The current state of the Generic Tax Policy Process and when does consultation become lobbying.

- Changing the rules around disposing of trading stock

- How do we pay for managed retreat?

- Tik-Tok and GST fraud

At last week’s International Fiscal Association’s Trans-Tasman conference, a lot of the discussion among New Zealand advisors outside of the seminar rooms was around the state of tax policy. There is a growing concern that a more active government with interventions and proposals such as the proposed zero rating of GST on fruit and frozen and fresh fruit and vegetables is undermining the Generic Tax Policy Process which has been in place for nearly 30 years.

Like many practitioners, I’ve been involved with the GTPP at various stages. It is well-regarded internationally and has operated since 1994. It is intended to ensure

“better, more effective tax policy development through early consideration of key policy elements and trade-offs of proposals, such as their revenue impact, compliance and administrative costs, and economic and social objectives. Another feature of the process is that it builds external consultation and feedback into the policy development process, providing opportunities for public comment at several stages.”

However, the concern is emerging that against this well-established background more recent measures such as the Tax Principles Bill, or the legislation that enabled Inland Revenue to carry out its high wealth individual research project, have happened outside the GTPP framework. The proposed GST zero rating of fresh and frozen fruit and vegetables could be another example. These developments are unsettling the previously predictable process for working through and discussing tax proposals.

I’m of the view that tax is fundamentally about politics and politicians will always make political calls. The GTPP is intended to minimise the effect of that and give more predictable tax policy outcomes. But you can’t eliminate it entirely and this dichotomy between efficient tax policy process and politics will always be there.

There is also the question raised in an interesting story this week by BusinessDesk (paywalled) in reference to the work of the Corporate Taxpayers Group (CTG) about when consultation ends and lobbying begins. The CTG includes the main corporate taxpayers such as Fonterra and the four big banks. The New Zealand Superannuation Fund, the largest single taxpayer in the country, is also a member.

The CTG meets regularly at the offices of Deloitte (more frequently than I had imagined) as the story outlines, and there is an annual membership fee which is to pay for the secretariat, which will make submissions to Parliament and to Inland Revenue.

But when does this move from consultation to lobbying. Very difficult to say. I don’t see it as lobbying although I do appreciate the risks that might be involved in that. But having been involved in the process and been in meetings with CTG representatives, Inland Revenue officials, I don’t believe that’s the case.

But as I said, I can understand why some might be concerned by this. It comes back to a key part of any democracy, and that’s transparency. But on the whole, as I said, I think New Zealand’s been very well-served by the GTPP. And I know that internationally it’s very well regarded because it has got a stability of process to it.

I think one of the issues that’s causing raising concern is because left wing governments are likely to more interventionist. But I do think this situation is exacerbated at the moment because the strain of the boundary between capital and revenue, and our general under taxation of capital, the lack of a capital gains tax, wealth, tax, death duties, are putting strains on the system. And so, politicians are trying to find shortcuts to try and deal with this issue and the need for more revenue. You can dispute how much is needed. But when I look at the state of roads and hospitals and you see the growing bill for climate change, my view is and it’s also the view of Treasury, as I pointed out a number of times, and its Long Term Insights Briefing He Tirohanga Mokopuna we need more revenue.

A whole lot of hissing

So, there are strains emerging and it’s impacting the GTPP, which makes tax advisers understandably a little unsettled about how well that process will continue. As Louis XIV’s finance minister Jean-Baptiste Colbert said in probably one of the most famous maxims about taxation: “The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing.” That was true in the 17th Century and remains true today. And there is quite a lot of hissing going on at the moment.

The GTPP in operation – consulting on trading stock

Moving on and still on to the topic of consultation and an example of the GDP in operation. Inland Revenue has released a paper for consultation on the treatment of trading stock disposed of below market value.

At present, whenever trading stock is given away, or disposed of for below market value it’s deemed to have been disposed of at market value. The reason for that rule is reasonably solid. It’s to counter potential tax avoidance where the stock is given away or may be used for private consumption by a business owner or sold at a deep discount to associated persons. In some cases, it could apply for a particular industry, exchanges of stock could take place at cost or less. All of those generate benefits in terms of the under taxation of revenue. So that’s why that rule exists.

But there have been instances where businesses have wanted to give away stock and make donations for charitable purposes, and that’s when this rule becomes problematic because they can’t effectively do so. Over time the practice has developed for granting temporary emergency relief in some situations as a work-around.

In 2004 a permanent override was put in place with donations to farming, agricultural and fishing businesses during what is termed an adverse event. And there have been a large number of those weather-related adverse events either for drought or like we’ve experienced this year, flooding.

Between 2010 and 2012, there was a temporary override for 18 months in response to the Canterbury earthquakes. And then again, starting in March 2020, a temporary override was put in place for four years in response to COVID 19.

