- Reforming Working for Families

- UK cash basis to be expanded

The end of the tax year on March 31st is fast approaching. This is a time of year where myself and other tax advisers are frantically tidying up outstanding tax returns and advising clients on steps they should be taking to make sure there are no unwelcome tax surprises for them. So here are a few common tips that we are passing through to clients.

Firstly, go through your debtor ledger and write off any bad debts. A bad debt deduction is only allowable if the debt is written off in the tax year in question. In doing this you really need to take a hard eyed look at your debtor ledger and tell yourself, realistically, are these debts going to be paid? Factor in how long the debt has been outstanding, the credit history of the client and what you know about how the client’s business is going. You can always write these debts off, take the deduction, and then if fortunately the cash comes through, then you write it back the following year. But the key thing is you can’t take a bad debt deduction until you write it off. And my recommendation is always to err on the side of caution on this one. So that’s my main tip.

My number two tip is one we see a lot of in our business and that is overdrawn current accounts. These happen when the shareholders/owners have often taken out more money than they’ve been paid through the salaries or are likely to receive. Where a client has an overdrawn current account there are a couple of options to offset against the overdrawn current account, an increased salary or a dividend.

If neither of those are possible because there are no reserves or the company has not been profitable, then what you will be faced with is having to charge interest on the overdrawn amount. The rate applicable is the fringe benefit tax prescribed rate of interest and for the quarter beginning 1st January 2023 it’s 6.71%. You calculate an interest charge based on the current account balance throughout the tax year. Keep in mind the rates have been rising, back on 1st April 2022, they were 4.5% and it’s due to rise again on 1st April to 7.89%.

This is an issue we commonly see, and we don’t often get to hear about it until it’s too late and often before remedial steps can be taken. A common reason for its occurrence is people take out too much money or the company has realised a capital gain and they’ve helped themselves to the capital profit without realising that actually it’s not as easy as that, that there are proper processes to be followed for distributing capital. This is a common issue most accountants will encounter and you need to take action, preferably before 31st March, to mitigate the impact.

Still on companies, a key area you’ve got to keep an eye on is what we call the shareholding continuity provisions. That is making sure that the relevant percentage of shareholders doesn’t drop below certain thresholds. For example, if it drops below 49% a company which has accumulated tax losses could potentially lose those tax losses. More critically, if it drops below 66%, then any imputation credits that have been accumulated will be lost. This will affect the distribution of dividends and lead to an effective double tax charge.

So again, check shareholding percentages very carefully. If there have been any changes, you need to make sure that they will not affect any tax losses or imputation credits a company may have.

Another important area is fixed assets. Where the fixed asset cost less than $1,000 check to see you have been taking an immediate tax deduction for the full amount. You should also go through assets that have been on the fixed assets ledger for some time, and just consider whether, in fact, they are in use anymore. If not, write them off and tidy up the balance sheet at that point.

A little pro tip here. You get a full month’s deduction for depreciation purposes regardless of when you purchased depreciable asset during the month. So, if you purchase an asset on 30th March, you will get the relevant full month’s depreciation deduction for that asset. So, if you are considering purchasing assets and they don’t fall within that low value asset write off limit of $1,000, you can maximise in a temporary way the depreciation deduction.

The final tip is to make sure that you’ve got all your elections filed on time. For example, if you’re considering, electing to join the look through company regime, those elections must be filed before the start of the new tax year (unless you’ve got a startup company). There are also some residual elections around in respect of qualifying companies. We don’t see so many of those now because that regime was abolished more than ten years ago.

Filing elections on time is crucial because if you missed the deadline you’ll have to wait a year. Inland Revenue, although it does have some discretion around late elections, very, very rarely will exercise that discretion. There may be some relief where it has been quite apparent that the recent cyclone and flooding events have disrupted a business.

You should also be trying to file all tax returns due by the end of the tax year. Otherwise, what we call the time bar provisions effectively get extended there – in effect Inland Revenue has another year to re-open prior year tax returns.

So that’s a few tips on how to get ready for tax year end and the most common areas we encounter. There are some good checklists around, including this comprehensive one from BDO.

The key thing is to be aware and get in front of your accountant or tax agent as soon as possible, don’t leave it until the 31st to ask these questions. We work miracles a lot of the time, but not every day.

‘Serious design issues’

Moving on, earlier this week, there was a report that a major review of the Working for Families scheme is currently under consideration by Social Development Minister Carmel Sepuloni.

The report has “found serious design issues” in the way some of the tax credits are applied. It highlights a number of factors which I’ve talked about for several years now, such as the increasing impact of the low abatement threshold.

Just as a refresher, the abatement threshold for Working for Families kicks in at $42,700. If your family income is above that threshold, then for every dollar of taxcredit you receive, $0.27 is abated, which means effectively that’s a 27% tax on that income.

Now, you’ll note that $42,700 is below the threshold of $48,000, where the tax rate increases from 17.5% to 30%. So as this report notes, the abatement threshold kicks in at relatively low incomes and not far below what someone on the minimum wage from 1st April will be receiving. So the whole system is due for a thorough review.

This issue was raised by the Welfare Expert Advisory Group and the Child Poverty Action Group, have been hammering away at the inequities of the Working for Families system for years now. Last week I talked about the interesting initiative in the UK budget for childcare to be provided to basically every child over the age of nine months. But that came with a sting in the tail that there was a very, very penal abatement regime once you crossed a threshold even though that threshold was quite high.

But the point stands that thresholds and abatements can produce some very unwelcome outcomes, and one of which is that people may no longer have the incentive to work because they just look through the numbers and decide once the extra tax and the abatement is taken into consideration, they are no better off.

