An Australian case highlights the problems around removing GST from food, and as the Government’s financial statements for the year ended 30th June 2023 are released, instead of our tax cuts do we actually need more tax?

Last week I mentioned the retirement of Geof Nightingale and I also surmised that it wouldn’t be long before we heard from him again. And sure enough, this week he popped up on Mike Hosking breakfast show talking about the various tax policies on offer. After a tongue in cheek confession that this had all given him a bit of a headache, Geof then made the very wise suggestion that perhaps it is time to establish an independent fiscal costings unit so that during an election campaign the claims of the various parties can be scrutinised impartially.

As Geof noted, this is actually something the Labour Party proposed in the run up to the 2014 election. Now, given the claims, counterclaims and accusations this week about exactly how many families would gain the maximum benefit from National’s tax proposals, maybe this is something which should be looked at again. On the other hand, someone else has also suggested perhaps we can refer them for false advertising? Probably a bit too late for that really.

Removing GST on food – a legislative headache in the making?

Moving on, the multi-party debate on Thursday night on TV1 threw up several moments of light relief, including when the leaders were asked to comment on National’s foreign buyer tax policy and Labour’s proposal to remove GST from fresh and frozen fruit and vegetables. None of the leaders thought much of either policy.

This prompted moderator Jack Tame to challenge Winston Peters, noting that New Zealand First’s manifesto proposed the removal of GST from food. (For the record, the Greens and Te Pati Māori both propose to go further than Labour on this point). It turned out, however, that New Zealand First had literally just updated their manifesto, dropping the original proposal and instead proposing it would “secure a select committee inquiry into GST off basic fresh foods. We must examine if this would deliver real benefits for taxpayers before legislating for it.”

Maybe New Zealand First’s change of tack on this topic was prompted by a recent Australian tax case. In this case the court ruled that a series of frozen food products were subject to GST and could not be zero rated (or “GST-free”, in Australia’s somewhat peculiar GST terminology). In brief, what happened was that Simplot was marketing six frozen food products such as a fried rice or pasta product, each of which contained a combination of vegetables and seasonings, as well as grains, pasta and/or egg.

The case turned on around what constitutes a kind of food marketed as a prepared meal. If they were food, as Simplot argued, then no GST applied. However, if they were if they represented a kind of “food marketed as a prepared meal but not including soup as per Australia’s GST legislation“, then it would have been subject to GST.

After an exhaustive analysis, including examining the packaging and advertising, Justice Hespe ruled GST applied. But it appears that she was none too happy with the whole process and the legislation. She remarked in paragraph 141 of her judgement

“The legislative scheme with its arbitrary exemptions is not productive of cohesive outcomes. It has left the Court in the unsatisfactory position of having to determine whether to assign novel food products to a category drafted on the premise of unarticulated preconceptions and notions of a “prepared meal”. It may be doubted whether this is a satisfactory basis on which taxation liabilities ought to be determined.”

Now that’s probably justice speak for “You have got to be kidding that we have to do this every time.” But they represent pretty wise words of warning for future drafters of any New Zealand legislation removing GST from food.

More tax, not less?

As mentioned at the beginning, a key part of the election campaign has been the various tax proposals on offer, and particularly promises of tax relief in the form of tax cuts or threshold adjustments. Each of the parties, with the exception of Labour, have something on this. But in Stuff economist and previous podcast guest Shamubeel Eaqub said of both Labour and National that they were, “pretending somehow we don’t have long term big, long term issues that we need to deal with and time is running out.” He continued, “In terms of reaching surplus they are all saying getting back to surplus is important but how do you do it while giving tax cuts and spending on things we’ve already promised ourselves?”

I echoed his comments in part by saying that I didn’t believe the politicians of the two main parties are “being serious enough about funding what’s ahead.” And I noted that it was the coming challenges in terms of the ageing population and in particular related health care and superannuation costs that had prompted the last Tax Working Group to propose a capital gains tax.

Several other commentators weighed in as well, and I’d recommend reading in particular what I thought was some fairly insightful commentary from Gareth Kiernan, the Chief Forecaster at Infometrics. He noted something that’s been a theme of this podcast for some time, that New Zealanders are already paying significantly more tax due to the issue of bracket creep because income tax thresholds had not been adjusted since 2010. Governments had benefited from inflation moving people into higher tax brackets.

But in his opinion, this policy,

“It reduces discipline on government spending and muddies the tax and welfare decision for voters. It would be more appropriate for tax thresholds to be indexed to incomes or inflation, so that if any government wanted to alter the income tax rates or thresholds, they would need to articulate the reasons for their policy.”

He also went on to note,

“..in the current environment, one might argue that there needs to be more investment in infrastructure, and more funding for healthcare, and therefore taxes need to go up to pay for that. Alternatively, one might argue that there has been considerable expansion in government spending in recent years with few results to show for it, so spending needs to be reined in and taxes can be cut to go alongside that change.”

Now, I posted a link to this story on LinkedIn and it provoked a lively debate. A couple of people came back straight away with the reasonable assertions if we cut out wasteful expenditure and enforce the tax legislation, we would have sufficient income and that we may not necessarily get a better economy or better outcomes for people by increasing tax.

What is the state of the Government’s finances?

Now, the question of how much the Government spends is quite relevant in this particular example, because this week and providing some context, the Government’s financial statements for the year ended 30th June 2023 were released.

Tax revenue was up +$3.9 billion on June 2022 to a total of $111.7 billion. But that’s actually about $3 billion less than what was projected in the Budget in May. And the main reason for that fall is that corporate tax income at just under $18 billion, is -$2.4 billion below forecast, although higher withholding taxes on interest and dividend income has somewhat compensated for that fall. The GST take was bang on with what was projected at the Budget ($28.13 billion)

Ultimately the Government overall had an operating deficit before gains and losses of $9.4 billion. There’s been a lot of debate about government spending and core Crown expenses as a proportion of GDP were 32.2% of GDP, which is down from 34.5% in the June 2022 year. And the reason for that is the end of the COVID 19 restrictions and support that was given. Net debt is 18% of GDP, which is incredibly low by world standards.

And actually, here’s something we’ve I’ve mentioned before, but perhaps isn’t really known is that we are currently one of the few countries, according to our financials where the Government has positive net worth.

The government has net wealth of about 46% of GDP, whereas some countries such including Australia, which surprises me, are actually negative. Obviously, the big standout here is Norway, thanks to its trillion-dollar sovereign wealth fund.

