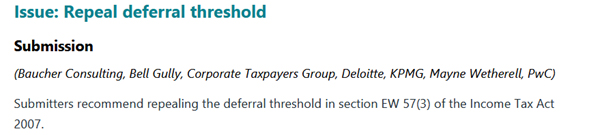

A big and welcome surprise relates to changes to the financial arrangements regime. Under the financial arrangements regime if certain thresholds are exceeded taxpayers must calculate income and expenditure on an accrual, or unrealised, basis rather than on a cash, or receipts, basis. These thresholds had not been increased since 1999, and the bill proposed to double them.

The regime also has a deferral threshold which means income and expenditure must be calculated on an accrual basis (unrealised) if the difference between calculating income on a cash (receipts) basis and the accrual basis exceeded $40,000 at any point. This applied regardless of whether a taxpayer’s total financial arrangements were under the $1 million threshold. Unsurprisingly, this deferral threshold frequently tripped up taxpayers (I even once saw advice from a Big Four firm which had overlooked its impact). I was one of several submissions recommending repeal of this threshold.

Inland Revenue has accepted our submission noting the deferral threshold

“…imposes a high compliance burden, requiring taxpayers to calculate income and expenditure on an accrual basis to compare it with a cash basis result and ensure that the difference is below a threshold. This is the same compliance burden that being a cash basis person is intended to avoid.”

This is an excellent result.

But wait, it gets better

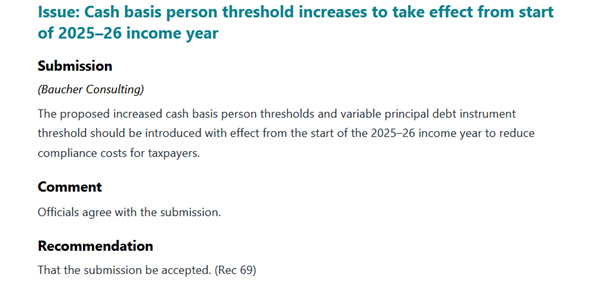

Under the Bill the increased thresholds were due to take effect from the start of the 2026-27 income year (1st April for most people). Adopting the principle of you don’t ask, you don’t get, I also submitted the threshold changes should be effective as of the start of current tax year (i.e. 1st April 2025). This would reduce compliance costs for the taxpayers, one of the key objectives of the Bill.

To my great surprise and delight, that was accepted as well, which is another excellent result.

But wait, there’s more…

KPMG made a very sensible submission that foreign currency loans used as mortgages over property should be removed from the financial arrangements rules and calculations. Exchange rate fluctuations can mean the deferral threshold is breached making any unrealised foreign exchange gains taxable. This once happened to one of my clients resulting in a tax bill of over $100,000.

Although Inland Revenue did not accept KPMG’s submission in full, it proposed instead “limiting the effect of foreign exchange fluctuations for the absolute value threshold”. This would be achieved by testing the absolute value threshold (now $2 million) is tested using the principal amount converted at a set date, for example, the first day of the financial arrangement, and ignoring subsequent foreign exchange fluctuations. If the principal amount changes for non-foreign exchange rate, reasons i.e. increases or decreases in borrowing, the financial arrangement should be reassessed for the threshold.

A bit late for my client perhaps but still a good result. The three change are also good examples of the Generic Tax Policy Process in action resulting in sensible law changes.

Controversial shareholder loan proposal halted

Moving on, late last year, Inland Revenue dropped what I described as a bombshell, with a consultation proposal for significant changes to the treatment of shareholder loans. Inland Revenue proposed that shareholder loans above a certain threshold would instead be treated as dividends, similar to the treatment for Australian and UK taxation purposes.

These proposals have hit a major roadblock with opposition from Winston Peters and New Zealand First together with the ACT Party. The end result is that the proposals as put forward in December will not be proceeding. Instead, Inland Revenue will continue to review the issue of the treatment of outstanding shareholder loans when a company goes into liquidation owing tax.

The proposals were quite controversial but the same time there was something of a tacit acceptance that yes, perhaps something needed to change. Simultaneously, there were concerns that Inland Revenue was perhaps muddling two issues. One of the issues was that companies that went under often sometimes owed substantial sums by shareholders, and in some cases, this meant Inland Revenue was missing out because funds were paid to shareholders instead.

John Cantin, former guest of the podcast, and also the independent advisor to the Finance and Expenditure Committee on the current tax bill has made public his submission to Inland Revenue on the shareholder loan proposals. His view is that more information is needed on the interaction between outstanding shareholder loans and company failures and the composition of the tax debt of such companies. If it is mostly GST and PAYE? Then yes, maybe that is something to be considered. He also thought there was merit in looking at changing the tax treatment of what happens on liquidation.

The upshot is we’ll be going back for round two of consultation. It’ll be interesting to see what comes out of this. Like John I think changes around what happens when a company is put into liquidation are sensible and also around keeping records of what we call available capital distribution amounts and available subscribed capital.

Property flippers – what about the tax impact?

And finally, an interesting story from RNZ about a complaint to the Real Estate Authority about a rise in so-called ‘property flippers’ making six-figure returns from unwitting vendors. Property data firm Cotality has noted a rise in significant rise in what’s called contemporaneous sales, with the number happening last year was almost double the total for 2024.

In a contemporaneous settlement, a property flipper makes a purchase offer with a long settlement period and then finds another buyer to purchase the property on the same day the property flipper has to settle their purchase. If it all goes to plan the property flipper makes a quick gain.

According to iFindProperty co-founder Maree Tassell who has complained to the Real Estate Authority about the practice:

“It’s quite common that there are some deals out there where people are making over $100,000-plus on contemporaneous settlements, getting a property under contract. The poor old vendor, and even often the vendor’s agents will think ‘oh this is a real purchaser’. …It’s quite deceptive to the vendors and quite deceptive sometimes to the agents.”

Although tax isn’t actually discussed in this story, these transactions would be considered a taxable trading activity even if they are not specifically within the bright-line test rules. It’s the sort of activity Inland Revenue should be watching with great interest. Property flippers should therefore beware, you may be making a quick buck, but Inland Revenue will be tracking these transactions. If you are not declaring the income, then you could find yourself with a big please explain somewhere down the line.

And on that note, that’s all for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.