It’s been a busy week in the tax world. The Taxation Principles Reporting Bill passed its third reading in Parliament and very shortly will receive the Royal assent. Now this was the bill introduced at the time of the May Budget, the purpose of which was to provide a statutory reporting framework and required the Commissioner of Inland Revenue to provide the Minister of Revenue with an annual report on the operation of the tax system.

This report would outline aspects of the tax system against a set of tax principles such as equity, efficiency and certainty. As commentary provided by Inland Revenue to the Finance Expenditure Committee noted. “These principles are often considered when designing changes to a tax system”.

Tax being political the Government also wants this bill to

…help improve the public’s understanding of the tax system and encourage informed debate about its future. New Zealand has seen several Tax Working Groups and Committees over the last 20 years, with the most recent being the 2019 Tax Working Group These reviews have offered useful insights into the operation of the tax system and suggestions for improvement. These reviews have also highlighted areas of the tax system where information is lacking, which makes a fully informed debate on some aspects of the tax system more difficult.

The bill requires the Commissioner of Inland Revenue to prepare and publish an annual report which considers the tax system measured against the principles included in this bill.

What will happen is Inland Revenue will produce a short form report annually with a full report every three years. The first full report will be produced in 2025 with the shorter version reports produced in the interim years starting later this year. The intention is to align the requirement for this report to be produced the second calendar year of each parliamentary term.

There’s been some discussion around whether we need this bill and how does it sit within the Generic Tax Policy Process (GTPP)? You could say it’s an extension of the GTPP and of course, it does mean that we can have a look at some of the tax policies that have been put out by the various parties and compare them against the principles set out in this bill. And I’ll be doing that a little later on. The politicians may find this new bill is something of a double edged sword.

A Digital Services Tax just in case…

It so happens a digital services tax bill was introduced on the last sitting day of this parliamentary term which is a bit of a surprise. Digital services taxes (DST) have been talked about for some time but have generally not been brought into effect. They’re obviously not favoured by the targets, the digital giants such as Google and Facebook. But they are a tool that many governments around the world have been considering implementing.

The ongoing OECD Pillar One and Pillar Two negotiations are intended to eliminate the need for these taxes. In fact, it’s a condition of the introduction of the OECD model that any digital services tax in effect would be repealed.

The Government’s actually been looking at a DST for some time. There was a discussion document back in 2019 on the topic. That said, it still was a bit of a surprise to see this bill pop up at this particular time. Arguably, you could see it as a bit of politicking. The key thing is the Government is already committed to not introducing a DST until 1st January 2025 at the earliest. Now Inland Revenue and Treasury have said it will be handy to have the legislation ready just in case the OECD deal falls over. So that’s a reason given for this bill being introduced now.

The DST would target multinational multinationals with global revenue in excess of €750 million per year from digital activities and New Zealand revenue from these activities which exceeds $3.5 million per year. The DST taxes the revenues rather than the profits, because then it doesn’t require trying to establish a connection with a multinational’s physical presence in New Zealand. The rate to be proposed is 3%, pretty standard compared with others around the world.

This bill is a more fallback measure and it’s interesting to see where it stands that they’ve made this move now. But many countries have DSTs, Britain is one, France another and India is probably the biggest exponent of them. And as I said, the Government’s basically saying, ‘We want this in our back pocket in case the OECD Pillar One and Pillar Two deals fall over.’ These are still very much up in the air for discussion, as we’ve mentioned in previous podcasts.

National unveils its tax policy

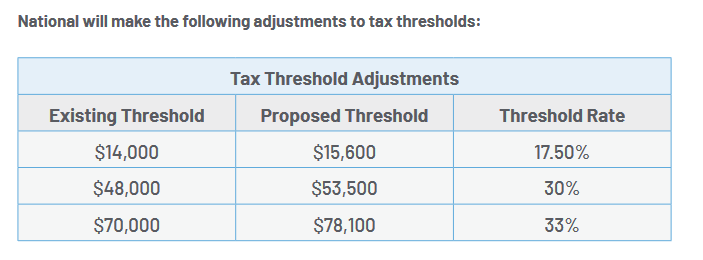

But the big news this week would have been the launch of the National Party’s tax policy on Wednesday, and it landed with quite a thump and contained quite a few surprises. National had already signaled well in advance that it proposes to increase thresholds by 11.5%. As regular listeners to this podcast will know my view is tax threshold increases are long overdue.

What about Working for Families abatement?

National has an identical proposal to that of Labour to increase the Working for Families In-Work Tax Credit by $25 to $97.50 per week starting next April. There’s a commitment that the current $42,700 abatement threshold for Working for Families will rise to $50,000 from 1st April 2026. This is also a Labour Party commitment. But as I said to a number of media outlets, the problem is that the Working for Families abatement threshold already kicks in at very low level and in fact if they had been adjusted for inflation since the last adjustment in July 2018, it would now be $51,800.

Both parties promising to raise the threshold to $50,000 in three years’ time is frankly a little off in my view. It just compounds the problem these families at the lower end of the income scale face with what we call high effective marginal tax rates because of the abatement level of 27 cents per dollar above the $42,700 threshold. This issue isn’t being addressed but instead the can has been kicked down the road.

But on the other hand, there is the proposed FamilyBoost childcare tax credit, which is worth up to $150 per fortnight for couples with childcare costs. This will be no doubt welcome, but the trade-off is the loss of the proposed extension of the Early Childhood Education subsidy that Labour included in its May Budget.

All good but how are you paying it?

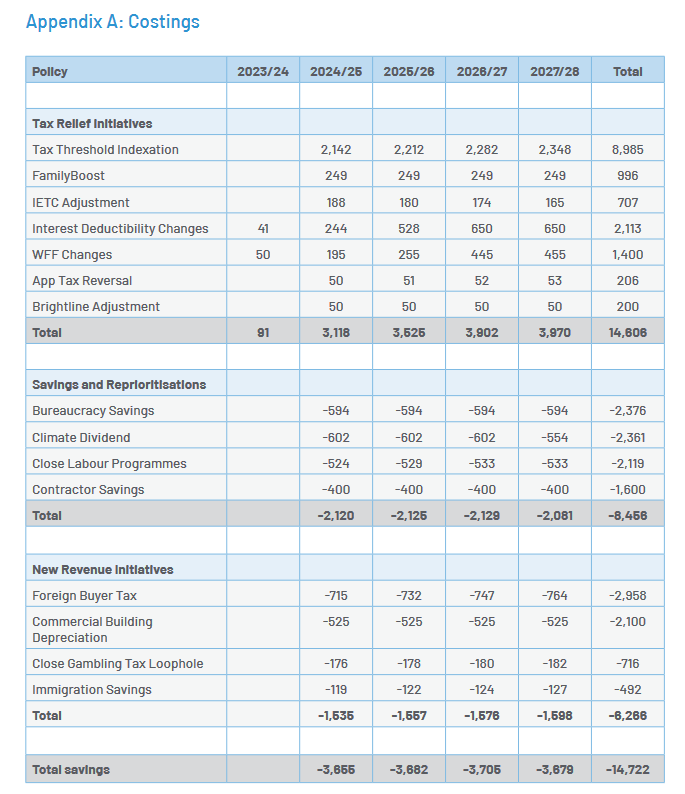

In fact, the controversy around National’s plan has broken out over how it’s going to fund this program and of these proposed tax adjustments. There are several surprises here, the first of which was this proposed foreign buyer tax. Currently no one who does not have permanent residency can buy property. National are proposing to keep that in place for properties worth less than $2 million, but to allow properties worth more than $2 million to be purchased. But that would be subject to a 15% tax, which sounds a bit like a stamp duty. We haven’t had stamp duty, by the way, since 1999.

The controversy is around the numbers involved, which do seem very optimistic. Revenue of $700 million a year would imply sales of at least $6 billion in property. I’ve seen a report in the New Zealand Herald which suggests that actually something like 60 to $65 million is more reasonable. But the proposal also runs up against questions that certain of our double tax treaties and trade agreements have clauses that would not allow such a clause to be a tax to be introduced, notably Singapore and Australia.

But now it’s been pointed out that what we call non-discrimination clauses in double tax agreements may apply to this. In which case these income assumptions of tax revenue would be well short.

