the winners of this year’s Tax Policy Charitable Trust Scholarship are announced.

A preview of next week’s United Kingdom Budget.

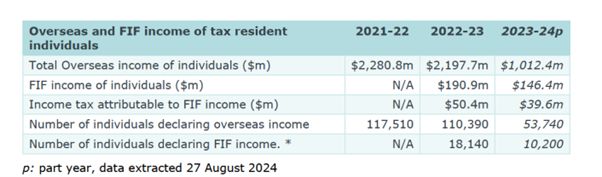

Inland Revenue regularly releases Official Information Act requests that it has answered. One from last month was in relation to the amount of overseas income reported by individuals. My attention was first drawn to this OIA by Robyn Walker of Deloitte (thanks Robyn) who like me, and many other professionals were quite surprised when we saw the number of people reporting Foreign Investment Fund (FIF) income.

Is there under-reporting?

According to Inland Revenue, which only really started gathering exact data on this in the 2023 income year, 18,140 individuals reported a total of $190.9 million of FIF income for that year.

When you consider that based on the latest Census 28% of the population of New Zealand were born outside the country, it seems to me that the amount of overseas income being reported, and in particular in relation to FIF income, is probably below what we would expect to see. And that’s what caught Robyn’s eye. One or two other advisors have made the same comment.

It could be because we deal in this space, there’s a bit of an echo chamber effect because we will regularly advise on these matters. If we’re dealing with a fairly high proportion of overseas migrants, and our practise Baucher Consulting does, then it’s natural we might think there is a broader scale of overseas investments generally.

But the number seems incredibly low in relation to the FIF income being reported, and also generally speaking, when you think about the number of overseas persons declaring overseas income.

A question of non-compliance

The issue therefore arises as to whether in fact we have non-compliance happening. I raised my concerns about this with Jenny Ruth of Good Returns. In our practice we regularly encounter clients coming to us who have realised that they have not been compliant with the Foreign Investment Fund regime. In some cases, they’ve come to us on another matter and in the course of discussions, it’s emerged that they have not been compliant. At any one time we are usually filing disclosures and bringing tax returns up to date.

Complexity and non-compliance

In my view this possible level of non-compliance speaks to the complexity of the Foreign Investment Fund regime. It’s not a capital gains tax, it operates as a quasi-wealth tax. That’s how I describe it to taxpayers and whenever I’m speaking to overseas advisors on the matter.

Old habits die hard

The FIF regime is not intuitive and I’m often dealing with people who come from overseas jurisdictions which have capital gains tax. They’re aware that where there’s a disposal there is a tax point that’s triggered. This may seem strange to say, but I’ve found in my practise that people’s tax habits developed in their country of origin take long to die even after many years in New Zealand.

Now, coincidentally, just to give some idea of the complexities involved in the FIF regime, Inland Revenue has just released a draft interpretation statement for consultation on the income tax issues involved in using the cost method to determine FIF income.

The Cost Method and the FIF regime

Those who have investments within the regime will be familiar that a fair dividend rate of 5% will apply to the value of your Foreign Investment Fund interest as of the start of the tax year. The alternative is to look at the total realised and unrealised gains of your portfolio including dividends over the year and report that instead, if that’s the lower amount. Incidentally that option way is not available for KiwiSaver funds or for the New Zealand Super Fund which is why it’s regularly one of the largest taxpayers in the country.

But what happens if your FIF interest is unlisted? The cost method generally applies when an investor is holding shares in an unlisted overseas company. And so this interpretation statement explains when that cost method may be applied and how it operates. As is now common, there are lots of examples and flow charts which explain the process. But the fact that there’s an interpretation statement on this matter which has set out and explains when you can or cannot use it the methodology, speaks to the complexity of the regime, and also the compliance costs involved in this.

The cost regime is generally to be used when the values of shares are not readily available. As part of that it will require the taxpayers to find and obtain an initial market value of the overseas stock, so they have a base cost for the purposes of the FIF calculations. It’s possible in some circumstances to use the net asset value of the accounts, usually if those accounts are audited.

Practical problems with the FIF regime

But as can be seen when people are required to obtain independent valuations this means additional compliance costs in what is already quite an involved regime. The other reason why the FIF regime causes consternation amongst taxpayers is the tax liability is not based on cash flows. A tax liability arises under the FIF regime even if the company in question is a growth company and not paying any dividends. Earlier this year I discussed a reportThe place where talent does not want to live, about the issues the FIF regime creates for startup companies and New Zealand resident investors.

