The investment boost tax incentive announced as a centre piece of “The Growth Budget” is one of the bolder tax initiatives in recent years.

From today businesses of any size can fully deduct 20% of the value of new assets (or secondhand assets purchased from overseas) in the year of purchase. For example, if a company invested $200,000 in new plant, $40,000 would be immediately deductible. The remaining $160,000 would be depreciated as normal. There is no cap on this allowance which is also welcome (and a little surprising).

Investment boost also applies to new commercial and industrial buildings. Although residential buildings and most buildings used to provide accommodation will not be eligible there will be explicit exceptions for hotels, hospitals and rest homes. Any construction project underway before 22nd May 2025 may also qualify if the asset is used or available for use for the first time after that date.

The allowance may also be available for improvements to depreciable property such as significant strengthening of an industrial building. This should be welcome news for owners facing earthquake strengthening costs.

Treasury and Inland Revenue estimate this initiative will increase GDP by 1%, wages by 1.5% and the country’s capital stock by 1.6% over the next 20 years. Half of those gains are expected in the next five years as it sparks an investment boom.

On the other hand, investment boost doesn’t come cheap with an expected cost of $1.7 billion per year over the next four years to 30 June 2029.

I speculated last week that the Budget might contain changes around accelerated depreciation, which I considered would be a better and more affordable option than a cut in the corporate tax rate.

Which is exactly what the Finance Minister Nicola Willis acknowledged when announcing the incentive it; “delivers more bang for buck than a company tax cut because it only applies to new investments, not those made in the past.”

I thought we might have seen an increase in the $1,000 full write-off for low-value assets. Although that didn’t happen this is a welcome move particularly as it is available for any businesses of any size without cap.

On the other hand it is somewhat ironic that having removed depreciation on commercial and industrial buildings last year, the Government has now enabled new commercial and industrial buildings to qualify for the 20% deduction. Allowing this is perhaps a belated recognition that removing depreciation in the first place would hinder investment?

The Ghost of Bill English?

I also described last week the many and quite significant changes to KiwiSaver Bill English made during his time as Finance Minister. The reduction in the Government’s contribution to a maximum of $260.72 annually and removal in full for those earning over $180,000 annually is therefore straight out of English’s playbook. (In fact during the question & answer session the Finance Minister commented that officials had advised removing the contribution completely).

This is to be compensated by increased employer and employee contributions first to 3.5% from 1 April 2026 and then to 4% from 1 April 2028. How that plays out in boosting saving will be interesting to see. On the other hand, the proposal to extend KiwiSaver eligibility to 16-17 year olds is a good move.

Not much love for low-income families

Earlier this year a Treasury paper noted 30% of all single-parent families faced an effective marginal tax rate of 50% or more. The Budget contains changes to the Working for Families which (very) partially addresses this with a lift in the family income threshold from $42,700 to $44,900. However, this has been paid for by means testing the first year of the Best Start tax credit and lifting the Working for Families abatement rate from 27% to 27.5%. (Another very Bill English-type move).

To put that in context if the Working for Families threshold had been adjusted for inflation since it was last set in June 2018, it would now be $54,650 or nearly $10,000 more.

The low threshold and high abatement rate mean many families find themselves in debt with Inland Revenue. To address this the Government is releasing a discussion document with proposals to make Working for Families payments more accurate. This is helpful but nowhere near as much as a meaningful increase in the threshold which, remember, is still below what a person on minimum wage would earn annually.

(Also worth noting that an additional $154 million over four years was found to increase the abatement income threshold for SuperGold cardholders from $31,510 to $45,000. That’s welcome but it’s interesting to compare this with the assistance given to younger families and workers whose taxes pay for NZ Superannuation).

More money for Inland Revenue

As expected, Inland Revenue will get another $35 million a year for compliance and debt collection. This is expected to return four dollars for every dollar spent in the year to 30 June 2026 and rising to eight dollars per dollar spent in the year to 30 June 2027. The expectation is that Inland Revenue is on track to collect more than $4 billion in overdue debt by 30 June.

Elsewhere, we got no further details on the proposed tax changes to thin capitalisation and employee share schemes announced earlier this week. These are expected to cost $75 million over four years, the majority of which relates to the thin capitalisation proposals.

Overall, a growth budget perhaps but one that relies on several sleight of hand moves, and does next to nothing to address the problem of low-income families facing high effective marginal tax rates.

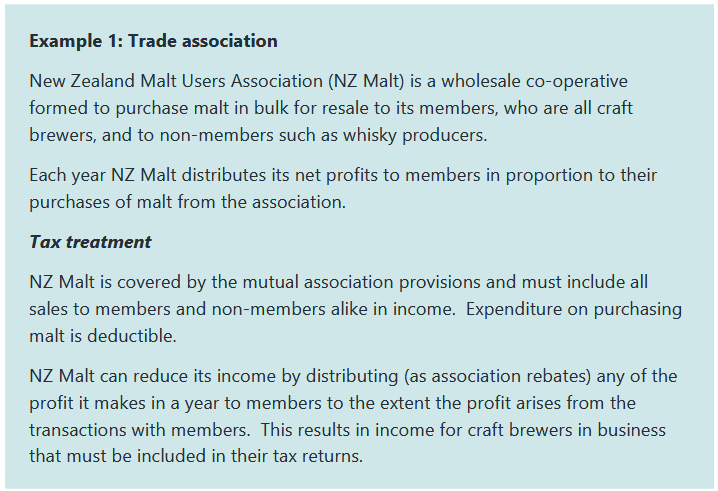

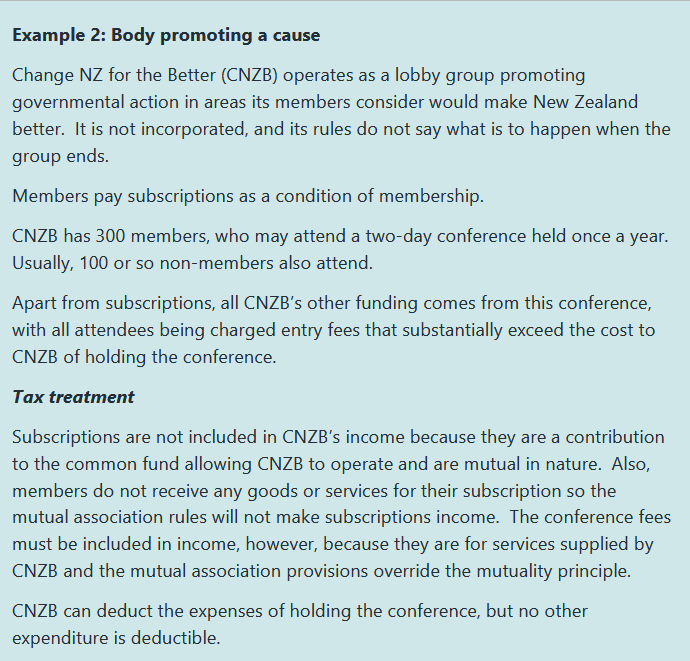

Earlier this year, Inland Revenue ran a consultation on the not-for-profit sector. In the course of that consultation it raised the treatment of the taxation of mutual associations, including clubs and societies. Inland Revenue indicated that mutual transactions between clubs and members, such as subscriptions, which were previously thought to be exempt from tax, were in fact taxable. It transpired Inland Revenue had actually been sitting on a draft operational statement on this matter for some time.