There is a proposal to close an online casino gambling tax loophole as its described. This would require offshore operators to pay GST and register and report their earnings for tax purposes. The suggested penalty for non-compliance would be IP geo blocking of services. It subsequently emerged that the Government got $38 million in online GST for the year ended 31st March 2023. This is a result of the so-called “Netflix Tax” which, ironically, was introduced by the National Government in 2016.

National assume the measure will raise $180 million, and I admit I raised my eyebrows when I saw that suggestion. This seemed high to me particularly when I considered that the proposed DST I mentioned earlier is expected to raise about $55 million a year. Online gambling would seem to be a similar type of activity, if not quite identical, so assuming they’re going to raise 2 to 3 times as much as a DST struck me as optimistic.

National Party documents seem to be saying this is essentially a corporate income tax. In which case, it appears this particular tax could also be caught by the anti-discrimination articles in double tax agreements. And that could mean a $140 million shortfall in National’s projections.

Good news for singletons…ironically

On the other hand I do think the proposal to increase the Independent Earner Tax Credit threshold to $70,000 from its current $48,000 is a good initiative. I’ll be honest, I was a bit surprised that Labour didn’t think to do something similar as part of its budget earlier this year. But there is actually a little bit of an irony in that this Independent Earner Tax Credit was actually going to be abolished by National under the last budget it published in May 2017. But that measure never went through because of the change of government later that year.

A counter-productive proposal and more irony

But I think one of the measures that should attract more controversy, is the proposal to remove depreciation for commercial property which includes factories. Now this is something that Labour have also proposed to pay for the proposed removal of GST on fresh and frozen fruit and vegetables.

This is a counterproductive move in my view. The proposal refers to “commercial building” but the depreciation deduction covers all sorts of property such as factories, farming sheds etc. These all depreciate. It was recognised by the last tax working group, that depreciation on commercial and industrial buildings should really be re-introduced, introduced and is actually quite common around the world.

A measure that takes it away seems to be counterproductive particularly if we’re talking about encouraging investment in productive assets. There’s also the added irony that this would be the second time that a National government had removed that depreciation to pay for tax cuts.

Overall there’s an awful lot to pick apart here and the devil is always in the detail. This does seem to point to the revenue forecasts being on the optimistic side, certainly in relation to the foreign buyer online gambling taxes.

Good news for landlords…mostly?

On the other hand, there was also no surprise about the reintroduction of interest deductibility for residential properties. But what is interesting about this move is that’s it’s not simply being fully restored as of a change of government. What’s proposed is for it to be brought back in over a two-year period from 1st April 2024. At present the proportion which would become non-deductible is due to rise to 75%. Instead it will stay at 50% non-deductible and then starting 1 April 2025 the non-deductible proportion will year drop down to 25% before becoming fully deductible with effect from 1st April 2026.

Reducing the bright-line test back down to two years will be welcome for a lot of people. The unintended consequences arising from the extension of the period to first five and then ten years were giving me and plenty of other advisors a lot of work as we try to unpick where the boundary was, and what transactions were caught. So that’s probably quite welcome.

On the other hand, there’s a surprise that nothing has been said about allowing losses from residential property investment (“loss ring-fencing”) to again be offset against other income. This hasn’t been allowed since 2019. It also appears that the proposed increase in the trustee tax rate to 39% will still go ahead. I had heard whispers to that effect, and although there’s been plenty of pushback on the proposed increase it will be interesting to see what eventually emerges.

Now about those Tax Principles…

Having just got a new Tax Principles Reporting Act in place, it is interesting to compare the principles set out in there against these policies. You’d have to say for now, not entirely a big pass. Indexing the thresholds is a reasonable measure, as I said, but that’s a minor point. The tax on foreign homebuyers probably could be said to be questionable in terms of equity. Why should one group of people suddenly get a far higher tax charge than other groups of people in reasonably similar circumstances.

The removal of depreciation for commercial and industrial buildings doesn’t seem to fit with the tax principles. And since we’re talking about things that wouldn’t pass that bill, I’d have to say removing GST on fresh and frozen fruit and vegetables wouldn’t pass muster either.

Sucks to be a student…and an Auckland ratepayer?

But to summarise, tax is politics, so we can expect plenty of politicking. There’s no doubt that the tax relief in terms of the changes in the thresholds will be welcome, but there’s going to be quite a few losers as well. Following the announcement I spoke to a student radio station in Christchurch who were wondering about the impact for students. The answer was not very much and if the proposal to remove the 50% discount on public transport goes ahead, students would be worse off as a consequence.

Auckland ratepayers are also probably worse off with the proposed abolition of the Auckland Regional Fuel tax. Mayor Wayne Brown has already said that could mean a $2 billion funding shortfall. How is that gap going to be funded?

Overall National’s proposals are very much a sort of the Lord giveth and the Lord taketh. And where you sit on that spectrum depends on how well you end up. If you’re a landlord and high-income earner, and you don’t use public transport, you’ll be reasonably okay.

On the other hand, if you’re on lower incomes, perhaps receiving Working for Families income and you do use public transport, you’re going to be worse off. But this is politics, the electorate will decide in six weeks exactly which tax policy is fair.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

My guest this week is Tammy McLeod, Managing Director of North Shore based firm Davenports Law. Tammy is a trust and asset structuring specialist with over 25 years’ legal experience, specialising in the areas of personal asset planning, trust law and Property Relationships Act. Tammy leads the Davenports trust team and has been a principal in the firm since 2006. Kia ora Tammy. Welcome to the podcast. Thank you for joining us.

Tammy McLeod

Thank you so much for having me, Terry. It’s a pleasure.

TB

Not at all. The Trust Act 2019 came into force on 30th January 2021, and it’s caused quite a big upheaval in the trusts ecosystem. What have you seen as the main changes coming out of the implementation of the act?

Tammy McLeod

A couple of things. The first one is that there’s been a major shift towards the rights of beneficiaries and knowledge of beneficiaries regarding trusts. So, I guess if you think about the shift that we’ve seen over the last ten, 15 years from employer to employee, employees have more rights, landlords/tenants. Now there seems to be a shift from trustees to beneficiaries, to the beneficiaries being entitled to ask for more information and holding trustees to account has really shifted the whole landscape. That’s the first thing.

The second thing is I think that a lot of people are actually deciding whether they actually need a trust anymore. So particularly through the 2000s, we used to set trusts up left, right and centre because their accountant might see the need for a trust, or the neighbours had a trust and it just seems to be the thing to do.

And a lot of people are now taking stock and seeing whether they still actually need a trust or whether it’s something that they don’t need any more given the extra compliance costs that have come about, in particular because of new changes to the law, not just the Trust Act, but also changes to the Income Tax Act and the way trusts report to the IRD.

TB

Yes, that’s a good point, that last one. I’ve seen quite a bit of rethinking about what role the trust has in relation to income tax purposes with the increased disclosure requirements Inland Revenue asked for in the March 2022 and March 2023 years. And now we have, as you may be aware, the bill going through Parliament, which proposes increasing the trustee tax rate to 39%.

A lot of interesting commentary is going around. Many trusts, the majority in fact, rarely distribute their income and have minimal income. Once you aggregate that trusts income with those of the principal settlors, they’re well short of the $180,000 threshold where the 39% tax rate kicks in. So, there’s quite a rethinking going on in that. And that’s certainly what I’ve been seeing.

A lot went on in the nineties and early noughties, as you say, in terms of trust setting up. But right now, as that generation of business owners passes through into retirement, they’re thinking about winding up trusts.

And then there’s the other area where I get asked to help quite a bit. And that’s where you’ve got beneficiaries or trustees overseas. People think of trusts and think of tax. That’s not really why we use trusts, is it? What’s the real purpose of trusts?

Tammy McLeod

No, and in fact what I was taught early on was to never mention tax in the first three things that you talked about the benefits of trusts, simply because that shouldn’t be the only reason.

From a lawyer’s perspective, or from a legal perspective, I think asset protection to asset protection, still should be the number one driver. So, if you are in a position of risk, say the director of a company, own your own business and you could be at risk for because of your actions, then very, very simplistically put, because if your assets are in a trust, that could actually help protect in the event that you were sued for whatever reason, or something went wrong with your business.

