Welcome to 2026. It’s early in the year, but the main drivers for the tax year seem already set. With $9.3 billion of tax interest and penalties outstanding as of 30th June 2025 Inland Revenue’s crackdown on debt will continue. It will also ramp up its investigation activities, with holders of crypto-assets under particular scrutiny.

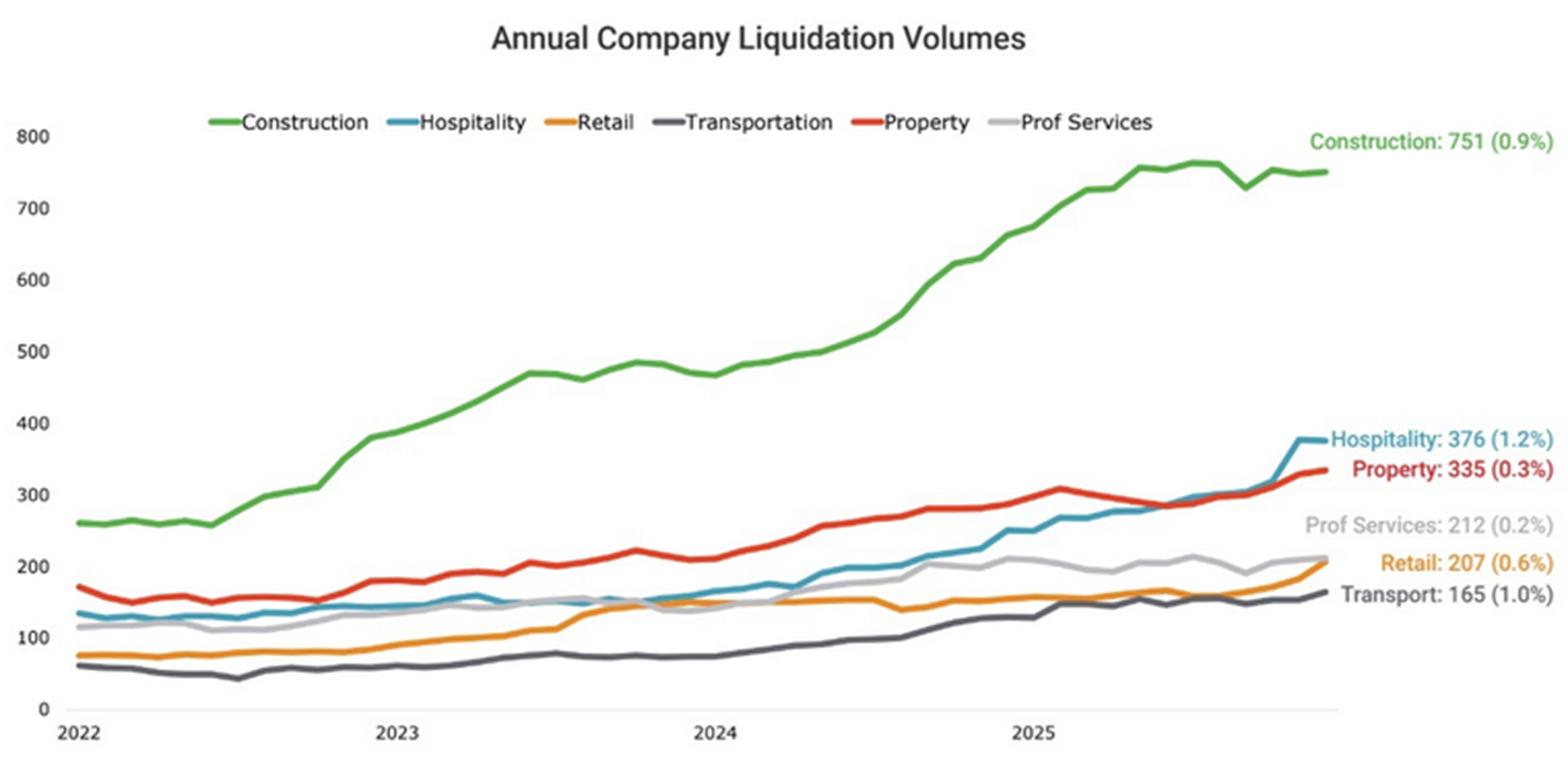

Inland Revenue is working hard to get the overdue tax debt down. However, the economy isn’t in great shape, with a recent story pointing out that liquidations have been the highest since the global financial crisis in 2008-2010. The construction sector in particular is struggling.

If you are behind with tax debt contact Inland Revenue

I cannot stress this enough, if you are in trouble with your tax debt, the first and best thing you should do, is to approach Inland Revenue. So long as you are realistic and open with, you will probably find it is prepared to work with you on an instalment plan. And in some cases where the debt is relatively small, say under $20,000, you can set up your own instalment plan, or your tax agent can help you do it.

The key thing is you have got to make the initial approach because Inland Revenue’s attitude hardens if it feels that a tax debtor is not making realistic attempts to address the scenario.

The 80:20 rule in reverse

An interesting feature about the composition of tax debt is that although the bulk of tax is paid by the very largest companies in the form of PAYE, GST, and company income tax, the majority of tax debt comes from SMEs, micro-businesses and individuals. As of 30th June 2025, over 527,000 taxpayers owed tax. For many of those small businesses, the owners are under enormous stress and it’s difficult to address the issue of tax debt. Perhaps surprisingly, my experience has been that many clients are relieved when they eventually do contact Inland Revenue as it’s often not as bad as feared and a plan is now in place.

Don’t expect the Election to change anything

We can also expect to see Inland Revenue ramping up activities. I would not be surprised if this year’s Budget has more funds for investigation and debt collection activities on top of the $35 million per annum boost it received in last year’s Budget. And by the way, this will be something that will remain the same even if there’s a change in government after the Election. Inland Revenue will still be expected to crank up its enforcement activities.

Cryptoasset investors targeted

On investigations, I’m hearing noises that transfer pricing reviews are increasing, but a key focus area is cryptoassets. Inland Revenue noted in its last annual report that it had several cases going through its dispute process, which involved “tens of millions of dollars”. It seems to be taking a fairly aggressive approach.

A client has shown me a letter where Inland Revenue have said, “if you do not make a voluntary disclosure or contact me directly, I will assume that you have deliberately failed to correctly declare your cryptoasset income.”

The tone of this letter was really quite surprising to me. Generally speaking, when Inland Revenue is considering investigations and audits, it is never as aggressive as that. More often the questions/letters that come in are along the lines of “Are you sure about that? Maybe you might want to check and come back to us.” Whatever Inland Revenue’s tone cryptoasset investors and traders should expect enquiries.

Wrapping, bridging, lending, borrowing and staking cryptoassets

Still on crypto, Inland Revenue has released a 30 pages issues paper for discussion setting out its view on the income tax treatment of wrapping, bridging, lending, borrowing, and staking cryptoassets, or decentralised finance (DeFi) transactions.

The basic position Inland Revenue has adopted with crypto is that it is property, and therefore the general rules apply that the disposals of crypto will be taxable if they were acquired for a main purpose of disposal or as part of a profit-making activity.

The paper refers to increases in crypto arising from DeFi transactions as “rewards”. Inland Revenue’s view is these are money’s worth and usually taxable when received. The analogy would be these rewards are like a dividend or an interest payment and should therefore be taxed. Submissions on the paper are open until 12th March.