Inland Revenue has now released a draft operational statement (“OS”) on the taxation of mutual transactions of associations, clubs and societies.

This OS takes into account submissions Inland Revenue received on the not for profits consultation. One of the issues this draft OS considers is whether the principle of mutuality applies. As the draft OS notes, under the common law principle of mutuality, an association of people such as a club or society, cannot derive taxable income from transactions within the circle of membership of the association. Mutual transactions do not generate profits for the association, because the amounts received by the association come from members transacting with themselves.

This primarily refers to subscriptions, but as the draft OS also notes, the principle does not apply where legislation provides otherwise. And what Inland Revenue has highlighted in this consultation is that it wants to give greater clarification about the scope of these potentially mutual transactions.

The basic position is supplying stock or services to members is taxable. That’s not a new position, but as the draft OS comments

“…this has not been communicated clearly or consistently, and Inland Revenue is aware affected customers take different approaches. We are hoping to increase awareness of the correct treatment and achieve certainty and consistency by finalising a statement on this aspect following consultation.”

A change of tack

The key point the draft OS proposes is that member subscriptions may be subject to tax, which does represent a change in practice. Therefore, “an object of this consultation is to test whether the reasoning for that conclusion is sound.”

To be frank, this has caused a bit of a stir amongst the potentially affected clubs and societies. There are exemptions given for specific charities and sports clubs, but a large number of organisations would previously have thought and filed tax returns on the basis that transactions involving member subscriptions were exempt. This does work both ways. If the subscription is treated as exempt, then costs relating to subscriptions are not deductible.

The paper contains 7 examples setting out various scenarios and how transactions might be treated. As noted, Inland Revenue’s position is that in some cases membership fees and levies are not mutual in nature but represent income and are taxable. A key point in this approach is if the associations constitution allows distributions to be made to members. If distributions are prohibited, then membership fees and levies are income. The following examples taken from the draft OS illustrate the issues under consideration.

One for legislative reform?

The sector has been taken a bit by surprise by this consultation. In my view it represents such a change of interpretation it should be legislated if Inland Revenue wants to achieve that clarity. To be fair, Inland Revenue is saying that any changes made after consultation is finalised would be prospective and it would not generally seek to reopen prior years. I recommend all potentially affected groups to submit on this draft OS, consultation on which is open until 25th of June.

Inland Revenue gets tough on student loan debts

Moving on, Inland Revenue has been regularly providing updates on the progress of its debt collection and general enforcement in the wake of the additional funding of $116 million over 4 years it got in last year’s Budget for this purpose. Last week, we discussed the extra $153 million Inland Revenue has recovered in the year to date from the property sector alone.

Its latest update this week is about its progress on recovering student loan debt and included the news that “One person was arrested at the border last month and they have since paid off their debt.” According to Inland Revenue at the end of April, there were 113,733 people with student loans believed to be based overseas. More than 70% of those people were in default of their loans and in total they owe $2.3 billion. This includes 150 overseas based borrowers with a combined default debt of $15 million. It is therefore understandable why Inland Revenue is a tougher line on student loan debt.

Information sharing with New Zealand Customs…and airlines

Inland Revenue gets notified by New Zealand Customs about any border crossings into New Zealand by overseas based borrowers. According to the RNZ report apparently airlines are also providing similar information to Inland Revenue. This is an interesting, and previously unknown, detail.

Once notified Inland Revenue will then apply to the District Court and the police can make an actual arrest, which, as noted, happened last month. Since 1st January 2024, 89 people have been advised they could be arrested at the border. This has prompted 11 of them to take action, either by making acceptable repayments or entering into repayment plans and applying for hardship. So far during the current financial year to 30th June, this programme has collected $207 million in repayments from overseas borrowers. This is up 43% on the same period in the previous year. So yes, it’s making progress.

Progress, but…

On the other hand, some of the reported numbers are quite concerning to me, and I consider also highlight why student loan debt has become such a problem. As noted above those 113,733 overseas based borrowers owe over $2.3 billion, but more than a billion dollars represents penalties and interest. What happens is that as the interest and penalties pile up, many debtors get to a point where they feel it can’t be repaid, and they simply freeze hoping the issue will somehow go away. This phenomenon is well understood by Inland Revenue because it happens with other tax debt.

Therefore, the question arises about the efficacy of the current penalty and interest rate regime. Interest and penalties accumulate swamping repayments, so little progress in repaying debt is made even where repayments are being made. The overall amount of debt on Inland Revenue’s books then just blows out.

Debt more than 15 years old? How did that happen?

One particular point really concerns me about Inland Revenue’s latest update. Apparently for over 24,000 of the overseas based borrowers, the debt is more than 15 years old. In many cases, it’s highly likely that people in that category are not going to return to the country, so the threats of arrest at the border are probably not going to be effective.

But then the question also arises is it really very realistic to expect people to repay debt which has been allowed to accumulate for 15 years? And a really big question here is what was Inland Revenue doing during that time?

It’s all well and good to say Inland Revenue is clamping down now. But it seems to me to be against natural justice that it can target debtors where the debt has been allowed to accumulate, and insufficient action was taken early enough to control the debt and prompt earlier repayment.

Inland Revenue, as we repeatedly mention on this podcast, has enormous information sharing and gathering powers. The question really arises as to whether sufficient resources were made available in the first instance to keep control of the student loan debt. And now we’ve reached a situation where, to borrow an old saying, “You owe the bank $100,000, it’s your problem. You owe the bank $1 million; it becomes their problem.” It seems to me that’s where we’ve reached with overdue student loan debt.

Are the rules fit for purpose?