All of this just underlines the complexities of the FIF regime. As I told Jenny Ruth of Good Returns, whenever I hear someone arguing “Oh well, capital gains tax is very complicated” I immediately think, ‘Well, they’ve clearly never dealt with the Foreign Investment Fund or financial arrangements regimes.’

Complexity leads to non-compliance?

Anyway, the upshot of all of this is there’s probably a considerable amount of non-compliance happening in in relation to reporting of FIF income. And Inland Revenue are now cracking down on this by making use of the information now available to them under the Common Reporting Standards on the Automatic Exchange of Information.

Now this is an OECD information sharing initiative which started in 2017. Inland Revenue which started a compliance project in late 2019 using this data. But then Covid turned up so that project had to be parked but it has now been reinitiated. As a result, I’ve recently taken on clients contacted by Inland Revenue advising it has received information under the Common Reporting Standards. The clients have been asked for an explanation about their apparent non-disclosure of overseas income and ‘invited’ to make the relevant income disclosures.

Keep in mind also that in the May Budget Inland Revenue was given $116 million over the next four years for investigation activity. The upshot is we’re probably going to see a lot more disclosures about FIF income when we’re looking at the numbers for the 2025 year.

In the meantime, I urge readers and listeners to consider their position and check with their tax advisor if they think they may have investments within the Foreign Investment Fund regime and have not made the disclosures they should have.

And the winners are…

Now moving on, the winners of this year’s Tax Policy Charitable Scholarship were announced in Wellington on Tuesday night. The Tax Policy Charitable Trust was established by Tax Management New Zealand and its founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa New Zealand. Three of this year’s finalists, Matthew Handford, Claudia Siriwardena and Matthew Seddon have appeared on the podcast over the past few months discussing their proposals.

The format for Tuesday night was that the four finalists, having already prepared a 4000-word final submission, would then present their proposals to a judging panel and the audience, as part of a Q&A.

The judging panel consisted of Joanne Hodge, who’s a former tax partner at Bell Gully and a member of the last Tax Working group. Professor Craig Elliffe Professor of Law at the University of Auckland and another member of the last Tax Working Group. Nick Clark, Senior Fellow of Economics and Advocacy at the New Zealand Initiative and Chris Cunniffe, Strategic Advisor of Tax Management New Zealand. A pretty daunting panel to be frank.

According to Chris Cunniffe “the quality of the presentations on Tuesday night was exceptionally good” and in the end the judges were unable to separate Matthew Seddon and Andrew Paynter.

Winners Andrew Paynter (left) and Matthew Seddon (right) with the judging panel

Matthew’s proposal, is to extend withholding taxes to payments received by independent contractors.

Andrew works as a policy adviser in Inland Revenue. His proposal is to increase the GST rate to 17.5% and introduce a GST refund tax credit for lower and middle income individuals. This would be a means tested individualised credit and would be paid at a flat rate to all qualifying tax resident individuals under a particular income threshold. It’s a fascinating proposal and I’ve reached out to Andrew about appearing on the podcast in the near future.

In the meantime, congratulations to the winners Andrew and Matthew and also to the runners up Claudia and Matthew Handford. Don’t be surprised if you see something popping up in legislation in the near future involving one or more of these proposals. They were all of a very high standard this year, so well done everyone.

UK Budget preview

And finally this week, a brief preview of next week’s UK budget. The new Labour government has been in office now for three months and it’s finally getting around to announcing its first budget. That is part of what they call the Autumn budget statement.

The UK has two budget statements a year, but this one is going to be quite significant because there’s a lot of noise and chatter around tax changes. A quite significant part of my practice at the moment is advising New Zealanders going to the UK, and migrants coming here, and the tax implications involved.

I’m therefore watching this budget with some interest because we know there are going to be two proposals, the final details of which will come out, which will have an impact for quite a number of people. Firstly the so-called foreign income and gains exemption, which is the UK equivalent of our transitional resident’s exemption. This was first announced by the Conservatives in their Spring budget in March this year, but then the General Election happened so full details of the proposals were not released.