And it does date back to the days of the Crusades when the knight would ride off to the Crusades and leave his estate in the hands of the neighbours to look after for his wife and family. Because if he didn’t have someone holding that in trust, then it’s likely that it could have been taken for taxes or just taken. So asset protection is still a big driver.

With relationship property, a trust is not the panacea to all ills when it comes to relationship property. But they certainly help with segmenting estates and ring-fencing assets that people might receive by way of inheritance from relationship property pools. And it’s a really good way of protecting those assets.

Another reason is often people may want to treat their children differently. Under a trust, you can’t claim against a trust in the same way that you can make a claim against an estate. So this is a really good way of estate planning, sort of outside the normal rules around will making and estates and how they’re distributed.

And then lastly, people that have assets might just want to keep it in trust for future generations. So think of a family holiday home as an example, or a family business that’s wanting to be kept for future generations. There’s a number of reasons why trusts can be very, very helpful with asset structuring.

TB

Yes, I’ve come across all of those scenarios and in some sad cases you actually have to ringfence the assets because either the beneficiary is incapable or is an addict sometimes.

On trusts and the government’s proposed 39% trustee tax rate rise, one of the points of debate that I saw raised in submissions to Parliament, it’s a question of will trusts. Because they initially were saying, oh well, they will be taxed at 33% for the first 12 months, but that’s way too short a period in my view. What in your view will be more likely period? More realistic?

Tammy McLeod

Well, I think that probably flagging the 12 months because in estate matters, usually everything’s distributed within 12 months on the grounds of probate. But obviously there’s often times where assets are held on trust under an estate for a much longer period of time, you’ve got minor beneficiaries is the usual rule.

But I would say that probably 85 to 90% of estates are distributed within the first 12 months. So, I think that’s where they’ve got it from.

And another one of those perhaps tax rules where you wind up paying your advisors a whole lot more to sort out what should be something that is quite simple and quite straightforward. But it doesn’t seem fair if you like, for assets or money that’s being held on trust for a minor beneficiary to be taxed at 39 cents, it’s highly unlikely a minor beneficiary would be paying 39 cents on the dollar.

TB

And then as I’ve occasionally come across, there’s disputes over who’s to get what which will delay winding up. Whenever these erupt the only people, in my view, who ever win are the lawyers and accountants.

Tammy McLeod

Without a doubt. Lawyers in particular.

TB

As I said, one of the things I see quite a bit of is – we’ve got a very mobile population – people, beneficiaries, trustees, moving settlors, all moving around the place. What’s your experience with this? How often do you encounter those scenarios?

Tammy McLeod

At the moment, all the time, as you say, particularly after we’ve been shut down in the country, I guess for two years plus, people are just moving all over the place. A lot of people are moving to live in Australia in particular and it’s a real moving feast. There seems to be a lot of the next generation moving to Australia and other places.

And so that’s something that trustees have to be hugely aware of and I think there’s a real onus on trustees to ensure that they are aware of the movement of beneficiaries because it might have an impact on how they’re taxed in relation to the country that they’re in. So for an example, an Australian tax resident beneficiary will be taxed on a distribution from a New Zealand trust, and so proper advice needs to be taken upfront.

And I think that’s one benefit to having an independent professional trustee, is that they should be keeping on top of these issues and flagging these issues. And every time a distribution is made from a trust to a beneficiary, where that beneficiary is situated, should be considered.

Therefore, any trust that we are a trustee of, we ensure that we have regular meetings and it’s one of our agenda items, the location of some of the beneficiaries and making sure that you’re on top of that and then planning for that. Because it’s not even a distribution being made during the lifetime of the parents if they’re settlors and trustees of the trust. It’s what happens if the children are to receive as beneficiaries of the trust assets upon both parents death So it might not be in the immediate picture, but it could be something in the future, it should be planned for.

TB

That’s quite an issue. Particularly in Australia, there are two things. There are the beneficiaries who should qualify for the temporary residence exemption in some cases. That applies to exempt non-Australian sourced income so long as the beneficiary is not a citizen.

And that’s something I think trustees now need to be aware of as people become Australian citizens, then those rules where previously a distribution from New Zealand trust or New Zealand income would not be taxable in Australia. The easier ability to become an Australian citizen changes everything.

And then of course the other one, and I’m sure you’ve seen this, is when a trustee wanders across to Australia and they don’t tell you. I’m sure you’ve encountered that quite a few times.

Tammy McLeod

Many times. And I think it’s one that we’ve been more aware of and there’s been a lot more talk of. But I think the beneficiary one is really becoming an issue because as you say, the population is so mobile and one year you could be in Australia the next year, that could be in the UK, in Singapore, it’s just people are moving around. All over the show.

TB

Distributions to persons in Australia who are not Australian citizens, are manageable. But the real headaches I keep encountering are distributions to people in say Britain, particularly Britain, or America, where the rules can be quite brutal. You can be looking at a 45% tax rate because we use discretionary trusts so much, that can be really quite disadvantageous.

One of those things I see crop up, is that there is a certain proprietorial interest, “this is my trust”. Say the family set it up and were told you can self-manage this and then were sent away. A lot of those got set up during the 1990s..

How do you manage that? You come in, you find someone wants to do something, and then you find out that they’ve done a lot of things they shouldn’t have done in trust law. But what’s the process there?

Tammy McLeod

My pet peeve is how you can manage your own trust. And one thing that really frustrates me is where a lot of professionals are now saying they don’t want to be trustees, and so they’re setting up trustee companies that only mom and dad are the only directors and shareholders, often saying that’s a different entity for Mum and Dad. And I just think that’s wrong.

To me, having an independent trustee is what really makes your trust robust. And so that’s where you can put your hand on the heart and say, I can’t sell this, a trustee has to think “I can’t mortgage this property, I can’t borrow this money or buy this business without my independent trustee knowing. It’s not my decision anymore”.

And to me, that’s the first line of defence of what actually is a trust. Funnily enough, it’s not a legal requirement or one of the certainties of trusts. But from a robustness perspective, definitely having an independent trustee is important. And what has also happened over the last five years in particular, but maybe 5 to 10 years, is that the independent trustees are tending to become professional trustees.

So previously people would often use a family member, or a family friend. And I think the landscape has changed. Not only because of the risk to trustees, and so professional trustees understand the risk, know the risk and can insure against the risk.

I always say professional trustees care, but they don’t care. The numbers on the page are just numbers to us. Whereas for a friend or family member to know how much money the trust is losing, how quickly it’s paying down the debt, that can be too, too much.

So, my view is always have independent trustee, and ideally a professional independent trustee. And it also helps with the management as well. The things that we’ve just been talking about with Australian beneficiaries, if you’ve just got Ma and Pa as the only trustees, how can they keep on top of these issues without the input of a third independent person? So I’m hot on having a professional trustee.

TB

I mean, are you seeing as a result of two things – suppose that the greater rights for beneficiaries, as you mentioned in the start, but are you seeing more issues emerge from those Ma and Pa trusts set up 20, 30 years ago. Are they starting to boil over in difficult ways? What issues are those leading to?

Tammy McLeod

The major difficulty with those ones at the moment, and I’m sure there’ll be more issues that come out over time, but the big thing at the moment is if Ma or Pa dies, or in particular loses capacity, or one’s died and the others lost capacity, who are the trustees now and how are they appointed? Who are they going to be? Often children fighting between themselves. So that can be an issue. And children trying to influence aging, elderly parents. Whereas if you do have the professional in there, A you’ve got a referee, and B you’ve got a platform for how these types of issues are to be managed.

TB

That last point you made about losing capacity is one that makes me very nervous. I talk with clients on this because I’m just encountering it in tragic circumstances. If a trustee loses capacity, am I right in thinking that that means that you probably have to go to court to get things done?

Tammy McLeod

No, not anymore. So under the new Trusts Act, that’s another one of the changes, if a trustee loses capacity, then he or she is then deemed to be incapable of being a trustee going forwards and are immediately removed by virtue of the statute.

So that’s new. Previously there were no rules around who could be a trustee. The other thing the new act has also done is put in place vesting rules. Previously you had to go to court, unless the trustee had said otherwise, to enable a new trustee to be registered on titles to properties and companies, shareholding registrars and so forth.