Expect some crypto related court decisions

Last November I discussed the Technical Discussion Summary TDS 25/23 on the taxation of cryptoassets. As previously noted, Inland Revenue is currently involved with several similar cases involving “tens of millions of tax” so I expect some cases to appear in the courts this year perhaps either before the Taxation Review Authority, or the High Court.

As an aside it’s worth noting one of the interesting (and I don’t think it’s entirely healthy to be frank) issues with our tax system at present is that we don’t actually get an awful lot of tax cases coming through, partly because the dispute process is designed to try and resolve most issues before they get to court.

But I do wonder if it’s gone too far the other way. Supreme Court Justice Susan Glazebrook has publicly remarked on the decline in tax cases in the courts. Is that entirely healthy, given that tax is a fairly litigious topic? It is a little surprising when you step back and reflect that we don’t see many tax cases coming through. That said, I expect we will see some crypto related cases this year.

International tax – America goes its own way

Moving on, the year has been quite frantic with international developments. One of the features of the new second Trump administration is its withdrawal from many international agreements, and it has also made it very clear that it will view unfavourably what it regards as discriminatory tax practices.

As a result, the international two-pillar agreement that the OECD/G20 been working on for close to a decade now has hit a big speed bump, with the Americans making it very clear they don’t believe or consider that its multinationals (we’re talking particularly the tech companies) should be subject to those rules.

Now the end result of that is that there’s been a development called the side-by-side package which the OECD released in early January. l It’s convoluted as always with international tax, but at the moment, there’s only one country that qualifies for the side-by-side system, and you’ll not be surprised to hear that’s the United States. Basically, the idea is to allow Pillar Two to continue to coexist with the American tax regime and in theory deliver comparable minimum tax outcomes. In theory everyone is still progressing towards the 15% minimum corporate income tax rate globally.

Incidentally, the Pillar Two rules were effective for 2025 from a New Zealand perspective which means some multinationals may be subject to these rules. As I mentioned earlier, there’s been reports coming out from the Big Four that more transfer pricing reviews are happening. Anyway, we’ll keep our eyes on what’s going on in the global tax space. We expect to see more developments in that area. And it’d be interesting to see how Inland Revenue approaches its audit work in relation in this space.

“What’s in a name? That which we call a rose by any other name would smell as sweet”

Finally, it’s an election year and tax seems set to play a major part of the debate this year. So far Labour has proposed a capital gains tax on residential properties (excluding the family home) and commercial properties.

Meanwhile, echoing Juliet’s question in Romeo and Juliet, a sharp debate broke out last week, in relation to the Government’s gas levy to help pay for the proposed LNG facility in New Plymouth. Is it a tax or “just” a levy? We can expect to see more of this verbal jousting in the months ahead of the election.

Last week, the Finance Minister Nicola Willis was one of the speakers at a two-day economic forum at Waikato University. Interestingly, she brought up the question of tax policy, which is often a matter that’s debated at tax conferences although usually it’s the Revenue Minister discussing the topic.

The Finance Minister hasn’t exactly gone outside her lane because tax is a key part of her portfolio, but it is unusual to see her discuss it publicly.

She noted “tax policy certainty needs to span successive governments.” And that’s very true. The issue she was driving was a hope that Labour would support the Investment Boost package that was renounced as part of last year’s budget.

Investment Boost is an interesting initiative, one of what we call accelerated depreciation, which the OECD suggests we should be doing if we want to boost productivity. It’s an interesting mix of reactions to it, mostly positive.

I’ve had clients who are in the business financing sector report that it hasn’t had the booster effect that they were expecting.

So anyway, the Finance Minister was saying she hopes that Labour in the interests of consistent tax policy would keep Investment Boost. That remains to be seen. It’s an election year and to possibly; to borrow a rugby phrase, she’s getting her retaliation in first.

A bank taxation review?

In her speech the Finance Minister also raised the question of whether the four main big Australian-owned banks are paying enough tax. This seems a classic example of Bettridge’s law of headlines, that is, any headline that ends in a question mark can be answered by the word no. There’s a great deal of commentary around how much tax is paid by the big four banks and whether it is appropriate. They seem to have higher margins than their Australian parents and a higher margin compared with many other countries.

Australian introduced its Major Bank Levy in 2017 and there has been a long-running bank levy in the UK. Infamously, as the Green Party pointed out, Margaret Thatcher introduced a bank levy on excessive profits in the early 1980s. Anyway what the Finance Minister has apparently put on the radar is some form of review of the tax treatment or what’s happening with the tax and the big four banks. It will be interesting to see what comes out of the review.

Budget date announced

Finally, this year’s Budget will be on Thursday 28th May, a little later than I anticipated. We’ve been told it won’t be a “lolly scramble”, but being an election year, I expect we may see some surprise announcements.

Meanwhile the main themes for the year are set, more Inland Revenue debt recovery and investigation activity, an international tax picture in flux and finally because of the forthcoming election we’re going to be hearing a lot about tax. Whatever eventuates we will keep you up to date with developments.

And on that note, that’s all for this week, I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

Earlier last year, Inland Revenue conducted a policy consultation on tax matters relating to charities and not-for-profit sector. At the time, there was a fair bit of speculation that there would be changes announced in the May budget in relation to the taxation of charities and in particular what was seen perceived to be the unfair tax advantage given to charities which owned businesses.

That actually didn’t play out, but instead Inland Revenue pushed forward with consultation on the taxation of mutual transactions of associations or not-for-profits, including clubs and societies. Behind the scenes it began targeted consultation in November with around 50 persons and organisations who had provided feedback on the previous consultations. This consultation covered donor-controlled charities, membership subscriptions, and other matters.

A Christmas surprise?

On 15th December, just before Christmas, Inland Revenue then released what it called a ‘Targeted policy consultation’. This explained what had happened in November and that it was now seeking more feedback because of wider public interest in the issue. The thing was, though, the initial deadline for submissions was 24th December. However, Inland Revenue added it would be prepared to extend this submission deadline on request, but it plans to review all submissions by late January.

The surprise part of the consultation is in relation to membership subscriptions and related matters. The consultation makes clear that membership subscriptions charged by tax-exempt not-for-profits, such as the 29,000 registered charities and 19,000 amateur sports clubs, are not taxable currently and will not be taxed under the proposals out for consultation.

Are membership subscriptions taxable?

But the question under consideration is around membership subscriptions for most not-for-profit organisations. Currently, the accepted treatment is that trading with members, such as conferences and sales of merchandise, are considered taxable income, but membership subscriptions were not as they were covered by the ‘mutuality principle’. However, Inland Revenue has drafted an operational statement “…indicating that it is likely to formally change its view and state that under current law many membership subscriptions would be taxable.” Needless to say, this would be an unwelcome surprise for quite a lot of groups. Although there may be a trade-off in that some other expenses which are currently not deductible may become deductible.

The consultation also suggests the current annual tax-free threshold of $1000 could be raised to $10,000. There are also suggestions to simplify the income tax filing requirements for taxable not-for-profits, but Inland Revenue also wants to require banks and other financial institutions to provide it with financial information for those not-for-profits who use the tax-free threshold.

This is a surprising and for many organisations unwelcome development estimated to raise perhaps $50 million annually. From what I’ve seen there’s no clear explanation given as to why Inland Revenue thinks the mutuality principle no longer applies in relation to the subscriptions. I imagine there will be quite some pushback on the membership subscription issue. It will be interesting to see how this plays out and what changes are announced in the 2026 Budget.

