Lessons from the largest known GST fraudster – could it happen again?

Corporate tax cuts – who benefits and what does the public think?

The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year’s tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it’s often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They’ve therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock.

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

the asset was acquired before 1st of April 2023; and

it was not acquired for the principal purpose of making taxable supplies; and

it was not used for the principal purpose of making taxable supplies; and

a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don’t pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don’t necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you’re registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called “time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn’t entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I’d like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken’s release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn’t always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there’s been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they’d have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I’ve heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

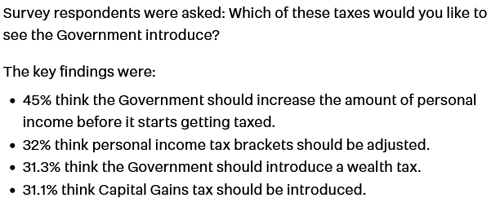

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it’s interesting to marry that along with the public’s general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Every year, the International Monetary Fund (IMF) undertake an official staff visit or mission to New Zealand as part of regular consultations under Article IV of the IMF Articles of Association. Each IMF mission speak with the Minister of Finance, Treasury officials and other persons – economists, academics and the like about the state of New Zealand’s economy and related issues. At the end of the visit the Mission then issues a short concluding statement of its preliminary findings.

The IMF will then prepare a lengthier report setting out its findings in more detail which we can expect to see in a couple of months time.

“A window of opportunity”

After noting it expects real GDP growth to rise to 1.4% for this year and then to 2.7% in 2026 the Mission noted:

“The macroeconomic environment provides a window of opportunity for New Zealand to consider broad based reforms needed to address medium- and long-term challenges, including to secure fiscal sustainability, boost productivity, address persistent infrastructure and housing supply gaps, and initiate early dialogue on population aging.”

“A comprehensive capital gains tax”

My understanding of the IMF submission is that each Mission has a different focus. This year, I understand the Mission was looking at the question of funding the future cost of New Zealand Superannuation and therefore the tax policies required. This led the Mission to call for some tax policy reforms

“Tax policy can support a more growth-friendly fiscal consolidation, and reforms aimed at improving the tax mix can help increase the efficiency of the income tax system while reducing the cost of capital to incentivize investment and foster productivity growth. Options include a comprehensive capital gains tax, a land value tax, and judicious adjustments to the corporate income tax regime.”

I expect we’ll hear a lot more about this when we see the final report.

“Initiate early dialogue”

It’s not the first time the IMF have suggested a comprehensive capital gains tax, and the Organisation for Economic Cooperation and Development has also frequently made a similar suggestion. Generally speaking, the government of the day just responds, “Yeah, but, nah”. However, the issues prompting the suggestion still don’t go away. In this particular case, the IMF suggests we need to start transitioning into a new system to cope with the rising cost of New Zealand superannuation.

“It is essential to initiate early dialogue among all stakeholders regarding comprehensive reform options that can help mitigate these challenges and other long term spending pressures from healthcare and aged care care needs with a fair burden sharing across generations. This can be further supported by KiwiSaver reforms aimed at achieving greater private savings retirement savings.”

The IMF is echoing comments myself and others have repeatedly made. We have rising costs in relation to aged healthcare and superannuation and we need to start thinking seriously about how we’re going to address those. This is a multi-generational impact. One of the unusual points about New Zealand Superannuation is it is a fully funded universal pay as you go system.

An intergenerational issue

In other words, it’s available to everyone, but it’s funded out of current taxation. I think there’s a widespread perception that some part of your tax pays for your future superannuation. It doesn’t. Tax paid by working people below the age of retirement is used to fund the current superannuation of those who have retired. The funding of superannuation is therefore a major intergenerational issue but one rarely discussed. Hence the IMF’s call to initiate early dialogue. I’ll have more on this when the IMF releases its final report.

In the meantime, whenever the IMF or OECD calls for tax reforms, the Minister of Finance of the day usually responds, sometimes in quite snippy terms. Sir Michael Cullen was wont to do so as did Nicola Willis last year. This year the Finance Minister hasn’t publicly responded to the IMF concluding statement, possibly because her attention was on this week’s Infrastructure Investment Summit in Auckland.

Foreign Investment Fund changes announced

As part of the summit, the Minister of Revenue Simon Watts has announced that there will be changes to the current Foreign Investment Fund, or FIF regime. The Government has very heavily signalled that it would do something in this space, so this is no surprise.

The proposed changes to the FIF rules include the addition of a new method to calculate a person’s taxable FIF income, the revenue account method, in other words taxing capital gains. According to the Minister;

“This will allow new migrants to be taxed on the realisation basis for their FIF interests that are not easily disposable and acquired before they came to New Zealand. For migrants who risk being double taxed due to their continuing citizenship tax obligations, this method can apply to all their FIF interests.”

This last point is of particular interest to United States citizens who face this double taxation issue, and which is turning people away. Furthermore, these changes will apply to migrants who became New Zealand tax residents on or after 1st April 2024.

More detail needed and further changes ahead?