Whereas now under the new act is an automatic deeming or vesting of the trust assets on the capable trustees. The difficulty can be assessing what capable means.

And just to give an example, I talked to a client last week and one of the settlors is verging on the early stages of dementia and he’s heavily involved in the family businesses. And the question was asked, at what point do we say that he’s not capable?

There’s this balance – is he’s capable of being a trustee? At the moment he understands what he’s doing. Can he make good decisions for the trustees going forward? How do we deem him to be incapacitated? And it might be different for him than it might be for someone else in a similar set of circumstances.

So, if you had an incapacitated, or bordering on incapacitated settlor, who doesn’t have the sophistication of understanding business, etc., that might be a different level of capacity to be a trustee.

So this is a whole minefield. And lawyers have to ask some pretty hard questions and also talk quite robustly with family, doctors, geriatricians and the like particularly with an ageing population.

If you think back about the comments that we’ve made around the lots of trusts being set up in the 1990s and early 2000s, some 20 years on we’ve got a whole raft of settlors and trustees heading towards their mid to late eighties and nineties. It’s a bubble that’s moving through which is going to create lots of issues because the other thing to remember is that enduring powers of attorney don’t fit with trusts.

TB

I was just about to ask you about that one.

Tammy McLeod

So your enduring power of attorney relates to your personal property, it doesn’t relate to your powers as a trustee. There can be mechanisms within trust deeds which help with who has the power to appoint or remove trustees or a settlor who loses capacity. But it’s not a given that the powers of attorney and the trustees have any connection at all, you need to go back to the source documents and see what’s there.

TB

What do you see going forward with trusts? Do you see much change in this area?

Tammy McLeod

I see massive change and I’m seeing it already, probably in the last three or four years, rather. We’re still setting up a lot of trusts. But we’re winding up as many, if not more probably, than what we’ve been setting up. There are still great reasons, as we talked about earlier, for people to have trusts and most people are still putting in place asset structuring.

But I see there’s a lot more dispute. A lot of the work that I’m now doing – I used to say that my legal practice is all about the good, positive things of setting up, good positive structures for people, for the future. And now a lot of it is actually how do we unwind the structure of these trustees not doing what I want them to do?

How do I make this beneficiary behave? There are disputes after Mum and Dad have died between beneficiaries as to what’s to happen with the trust assets. It’s disputes between trustees, disputes between beneficiaries.

So it’s become a lot more fraught, bordering on litigation type issues. A lot more people separating, the impact on relationship property. That’s how I sort of got more into that area was people separating, myriads of trusts which had to be unwound which were complicating factors.

What I do nowadays is more quasi litigation rather than setting up structures. And I guess that’s interesting from a purely legal perspective as well as my practice matures. So that’s interesting as well, but definitely very, very different to what it was five, ten years ago.

TB

As I said, the explosion of trusts, and we don’t actually know how many trusts we have in the country, and it’s one of those per capita starts we probably shouldn’t be too proud of.

With the administration of trusts you’ve mentioned trustees’ meetings. How critical are they in this process, particularly what you just talked about with the potential incapacity, etc., and the professional trustee?

Tammy McLeod

I think that companies, to give as an example, as opposed to trusts, are quite easy to manage in a way because the Companies Act 1993 is quite prescriptive about what you need to do to make sure that your company carries on as a company with the Annual Return and so forth.

Trusts aren’t like that. So even under the new act, there’s no real prescription there. But that’s your only evidence really, of having a trust, because trusts are this kind of ethereal being, I can’t give you something and say, here, this is a trust for your record keeping.

So having those trustee meetings are imperative to go over the kinds of things that we’ve been talking about today. Where are the beneficiaries? What’s the capacity of the trustees? Tax issues, etc.

And in fact, I’m presenting a seminar next week at the North Harbour stadium which got around 600 people registered for. And we’re going to be covering things like this. So why do you need a trust is often the first question I get asked about in trustee meetings “Remind me again why I need this trust.”

I’ll be talking about things like capacity, powers of attorney, the changes to the act, disclosure of information to beneficiaries. So, I’ll be covering all that at the seminar next week. Those are the sorts of things that we talk about at the annual trustee meetings.

TB

I’d agree trusts are quite ethereal. Sometimes you see on companies’ office documents that the ABC trust holds the shares in this. Which is not correct at all. It’s the trustees that should be named as shareholders.

So, there’s a lot of sloppy or untidy administration out there and it can lead to quite a number of issues. We’ve mentioned beneficiaries overseas. What I get very concerned about in tax is when settlors or trustees move overseas, particularly in the case of Australia if a trustee goes over there, the New Zealand property could become taxable subject to Australian capital gains tax, even if the gain is distributed to a New Zealand resident. So heaps of things going on.

I think that might be a good place to leave it there. If you’ve got this seminar coming up, I know I’ve seen you present, that will be well worth attending with 600 attendees. I’m sure you can squeeze a few more in.

My thanks very much to you, Tammy, for coming along and talking to us on this podcast. Good luck with the seminar next week.

Tammy McLeod

Fantastic. Thank you so much, Terry. I really appreciate it. We’ve been friends for a very long time, so it’s nice to get a spot on the podcast.

TB

I can very highly recommend Tammy, she’s a highly experienced veteran of the trust field. You’ll be in very good hands and the seminar will be well worth attending.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

At last week’s International Fiscal Association’s Trans-Tasman conference, a lot of the discussion among New Zealand advisors outside of the seminar rooms was around the state of tax policy. There is a growing concern that a more active government with interventions and proposals such as the proposed zero rating of GST on fruit and frozen and fresh fruit and vegetables is undermining the Generic Tax Policy Process which has been in place for nearly 30 years.

Like many practitioners, I’ve been involved with the GTPP at various stages. It is well-regarded internationally and has operated since 1994. It is intended to ensure

“better, more effective tax policy development through early consideration of key policy elements and trade-offs of proposals, such as their revenue impact, compliance and administrative costs, and economic and social objectives. Another feature of the process is that it builds external consultation and feedback into the policy development process, providing opportunities for public comment at several stages.”

However, the concern is emerging that against this well-established background more recent measures such as the Tax Principles Bill, or the legislation that enabled Inland Revenue to carry out its high wealth individual research project, have happened outside the GTPP framework. The proposed GST zero rating of fresh and frozen fruit and vegetables could be another example. These developments are unsettling the previously predictable process for working through and discussing tax proposals.

I’m of the view that tax is fundamentally about politics and politicians will always make political calls. The GTPP is intended to minimise the effect of that and give more predictable tax policy outcomes. But you can’t eliminate it entirely and this dichotomy between efficient tax policy process and politics will always be there.

There is also the question raised in an interesting story this week by BusinessDesk (paywalled) in reference to the work of the Corporate Taxpayers Group (CTG) about when consultation ends and lobbying begins. The CTG includes the main corporate taxpayers such as Fonterra and the four big banks. The New Zealand Superannuation Fund, the largest single taxpayer in the country, is also a member.

The CTG meets regularly at the offices of Deloitte (more frequently than I had imagined) as the story outlines, and there is an annual membership fee which is to pay for the secretariat, which will make submissions to Parliament and to Inland Revenue.

But when does this move from consultation to lobbying. Very difficult to say. I don’t see it as lobbying although I do appreciate the risks that might be involved in that. But having been involved in the process and been in meetings with CTG representatives, Inland Revenue officials, I don’t believe that’s the case.

But as I said, I can understand why some might be concerned by this. It comes back to a key part of any democracy, and that’s transparency. But on the whole, as I said, I think New Zealand’s been very well-served by the GTPP. And I know that internationally it’s very well regarded because it has got a stability of process to it.

I think one of the issues that’s causing raising concern is because left wing governments are likely to more interventionist. But I do think this situation is exacerbated at the moment because the strain of the boundary between capital and revenue, and our general under taxation of capital, the lack of a capital gains tax, wealth, tax, death duties, are putting strains on the system. And so, politicians are trying to find shortcuts to try and deal with this issue and the need for more revenue. You can dispute how much is needed. But when I look at the state of roads and hospitals and you see the growing bill for climate change, my view is and it’s also the view of Treasury, as I pointed out a number of times, and its Long Term Insights Briefing He Tirohanga Mokopuna we need more revenue.