“Don’t look back in anger” – 2025 in review

Talking of Budgets, the 2025 budget on 22nd May contained a pleasant surprise with the announcement of the Investment Boost allowance. This enables businesses of any size to fully deduct 20% of the value of any new assets in the year of purchase. Interestingly, it also includes new commercial and industrial buildings and would also cover earthquake strengthening in some cases. Perhaps surprisingly, there was no cap put on the amount which could be claimed by a business.

The Investment Boost initiative is designed to boost investment and productivity, a theme in common with other tax initiatives, for example, proposals for digital nomads and changes to the Foreign Investment Fund regime included in the Taxation (Annual Rates for 2025−26, Compliance Simplification, and Remedial Measures) Bill currently before Parliament. It’s actually a on long-standing principle of our tax policy to enable investment in New Zealand and remove barriers to doing so.

The investment boost was a big surprise. Whether it’s had the hoped for impact is not clear yet. As everyone is well aware, economic activity was bumpy in 2025, but it could be that the groundwork has been laid for a stronger recovery this year.

Boosting Inland Revenue’s compliance activities

Another constant theme for the year, was more money in the 2025 Budget for Inland Revenue to boost its compliance activities. On top of the $116 million it was given over 4 years in the 2024 Budget it got another $35 million in the 2025 Budget. Consequently, 2025 saw great degree of investigative work by Inland Revenue. According to Inland Revenue’s 2025 Annual Report, it has achieved great returns from its increased compliance activities.

In addition to investigation and review work, Inland Revenue is also trying to close off what it considers loopholes and areas where there appears to be seepage in the tax system. The not-for-profits consultation we discussed earlier is one such example. However, arguably the biggest single example, and which was such a bolt from the blue, I called it a bombshell, was the recently announced consultation on the taxation of shareholder advances. It’s one of the most significant changes to the taxation of small businesses in recent years, potentially worth several hundred million of additional tax revenue annually. We’re therefore going to see a fair bit of lobbying and feedback about the proposals which are almost certain to be as part of the 2026 Budget and the annual tax bill. Watch that space.

Targeting crypto-assets

The taxation of crypt-assets is one specific area where Inland Revenue is currently very active. In November I discussed Technical Decision Summary TDS 25/23 where investors in crypto-assets lost the argument that gains were on capital account and therefore non-taxable. This case is probably the tip of the iceberg as according to Inland Revenue’s 2025 Annual Report “As at 30 June 2025, more than 150 customers were under review, with total tax at risk in the tens of millions.”

We’ll also see ongoing activity from Inland Revenue reviewing property transactions. Everyone tends to underestimate how much access to data Inland Revenue has and the information sharing which goes on with other Government agencies and tax authorities around the world. I’m sure I’m not the only tax agent seeing increasing numbers of inquiries from clients and Inland Revenue relating to investigations or reviews covering overseas income which may or may not have been declared properly.

Tax debt – a $9.3 billion problem

The other big area for Inland Revenue is managing the debt book, in late November I had a very interesting discussion with Tony Morris from Inland Revenue about how it is approaching the management of its debt book, which is over $9.3 billion and what steps are being taken to reduce this.

I’m seeing a much more forceful attitude from Inland Revenue around earlier interventions and debt collection. In some cases, that’s well merited. Other cases, I think it’s been a little ham-fisted. There’s also work to be done in managing companies which fall behind on GST and PAYE. Much earlier intervention is needed there. But one hopes that the extra money that Inland Revenue has received from the government will aid that. Getting the debt book under control is obviously very important for Inland Revenue and for the Government.

One area I think actually needs a fundamental redesign, is the question of student loans where only 30% of overseas-based debtors are making repayments at this point. Now, Inland Revenue does have the power in many double tax agreements to ask overseas authorities to intervene on its behalf, but it seems to have been a bit reluctant to do so. 2026 may see a change in this approach.

Overall, we can expect to see Inland Revenue gathering using all its available tools to collect the maximum amount of overdue debt and bring the debt book under control. That’s been a big theme in 2025 and it’s going to be a continuing theme this year.

The Trump effect

Internationally, the second Trump administration has caused all sorts of upheaval across the world order geopolitically, but also in the tax space where progress on the already grindingly slow Organisation for Economic Cooperation and Development/G20 multilateral tax proposals, the so-called Pillar 1 and Pillar 2 proposals, has basically ground to a halt.

The Trump administration made it clear early on it is hostile to what it considers unfair taxation and regulation. Its National Security Strategy released in November spelled it out bluntly.

(National Security Strategy of the United States of America, page 19)

Against this background it’s hardly surprising the Government in May decided to withdraw (“discharge”) the Digital Services Tax Bill.

Big Tech, Little Tax

The multilateral Pillar 1 and Pillar 2 deals seem dead in the water, but as the Tax Justice Aotearoa noted in their report, Big Tech, Little Tax that still leaves the problem of the tech companies’ apparently extensive use of transfer pricing methodologies to minimise their tax bills.

One of the examples the Tax Justice Aotearoa report considered was Oracle New Zealand, which according to its 2024 financials, earned revenue of $172.7 million, but paid licensing fees of $105.3 million to an Irish-related party company. It ultimately finished up with taxable income of just $5.3 million. It’s apparently paid royalties representing between one third and three-fifths of its total revenue. Oracle, incidentally, is currently undergoing an audit in Australia and there’s a related tax case going through the courts, which I expect Inland Revenue will be watching very closely.

And then there’s Microsoft, which earned revenue of $1.32 billion, but then paid over a billion dollars in purchases to another Irish located related party company.

The Digital Services Tax might have had some impact on this, but a more likely tool to try and recover additional tax would be to start applying non-resident withholding tax on the royalty element of any cross-border payment. The payments should remain deductible, but subject to a (typically) 5% withholding tax. Such an approach should be acceptable under most long-standing international agreements, but it will be interesting to see what pushback emerges if Inland Revenue adopts this approach.

Tax policy highlights the rising cost of demographic change

In the tax policy space in general, it’s been an interesting year with the Inland Revenue’s long-term insights briefing somewhat controversially looking at the question of the tax base. This was alongside Treasury’s He Tirohanga Mokopuna, statement on the long-term fiscal position which took a 40-year view of the Government’s fiscal position. A common theme was the demographic pressures on pension funding. Unsurprisingly that, together with the rising costs of climate change, was also a major theme the OECD’s review of tax policy in 2024.

Capital Gains Tax – a never-ending story?

The seemingly endless debate about capital gains tax continued through 2025. The International Monetary Fund paid its regular Article IV visit and suggested it might not be the worst thing in the world. The more interesting IMF report to me was about New Zealand productivity, where it directly suggested that the lack of a capital gains tax has meant excess capital has been gone into property rather than into productive investment, and it could be a factor in our low productivity. That’s not an unreasonable conclusion in my view.

Then we had the Labour Party finally announcing its somewhat limited capital gains tax proposal, which will apply to all residential investment and commercial property. That’s a little less bold than what Labour Party members wanted, but on the other hand is in line with our practice of incremental changes. It’s also pretty much in line with what the minority group on the last tax working group suggested, a comprehensive capital gains tax wasn’t needed, but expanding it into the taxation of residential property was certainly recommended.

The Tax Policy Charitable Trust brought down former IMF Deputy Director Professor Michael (Mick) Keane for a couple of lectures, one of which was in Wellington at Treasury. He made the interesting observation that most tax jurisdictions which do have a capital gains tax, and remember we’re in the minority, approach it from the basis that everything is in unless it’s out. Presently, our approach is the flip side, everything is out unless it’s in but the problem is there’s a lot more in than people realise and so there’s seepage of potential review. In terms of conceptuality, I think his approach is to be preferred. Include everything and then carve out exemptions (such as the family home). That is what we see around the world as he noted.