Related to that, and this is surprisingly important for a large number of people, are changes to the domicile regime also announced by the Conservatives. At present domicile is incredibly important for determining a person’s liability for UK inheritance tax, which is payable at 40% above net assets over £325,000. It appears the UK will move to a more residence-based regime, but we don’t yet know the details.

I’m therefore watching this with great interest and there are bound to be other measures which are likely to affect New Zealanders going to the UK, or the UK migrants moving here. We’ll therefore keep you abreast of developments in next week’s podcast.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Matthew Seddon suggests imposing withholding taxes on organisations that engage independent contractors, including through electronic marketplaces

My guest this week is Matthew Seddon. Matthew is a lawyer at Bell Gully and one of the four finalists for this year’s Tax Policy Charitable Trusts Scholarship competition. He has suggested extending the withholding tax regime to include more independent contractors. Kia Ora Matthew, welcome to the podcast. Thank you for joining us. So how did you get into this and where did your proposal come from?

Matthew Seddon Hi, Terry, thanks for inviting me onto your podcast. It’s great to be here. The Tax Policy Scholarship provides young tax professionals with the ability to set out a proposal for a significant reform in the New Zealand tax system. My proposal is to extend PAYE withholding to independent contractors engaged by persons with an existing PAYE withholding obligation, i.e. employers, and also to those independent contractors engaged through an electronic marketplace.

TB Those electronic marketplaces try and match buyers and service providers. You picked up on something from the Tax Working Group in this space, is that right?

Matthew Seddon Yes, the Tax Working Group in 2018 had identified the rise of self-employed independent contractors as the most likely and most significant challenge facing the integrity and sustainability of the New Zealand tax system. The Tax Working Group’s final report had noted that withholding taxes should be extended as far as practicable in order to ensure greater levels of compliance. Furthermore, the Government’s recent focus on increased compliance activities is another reason which prompted me into this proposal.

TB Yes, because Inland Revenue got $29 million a year. I think they were saying they’re expecting a $700 million return on that. Is that right?

Matthew Seddon Yes, the $29 million I think is over each year and I think $116 million is set across for the four-year period. So their expectation is to raise $702 million over a four-year period from those increased compliance activities. Inland Revenue has also been stating recently that they’re going to focus on taxpayers who have not been complying with their tax obligations. Especially in the hidden economy.

TB Like I was saying the other week, the hibernating bear has woken up and it’s hungry and it’s making moves. Yes, I mean just picking up on that, the Performance Improvement Review recently released on Inland Revenue was quite interesting in its discussion around the tax gap, which the Tax Working Group fenced around a little but didn’t really go into specifics. But this is the area, right on scope of the tax gap, isn’t it?

A billion dollar gap?

Matthew Seddon Indeed, and Terry, just for listeners to understand, the tax gap is the difference between what Inland Revenue should receive in taxes if all taxpayers are fully compliant with their obligations compared to what tax they actually receive. The Tax Working Group had received some research that was commissioned by Inland Revenue on the tax gap for independent contractors, and that research indicated that independent contractors were under reporting their taxable income by about 20% on average. This was resulting in a loss of revenue of $850 million a year.

TB And that’s in 2018 dollars. So now we’re talking potentially over a billion dollars per year.

Matthew Seddon Exactly.

TB Well, if I was Nicola Willis, I’d be very interested in that because that’s a quarter of a percent of GDP. It’s actually a significant number now. So how does your proposal work?

Matthew Seddon So my proposal looks at imposing withholding taxes on organisations which engage significant numbers of independent contractors. For example, a large number of independent contractors operate through electronic marketplaces. A lot of employers engage independent contractors. So it’s by centralising the withholding obligation and imposing it on employers and electronic marketplaces instead of the numerous independent contractors underneath, that provides Inland Revenue with a greater ability to receive those taxes rather than having to chase independent contractors individually.

TB Yes. So I mean we have an extensive withholding tax regime. It’s something that’s I think has always been taken for granted, but we don’t realise actually how very comprehensive it is. But when you look back on it, the sort of sphagnum moss collectors, charges for directors’ fees is a 33% rate I believe. But these withholding tax obligations aren’t updated frequently or as frequently as you might imagine. As the Tax Working Group pointed out, we’ve seen a big growth in this sector. You’re saying we’ve got these existing mechanisms in place and should extend it to this particular group. Is there going to be a de minimis or is it going to be for anyone who’s already got a PAYE obligations or who has employees?