This is a very good move but there’s a bit more detail still required. Does the reference to new residents arriving on or after 1st April 2024 mean those new residents are able to make use of this provision in the current tax year? One of the other key issues is if you do opt to be taxed on the revenue account method, what tax rate would apply? From discussions with Inland Revenue policy officials, they seem to be intending that it should be at the person’s marginal rate. Which for those on the 39% bracket would not be terribly welcome. So that’s a key design point.

The other thing of note is that Mr Watts added the Government will also be looking at how the rules impact New Zealand residents and will have more to say later in 2025. That’s interesting, because for me, the rules are quite a compliance burden in terms of calculations and have huge impact for everyone who has a KiwiSaver with overseas investments.

How to pay for New Zealand Superannuation

As noted above the IMF are looking very closely at the question of the fiscal cost of superannuation and aged healthcare which they suggest mean reforms to the tax system are needed to address those growing costs.

Coincidentally, Assistant Professor Susan St John of Auckland Business School’s Economic Policy Centre Pensions and Intergenerational Equity Hub released a working paper on New Zealand Superannuation as a basic income. This is an interesting proposal, which I know Susan has been working on for some time with the assistance of Treasury modelling.

The idea is that New Zealand Superannuation is changed into a universal basic income and treated as a grant. This allows an effective claw back mechanism to operate through the tax system. The proposal is that this claw back would generate additional revenue to help meet the cost of pensions and aged care.

The paper begins by setting out the background to the issue, the increasing demographic strains that we’re seeing. It notes that Treasury has been raising this issue for some time now, such as in its 2021 Long Term Fiscal Statement, He Tirohanga Mokopuna and speeches last year by Dominic Stephens of Treasury on the fiscal projections and costs.

Demography and migration

One of the interesting points the paper makes is although we face some financial strains ahead, because of our demographics the cost of New Zealand Superannuation will not be as high as what some nations are currently dealing with.

Incidentally, as part of their concluding statement, the IMF made a number of presentations illustrating certain areas they’re examining in more depth. One was the question of demographic pressures of superannuation, and it made the point that migration is not going to be the magic bullet some policymakers seem to think.

What about means testing?

After setting out the background Susan St John discusses the option of using means testing as a means of addressing costs. The paper looks at what happens in Australia and our own experience when New Zealand Superannuation was means tested for a while – right up until Winston Peters and New Zealand First became part of the first MMP Parliament in 1996. One of the conditions of that coalition agreement was the abolition of the New Zealand Superannuation Surcharge.

Australia tests income and assets but it’s highly complex and achieves a fiscal objective of managing the cost. On the other hand, Australia has a much more well developed long running compulsory private saving scheme, which makes what they call the Age Pension (the equivalent of New Zealand Superannuation) more of a backstop. The paper also notes that the private pension savings in Australia are more generously state subsidised than KiwiSaver.

The Australian means testing approach is very comprehensive and frankly a nightmare. The paper notes our surcharge which operated between 1985 and 1998 was highly unpopular, but it did deliver useful savings. In short, surcharges or means testing helps mitigate superannuation costs. But they are unpopular and like the Australian approach complicated to run. Furthermore, they encourage attempts to mitigate their effect.

Making New Zealand Superannuation a universal basic income

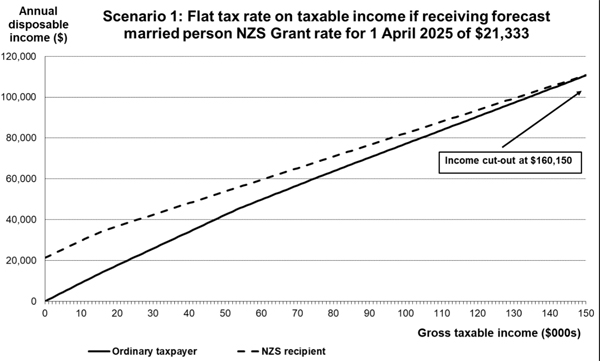

Instead, Susan proposes turning New Zealand Superannuation into a basic income, the New Zealand Superannuation Grant (the NZSG). She also suggests equalising the current different rates which currently apply depending on whether a person is in a relationship or living together, so it becomes a universal basic income for those who’ve reached the superannuation age.

As a basic income the NZSG would no longer be taxable. Instead, when a recipient earns additional income, it’s taxed under a progressive tax regime, so the tax system does the work of providing a claw back of the universal grant for high income people. The effect would be that above a certain point a person decides it’s simply not worth their while taking the NZSG.

For example with a flat tax of 40% on all other income, above $160,150 it would not be worthwhile taking the NZSG.

Another alternative would be a two-tiered rate of 17.5% for the first $15,000 of other income, and 43% on each dollar above. In this case the breakeven point becomes $151,885. A third scenario has a two-tiered rate, 20% for the first $20,000 earned and then 45% above that level. Under this scenario, the income cut out point drops to $135,000. Treasury has helped Susan with the modelling for this paper and its methodology is explained in the appendices to the paper.

15-20% savings possible?

Under Susan’s approach up to 5% of all eligible super annuitants will not apply for the NZSG because there’s no gain in it. She estimates savings could be between $2.8 billion and $3.8 billion or between 15% and 20%.

This is an interesting proposal which seems preferable to reintroducing the New Zealand Superannuation Surcharge or adopting the Australian means testing approach. I think it’s worth considering but the key thing is, as the IMF said, this is an issue we really need to start discussing now because these costs are starting to accelerate as baby boomers age.