A whole lot of hissing

So, there are strains emerging and it’s impacting the GTPP, which makes tax advisers understandably a little unsettled about how well that process will continue. As Louis XIV’s finance minister Jean-Baptiste Colbert said in probably one of the most famous maxims about taxation: “The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing.” That was true in the 17th Century and remains true today. And there is quite a lot of hissing going on at the moment.

The GTPP in operation – consulting on trading stock

Moving on and still on to the topic of consultation and an example of the GDP in operation. Inland Revenue has released a paper for consultation on the treatment of trading stock disposed of below market value.

At present, whenever trading stock is given away, or disposed of for below market value it’s deemed to have been disposed of at market value. The reason for that rule is reasonably solid. It’s to counter potential tax avoidance where the stock is given away or may be used for private consumption by a business owner or sold at a deep discount to associated persons. In some cases, it could apply for a particular industry, exchanges of stock could take place at cost or less. All of those generate benefits in terms of the under taxation of revenue. So that’s why that rule exists.

But there have been instances where businesses have wanted to give away stock and make donations for charitable purposes, and that’s when this rule becomes problematic because they can’t effectively do so. Over time the practice has developed for granting temporary emergency relief in some situations as a work-around.

In 2004 a permanent override was put in place with donations to farming, agricultural and fishing businesses during what is termed an adverse event. And there have been a large number of those weather-related adverse events either for drought or like we’ve experienced this year, flooding.

Between 2010 and 2012, there was a temporary override for 18 months in response to the Canterbury earthquakes. And then again, starting in March 2020, a temporary override was put in place for four years in response to COVID 19.

That override will end on 31st March next year, and the object of this consultation paper, is to propose a more permanent solution rather than using ad hoc solutions whenever we encounter a particular scenario such as COVID or earthquakes.

The consultation paper runs to 29 pages and includes a useful appendix which summarises all the potential summary policy options and how they may play out. Overall, this is a good example of the Generic Tax Policy Process in operation. Consultation on the paper is now open and closes on 6th September.

Managing retreat & how to pay for it.

As just mentioned, temporary emergency relief from the usual stock donation rules has been granted for a number of reasons, including this year, the flooding in January and February and the impact of Cyclone Gabrielle. A constant theme of this podcast is the question of environmental taxation and the need to address the longer-term question of how we going to pay for these climate related events.

Earlier this week a Government expert working group released its report on the question of what’s termed managed retreat.

The report, which clocks in at 284 pages, is very comprehensive and raises a number of potential scenarios and alternative measures that could be needed. One of which, as the excellent Newsroom story covering the report notes, is conditional powers to basically force people to leave particular areas that are under threat.

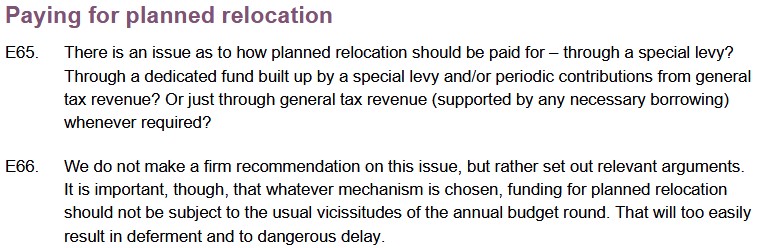

Being a tax podcast the question we are most concerned about with environmental and climate change impacts is how we are going to pay for it. The report has two key proposals E65 and E66.

But consider this, we have currently 700 homes which have been rendered uninhabitable following the flooding in January and February. And there’s another 10,000 homes that require flood protection. The Government has said it will split the costs over the uninhabitable homes with local councils affected. But, as far as I can tell, neither the councils nor the Government have really fully funded for these costs of maybe a cool billion or so this year and maybe every year and rising. So, it is an issue that needs to be addressed.

The report has some interesting discussion around what happened in Canterbury in relation to the earthquakes and then the first and I emphasise, first, example of managed retreat, from the Bay of Plenty settlement of Matatā

The report says, however we decide to fund this, the funding should not be subject to the usual vicissitudes of the annual budget round because that would mean it would lead deferment and dangerous delay. When it comes to kicking a football down the road, the politicians, as we know, are better than the Football Ferns at kicking it a long way out of trouble. Or so they think, but the issue still remains. I totally agree, therefore, with the report’s recommendation that there has to be a permanent funding solution.

I maintain that if we are going to do something around the lines of environmental taxation, the funds that are allocated to it should be hypothecated, and certainly not form part of the consolidated fund because we’ll then have politicians tempted to raid those funds. We’ve seen this in the recent Auckland Budget Council, by the way, where reserves built up for environmental purposes were used for other purposes.

In terms of holding politicians to account, I think we need to be asking a lot more questions about them on this matter because this is going to affect us all. We’ve had a miserable winter with extensive flooding and the ground is sodden. What happens when the next big floods come along, who pays for the clean-up?

No longer friends with Russia…

At the International Fiscal Association Trans-Tasman conference last week, we spent a lot of time discussing double tax agreements. It so happens, Russia has decided to suspend its double tax agreements with 38 countries, which it considers are now ‘unfriendly’ in the wake of the invasion of Ukraine. New Zealand is on that list. So that probably means that for someone in Russia trying to claim tax relief from under the double taxation between New Zealand and Russia, they’re out of luck and they’re probably going to be facing higher tax bills as a consequence.

TikTok and GST fraud

And finally, just on the topic du jour this week of GST, there’s an absolutely extraordinary story coming out of Australia about how social media influencers on TikTok encouraged at least 56,000 people to take part in a A$1.6 billion tax fraud scheme. Apparently these TikTok influencers explained how to get fraudulent GST refunds. The scam involved obtaining an Australian Business Number, then filing Business Activity Statements (the equivalent of GST returns) and claiming false GST refunds. In some cases, there were attempts to claim refunds of up to A$100,000.

The Australian Tax Office apparently is still grappling with the sheer size of the scandal. There’s a story in the Australian Financial Review about a Victorian woman who managed to stay out of jail, after repeated attempts to try and get A$115,000 fake GST refunds for a dog grooming business that had been set up more than a decade ago but had been largely dormant until 2020 before she attempted to pull this scam.

Fascinating story which will be interesting to see how it plays out. To me it lends support to the suggestion that we should look seriously at zero rating transactions between GST registered businesses. It should be a means of stopping such attempted frauds. Obviously, if that proposal is taken forward, it should go through the proper Generic Tax Policy Process consultation.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

As previously leaked, on Sunday Labour announced that if re-elected, it would introduce legislation to zero rate GST on fresh and frozen fruit and vegetables, with effect from 1st April next year. This is a key plank of what it’s calling its ten-point plan to address the cost of living.

According to the fact sheet supplied at the time of the launch, based on the latest statistics from the New Zealand Household Economic Survey in 2019, the policy is estimated conservatively to save households about $18 to $20 per month. Now, one of the key criticisms of this policy is of course its complexity. But Labour is confident that in defining where the boundary will lie, it will be able to draw down on overseas experience in this area. “There are boundaries everywhere in the tax system and we are confident tax officials can make it work”.

The framework around the policy is whether the fruit or vegetable has been processed or not. And processed in this context means cooked or combined with other ingredients. This therefore rules out anything canned because of the heating process that is involved. Processed does not include being cut up and wrapped without additives, so that prepared vegetables such as fresh spinach in a bag, presumably salads, would be zero rated. Similarly, mixed vegetables frozen together would be zero rated for GST. But on the other hand, the release gives an example of potatoes mashed into chips, coated in canola oil and then frozen, would be excluded and therefore still attract GST.

There is a proposal to establish a consultative expert group immediately after the election to work through the final details of the policy. One of the criticisms of the policy is, and I’ve said so previously, whether the benefit of the GST reduction would be passed through to consumers. This is to be addressed by tasking the newly established Grocery Commissioner with ensuring that supermarkets and other grocery outlets are not profiting from this change. The Grocery Commissioner has powers under the new Grocery Industry Competition Act 2023 to require it to request information and reports from supermarkets on matters such as their prices and margins.