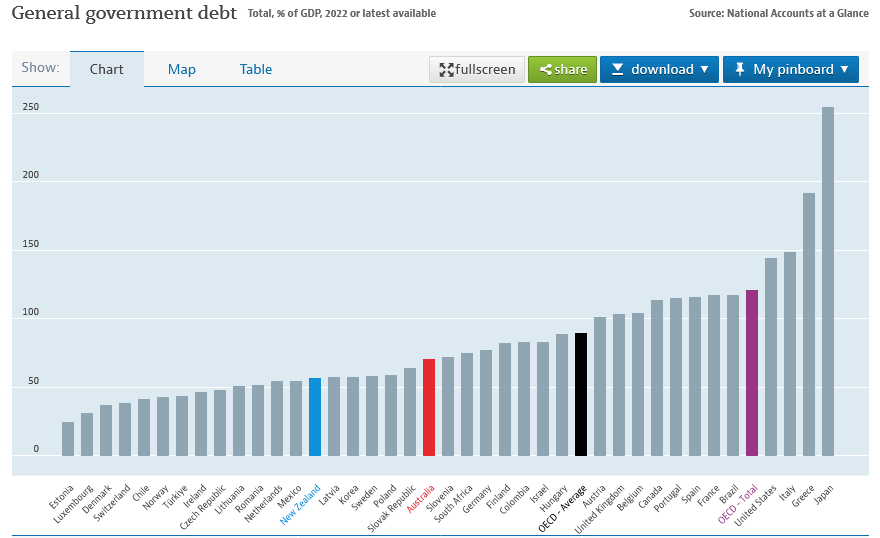

The OCED measures of debt is slightly different, but general government debt is still below the OECD average. But like the commentators who are thinking we should be looking at our spending, I’m of the view we need to be investing in our infrastructure beyond roads.

But one of the things that puzzles me and it’s always brought up about government spending, it seems, is that somehow $55 million was spent on a proposed cycleway across the Auckland Harbour Bridge, which never eventuated. And then there’s a significant amount of money that’s gone into mental health, but yet doesn’t seem to have found its way to the frontline. So, I definitely agree with the view that there’s questions to be asked about the quality of our spending and how effectively it’s deployed is the quality of our public service able to deliver on what’s required? It may mean the answer is a combination that we do need more funding, but also we may actually need to invest in the capacity of bureaucrats to actually deliver.

The climate change bills arrive for Auckland ratepayers and us all

But the key point I want to come back to about the costs ahead which we’re not hearing enough about from the two main parties, is how are we going to manage the impact of climate change? This week, remember, Auckland Council has just signed off on the process of what’s to happen with a buyout of 700 properties that were red stickered following the January and February floods. That’s going to cost a total of $774 million, $387 million of which is going to come from the government.

Of note here and it’s something quite a few people have raised a red flag about, is that although insured Category 3 property owners will receive 95% of the the pre-flood market value, those who were uninsured will receive 80%. This raises the issue of moral hazard – if that’s what’s going to happen why bother insuring.

This is a big issue that I think we have to discuss: how are we going to fund all of this? Then if we are going to be in a scenario where we have to be buying out property owners, is buying out uninsured people fair for the those who have insured themselves? Is this approach a fair cost both to the people in the affected local government area and those generally in the wider population, because that’s who’s funding these buyouts.

In my view this is going to be a bigger issue because, I want to repeat again, we have so much of our wealth tied up in property, and yet property is the asset class that is most exposed to the effects of climate change. We’ve had Auckland with 700 homes, and over on the East Coast there’s another 400 homes, I believe, where this buy out process is underway.

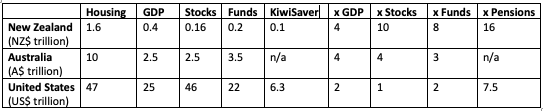

If we are going to be assisting property owners, and I believe we should, is the quid pro quo that the level of taxation on property rises? Bernard Hickey had some interesting stats in his daily Substack The Kākā around how much of our wealth relative to the country’s GDP is committed to housing. A total of $1.6 trillion, or four times our GDP, is committed to housing. But more importantly, although that’s not so out of line with other countries, it dwarfs our other investments

This royally skewed set of incentives is why our housing market is worth NZ$1.6 trillion, which is four times our GDP (NZ$400 billion), 10 times the value of our listed companies (NZX total market value of $160 billion), eight times larger than our total managed funds sector ($200 billion including NZ Super Fund and ACC) and 16 times larger than our only-very-marginally-incentivised household pension funds (Kiwisaver at $100 billion). For comparison, Australia’s housing market is worth the same four times GDP, but is worth four times stocks, three times and funds under management. In the United States, its housing market is worth twice GDP, once the stock market, twice funds under management and 7.5 times its comparable ‘subsidised’ household pensions market, which is known as 401k in America, rather than KiwiSaver.

Bernard believes, and I agree having looked at it when researching Tax and Fairness this overinvestment is a by-product of our tax settings. Therefore, if we change those tax settings around the incentive to invest in property that may change two things. One, we invest in more productive assets. And two, we raise the revenue to help deal with the coming crisis around climate change.

Will the Election change the discussion?

But at the moment it has to be said that funding the cost of climate change is not part of the two major parties’ discussions around tax, but who knows? My view is the debate around tax policy and our tax settings isn’t going to end with the Election next Saturday, it’s going to continue beyond that. In my view these issues around funding climate change will accelerate. If we can come to some form of multi-party accord on this, I think it will be better for us. But tax is politics, so don’t be holding out too much hope for agreement soon.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

With effect from 1st July this year, there was a change in the Child Support system so that from that date whenever a liable parent makes a child support payment, it will be passed on to receiving carers on a sole parent rate of benefit.

Previously, any such payment was used to pay the cost of providing the benefit. This change is designed to put more money in the pockets of carers.

The change begins with child support payments due for the month of July 2023 onwards. Child support payments are paid by Inland Revenue in the month following deduction. The first payment that receiving carers receive under the new system would have been made by Inland Revenue on 22nd August “as long as the liable payment parent makes their payment on time.”

And that is a very big ‘but’. As an article at the start of the week in Stuff by Susan Edmunds notes, as of the end of August over $1 billion of child support was due. slightly down from the amount owed in August 2022. But of that amount owing $488 million represents penalties charged.

Inland Revenue acts as the intermediary in the system. It calculates the amount due and then payments by liable parents to receiving carers are made through Inland Revenue. This is done when parties after a relationship breakdown can’t agree how financial support is to be provided. Under the Child Support Act 1991 Inland Revenue manage this whole process by collecting payments from liable parents and passing them on to the receiving carers.

To encourage prompt payment, late payment penalties are payable. Those penalties have been adjusted recently, but the basic charge is an initial 2% penalty of the amount not paid, and then another 8% is added to that 28 days later, if it still hasn’t been paid. These penalties arise for each payment. So, if you keep missing payments, debt piles up, which is what we’ve seen.

