the first ever sentencing for possession of tax evasion tools.

Inland Revenue’s draft long-term insights briefing currently out for consultation has generated quite a bit of debate. The paper discusses the future shape of the system and how to fund the rising cost of superannuation and related health costs.

Sir Roger Douglas has now entered the chat as he, together with Professor Robert MacCulloch of Auckland University, have released a paper titled How to change the welfare state from a taxation to a savings-based model. In some typically bold thinking from Sir Roger, the proposal is to dramatically change the tax system, and instead of trying to raise additional tax to meet these costs, take a completely different approach.

A tax cut or something else?

Sir Roger and Professor MacCulloch suggestion is for the first $60,000 of income to be tax free. Based on current tax rates, that’s at least a $10,000 tax cut for everyone with income of at least $60,000. Instead, those taxes would be directed into mandatory savings accounts for health, pensions and other risk cover. These would then be supplemented by employer contributions (effectively a social security tax, although not specifically described as such) with the trade-off for these contributions being a cut to the corporate income tax rate.

They’ve released a short paper outlining their proposal (there’s also a more detailed paper that Sir Roger and Professor MacCulloch produced in 2020). The paper starts with an analysis of the forthcoming rise in health and superannuation costs and the need to take a long-term view on addressing this issue. Sir Roger and Professor MacCulloch take the view that the conventional approach, raising taxes to meet these costs isn’t going to cut it. Something more dramatic is needed.

Taking the axe to corporate welfare

In addition to the proposed mandatory savings accounts, Sir Roger and Professor MacCulloch propose cuts to what they call corporate welfare and grants to high earners. The cuts include the removal of screen production grants, ending accelerated depreciation allowances for industries such as forestry, fishing and bloodstock, withdrawing winter energy payments to wealthy households and KiwiSaver subsidies to higher earners. They also propose ending the “favourable tax treatment to owners of rental housing” but this isn’t defined. I’d be very intrigued to know more about what exactly they’re driving at there. All up Sir Roger and Professor MacCulloch suggest these could save over $12 billion annually.

Yeah, but…

This is quite a radical proposal which would be quite a shock to the system, and I’d be very interested to see what other economists think of it. One hurdle I see is with the proposals aimed at introducing competition into the provision of health services. This is a perennial problem for our economy. We are just 5.2 million people and 2,000 kilometres away from the nearest neighbour. Competition in that context is always going to be difficult but it’s an issue we need to address, not just in this context but across the economy as a whole, because I think it’s a major problem for our economy.

Overall, you can never say that Sir Roger Douglas would die wondering. As a RNZ report noted it’s a bold plan and I recommend reading the summary paper. Bear in mind some of what it proposes in terms of removing subsidies such as the Government’s KiwiSaver contribution for high-income employees are now actually happening.

What about increasing GST?

On a more conventional approach Inland Revenue’s briefing paper includes a discussion about the implications of raising GST from 15% to 18%. Last Thursday I spoke with Wallace Chapman of RNZ’s The Panel about this proposal.

The Inland Revenue briefing paper notes the suggested GST increase could raise $5.5 billion of tax annually. This is because, as I explained to Wallace and his panellists, GST is an enormously efficient tax. It does meet the classic broad based low-rate approach. You broaden the basis as widely as possible so you can have as low rate as possible. Furthermore, because we have no exemptions, our GST is enormously efficient. So really if you were thinking of increasing taxes your first point of call would be to raise GST.

A regressive tax

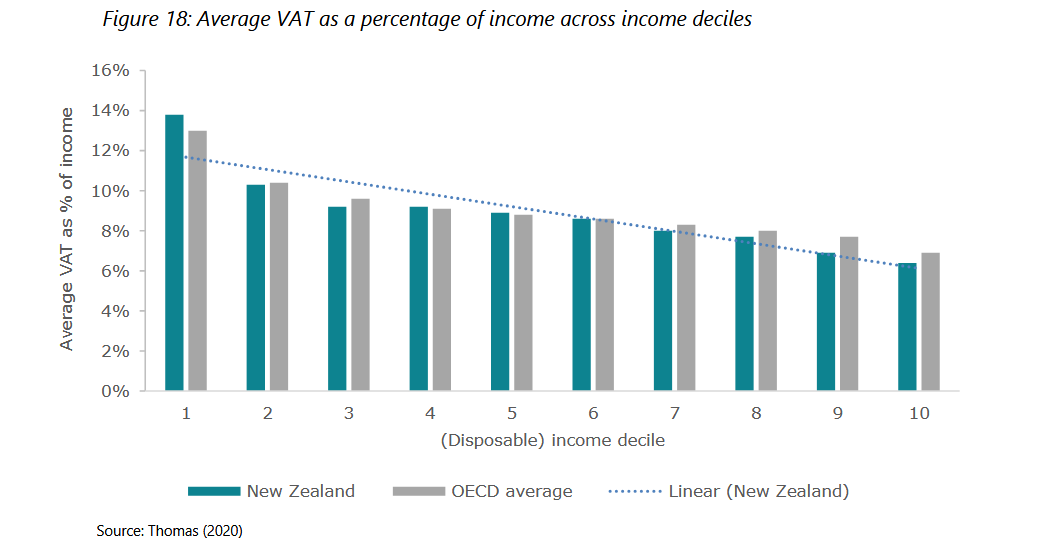

The problem is though, as Inland Revenue pointed out and as Holly Bennett, one of Wallace’s guests immediately jumped on, GST is a regressive tax. There’s quite an interesting analysis of this in the Inland Revenue briefing paper. The paper notes that GST or VAT (value added tax) is regressive relative to income.

According to the organisation of Economic Cooperation and Development (the OECD), the average GST to income ratio declines from 10.4% in Decile 2 to 6.9% in Decile 10. We follow a similar profile with our GST to income ratio declining from 10.3% in Decile 2 to 6.4% in Decile 10.

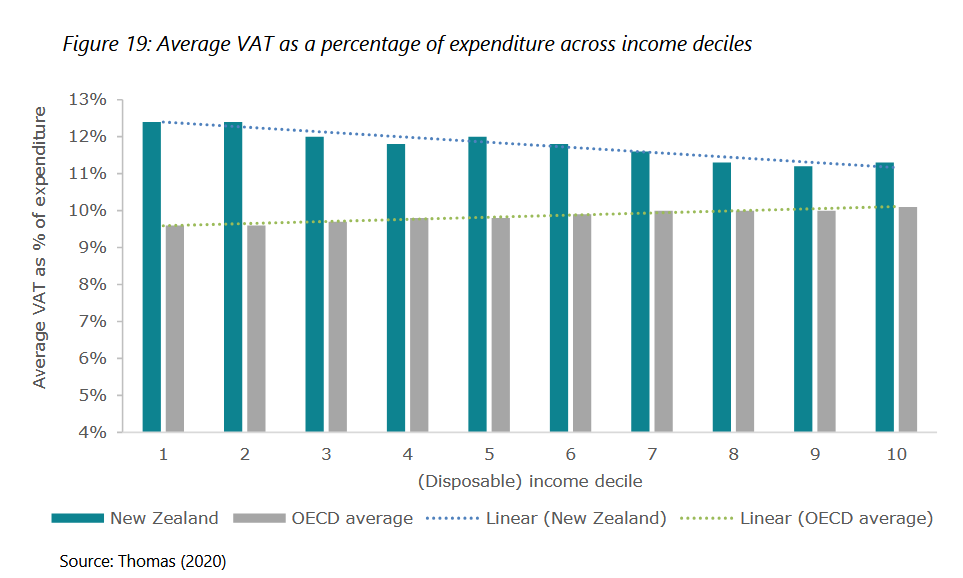

The Inland Revenue paper also considers the effect of GST relative to expenditure. In this instance GST or VAT is slightly progressive for most OECD countries because of the exemption of tax of necessities such as food and some sanitary products and various other Items which make up a very large proportion of the consumption basket of lower income households. However, our GST, because we don’t have any such exemptions, is mildly regressive.

Increasing poverty?

As Holly Bennet (one of Wallace’s panelists) was quick to also point out, an effect of GST increases is to increase the poverty headcount. According to Inland Revenue, based on the 2015/2016 Household Expenditure Survey GST “increased the imposition of GST in New Zealand increased the poverty headcount by 4.7%, the poverty gap by 1.7%, and the squared poverty gap by 0.8.” What’s worse is that the effect of those increases is higher than the OECD averages of 3.1%, 0.7%, and 0.3% respectively, again, because we have no exemptions.

The GST dilemma

So, raising GST results in the dilemma that it would raise a lot of revenue very quickly but hit lower income families harder. The suggestion in Inland Revenue’s paper is that there should be a compensation increase in welfare benefits for low-income families. They suggest that would probably cost maybe $440 million a year in total.

Readers and listeners may recall that last year a guest was Andrew Paynter, one of the Tax Policy Charitable Trusts co-winners. We discussed his proposal of raising GST to 17.5 % and introducing a GST refund tax credit for low- and middle-income earners.