Depreciation on commercial property to be removed, again

Labour estimates the cost of this policy to be about $2 billion over a four-year forecast period to 30th June 2028. And the sting in the tail is that this is going to be paid for by commercial property landlords. Because Labour is proposing to remove what it has called in the fact sheets, “the last remaining large COVID 19 economic stimulus measure”, which was the introduction of depreciation for non-residential buildings.

According to Treasury’s costing of the COVID 19 Response and Recovery funding decisions, that particular decision back in March 2020 costs an estimated $545 million annually. it should be said that back in 2020 when depreciation was reintroduced, there was no indication that this was going to be a temporary measure. In fact, the accompanying commentary noted:

“New Zealand’s position of a zero-depreciation rate for almost all buildings is unusual internationally. International studies have generally found buildings do depreciate. The Tax Working Group reviewed and recommended changes to these tax settings. The Government has accepted the group’s recommendation to reinstate depreciation for industrial and commercial buildings.”

So the news that barely three years after it was brought back in, it’s to be removed again will be a big surprise for the commercial property sector. And you can expect very strong representations about that. Certainly, some projects in the pipeline may be delayed as companies and investors work out the impact of the withdrawal of depreciation.

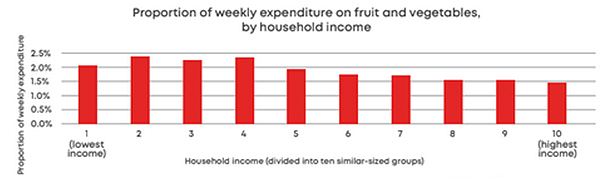

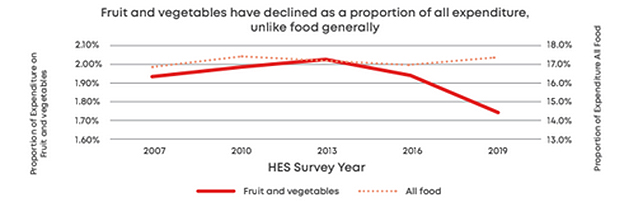

There was some interesting stuff in the accompanying fact sheet about the proportion of weekly expenditure on fruit and vegetables by household income. And what might surprise people is that it’s the lower deciles, deciles one to four, who actually spend the greatest proportion of their budget on fresh fruit and vegetables. It works out nearly 2.5% for some of the deciles. So that’s greater in relative terms than what happens for decile ten households.

But what’s also notable here is that this survey apparently shows that the amount of fruit and vegetables being purchased as a proportion of all expenditure has been declining for some time, and it declined from just under 2% in 2013 to just over 1.7% in 2019.

What’s happening there would be interesting to know, but it could be that the cost pressures on fresh fruit and vegetables are actually more longstanding than just the post COVID 19/climate related events burst we are experiencing at the moment. The Grocery Commissioner will obviously be paying particular attention to that on a longer term.

Increasing Working for Families support

The announcement, or the focus on the GST policy, overshadowed the other big announcement made, which was a proposal to increase the Working for Families in-work tax credit by $25 a week from 1st of April next year. This is going to provide additional support to around 175,000 low- and middle-income working families. It’s the sort of measure which is supported by many, and I would be in that group, because it’s targeted and it gives to those most in need. Although I do note that Child Poverty Action Group are still disappointed that the criteria for this is still about being in work. Their long-standing position is that the in-work criteria should be removed because that would benefit all families and particularly children of those on the lowest incomes.

The other thing that Labour’s also planning to do is to lift the Working for Families abatement threshold from its current level of $42,700 to $50,000. But that’s not going to happen until 1st April 2026. That would be worth another $13 a week to eligible families.

I’ve spoken before about what goes on with the abatement levels, and it’s worth pointing out again that when Working for Families was first introduced in 2006, the abatement thresholds were adjusted annually. That was stopped by Bill English in the 2009 Budget, with the effect that if the then threshold of $36,827 had continued to be indexed to CPI, it would now be $51,702. In that context, Labour’s promise to raise to $50,000 in three years seems a little ungenerous.

Whether yesterday’s announcements are the sum of Labour’s tax policy for the election is not yet clear. Apparently, they are. But I note that they are still promising three more cost of living policy announcements to be made during the election. So, we’ll have to wait and see.

More GST – the importance of GST groups

Moving on, Inland Revenue is presently engaged in updating its various Interpretation Statements and other guidance, such as Questions We’ve Been Asked and in various statements of practice, to update various legislative updates that have happened over time. Some of this advice refers to the Income Tax Act 1994, whereas now we’re on the Income Tax Act 2007. So, Inland Revenue has been releasing a steady stream of updated guidance for consultation, and most of these updates confirm the existing position.

The latest released last week and also continuing this week’s GST theme, are two draft interpretation statements for consultation on the treatment of GST groups. One looks at when GST groups may be formed in general, and the second looks specifically at the rules around GST groups for companies

There has been a little bit of uncertainty around how the GST group rules interacted with other parts of the GST Act, and that was taken care of by an amendment included in the Taxation (Annual Rates for 2021-22, GST and other Remedial Matters) Act in 2022, which clarified the interaction of the GST group rules with the Income Tax Act. The position now is that the GST grouping rules are applied before the other provisions in the GST Act.

The idea behind the GST grouping rules is to eliminate the need to be charging and recovering GST on intra group sales. Think of a large group that’s supplying goods and services to another group member. If they are not within the same GST group, one party would charge GST and the other party would have to recover the GST. So, the idea of the grouping rules is to simplify administration.

How it’s done is that there is a representative group member chosen that carries on all the group members activities and that entity, whoever it is, is responsible for all the administration of GST. If a sale is made by someone outside the GST group, to a member of the group, it’s deemed to be made to the representative member as the registered person. Similarly, the various sales that might be made by group members to outside the GST group, are all treated as taxable supplies made by the representative member.

However, taxable supplies between group members are mainly disregarded with the idea of simplifying administration. One paper considers what happens with GST groups of companies. These can be formed where there is 66% commonality of shareholders, similar to the income tax rules for loss-offsets between group companies. In some cases, you can have non-registered entities as part of the GST group. The other paper covers the rules in general and where you can have groups of other entities such as trusts, for example, or maybe limited partnerships.

So, the two papers explore that and explain the background behind how the GST group rules operate. And as I say, these are part of a wider Inland Revenue project to update its material. These are very useful Interpretation Statements and consultation on these is open until 14th of September.

At the same time, I can’t help but think that Inland Revenue should be exploring the idea of introducing compulsory zero rating of GST between all GST registered entities. This would largely eliminate the need for rules around GST grouping. I think what it would also do is tackle an area of GST fraud which incurs relatively frequently where a fraudster might register for GST and then files a number of false GST returns, claiming input tax based on made up invoices.

Although Inland Revenue tracks down and catches these people, there is a time lag while the fraud is going on. I’m beginning to think if you want to try and tackle that, compulsory zero rating between GST registered businesses is perhaps a place to start. Giving Inland Revenue more resources to look into it, is another interim measure that could be done.

Trans-Tasman Tax issues

And finally on the Thursday and Friday just gone I was at the International Fiscal Association Australia-New Zealand Joint Conference in Queenstown. This is the first time in over 30 years the Australian and New Zealand branches have held a joint conference. It was highly successful. One reason IFA conferences are so attractive is because very senior Inland Revenue, and Treasury officials, and for this conference, Australian Tax Office and Australian Treasury officials, attend and share their views on insights on current tax topics. (Consequently, the conferences are held under Chatham House rules to enable officials to speak freely).

It’s always interesting to swap notes with other attendees and this conference was no exception, but it was particularly interesting because of the focus on Australasian issues. Both sides got to see differing perspectives on common topics, which included the question of tax treaty policy and updates from very senior people from both Australia and New Zealand on the OECD Pillar One and Pillar Two proposals. Australia and New Zealand are very well represented on the key working groups on this, we’ve got very good knowledge of how things are progressing. We also got a view on the latest environmental and tax developments, including a view from the IMF’s principal environmental fiscal policy expert.

“A hot steaming mess” – the perils of Australian taxation

A particularly interesting session was on the taxation of trusts in the trans-Tasman context. the current state of Australia’s trust tax law was described as a “steaming hot mess”. I regularly encounter scenarios where trustees have migrated to Australia without considering the tax ramifications, and a steaming hot mess is perhaps an understatement of the consequences. Overall a very useful session.

