a new report on how the tech companies minimise their tax.

and tax agents rate Inland Revenue.

Recently we discussed the Taxation (Annual Rates for 2025−26, Compliance Simplification, and Remedial Measures) Bill which coincided happily with the New Zealand Law Society’s annual tax conference.

Making compliance with the financial arrangements regime easier

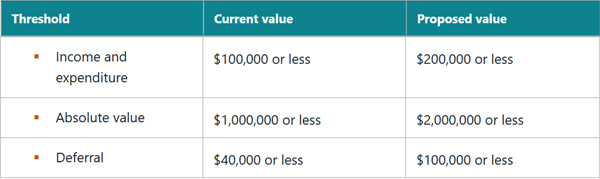

Amidst all the excitement, I overlooked a fairly critical measure in relation to the financial arrangements regime. As regular readers will know, the financial arrangements regime is highly complex, and little known to the average taxpayer. A major issue with the regime is that once certain thresholds are breached unrealised gains and losses must be included in taxable income, i.e. on an accrual basis.

These thresholds have not been amended since 1999 which was the last time there was a serious review of the financial arrangements regime. It’s therefore very welcome news to see a proposal to significantly increase the three key thresholds allowing persons to be treated as a ““cash basis person” and therefore able to return income or expenditure from a financial arrangement on a cash (realised) rather than an accrual (unrealised) basis.

However, Robyn Walker of Deloitte has pointed out the continued existence of the deferral threshold remains problematic. At present, even if the other two thresholds are met, income may still have to be returned on an accrual basis if the difference between income and expenditure calculated on an accrual basis and that under the cash basis exceeds the deferral threshold. In other words, in order to comply with the cash basis method taxpayers are required to calculate and track income and expenditure under the accrual basis.

As Robyn notes the deferral threshold just needlessly complicates matters. (The anecdotal evidence is that its effect is often not realised). She is therefore campaigning for the repeal of the relevant provision requiring the deferral threshold calculation. I fully support her suggestion as bringing about a much-needed simplification. As an aside my personal preference would be for the new thresholds to have retrospective effect from 1st April 2025, rather than 1st April 2026 as proposed.

PepsiCo and Big Tech

One of the papers at the recent New Zealand Law Society tax conference reviewed the Australian PepsiCo case involving what’s called an “embedded royalty”. In this case the Australian Tax Office (“ATO”) said that a bottling agreement for concentrate agreement between PepsiCo and Schweppes Australia Pty Limited involved an embedded royalty and therefore withholding tax was due on a portion of the payments under the agreement.

The ATO won in the initial court case in March 2023, but on appeal and a majority of the Full Federal Court ruled in favour of the taxpayers in March 2024. The case then went to the High Court of Australia which has just ruled 3:2 in favour of Schweppes Australia/PepsiCo.

That would appear to be the end of the matter in Australia but as the paper and session at the New Zealand Law Society tax conference noted, the case remains of interest here. In particular, could our non-resident withholding tax and non-resident contractor’s tax rules apply to part of any payments made to an offshore related party by a New Zealand company.

The PepsiCo decision coincides with the release of a report from Tax Justice Aotearoa entitled Big Tech Little Tax – Tax minimisation in the technology sector. This report examines the publicly available records of the major tech companies in New Zealand to determine how much income tax they are paying and how they are structuring their affairs.

There’s a lot to pick apart in this report. It notes the Government has decided to withdraw the bill introducing a Digital Services Tax (DST) given the Trump administration’s plain declaration that any form of DST would be viewed unfavourably. Inland Revenue had estimated a DST would have been yielded perhaps $100 million in annual revenue.

Targeting the tech giants

The purpose of the paper (written by ex HMRC/Inland Revenue international tax specialist) is

“…to identify practical options to capture a greater proportion of income, including through the application of existing legislation. It argues, for example, that applying the 5% withholding tax stipulated in the New Zealand US double tax aggregation agreement to the service and licence fees of Google, Facebook, Amazon Web Services and Microsoft would have yielded withholding tax revenue of $130 million.”