It also seems fairer than raising the age of eligibility, which is unfair on Māori and Pasifika. There’s already a seven-year life expectancy gap between Māori and non-Māori so raising the age of eligibility for superannuation is politically difficult particularly as the proportion of the Māori population grows because of those changing demographics.

This is a worthwhile proposal which merits serious consideration as part of the ongoing debate.

This is an edited transcript of the podcast episode recorded on 14th March – it has been edited for clarity and length.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

IMF and Climate Change Commission suggest changes to the Emissions Trading Scheme are needed.

Like a never-ending Groundhog Day, every International Monetary Fund report on the New Zealand economy suggests tax reforms would promote efficiency. For example,

“There is a sense that the asset allocation in New Zealand households has a bit too much emphasis on housing versus other investments. We think a capital gains tax at the margin would help.”

That was IMF Mission Chief Thomas Helbling in 2017.

“…tax policy reforms are needed to promote investment and productivity and growth increase, increase the progressivity of income tax and mobilise additional revenue in response to long term fiscal challenges. To achieve these objectives, reforms should combine comprehensive capital gains tax, land value tax and changes to corporate income tax.”

And invariably the IMF’s conclusions are usually followed by a fairly dismissive response from the Minister of Finance of the day.

In 2002 it was the late Sir Michael Cullen responded to that year’s report: “The IMF’s credibility is not assisted by the fact that it tends to apply the same policy template regardless of the country’s circumstances”. This year Nicola Willis’s retort was “There are some things that are certain in life, death, taxes and the IMF recommending a capital gains tax.”

Associate Minister of Finance David Seymour also weighed in commenting. “I see the IMF again saying, oh, you need a capital gains tax. Every country has one. The only countries that don’t have one are New Zealand and Switzerland. But I say let’s be more like Switzerland.”

However, I’m not so sure that this was quite the zinger he hoped because as someone mischievously pointed out on Twitter, Switzerland has a wealth tax and a $59 per hour minimum wage in Geneva.

Deputy Prime Minister and former Treasurer Winston Peters was apparently not available for comment.

A de-facto capital gains tax – the bright-line test

Now, amidst all of the commentary about the IMF’s suggestions, one of the things that came up time and again is that in many ways, we do have a de-facto capital gains tax, except we don’t call it that. The bright-line test is an example of the approach that we’ve adopted, which has been ad hoc and responsive based on the government of the day’s policies at the time.

As you may recall the bright-line test was brought in with effect from 1st October 2015 by the National Government and it then applied to disposals within two years. In March 2018 the Labour Government introduced a five-year period and in 2021 it was increased a 10-year period. And so, a quite confusing scenario has developed as to which bright-line test applies because some of the exemptions have changed over time as well, particularly in relation to the main family home.

In one way, therefore, the reduction of the bright-line test back to two years again from 1st July is to be welcomed because it is clarifying and simplifying what has become an incredibly complicated area.

Tax Red Flags: More than just the bright-line test to be considered

The bright-line test and taxation of land has plenty of red flags when together with the excellent Shelley-ann Brinkley and Riaan Geldenhuys and moderator Tammy McLeod, I made a presentation about tax red flags on Tuesday to the Law Association. (Formerly the Auckland District Law Society). My thanks again for the invitation to present and to my excellent co-presenters, we had a very lively session talking around this.

In short when you drill into our current land taxation rules, they are very incoherent. The bright-line test is a backup test. It applies if none of the other land taxing provisions apply. And this is something that tripped up people before the bright-line test was introduced and will continue to do so even now it’s been reduced down to two years.

For many people, the particular issue to watch out for is the question of subdivision. If you own a property and undertake a subdivision within 10 years of acquisition it may still be caught under the existing rules, outside of the bright-line test. And in some cases, you may be caught by the combination of the provisions with the associated persons test which deem transactions to be taxable if at the time you acquired the land you were associated with the builder, dealer, or developer in land.

Sometimes the tax charge can be triggered way past the 10-year timetable since acquisition. That’s particularly the case in relation to a disposal of property where building improvements have been carried out. That particular provision, section CB 11 of the Income Tax Act, deems income to arise if a person disposes of land and

“within 10 years before the disposal”, the person or an associate of the person completed improvements to the land and at the time the improvements were begun, the person or an associated person carried on a business of erecting buildings. Note, the reference to “within 10 years before the disposal.” So, you may have owned that land for considerably longer than 10 years and yet still be subject to the provision.

Just a pro tip for anyone thinking ‘Great, with a two year bright-line test coming in, I can now sign a sale and purchase agreement, make sure settlement takes place after July 1st and it’s not going to be subject to the bright-line test.’ That’s not the case. The sale point for the bright-line test in that case is when the sale and purchase agreement is signed and not when settlement happens. I had at least one client get caught by that very provision because they went for a long settlement thinking that got past the two year period. It didn’t, and it is another case of always seek advice on transactions involving land, because as I’ve just outlined, the provisions are complicated.

Could a capital gains tax be ‘simpler?’

And this was the point we reinforced during our seminar. There is a lot of complexity already in our tax system around the taxation of land and in my view, in some ways a capital gains tax would actually clear away a lot of that uncertainty. It’ll become clearer that, broadly speaking, if you buy something, and you sell it subsequently, any gain will be taxable.