Matthew Seddon That’s right, Terry. So, the starting point is that if you’re an employee, your employer withholds PAYE. If you’re an independent contractor, generally you deal with your own tax obligations. What you’re referencing there about sphagnum moss collectors and directors’ fees are schedular payments and that imposes an obligation to withhold on the payer of those payments. My proposal would be to extend that schedule and the schedular payments regime to include those employers and electronic marketplaces that engage the independent contractors.

Now the reason why I was looking at employers in particular and the reason why I would not have a de minimis, is because employers have the systems and software in place that pay their existing employees and they also make those payments to independent contractors. So the software and systems should only require minor modification and configuration to be able to deal with withholding on payments to those independent contractors. The independent contractors that are engaged by employers and electronic marketplaces. It wouldn’t be all of those independent contractors that are subject to the withholding. It would only be those independent contractors who are principally providing services to the employer or the electronic marketplace such that they are functionally equivalent to employees.

TB Yeah, that’s a really interesting point there because often you find that someone walks out the door on Friday is contracting back on Monday. So this question of functionally acting as an employee – is that going to be a requirement, do you think? Would it perhaps just be extended if a person is providing personal services to a company, would that perhaps be a stronger approach? I think so rather than try to get to a definition that they’re doing the same as if they were an employee because all the employment lawyers listening will be twitching on that one because there is a big case going through the courts at the moment, I believe on that matter.

Matthew Seddon It’s essentially to look at who is providing services to the employer or the electronic marketplace. It’s designed to carve out people who are genuinely supplying goods to an employer or an electronic marketplace. So, you don’t have an overreach of withholding obligations. You could imagine if withholding was made on all payments to independent contractors, it would lead to chaos. There would be withholding on every single payment that’s made by an employer.

Furthermore, proposals to extend withholding to all independent contractors have a significant downside in the fact that you’d be requiring, for example, home owners to withhold tax and pay that to Inland Revenue for a painter that was engaged to paint their house. So this proposal is designed to narrow the focus to the independent contractors who are providing services to employers and electronic marketplaces.

TB That makes perfect sense. It’s a huge area though. But as I said, the scope of this with downsizing that’s been going on through Ministries, for example, this exactly is happening, as I said, some people are probably coming out on Friday as employees and coming back contracting with a different role on the Monday. A flat 20% rate, was that what you are thinking?

Matthew Seddon Yes. The default rate would be 20%. This is in recognition of the fact that independent contractors can claim deductions for income tax purposes. It also aligns with the current voluntary schedular payments regime that already exists.

TB Yes, the voluntary schedular payments regime. So right now, if you were contracting to an employer, you could say take 20% off and the employer or rather the contracting company could do that?

Matthew Seddon Yes, there is a mechanism whereby both parties can agree to undertake a withholding. The one thing I would note about my proposal is that it is simply the default rate of 20%. There is an existing regime for schedular payments which provides that an independent contractor can notify the payer of their name, IRD number and an elected rate no less than 10%. The independent contractor can essentially toggle the rate to reflect their effective tax rates so that they they’re not overpaying tax throughout the year. And they’re not underpaying as well, so that they can get a correct tax outcome by the end of the year.

TB Yes. Our pay-as-you-earn-system is more flexible than it was, but there’s scope for improvement there. I think real time payments are the next step in the evolution of our tax system. Something just popped into my mind. If I recall correctly, if a company is providing hiring, hiring contractors, they have a withholding tax obligation automatically. Is that correct?

Matthew Seddon The labour hire rules in the schedular payments regime, I think it’s a 20% rate.

TB Yes, 20%. And it wouldn’t matter, say a contractor was working individually or through a company. Generally speaking, you can under the schedular payments rules, generally speaking, if you’re working through a company, the payer doesn’t have to withhold tax. What do you think? Would you change that here?

Matthew Seddon I think there’s a company exemption in the schedular payments regime which looks through certain companies. So, I think that could also fit in with this proposal.

TB Because mainly the fact someone’s running through a company doesn’t mean that they’re actually completely up to date with their obligations, as week after week Inland Revenue tells us what’s going on. And the other thing that you touched on in there was about the fact that as contractors, they have the ability to claim deductions. I think this is where the paper prepared for the Tax Working Group was saying basically that it seems given comparable levels of income there is this gap of about 20% and they identified that on the basis that self-employed or contractors appear to have 20% more discretionary spending than their employee counterparts.