Coincidentally or not, Andrew works for Inland Revenue, but there’s a worldwide trend looking at this particular issue. For example, the International Monetary Fund released a paper last year Designing a Progressive VAT which suggested a point of sale credit for low-income families. As the Inland Revenue paper notes Canada and Thailand have point of sales/refund credits for low-income earners.

Some form of capital taxation also needed

If you were adopting a conventional approach to addressing the rising expenditure gap, then raising GST is the most likely approach. My personal view is we also need to have some form of capital taxation because as I explained to the Panel, not only do we have rising health and superannuation costs, the cost of dealing with the impact of climate change, is rapidly accelerating.

This week Forsyths Barr and the Insurance Council released data that showed that over 40 years, the average annual cost of dealing with weather related events was $203 million. However, in the latest 10 years those costs had risen to $606 million annually and the five-year average is now $952 million per annum. Currently Tasman is spending $500,000 a day repairing its roads in the wake of the recent floods.

So climate change is having a huge impact now and there are a huge number of properties – 220,000 in total – presently worth over $180 billion, which are located within coastal inundation and inland flood zones. More than a quarter of those are in the Canterbury, Tasman, Gisborne, West Coast and Nelson regions. Those last four of which have all had severe weather events in the last year.

A quid pro quo

Protection against climate events will be another growing demand, particularly since for most people their property is their principal capital asset. This is where I think some form of capital taxation/capital gains tax is perhaps appropriate because if the Government and local councils are expected to spend more to protect capital assets, the quid pro quo must be that those capital assets become taxable.

Working for Families – a correction

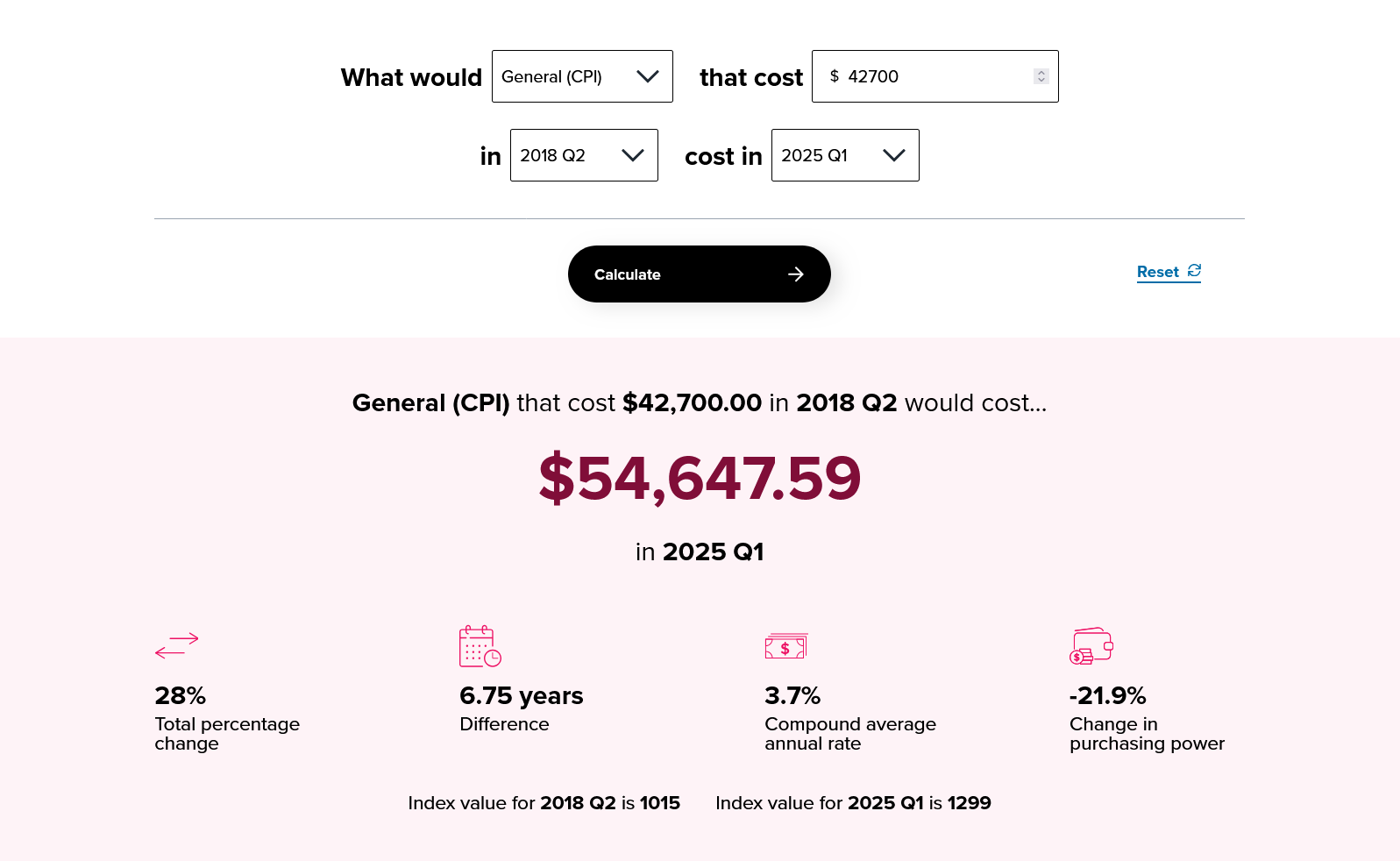

Moving on, last week I talked about the changes to FamilyBoost and I noted that there had been no change to the threshold for Working for Families. That was actually incorrect. A kind reader from Inland Revenue pointed out that the Working for Families threshold will increase to $44,900 with effect from 1st of April next year its first increase since July 2018. Thanks for getting in touch and apologies for my error.

I’ll just simply add that on an inflation adjusted basis, that threshold should have gone up to something like $54,650 so it’s still way short of where it should be.

In any case the effect of the increase in the threshold from$42,700 to $44,900, which remember is for a family’s income, is mitigated by the increase in the abatement rate went up from 27.5 cents per $100 to 28 cents per $100.

Furthermore, the other point I made last week was about the focus of the FamilyBoost towards higher income families. That point doesn’t change just because the threshold for Working for Families has been (slightly) increased.

A New Zealand first

A recurrent theme this year is how Inland Revenue has increased its focus on chasing non-compliance. The latest example is the Auckland man who has become the first person in New Zealand to be convicted and sentenced for aiding and abetting his company’s possession of the electronic sales suppression tools.

Now these sales suppressions tools basically alter the Eftpos record so they’re very much about suppressing income and basically trying to defraud the taxpayer. In this case, Gurwinder Singh has been sentenced to seven months home detention on tax evasion charges, including the charge of aiding and abetting this company for possessing electronic sales suppression tools for the purpose of evading the assessment and payment of tax.

All up, Singh’s tax evasion amounted to $198,500. Apparently one of the things he was also doing was although he had four employees, including himself, he was only reporting PAYE returns for two staff. So, some obvious and not so obvious tax evasion was going on here. Anyway, this is the first time the new law in relation to electronic sales suppression tools has been applied. Would-be fraudsters have been warned.

The pitfalls of schedular payments

As often mentioned, Inland Revenue turns out vast amounts of very interesting and helpful material. Once such source are its Technical Decision Summaries about issues or rulings that Inland Revenue has encountered.

One TDS released this week is a private ruling in relation to the application of the schedular payment rules.

This involved a company wanting to make use of offshore personnel to act as directors in New Zealand. The question of interest here is a reminder that if you are making payments to overseas persons, they may, even if they are contractors, be subject to non-resident withholding taxes/schedular payments.

That’s why this one is useful. This ruling explained why those provisions would not apply. But typically, if they do apply then 15% withholding tax can be deducted which can come as a shock to some overseas persons. This is a useful ruling on a point which we often encounter but is one of those cases where I suspect the compliance isn’t always as diligent as it could be.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue releases submissions on the taxation of not-for-profits.

A major report on climate adaptation ducks a key issue.

Last week, it emerged that the Finance Minister, Nicola Willis has sought advice from Inland Revenue and Treasury on whether New Zealand’s major banks are paying enough tax.

According to a release on policy work being undertaken by Treasury and the Reserve Bank, the Finance Minister “and the Minister of Revenue have commissioned Inland Revenue to review whether income tax settings are applying correctly to banks for potential consideration at Budget 2026.”

This is a clear implication that some changes may be ahead, or are being considered for next year’s Budget, which coincidentally is also an election year.

“A wide range of options”

It appears Inland Revenue are considering, “a wide range of options.” What’s often brought up with banks is whether they have excessive levels of profits and therefore should be subject to a windfall tax.

The debate around excess profits and windfall taxes frequently arises. As the Greens rather ironically pointed out, Margaret Thatcher introduced a surcharge for banks in the early 1980s, when the monetarist policy that the British Thatcher government had adopted meant that increases in interest rates would naturally flow through to higher profits for the banks.