The paper analyses the various types of fees paid by the New Zealand subsidiaries of companies like Google, Facebook, Amazon Web Services, and Microsoft, and explores whether some of these payments might, in substance, constitute royalties and therefore subject to non-resident withholding tax of 5%. This is where the PepsiCo case becomes particularly relevant, as it provides insight into how such payments might be classified.

The paper analyses the tax practices of the tech giants and their three primary models of tax minimisation: the service fee model, the inflated licence fee model, and the service company model. Facebook, Google and Amazon Web Services appear to use the service fee model involving substantial “service fees” to related offshore companies.

Oracle New Zealand and Microsoft New Zealand use the inflated licence fee model, under which the local subsidiary pays a large percentage of their revenue to offshore subsidiaries for the licensed use of certain intellectual property rights. According to the report in 2024:

“Oracle New Zealand earned revenue of $172.7m but paid licensing fees of $105.3m to an Irish related party, leaving taxable income of just $5.3m. In previous years, the company has disclosed royalties, which, at that time, made up between a third and three-fifths of total revenue.

Microsoft New Zealand earned revenue of $1.32bn but paid $1.075bn in “purchases” to an Irish related party, leaving taxable income of $62.8m.”

It so happens that Oracle in Australia is currently in the middle of litigation with the ATO regarding the sub-licensing of software and hardware from Oracle Ireland to Oracle Australia and whether these should be treated as a royalty. This is a major case as apparently at least 15 other multinationals are facing a similar dispute with the ATO. Inland Revenue (which tends to follow Australia’s lead on transfer pricing issues) will be watching with interest.

A lack of transparency

The paper also discusses MasterCard, Visa and Netflix where we really don’t know what’s going on because there is no publicly available information. At present all three companies meet the requirements to be exempt from publishing financial statements. The paper surmises the three companies utilise the service company model under which “the local subsidiary operates only as a marketing and support service to an overseas group company, while sales or service revenue is booked offshore.”

I agree with the paper’s recommendation that the Companies Act reporting requirements are changed “to require all local subsidiaries of overseas-headquartered companies to file accounts publicly.” The numbers are reportedly quite large for MasterCard and Visa; it’s the commission on $49.5 billion of credit card payments. In the case of Netflix, if it has 1.2 million subscribers in New Zealand then its expected subscription revenue should be approximately $250 million a year.

Overall it appears there is substantial potential profit shifting happening through the use of various fees, some of which could be subject to non-resident withholding tax. As noted above there is significant litigation happening in Australia on the issue and I don’t think the ATO is going to back off on the matter. I do wonder where Inland Revenue is on this and I expect that we will see more chatter and more discussion of this topic.

Tax agents survey results

Finally, what do tax agents think of Inland Revenue? Quite a few times it depends on what we receive in the morning mail and how our clients react. Joking aside Inland Revenue regularly surveys tax agents and it has just published its Tax Agents Voice of the Customer survey results for the just ended 2024/25 financial year.

According to Inland Revenue tax agents “continue to report strong satisfaction with our services. Some of these results are at their highest levels so far:

92% of tax agents are satisfied with their overall experience

95% found it easy to get what they needed, which is a significant improvement

88% trust Inland Revenue.”

Those are all fantastic numbers and very encouraging.

The benefits of answering the phone

Inland Revenue considers these results “reflect our improved responsiveness” which includes that “Over the past six months, many of you have noticed it’s now easier to talk to us on the phone.” Not being able to get through and speak with someone at Inland Revenue has been a sore point for many tax agents.

The reality is that although Inland Revenue would prefer tax agents and the general public interacted online with it, sometimes there is no substitute for a phone call. This is the swiftest way of sorting out any issues resulting from Inland Revenue not processing a transaction correctly. Often a tax agent will come under pressure from a client to resolve an issue swiftly. I think Inland Revenue doesn’t always appreciate that when it drops the ball, we as tax agent cop the flack for it because something we’ve said is going to happen hasn’t been done. It’s therefore encouraging that phone response times have improved.