That override will end on 31st March next year, and the object of this consultation paper, is to propose a more permanent solution rather than using ad hoc solutions whenever we encounter a particular scenario such as COVID or earthquakes.

The consultation paper runs to 29 pages and includes a useful appendix which summarises all the potential summary policy options and how they may play out. Overall, this is a good example of the Generic Tax Policy Process in operation. Consultation on the paper is now open and closes on 6th September.

Managing retreat & how to pay for it.

As just mentioned, temporary emergency relief from the usual stock donation rules has been granted for a number of reasons, including this year, the flooding in January and February and the impact of Cyclone Gabrielle. A constant theme of this podcast is the question of environmental taxation and the need to address the longer-term question of how we going to pay for these climate related events.

Earlier this week a Government expert working group released its report on the question of what’s termed managed retreat.

The report, which clocks in at 284 pages, is very comprehensive and raises a number of potential scenarios and alternative measures that could be needed. One of which, as the excellent Newsroom story covering the report notes, is conditional powers to basically force people to leave particular areas that are under threat.

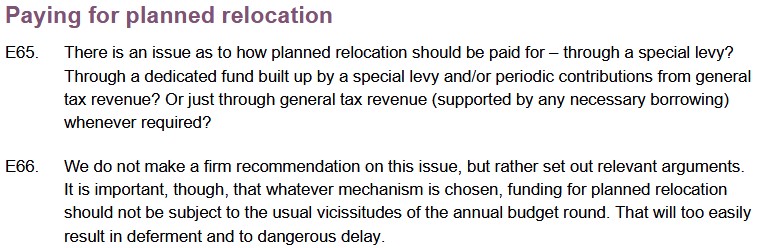

Being a tax podcast the question we are most concerned about with environmental and climate change impacts is how we are going to pay for it. The report has two key proposals E65 and E66.

But consider this, we have currently 700 homes which have been rendered uninhabitable following the flooding in January and February. And there’s another 10,000 homes that require flood protection. The Government has said it will split the costs over the uninhabitable homes with local councils affected. But, as far as I can tell, neither the councils nor the Government have really fully funded for these costs of maybe a cool billion or so this year and maybe every year and rising. So, it is an issue that needs to be addressed.

The report has some interesting discussion around what happened in Canterbury in relation to the earthquakes and then the first and I emphasise, first, example of managed retreat, from the Bay of Plenty settlement of Matatā

The report says, however we decide to fund this, the funding should not be subject to the usual vicissitudes of the annual budget round because that would mean it would lead deferment and dangerous delay. When it comes to kicking a football down the road, the politicians, as we know, are better than the Football Ferns at kicking it a long way out of trouble. Or so they think, but the issue still remains. I totally agree, therefore, with the report’s recommendation that there has to be a permanent funding solution.

I maintain that if we are going to do something around the lines of environmental taxation, the funds that are allocated to it should be hypothecated, and certainly not form part of the consolidated fund because we’ll then have politicians tempted to raid those funds. We’ve seen this in the recent Auckland Budget Council, by the way, where reserves built up for environmental purposes were used for other purposes.

In terms of holding politicians to account, I think we need to be asking a lot more questions about them on this matter because this is going to affect us all. We’ve had a miserable winter with extensive flooding and the ground is sodden. What happens when the next big floods come along, who pays for the clean-up?

No longer friends with Russia…

At the International Fiscal Association Trans-Tasman conference last week, we spent a lot of time discussing double tax agreements. It so happens, Russia has decided to suspend its double tax agreements with 38 countries, which it considers are now ‘unfriendly’ in the wake of the invasion of Ukraine. New Zealand is on that list. So that probably means that for someone in Russia trying to claim tax relief from under the double taxation between New Zealand and Russia, they’re out of luck and they’re probably going to be facing higher tax bills as a consequence.

TikTok and GST fraud

And finally, just on the topic du jour this week of GST, there’s an absolutely extraordinary story coming out of Australia about how social media influencers on TikTok encouraged at least 56,000 people to take part in a A$1.6 billion tax fraud scheme. Apparently these TikTok influencers explained how to get fraudulent GST refunds. The scam involved obtaining an Australian Business Number, then filing Business Activity Statements (the equivalent of GST returns) and claiming false GST refunds. In some cases, there were attempts to claim refunds of up to A$100,000.

The Australian Tax Office apparently is still grappling with the sheer size of the scandal. There’s a story in the Australian Financial Review about a Victorian woman who managed to stay out of jail, after repeated attempts to try and get A$115,000 fake GST refunds for a dog grooming business that had been set up more than a decade ago but had been largely dormant until 2020 before she attempted to pull this scam.

Fascinating story which will be interesting to see how it plays out. To me it lends support to the suggestion that we should look seriously at zero rating transactions between GST registered businesses. It should be a means of stopping such attempted frauds. Obviously, if that proposal is taken forward, it should go through the proper Generic Tax Policy Process consultation.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.