Now, how the gain is calculated and the rate at which it’s taxed are two different things. But often in the debate around the capital gains tax, those two things get conflated to run as an argument against the taxation of capital gains.

In my view, the point still remains that we have a confusing hotchpotch approach to taxing capital gains and at some point, grasping the nettle with a CGT as suggested by the IMF and also the OECD, would ultimately perhaps be a better approach.

Incidentally, doing so would be consistent with the well-established principle we have of the broad-based low-rate approach. There’s nothing to say that by broadening the tax base, we could not hold tax rates at current levels or even lower. Bear in mind that the when the last tax working group recommended the capital gains tax, it was intended to keep to help keep the top tax rate at 33%.

Watch out for trustees on the move across to Australia

One of the other issues that came up in our Tax Red Flag Seminar was the question of trustees, and beneficiaries and settlors moving cross-border, particularly to and from Australia. That is something all three of us are seeing quite a bit of and it is something to watch out for as a key red flag.

The IMF on how to tax wealth

If there is a certain repetitiveness to the IMF’s discourse about taxing capital, it’s part of a global discourse on the topic. Earlier this month the IMF released a How to Tax Wealth note. These how to notes are “intended to offer practical advice from IMF staff members to policy makers on important issues.” And this this was a very interesting read as you might expect.

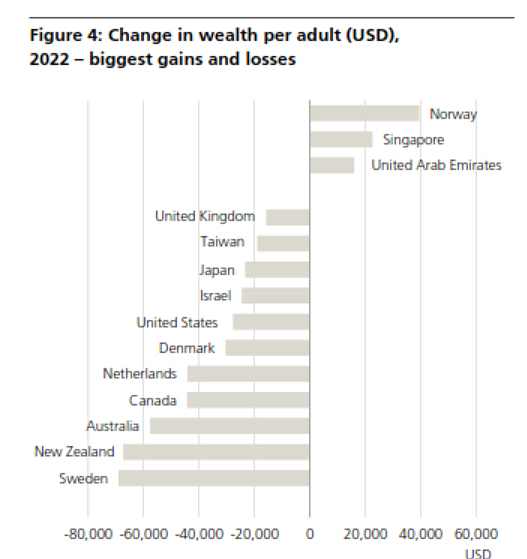

The IMF’s How to Tax Wealth note neatly coincided with the release of the UBS/Credit Suisse, Global Wealth Report for 2023. According to the report, in 2022 New Zealand ranked sixth in the world with an average wealth of US$388,760 per adult. On the basis of median adult wealth per adult, again in U.S. dollars, we ranked 4th behind Belgium, Australia and Hong Kong, with a median wealth of US$193,060.

Incidentally, these rankings were after a very sharp fall from 2021 levels, where New Zealand was only behind Sweden in the biggest loss in wealth per adult.

I am genuinely very surprised to see New Zealand rating so highly for both average wealth and median wealth. On the other hand this Credit Swisse/UBS report is another example of why there’s a great debate going on around the taxation of wealth not just here, but globally.

And this IMF How to Tax Wealth note is instructive in its approach. It starts by making a very obvious point, how much to tax wealth is a distinct question from how to tax wealth. The note argues that:

“returns to capital generally should be taxed for equity and possibly efficiency reasons. and that in many countries, wealth inequality and better tax enforcement strengthen the case for higher effective taxation than in the past.”

Now the IMF doesn’t make any particular proposal about a specific level of tax, the note is basically about ‘here are things you should consider.’ But on the question of wealth taxes, it does come down pretty much against them noting,

“Improving capital income taxes tends to be both more equitable and more efficient compared with replacing them with net wealth taxes. Countries hence should prioritise improving capital income taxation over considering the introduction of wealth taxes”.

Then it talks about – in terms of strengthening capital taxes – addressing loopholes, notably the under taxation of capital gains in many countries. There’s a passing comment, that perhaps you can use a one-off net wealth tax or maybe apply it to very, very high wealth levels.

Time for inheritance tax?

But the Note also concludes “taxing capital transfers through gifts or inheritance provides another opportunity to address wealth inequality.” The IMF comments that the efficiency costs of such taxes are modest, and notes that “inheritance taxes are better aligned with redistribution than estate taxes, since exemptions and rate structures can account for the circumstances of the heirs.”

What really makes the New Zealand tax system unique is not the absence of a capital gains tax because, as David Seymour pointed out, other countries don’t have that, namely Switzerland. It’s the complete absence of taxes on the transfer of wealth, which has been the case now since 1992. That’s what makes New Zealand unique – we have no general capital gains tax together with no estate or gift or wealth taxes.

And this is an area where I think a lot more consideration needs to go into because as the IMF noted, we’ve got fiscal challenges ahead, and where might the revenue be raised from to meet those challenges.

The IMF and Climate Change Commission suggest changes to the ETS

And finally, back to the IMF again. It concluded its mission report by noting that “New Zealand’s ambitious climate goals call for major reforms,” and it referenced the Emissions Trading Scheme, having helped limit net emissions by encouraging robust reductions and removals, particularly from afforestation.