I’ve been a long standing critic of this penalty regime. It leads to large amounts of debt building up, a very high proportion of which represents penalties. As Susan Edmunds pointed out, for the June 2021 year, Inland Revenue wrote off nearly a billion dollars of debt and then wrote off another $181 million in the June 2022 year. The system has been like this for years, basically it’s never worked as well as people thought it would.

Somehow, we have ended up with a system where the penalties for not paying your child support on time are greater than those for not paying your tax on time. Remember Inland Revenue is just acting as an intermediary. As I told Susan, the current penalty system is outrageous. Really, we need to have a harder think about it.

Can pay, won’t pay?

This is always going to be a difficult matter because relationship breakdowns can get very toxic. Resentment builds up and without some form of compulsion/penalty, the system would probably be even more dysfunctional. Still, we’ve got to find a middle way.

Incidentally Inland Revenue also has a right to issue deduction notices which I’ve discussed before. It can issue these to an employer on the grounds that this person owes X and you are to take an extra 10% of their salary when you are applying PAYE. I understand quite a substantial number of the deduction notices are that are issued each year relate to arrears of child support.

But even so, it’s a question, I think, for all of us to think about – why is the system like this and what can we do to make it better? There’s been some tinkering around the edges but really, whoever forms the Government after the Election, this is something I’d like to see them think longer and harder about improving.

FBT interest rates to rise

The prescribed rate of interest applies when someone has taken a loan from a company or is a shareholder/director with an overdrawn current account balance. In such situations interest is calculated using the prescribed rate of interest on that overdrawn balance or loan to determine the FBT payable by the company. This interest rate is to increase on 1st October from 7.89% to 8.41%. As recently as 30th June last year the rate was 4.50% so you can see there’s been a very rapid increase in the rate payable.

The downsides of holding property in trust

A few weeks back Tammy McLeod of Davenports Law was a guest and we discussed the new landscape for trusts in the wake of the Trusts Act 2019. One of the areas we discussed was whether in fact so much property should be held in trust. Are there in fact too many trusts? The reason people set up trusts are manyfold, some tying back to the story at the start of this week’s podcast about relationship breakdowns.

But trusts come with downsides. And one has been illustrated in a story that emerged this week regarding people applying for government assistance following the floods in January and February. It turns out that the assistance package provides up to $160 a week to help with the cost of renting a house because your home has been red or yellow stickered.

However, according to this story from 1News the package only covers displaced homeowners. Those people who have property held in trusts are not covered. And this has come as a quite understandably unpleasant shock for a number of affected people.

The story is also interesting in that you can see a number of common misconceptions about trusts pop up, such as one affected homeowner saying, “I own the trust I have that owns my house. I’ve had it for 20, 30 years”. That’s not the case. You may be a trustee, but you don’t own the trust. And then a representative from Ministry of Social Development who’s handling these claims saying “a trust is a separate legal entity.” No, that’s not the case either, the property is registered in the name of the trustees of the trust but a trust does not have any separate legal status, whatsoever.

This misrepresentation might actually be hopefully a window of opportunity for the affected homeowners. Someone looked at this and think, well, if there are trust beneficiaries who are also trustees living in that house, then technically they are homeowners and they then may qualify for support.

I’ll keep an eye on this story and see how it pans out. But it’s another example of what Tammy and I discussed, at the time a trust was set up, it served a very specific purpose. But over time, life changes and maybe those original purposes are no longer valid. It may therefore be time to rethink and perhaps wind up the trust.

Just on the other hand, like I said at the top of the podcast, you may have gone through a relationship breakdown. You’re going into a new relationship and you may wish to protect your assets from the impact of another relationship breakdown through settling a trust. There are other mechanisms that might apply there, but the use of trusts by parties to second or third marriages is not uncommon.

A public mood for change?

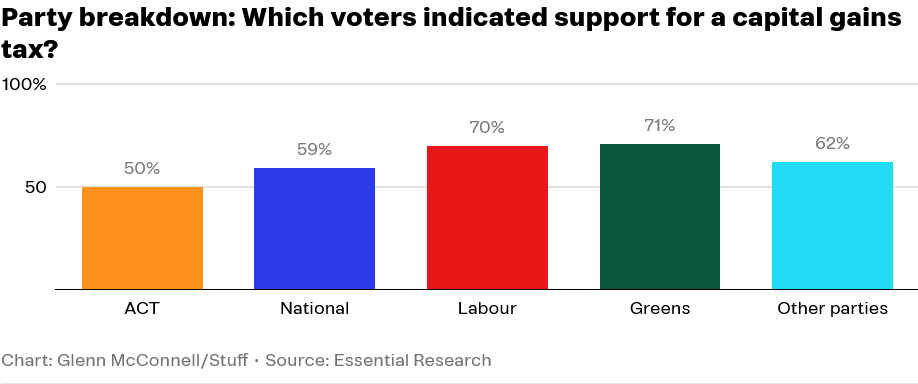

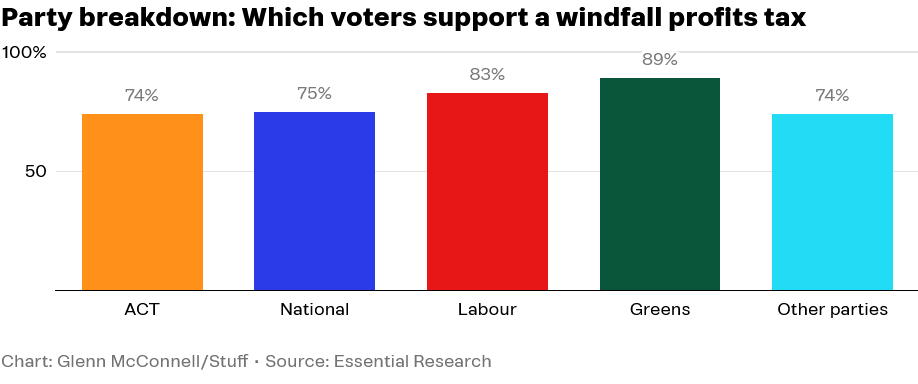

The Election campaign is still rumbling on with just two weeks to go. This week a survey run for Tova O’Brien’s podcast Tova indicates widespread support for taxes on excess profits and capital gains.

Both suggestions have been ruled out by National and Labour but what’s interesting is the apparent cross-party support amongst voters for the proposals.

What makes this poll a bit more interesting is the fact that when it was broken down across the various parties, there was still fairly widespread support for a capital gains tax even amongst National and ACT supporters.

Cross-party support for a windfall profits tax was also surprisingly strong with 74% of ACT supporters and 75% of National supporters in favour.