How would you counter that? I know as a small business, when you are dealing with small businesses, people are very keen to claim everything they can, and they don’t always tell you what they’ve claimed or they’re not always as straight up or as accurate as we would all like in this space. I’ve wondered whether we should have standard deductions. What’s your view on that? I know in the UK they did that for self-employed individual. Any thoughts on that particular idea?

Matthew Seddon My proposal primarily focuses on the withholding obligation, that is on the income side of the equation, so by being able to report and withhold on these payments, Inland Revenue is going to see exactly what these independent contractors are earning.

I guess to the extent that independent contractors are claiming sizable amounts of deductions relative to their industry peers. It would allow Inland Revenue to go and look and audit those independent contractors. On the deduction side, it’s something that I have thought about. I know in the GST rules for listed services there are flat rate credits for non-GST registered persons. So, there could be a similar flat rate deduction for independent contractors to align themselves across the board.

TB I deal with quite a number of American clients and their tax returns have what they call a standard deduction of $12,000. But you don’t have to claim that, you can go for what they call itemised deductions which presumably you do so on the basis that you’ve got more to claim.

It just crossed my mind that one of the things coming out of the Performance Improvement Review of Inland Revenue which we discussed a couple of weeks back, they talked about the tax gap, and I think they also talked about making one of its objectives to make the tax system easier and simpler and particularly for small businesses micro businesses. Your proposal basically is in that space, isn’t it? And it does have that benefit.

Matthew Seddon Exactly. It provides greater levels of compliance for those small businesses, those independent contractors. There’s going to be less need for them to engage accountants and third-party providers. There’s going to be less engagement with the provisional tax system. That’s going to be a much simpler experience for those independent contractors. My proposal also recognises that there will be some costs imposed on employers and electronic marketplaces. But by leveraging off the existing PAYE rules and schedular payments rules, it is designed to minimise those compliance costs as much as possible requiring them to just modify and configure their software and systems.

I think it’s important as well to notice that prior to any implementation of this proposal, there should be a sufficient period of time in which engagement can take place between Inland Revenue and these payroll software providers. I know this has recently taken place for the personal tax cut changes which had effect from 31 July.

TB That’s actually quite critical, and wider consultation is always welcomed in this space. Something just came to mind. I mean, obviously what we’re talking about here, this could be a measure that helps to close the tax gap and raise revenue, which is great from Inland Revenue’s perspective and for Treasury, but it’s actually as I see it, and what I find attractive about this is that it’s also a benefit to contractors.

I deal a lot with small businesses here and you know, managing their tax isn’t always easy and everyone is not as diligent about managing their tax as they should be. I’m a big believer in making payments regularly, and in this case, withholding payments seems to me would contribute quite a bit to that. That was something you had that in mind when you were looking at the proposal weren’t you, because that’s one of the judging criteria of the competition.

Matthew Seddon Exactly, minimising compliance costs for taxpayers and also minimising administration costs for Inland Revenue as well.

I think independent contractors, while they might have the benefit of the time value of money by only making provisional tax payments three times a year, as they currently have no withholding may allow them to have less tax obligations in the first place, as it’s all dealt with by their employer or the electronic marketplace and really allows them to focus on doing what they do best, and that’s running their own business.

TB Yeah, I’d endorse that approach. I do recommend to a lot of my clients, they run businesses, they’re shareholder-employees, we don’t often use the shareholder-employee regime and I tell them, go through the pay-as-you-earn system making your payments regularly, so you keep on top of your tax payments. That’s one of the things, as I mentioned a minute or two ago, I like about the more frequently people make their tax payments, they’re going to be more compliant, get up to date and they will have less stress about it. It’s one of the things about managing small businesses. There’s a lot to deal with and there’s not much that you can actually do, there’s an irreducible minimum you’re dealing with at times and withholding payments helps in that space.

Slightly related topic, what about GST? Now it’s not directly in scope, but to me, I think this is the next frontier of tax could be compulsory zero-rating which would be easy for both the employer or the contracting company and the contractor. What’s your thoughts on that?