It should also be noted that looking into the legislation applying to student loan debt it appears it’s quite difficult for Inland Revenue to write off debt and interest as part of reaching a settlement. The rules are very prescriptive in such instances, apparently deliberately so.

As a consequence, I wonder if this holds people back about making attempts to settle outstanding debt. There’s also the question of debt over 15 years old and what records are available to prove outstanding amounts. Inland Revenue has the luxury of having the upper hand here where the age of the debt means debtors may not be able to provide any contradictory evidence about lost payments or incorrect adjustments. Although it’s good to see Inland Revenue is making progress on the overall collection, I don’t think that means that it should avoid scrutiny for how the debt book has been handled in the past.

Pre-Budget teasers

The Budget is next Thursday and ahead of it, there’s always plenty of speculation as to its contents. Things have got spicier because of the pay equity issue: depending on who you want to believe this has either “saved the Budget” or just happens to be a coincidence.

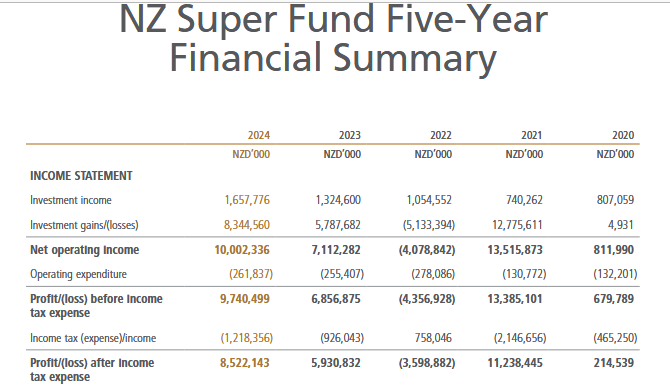

As usual there’s been a steady stream of announcements from the Government about particular items which will be in the Budget. A very interesting and quite significant one relates to future drawdowns from the New Zealand Superannuation Fund (“the NZSF”), established by the late Sir Michael Cullen in 2002.

The country’s biggest taxpayer

Ahead of the Budget the Finance Minister announced that the Government will start drawing down on the NZSF with effect from 2028, five years ahead of first forecast. It is just worth keeping in mind that since inception the NZSF has been paying tax. In fact, it is the only sovereign wealth fund in the world which is taxed. For the year ended 30th June 2024, its tax bill was $1.2 billion. It’s usually the largest single taxpayer in the country, meaning it’s already contributing to the funding of New Zealand Superannuation.

Changes ahead for KiwiSaver? National’s record would indicate so

Elsewhere there’s been speculation about what’s going to happen with KiwiSaver. The Finance Minister has alluded to some changes leading to speculation that the Government’s contribution could be increased for lower income earners or might be means tested for higher income earners.

It’s worth noting that previous National-led governments have a pattern of playing around with KiwiSaver. The maximum Government contribution each year used to be $1,043 a year until that was halved by Sir Bill English with effect from 1 July 2012. He also scrapped in 2009 a $40 annual fee subsidy. English also removed the $1,000 kick start payment from 21st May 2015.

The biggest KiwiSaver change English made was introducing employer superannuation contribution tax (“ESCT”) on employer contributions to KiwiSaver funds from 1 April 2012. To illustrate how important that change was, the amount of ESCT collected annually was $1.982 billion for the year to 30th June 2024 or about 1.7% of the Government’s total tax take for the year. Consequently, ESCT is too big for it to be changed in any way. But I do think we might see some tweaking of the Government’s KiwiSaver contribution settings.

A potential corporate tax cut or accelerated depreciation?

There’s also been talk about a potential corporate income tax cut, but I’m with Robin Oliver who said that if they’re going to do it, they’d have to go big. In other words, from probably 28% down to 18%, and that’s simply not going to happen because it would be unaffordable. On the other hand I do think we might see some more targeted investments around increased or accelerated depreciation allowances, which I, and the business sector, would certainly welcome.

The Green alternative

The Greens took the opportunity also to publish their alternative budget on Wednesday. Looking past the predictable scoffing from opponents a few initiatives stand out. They’re proposing a higher top rate of 45%, which is the same top rate as Australia and the UK just for reference, it should kick in at income over $180,000 with the 39% rate starting at $120,000. The trade-off is that every person will get $10,000 a year tax free exemption. The 45% top rate is comparable to other jurisdictions, notably Australia and the UK. I’m not so sure about the thresholds though as the level they kick in seem on the low side.

Think 45% is high? Try Austria

As an aside and about high tax rates I was very surprised to find out this week that Austrian Government, which is a centre right coalition, has kept in place for the next four years a top income tax rate of 55% applicable to income above €1,000,000. Food for thought therefore claiming the Greens’ suggestions are excessive. (As a sidebar and follow on from my comments last week about mandatory indexation of thresholds, Austria is actually reducing part of the inflation adjustment for the tax rate thresholds. In Austria income tax thresholds are automatically adjusted annually by 2/3 of the inflation rate unless the government legislates otherwise).

A Capital Acquisitions Tax?

The Greens are also proposing a 2.5% wealth tax on net assets over an individual’s threshold of $2,000,000 with a 1.5% tax applying to net assets held in “private trusts,” The press has talked about the Greens introducing an inheritance tax, but that’s not actually correct. In fact, and I think this is probably the most interesting revenue raising idea from the Greens, what they are actually proposing is a variation of the Irish Capital Acquisitions Tax. Why this is interesting is Capital Acquisitions Tax is a donee based tax. In other words, it is the person who receives the gift who is taxed. By contrast a typical inheritance tax or estate duty work on the principle of any taxes being paid by the donor (the person, or their estate making the gift.

Under the Greens proposal a 33% wealth transfer tax will apply to significant gifts and inheritances received, over an accumulated lifetime threshold of $1,000,000. The 33% rate is the same as the Irish Capital Acquisitions Tax. This is an interesting proposal and it’s the first time I’ve seen a New Zealand party raise it as an option.

Elsewhere the Greens want to increase the corporate tax rate to 33% and also restore a 10-year bright-line test, as well as reintroducing interest deductibility restrictions. All of the tax increases are to pay for a huge social. Investment programme, including free dental care. It would also include a major increase in the threshold for Working for Families from the current $42,700, which has not changed since June 2018, to $61,000. The current 27% abatement rate would also be reduced.

Wealth taxes and capital flight

On wealth taxes, a reason why tax practitioners including myself are sceptical about the revenue projections for a wealth tax are the issues of valuation and capital flight. Valuation issues are always a key objection to wealth taxes, but I think the question of capital flight is one that we perhaps have to think hard about when considering the impact of a wealth tax. That’s because I think we are very vulnerable to capital flight to Australia.