Incidentally, Australia and New Zealand are currently renegotiating the double tax agreement between the two countries. And the point was made that although as tax professionals we tend to look at tax treaties solely tax related, one panelist reminded everyone that they’re actually often part of bigger trade negotiations.

For example, as part of its efforts to obtain a free trade agreement with the EU, Australia has opened negotiations with double tax agreements with several EU countries. Apparently one reason a UK a double tax agreement between the United States and the United Kingdom in the mid-1970s was so advantageous for the Americans was because at that time the UK was negotiating the purchase of upgraded missiles for its submarine fleet.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

New Zealand has undoubtedly entered a slowdown economically and that’s flowing through to lower tax receipts leading to claims this week of the Governments being in a big fiscal hole. According to the Companies Office’s latest statistics for the quarter ended 30th June 2023, there were 461 liquidator appointments in the quarter.

That’s 47.8% up on the 312 for the same quarter last year.

As Professor Lisa Marriott noted in an article late last week, the ripple effect of companies going into liquidation is considerable, particularly for unpaid suppliers and employees. Her research suggests that Inland Revenue could be doing a lot more to share information about businesses that are failing. According to Professor Marriott Inland Revenue is actually less proactive than some comparable overseas government agencies such as the Australian Tax Office.

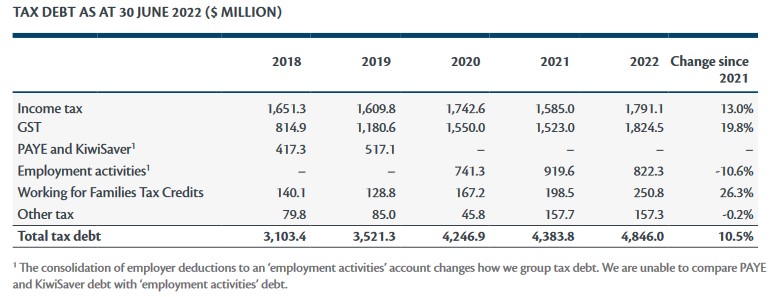

Inland Revenue initiates more than 60% of liquidations in the average year, and that sometimes happens after quite a considerable period of non-payment of key taxes such as GST and PAYE. For example, $2.6 billion or over 54% of the $4.8 billion owed to Inland Revenue as of 30th June 2022 represented GST and what it terms “employment activities” (i.e. PAYE and KiwiSaver contributions).

(Inland Revenue June 2022 Annual Report)

Professor Marriott’s research points to non-payment of these particular taxes as being a very early warning sign of businesses running into trouble. Picking up overseas initiatives she suggests three particular responses could be adopted here to help businesses be aware that a particular business they may be dealing with may represent a credit risk.

For example, in Ireland, Revenue Ireland produces a quarterly list of tax defaulters which identifies the name, address, occupation and the amount of tax owed. This is triggered when the debts exceed €50,000 or approximately $90,000.

Another option would be as the Australian Tax Office does, to advise credit rating agencies that a business has tax debts. This happens if the amount owed exceeds A$100,000 and is more than 90 days overdue.

A third option and one the Tax Working Group looked at, is following another Australian initiative and making business directors personally accountable for unpaid tax through Director Penalty Notices. These are issued in relation to the Australian equivalent of PAYE, GST and KiwiSaver. Once a Director Penalty Notice has been issued, it can only be cancelled by full payment of the tax debt within 21 days or some other action such as commencing winding up proceedings. If no action is taken, then the director becomes personally liable, effectively sidestepping creditor protection and limited liability issues.

These are sensible suggestions, but in my view perhaps another thing Inland Revenue could do would be to be much more proactive in managing debt, particularly in relation to GST and PAYE. I occasionally get involved with helping taxpayers who have fallen behind with their tax payments. And there’s invariably a couple of common points in every case.

Common problems with tax debt

Firstly, Inland Revenue’s present policy of charging interest and late payment penalties doesn’t seem particularly effective to me. In fact, arguably, I’d say it counterproductive.

Debt builds up very quickly and consequently, at a remarkably low level somewhere between $10 and $20,000, the taxpayers often just feel defeated and basically give up. At this point they haven’t engaged with Inland Revenue and all they see is just the amount owed going up and up and up resulting in a sort of death spiral procrastination spiral.

The second common factor in dealing with clients in this scenario is that the situation has been allowed to carry on and develop over a long period of time. These businesses have been going through a slow decline before Inland Revenue finally steps in and decides either to liquidate it or impose some other form of action to recover the outstanding amounts.

One of those actions is the use of “Deduction Notices”. These enable Inland Revenue to go to a customer of a defaulting taxpayer and require them to withhold a certain percentage of any payment they may make to the defaulting taxpayer, and instead pay it over to Inland Revenue. Most often Deduction Notices are issued to employees and often in relation to unpaid child support. But they can be used in other circumstances. In one case I saw a Deduction Notice applied was 100%, although I’m not entirely certain what was meant to be achieved by issuing such a notice.

Adopting the measures suggested by Professor Marriott would take some time to go through the full consultation and legislative process. Although these are tools Inland Revenue perhaps could consider adopting, given the current rise in liquidations, I consider it needs to be taking action sooner rather than wait for these additional options.

Harden up Inland Revenue?

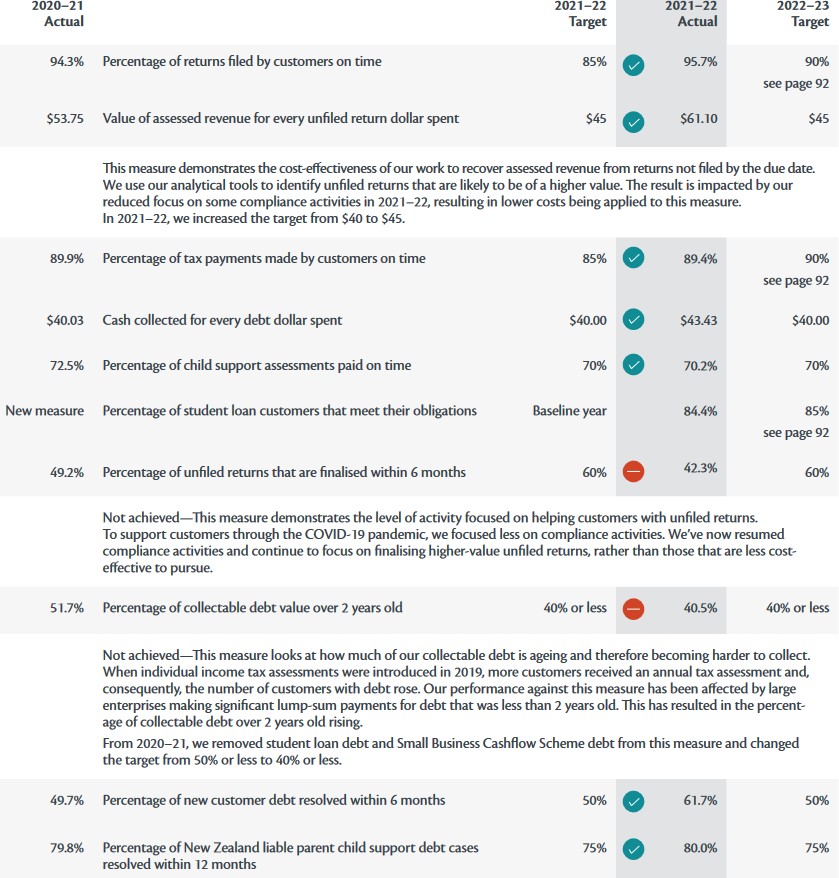

One of the things it ought to do is toughen up its own performance measures in relation to the management of debt. Each year in its annual report Inland Revenue will publish its performance measure results broken down by various sectors. For the year ended 30th June 2022, it achieved seven out of nine measures that it set in relation to the management of debt and on file returns.

But critically, one of the measures where it fell down was the percentage of collectable debt over two years old. The target for the year was 40% or less and in fact it achieved 40.5%, just above its target. That, by the way, was a considerable improvement on the 51.7% achieved for the year to June 2021.