Matthew Seddon Yeah, that’s right. It’s not directly included in my proposal, but I think when thinking holistically about the tax obligations of these independent contractors and how they can be automated as much as possible. GST is obviously another area to consider. I think zero-rating, there might be some scope for that. It would mean there’s less obligations on the independent contractor and would not be required to return the GST amount and they’d still be able to claim some GST credits.

The alternative I was thinking about was potentially having the carve out for employment apply to these independent contractors who are functionally equivalent to employees. You should ideally end up with a scenario where if you’ve got an employee and an independent contractor sitting across from the table from one another at their employers’ offices, they should be treated as similarly as possible so that there’s horizontal equity between the two.

TB So what’s next for you? 1500 words was your initial proposal. So now you’ve got the 4000 words which means you’re in the money, you’re going to come away with a medal of some sort. As they say, it’s always good to make the medal rounds. So it’s in mid-October sometime. You’ve got to finalise your entry and what’s involved in that?

Matthew Seddon The final oral presentation is in October and our 4000-word submission is due in September. The 4000 words is essentially branching out and expanding on our initial 1500-word proposal. The 1500-word proposal was a teaser to the judges to set out what the concept was and how it met the relevant judging criteria. The 4000 words will expand on this initial idea.

TB It’s not many though, 4000 words, really when you think about it and then obviously your oral presentation, you’ll be in front of several gurus of tax. That would be interesting, I’d say.

Matthew Seddon Indeed, it will be interesting to hear the judge’s comments and questions in person.

TB Well, I’m sure you’re looking forward to it. I am. I think it’s a very interesting proposal. It sounds mundane, but it’s actually quite important. Thank you very much, Matthew Seddon. Thank you for coming along. Good luck for October for this scholarship, we’ll watch with interest.

Matthew Seddon Thanks Terry.

TB And on that note, that’s all for this week. We’d like to thank Matthew Seddon again for joining us and wish him all the best for the scholarship. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Government introduces a surprise fringe benefit tax exemption

The potential implications for New Zealanders from the UK’s Spring Budget

Inland Revenue has now formally launched its campaign to improve tax compliance in the construction industry, which I first mentioned a couple of weeks back. Under the heading, “Take the stress out of tax” it is promoting a tax toolbox for tradies.

This is intended to provide the rules, resources and tools to enable people to get their tax position correct. Proclaiming “We’re here to help”, there’s a series of pre-recorded online seminars covering the most common topics, such as an introduction to business, a GST workshop and employers’ responsibilities. There’s also offers for more direct contact, such as a business advisory or social policy visit. And then there’s a reminder that people can also talk to tax agents or use accounting software to, “take the pressure off.”

The background notes released comment that 42% of construction industry taxpayers who are behind either in tax payments or in filings have a tax agent. So, the role of tax agents is seen as important and obviously Inland Revenue is hoping that the role of agents will expand.

There’s also a reminder that Inland Revenue has access to data, which, as it puts it, means “We have a good handle on what happens in the construction industry”, adding it’s never too late to do the right thing. And it goes on to suggest people should come forward if they’ve forgotten some income of past tax returns or maybe have overinflated their expenses.

This is a welcome initiative by Inland Revenue. The phrasing of the campaign “Take the stress out of tax” is a classic example of speaking softly but carrying a very big stick. My view is that too many people either underestimate or are unaware of just how much data is available to Inland Revenue. This campaign phrasing also touches on something of a paradox I’ve experienced when dealing with clients with tax arrears. They’re often relieved to discover after discussing the matter the position is nowhere near as bad as they had feared, and they can now sleep easier. And I expect I’m not the only tax agent to have observed that.

It will be interesting to see the outcomes from the campaign. And as always, we’ll keep you updated with developments.

Exemption from FBT for bicycles, e-bikes, e-scooters … and mobility scooters

Now, two weeks back, I discussed the so-called apps tax. This is part of the Finance and Expenditure Committee report back on the Taxation Annual Rates for 2022-2023 (Platform Economy and Remedial Matters) Bill (No.2). The updated bill included some provisions around the proposals to charge GST on services supplied by the likes of Uber and Airbnb. The bill also included clarifications to a proposed fringe benefit tax exemption for the use of public transport.

As part of the bill, over 400 submitters, including myself, made submissions proposing some form of FBT exemption for e-bikes and e-scooters. The officials report declined the submissions commenting,

“Our overall conclusion is that a specific FBT exemption for bicycles would increase the distortion between the taxation of transport benefits and other fringe benefits, reducing the overall fairness and coherence of the tax system and giving rise to integrity risks, impacting on the fiscal cost.