Australia has always been a huge land of opportunity for many Kiwis but it’s also very attractive for those Kiwis moving there who qualify for the Australian Temporary Resident exemption. This exempts non Australian sourced income and capital gains from Australian tax. It’s similar to our Transitional Resident exemption, but unlike that which is generally only available for 48 months, the Australian Temporary Resident exemption, is more or less indefinite or until the point you either become an Australian citizen or marry or cohabit with an Australian citizen.

A bewildering brouhaha

In the run up to the Budget, there’s been a quite bewildering to me brouhaha over who can or cannot attend the Budget Lockup. It’s really surprising that Treasury would get itself dragged into such a controversy with its unpleasant tones of attempting to silence critics. I do think as a result of that, together with the pay equity issue, Thursday’s Budget Lockup could get a little fractious. I certainly think the Parliamentary ‘debate’ will be particularly rowdy.

What does happen in the Budget Lockup?

Thursday should be my 15th Budget Lockiup. I’ve attended every single one since 2010 other than the COVID affected 2020 Budget. The routine is that we get access to the Budget documents at 10:30 and then we have about 90 minutes to analyse them before the Minister of Finance (and several colleagues) comes in to give a speech and answer questions. After that Q&A session Treasury provides lunch, and everyone finalises their analysis for release at 2 o’clock when the Finance Minister starts delivering the Budget to Parliament.

To be honest, I don’t know why the Finance Minister bothers with a speech to analysts. We’ve all read the material and frankly it’s much more interesting to ask questions about particular details. Obviously, finance ministers all want to sell the big picture, but for most in the Lockup, including myself, we’re very much more interested in the detail.

This is why the Lockup matters; it’s one of those few opportunities where experts can directly ask questions of the Minister of Finance and other attending ministers. The first few questions will go to the Press Gallery after which economists and other experts chime in.

It’s quite interesting to see who attends the Lockup. I’ve sat next to next to overseas economists, analysts from the British Embassy as well as plenty of other colleagues from the Big Four and other various accounting and advisory firms. But the best part of the Lockup is the question and answer with the Finance Minister which I’m looking forward to as I think it could be a bit spicy this year.

Budget predictions?

I don’t actually think that we’ll see a lot of tax measures in the Budget other than possible accelerated depreciation changes. We might get more details about those changes previously announced in relation to the Foreign Investment Fund regime. As I said, I think the Lockup could be a little bit more entertaining this year and I do expect the Parliamentary debate to be more raucous than usual.

Tax Freedom Day

16th May was Tax Freedom Day according to business accounting firm Baker Tilly Staples Rodway. From this day onwards, workers will have paid their tax bill for the year and are now working for themselves for the rest of the year. Interestingly, according to Bake Tilly Staples Rodway the overall tax paid has increased by 4.66% on last year. That’s despite the tax cuts announced in last year’s budget.

Happy Anniversary…to me 😊

May 16th was also the 32nd anniversary of my arrival in New Zealand, and for those who don’t know my back story, I arrived on this day in 1993 as a backpacker, to follow that year’s Lions tour. The All Blacks finished up winning that series 2-1. Despite that result, I had a great time, and I decided I rather liked New Zealand so I explored opportunities about how I could stay. The rest, as they say, is history. One of the key changes is these days I’m very much an All Blacks fan. Anyway, happy anniversary to me and many thanks to many, many people not least of all my wife Tina for what’s been a fantastic 32 years.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Inland Revenue uncovers over $150m from property sector.

Five suggested changes to the tax system compliance.

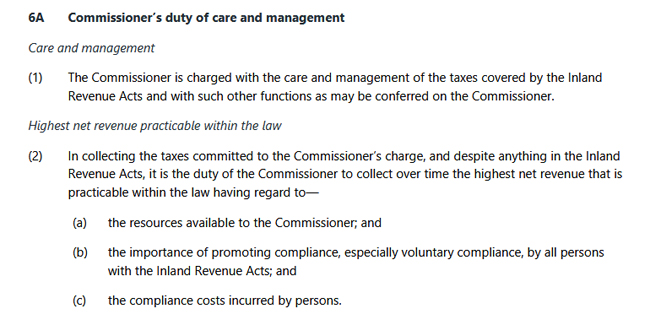

Early last month, Inland Revenue issued a draft interpretation statement The Commissioner’s duty of care and management under Section 6A of the Tax Administration Act 1994. This is a largely unchanged update of the previous interpretation statement issued in 2010.

This might sound a little arcane, but Section 6A, and the related section 6 of the Tax Administration Act are, in my mind, two of the most important sections in the tax legislation. As the interpretation statement puts it, “these are important provisions governing the day-to-day operation of Inland Revenue and the exercise of the Commissioner’s power of the under the Inland Revenue Acts.”

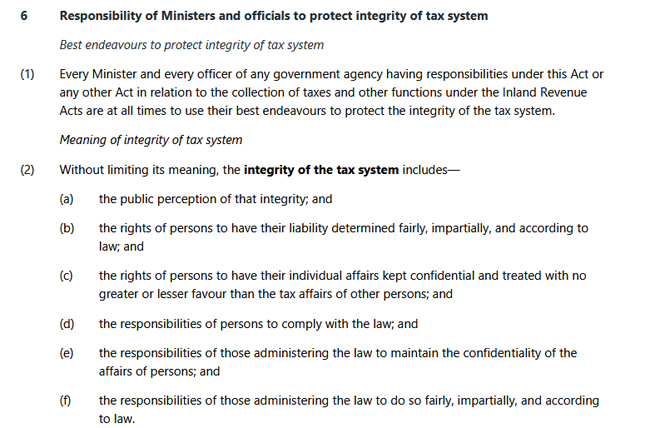

So, what are these provisions? As you can see Section 6 requires Ministers and officials to “protect integrity of tax system” including “the public perception of that integrity.”

Section 6A then sets out the Commissioner’s duty of care and management.

What does “care and management” mean and why are these provisions here? The opening two paragraphs of the interpretation statement explains it as follows:

“A reality of modern tax administration is that the Commissioner must operate the tax system with limited resources. This means the Commissioner cannot always collect every last dollar of tax owing in every case. As a result, the Commissioner must decide how to best use his resources to maximise the taxes collected and to foster the integrity and effective functioning of the tax system.