Thatcher, together with Chancellor of the Exchequer (Finance Minister) Geoffrey Howe took the view that as the banks were profiting from monetarism they should pay additional tax as a result. However, windfall taxes are highly problematic in terms of defining.

Clearly it would be perhaps appropriate to align settings with Australia. An alternative therefore might be to adopt the Australian bank levy.

A 0.6% levy on banks with liabilities over A$100 billion has been in place since 2017 and there have been calls to increase it. If you’re aligning the treatment of the big four banks with what their parents are subject to in Australia, then politically you have probably removed one objection to any such surcharge.

Another area which could be considered are the thin capitalisation rules. That is, the level of debt that banks would be allowed to carry and still claim deductions.

The general rule is that if the debt/asset threshold exceeds 60% then interest restrictions are put in place.

There is a lot going on in this space around the world. Last year the OECD’s corporate tax statistics report said that there are now over 100 interest limitation rules in place, which is up from 67 jurisdictions having such rules in 2019.

Obviously, the Government considers there is some scope for tweaking the tax rules, but this is a political matter and ACT leader David Seymour has already put the kibosh on that. Whether that means the Government will not proceed, or that it reaches out to see if it can get cross party support on any proposals, we’ll have to wait and see. This is an interesting development which we will watch with some interest.

FamilyBoost scheme changes

The Finance Minister also announced on Monday that there would be changes to the FamilyBoost scheme which gives eligible families a rebate on fees paid to early childhood education centres. Take up has not been anywhere near as high as was expected or promoted when the proposal was made.

In recognition of this, the Government decided to revamp the scheme and has lifted the threshold for maximum eligible income from $45,000 per quarter to $57,286 per quarter. In other words, from $180,000 per annum to $229,000 annual household income.

The amount that can be increased has gone from 25% to 40%, up to a maximum of $1,560 per quarter. There’s also a reduction in the abatement rate from 9.75% to 7% for household income over $35,000 per quarter.

The intention is that these changes will come into effect for childhood education costs incurred in the current quarter from 1st July to 30th September onwards. Legislation will come be coming through on this.

As the tireless Craig Renney, Chief Economist for the Council of Trade Unions, has noted, this change is very generous and is weighted towards higher income families.

What about Working for Families?

Looking at the increased abatement thresholds coupled with reduced abatement rate, I do not understand why the Government has done nothing in relation to increasing the abatement threshold for Working for Families, which still remains at $42,700 for total family income.

Although there were changes in this year’s Budget (including an increase in the abatement rate to 28%) this threshold has not been changed since 1st of July 2018, seven years ago now.

The Government is sending mixed messages. Both measures – Working for Families and FamilyBoost – help working families, but it appears only high-end families have the issues of abatements and the impact of high effective marginal tax rates addressed.

There would probably be greater cost involved in lifting thresholds and/or reducing abatement rates for Working for Families, but whoever said politicians would be consistent in their approach?

To me the changes create a weird scenario. But FamilyBoost was a Government election commitment, so it’s understandable the Government is trying to make it more accessible.

Inland Revenue releases submissions

At the start of this year there was a lot going on in relation to the not-for-profit sector, with many thinking the Government was looking to change the tax treatment of this sector and in particular the exemption from business taxation for businesses run by charities.

It subsequently backed away from that although the issue of the taxation of mutual transactions of associations, clubs and societies is still under review.

Last Monday (it was a busy old day) Inland Revenue proactively released the submissions it received on the issues paper Taxation and the Not-for-profit Sector it sent out for consultation in February. It received 826 submissions, which is quite a number, and it has published all these submissions where permission has been given. It’s also produced a four-page summary of the common themes in the submission.

One was that consultation needed more time, which I totally agree with. Others felt the Government was looking at the wrong end of the issue in that not-for-profits provide a net benefit, not a net cost for the Government, because they save government expenditure.

Another was that the issues paper lacked clarity about what was the problem to be addressed, with many submissions suggesting the focus should be on the bad actors. All good points in my view.

What about the charity business exemption?

On the charity business income exemption, there were differing views as to whether in fact charities had a competitive advantage.

Economists generally agreed with Inland Revenue‘s view that no advantage existed. But other submitters disagreed. There were questions about the complexity of defining the issue at stake, with some submitters skeptical about how much revenue could be raised.

There were also suggestions that maybe a minimum distribution rule could be a more effective policy response.

There was a mixed response on the issue of donor-controlled charities. As usual, some acknowledged there were concerns on this, but others thought again that the existing regime was rigorous enough and any changes would impose increased compliance costs.

On the vexed issue of not-for-profits and friendly society transactions, the view was that these should be removed from the system and member subscription should remain non-taxable.

In relation to a de-minimis tax free threshold “There was near universal support from those that submitted on the mutuality topic that the $1000 income tax deduction was too low and should be increased.”

Overall interesting to see these responses. As noted above, consultation has just closed on the application of the mutuality principle to transactions of associations, clubs and societies. There has been strong pushback on this as well so it will be interesting to see what emerges.

This is a group that’s been put together to give the Government some guidance on developing a framework for dealing with climate adaptation. It’s a short report, only 16 pages and well worth the read.

The report’s opening paragraphs dive right in:

“The group considers there to be an urgent need to change the way New Zealand adapts to climate change. New Zealand is already experiencing the impacts of climate change, but it is currently underprepared. This is leading to larger and more frequent recovery costs, unmanaged financial strain and disproportionate impacts on some groups.

Climate change will continue to bring substantial financial costs for the country. Failing to act or delaying decisions will not avoid or reduce costs that New Zealand governments, businesses and individuals face.”

That’s an on the nose and in my view accurate summary of the position we face. As I’m recording this podcast the Nelson/Tasman region is under a state of emergency for yet another storm that is expected to hit in the next few hours. This is just the latest experience of the “impacts of climate change. Achieving “a consistent approach”

The report considers that “New Zealand needs a consistent approach to decision making that is well informed about the risks.” To achieve this approach, it suggests there are three key areas which need to change.

Firstly – New Zealanders need to have fair warning about the way natural hazards could impact them, so they can make informed decisions too.

Secondly – New Zealand should take “the broadest interpretation of a ‘beneficiary pays’ approach to funding the increased investment and risk reduction because of climate change. This would mean that those who benefit most from these investments contribute more.”

Finally, people and markets should adjust over time to a change in climate. The adjustment is already happening. Insurers have been raising premiums and making it clear that there are areas where the insurance risk is greater than they are comfortable with.

The question that the report raises is the length of this transition period beyond which “people should not expect buyouts”. In its view

“The Group acknowledges there is no right answer to how long a transition should take. However, the Group considers that a transition period of 20 years would appropriately balance the need to spread costs with creating the right incentives to act.”

Who pays?

However, the report is pretty silent about the meaning and extent of what it refers to as “financial assistance” which, it suggests, does not continue beyond the transition period. Neither of the words ‘tax’ or ‘levy’ appear in the report and in my view, that’s kicking the can down the road.

The report is right to highlight the scale and urgency of climate adaptation, but it should have gone further and said, “we need to prepare for this, we suggest that it’s going to need either higher taxation or a climate levy.”

By doing so, the issue comes up for discussion. Instead, it has rather ducked that point.

This has drawn criticism from a climate policy expert, Professor Jonathan Boston, who said phasing out government assistance for climate adaptation and property buyouts would be “morally bankrupt.”

Although he agrees we should not be creating incentives for people to stay in risky areas, he feels that a 20-year transition period is not long enough, and ongoing government support will be needed. I agree with both those points.

The costs of climate change are happening now

The issue of how governments manage rising superannuation and health costs is important. But I think the more immediate financial impact we have to address is climate adaptation.

And unfortunately this report, although it clearly spells out the risks that we’re facing and the need to develop a framework to respond, ducks the key question of “who’s going to pay for this, and how do we finance that transition?”

As I have said repeatedly, this is going to involve some form of tax increase or specific levy.

The cost of climate adaptation is an issue where we really do need all the politicians to put party politics aside and address the longer-term issues – that climate adaptation will involve huge costs which presently falls on local councils who are in no position to fund the burden.

It is going to require central government support, in the form of specific tax or levy.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day and best wishes to everyone in Nelson/Tasman, or anywhere else affected by the bad weather.

Last week I discussed the Green Party’s wealth tax proposals, and commented about how what makes New Zealand an outlier in world tax terms is not so much that we don’t have a capital gains tax, but we also don’t have an estate tax, gift tax, land taxes (other than rates), stamp duties and taxes on wealth or wealth transfers, which exist in many other jurisdictions.

This prompted reader kiwikidsnz to respond as follows

It’s a really interesting comment and thank you for that, because it gets to the heart of the issue around tax and how it changes people’s behaviour. Tax is regarded in economic literature as a deadweight cost. Any tax is therefore distortionary, but we have taxes because they pay for things that people like, such as roads, schools, hospitals, infrastructure and pensions, and a whole heap of other services. Accordingly, a key purpose of taxation is to raise the maximum amount of revenue without producing too many distortions and disincentives.