If Parliament wanted to increase the uptake of cycling to help achieve improved health outcomes and assist New Zealand to achieve emissions reductions, it would instead recommend a more transparent and potentially targeted subsidy specifically designed to achieve considered policy outcomes.”

This is Inland Revenue’s boilerplate for “Nah, go away. We don’t like subsidies and special tax exemptions.”

That was then. But in what has become something of a pattern following Chris Hipkins’ elevation to Prime Minister, this week the Government has released a Supplementary Order Paper for the bill, which now introduces an exemption from FBT for bicycles, e-bikes, e-scooters and mobility scooters.

According to Revenue Minister David Parker the Government “considers that there is a public good to be gained from encouraging low emission transport” and “This measure will support New Zealand’s shift to more sustainable transport options and encourage employers to provide further sustainable and climate-friendly transport options for their staff.”

The bill includes a regulation making power which would specify the maximum cost of the exemption and the specifications to qualify. When I made my submission, I suggested a cap of about $4,000 should apply. It will be interesting to see what will be the maximum available under the exemption and how many employers make use of it, which will come into force on 1st April.

An English Budget and why it’s interesting here

On Wednesday night, the British Government unveiled its Spring Budget. This is a far less dramatic affair than the Autumn Statement last September, just after the Queen died, which led to the downfall of Liz Truss. This time the Chancellor of the Exchequer (Finance Minister) Jeremy Hunt has gone for something rather more cautious in its approach with one or two twists.

I was actually surprised there weren’t any moves around restricting the availability of non-residents to make use of the Personal Allowances exemption, or just generally increase the taxation of non-residents. That’s something I’ve seen other countries do. Australia is a very good example of where that happens. A cynic might say that’s because some of those non-residents are Conservative Party donors. But cynicism aside, given the financial pressures that the British government faces, not kicking over the stone and looking, is a bit surprising,

For example, there weren’t any changes to the controversial non domiciled or “Non-dom” scheme which gives a tax advantage on foreign income for people who are not tax-domiciled in the UK (including Prime Minister Rishi Sunak’s wife). (Most New Zealanders would qualify for this exemption).