This is interesting to see and whether any party follows through on any of this is of course a matter which we will only find out after the Election. But even so, the survey perhaps indicates the electorate in some ways thinks there may need to be changes. But on the other hand, as some people rightly pointed out, the Labour Party ran on introducing a capital gains tax in both 2011 and 2014 and got nowhere. Subsequently both Jacinda Ardern and Chris Hipkins ruled out capital gains tax on their watch. The question remains where exactly does the political will amongst the electorate really lie on this issue?

Haere ra Geof Nightingale

Finally this week, haere ra to Geof Nightingale who retired yesterday as a partner from PWC after what can only be described as an distinguished career. Amongst his many accomplishments Geof was a member of the last two tax working groups and has been one of the leading tax professionals in the country for many years. As the many comments on his LinkedIn post announcing his retirement attests, I am one of many he has given sage advice and guidance and it was a delight to have him as an early guest of this podcast. I’m sure this won’t be the last we hear from Geof on tax but for now thank you Geof and go well in your new direction.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week The Post published a story about Roger and Shaun Nixon, father and son landlords who by The Post’s calculation owned at least 111 residential and lifestyle properties either in person or through a combination of trusts and companies. (In total across various entities and including commercial, industrial and retail properties the pair apparently own over 300 properties across the length of the country from Kaitaia to Invercargill, including properties on Waiheke Island and Omaha, where former Prime minister Sir John Key had a holiday home).

The story was produced as part of The Post’s Mega Landlords series, and I spoke to journalist Ged Cann on the question whether many of the homes in this property empire would ever re-enter the market for sale. As I explained, at the moment there are no tax incentives such as a capital gains tax or an inheritance tax (what we used to call Estate Duties), which could force the break-up of the Nixon’s holdings.

Estate and Gift Duties were first introduced in the 1890s, and were in part designed to provide a relatively good source of revenue for the Government, but they were also a means of breaking down large estates. The Liberal government of the time was concerned about accumulation of excess wealth and the related issue of inequality which drives a lot of discussion in this area. Inequality will exist in any society, no matter what the tax setting settings are. I think it’s a by-product of any modern capitalist society. Some people are extremely able to use their advantages of natural and inherited capital to make fortunes. And by and large, I don’t have a problem with that at all.

The question we should be addressing is how far we are prepared to accept inequality and what strains it puts on our social system. It’s a difficult question to answer. We have seen a rise in inequality since the 1980s and the end of the post-war consensus where higher taxes were seen as means of equalising society. And I spoke to Ged about one of those tax tools used, Estate Duty which disappeared just over 30 years ago.

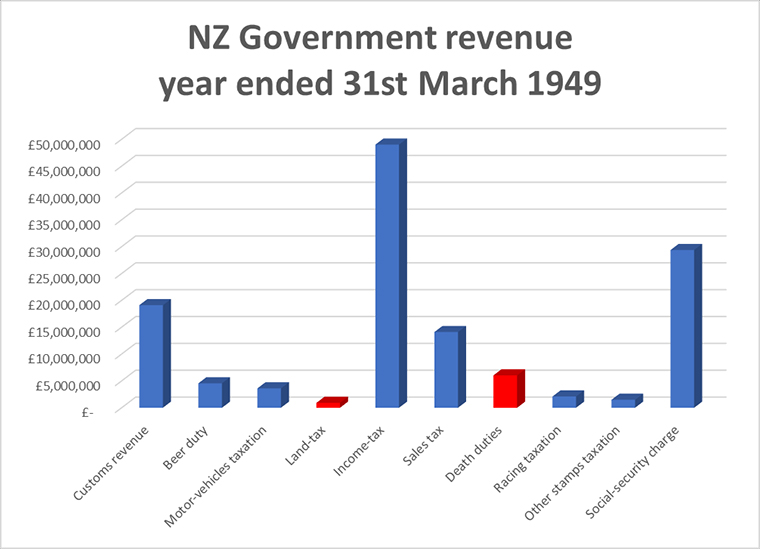

Estate and Gift duties were quite a substantial part of the tax revenue for New Zealand governments for a long period of time after the 1890s, right up until probably the turning point with the election of the First National Government in 1949. For the year ended 31st March 1949 the total amount of land tax, estate and gift duties amounted to just under £7 million of the government’s £130 million revenue. In other words, it was the equivalent of 5.3% of the total tax take for that year. If you were to project that forward, it would be the equivalent of $5.7 billion using the June 2022 numbers. So, these taxes were a very significant proportion of past governments’ revenue.

Whatever happened to Estate Duty?

Starting with the election of the First National Government the exemptions from Estate Duty were widened. This started to undermine the theory we’ve often discussed here and which I strongly support, of a broad based, low-rate approach to taxation. The broader the tax base, the lower the tax rate you can apply. And to a large extent this was the case with estate and gift duties.

But what happened was that exemptions for Estate Duties (and Land Tax) began to be expanded. And therefore, as the exemptions expand, the tax base is narrowing and then the tax take starts to fall away. And gradually, over time, the numbers diminished to the point of insignificance. Land tax was abolished in 1990 and Estate Duty reached its end point in 1992. Gift duties, for whatever reason, lingered on until 2011, before they went on the not on reasonable grounds that the barely $2 million revenue collected was far outweighed by the compliance costs.

The question that should come up is whether, in fact, the abolition of Estate and Gift Duties was a wise move on two points, firstly for maintaining a broader tax base. And secondly around this question of inequality, because Estate Duties are something that can hit estates very, very hard particularly where perhaps too much is tied up in illiquid assets, such as property. This is something I’ve seen quite a lot in the UK with the effect of what is now called Inheritance Tax.

To repeat a point I have made before, the absence of Estate and Gift Duties makes our system unusual because we don’t have a capital gains tax. (We’ve also removed stamp duty although by and large, tax theory has that stamp duties are pretty inefficient taxes. Still, they linger on everywhere else). So, we have no taxes which could be part of breaking down large estates. We have to accept whether that’s a good or bad thing.

Following IAG’s move do we need to broaden our tax base to deal with climate change?

My view is that we ought to be thinking about the question of broadening our tax base. And in that context, I’ve been thinking quite a bit on this question of estate and gift duties, because this week there was another reminder of an issue I keep raising – the growing costs of dealing with climate change.

The insurer IAG announced this week it will not offer ongoing insurance for properties in Category 3 of the Government’s Land Categorisation framework for regions affected by the floods earlier this year.

The cost of the property damage this year by those events is currently several billion and climbing. Of course, property owners are the persons that are most closely affected.

One of the doubts I have about National’s proposed foreign buyers tax is about the type of properties foreign buyers are likely to be purchasing. In Auckland, there is a growing number of suburbs where the average price is $2million. But foreign buyers aren’t necessarily wanting to buy a rundown villa in Grey Lynn or Devonport, they’d probably be looking at flashier properties in coastal areas. However, these coastal properties could now be more exposed to climate change which could be a factor in them deciding not to purchase.