International Monetary Fund on productivity “a significant challenge”

kiwikidsnz’s comments coincided with a report issued by the International Monetary Fund (the IMF) on New Zealand’s productivity challenge. This paper was prepared following the IMF’s visit here in late February and early March as part of their annual review of the New Zealand economy and it does not make for good reading.

As the paper’s opening paragraph notes:

“Weak productivity growth poses a significant challenge for New Zealand’s long-term prospects. Low productivity growth partly reflects structural factors, including New Zealand’s remote geography and small markets, as well as the relatively large role of the tourism and agricultural sectors. However, it also reflects costs and incentives for investment and innovation, which are in turn shaped by features of the business environment and limited financing options.”

Tax is a part of the business environment and as mentioned above the question arises about the distortionary effect of tax. Now the report, and I recommend reading it, is relatively short, but it’s very thorough. But as I said, it’s pretty grim reading because

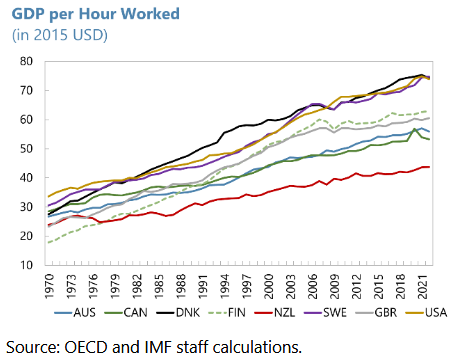

“Over the past five decades, labor productivity growth in New Zealand has lagged that in peer advanced economies, resulting in a widening gap between New Zealand’s GDP per hour worked and that in peers. As a result, by 2022, GDP per hour worked was well below levels in comparable economies.”

A productivity growth challenge across the economy

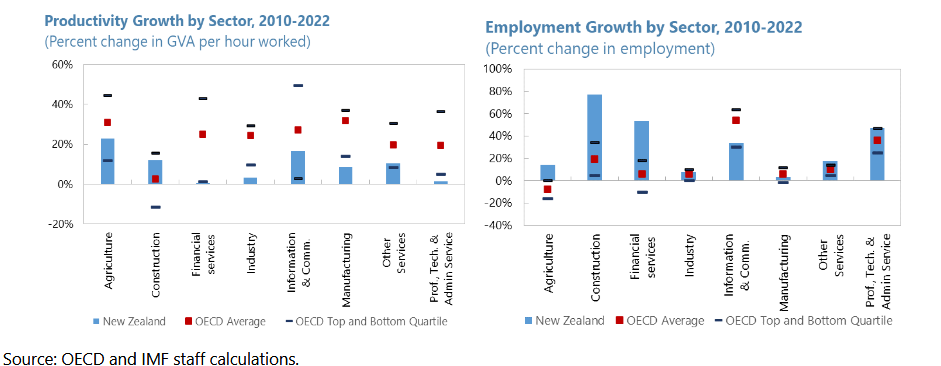

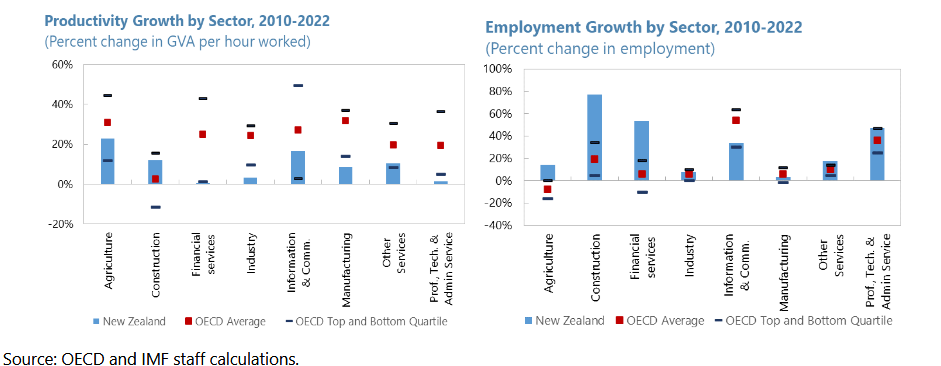

The paper examines this why this has happened and it’s not good reading. A part of the paper that really jumped out at me was paragraph 8 Productivity at the Sector Level. According to the paper labour productivity growth from 2010 to 2022 was below the OECD peer average in agriculture, information and communication (ICT) and some service sectors. In fact

“Productivity growth in New Zealand was in the bottom quartile among OECD peers for financial services, industry, manufacturing and professional and technical service sectors over the same period. The only sector where productivity growth in New Zealand was above the OECD average over this period was the construction sector. New Zealand’s productivity growth challenge thus does not appear to be confined to a few sectors, but to reflect broader issues across the economy.”

Basically, it appears our high immigration has been masking the low GDP per capita growth. ”New Zealand’s workforce has not witnessed the same efficiency gains as workforces in AE [advanced economy] peers (has not been ‘working smarter’), but it has compensated for this with adding more workers at a faster pace.”

Not enough gazelles and too many in the wrong sectors

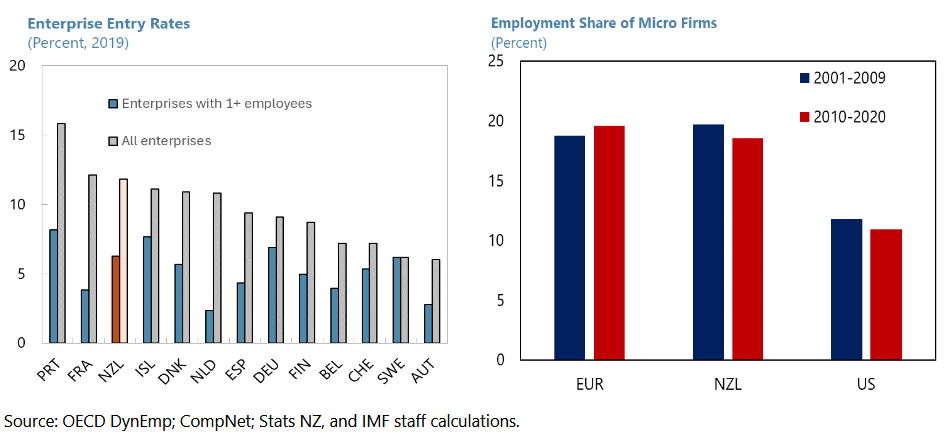

Another damning part of the report is Section B In Search of New Zealand’s Gazelles. Gazelles are young high growth firms that see 20% growth in sales over at least one three-year period when they are under 10 years, from a base of at least USD100,000. Basically, we don’t have enough:

“Since the Global Financial Crisis, birth rates of gazelles in New Zealand, as a share of all new firms established, have been below the median observed in peer advanced economies. At around 13% gazelle birth rates in New Zealand were below levels observed in Australia, Finland or Sweden, but above levels observed in the Netherlands or Denmark.”

Paragraph 14 of the report I think, gets to where the real problems within our economy have arisen, and where tax may have played a very significant part. It notes young, high growth firms in New Zealand have been concentrated in a few sectors:

“Over 2008 to 2018 new gazelles in New Zealand were primarily concentrated in the financial and real estate sectors. The share of new gazelles in this sector was higher in New Zealand than in most peers, even as the sector saw lower overall productivity growth. At that same time, the share of new gazelles in ICT and professional and technical services, which include hi-tech product, high-productivity sectors dependent on innovation, has been lower in New Zealand than in peers. These trends suggest investment and innovation incentives may be misaligned between sectors in New Zealand. Trends could also be a symptom of the high propensity to save in real estate.”

This is where I think the issue of our lack of capital gains tax and a general lack of capital taxation comes home to roost. The incentives to invest in businesses have been trumped by the investment and lending practises in real estate. I think it was a particularly telling comment here about how those new gazelles, which are a very important part of productivity growth, are primarily concentrated in the financial and real estate sectors.

Replacing one set of disincentives with another

To pick up the issue that kiwikidsnz raised, economic efficiencies do arise from tax policies. Removing incentives such as 66% tax rates and a whole pile of distortionary tax incentives that are given because a government is trying to promote particular behaviour is a good move. But there’s also the disincentives to divert capital if you do not tax something, and it’s is becoming clearer and clearer to me that this is the biggest single problem with not taxing capital gains comprehensively. Coupled with bank lending practices what has happened is we’ve diverted resources into real estate resulting in lower productivity growth and less efficient use of our limited capital. That’s a policy issue that all parties need to consider.

The Australian counter-example

It’s worth talking about the long run implications of the Rogernomics reforms that happened starting in 1984. In October 1985 Australia was also going through its reform period but taking a more measured approach. One of the things it did was to introduce a comprehensive capital gains tax with effect from October 1985. We actually therefore have 40 years of examples to look at what happened around productivity.

