- Australian Tax Office ruling on residency – time for a clearer statutory definition?

- Applying for Australian citizenship? Watch out for the sting in the tail.

Submissions closed Friday on the Tax Principles Reporting Bill. Now for a bill that doesn’t actually increase the tax rates this has been a surprisingly controversial bill, mainly because it’s actually perceived as being highly political in its ambit in introducing reporting on tax principles. The speed with which with which it has been rushed through is also controversial because normally tax legislation is developed through what we call the generic tax policy process (GTPP). The GTPP is very well regarded around the world.

But every so often, for whatever reason, the process is bypassed. Sometimes as during the COVID emergency because things need to be done immediately. It’s a framework through which New Zealand tax policy has operated for the better part of nearly 30 years. And it means changes of tax policy and of the particular tax treatment of certain items are developed over time through consultation.

Controversy around the Tax Principles Reporting Bill

In this case, the Tax Principles Reporting Bill came out of left field. There’s been very little consultation about it. In fact, we’ve only had barely three weeks between its introduction alongside the Budget and today. So that’s part of the controversy around it.

The other question is what it really is setting out to do. I think most objections will centre around this question of why is this here? The idea of setting out some ideas about what tax principles might be is not unreasonable in itself. But criticism of the Bill is focusing on whether it’s very clear about what it’s trying to do. For example, Inland Revenue is required to report on certain effective principles and whether there are inconsistencies in the tax system with these principles. But then, as several tax advisors have asked, what action will be taken at that point. There is also no acknowledgement that tax policy ultimately involves trade-offs between principles and politics. To be frank, tax is politics.

I’ve seen one or two interesting comments about which agency should be reporting under the Bill. Inland Revenue or maybe Treasury? There are a whole heap of things to consider about the Bill. Although it comes into effect on 1st July, if there is a change of government, it will almost certainly be repealed.

It’s an interesting Bill because it’s attempting to clarify the basis on which we design and operate a tax system. But it’s also flawed because I don’t think it’s has actually achieved that. We’ll see plenty of pushback and I’ll be interested to read the submissions on the bill. (Shortly after the podcast was recorded, John Cantin published his submission).

Australian tax residency

Moving on, I frequently deal with issues of tax residency. It’s a core part of what I do because tax residency determines what sources of income will be taxed in Aoteaora-New Zealand. There are also rules set out in double tax agreements, and one pretty basic principle wherever you go in the world is that if you have property situated in the country, that country gets what we call the primary taxing rights to it.

But individual tax residency is a matter of great practical importance. If a person is resident in the country, then that country can tax them on their world-wide income, and that can have quite significant implications.

The Australian Tax Office (ATO) has just updated and released a tax ruling TR 2023/1, on income tax residency tests for individuals. Australia deems a person to be tax resident in Australia if they reside in Australia under what they call the ‘ordinary concepts’ test, and that includes a person whose domicile in Australia, unless they’re satisfied that they have a permanent place of abode outside Australia.

A person is also resident if they have actually been in Australia continuously or intermittently during more than half of the year of income, unless they’re satisfied that they have a usual place of abode outside Australia and they do not intend to take up residency in Australia. There’s also another series of tests, which I’ve not come across, relating whether or not they’re a member of a superannuation scheme or are covered under the Commonwealth Fund.

When you look at these tests you can see there are quite a few value judgements involved. And so there have been calls for the Australian tax residency test to be put on a more statutorily defined basis, most notably by the Australian Board of Taxation. “The Board’s core finding is that the current individual tax residency rules are no longer appropriate and require modernisation and simplification.”