Tax agent satisfaction with responsiveness on web messages is now 74% up from 70% for the year ended 30th June 2024. I think that’s too low it should be at least 80% in my view. To be fair I think Inland Revenue would want to reach this level too. Satisfaction with consistency of Inland Revenue’s advice was 76% for the year which is down from 79% for the 2024 year. As Inland Revenue notes consistency of advice is important but remains a challenge.

Outside of survey bodies such as the Accountants and Tax Agents Institute of New Zealand, the Chartered Accountants of Australia and New Zealand, and the New Zealand branch of CPA Australia all regularly discuss service delivery and operational matters with Inland Revenue officials. Overall, the survey is a pass mark for Inland Revenue, but areas for improvement remain and it’s good to see it acknowledging this.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Should the New Zealand Superannuation Fund become tax exempt? Inland Revenue is under scrutiny for its use of social media.

A bad week for Apple and Google in the European courts.

Inland Revenue releases an intriguing consultation on GST and management services supplied to managed funds.

In the past few weeks, the question of taxing capital has reappeared on the agenda featuring across a number of news stories. It probably kicked off initially when Inland Revenue’s long term insights briefing consultation document raised the question of whether the tax base should be expanded to meet what is the anticipated growing fiscal costs of superannuation, health and climate change.

“New ways of generating revenue”

Then a couple of weeks back, the outgoing chief executive and Secretary to the Treasury, Caralee McLiesh, commented to the New Zealand Herald that New Zealand needs new ways of generating revenue and cutting expenditure. She suggested a capital gains tax and a more efficient superannuation scheme.

Labour leader Chris Hipkins has been in the news talking about the Labour Party’s internal discussions around the question of taxing capital. And then at the start of the week, Bruce Plested billionaire co-founder of Mainfreight, raised the idea of wealth tax. Understandably he caveated it with a question around whether the funds raised would be spent wisely.

But the point is, across the whole spectrum the question of taxing capital is back on the agenda. It never actually goes away to be perfectly honest. Like spring it comes around at least once every year. Anyway, it’s interesting to see this debate carried on. I think a driving factor is a growing recognition that the present tax base probably isn’t sufficient to meet the coming demands of rising superannuation, rising health costs and climate change. Sure, managing government expenditure more efficiently will help, but it will only go so far.

The Treasury has talked about a structural deficit of 2% of GDP which is $8 billion. That’s a fairly sizable sum, and with the best will in the world, cuts in government spending aren’t going to fill that gap. So, a discussion has to be had on how this gap is to be filled.

Given we will need to find extra revenue, taxation of capital is the obvious point. We should be considering whether it’s a wealth tax, land tax, capital gains tax or even restoration of estate and gift duties, which were once quite a substantial part of the New Zealand tax base. It could be a combination of all or some of those, but the debate isn’t going away.

Time to make the New Zealand Superannuation Fund tax exempt?

Moving on, and talking about the rising cost of superannuation, the New Zealand Superannuation Fund (NZSF) was established more than 20 years ago by Michael Cullen, to help smooth the cost of superannuation. It has been an enormous success. The NZSF has now grown to well over $70 billion and along the way it has been paying tax.

This is quite unusual for sovereign wealth funds because most are tax exempt. New Zealand has two other sovereign wealth funds, ACC and the Reserve Bank of New Zealand, and neither of those are taxed. They have between them another $60 billion of assets. But when the NZSF was established back in 2003, the decision was taken that it would pay tax. Part of the reason for doing so was to provide a commercial incentive so the NZSF made decisions around investments on strong commercial grounds, rather than because of a tax-exempt status.

But this has created a sort of slightly odd money-go-round. The government would contribute capital to it based on a formula, and then the NZSF would then pay part of that back in the form of tax. This is before its designated drawdown date, which is coming up towards the latter part of this decade, when it’s expected that regular withdrawals will be made to start funding superannuation.