But I would suggest that the 40% target is actually too generous. Inland Revenue really should be looking to drive that down to 20% or less. In fact, looking at this measure, it used to include student loan debt and Small Business Cashflow Scheme debt, but they were taken out and the debt target was then reduced from 50% to 40%.

(As an aside, student loan debt is a particular problem where I think Inland Revenue inaction has allowed very large sums of debt built up with people going overseas as the main issue here. But Inland Revenue, to my mind, has not been quick enough to develop the tools it needs to keep on top of that particular issue, which means often applying to overseas tax agencies for details of defaulting taxpayers.

I think it’s picking up its efforts in this space, but the scenario perhaps shouldn’t be allowed to develop to the extent it did. I’ve recently come across a case where the taxpayer left over 20 years ago but basically Inland Revenue has only now really started to take action to collect the outstanding debt.)

The other thing that’s also noticeable from Inland Revenue’s June 2022 annual report is that it did not actually spend the full amount allocated to it from the relevant budget appropriations.

Some questions for Inland Revenue

The amount allocated was just over $92 million, but in fact Inland Revenue underspent by $2.5 million for the year. A couple of questions I have about this are how did that happen and what’s being done to improve the performance and make sure that the funds allocated are effectively used? (I note that for the year to June 2023, there was an increase in the appropriations.)

It will be interesting to see how that’s played out when we see the annual report later this year. This debt management issue, by the way, points to something I’ve mentioned in previous podcasts – has Inland Revenue’s Business Transformation program deprived it of some capacity in key areas? Inland Revenue has reduced its staffing by more than 25% of your staff and not all of that might be dead wood no longer needed because of the upgrade. I think vitally important staff have gone from key areas such as investigations. And it may be that debt management is another area where key personnel have been allowed to go and the gap has been allowed to develop as a consequence.

As I said, it will be interesting to see the annual report later this year. But in summary, I’d have to agree with Professor Marriott, there’s plenty of room for improvement.

More interest rate rises…

Moving on, a key weapon for Inland Revenue in ensuring payment of tax debts is the ability to charge use of money interest on unpaid tax debt. The current rate is a fairly chunky 10.39%. But as of 29th August, the day after the next provisional tax payment date, the rate will increase to 10.91%. (Incidentally, the rate payable for overpaid tax will also rise, and that goes from 3.53% to 4.67%).

It is necessary for Inland Revenue to have a tool such as an interest charge for unpaid tax. Otherwise, people would just not take any action. But I think that is only one of the tools in its arsenal, as I just mentioned it really does need to back this up with greater enforcement and earlier interventions.

At the same time, Inland Revenue and tax advisers can all work together and let people know that when you take proactive steps on tax debt, you will find Inland Revenue is much more prepared to work with taxpayers in default than people might imagine. This has always been my experience. You front foot these issues with Inland Revenue, and you will find they will be prepared to work with you and your clients unless they are actually dealing with a serial defaulter.

For example, yesterday I was speaking with someone who’d run into some difficulties and had gone to Inland Revenue. They had been very pleasantly surprised by how proactive Inland Revenue had been in working with them on sorting out their unpaid tax. I could see clearly see that they felt a lot happier about the position. They still owed money, but they were in a position where they knew there was a way forward.

The key lesson is if you’re in trouble with Inland Revenue over unpaid debt, talk to it and your advisers and then you’ll hopefully get better results.

Incidentally, the rate of prescribed rate of interest for calculating fringe benefit tax on employer provided loans and some other measures is also being increased with effect from the quarter starting 1st October. From that date, the rate will rise from its current 7.89% to 8.41%.

Upstart Nation? Changing the tax system to boost startups

And finally this week, an interesting report called Upstart Nation from the government’s Start-Up Advisory Council.

This has been the business group looking at how to improve the rate of startups and develop more startups into major companies. On 1st August it released its report which included suggestions regarding changes to the tax system to help boost startups.

The report’s objective to “present a comprehensive strategy aimed at transforming New Zealand into a thriving hub for innovative UpStarts”. The Council identified four primary pillars as key: Capital Capability, Connectivity and Culture. Specific recommendations were made by the Council for each of those pillars to address identified gaps and leverage opportunities.

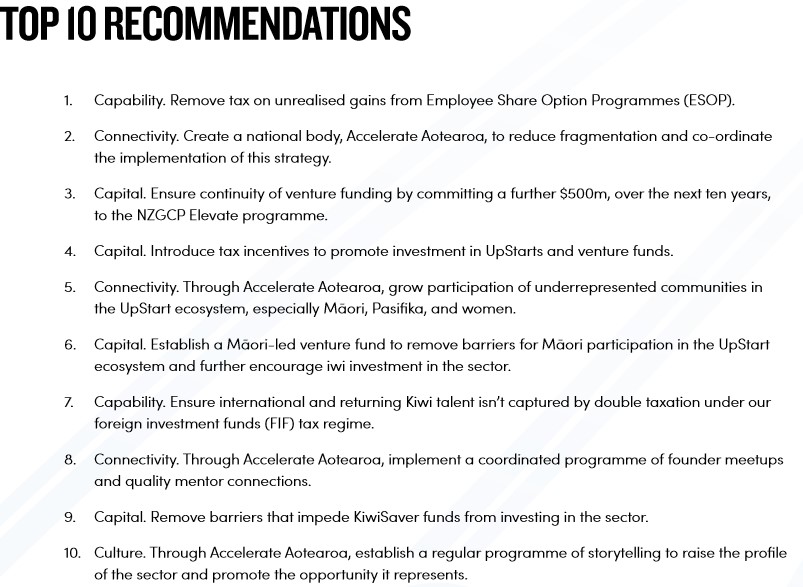

It had ten recommendations which it felt “will have the greatest impact on our ecosystem”.

Interestingly, three of those recommendations involve changes to the tax system. The first was wanting changes around the taxation treatment of share options and employee share option programs (ESOPs) in particular.

Generally, the current position is a taxable gain arises on the exercise of the options. The Council thinks it would be more appropriate to move that taxing point to when the underlying shares relating to those options are sold. ESOPs are intended to attract and retain investors and key employees as the business grows. Accordingly, hitting them with early tax charges ahead of when they actually can realise their position is a bit of an impediment. There are also questions around the compliance costs involved in getting accurate valuations in what is often an illiquid market. I hear this quite a bit.

Another was specific incentives to promote investment in UpStarts and venture funds in is some form of deduction for such investments. The Council recommends officials carefully review the Australian and UK tax concession schemes and develop something tailored to the New Zealand setting. In particular, they were looking at the Australian Early Stage Innovation Company scheme, which provides a deduction for an investment and a capital gains tax exemption.

The council suggests a deduction of maybe up to 30% of the capital invested directly in an UpStart or UpStart venture fund capped at $200,000 a year. That’s an interesting suggestion and one worth considering even though it probably won’t be accepted by fiscally prudent governments.

An urgent issue with the foreign investment fund regime

The third suggestion included in the top ten recommendations was to “Ensure international and returning Kiwi talent isn’t captured by double taxation under our foreign investment funds regime.” This issue almost exclusively affects American investors and employees with overseas investments. Once their four-year transitional residence exemption expires and the foreign investment fund (FIF) regime takes full effect, they are essentially taxed on an unrealised basis. At the same time, because America requires all its citizens to file tax returns, they are still subject to tax there and in particular capital gains tax.

This is something I’ve discussed with a number of clients. Although they can claim foreign tax credits in America in relation to the FIF tax payable, it often exceeds the equivalent amount of US tax payable on the realised gains. They are therefore accruing a tax liability, which in some cases they can never fully offset. In effect, they feel they are facing a double tax charge.

The Council recommended “this issue be investigated under urgency with a view to removing FDR on people caught under this double tax conundrum to ensure we can attract and retain them in New Zealand”.

I agree this needs reviewing. We hear frequently we are in the business of attracting talent here. In this particular case, we have an issue (somewhat ironically, a by-product of not having a comprehensive capital gains tax) which potentially hinders getting vitally important migrants.

You could argue that not this particular issue doesn’t just affect investors in the startup sector, but also any American citizen or returning New Zealanders who have acquired American citizenship or a Green Card and are among the groups of skilled migrants such as doctors or other specialist engineers, etc. This is a real impediment we need to consider.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.