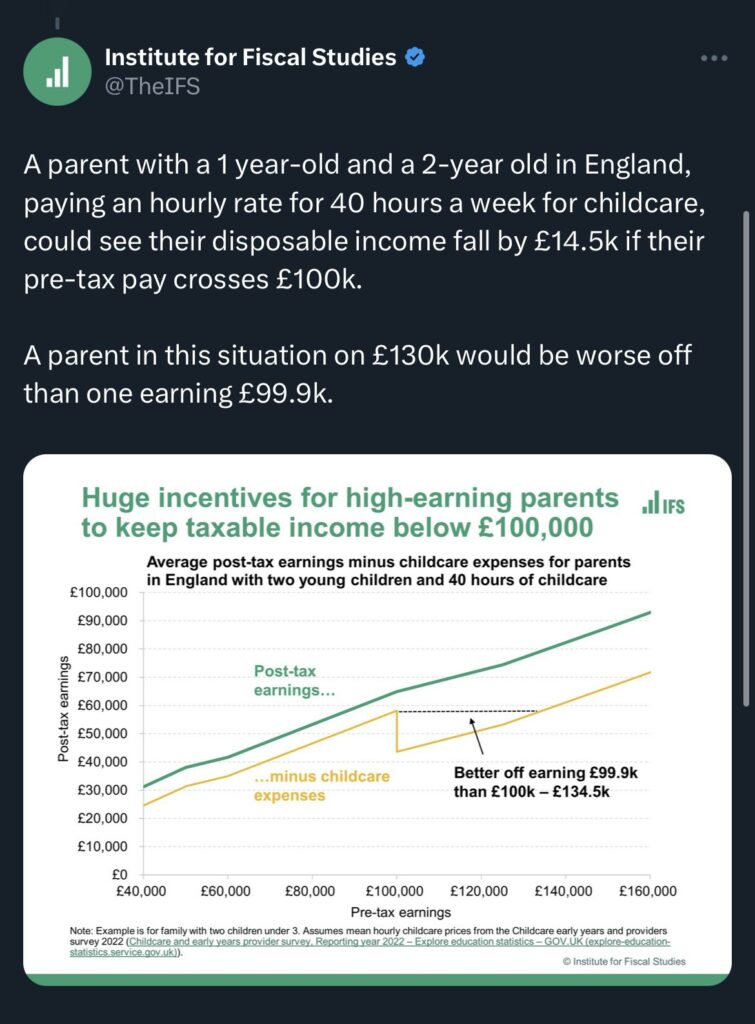

But what has perhaps attracted a fair bit of interest here was an excellent proposal, to provide and support up to 30 hours each week of free childcare support for working parents with children now aged between nine months and three years. Basically, free childcare will be available from between the ages of nine months and when children go to school. The National Party has recently announced proposals boosting childcare access.

There is a kicker to this in that it’s not available to anyone whose adjusted income is above £100,000. Basically, if someone earns more than £100,000, then all of those childcare costs they might have received are clawed back. Essentially, they don’t get back into the same net position until their income rises to £191,000. A 100% effective marginal tax rate will apply.

Now, you might well say, and I have to agree with you, that income of over £100,000 is a nice problem to have. However, it highlights a similar issue we have in our tax system in relation to clawback of Working for Families tax credits that effectively people on what modest incomes face higher than expected marginal tax rates. The clawback kicks in at a rate of 27 cents per dollar of income above $42,700.

I would hope whoever’s in Government will look seriously at this question of the clawback, the amount applicable and the threshold.

Of more direct interest to some New Zealanders is a change to what is known as the Lifetime Allowance Charge. Now, this is a controversial move that was brought in some years back because Britain has generous tax exemptions for pensions contributions. Consequently, some had accumulated very substantial pension pots tax free. To counter this, the Lifetime Allowance Charge was introduced, which imposed a charge which could be as high as 55% where the accumulated funds were above a threshold (£1,073,100).

The Lifetime Allowance Charge will be removed from 6th April and will be abolished in a future finance bill. Apparently up to 1.4 million people were caught by this. I know of several clients within this group. So they were considering their options about when and how to withdraw funds from their UK pensions. The removal of the charge means they may wish to reconsider their options.

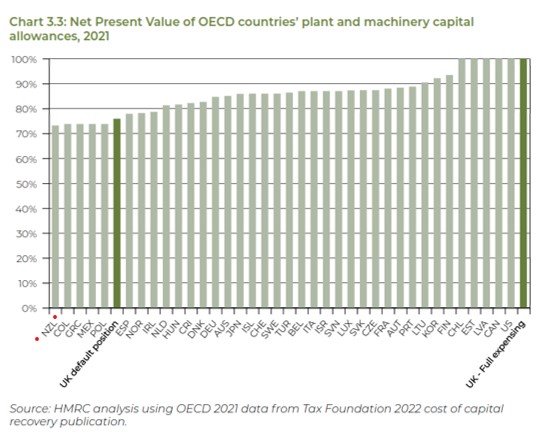

But the other thing that was particularly interesting to me is, and I think for our economy at wide was the decision to allow full expensing for capital assets acquired up to £1 million per year. Under this “Investment Allowance”, a first year allowance of 100% will be available up to the £1 million threshold. The idea is to encourage investment.

This is a topic that comes up in discussions down here. But what caught my eye was a graph produced as part of the background papers showing the net present value of all OECD countries plant and machinery capital allowances as of 2021.

As you can see under the present previous tax treatment, the UK would have been 33rd in the OECD. By going to full expensing, it moves up to be jointly top of the OECD. However, what caught my eye is that New Zealand is bottom of the OECD.

The question therefore arises whether we ought to be looking at our capital allowances regime. A similar type of initiative would be expensive, there’s no doubt about that. That’s one of the main reasons cited against such initiatives. But on the other hand, Britain has made this move because it wants to boost productivity and we know we’ve got problems with productivity.

So, here’s another challenge for the Finance Minister, Grant Robertson, to be considering right now. How do you boost our productivity? Is something similar to the UK investment allowance worth considering? We will see how that plays out in the UK. I see speculation about what might be in our budget in May is already emerging. Increasing capital allowance deductions is something I’m sure is under consideration. However, I’m also, to be honest, sceptical that we’ll see anything in the Budget.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!