Of course property owners, maybe including the Nixons, have already been affected by climate change and if they are struggling to insure their properties, they will be looking to the Government for assistance with this. And so it seems to me we are rapidly reaching a break point because we’re not taxing capital and property in particular. This is going to create a huge issue between those on one hand who have property and want government assistance when their property is flooded out or damaged beyond repair and insurance is limited or not available. On the other hand, there is a group who don’t have property and can’t get onto the ladder, who will, through their taxes end up paying for the former. This dichotomy sets up a whole social strain, which I don’t think we really want.

To repeat, the thing about this story of the megalandlord Nixons is how it illustrates to me this dilemma we have created around the taxation of capital and the preference for property as an asset class.

So why is the New Zealand Super Fund taxed?

There were some very interesting responses to last week’s commentary about the New Zealand Superannuation Fund’s (“the Super Fund”), retiring CEO Matt Whineray’s remarks on the fund’s tax status. (Thank you again to all my readers and listeners for your contributions). The question was asked, ‘Well, why does it pay tax?’ The answer, as I indicated in last week’s podcast, it was designed as such when the Super Fund was being set up prior to when it actually started investing 20 years ago this month.

“There are two main issues surrounding the tax status of the proposed super fund. The first of these is the tax avoidance opportunities that would be created if the fund was tax-exempt. The second is whether poor incentives would be created regarding investment behaviour.

…By making an entity tax exempt, the government effectively gives it an asset that it can trade with taxable entities. Current tax-exempt organisations such as charities have engaged in complicated schemes to take advantage of this kind of opportunity. …

We consider that making the fund tax exempt will create an opportunity for this kind of avoidance activity.”

The driving force of this paper was concern that giving the Super Fund tax exempt status would give it poor incentives. And so, the fund was set up on that basis. (It’s also interesting to note that the paper assumed the Super Fund would be contracting out most of its fund management activity. However, as we know, the Super Fund is now one of the largest fund managers in the country).

Changing the FIF rules

Back when the Super Fund was being established the tax treatment under the foreign investment fund regime was very different. There was what we call a “Grey list” that applied to investments in several countries such as the US, Australia, UK, Germany, Japan and others. Investments here were only taxed on dividends and capital gains would be taxed under the normal rules, similar to those we have now for investing in Australia and New Zealand. The amount of tax payable on these investment would not have been quite significant under those rules.

However, in 2006, proposals were introduced establishing the current Foreign Investment Fund regime which took effect from 1st April 2007. Now, the interesting thing is that I cannot see any commentary or submission to the Finance and Expenditure Committee by the New Zealand Super about the changes, although there’s plenty of commentary from the Corporate Taxpayers Group and others. As I mentioned last week, some 3,400 submissions opposed the changes, and only two were in favour. So of course, the measure went ahead.

From that point the New Zealand Super Fund started to pay a lot more tax. (In the year to June 2008 the fund had a loss of $704 million but had a net tax bill of $164 million because of the changes to the FIF regime). The effect of the FIF regime was described in a submission the New Zealand Super Fund made in 2018 to the last Tax Working Group. It said it would like to be tax exempt because as I noted earlier it’s the only sovereign wealth fund in the world which is taxed. Its tax status also creates some issues when it is investing overseas. In support of tax exempt status, the submission (signed off by then acting CEO Matt Whineray) noted.

“The fund’s tax position can be volatile depending on the performance of the fund and the contributors to that performance. This is often illustrated by our effective tax rate. For example, our effective tax rate was 3% in 2015, 96% in 2016 and 20% in 2017. The main driver of this volatility is how our physical global equities are taxed under the fair dividend rate regime. In simple terms, this means that in any given year, if our return in global equities exceeds 5%, then our tax rate will be lower than 28%. And if our returns are less than 5%, then our tax rate will be higher than 28%.”

Another interconnected issue for the Super Fund is that as so often is the case, I think Governments rather like the tax revenue from the Super Fund. However, as the Fund’s Tax Working Group submission noted if it was tax exempt it would not be forced to sell assets to pay “the Government provisional tax with the Government then turning around to pay the Fund contributions, thereby removing the need for practical work arounds in terms of offsetting provisional tax”.

As I said, way back in 2000 when they were considering the tax status of the New Zealand Super Fund, the FIF regime was very different. And I wonder whether if they had foreseen the impact of the FIF regime that was introduced from 2007, whether they might have rethought the decision to tax the Fund.

Act is now accepting that cannot happen but instead the top rate from 2026 will be 33%. What it has also said, and this is interesting, is that the top 39% rate will remain until then.

One of the proposals in ACT’s “Alternative Budget” is the Government will stop making contributions to the New Zealand Super Fund. But what won’t change, however, is the tax status of the fund, and it will still be taxed.

Now the ACT numbers are quite detailed, and they note that the expected tax revenue from the New Zealand Super Fund will actually drop by about $100 million over the three years to June 2027 period because of lower Government contributions. (Incidentally, in measuring debt-GDP ratio ACT’s Alternative Budget excludes the $65 billion value of the NZSF which rather unfavourably distorts the ratio).

ACT also proposes winding back the KiwiSaver member’s tax credit (the Government contribution you receive if you make contributions of at least than $1,043 a year), for higher income earners. Instead, it will be capped at 5% of a participant’s taxable income. The maximum subsidy amount will reduce by 3% per dollar of income above $48,000, reducing to zero by around $65,000.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Tax continues to feature heavily in the Election with the ongoing debate over the validity or otherwise of National’s proposed foreign buyer tax. But away from the election, it has been a busy week in the tax world. By far the most interesting story, partly because of its source, but also how it speaks to the structure of our tax system, is the commentary from Matt Whineray, the outgoing chief executive of the New Zealand Superannuation Fund (NZSF), about the fund’s tax status.

In an interview with the New Zealand Herald’s Markets with Madison, he remarked on the NZSF’s tax status, noting that since the fund began investing in 2003, it had paid nearly $10 billion in tax, including $2.2 billion for the year to June 2022.

This makes it by far and away the largest single taxpayer in the country. He thought this was rather nonsensical and that the fund really should have tax immunity status in line with many other sovereign wealth funds around the world, (including ACC and the Reserve Bank of New Zealand, both quite substantial investment funds). “My wish would be that we didn’t pay tax because I think that would solve a few issues.”

A nonsensical money-go-round?

He questioned the practice of the NZSF returning money to the Crown in tax, and the Crown in return contributes to the fund annually. “If I take my wallet out of this pocket and put it into this pocket, I haven’t got richer.” The problem, in his view, was exacerbated when the Crown stopped contributing to the fund completely, as it did for almost a decade between 2009 and 2017.