Now productivity growth in Western advanced economies has been an issue, but Australia has seen higher productivity over the past 40 years. It has a capital gains tax. We have had lower capital productivity growth, and we don’t have a capital gains tax. Now, correlation is not causation, but there’s 40 years of examples there to make everyone think very hard that maybe in this case correlation does equal causation.

Interestingly, around the whole question of the 1980s idea of supply side economics and cutting taxes to generate economic growth, generally now seems to have run its course, and it probably was always going to do that. Simply because if you’re starting in the 1980s, individual tax rates were then at 60-70% and even more, in some cases. If you’re cutting rates down to 30-40% that’s a significant move and you’re bound to see something happen. But once rates get down to 30%-40%, the impact of tax cuts is less clear.

Meanwhile, in America, maybe not such a Big Beautiful Bill?

What’s really interesting is at the same time as the IMF report came out over the United States) someone who’s been described as the MAGA movement’s top economic guru, Oren Cass, has come out and been very critical of the latest President Trump backed tax cuts included in the Big Beautiful Bill (yes, it really is called that). Mr. Cass is the chief economist for the right leaning American think tank American Compass. He remains the leading proponent of conservative economic populism amongst allies of President Trump.

In talking about the Big Beautiful Bill and the tax cuts that have been included in that, Oren Cass has basically said that the ideas around the Laffer Curve and supply-side theories which have dominated tax policy thinking for the last 40 years have essentially run their race. After commenting “There’s much less confidence in the 1980s-style supply-side tax cutting” he went on

“The reality is we are not going to solve our economic problems if we do not get serious about the fiscal push and fiscal picture and actively reduce the deficit that’s going to require both reduced spending and raising revenue. If you’re not willing to do that, then I don’t think you can credibly say you’re addressing our economic problems.

…Whereas in the past you would have just said, “Well, this thing pays for itself,” This time there is a recognition that it does not pay for itself, — and we have a fiscal crisis — so we also need to explain how we’re at least partly going to pay for it.”

This is an absolutely astonishing admission to hear from a right wing think tank, and particularly in America, which is the home of the supply-side theory.

The thing to keep in mind about taxes, as I said last week, it’s all about politics. But taxes reflect economies and economies change. kiwikidsnz was right to make the comments that there were inefficiencies in our tax system in the 1980s and they were ripe for reform. But it is not a question of set and forget and that’s it, job done, we never have to change again. The dynamics of tax and economies change all the time. And our thinking around that needs to change and reflect that. As a few people pointed out in response to kiwikidsnz we may not have a capital gains tax but other countries do and they have also inheritance taxes, stamp duties, etc and in most cases those peers are wealthier than us. There is 40 years of evidence to suggest that non taxation of capital isn’t actually the economic Nirvana you might think, and it has distorted our economy, particularly our productivity as the IMF notes.

Dr Rod Carr on markets: “myopic, reckless and selfish”

On a related point there was a really interesting leader opinion piece by Dr Rod Carr in the Sunday Star-Times on 1st June. Dr Carr has had a hugely impressive career. He’s been previously chair of the Reserve Bank of New Zealand, worked at Treasury in the 1980s during the Rogernomics reforms and was the inaugural chair of the Climate Change Commission. In summary he has a vast wealth of knowledge about economic policy development in New Zealand over the past 40 years.

His topic was the role and influence of markets. Looking back, after completing an MBA in Columbia University in the mid-1980s, there was little doubt then that markets could allocate financial capital more efficiently than politicians and technocrats and corporate conglomerates. And he believes markets are still, “ruthlessly efficient at allocating privately scarce resources with a price.”

However, he continues markets are “myopic, reckless and selfish,” and understate future benefits and exclude or understate future costs. This results in

“…underinvestment in long-life infrastructure, the degradation of natural ecosystems and under investment in public health and education markets. Markets are reckless because we have created an asymmetry that sees profit accrue to those with private property, while costs are left to lie with the general public.”

He concluded “Markets should be a tool to enable us, not a mantra to enslave us.”

After 40 years, time to think again?

If you combine what Dr Carr said with the comments of Oren Cass and the IMF report on productivity, we’ve now had 40 years of results to look back at how our tax system has evolved and worked in relation to taxation and capital. In my view the long and the short of it is, it hasn’t gone according to plan. Maybe it’s time to look at the script all over again and rethink how we want to have our capital used if we want to start growing a few more gazelles, lift productivity and our living standards.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Inland Revenue’s clampdown on the horticultural sector.

Earlier this year Inland Revenue released an issues paper consulting on fringe benefit tax changes. This originated from a 2022 stewardship review of FBT. The issues paper noted it has been 40 years since FBT was introduced and it was therefore opportune to reconsider certain areas of the tax.

One of the key areas the Government is consulting on is in relation to the FBT treatment of motor vehicles. The issues paper noted that there may be some concerns and misconceptions around the work-related vehicle exemption as it applied for twin or double cab utes. There appears to be a widespread perception that twin cab utes are exempt from FBT because they represent work related vehicles.

On Tuesday, Inland Revenue Deputy Commissioner for policy David Carrigan stated in a press release that it is a myth that utes have always been free from FBT.

“When it comes to double cab utes, these are treated no differently to any other vehicle unless the use of the vehicle meets all requirements for an exemption from FBT, then a double cab ute is and always has been subject to FBT. That is the current law.”

He added that work related vehicles are only exempt from FBT if they meet specific requirements. But there is no blanket exemption for twin cab utes.

The press release goes on to explain the way the rules work and how the exemption might work. The basic position being that it is only exempt on days when it is used for essential work purposes as defined by Inland Revenue. Where vehicles are used partly for business and partly privately, they’ve always been subject to FBT on the days those vehicles are used for private purposes.

Simplifying FBT

According to the press release the purpose of the proposals out for consultation, if implemented, is to simplify FBT and reduce compliance costs, not create additional obligations. If a business, including a farm, is not currently liable for FBT on a vehicle, then it’s unlikely that that business would become liable for FBT on any proposals taken forward.

The press release then concludes by reminding that government still hasn’t made any final decisions in relation to any potential changes for FBT as it’s still considering the feedback it received on the issues paper released in April consultation which closed on 5th May.

My expectation is that if we’re going to see anything happen, we’ll see any changes included in this year’s tax bill, which we can expect to see in late August/early September based on previous years.

In the meantime, it is interesting to see Inland Revenue feels compelled to come out and remind people of the rules. Clearly, the perceived status of twin cab utes was something of a sore point for some people who felt that the work-related vehicle exemption was being abused.

Inland Revenue targets the horticulture sector.

Moving on, we’ve frequently discussed Inland Revenue initiatives on compliance and debt enforcement. As we noted last week, the Budget allocated close to $90 million this year in additional funding to Inland Revenue for investigation and general compliance work and debt management. The expectation is that Inland Revenue will get a return of $8 for every dollar put into such activity.

And then on Wednesday, the latest update on Inland Revenue’s progress in these areas was in relation to the horticultural sector where the press release noted

“Inland Revenue is seeing a few concerning practises in the horticultural sector, including people being paid under the table.”

In the past ten months, Inland Revenue has found $45 million of undeclared tax in the horticultural industry from under the table cash sales not being reported correctly, withholding tax either not being deducted on schedular payments made or deducted at the wrong rates. In some cases, the payments were not even reported to Inland Revenue.

Convoluted structures

According to the press release, many of the issues Inland Revenue has seen arise are in relation to labour hire firms, who frequently pay the labourers in cash. Some of those firms then use convoluted business structures to try and hide those payments and avoid the withholding tax obligations that come with them.

The problem Inland Revenue has with this behaviour is the withholding tax it’s obviously missing out on. But it also means that because the labourers’ incomes have been understated, they could possibly get benefit payments they’re not entitled to and in some cases avoid their child support and student loan payments.

Unsurprisingly, Inland Revenue is cracking down on this .

“…by requiring many contracting firms to withhold tax from their labour repayments and pay that directly to Inland Revenue, where Inland Revenue identifies growers and other payments not correctly deducting or accounting for their tax. We’re also following these up with interviews.”

It’s also pursuing the contracting firms through audits and prosecutions, and apparently there are nearly 100 such audits active at the moment.

“High use of cash and migrant labour”

The press release concludes by noting that there’s a high use of cash and migrant labour. The horticultural industry is therefore a sector open to abusing workers so Inland Revenue will work with other New Zealand government agencies to address these issues.

Cash payments are always a target for Inland Revenue, but it’s interesting to see a sector singled out and certain types of firms identified as the risky part of the equation. The initiative is another sign of how Inland Revenue is using its increased funding and the ongoing issues it encounters in the sector. It will be interesting to see the results of the prosecutions.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

The lastest Rich List re-ignites wealth tax debate.