For the period to June 2024, the Super Fund received contributions of roughly $1.6 billion overall and paid nearly $1.5 billion in tax. It is by far and away the largest single taxpayer in the country, a reflection, by the way of our Foreign Investment Fund regime rules. Finance Minister Nicola Willis is now seeking advice as to whether in fact it should become tax exempt, on the basis now that its tax bill is beginning to outgrow crown contributions.

Now that the Government has contributed $16.9 billion after accounting for $9.6 billion in tax paid since the fund was set up, the Finance Minister will be thinking whether it’s now time the Government can wind back the contribution. Ultimately, this should have the same effect as also removing its taxable status. We shall see how this develops, but it’s interesting to see the discussions in this space, which are also a by-product of the question of how do we fund superannuation?

Inland Revenue under fire

Moving on, Inland Revenue is in a little bit of hot water after it emerged that it’s giving hundreds of thousands of taxpayers’ details to social media platforms as part of its various marketing campaigns. These campaigns are intended to target taxpayers who might owe taxes.

Unpaid student loans are one particular area that that pops up here. The controversy revolves around the anonymisation tool which is used to ensure that whatever information the social media companies get, the details are minimised as far as possible to protect the privacy of the taxpayers involved.

The question has been raised as to whether that tool is sufficient.

The horns of a dilemma

There are two issues here. One is the technical question about how effective is the anonymisation tool. But the bigger question is whether Inland Revenue should be doing that. It faces a problem that if it wants to reach out to the general public – or certain sectors of the public – to remind them about their tax obligations. The best outreach method is through social media platforms. Inland Revenue is on the horns of a dilemma.

I will say this, that in my 20-30 years’ experience watching and working with Inland Revenue, it has an exemplary record around disclosure of private details. It has strong processes in place, and I cannot recall over that time a data breach scenario similar to those we’ve seen with both ACC and MSD where private data of taxpayers has been emailed to persons outside the agency.

Notwithstanding Inland Revenue’s record, the practice seems questionable because of the fact that social media sites are constantly under attack from hackers. Supplying private information to social media companies, no matter how laudable the intentions, puts that data at risk. It would be interesting to hear from the Privacy Commissioner on this.

Then there is the huge irony that these social media companies are amongst the most aggressive exponents of tax planning in in the world. For the year ended 31st December 2023 Facebook New Zealand, for example, reported taxable income of $9.1 million, but we know from its accounts that it paid over $157 million offshore to related entities. And Google’s numbers are even bigger. The extent of the advertising now going offshore has absolutely gutted local media and the implications of this loss of revenue for our media landscape are still being worked through.

Inland Revenue has to work through the dilemma as to how far it should go with providing information to social media companies. Ideally, you’d say it should not. But if you want to reach out to taxpayers about their obligations, you have to go where you might find those taxpayers. And at the moment that’s the social media companies.

Apple and Google lose bigly in Europe

Speaking of the big tech companies, over in Europe, Google and Apple had a week to forget. The European Union’s top court the Supreme Court of the European Court of Justice (the ECJ) ruled that Google must pay a €2.4 billion fine for abusing its market dominance of its shopping comparison service. This fine had been levied by the European Commission in 2017, and Google has been fighting it since then but has now lost in the ECJ, the highest court in Europe.

But that news was overshadowed by a major tax decision by the ECJ the same day, ordering Apple to pay Ireland €13 billion. That’s an eye watering $23.3 billion the equivalent of just over 12. 5% of Ireland’s total tax revenue for 2023.

What’s particularly interesting about this case is that Ireland was also a defendant alongside Apple. Ireland had been accused by the European Commission of having given Apple illegal tax advantages in the form of state support. The European Commission ruled the state support was illegal in 2016. Apple appealed and won in the lower court of the ECJ in 2020. But now the ECJ’s Supreme Court Justice has ruled that there was illegal state support which must be repaid.

A major transfer pricing decision

This is going to be a key transfer pricing case which will be analysed for many years to come because it revolves around the way profits generated by two Apple subsidiaries based in Ireland were treated for tax purposes. The ECJ ruled these arrangements were illegal because only Apple was able to benefit from them. Other companies based in Ireland could not.