But the IMF then went on to say that “significant reforms” are going to be needed to meet domestic and international targets, and these include reducing the number of available units in the ETS, pricing agricultural emissions and strengthening the incentives for gross emissions reductions within the ETS. The IMF finally note that given the ambition of New Zealand’s first nationally determined contribution under the Paris Agreement, the use of international mitigation i.e.; buying credits from offshore, is likely to be required.

Now the IMF report was a week after the Climate Change Commission, and pretty much said the same thing, and advised the coalition government they should halve the number of ETS units on offer in each of the next six years. The last ETS auction did not go brilliantly. That has a flow on effect in that by reducing the amount of income from emission trading unit sales, it’s going to limit crown revenue for tax cuts.

Vale Rod Oram

It’s interesting to see a confluence of opinion happening here and an appropriate time to remember the late Rod Oram someone who was a very strong environmental journalist. I was fortunate enough to know him all too briefly after we met at a panel discussion. We’d planned on him appearing as a guest on the podcast. Sadly, with his passing that will never happen now, and our thoughts go out to his family and friends.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

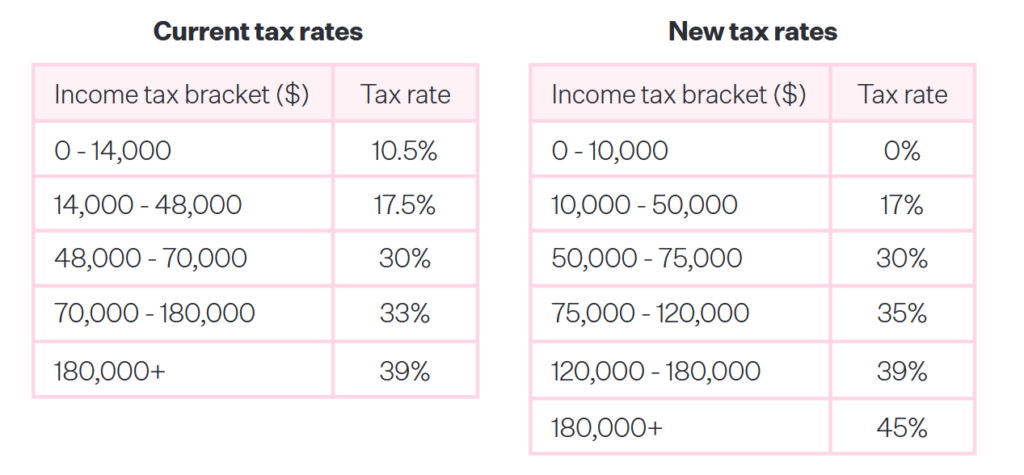

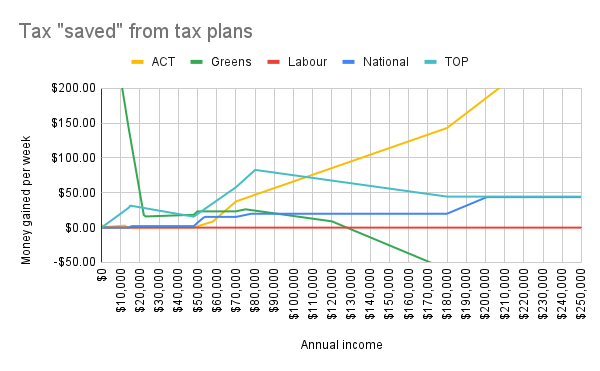

The Greens announced their tax proposals a week ago, last Sunday.

And my reaction was, “These are very bold.” They proposed major tax cuts at the lower end, meaning 95% of taxpayers will be better off under the Greens. Those cuts are paid for by increasing the top tax rate to 45% and increasing the 33% tax rate to 35% as well. These increases are part of the trade-off for the proposed nil rate band of $10,000, which no doubt will be very popular. As is well known, many other jurisdictions have something similar and given the fact that nothing has been done in relation to indexation of thresholds for well-nigh 13years now, it’s unsurprising that the pressure is built up, particularly at the lower end, to change the tax rates.

But most of that got swept away by the Greens controversial wealth tax proposal. In summary, there are two parts to it. Any individual whose net assets, net of mortgages for example, exceed $2 million will be subject to a wealth tax of 2.5% on the excess. For family trusts there is no nil rate band or threshold at all. It’s a flat 1.5% which is a deliberate anti-avoidance mechanism.

Latest Inland Revenue data on trusts

Trusts were used to avoid the impact of estate and gift duties in the past and are used in other jurisdictions to mitigate the impact of wealth and estate duties. So, the Greens have targeted this avoidance. Coincidentally, last Saturday the New Zealand Herald published a piece including details of the trust tax return filings made to Inland Revenue for the year end 31st March 2022 which indicated the value of assets held in trusts. The net assets of the 201,100 trusts which reported, was just over $300 billion. So at 1.5%, theoretically that’s $4.5 billion dollars straight up there.

Incidentally, what that Inland Revenue report doesn’t show is the non-reporting trusts, those are likely to be quite significant. We really don’t know how many trusts there are in New Zealand, the best estimates are somewhere between 500,000 and 600,000. Many of the non-reporting trusts don’t do so because they have no income, but they hold assets such as the family home. So, family homes that have been held in trusts may now be subject to the Greens’ proposal.