Looking ahead as always, there will be a huge debate going on around what are the best tax settings for New Zealand as we head into the second half of this decade. With 2026 being an election year, we’re going to hear a lot about capital gains tax. I’m afraid non-tax geeks will probably be heartily sick of it by the end of the year.

Thank you

Finally, I’ve been very fortunate with the guests I’ve had this year, so thank you all, you’ve been most interesting and generous with your time. A special shout-out to Tony Morris of Inland Revenue for a fascinating discussion on where Inland Revenue is working in the debt space. (Transcript coming soon).

And on that note, that’s all for 2025, we’ll be back in late January to cover all the latest developments in tax as always. I’m Terry Baucher and thank you for reading and commenting. Please send me your feedback and requests for topics or guests. In the meantime, best wishes for 2026!

calls for capital gains tax to help solve housing affordability.

Earlier this year, the popular Auckland Cafe chain Little and Friday closed its final store in Ponsonby. That was a great personal disappointment for me as its food was wonderful, although my waistline is probably all the better for its closure.

It has now emerged that at the time of its closure, the owners owed $640,000 in tax and the company has now been put into liquidation owing creditors over $1.4 million.

This obviously puts a different complexion on the closure, and it also prompted an interesting debate amongst my tax agent colleagues, with quite a few pointing out the inconsistencies that they see in Inland Revenue’s debt management. One took particular exception to the news, commenting how he had been grilled over a relatively small adjustment, less than three figures, and yet somehow Little and Friday had been allowed to build up unpaid GST and PAYE totalling $640,000.

Focusing on the wrong target?

Another tax agent noted that he had received a call regarding a client being overdue in making their small business cashflow scheme repayments. The amount outstanding was $18,000, but as the tax agent pointed out, the client also owed several hundred thousand dollars in relation to unpaid GST and income tax. The agent was therefore rather puzzled as to why Inland Revenue seemed to prioritise the small business cashflow scheme arrears. Several other tax agents weighed in with similar points about such inconsistencies.

Now, debt management is a core role for Inland Revenue. That goes without saying. But it is also an issue where there are clearly strains emerging. We’ve talked previously about what’s been going on with the student loan scheme, where substantial amounts of debt are allowed to build up over enormously long periods of time.

My attention has been drawn to a case where the student loan borrower left more than 20 years ago and was eventually contacted by Inland Revenue demanding over $200,000 of accumulated interest and penalties. Like Little and Friday, and other cases noted above, the unanswered question is “How did Inland Revenue manage to let it get to that stage?”

Earlier intervention needed?

When looking at Inland Revenue’s management of its debt portfolio two concerns arise – its approach seems inconsistent and it doesn’t intervene soon enough.

Inland Revenue has enormous tools at its disposal. It can put companies into liquidation and that’s actually what happened with Little and Friday. But it doesn’t want to do that all the time. It will sometimes hesitate before doing anything, for perfectly reasonable circumstances. But there does come a point where it is probably better for all concerned that the Inland Revenue moves sooner and doesn’t allow the debt to build up.