It’s interesting to hear such commentary from Matt Whineray, which highlights an anomaly about the NZSF, in that it is a sovereign wealth fund, but it pays tax, which is highly unusual around the world. In fact, I’m not sure there are any other sovereign wealth funds which do pay tax. (It’s an issue Whineray’s predecessor Adrian Orr also raised, ashas Whineray previously).

Now when the NZSF was set up 20 years ago, the rationale behind it paying tax was this would help it make sound investment decisions based on investment principles and not by tax considerations. And in a broader sense, that’s not unreasonable. I always tell my clients, don’t let the tax tail wag the investment dog. Think in the longer-term investment and returns rather than the short, potentially shorter-term tax implications.

A “Fair” Dividend Rate?

Someone else this week commenting on this question of the tax status of savings was financial planner Rachelle Blanch speaking to Susan Edmonds of Stuff.

Rachelle thought it was time for a review of the Foreign Investment Fund (FIF) regime, particularly in relation to how it applies to portfolio investment entities such as KiwiSaver funds. Now, the FIF regime and the Financial Arrangement regime are the two main reasons the NZSF pays so much tax. That’s because both regimes tax unrealised gains and there will be substantial unrealised gains in investment funds.

As the story in Stuff noted, under the FIF regime KiwiSaver funds and the NZSF must use what’s called the fair dividend rate in respect of their overseas shareholdings. This deems 5% of the opening market value of the investments held at the start of the tax year to be taxable income. Now obviously as KiwiSaver funds grow in size, and they diversify out of the New Zealand market as the NZSF has done, then the amount of tax payable as a consequence of the FIF regime will increase. However, unlike individuals or trusts, who can switch methods to mitigate the impact of a drop in values of some of investment funds by adopting what we call the comparative value method, KiwiSaver funds and the NZSF can’t do that.

How much tax is payable under the FIF regime is not at all clear. The NZSF is probably the only entity which can give a pretty accurate gauge on that. But to give you some idea of the total tax that might be payable – the Financial Markets Authority produces an annual report each year on KiwiSaver funds, and it notes that for the year to June 2022, KiwiSaver funds paid over $256 million in tax for that year. Remember in the same period, the NZSF paid over $2.2 billion.

Rachelle Bland has raised a very good question as to whether, in fact, this is an appropriate tax policy response where people have long term savings. She describes it as effectively a capital gains tax. Another way of looking at this, and it’s how I describe it whenever explaining the regime to overseas clients, is that it operates as a quasi-wealth tax.

As I said, there’s no mitigation for significant falls in stock markets. Unlike a capital gains tax regime which taxes on a realisation basis you can decide to realise capital losses and offset them against capital gains. You can’t do that under a FIF regime. Therefore you have this situation where the value of investments are falling but you’re still paying tax on the value of those investments. And that’s been the scenario for quite a few funds over the past 12 to 18 months.

What about a tax exemption then?

It’s not surprising then that quite apart from this anomalous washing – as Matt Whineray referred to the process of cycling funds from the Crown to the NZSF and then back in the form of tax – there’s also calls for some form of tax exemptions for KiwiSaver funds. You see such tax exemptions around the world for other pension schemes. New Zealand is yet again, a bit of an outlier here. The reason such exemptions were taken away in the late 1980s is they are costly. However, in overseas jurisdictions where tax exemptions apply to pension schemes withdrawals are taxed, whereas in our system we apply what we call a tax-tax-exempt approach where the contributions are made out of after-tax income, the schemes are subject to the ordinary taxation rules, but any withdrawals are exempt.

What’s the most effective approach? Well, that’s still a matter for debate. But one thing to keep in mind is that tax does have an impact on the long-term return of funds. Now, whether anyone is going to do anything about this is very questionable. The FIF regime in its current iteration has been in place now since 1st April 2007, and it generally works pretty well. The rules were very controversial when they were first proposed. There was an absolute storm of protest when they were first proposed, with Parliament’s Finance and Expenditure select committee receiving 3,400 submissions against the introduction of what is now the FIF regime, and only two in favour. In the face of this criticism, they were actually reshaped and now everyone has got used to working with the regime.

And this perhaps is the critical point. Governments appreciate the tax paid by the NZSF and KiwiSaver funds. The total tax for the year ended 30th June 2022 from those two sources probably represents just about 2% of the total tax take for that year. Therefore, changing the tax treatment for the NZSF and for KiwiSaver Funds would be an expensive move even if as a trade-off the Government might not then need to make any more contributions to the NZSF.

Wrong sort of investment signals?

Given the short-term pressures at the moment on the Government’s books, I think any move in this area is not going to happen. But I also consider it underlines a scenario where we’re prepared to tax savings under the current tax system, but generally whole asset classes, such as property, the bright line test excepted, are outside the tax net. This treatment sends an investment signal which politicians aren’t prepared to address.

Where does investment get directed? The evidence we have points to it being directed into relatively unproductive residential property investment as opposed to the likes of KiwiSaver funds, which will invest in productive businesses.

The discussion we’re not having

Now, this is a discussion we’re not having at the moment about how the tax system and investment interacts. As I’ve said in previous podcasts when you consider National is proposing removing commercial property depreciation on non-residential property again, (as is Labour for its part) in both cases to fund some form of tax cuts this to me sends the wrong signals. We’re basically directing funds away from investment in our economy into consumption.

But this is not a discussion we’re going to have because although politicians quietly recognise that whatever we the electorate might say about the impact of tax in the back pockets – and we’ll happily all take tax relief, tax cuts, how you phrase them – we also like the services tax provides. So, this dichotomy exists. We’ve got to maintain services as far as possible but not want to pay for them. But as I’ve said repeatedly, I think the under taxation of capital is an unsustainable position long term.

Donations tax credit review announced

Moving on, Inland Revenue just carries on carrying on regardless of whether the Government is out campaigning. It has been busy churning out quite a lot of interesting material. But two particular initiatives happened this week.

Firstly, on Friday, it announced it is going to undertake a review of the rules relating to the donations rebate rule. This review is part of the Regulatory Stewardship programme required of all state agencies in respect of the rules they administer. In this case, a review is going to assess whether the donations tax credit regime is operating effectively, is achieving its policy intent, and how it compares internationally.

Inland Revenue will open up consultation with an aim of undertaking this review and completing a report, setting out its findings as well as any recommendations by mid-2024. Interested parties will be contacted on this. I imagine you can expect the Charities Commission, some more major charities, would be approached. I think the main accounting bodies, together with the New Zealand Law Society will also be approached for comment on the matter.

A fairer Government debt policy framework?

The second Inland Revenue initiative and probably something that’s going to have more immediate impact ties into the rather strange case we talked about last week involving the Nelson woman who got herself into a whole heap of trouble with Inland Revenue and decided the best way out of avoiding a $365,000 tax debt was to sell her property worth $845,000 to a UK company. The Official Assignee took a dim view of the idea and obtained a court order striking the sale down.