Now this kicked off quite a storm, which I watched with a little bemusement because the Greens first of all have to put themselves in a position of such leverage that its coalition partners, almost certainly Labour and Te Pati Māori, agree to the proposal. And then somehow between 14th October, the date of the election, and 1st April next year, the legislation to introduce all of this is drafted and passed through Parliament. So ,it’s a big challenge ahead.

But it caused quite a stir, and I fielded several calls from people concerned about what they saw here, trying to get an understanding about it and my views on it. At our Accountants and Tax Agents Institute New Zealand’s regional meeting on Tuesday we had a very lively debate around the question of this wealth tax. Normally, a lot of the time we’re talking about what’s in the legislation and whether Inland Revenue ever answer their phones again. All this I think shows the impact of the proposals, even though in theory they affect only a small group of people, the top 1%.

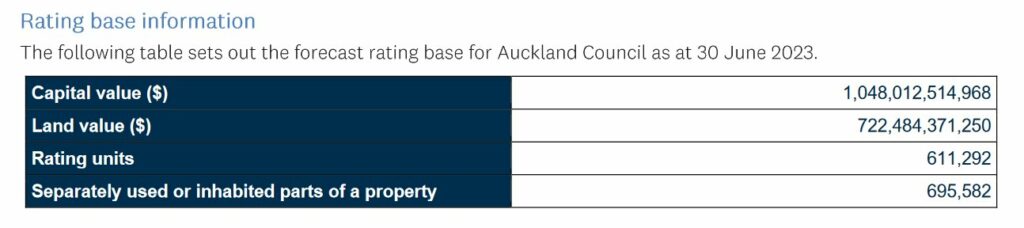

But there is substantial wealth locked up in property. We know that from digging around the official figures. For example, Auckland Council estimates the rateable value for all property within the Auckland Council region will be over one trillion dollars as of 30th June. Obviously, not all of those would be subject to a wealth tax.

What’s being suggested by other parties?

But I thought it was interesting that people are taking the Green’s proposals very seriously. The income tax shift to 45% on income over $180,000 won’t be terribly popular. But at present, the proposals that they’ve put out for the income tax cuts would affect many more people and benefit many more people, all those earning under $125,000, which is something like just over 4 million people. This has a broader impact than either National or Act’s proposals.

It’s quite interesting now as the election comes ever closer, we can start to see the tax policies of the various parties taking shape. The Greens are raising a substantial amount of tax to deal with poverty. Act is proposing tax cuts and it’s taking the ideologically opposite approach of substantial cuts to spending in order to achieve its top rate of 28%.

TOP, The Opportunities Party, are putting out a policy which has a land value tax, and they also propose tax increases at the higher end together a nil rate band and also substantial tax cuts at the lower end.

We haven’t yet heard from Labour on what they would do. Over on Twitter @binkenstein put together a graph comparing the various parties’ proposals so far.

So, the debate has ramped up quite a bit. Obviously, the Greens wealth tax is the most controversial part of it, but the other part which really got very little commentary but is equally controversial, was a proposal to raise the income tax rate for companies from 28% to 33%. More than most of the Greens’ proposals, that would probably produce a certain frisson of tension amongst multinationals. They may look and think “Maybe we might not increase our activities in New Zealand” or they may ramp up what they try and do under profit shifting.

Anyway, it all made for a very lively discussion all round. As I told people, wait and see. But it is interesting to see the pressure point for those are likely to be affected around a wealth tax.

What does the IMF think?

With almost impeccable timing, the IMF, the International Monetary Fund, were in town and it suggested that maybe it was time for a capital gains tax.

The Concluding Statement of the 2023 Article IV Mission noted:

Well-designed tax reform could allow for lower corporate and personal income tax rates by broadening the tax base to other more progressive sources, such as comprehensive capital gains and land taxes, while also addressing fiscal drag and improving efficiency.

It’s not the first time the IMF has suggested changing the tax system. They did so in 2021. In fact, there’s a regular pattern of the IMF and/or the OECD coming here looking around saying, “Well, guys, the country is in good shape, generally government policy is pretty sound, but you need to do something about capital gains taxes.” Regardless of whichever party is in power the Government’s reaction is quite funny. They like the bit about everything being under control. But at the mention of capital gains tax, they all throw up their hands in horror. And yet, as we know all around the world, capital gains taxes are a common feature of tax policy.

The Crypto-Asset Reporting Framework, the latest expansion of the Common Reporting Standards

Now, the Greens wealth tax proposal will probably be music to the ears of the French economist Thomas Piketty, who has proposed a global wealth tax, as one of the core points of his monumental work, Capital in the 21st Century. And at the time of publication in 2014, the opportunities for that global wealth tax to ever eventuate were probably just about zero or maybe marginally above zero.

But since then, we’ve had the introduction of the Common Reporting Standards which I think is actually revolutionising the tax world quietly because an enormous amount of information sharing is now happening on. We know from what’s been reported under the Automatic Exchange of Information that there’s something like €11 trillion held in offshore bank accounts. The Americans have got their FATCA, the Foreign Account Tax Compliance Act, and as a result of that, they know that American citizens have got maybe US$4 trillion held offshore.