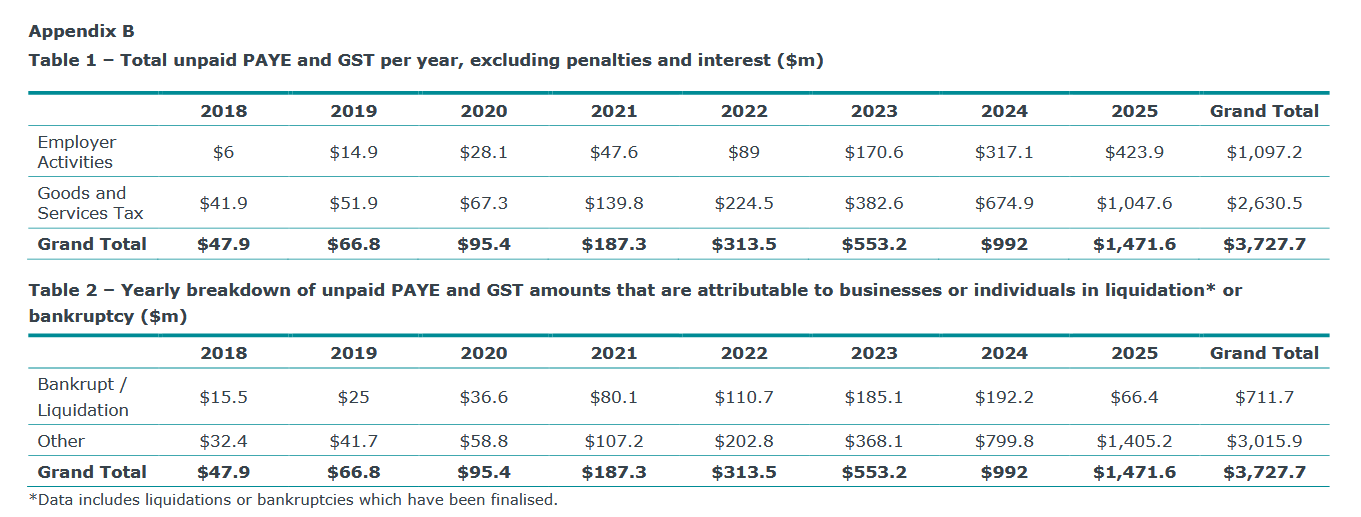

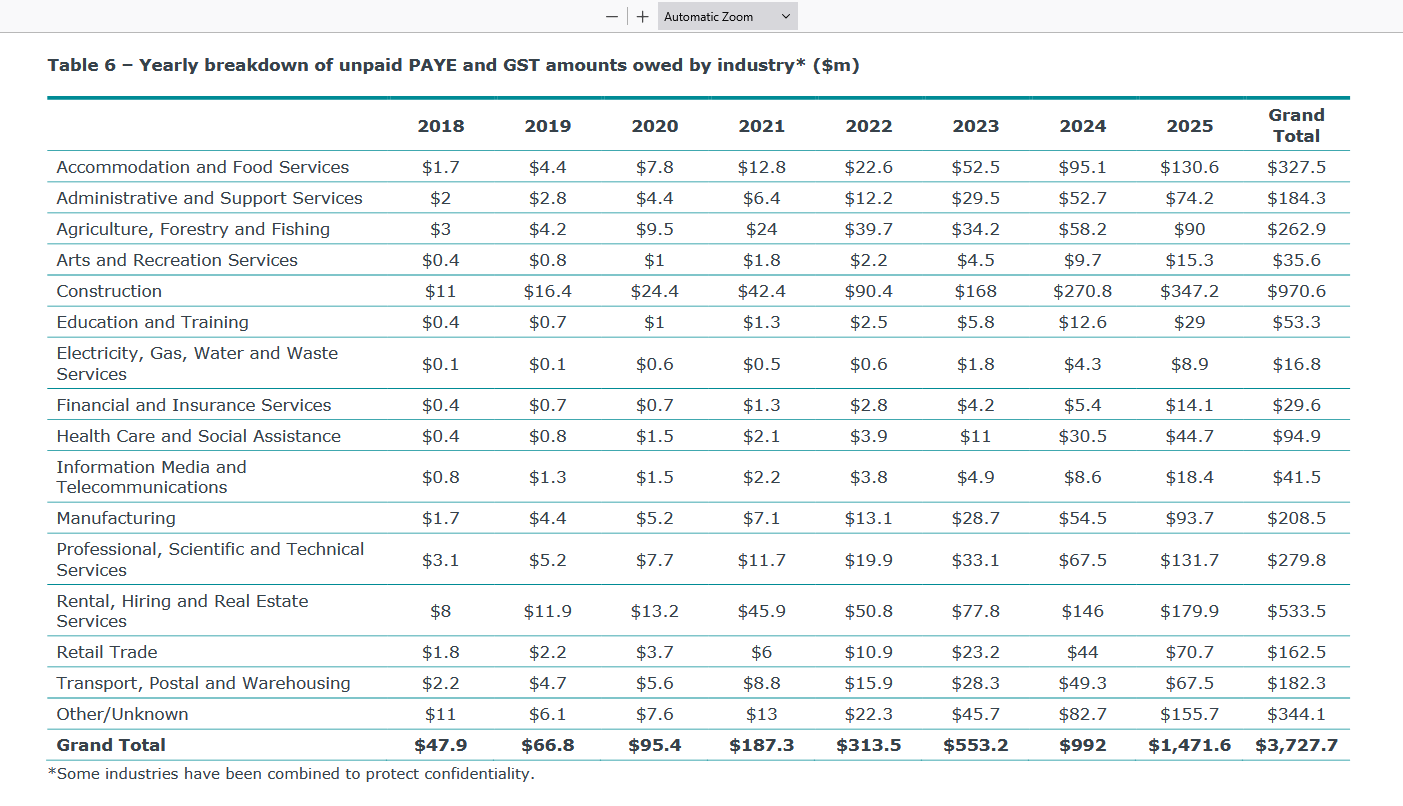

Now Little and Friday is not an unusual circumstance. While preparing for this podcast I came across an Official Information Act request about debt dating from June this year, and the number being reported was frankly horrifying. According to this report, as of 31st of March 2025, the total amount of unpaid PAYE and GST, excluding penalties and interest, stands at $3.727 billion.

As can be seen $711.7 million of that $3.7 billion represents businesses or individuals going into liquidation. The rest is simply outstanding debt which Inland Revenue is hoping to obviously try and recover. But the amount of debt it is writing off is starting to increase, as is the amount of debt that it deems non-collectible. According to this OIA report the non-collectible amount as of 31st of March 2025 is expected to be $1.1 billion dollars.

Then there’s a very interesting industry breakdown of how that amount of debt has accumulated.

The sectors hardest hit in that are our construction which has $347.2 million of unpaid debt as of March 2025. accommodation and food services, i.e. cafes like Little and Friday owe $130.6 million, manufacturing $93.7 million and professional, scientific and technical services have also accelerated remarkably $131.7 million. Even rental hiring and real estate services, which you would regard as relatively strong industries, has unpaid GST and PAYE of $179.9 million as of 31st March this year.

Across the whole of the economy, these numbers are piling up and it presents a huge problem for Inland Revenue, and by extension for the Government as to how is it going to manage this issue.

Unfairly targeting student loan defaulters?

A very real threat for people owing student loans who are not meeting their obligations is being arrested at the border. But none owe $600,000 of tax. In theory, someone owing that amount of unpaid GST and PAYE could be freely entering and leaving the country without customs making a move against them.

On the other hand, someone owing $100,000 of student loan debt, which is sizeable, yes, could enter the country and be arrested. I wonder why such an inconsistent approach applies.

To be fair Inland Revenue is working through the overdue debt issue and taking enforcement action. This week it reported how an accountant, Luke Daniel Rivers, also known as Mai Qu was jailed for six years over a $1.7 million COVID-19 fraud. He made false claims over wage subsidies in the small business cash flow scheme.

Now quite correctly Inland Revenue and the Ministry of Social Development have pursued that. But at the same time, we have these other businesses falling over, owing very substantial sums of money, and it appears almost as if the defaulters are able to walk away without consequences, to the frustration of myself and other tax agents.

What about MBIE?

One other thing of note in this area are the potential breaches under the Companies Act 1993. In some cases, you’d have to say there there’s a strong argument that businesses racking up hundreds of thousands of dollars of tax debt are in breach of their Companies Act obligations, which could lead to action by the Ministry of Business, Innovation and Employment.

The economy is under strain and tax debt is rising. Sometimes really bad luck hits a business or person. Small businesses can get hit particularly hard if a key person falls ill. Tax debt may just be down to sheer bad luck, the wrong thing happening at the wrong time.

But overall, Inland Revenue looks to be struggling, for want of a better word, managing the portfolio. Even allowing for maybe getting better resources to manage this, there’s still the question of an inconsistent approach that I and other tax agents have noted. So, there’s a lot of going on in this space.

I expect the Commissioner of Inland Revenue is reporting very frequently to the Minister of Revenue on this issue and any new initiatives to address these concerns. The most important thing would be to get the economy going again and hopefully some of these businesses are able to trade their way out. But we’ll have to wait and see.

Capital gains tax to deal with housing affordability?

Now, in recent weeks, there’s been quite a lot of chatter around Inland Revenue’s long-term insights briefing, which has talked about the need to perhaps expand the tax base. Last week we discussed how CPA Australia called for a capital gains tax.

This week at the Government’s Building Nations 2025 Infrastructure Summit on Wednesday 6 August, Group Chief Economist and Head of Research for ANZ Richard Yetsenga discussed the question of what he described as runaway house prices in Auckland, Australia and New Zealand. He said that we should look seriously at introducing a capital gains tax as a means of addressing house price affordability. In his view, if this issue is not resolved, “I think it’s going to eat us alive. It’s our biggest intergenerational issue.”

Mr Yetsenga was speaking after addresses from the Finance Minister, Nicola Willis, and Transport Minister and Housing Minister Chris Bishop. In response he suggested looking at both the supply and demand issues of the tax system, which in his view, was one of most effective ways available to influence economic activity.

That’s something I would agree with. What we don’t tax is as important as what we do tax. I think the fact that we don’t have a capital gains tax has resulted in major distortions for our economy. This was something which the recent International Monetary Fund report on our poor productivity mentioned. It’s very interesting to see all the constant chatter on the topic of capital gains taxation.

How many people return overseas income?

Finally, Inland Revenue proactively publishes any Official Information Act (OIA) requests that it receives. These often include some very interesting data such as the breakdown of debt I discussed earlier.

The question was rather oddly phrased because the requester asked “Do you know if/believe there high compliance with NZ tax rules for NZers working overseas?” Inland Revenue’s response was basically this is actually not a request for information, it’s more for an opinion so we aren’t answering that.

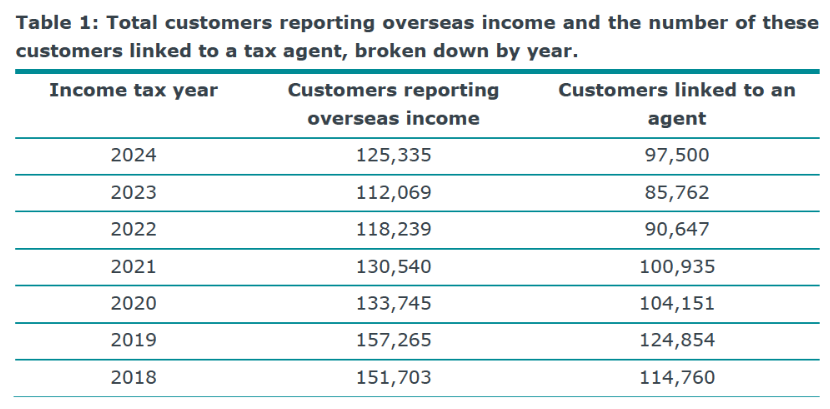

The request then asked for specific data about taxpayers reporting overseas income, and also the split between taxpayers who reported it and those taxpayers with tax agents who report it. Inland Revenue provided the following breakdown for the 2018 to 2024 tax years. (The final due date for filing tax returns for the 2024 tax year is 31st March 2025 so 2024 is the latest year for which complete details are available).