Late last year, the Finance Minister, Nicola Willis, suggested that the charities area was ripe for some tax reform. She expressed concern that the exemption for charities business profits could be being exploited. The sector has nearly 8000 entities, which apparently report a total of over $36 billion of gross income with potential taxable profits of $1.56 billion annually. Now, in theory, those profits would represent over $400 million of tax revenue if the exemption was removed in full. Given the Government’s current straitened circumstances $400 million is not an insignificant sum.

Inland Revenue subsequently issued a consultation document on the topic in late February which closed on 31st March. The consultation sparked quite a bit of concern throughout the charity sector although the main concerns under consultation appeared to be about large organisations making use of the business exemption and donor-controlled charities.

In April, following the end of the consultation period, it became clear from the Finance Minister that in fact, contrary to what was anticipated, there wouldn’t be any budget reforms for the charity sector contained in this year’s budget.

Matt Nippert, the redoubtable business investigations reporter for the New Zealand Herald, filed various Official Information Act requests to get more background on what happened in that consultation process, and an understanding of why the Government might have changed its mind, and he published a story in the New Zealand Herald last Monday.

Sector push back

In essence, the sector unsurprisingly pushed back very significantly with 901 submissions received, which is actually a significant number given there are about 8,000 charities in the sector. 86% of those responding were opposed to removing the charity business tax exemption.

Incidentally, as part of the process, Inland Revenue met with 14 large charities and sector groups as part of the consultation. This is actually quite standard when Inland Revenue is doing consultation. It does go out to interested sector groups and discusses proposals. There can be arguments as to whether or not this borders on lobbying, but it’s a part of the Generic Tax Policy Process and it gives Inland Revenue a boots on the ground insight on its proposals. What was actually discussed at those meetings won’t be released under the Official Information Act request, although the formal submissions on the consultation will be published in due course.

There were complaints it was a very short period of consultation. And obviously there were big concerns about the potential implications for many charities if the exemption was removed in terms of compliance costs and funding. Quite a few people responded that it might be better if Inland Revenue and the charity service focused on the bad actors within the system, rather than taking a blanket approach.

It also became clear following consultation that the possible tax gains from reforms were nowhere near the suggested amount, in fact, were more likely to be around $50 million per annum. As Matt Nippert explained the sector is quite fragmented, with a huge pool of tiny operators and then a very small pool of huge operators such as Sanitarium. Inland Revenue’s proposals would probably have left at least 85% of the organisations untouched.

“A bit scattershot”

Speaking to Matt Nippert KPMG principal Darshana Elwela remarked the Inland Revenue proposals were “a bit scattershot and there was in our view a bit of incoherence about what the potential problem was and how it was being proposed to be fixed.”

I think with Darshana’s comment, sometimes we’ve seen Inland Revenue propose something and it’s not exactly clear the extent of the issue to be resolved, the only references involving subjective word like “significant” without an explanation as to how much represents “significant “.

The other interesting feedback I saw reported by Matt Nippert is that in relation to the potential issue around donor-controlled charities – which I think is a concern – only 46% of respondents opposed a mandatory minimum for distributions for such entities.

I thought that was very surprising because the issue around donor-controlled entities is whether in fact they’re making donations or using the funds appropriately for charitable purposes. Darshana Elwela of KPMG also touched on this, commenting

“Transactions between the donor and the charity could result in the more favourable tax profile for the tax paying side. There were some genuine concerns some of that might be happening.

“The question we had does raise a wider question as to whether these entities should be charities to begin with.”

“A lot of complexity”

Willis denied there has been an about-face, commenting “There is a lot of complexity involved with designing new rules so as to ensure they have integrity and are simple to understand. Therefore, the Government has asked Inland Revenue to do more work on the options.”

The end result is Inland Revenue has gone away to think again because, as the Finance Minister’s office noted, “the Government is focused on fairness and integrity of the tax system. It is important that any changes be the right one, so it’s going to take the time needed to get it right.” In short, watch this space.

Rich List re-ignites the wealth tax debate

Moving on, this week saw the publication of the National Business Review’s annual rich list for 2025, and it showed that for the first time ever, the country’s wealthiest people are collectively worth more than $100 billion. That’s up nearly $7 billion from last year and the criteria now to be included in the rich list is over $100 million of estimated net worth.

It should be said, establishing the wealth of our richest is often educated guesswork, to be frank. That’s because unlisted companies often form the core of the wealth of many of the wealthiest families and persons on the rich list.

By contrast, overall, in 2024 the net worth of all households declined by over $4 billion. Infometrics’ chief forecaster Gareth Kiernan said that average household wealth had fallen since the end of 2021, but that was unsurprising because housing makes up more than half of household assets, and house prices remain below their 2021 peak.

That is the knock-on effect for the average person in New Zealand. And just this week councils have been releasing their rating valuations, and they are showing declines too.

By contrast, the super wealthy have very much more diversified portfolios, so the core of their wealth is actually held in businesses and not so concentrated in property. There are some property magnates in that group, of course, but you’ll find highly diversified wealth, and wealth generates wealth and Thomas Piketty’s famous r > g formula from his monumental Capital in the Twenty-First Century.

Time for a wealth tax?

The publication of the Rich List prompted Chlöe Swarbrick of the Green Party to set out the Green Party’s Budget proposal for a fairly chunky wealth tax of 2.5%. In theory it all sounds very attractive, but as we’ve just discussed, the valuation issues are far trickier than people anticipate in this area, particularly when you have large numbers of unlisted companies in the mix.

And then there is the real risk of capital flight. And as I’ve said before, in our case, I think it’s significantly bigger than people might imagine because moving to Australia is very common and Australia has the temporary residence exemption, which is highly tax favourable. It would mean that, for most Kiwis moving to Australia, their non-Australian assets would not be subject to Australian capital gains taxes unless they became Australian citizens.

Tax is politics and why New Zealand is unique

The key thing to be kept in mind in the debate around wealth tax, and with all debates around taxes, is that what is taxed is entirely a political decision. So, the wealth tax yay or nay debate is going to be resolved at the ballot box ultimately. What is interesting at the moment is that other accountants are reporting they are getting queries from clients concerned about what they could do about a wealth tax if it happened. What are the options around that? This is interesting because it may reveal a shift in thinking that something might be happening. The debate seems to have heated up with growing concerns about inequality and record numbers of people applying for benefits.

In terms of wealth taxes, the classic wealth tax that’s being described by the Greens is basically an annual charge on all wealth. It’s well known that New Zealand does not have a general capital gains tax, but what really makes us unique relative to other countries in the Organisation for Economic Cooperation and Development (OECD) is we don’t have an estate tax, we don’t have a gift tax, we don’t have land tax (other than rates), and we don’t have stamp duties (which, although they’re transfer taxes, are effectively also a tax on wealth, being the value of the land at the time of transfer).

We’ve none of these taxes. But they used to be quite a significant part of the tax base. Back in 1949 such taxes represented 5% of all government revenue at the time, which would be $6 billion now, a very significant sum.

The absence of these taxes and any real form of capital taxation is putting pressure on the tax system to respond to growing pressures on funding. The calls are coming in for variations on some form of capital taxation, whether it’s a capital gains tax, a wealth tax or potentially an estate tax.

We are, as I said, an outlier with the absence of capital taxes, but ultimately tax is political. The arguments will be decided by the electorate and politicians taking a stance and running on tax reform in the future.

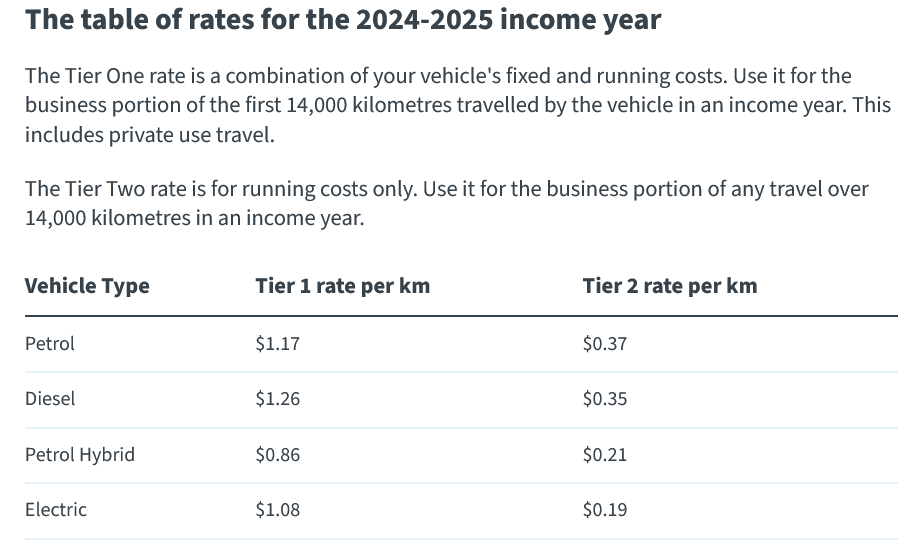

New Inland Revenue kilometre rates come with a change in approach

What makes these rates different this year is that, as Inland Revenue explained, traditionally the Commissioner has set a single Tier One rate. However, due to the significant difference in vehicle running costs between the different vehicle types (Petrol, Diesel, Petrol Hybrid and Electric), a Tier One rate has been set for each vehicle category – being petrol, diesel, petrol/ hybrid and electric – to ensure the rates accurately reflect reasonable expenditure related to the business use of that particular vehicle

The new approach may mean that you have to make adjustments to your mileage reimbursement processes going forward.