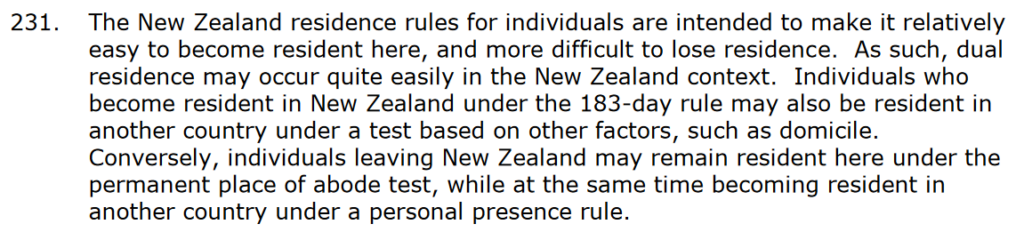

Now it’s of interest here obviously for people going across to Australia, but also because our own residency test is twofold. The primary test, and this is often forgotten, is a person is tax resident in New Zealand if they have a permanent place of abode in New Zealand. You’ll note that phrase, “permanent place of abode” is actually also used in Australia.

Failing that, there’s the days present test where a person is deemed to be resident in New Zealand if they are physically present in New Zealand for more than 183 days in any 12-month period. There’s a subtle difference there between our days present test and many other jurisdictions in that it is based on a rolling 12-month period rather than a tax year. On the other hand, when you get down to defining a permanent place of abode, that involves quite a number of value judgements.

The current residency test is now over 30 years old. As noted above the Australian Board of Taxation suggested that really the Australian test perhaps should be more clearly defined in statutory legislation. And I’m coming around to the view that maybe that’s what we need to do in New Zealand as well. I’ve seen at least one academic article in the past year that’s picked up on this point.

“You can check out any time, but you can never leave”

Now, why we don’t do that is explained in the Inland Revenue Interpretation Statement on residency. Right now the permanent place of abode test does make it easy for someone to be defined as tax resident, but difficult to lose that.

Notably, the Interpretation Statement does not have an example of a time period of how many years must a person be overseas before Inland Revenue would consider that someone has lost their permanent place of abode.

So, this makes residency a very open-ended issue, which is not terribly good in terms of certainty for taxpayers. It’s become more of an issue in the past 30 years since we introduced the permanent place of abode test in 1989 because as we have seen in the last three or four years, the world’s got a lot more mobile with people moving and working around the world.

This issue of being tax resident here, perhaps inadvertently, is actually something that individuals are concerned about. They obviously want to minimise their tax obligations as far as legally possible. On the other hand, governments know that if you set out very specific tests then people will play to the letter of those rules by watching carefully the number of days present in a country.

A British alternative?

The British residency test, the statutory residence test, actually deals with this day count issue pretty well by specifying what it calls “ties”. Depending on how many ties to the UK you have, whether you’ve been tax resident beforehand and how many days you spent in the previous tax years, then the number of days you can spend in a in the UK in a tax year before you become resident drops.

It’s therefore not as simple as you can spend 182 days and then you’re okay. Each year it drops off quite dramatically and basically at its tightest definition you can only spend 16 days in the UK. Obviously, people will still try and manipulate their timing within these limits but the UK test is much more specific and it gives a great deal of clarity.

And I think in our case, just as the Australian Board of Taxation considers, it’s not an unreasonable objective to be looking at a statutory definition of residency which addresses the concerns Inland Revenue rightly has about people trying to game the system, but it provides certainty for people.

Becoming an Australian citizen – beware the potential tax trap

Still on Australia, there was good news recently that there’s now a pathway for Australia and New Zealanders who live in Australia to become citizens. This is very important for the huge numbers of New Zealanders over there, well over half a million. There is, however, a potential sting in the tail.

People will be aware that New Zealand has what we call a transitional residents exemption, which applies to new migrants or people who have returned to here and have not been tax resident for ten years. Under this exemption their non-New Zealand sourced investment income for the first 48 months is generally not taxable here.

Australia has a similar test if it applies to what they call temporary residents and it applies to most New Zealanders living in Australia. The sting in the tail is that if you apply for citizenship in Australia, you are no longer a temporary resident. What that means in particular is your New Zealand assets here become subject to Australian tax, including capital gains tax. The impact of Australian capital gains tax on New Zealand assets is often overlooked. It’s an issue I deal with regularly.

So that’s the trade off on Australian citizenship. Overall, it’s a good news and it puts people who have contributed significantly to the Australian economy on a level footing. But there is a wee sting in the tail for some. So, approach with caution.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.