What caught my eye about this data is that the numbers have fallen since the 2019 year. In 2018, 151,703 taxpayers reported overseas income, of which 114,760 were linked to a tax agent. After an increase in the 2019 year the numbers reporting income decline each year until the 2024 year when it rises from 112,069 to 125,335.

I find it quite surprising, given the international mobility of our labour, that fewer people appear to be reporting overseas income when we have a lot more migrants arriving.

I suspect it’s possibly piqued Inland Revenue’s interest, because I’ve had some clients requesting assistance after they have been contacted by Inland Revenue which has received information under the Common Reporting Standards of Automatic Exchange of Information. It will be interesting to see how that number of taxpayers reporting overseas income tracks.

By the way, this OIA also references the Common Reporting Standard, confirming in response to a question it “receives financial account information automatically from the Australian Tax Office under the Common Reporting Standard. This information is matched to taxpayer accounts and risk assessments.”

This ought to be well known and, as noted above, maybe we might see an increase in the numbers reporting overseas income.

Happy Twenty-first!

Now finally this week, according to LinkedIn, Baucher Consulting is 21 years old today. So Happy Birthday to me. It’s been and continues to be an amazing journey and who knows what the future will bring. In the meantime, thank you all for all the messages of support.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The debate over international taxation and the so-called Two Pillar proposals has been driven largely by the G20 and the Organisation for Economic Cooperation and Development, (the OECD). But in recent years the United Nations has started to flex its muscles in this space. This is unsurprising, because the UN represents the wider world view outside the 40-odd countries which make up the G20/OECD.

All of this is behind the story that RNZ ran at the start of the week about the United Nations Committee on Economic, Social and Cultural Rights statement on tax policy. The RNZ ran this statement under the banner headline “UN Report questions fairness of GST”, in which it pointed out that GST can be regressive for low-income earners.

In fact, the UN Committee statement went much further than GST. It noted the terms of reference to the United Nations Framework Convention on International Tax Cooperation, which had been adopted by the General Assembly,

“This development represents an important opportunity to create global tax governance that enables state parties to adopt fair, inclusive and effective tax systems and combat related illicit financial flows.”

“regressive and ineffective tax policies”

The key paragraph to the UN Committee statement is paragraph 4, which refers to “regressive and ineffective tax policies”, having

“…a disproportionate impact on low-income households, women, and disadvantaged groups. One such example is a tax policy that maintains low personal and corporate income taxes without adequately addressing high income inequalities. In addition, consumption taxes such as value added tax can have adverse effects on disadvantaged groups such as low-income families and single parent households, which typically spend a higher percentage of their income on everyday goods and services. In this context, the Committee has called upon States Parties to design and implement tax policies that are effective, adequate, progressive and socially just.”

It’s the reference to consumption taxes that was picked up by RNZ. The regressivity of GST is well known and was noted by the last Tax Working Group. The general approach we’ve taken here to that issue is to try and ameliorate the impact by benefits or transfer payments such as Working for Families and Accommodation Supplement to lower income families.

The thing is though, as Alan Bullôt, of Deloitte noted in the RNZ story, GST is a very effective tool for the government to raise a large amount of money relatively easy. In fact, GST represents about 25% of all tax revenue a point I repeated when I discussed the whole story on RNZ’s The Panel last Monday.

Principles of a well-designed tax system

But the Committee statement is interesting beyond the GST issue because it goes on in paragraph 6 to set out what it regards as the principles of a well-designed tax system. It suggests, for example,

“…ensuring that those with higher income and wealth, in particular those at the top of the income and wealth spectrums, are subject to a proportionate and appropriate tax burden.”

That can be clearly interpreted as a call for a capital gains tax or some form of capital taxation, a point I made to The Panel.

The Committee also fires a few shots over international tax, stating

“The Committee has observed situations in some States where low effective corporate tax rates, wasteful tax incentives, weak oversight and enforcement against illicit financial flows, tax evasion and tax avoidance, and the permitting of tax havens and financial secrecy drive a race to the bottom, depriving other States of significant resources for public services such as health, education and housing and for social security and environmental policies.”

That clearly targets tax havens, but it’s also a shot across the likes of Ireland, for example, with its low corporate tax rate.

A global minimum tax

The Committee also calls for a “global minimum tax on the profits of large multinational enterprises across all jurisdictions where they operate and to explore the possibility of taxing those enterprises as single firms based on the total global profits, with the tax then apportioned fairly among all the countries in which they undertake their activities.”

That’s quite the statement even if probably forlorn given the Trump administration’s recent declarations. It’s probably what the less developed world is after, because they’re quite concerned they’re losers under the current system. This is going to lead to wider clashes over the G20/ OECD proposal, which I think to be frank, is probably dead. In any case, I thought it was always noteworthy that Pakistan, the World’s fifth most populous country and Nigeria, the sixth most populus country and also Africa’s largest economy, both refused to sign up for Two Pillars.

Now economically, that was not highly significant because the economies are small relative to the giant economies of the developed world. However, I think this refusal points to existing issues and this statement underlines there’s global tensions ahead on this question of international tax.

As I said, the Trump administration basically is saying no go. But I think you will see countries attempting to find ways of taxing what they regard as their part of the international multinationals’ income. So, plenty ahead in this space.

Rising GST debt

Now moving on, another RNZ report picked up that there had been a substantial growth in GST debt. Allan Bullôt, of Deloitte raised a concern this could be creating zombie companies. In particular he noted the amount of GST collected but not paid to the Government, has risen from $1.9 billion in March 2023 to $2.6 billion by March 2024.

As mentioned earlier, GST represents 25% of tax revenue. It also represents just under 40% of all tax debt and has been rising sharply. That’s a reflection of the economic slowdown and the cash flow crunch that’s happening to a lot of businesses.

Even so, this is a matter where Inland Revenue has a number of resources it can deploy, and one Alan mentioned is the power to notify credit reporting agencies about tax debt. According to the Inland Revenue, it only did that three times in the year ended 20 June 2024 and not at all during the June 2023 year.

This means that people were trading and doing business with companies without realising the potential risk. What that might mean is that you provide services to a company which is struggling with GST debt, and lo and behold, you suddenly find you’ve got a bad debt on your hand.

Creating zombie companies?

This is a major issue and as Allan put it,

“That’s grown and grown. I get very nervous we’re creating zombie companies … if you’re three or four GST returns behind, it’s incredibly unlikely if you’re a retail or service business that you’ll ever come back. If you’re three of four GST payments behind, it’s incredibly unlikely that your retail or service business will ever come back.

Maybe if you’re a property developer who’s got big assets that you sell and settle your debt. But if you’re a normal business, a restaurant or something like that, you go belly up.”

This is an area where Inland Revenue has information which is not available to the general public and maybe it should be making that more widely available. There’s a question here to my mind, of what proportion of debt you would report. The Inland Revenue I think has every right to say this person owes X amount of GST, or is behind on GST, but bear in mind in some cases the debt is inflated by interest and penalties. Or in some cases there may have been estimated assessments.