Inland Revenue performance targets

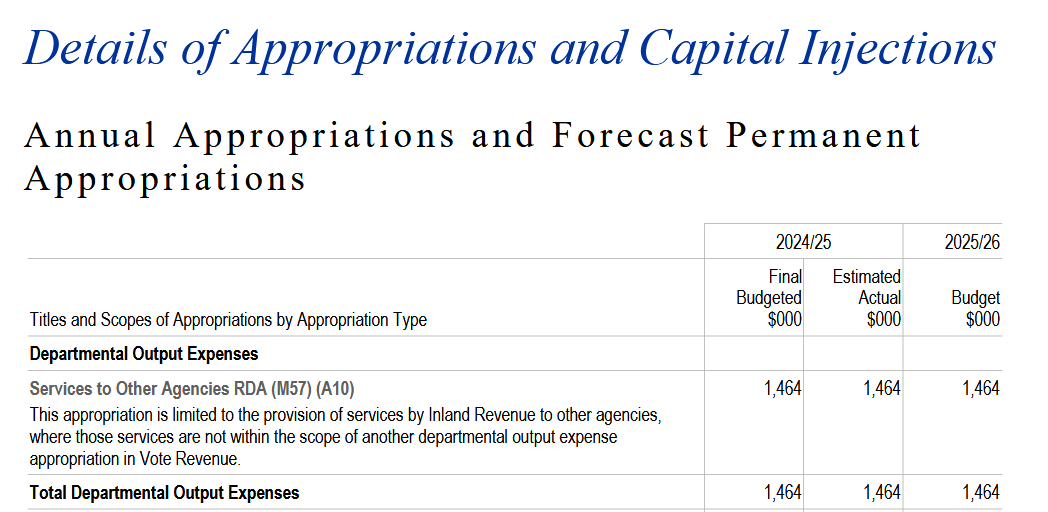

Finally this week, as part of the Budget, every government produces detailed breakdowns of spending for each ‘Appropriation’ or ‘Vote’ to be approved by Parliament as part of the Budget process. Reviewing the Vote Revenue Appropriation gives some useful guidance and detail about what specifically Inland Revenue is expected to do.

These appropriations are incredibly detailed. The Vote Revenue appropriation revenue runs to 40 odd pages setting out the various items of expenditure and what is to be spent or appropriated.

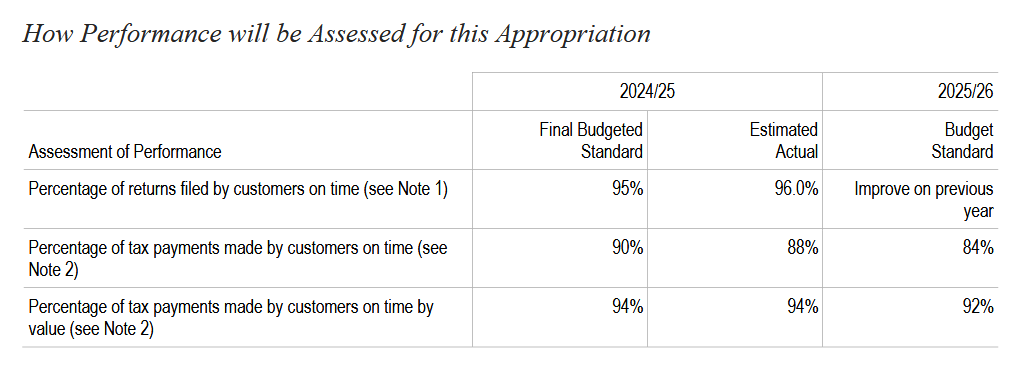

What’s also of interest are the performance criteria for each sub-part of the overall appropriation including a summary of what is intended to be achieved by the appropriation, and how performance will be assessed. Now, not every appropriation line item has an investment. Some get an exemption under the Public Finance Act.

Tax payments & debt collection

As can be seen the performance expectation for tax payments made on time for the current year to June 2025 is 90% but for next year it’s expected to be 84% maybe reflecting harder conditions in the economy are expected.

We’ve recently discussed the issue of student loans and overseas based student loan borrowers. Inland Revenue has a new expectation that 31% to 35% of all such borrowers will be making payments or meeting their obligations in the 2025-26 year. The percentage of collectable debt that’s going to be over two years old is estimated for the current year to stand at 35.3% but is expected to be 40% or less going forward.

In other interesting snippets the percentage of litigation judgements found in favour of the Commissioner is expected to be 75%. The actual is running at 90%, and as we regularly report, there is a whole series of cases coming through where criminal prosecutions have been successfully taken by Inland Revenue.

How long to answer a call?

Now, how long does it take Inland Revenue to answer a telephone call? Well, the budgeted standard they try to meet is currently 4 minutes, 30 seconds or less. At present they’re managing 3 minutes 8 seconds, which is very good. And next year the standard is again set at 4 minutes 30 seconds.

So, if you call Inland Revenue and you’re waiting for more than 4 ½ minutes, it has not met its expectations. In fairness, just remember, this is currently the busiest time of year for Inland Revenue as they process the March 2025 tax returns for over two million people. The chances are if you do find yourself waiting for more than 4 ½ minutes, you won’t be the only one.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Budget Day lockup is a mad frenzy of activity as you basically have three and half hours to sift through a massive information dump, determine the key points and write something for release at 2PM when the Budget is officially released.

Surprisingly, in the midst of all the information provided, you don’t get copies of any accompanying legislation, bill commentary and Regulatory Impact Statements that will be also released at 2PM. Therefore, those of us who are in the Budget Lockup are a still little bit blind as to the full details of the Budget initiatives. Because of this I increasingly view the Budget Lockup as an interesting experience, a good opportunity to interact with Treasury officials, because you can actually ask for specific information and an opportunity to perhaps quiz the Minister of Finance on some points.

Budget Day – just a government showpiece?

On the other hand, it is increasingly clear from the run up to Budget Day that the budget itself is very much a set piece for the government of the day to boost specific Budget initiatives and narratives. Any detailed analysis on the day is swamped by all the good or bad news about the state of the economy or who’s getting extra or reduced funding. It’s not really until the week following the Budget that you start to get some detailed analysis of what is in the budget and the potential implications.

Investment Boost – a real boost to productivity or just meh?

On Budget Day the Investment Boost proposal was well received, but as people looked into the detail some concerns have emerged. What the measure does is essentially accelerate the depreciation which would have been claimed on these assets. This is done by way of an immediate 20% deduction with the remaining 80% of the asset expenditure depreciated as normal. My initial reaction was to recall the First Year Allowances I used to deal with when I was working in the UK and which operated in a similar fashion.

The twist is last year the Government removed depreciation on commercial buildings, including factories, to pay for its tax cuts. But this year commercial buildings are included in those groups of assets that are able to qualify for the Investment Boost. This about-face has prompted Andrea Black the former independent advisor to the last Tax Working Group, and a previous a guest on the podcast to write an op-ed in The Post about the Investment Boost initiative. In summary, she argues if we are trying to boost productivity, then Investment Boost is a step in the right direction but is not the productivity game changer that is being promoted.

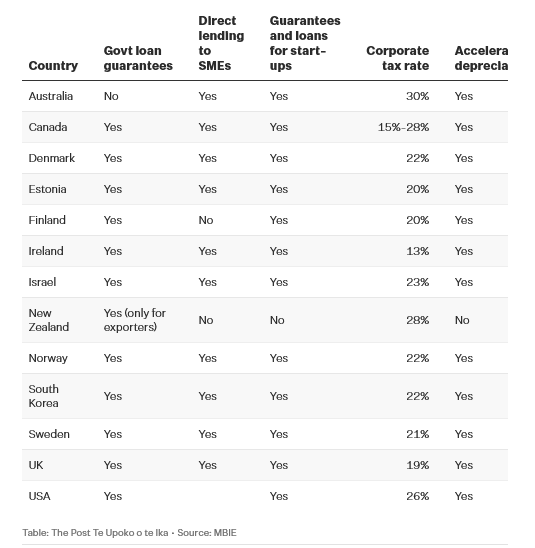

New Zealand is an outlier, again

Andrea is critical that the Investment Boost initiative does include commercial property and notes that our labour productivity is poor and that direct assistance in terms of accelerated depreciation – which she strongly supports – doesn’t really exist for many New Zealand manufacturers. She includes a very telling graph put together based on information obtained under the Official Information Act from the Ministry of Business, Innovation and Employment about how other countries subsidise business, including through tax breaks and government loan guarantees.