Now, the latest part of the Common Reporting Standards is extending the framework to crypto-assets and I talked about this last year when the proposals first came out. Those proposals have now been finalised and the Crypto-Asset Reporting Framework is now in place. There have also been some amendments to the Common Reporting Standards. I’m going to cover all these changes in a separate podcast because I think they’re worth looking at in a bit more detail.

The tightening noose of information exchange

But the key trend in international taxation that’s going on, which I think is going to have a long-term impact around the world, and particularly for tax havens, is this growing interconnectedness, the sharing of information that goes on between tax authorities through mechanisms such as the Common Reporting Standards. I asked Inland Revenue about what information they had been supplied under the CRS in relation to the numbers of taxpayers and the amounts held in overseas bank accounts. Inland Revenue turned down my Official Information Act request on the basis that much of this is obviously confidential, but also would be compromising to the principles under which the information is shared.

Now, I’m not entirely sure about that. I think the more openness we have about what is being shared, the better the likelihood of tax enforcement once people cotton on to what’s happening. They will not think “Yeah, well, I’m just going to leave it over in the UK or the US or wherever, and Inland Revenue will never find out.” My view, as I tell my clients, is they always find out and they know much, much more than you can imagine.

And outside of the CRS there appears to be a regular exchange of information about property purchases between the United States Internal Revenue Service and Inland Revenue here. So be advised, the Crypto-Asset Reporting Framework is just the latest in a building block of international information exchange.

The Auckland Budget – what about climate change?

And finally, the Auckland budget got signed off last week. I’ve been in the press disagreeing with the sale of any part of the Auckland airport shares, and I still stand by that. I think it’s a short-term fix for a long-term problem, but that’s now done and we move on.

What I did think was quite surprising as you delve into the budget is some of the numbers that come out. As I mentioned earlier, the rating base for Auckland and according to the Auckland Council’s documents is over $1 trillion.

But the thing that really surprises me, which wasn’t addressed in the budget so we’re going to have to address it next year, is the question of climate change. Towards the end of the process, the Government announced that in the wake of Cyclone Gabrielle 700 homes around the country are too risky to rebuild. The Government and councils will offer a buyout option to those property owners.

400 of those are in the Auckland region and apparently it doesn’t also take into account what is going to have to happen out at Muriwai because of the slips and the dangerous cliffs over there. As Deputy Mayor Desley Simpson pointed out, “If you say it’s 400 [Auckland homes] times $1.2 million, give-or-take just like the average house price, you’re talking half a billion dollars.”

The question arises how is that split between Auckland ratepayers and the rest of the country? Yet there was nothing in the Auckland budget about this, and that’s just this year’s damage. What happens if we get another Cyclone Gabrielle, next year?

We’ve got an interesting scenario developing where we’re talking about reducing emissions and we’ve got a distant horizon 2030 or whatever farmers and other parties want to extend it to. But in the meantime, we are picking up the bill now for increased damage and we don’t seem to be thinking in terms of how does that affect our taxes and rates? And this is going to be an ongoing issue. So, the question of paying for that, whether it’s a wealth tax, capital gains tax, whatever, is going to become ever more present, in my view.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week Inland Revenue issued a press release warning real estate agents that this was an area that its analysis “suggests real estate salespeople/agents commonly claim a high level of expenses relative to their income. Inland Revenue believes the issue is widespread and we must act. People are claiming private expenditure, but not keeping logbooks or other business records to support the claim.”

The release goes on to warn that if someone has over-claimed expenses in Inland Revenue’s view, “they will receive a letter from us requesting they prove the expenses claimed.”

Now, this is a little bit unusual from Inland Revenue because we haven’t heard anything in the grapevine that this was something they were looking at. But it is not entirely surprising because one thing that emerged from hearing the Commissioner of Inland Revenue speak at the excellent Accountants and Tax Agents Institute of New Zealand conference is that Inland Revenue has great faith in its Business Transformation systems. These give it the ability to analyse data and identify areas where it believes income is either being under declared or in this case, taxpayers are, shall we say, being overly generous in their calculation of the deduction available.

Although, as I mentioned, we haven’t previously had an indication Inland Revenue viewed this as an issue, it’s apparent from what they’ve said here, that they’ve done enough preliminary work to identify that expenses being claimed by real estate agents seem high relative to income.

In one way I think this is a positive development in that Inland Revenue by warning people what it can do, can clear out some of the chaff.

On the other hand, there’s a lack of specific detail in this press release which concerns me. It’s “We think there’s an issue, but we haven’t actually specified what particularly is concerning us”. And simply to say that people claim a high level of expenses relative to their income is to assume that that expenses automatically should follow income. It could well be that there is a fair amount of baseline expenditure that people would incur in this business, running around making phone calls, driving to see clients and the like sometimes without actually a great deal of success, as the real estate sector is largely commission only based.

And so one of the things that taxpayers perhaps should consider is the implications of Inland Revenue’s capability to do a great deal of analysis. One thing Inland Revenue could do is to start saying, “Well, here is a standard deduction. You can claim X amount which to we’re going to accept as deductible without the need to keep very detailed records because our indication is that is likely to be the level of expenditure you would incur in your business.”

Now, Inland Revenue will come straight back and say they don’t want to do that because people will abuse that. But on the other hand, you’ve got to wonder the benefit of the current approach when you consider the time and energy put in by people preparing their tax returns and also the effort Inland Revenue then spends investigating what may well turn out to be an entirely legitimate expenditure. Maybe just simplifying matters all around would be more efficient.