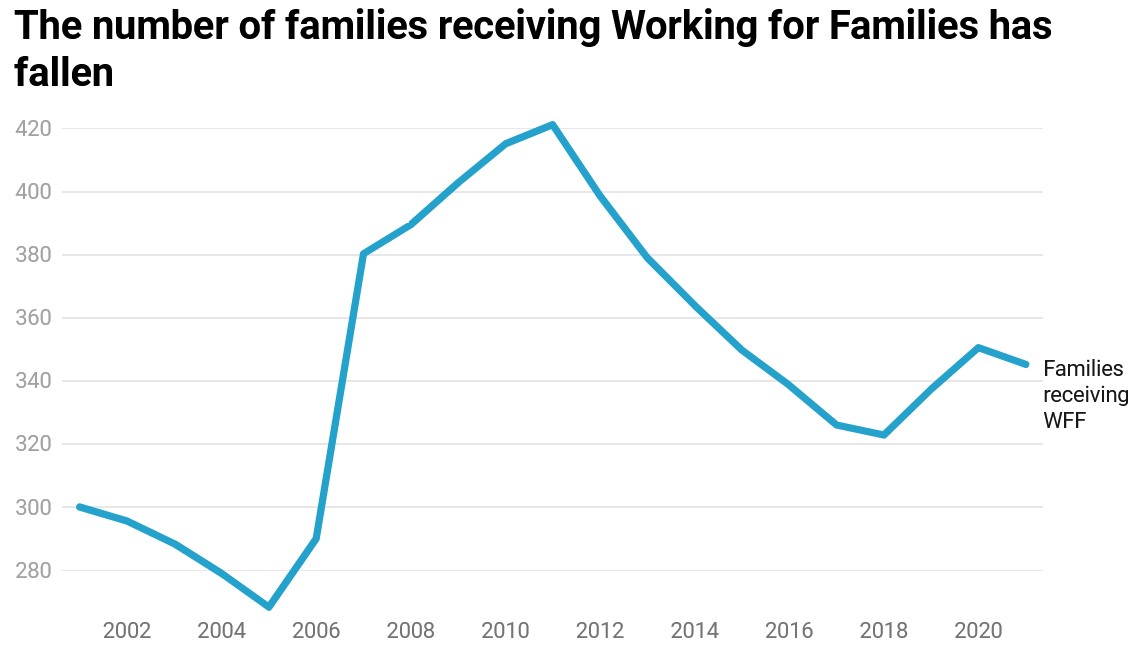

And one of the interesting things that this report shows is the number of families receiving Working for Families has fallen from about 420,000 in 2011 to just over 340,000 in 2021. When you consider the population growth in that time, that’s quite a significant fall in relative terms.

Another issue which requires resolution is that more and more families are falling into debt because they were overpaid Working for Families tax credits during the year. Apparently 57,000 families now owe debts worth $250 million, which includes $71 million of penalties and interest. Almost certainly most of these families are at the low income, so digging their way out of debt is a real problem.

It’s good to see that a report is being considered as major changes are needed. I have a sense that this year’s budget is going to tackle some of those issues, not least of which would be increasing the abatement threshold. A point of interest about the abatement threshold is that when Working for Families was introduced, the abatement threshold was $35,000, but the abatement rate was 20 cents on the dollar.

Not only has the threshold not kept up with inflation since its introduction in December 2005 (based on inflation to the December 2022 quarter it should be $52,700) but also abatement applied now is 27 cents on the dollar, quite a significant increase. So there’s a lot of strain in this situation and it’s something I’m glad to see the Government is considering actively.

Low compliance option for tiny cash businesses

And finally, this week, something else from last week’s British budget, which again, I think has relevance for New Zealand, and that is consulting on expanding the so-called cash accounting regime, a simpler tax regime for smaller businesses.

The British initiative recognises that there are businesses which are not significant enterprises. They’re often one person operations, so they don’t derive significant amounts of income. But under present tax policy, they would have to prepare normal full accrual accounting. However, most of the time these operations are too busy running their businesses and operate everything basically on a cash basis.

So, ten years ago the UK introduced a low compliance regime for cash businesses, which said that those self-employed persons with income under £150,000 could drop into this regime. Under the regime income is taxable on receipt and expenses deductible when paid. There is no need to accrue for income and expenditure. Incidentally, the regime doesn’t worry itself too much about the niceties of depreciation. Basically, you can take a full deduction for capital assets. Last week’s UK Budget is planning to extend this regime.

I think something like this is well worth considering in the New Zealand context. It was something we talked about when I was on the Small Business Council. Inland Revenue has fenced around this issue for some time. I’ve also had intermittent discussions with Inland Revenue policy officials about a similar scheme.

Inland Revenue’s concerns centre on the fiscal costs and whether it could be too generous. On the other hand, how much free time would such a regime free up for those businesses who are often run by some pretty stressed individuals? I am sceptical that the fiscal cost is as great as Inland Revenue imagines. Its duty is to maintain the integrity of the tax system so its approach is not unreasonable.

Anyway, it’s something worth considering. In Britain, it’s only applicable to unincorporated businesses. But I think it’s easily adaptable for smaller enterprises, for example those with turnover below $500,000 per annum who are eligible for six-monthly GST filing.

To address some of Inland Revenue’s concerns, it could also introduce something like fixed deductions on the principle “You can drop into this regime, but here are the fixed amounts of deductions because we know in your type of business these are type of deductions we see and the average amount of expenditure in respect of those items.” It should have the data to support this approach.

I’ve occasionally spoken to Inland Revenue policy officials on this topic but progress on these sort of initiatives often gets interrupted when something like a pandemic or a flood turns up. At which point Inland Revenue’s attention rightly gets diverted to more immediate matters. Anyway, this is something for further consideration and I’ll be watching closely to see how it pans out in the UK. Maybe we might see something similar in New Zealand eventually.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!