Leaving aside the oddities involved the case is relevant for the important question of tax debt and other debt that’s owed to the Government. According to the New Zealand Herald story reported last week, as of 30th June 2023 Inland Revenue is owed nearly $5 billion.

Now, both the Tax Working Group and the Welfare Expert Advisory Group took a look at the question of debt owed to the Government as part of their reviews, and they recommended there should be some form of all of government approach to debt. Firstly trying to prevent debt arising with the Government, but also how each relevant government agency responds and manages that issue.

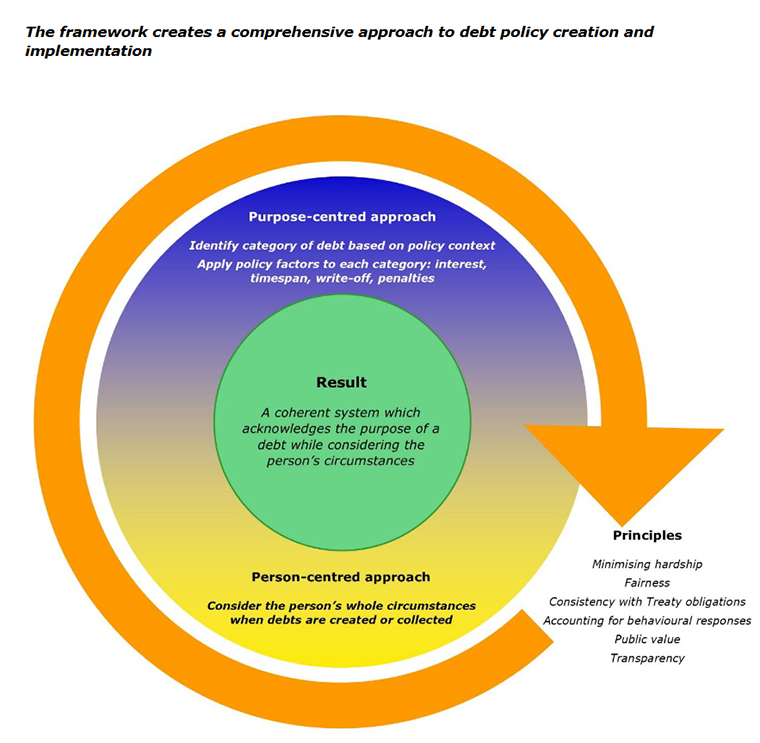

Consequently, a policy framework for debts the Government is owed has now been developed and has been signed off by the Cabinet. Inland Revenue this week released its report and background details on this framework.

There’s quite a bit to consider in here, not just the $5 billion Inland Revenue is owed but the other debts built up, primarily with the Ministry of Social Development and also with the Ministry of Justice.

According to this report, at present 762,460 New Zealand residents collectively owe $4.68 billion of debt to these three agencies – Ministry of Social Development, Inland Revenue and the Ministry of Justice. More than a quarter of these persons owe debt to two or more agencies and 6% that’s over 45,000 people owe a debt to all three. Furthermore, around three quarters of this debt, so that’s well over $3 billion, is owed by low-income individuals, many of whom rely on government benefits as well. 13% or just over 99,000 people owe more than $10,000 to the Government.

More than 85% of those who do owe a debt have owed it for more than a year and about 45% cent, an incredible number, have owed debt for at least four years. Finally, Māori and Pacific people are overrepresented in almost all categories of debt a sadly quite typical issue.

The debt policy framework is trying to ensure is that debt recovery is fair and effective and avoids exacerbating hardship. And above all, it aims to prevent debt occurring in the first place and not exacerbate issues.

There are three main parts to the framework. Firstly, a set of overarching principles for creating and managing debt. Then secondly, a purpose centred approach which classifies debt into different groups according to the policy purpose and discusses how different settings might be appropriate for some purpose and others. And then finally, what’s called term to person centred approach, which takes into consideration the personal circumstances, with focus on consideration of financial hardships, as I said.

These debt issues tend to exacerbate and build on each other leading to a circle of despair. $10,000 of debt doesn’t sound like a lot, but for very low-income people it seems like an insurmountable mountain.

Anyway, this framework has been signed off by the Government after feedback from quite a number of interested agencies. For example, the Citizens Advice Bureau, the Methodist Alliance, the New Zealand Council of Christian Social Services, the Salvation Army, and a whole range of other non-governmental organisations. Hopefully this feedback will build a better framework for the practice of managing this debt.

Good but Inland Revenue also needs to do its part

I welcome this initiative, but I also think that as part of it, Inland Revenue needs to be also considering its approach to debt management, such as the effectiveness of the late penalty regime, and how efficiently it is on top of managing debts, because if the debts get away from people, they just give up. That’s what my experience has shown time and again and it’s also what Inland Revenue has experienced.

I think it’s still a good step forward, particularly, in trying to bring a coordinated approach because there’s nothing more infuriating to someone who might be unlucky enough to find ourselves in a position of debt with two or three agencies, and finding that the approach taken by each of those agencies is different.

The Tax Working Group recommended a single Crown agency to manage current debt should be established to deal with this issue. That does not seem to have been part of these recommendations at the moment, maybe it might be picked up at a later stage. Nevertheless, it’s a step forward in the right direction and we’ll hope that it starts to address these issues of managing the debt fairly and efficiently for people.

The $5 billion PREFU hole no-one is worried about

And finally, this week, back to the Election. We’re still hearing plenty about tax in the election campaign. Politicians are all out on the trail telling us everything that’s going to happen or not happen. This week the formal opening of the government books happened with the release of the Pre-election Economic and Fiscal Update (PREFU). There was plenty of differing interpretation about the state of the government’s finances going forward.

But there was a wonderfully interesting little snippet which Newsroom picked up on, and that was the impact of next year’s Matariki public holiday. Matariki always falls on a Friday, and next year it falls on 28th June, which is the last working day of the fiscal year to 30th June 2024. And because of that, the cash that would come in on that day, which represents about $5 billion of GST and provisional tax won’t actually hit the Government’s coffers until the following Monday, which is 1st July and the start of the following tax year. So, on the face of it, the Government’s going to be $5 billion short of cash for the current year ending 30th June 2024.

As a Treasury spokesperson said, “This public holiday effect is expected to affect the Crown’s tax receipts but not tax revenue, since Inland Revenue will calculate accrued tax revenue as at 30 June 2024 as it normally would at any other year end.”