The Commissioner’s resource allocation and management decisions can affect the integrity of the tax system, including taxpayers’ perceptions of that integrity. What one taxpayer may consider as flexibility that achieves a practical and sensible outcome, others may consider as inconsistency or favouritism.”

What has this got to do with Mickey Mouse?

Setting out the history as to how this section gets here is very interesting, and that’s where Mickey Mouse comes into play. It might be no surprise to find out the actual origins of Mickey Mouse’s involvement in our tax system go back to the UK and a case known as the Fleet St Casuals[i] case.

This was a decision by [the British] HM Inspector of Taxes to reach a settlement with casual workers in the Fleet Street printing industry who had not been compliant with meeting their tax obligations. Instead the workers had “engaged in the process of depriving the Inland Revenue of tax due on their casual earnings.”

As part of this the casual workers had falsified their identities and addresses when collecting their pay so that HM Inspector of Taxes could not assess and collect tax due. Apparently, Mickey Mouse of 1 Sunset Blvd was a regular worker and there were several similar such aliases employed. When the HM Inspector of Taxes investigated, they found there was around 6,000 workers who had not been compliant at all, and many of them had provided false addresses. Chasing down every amount of tax due was impracticable. So, a settlement was reached.

When this became known it attracted the ire of the National Federation of Self-Employed and Small Businesses, and they took a case against the Commissioner of Revenue, on the basis that they were being unfairly discriminated against. The Federation sought out a writ of mandamus to basically compel the Commissioner to assess and collect all taxes properly owed.

The case eventually reached the House of Lords, who held that the Commissioner had a “wide managerial discretion under Section 1 of the Taxes Management Act.” It was therefore within the exercise of the Commissioner’s care and management to reach settlements, even though not all the tax due would be collected.

The Organisational Review of Inland Revenue

Back in 1981, when the House of Lords decided the case, there was no such equivalent provision in New Zealand. During the overhaul of our tax system in the 1980s and early 1990s, the Valabh Committee concluded that a similar measure was needed. Subsequently an organisational review of Inland Revenue was carried out by a committee chaired by Sir Ivor Richardson, the late great tax jurist. This was a highly important review if now somewhat lost in the mists of time.

The Organisational Review’s 1994 report concluded a similar discretion to that of the UK was needed and this led to the introduction of sections 6 and 6A of the Tax Administration Act. (The Organisational Review also prompted a substantial overhaul of the dispute process which is another story).

The thrust of Section 6 and 6A is Inland Revenue has some discretion about how far it can use its resources to collect tax, but in doing so it is bound by keeping the perceptions of the integrity of the tax system. A key point that is repeatedly made clear is that discretionary care and management does not mean that Inland Revenue can override or ignore tax law that exists. Nor do sections 6 and 6A give the Commissioner of Inland Revenue the ability to issue what might be called extra statutory concessions.

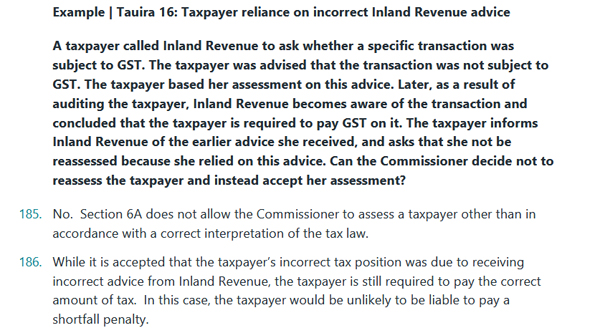

The interpretation statement includes a useful appendix setting out the history of the provisions. There’s a separate handy reading guide accompanying it as well for those who want to avoid wading through the full 59-page consultation. As is now common, the interpretation statement contains 17 examples illustrating how the Commissioner might use his discretion. This example will sound familiar.

The response given in the above example is what I would expect to see. Although it addresses the issue of a shortfall penalty, what about use of money interest? Would the Commissioner have discretion to remit that interest? The example doesn’t cover that, but it’s something that a taxpayer might raise an objection about. Obviously, everything is fact dependent and Inland Revenue may be able to point out that key facts were not provided at the time of the initial inquiry.

As I said, this is a highly important document. Even though the practical effects on day-to-day taxpayers may not seem significant, it’s good to see it updated.

What about Inland Revenue mistakes?

On the other hand, I have to say that the emphasis on Section 6A does overlook the question of whether operational practices of Inland Revenue may be a breach of Section 6. In other words, Inland Revenue does something operationally, which may be correct under the law, but actually is highly disruptive to taxpayers because it failed to process matters promptly or incorrectly.

What happens then, and also regarding the matter of costs that are incurred by the taxpayer? How does that affect the integrity of the tax system or taxpayers’ perception of the integrity of the tax system?

This is an interesting area and one where I think we ought to see more case law involved. But as this updated paper points out, there have only been four tax cases since 2010 where there has been some reference to section 6A, so it is yet to be tested. Consultation is open until 26th May

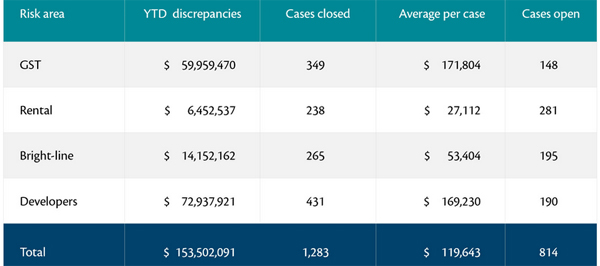

Inland Revenue’s clampdown on the property industry

Speaking of Inland Revenue and reassessments, last week Inland Revenue released a press release proclaiming its latest success in the clamp down on under-declared income and GST.

According to the press release, it has uncovered more than $150 million in undeclared income tax and GST from the property sector. This initiative is part of the additional $116 million funding given to Inland Revenue in last year’s budget. According to the press release, the $153.5 million discrepancy for the first nine months of the current financial year is almost the same as the total $156.8 million figure for the whole of the year ended 30th June 2024.

Now, there are four risk areas identified here. GST, rental, bright line and developers. The majority of the discrepancies relate to GST and developers.

Defaulting developers under increased scrutiny

The press release also revealed Inland Revenue is focusing on defaulting developers because

“…we’re also seeing a pattern of property developers claiming significant refunds as they incur costs upfront but then failing to file and pay once properties sell.

Where we expect a GST payment from a property sale and we don’t see the sale in the return, we contact the developer to make enquiries.

If there is no response or no return filed, we will take enforcement action quickly.”

This is unsurprising and will be an ongoing project. As noted above, Inland Revenue got $116 million over four years in last year’s budget. I would expect it to get more in this year’s budget, but who knows at this point?