As can be seen we only grant government loan guarantees for exporters, in contrast to most other countries in the OECD. Similarly, we and Finland are the only countries which do not provide direct government lending support to small and medium enterprises. The United States, for example, has the Small Business Administration, and this initiative was something we looked at when I was on the Small Business Council back in 2018-2019. I thought then, and still do, that the lack of government financial support for our SME sector is something we really need to address.

A step in the right direction but…

As Andrea notes until Investment Boost New Zealand had no accelerated depreciation which meant we were very much out of line with other jurisdictions. So the Investment Boost initiative is a step in the right direction even if it perhaps could have gone further. I have little doubt Investment Boost will have an effect on investment, like Andrea whether it will have the effect the government is hoping for in boosting productivity, I’m not so sure.

I’m particularly concerned wearing my devious tax planner cap that the opportunity now exists for some clever financiers to put some property related deals together to accelerate the building of some commercial properties to obtain the 20% upfront deduction. I saw something similar happen in the UK with the former Business Enterprise Scheme, which was designed to boost startups but quickly saw property backed schemes emerge to claim the generous deductions. Anyway we shall see how this plays out over time.

Investment Boost, Fringe Benefit Tax and skewing the composition of our vehicle fleet

Incidental to this issue Newsroom published an interesting article talking about the impact of proposed changes to the Fringe Benefit Tax (FBT) regime treatment of motor vehicles. The article suggested that the Investment Boost proposal, which applies to vehicles as well, might mean that we might see a shift away from the use of double cab utes.

There’s a number of reasons that they are now so prevalent on our streets and a growing component of the vehicle fleet. One reason is that there was a perception that double cab utes qualify for the work-related vehicles exemption from FBT. The other was that manufacturers were promoting these vehicles with some highly favourable deals.

The increase in the number of double cab utes prompted Angela Hodges, from NZ Tax Desk to comment the combination of those two factors and particularly the perceived exemption has

“skewed the composition of New Zealand’s vehicle fleet over time, with tax settings influencing business-purchasing decisions in ways that probably weren’t intended”.

The Newsroom article suggests that the coming FBT changes together with the Investment Boost initiative may encourage a switch away from double cab utes to alternative vehicles. It will be interesting to see how this develops.

Inland Revenue’s “significant funding boost”– what can we expect?

Moving on and in as big a surprise as the sun will rise tomorrow, Inland Revenue was given additional permanent funding of $35 million per year to invest in tax compliance and collection activities. As the Commissioner of Inland Revenue, Peter Mersi, pointed out, “This is a significant funding boost and is recognition of what we do and the excellent results we’ve had so far this year.”

These results include for the year to 31st March 2025 assessing additional tax of $880 million from audit activity and improved debt collection activities, with just under $3 billion collected in the year to date compared with $2.7 billion for the previous year. There’s also been a doubling in the number of prosecutions and a big increase in the collection of overseas student loan repayments. In my view this is a scheme that really needs a lot of re-thinking about how it’s managed.

In addition to that $35 million Inland Revenue also got an additional $29 million per year last year for compliance and debt collection. Furthermore, the Government has also agreed to continue $26.5 million of funding set to end this year. All up Inland Revenue is getting close to $90 million of funding for investigation and debt collection activities.

This should have a significant impact given the rate of return of between seven and eight dollars for each dollar invested, which has been achieved in the past. The total return from increased compliance and collection activities is therefore potentially as high as $700 million per year.

A warning and a reminder

Against this backdrop people should keep two things in mind. Firstly, as I’ve said on many previous occasions, Inland Revenue has vast resources. It receives data from many sources, and it is increasingly efficient at absorbing, analysing and acting on that data. The basic proposition you should operate on is; if you have put anything in writing anywhere, Inland Revenue will have access to that information at some point. In particular, Inland Revenue has become increasingly efficient in tracking property transactions.

The other point is in relation to tax debt. If you are behind, take action and front up to Inland Revenue. It’s much better doing so than hoping you won’t be on their radar. Being proactive will get a better result for you in the long term.

The Digital Services Tax is dead – now what?

Now at last, in the run up to the budget, the Minister of Revenue, Simon Watts, announced that the Government had decided to discharge the Digital Services Tax bill from the legislative programme. This had been introduced in 2023 by the previous Labour Government. It was really intended as a backstop to OECD’s Two-Pillar international tax initiative.

According to Mr. Watts, “we’ve been monitoring international developments and decided not to progress the Digital Services Tax bill at this time. A global solution has always been our preferred option and we have been encouraged by the recent commitment of countries to the OECD work in this area.”

The consequence of the decision is that the forecast revenues from the introduction of the Digital Services Tax will no longer be included in the Crown accounts. This represents a $476 million reduction in tax revenue over a four-year period. The question therefore arises as to what replaces this lost revenue.

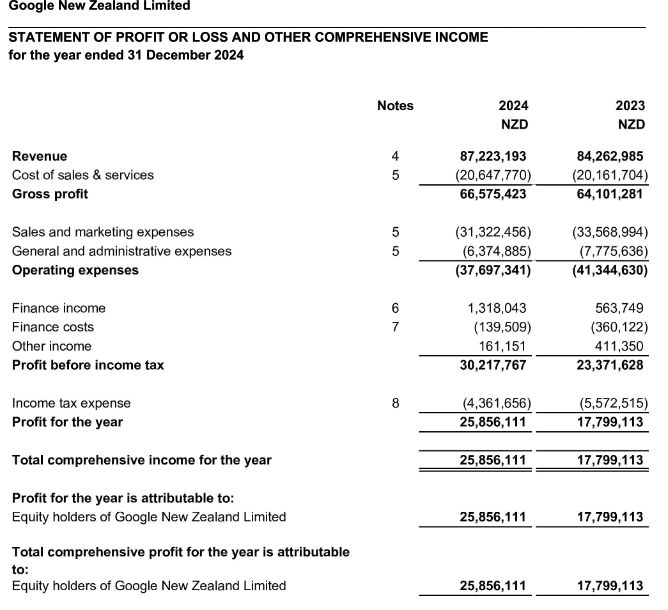

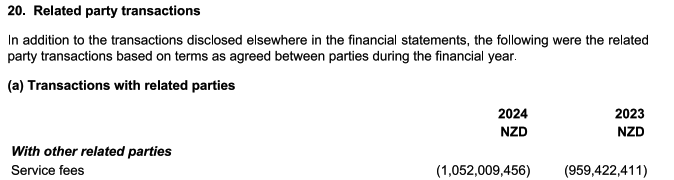

Google New Zealand’s billion-dollar service fees are not unique

In the same week as the Budget and the announcement about the Digital Services Tax, Google New Zealand released its results for the year ended 31 December 2024.

During the year Google NZ paid $1.05 billion in service fees to related parties, almost $100 million more than in 2023.

A week or so later, Facebook New Zealand announced its December 2024 results and the amount of fees it paid to associated entities was over $150 million, roughly the same as for 2023.

Jonathan Milne of Newsroom wrote an interesting article looking at the question of the payments that were being made by all the tech companies. Taking into consideration the fees paid by Apple, Amazon, Microsoft together with Google and Facebook he estimated the annual amount of service fees being paid to associated entities was close to $4 billion. Assuming all are deductible then at the corporate income tax rate of 28% that represents over $1.1 billion of lost tax revenue.

What about the OECD Two-Pillar deal?

Now, of course, it’s more complicated than this simple calculation. But the withdrawal of the Digital Services Tax should be seen alongside what can only be described as regulatory capture in Washington by the tech giants. That in turn has led to these trade threats made by President Trump against digital services taxes and other attempts to tax the tech giants. This all means that the international Pillar One and Pillar Two proposals in which Minister of Revenue Simon Watts places great faith are practically dead in the water.

The Government therefore has a problem. Having accepted it’s not going get $476 million of revenue from the Digital Services Tax, how does it replace that lost revenue. What about the potential $4 billion of service fees going in affiliate fees, should these be subject to some questions under the transfer pricing rules? What is going to happen in that space? Will some of the roughly additional funding of $90 million discussed earlier be deployed in boosting Inland Revenue’s reviews of the transfer pricing practices of the tech companies? We don’t know, but this is an area other jurisdictions around the world are also grappling with.

In Australia at the moment some of these transfer pricing issues are involved in the PepsiCo case. The case revolves around an embedded royalties issue, basically: do some of the payments made for concentrate include some form of royalty which should be subject to non-resident withholding tax? Typically, non-resident withholding taxes for royalties are between 5% and 10% of the payment. Increased focus here may be a means of recovering some of the lost revenue from the digital services tax.

This issue of the treatment of service fees is in my view probably one of the most interesting challenges in the international tax space right now. All around the world there’s great interest in addressing this issue of transfer pricing. We’re therefore watching to see how Inland Revenue moves and, as always, we will report on developments as and when they arise.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.