And for the record, this won’t really affect individuals because we file tax returns to 31st March each year. Furthermore, Inland Revenue won’t penalise people for making a payment on 1st July, the first working day after it was due because Inland Revenue hasn’t switched over to a seven-day banking. So nice quirky little story to end the week.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A few weeks back, an issue emerged over in the East Coast and here in Auckland about the potential application of the bright-line test to homeowners who had been forced to move out following Cyclone Gabrielle and the January and February flooding events. The issue was if they had to leave the property for more than 12 months while it was being repaired or because they could no longer live there, the bright-line test could apply if they were forced to sell within the relevant bright-line test period.

The Government this week announced that it is adding a Supplementary Order Paper (SOP) to a tax bill that’s going through Parliament at the moment (and which will be enacted after the election).

The SOP contains proposals to ensure that the main home exclusion from the bright-line test is not affected by a property owner needing to vacate their North Island flood or cyclone damaged home for more than 12 months so it can be remediated or repaired. It also ensures the bright-line and other land-based timing tests, because we have a number of them, are not triggered when local authorities or the crown buyout properties impacted by the 2023 Auckland flood events and or Cyclone Gabrielle. You’ll recall that last month Auckland Council and the Government agreed to a $2 billion package which will be used to buy out homes that were rendered unliveable following Cyclone Gabrielle or the Auckland Anniversary weekend floods.

So, this is a good result. That’s the problem with tests, they can have some harsh results. But as the Government said, by picking up examples from what happened following the Canterbury earthquakes, it will devise tests to ensure that those harsh treatments do not follow.

Fooling around and finding out…

And speaking of harsh treatments, some harsh lessons were learned by a couple of taxpayers about tangling with Inland Revenue. In the first, an Auckland second hand car dealer has been sentenced to six months community detention for tax fraud. The offender Mr Levada created a false identity and then as a director and shareholder set up two companies. The companies were then used to obtain GST refunds totaling $309,000 even though neither company traded. There was a bit of a hard story behind this in that he wanted to help his wife’s family in Ukraine. But he admitted that he knew he was stealing and he has repaid the full amount owing.

Apparently, this got picked up by the Ministry of Business, Innovation and Employment in April 2021. And then obviously from there Inland Revenue realised what was happening. To me this is another example of why we really ought to think hard about GST compulsory zero rating between GST registered businesses. It reduces the opportunity for people to try and defraud the system. They don’t always get away with it, as we’ve just seen here. But maybe remove the temptation in the first place is where I would go with my suggestion.

Avoiding tax by forgoing all income?

But that story is really quite tame compared with a story from Nelson in the New Zealand Herald. As I told the reporter this is an “absolutely wild story”. Mila Amber had run into trouble with Inland Revenue and at the end of 2017 she was told she owed at least $110,000 in taxes, penalties and overpaid Working for Families tax credits. (In fact, the final figure was amended to nearly $365,000).

Amber decided to devise a scheme in cooperation with a UK based company under which she sold her property in Nelson to this company for $847,000. The buyer didn’t have to pay a deposit or any interest and just would simply pay off the property over 25 annual payments with the first payment due a year after settlement. The deal meant that the property was out of the reaches of Inland Revenue if they were going to try and seize the property or force a sale to pay off the debts. Amber was made bankrupt, and the Official Assignee took the case to court to try and overturn the sale. Which is how all these details emerged.

It’s just quite staggering what was attempted and what people thought was going to happen here. This seems to have been one of those cases where the taxpayer got really enraged by Inland Revenue’s actions. She changed the name of her trading company to Abbey Services (Killed by Tax Maladministration) Ltd which as the judge in the decision, called it rather unsubtle and refused to acknowledge the name basically in the judgement. The judge overturned the sale effectively transferring the property to the Official Assignee.

The judgement includes this rather jaw dropping line “It’s hard to see how it is beneficial to avoid tax by forgoing all income” which may be true but didn’t work out for Ms Amber. As I told the Herald, as the property seems to have been mortgage free she basically did herself out of half a million dollars. She’d have done better to have sold the property, pay the tax and move on.

I use this case to repeat something I’ve said many times previously. When you run into trouble with your taxes, talk to Inland Revenue. Go forward and initiate action and in most cases, if you are making reasonable offers and reasonable attempts to meet your liabilities and Inland Revenue can see that you’re being reasonable in your approaches, it will be prepared to find a way forward for everyone. In this particular case going around renaming your company Killed by Tax Maladministration and entering into a quite scandalously scheme to avoid those liabilities got the taxpayer nowhere.

I also think H.M. Revenue and Customs might be very interested as to what was going with the UK company involved. And I would put good money on details of the case having been shared by Inland Revenue with HMRC. I know from experience that Inland Revenue and other authorities share information on a proactive basis. We’ve talked in other podcasts about the Common Reporting Standards for the Automatic Exchange Of Information. Tax authorities are sharing data on a vast scale now.

The cases of this Nelson lady and the second-hand car-salesman are more examples of never underestimating Inland Revenue because it may appear slow, but it will eventually catch up with you.

Having just talked about international tax agreements, it’s very interesting to see the continuing debate around National’s tax proposals, which I discussed last week and in particular the issues around the proposed foreign buyers tax. This has led to quite a debate with National confident that its numbers stack up and that it is legally possible.

The question raised last week continues to be asked ‘Well what about international tax treaties and the so-called non-discrimination clauses?’ It turns out that just after last Friday’s podcast was recorded, National went and sought advice from Robin Oliver, a former Deputy Commissioner of Inland Revenue, member of the Last Tax Working Group and a real guru of tax.

He told RNZ, this is a “very esoteric” area of tax law but it should be possible to introduce the tax.

In his view it would depend on tax residency, not nationality. In relation to the Chinese double tax treaty, it doesn’t allow discrimination on the basis of nationality. The potential argument is that a Chinese national residing in China who purchases property in New Zealand could be subject to the new law, whereas a Chinese national resident in New Zealand could not.

But even if it could be done, I’m of the view whether you should do that. Both myself and Eric Crampton the chief economist of the New Zealand Initiative think tank, told RNZ that, ‘Well, yes, it might be doable, but on the other hand, what would it do for our reputation internationally?’ We build our trade agreements around being an honest broker in this, that we follow a rules-based approach.

A point that was made at the recent International Fiscal Association trans-Tasman conference is that these tax treaties are often related to trade agreements. So, these sorts of issues would have been on the table and part of the discussions. Having signed an agreement fairly recently and then now looking to apply a workaround to tax nationals from that country doesn’t look good for our international reputation.

Just because you can doesn’t mean you should

What this comes back to is a situation myself and other tax advisers I’m sure will sometimes encounter where we’re asked to advise on something. We look at it and come back and we say, ‘Well, looking at the way the law was written we think it’s possible.’ But then sometimes the question boils down to ‘Well you could, but should you?’ Sometimes in tax just because you can doesn’t mean you should.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.