Five proposals to improve the tax system

Last month I had the very great privilege of speaking to Inland Revenue’s Policy Advice Division. They asked me to present to them some of my insights about the tax system and on communicating tax policy. It was a fascinating session around those wide-ranging topics. The Q and A session was particularly interesting and entertaining. Again, my thanks to Inland Revenue for inviting me along. It was an enormous privilege to speak to you all. I thoroughly enjoyed it, and I hope you did too.

Now, one of the questions was “if you’re in charge of tax policy for a day, what changes would you propose?”. I put forward the following five proposals.

Number one – introduce a capital gains tax

Firstly, I would introduce a capital gains tax, and I would do so as much for economic efficiency and clarity as for raising revenue. I don’t accept the argument that it’s too complex. Anyone who looks at the Foreign Investment Fund and financial arrangement regimes, both of which trip up experienced taxpayers and practitioners, can’t honestly be saying a CGT would be too complex.

At present there’s a large part of our tax system, particularly in relation to property transactions, that contains some rather subjective definitions around a person’s intent or work of a minor nature. Those are subjective terms and perhaps unsurprisingly, in my experience non-tax specialists people tend to think tax should be pretty much cut and dried. It is therefore surprising for them to discover there is so much potential subjectivity involved.

But I also think that when you consider how our economy has developed over the last 40 years leading to over investment in property (in my opinion and that of economists such as Bernard Hickey and Associate Professor Susan St John), then trying to shift the allocation of capital away from investing in property would be a good thing. I’m not saying capital gains tax would solve that issue overnight, but it would be a start.

Number two – time for the “Fair Economic Return”

My second suggestion would be the fair economic return (FER), which is something that I’ve talked about before which I’ve developed alongside Susan St John. How it operates is that above a certain threshold, a set percentage will be applied to the net value of a person’s residential property. I see this alongside a capital gains tax as a twin track approach to address the issue of better allocation of capital.

Furthermore, as the Tax Working Group noted in its discussion of the deemed return method (on which FER is based), it would initially raise more revenue than a CGT, and we need to raise revenue. The Government’s books are clearly under strain, and this will increase. That was something I talked to Inland Revenue Policy about where I saw the strains manifesting. Cost cutting is part of managing the books, but in my view, tax increases are inevitable.

Number three – mandatory indexation of income tax thresholds

The suggestion I have, and this has been a bugbear of mine for quite some time, is automatic indexation of income tax thresholds. To me, this is primarily about transparency and addressing the issue of fiscal drag (when inflation pushes taxpayers into higher tax brackets).

Fiscal drag has been a tool which governments of both hues over the past 30 years have been very happy to use to disguise the actual tax take. It led to the position we saw last year, where in the first threshold adjustment since 2010, the adjustment was limited to inflation since 2017. In other words, a lot of inflation gains were locked in.

I think there’s a lack of transparency about this process and it doesn’t just extend to income tax thresholds. It also extends to other income tax thresholds, in particular around the financial arrangements regime which have not been adjusted since 1999. It doesn’t apply to GST, however, because I think there are different issues involved with the GST threshold.

These thresholds wouldn’t need to be changed annually as happens in the United States, but they could be changed no more than three yearly or when a threshold, say 5% inflation, has been breached. The key thing is these threshold changes would happen automatically unless the government of the day specifically legislated otherwise. If a government decides not to increase thresholds this decision goes through the regular Parliamentary legislative process and the government must then explain its decision.

Number four – legalise and tax cannabis

I don’t smoke, but around the world there has been a trend to legalising/decriminalising cannabis. The present criminal status of marijuana enables its supply to be captured by organised crime syndicates and those of you who know crime history will know that it was tax evasion that got Al Capone busted.

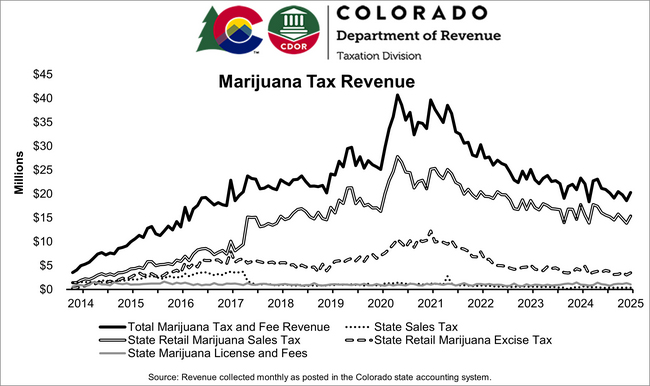

I think legalisation of cannabis is something that should happen and could be a useful revenue raiser. To give an example, Colorado, a state of about five million people, legalised cannabis in February 2014 and since then, its total tax collected has been over US$2.9 billion, roughly NZ$5 billion. In the year to December 2024, it collected US$255 million, about NZ$440 million.

Granted, the tax take from marijuana in has been falling in recent years. But that’s because other states are legalising it as well. If I was Nicola Willis, I’m not sure I’d want to leave a potential $400 million plus per year lying around.

Number five – time for a Tax Ombudsman

Finally, I would establish a tax ombudsman and a tax advocate for small businesses and small taxpayers. This is a more administrative issue, but it’s based on a report I was lucky enough to prepare for the Tax Working Group in 2018.

A tax ombudsman is common in other jurisdictions. For example, when preparing my report for the Tax Working Group, I spoke to the then Inspector-General of Taxation and Tax Ombudsman of Australia. It could be a standalone office, or it could be part of the Ombudsman’s office. Either way, it would give taxpayers a second right of complaint against improper practises as they see it, by Inland Revenue. In that way it ties into our main story this week about Inland Revenue’s duty to preserve the integrity of the tax system.

The tax advocate together with changes to the dispute process would redress the imbalance between Inland Revenue and smaller taxpayers. Something I raised in my presentation to Inland Revenue, is that for a very litigious subject, we actually don’t have many tax cases going through the courts (something Supreme Court Justice Glazebrook has also noted). I consider in many cases Inland Revenue wins because it is playing with a loaded deck. This is the result of the changes following the Organisational Review Committee. I think 30 years on from that review its time we had another look.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

My guest this week is Matt Edwards, the CEO of tax pooling company Tax Management New Zealand (TMNZ). Morena Matt, welcome to the podcast.

Matt Good morning, Terry. Thanks for having me this morning.

TB Not at all, our pleasure. Now you’ve just celebrated your first year as CEO of TMNZ, but you have a quite an interesting background. Prior to joining TMNZ what were you doing and what insights did you gain from?