It could be yes, there could be some seepage around the edges under a different approach and Inland Revenue doesn’t get as much as it could do if the rules were applied correctly. But applying a so-called standard deductions approach deals with an issue in the tax system, in that compliance is particularly onerous for smaller businesses. The rules are written around the expectation that people have a good understanding of the law and have the systems to manage their accounting and recording income and expenditure. And with the advent of online accounting systems such as Xero and MYOB that’s largely true.

But not everyone wants or needs to spend money on accountants. And I have felt for some time that adopting a different approach to what we call micro businesses, that are businesses with a turnover of say, less than $100,000, dollars would actually benefit everyone. Make it easier to comply and encourage more people to comply.

Anyway, we’ll watch with interest to see how this plays out with Inland Revenue. As I said, I’d like to see some more specific examples of the abuse that they are clearly warning against. But until some cases hit the courts or Inland Revenue releases some more information on the matter, we’ll just have to wait and see. In the meantime, it’s a good warning for anyone involved in business that you have to keep accurate records of your business expenditure.

The IMF wants tax action on overheated housing market

Moving on, the IMF, the International Monetary Fund, has waded into the debate over housing by recommending the Government should introduce a stamp duty or a more comprehensive capital gains tax to help deal with the overheated property market.

This is part of a routine check on the New Zealand economy, what’s called the Article IV discussions. These happen periodically when IMF staff come down here, talk to Treasury and other officials and draw their own conclusions on the state of the New Zealand economy and areas for improvement.

The Government will not welcome the call for a capital gains tax or stamp duties. We haven’t had stamp duties in nearly 30 years now, but they are used a tool used elsewhere. They’ve fallen out of fashion here because they are regarded as economically inefficient taxes, and there are concerns that they increase costs for purchasers. So as a means of helping first home buyers, a stamp duty isn’t necessarily going to be a great approach according to theory.

But for those who’ve read Tax and Fairness, the book I co-wrote with Deborah Russell MP, you’ll know that in chapter four, we talked extensively about how the IMF is not the first organisation to have raised the need for a capital gains tax to deal with housing inflation. The OECD raised the idea way, way back at the start of the century in November 2000 and then again in 2011, and the IMF also made similar suggestions back in February 2016.

I was going to say it’s really quite remarkable how this issue keeps popping up, but actually it’s not because the issues around tax were identified decades ago but have not been addressed. And meantime, the pressure on the Government builds now that the housing market has accelerated again. And this week (Tuesday) the Government will announce some proposed disincentives for property investors to try and reduce demand in the sector together with some form of targeted incentives to encourage savings in other sectors.

Just a little note on this, way back in 2000 the OECD concluded there was substantial overinvesting in housing, maybe one and a half times greater than that of major OECD countries. Now, I imagine that number has actually become considerably worse. So, as I’ve said before, the capital gains tax debate is not going to go away.

And on that debate, this coming Thursday, March 25th, I’ll be on a panel alongside Geof Nightingale of PWC and the Tax Working Group and Paul Dunn of EY together with Craig Elliffe and Julie Cassidy from Auckland University. Our topic is “Taxation: the ticking time bomb of our generation. Four tax questions for 2021”. This is an event run by the New Zealand Centre for Law Business I have no doubt whatsoever we will be talking about the issue of capital taxation.

End of year prep

And finally, more on one specific issue which will require action before 31st of March, and that is the question of overdrawn shareholder current accounts.

Now, this happens when a director or a shareholder of a company takes out more in cash from the company during the year. This is traditionally treated as drawings. So, prior to year-end, we take a look to see what we can do. And most times we deal with this issue by either paying a dividend before year-end (a particularly important thing to do this year before tax rates increase on 1st April) or voting a shareholder employee’s salary.

But in some cases, that is not enough. And in those situations, a company is required to charge interest using the FBT prescribed rate of interest. Now this rate is regularly adjusted and generally reflects what’s going on elsewhere in the market. Until 30th June 2020, the rate was 5.26%. It was then reduced to 4.5%, the lowest rate I can recall. This is the rate that should apply from 1st July 2020 right through until 31st March 2021.

But from 1st April the rate increases to 5.77%, something that has slipped under the radar and possibly reflects Inland Revenue unease about the use of current accounts to get around higher tax rates. On the face of it a rate increase in this low interest economy seems anomalous.

But as I said, I think it reflects Inland Revenue concern about the use of an overdrawn current account to get around income being taxed at either 33%, or from 1st of April, 39%. In some other jurisdictions the amount of an overdrawn current account is treated as a dividend. Our rules treat only require charging of interest. So if you’ve got an overdrawn current account of $100,000 in Australia, that’s going to be taxed as income of $100,000. Here we apply the FBT prescribed rate of interest of 4.5% so the taxable income is just $4,500.

So you can see there is some form of incentive to make use of overdrawn current accounts. In fact Inland Revenue has started paying a lot more attention to this issue and this small but quite subtle and unnoticed rate increase in the prescribed rate of interest is probably a clue it is planning to take greater action on the matter.

Well, that’s it for today, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week Ka kite ano!