Notwithstanding this Allan is right to raise concerns and I expect we will see more money being granted to Inland Revenue in this year’s Budget to chase this debt.

Meanwhile, jam tomorrow in the Australian Budget

It was the Australian budget on Tuesday night our time in which the ruling Australian Labor Party promised modest tax cuts starting in July 2026, with a further round in July 2027. Under the proposed cuts, a worker on average earnings of A$79,000 per year (about NZ$86,800) will receive A$268 in the first year and that will rise to A$536 in the second year. In addition, there will be a A$150 energy rebate payable in A$75 instalments.

Otherwise, there weren’t many other tax measures to report. That was hardly surprising because two days later, Prime Minister Anthony Albanese announced that the Federal Election would be held on 3rd May. The Budget was therefore what you might call a typical pre-election budget, promising jam tomorrow if you vote for the ALP.

One tax measure of note was that the Australian Tax Office is getting further funding for dealing with tax avoidance and tax evasion. I think that’s a pretty standard pattern we’re seeing around the world. The British had what they call their Spring Statement this week, the half yearly report by the Chancellor of the Exchequer or Finance Minister.

No new tax measures were announced. But like the ATO, HM Revenue and Customs was allocated more money to target tax evasion, with the expectation that it would achieve about a billion pounds a year in additional revenue, which seems very light given the scale of the UK economy.

Mega Marshmallows food or confectionery?

Finally, this week, a couple of years back, we discussed the Mega Marshmallows Value Added Tax (VAT) case from the United Kingdom. Basically, it involved the VAT treatment of large marshmallows. If deemed to be food they would be zero-rated for VAT purposes, but if they were confectionery, they would be standard rated which at 20% means quite a significant sum is at stake.

I will cite this and its very well-known predecessor the ‘Max Jaffa’ case involving Jaffa Cakes from the 1990s, when people make suggestions about maybe reducing the GST on food to help with the cost of living, particularly for lower-income families. It’s a well-meant policy except the practical issues you run across lead to absurdities at the margins. My view on this topic is if you want to assist people at the lower end of the income scale, it’s better give them income rather than try and fiddle with the GST system because there are unintended consequences, and this mega marshmallow case is a classic example.

The case involves unusually large marshmallows. The recommendation by the manufacturer is that they should be roasted as they’re marketed as part of the North American tradition of roasting marshmallows over an open fire. Except it’s not clear in fact, if that actually happens.

The story so far is that after HM Revenue and Customs lost in the First-Tier Tribunal, it appealed to the Upper-Tier Tribunal which basically said, “Nope, we’re not hearing it.” So HMRC appealed again to the Court of Appeal which has now issued its ruling. The Court of Appeals determined it was not absolutely clear whether in fact these marshmallows can only be eaten if they are cooked, in which case they must be food, or they can be eaten with the fingers, in which case they are confectionery.

Accordingly, the key issue is whether they are normally eaten with the fingers. This is a question of fact about which the first-tier tribunal has not made a finding. In some cases, it will be obvious from the nature of the product whether it is normally eaten with the fingers or in some other way. But that is not clear with this particular product.

The Court of Appeals therefore sent the case back to the First-Tier Tribunal to decide on this question of fact. Are these mega marshmallows mostly eaten with the fingers? If so they’re confectionery and subject to VAT at 20%. Alternatively, are they mostly cooked as supposedly intended, and therefore zero-rated food.

Time for the UK to apply VAT to food?

This case came to my attention through the UK tax thinktank Tax Policy Associates which is run by the estimable Dan Neidle, a former tax partner at the mega law firm Clifford Chance. Commenting on the Court of Appeal’s decision, he pointed out the sheer absurdity and costs involved and questioned why this was so. “Why do we have a horribly complicated set of rules that mostly benefit people on high incomes (because they spend more on food)? “

His solution – scrap zero-rating on food, in other words, adopt the approach we have here in New Zealand and tax everything. He estimates that would raise about £25 billion which could be used to reduce the standard rate of VAT from 20% to 17%.

Warming to his theme Dan thinks a better idea would be “Cut the rate to 18% and use the remaining [money] in benefit increases and tax cuts targeting those on low incomes, so they’re not out of pocket from the loss of the 0% rate.”

It’s the first time I can recall a British commentator suggest this. I doubt it will happen, but it’s just a reminder that although our GST is highly comprehensive, we don’t have these absurd but entertaining cases involving marshmallows of unusual size.

But a comprehensive GST is regressive, and I think a better approach is to address that by means of transfers to lower incomes rather than tinkering with exemptions. You never know, there may be something in this space in the Budget, we’ll find out next month.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Inland Revenue releases three special reports regarding the changes to the platform economy rules, the 39% trustee tax rate and the new 12% offshore gambling duty

Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don’t, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

Apparently, tax debt is high in the construction sector and there’s also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

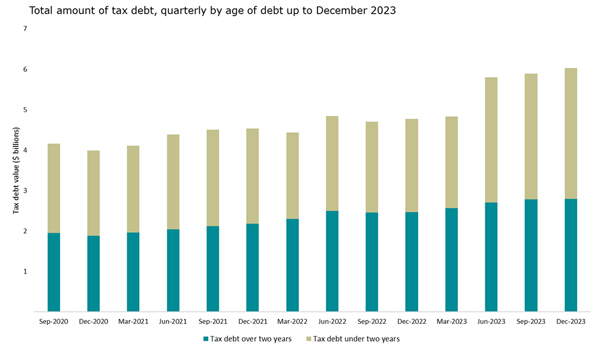

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over two years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

ADVERTISING

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it’s going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we’re going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

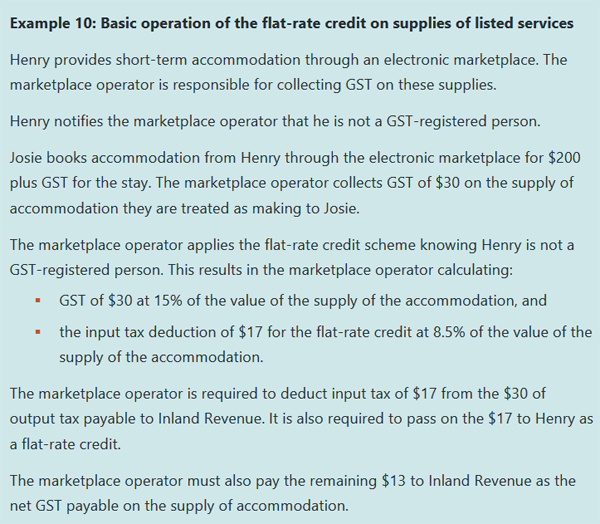

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators

Under the new rules, so-called online marketplace operators such as Airbnb, Uber and Bookabach will charge GST on all bookings made through them. However, the person who actually provides the ride or the accommodation may not be GST registered. This is where the flat-rate credit scheme comes into effect as the following example illustrates:

The full report is 68 pages so there’s plenty more to dive into.