A 12-month OE which lasted 20 years…

Matt So it’s an interesting story, Terry. I was born in New Zealand and went to university in New Zealand and after I thought I I’d had had enough of small-town Wellington, which is where I grew up I got on an aeroplane and went over to the UK for a 12-month getaway I suppose you’d call it, and 20 years later I I came back, which is which is how it panned out.

I spent the majority of my career involved in what we call Fintech, so that’s basically the intersection of financial services and technology. During the time I was in the UK, I built a couple of fintech businesses, the biggest one was a marketing services business actually that connected financial advisors to customers. So that was a very fun journey and that was going back, gosh, we started that business in 2010, I think.

So that was a little while ago now. And this was when Internet and Internet services were not brand new but still emerging a little bit. So, we were kind of on the cutting edge of that.

I sold that business to private equity five years later or so and then I got involved in running and developing portfolio businesses for private equity. The last business I was involved in, in the UK was actually a life insurance business. We were reimagining the way life insurance is bought and sold and consumed by the end user.

So, yes, most of that time has been spent taking technology and putting it into legacy businesses and seeing how we can make those businesses more efficient. So now I’m finding myself involved in tax and tax pooling, which is arguably a legacy business, having been around for 20 years.

TB Yes, that’s the surprising thing about tax pooling. It seems relatively recent, but it’s now over 20 years old. Your career is interesting because you’re not coming from a tax background. On the other hand, TMNZ’s founder Ian Kuperus and its previous CEO, Chris Cunniffe both worked at Inland Revenue. But you’re coming with a different perspective, so I’d be interested to hear more about that and how you build on this legacy system. But just as a quick recap, what is tax pooling and how does it work?

What is tax pooling?

Matt What it fundamentally is, when you when you boil it down, it’s a pool of tax sitting within Inland Revenue that has obviously been paid in at particular day. It’s used for provisional tax payments, and what that pool allows us to do is essentially in very simple terms, move tax payments around.

So, if your business has overpaid on a provisional tax payment and another business that’s underpaid on that payment, we’re able to essentially swap those payments around. So, what that means is the business that has overpaid benefits from a slightly higher use of money interest rate on that. And the business that has underpaid avoids some penalties and use of money interest for the gap between the dates they’ve paid, and that pool is significant.

From a TMNZ point of view, our pool can be as high as $10 billion and there’s other competitors in the market that do tax pooling as well. So you’re talking about a significant amount of tax that operates under the pool. Well into the multiple billions of dollars, so that’s at a very high-level what tax pooling is or how it works. Once you get into the detail, it becomes some more complex obviously.

TB But just to clarify for listeners, you don’t actually hold that money, you and all the other tax pooling companies do not have $10 billion sitting in your bank accounts or accounts, and Inland Revenue gets notified that those payments are going across so they can see your balances and who has made payments.

Matt Yeah, that’s right. It operates under a trust arrangement, so TMNZ or other tax poolers don’t actually physically touch any of those funds. They go via a trust arrangement and then they go into the Inland Revenue pool. So no, unfortunately we don’t have $10 billion on our balance sheet, although that would be lovely if we did.

TB Indeed. Actually, a key point about it is, if you’ve paid into a tax pooling account, one of the other advantages is you can withdraw those funds at any time. You do not need Inland Revenue’s permission to withdraw the funds, so that gives a bit of flexibility.

The benefits of tax pooling

Matt Yes, while the money sits in the pool effectively you can think of that as quasi liquidity for the business. It can be withdrawn at any time and the interesting thing about it is there’s no cost implication other than perhaps a very minor bit of administration from a business to use the pool, whether they require tax pool and products on the end of that or not.

This is interesting because when you look into the market, you’d expect when you look at tax pooling that every single business in New Zealand would make all their tax payments via the tax pool, because there’s no downside. The interesting thing about it is for an industry that’s been around for 20 years. there are still thousands of businesses out there that are not using tax pooling and we’re not paying their tax via the via the pool, which is quite surprising when you consider that there’s absolutely no downside for a for a business to use it.

But you you’re quite right, you can pull that money back out of the pool at any time, and there’s various mechanisms for doing that. But if needs be, yes it can be drawn back down out of the pool.

TB Yes that is true. This sounds so completely strange. Why would we do that? And I think there’s always inertia. Well, you know, the old accounting matter, what did we do last year? Look at what we did last year, and we’ll do it again this year.

TMNZ was the original tax pooling company, but you have several competitors in there. Still from what you’re just saying, the market is not saturated so to speak, there’s plenty of scope.

So why doesn’t everyone use tax pooling?

Matt No, and what’s interesting about the tax pooling industry is when you explore the stakeholders that are involved – you’ve got your taxpayer, obviously you’ve got your tax filing company, which in my instance is TMNZ and you’ve got your accounting services, and you’ve got Inland Revenue – there’s absolutely no downside to any of those stakeholders in the process.

So, everybody is a winner, and I think you’re right, Terry. I think It’s inertia. “Hey, we’ve never done this. We’ve never paid through the tax pool. Why would we do this?”

It’s nuanced to sort of understand why would I do this? I have a tax bill. I pay that to Inland Revenue. That’s how it works. And I think the other challenge you have is quite often from an advisor if they’ve not been engaged to a level where they’re able to provide advice on using tax pooling or an efficient way of operating tax payment, they’re probably not telling their client that.

So it is an inertia thing and it’s really interesting because in my experience, typically by the time a business model gets to 20 years old, you know you’ve reached the top of the bell curve. At the moment, the market is not saturated and you’d expect that most people who it’s applicable to would be using it. And it’s just simply not the case with tax pooling. There’s still many, many businesses out there that aren’t using it. From my point of view, that’s super exciting, because it means there’s a great deal of market out there that’s to be captured.

Using tax pooling beyond provisional tax

TB Yes, indeed. Now primarily tax pooling developed around provisional and terminal tax, particularly. And as you said, the key thing to understand is this arbitrage between the use of money interest Inland Revenue will charge and late payment penalties which I think frankly is a little rude

But if you’re charging 9.89% interest on overdue debt, then for the largest taxpayers such as the banks or the New Zealand Superannuation Fund their cost of funds is way below 9.89% and so they have the real problem of saying “we underpay our tax, we get crippling interest, but if we overpay our tax, we have no access to the funds.”

So, those taxpayers are very keen users and probably in every sense of the word, your biggest customers. But tax pooling has developed beyond provisional and terminal tax, hasn’t it? You can actually use it for other taxes, including GST for example. In what circumstances can you use tax pooling for those other taxes?