This is just the latest instalment of the general crackdown that Europe is going through right now about transfer pricing and other profit shifting mechanisms led by the European Commission. The decision is an enormously important case in the transfer pricing world.

It actually leaves Ireland in a little bit of an embarrassing case because, as I said, it’s an enormous sum of money, so people will be naturally saying, well, what are we going to do with this? The Irish Treasury has warned against using this for anything other than perhaps a one-off major capital project or debt repayment.

But the Irish also appear to be quite concerned about how their low tax regime (they have a corporate tax rate of 12.5%) will be perceived by other companies who would like to invest in Ireland which has pursued a long-term policy of attracting investment. Its industrial strategy was shaped in the late 50s, but really only started to come to fruition once Ireland joined the European Economic Community in 1973.

I would be very interested to see how this massive decision plays out in other jurisdictions and what lessons are taken by transfer price practitioners.

GST and managed funds – round two?

Finally this week, Inland Revenue has been busy releasing a number of draft consultations on a range of subjects, including Commissioner of Inland Revenue’s search and information gathering powers, the income tax treatment of short stay accommodation, arrangements involving tax losses carried forward under the business continuity rules, and a big paper on the income tax company amalgamation rules.

However, the one that’s got me a little bit intrigued because of its back story is a consultation on the GST treatment of fees paid in relation to managed funds. If you recall back in August 2022, the then Labour government introduced a tax bill which included a measure which would impose GST on management services supplied to managed funds.

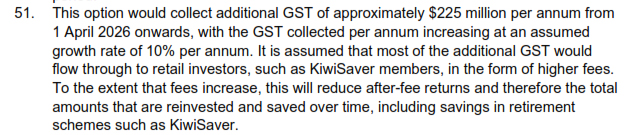

According to the supporting Regulatory Impact Statement that measure was to tidy up an anomaly that had been identified by a GST issues paper released by Inland Revenue In February 2020, just before COVID arrived. It was projected to bring in an estimated $225 million a year starting from 1 April 2026.

A furore erupted after the same regulatory impact statement noted that was according to modelling by the Financial Markets Authority, the impact of imposing GST on management fees would mean that the amount available for KiwiSaver investors would be reduced by an estimated $103 billion by 2070. For context, it’s worth pointing out that the KiwiSaver funds were projected to be valued at nearly $2.2 trillion. In an unprecedented move, Labour backed down and withdrew the bill within 24 hours.

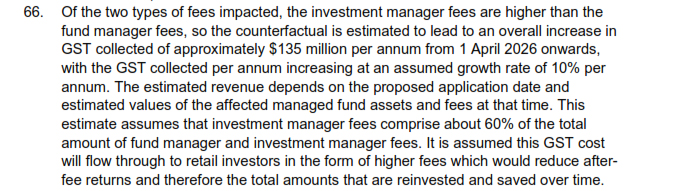

Against that background, it’s interesting to see Inland Revenue’s final consultation on the same topic. And this is where I’m intrigued to know a little bit more about what’s changed. Basically, it seems that Inland Revenue is going back to a default position where manager fees are treated as exempt, but investment manager fees become subject to 15%. The proposal in 2022 was all fees become subject to GST at 15%.

An intriguing counter-factual

What intrigues me is that the 2022 Regulatory Impact Statement noted as the counterfactual that this would probably result in something like an overall increase in GST collectible of approximately $135 million per annum from 1 April 2026 onwards. That’s not an insignificant sum of money.

Although Inland Revenue’s job is to provide interpretation and guidance, my thoughts on this are if this is a sum that’s going to potentially raise $135 million dollars of tax annually, maybe that’s something that Parliament should legislate.

There is also a subsidiary issue here which is a long-standing issue in our tax system at the moment. It is surprising, given that this was a controversial point, that this issue had not reached the courts, or that no one has taken a test case.

So, although Inland Revenue is doing its job, given the sums apparently involved I think that is something that should be put into legislation and go through the Select Committee process. But for the moment though, Inland Revenue is consulting on the issue until 25th October. As always, we will bring you any news and developments as they emerge.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.