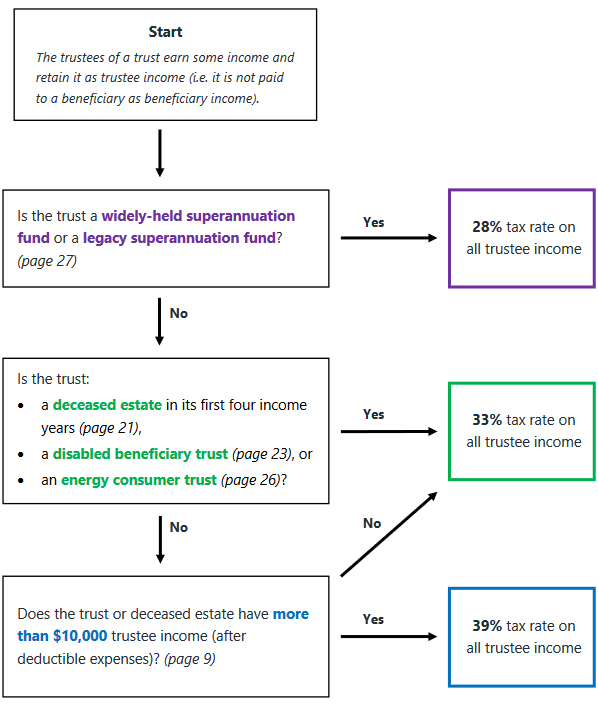

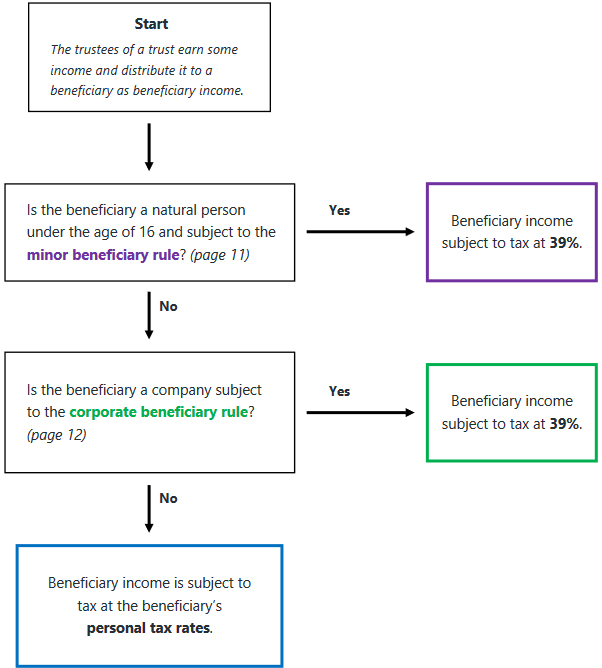

Special report on 39% trustee rate

One of the other reports that was issued is on the application of the trustee rate of 39%. Basically, trustee income is the net income of the trust, which has not been distributed to beneficiaries. The 30-page report explains the basic provisions about “beneficiary income” and “trustee income” together with a couple of useful flow charts.

Trustee income flowchart

Beneficiary income flowchart

The report references the minor beneficiary rule which applies where the beneficiary is a natural person under the age of 16. In such a case only $1,000 of income per year can be distributed to that person as beneficiary income and be taxed at that person’s marginal tax rate, presumably below 39%. Under the new rules, any beneficiary income in excess of $1,000 paid to a minor would be taxed at 39%.

Overall, this is useful guidance. Just remember the $10,000 threshold is all or nothing: if trustee income is $10,000 or less, the trustee tax rate that applies is 33%, but if it’s $10,001 then it’s 39% on everything.

The third report is on the proposed offshore gambling duty, which takes effect from 1st of July and will apply to online gambling provided by offshore operators to New Zealand residents.

The bright-line test and tax evasion – a couple of useful real-life case studies

Finally, this week a couple of interesting Technical Decision Summaries from Inland Revenue. Technical Decision Summaries are anonymised summaries of some interesting cases that Inland Revenue’s Tax Counsel Office has encountered either through tax disputes and investigations or applications for binding rulings.

The first one, TDS 24/06, is an application for a ruling regarding whether the bright-line test or section CB 14 of the Income Tax Act would apply. The facts are complicated but involve three sections of land currently owned by the ruling applicant.

The applicant had initially acquired one section outright before his spouse and another co-owner acquired interests as tenants in common. Over time, the applicants proportion of the ownership changed until at the time his spouse died the property was held 50% as tenants in common with his late spouse. The second section was owned 50% each as tenants in common with his late spouse. After her death her 50% interest had passed to him under her will. The third section was owned by the applicant and his late spouse as joint tenants. Following her death, her interest was automatically transmitted to him.

The ruling applicant was concerned about the treatment of future sales. Would the bright-line test apply or failing that, would section CB 14? This section is a little used provision and applies where there’s been a disposal within 10 years of acquisition and during that time there’s been a 20% more increase in value of the land thanks to a change in zoning, or removal of restrictions.

The Tax Counsel Office concluded neither the bright-line test nor section CB 14 would apply. This is obviously a good result for the taxpayer but it’s actually also a good example, of how you can apply for a ruling to get Inland Revenue’s interpretation on a tax issue. You don’t necessarily have to follow it, but if you don’t, you better have good reasons for not doing so.

Fiddling the books and getting found out

On the other hand, TDS 24/07 involved suppressed cash sales, GST and income tax evasion and shortfall penalties. The taxpayer carried on a restaurant business which was registered for income tax and GST. Inland Revenue’s Customer Compliance Services (CCS) investigated the company and formed the view that there was fraudulent activity going on. There was suppression of cash sales, and the taxpayer was under returning GST and income tax.

CCS reassessed the taxpayer’s GST and income tax returns for the relevant periods and they increased the taxable revenue for suppressed cash sales based on analysis of point of sale data, the taxpayer’s bank statements and industry benchmarking.

Industry benchmarking – an underused tool?

Just on industry benchmarking, I think Inland Revenue ought to be much more public about its data here and warn taxpayers there are benchmarks against which it will measure your business. It has done so in the past, but I think the combination of Business Transformation and then the pandemic interrupted progress in this space.

What people should remember is, Inland Revenue has some of the best data available anywhere about measuring industry benchmarking. I believe it should be making this much more public so that it can serve as an early warning shot for businesses that think they can suppress income. Everyone loses when this happens. Gresham’s law about bad money driving out the good is very applicable here, because businesses which are not tax compliant are undercutting those businesses which are following the rules. This is not a healthy situation as it leads to considerable frustration and anger and if not dealt with, will just simply encourage more of the same behaviour.

Tax evasion? Have a 150% shortfall penalty

In this particular case, the taxpayer’s fraud was identified, and GST and income tax reassessments followed. In addition, Inland Revenue also imposed tax evasion shortfall penalties, which are 150% of the tax involved. These evasion shortfall penalties were reduced by 50% for previous good behaviour, but that’s still represents a penalty of 75% of the tax and GST evaded.

Unsurprisingly, the taxpayer counter-filed a Notice of Proposed Adjustment under the formal dispute process, and the dispute ended up with the Adjudication Unit, which is run by the Tax Counsel Office as part of the formal dispute process. The Adjudication Unit did not accept the taxpayer’s counter arguments, including an attempt to claim an income tax and GST input tax deduction for the cost of fresh produce purchased with cash. The problem was there was no supporting evidence for this claim, so the Adjudication Unit probably found it easy to reject it. The Adjudication Unit ruled not only was the tax due, but the penalties were also correctly imposed.

Get ready for more Inland Revenue action

Circling back to our first story, this TDS illustrates what lies ahead for those in the construction industry who have been suppressing income. As I said, I do think Inland Revenue should make everyone more aware of its benchmarking data which would be a warning for would be tax evaders. It’s pretty clear from the announcement about the construction industry that Inland Revenue is gearing up for many campaigns targeting debt arrears and clamping down on tax evasion in particular industries. As always, we will keep you updated as to developments in those areas as they happen.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.