Matt If you’ve got funds in the tax pool you can use those funds to pay any of your standard corporate taxes that typically wouldn’t be used to pay a social tax. But in a business context you can use pool funds to pay any kind of tax.

So, if you’ve got $100,000 sitting in the pool then you can use this to make a GST payment. Having said that, you can’t take advantage as you described it of the arbitrage or the advantage and penalties and interest payments with other tax types.

So, if you’ve missed a GST payment and you’re incurring a penalty and interest against that, then tax pooling and won’t help you in that situation unless it’s a reassessment.

Tax pooling and reassessments

Matt So under a reassessment (assuming that you’ve acted reasonably and responsibly, and you’ve filed your tax returns appropriately) because there’s been a mistake made, there’s a calculation error, an advice error – in that instance you can use tax pooling to mitigate what those penalties and interest payments would be under the under the reassessment situation. But generally speaking, the tax pooling regime is focused on income tax or provisional tax payments.

TB I’m just talking about reassessments; that’s quite an important thing because that’s happening all the time. For example, Inland Revenue just recently trumpeted how it has raised over $900 million through reassessments. That’s where it really comes in handy, and you’ve got tax going back for quite some time

Matt The truth is we’ve got tax going back to 2007/2008 and the tax pool, which is a fascinating thing, when you think about it, should fall into a reassessment situation going back considerable amounts of time when you consider the interest implications over the course of seven or eight years. This could be significant in those situations.

TMNZ’s unique selling proposition

Matt The big USP we have being the incumbent is because we have tax going back that far. It’s highly likely that we can do something should you fall into that kind of reassessment situation and that interest is compounding on what’s owed. Over time, it’s obviously becoming a big number.

These are obviously not everyday instances, but when they do occur, they can have significant impacts on savings for the businesses involved.

TB Can you put that in context back in 2007/8? I think use of money interest rates reached a peak of 14.24%. So, if you’ve got something from there, you’ve been a very naughty boy. But as you say the savings would amount to tens of thousands of dollars.

A surprising fact about TMNZ’s customers

Matt Yes, they can be hundreds of thousands of dollars depending on the circumstances.

That’s also what’s interesting, Terry. You may have been a naughty boy or a naughty girl of course. But you know, I reviewed the stats on reassessments and when you look at it, and don’t quote me directly on it, but 65% of reassessments through Inland Revenue come from technical mistakes. They don’t come from someone trying to game the system or not pay their tax.

A better way to put that is, it’s compliant taxpayers that have made a mistake. Either because of the advice they’ve been provided, or they’ve simply made a mistake.

In that situation, where you’ve got a compliant taxpayer, a mistake has been made that goes back a number of years, which has a large implication from a cost point of view on that business. It’s brilliant, then, to be able to save some money across it because they really don’t deserve to be aggressively penalised in that situation, I suppose.

TB Just quickly about compliant taxpayers, that’s 65% estimate figures out in my experience. Tax is complicated and I’m perennially advising clients on the question of how our Foreign Investment Fund regime operates, it is really quite an alien concept to people who come from Britain, for example, where there is a capital gains tax regime or the United States.

The Inland Revenue has the ability to charge shortfall penalties as well as interest. But typically, in my experience, if you come forward and said “oops, my bad” only use of money interest will be payable, which is when you come in and mitigate that.

But I’ve yet to encounter many instances where shortfall penalties have also been thrown in there, and it leads on to what you’re seeing from Inland Revenue at the moment.

So obviously you get to deal with a lot of reassessments. Are you aware from Inland Revenue has the scale of those reassessments increased in the past few years?

Matt Bearing in mind that I’ve only been looking at it for the for the last 12 months, I don’t have a deep amount of data to look back into. Personally, I think the challenge for Inland Revenue now is growing tax debt.

The reason tax debt is growing is when you look at the cycle we’ve been through over the last five years – with COVID in particular that introduces a situation where businesses really don’t know what’s going to happen. There’s nothing you can compare that that to.

Inland Revenue’s post-COVID approach

Matt A huge amount of money then went into the economy to obviously booster the COVID situation which gave businesses a boom period. Really there were low interest rates and a huge amount of money sloshing around the economy.

We’ve gone straight from that to a very high-interest rate period – which let’s be honest – we haven’t experienced for decades, really. When you look at that run on very low interest rates for a long time, when you look at what those businesses have done, they’ve had COVID and then they’ve gone through this real boom period. Then it’s suddenly gone down. That’s impacted businesses, but of course they still have tax to pay from previous years.

The tax debt is growing, and I think the interesting challenge from Inland Revenue’s point of view is yes, they’ve been very clear both directly in the media and with our communications that they are in the market to collect more tax. They’re going to do more assessments. They are doing more reassessments, but they’re also juggling that against the fact that businesses are going through tough times now.

So, the challenge for them is determining between a business that’s just not being responsible, not paying their tax, and will never be able to pay their tax, and a viable business that’s just going through a difficult period and actually needs support through that period. And to be quite honest with you, with what I see, I think they have been and continue to be very good at trying to support those businesses to get them compliant again, to pay the tax and basically for it not to be a business ending event for them.

When you look at government expenditure and tax debt, or when you have a look at the budget that’s about to come out, there’s a big incentive to collect tax. I think that that IR’s approach is pragmatic Is probably what I would say there.

TB I totally agree with all of that. And just to repeat a point we often make on the podcast, if you get into trouble with Inland Revenue, talk to them. You’d be surprised at how reasonable they are prepared to be. Unless, as you say, the taxpayer has been grossly irresponsible.

Matt And I think you can separate those two categories relatively easily. But it’s surprising how many businesses are still reluctant to want to interact directly with Inland Revenue. If a number shows up on the phone, it’s Inland Revenue or it’s unknown and the reaction is “I’m not going to take that call.”

The interesting thing is though, if the number shows up on the phone and it’s TMNZ or a tax pooling solution, then the incentive to take that call and actually deal with the problem grows.

We can all play a part in this that delivers an outcome that’s best for everyone. So I think the days of super aggressive Inland Revenue – and you know some of the stories we heard in the past – those days have gone. But nevertheless, I think business owners still enjoy that friendly face of dealing with someone who isn’t ringing from Inland Revenue.

The impact of Inland Revenue’s Business Transformation

TB Yes, absolutely. COVID is a very interesting thing because looking back over this, I talked to your predecessor, Chris Cunniffe, five years ago in December 2019. Time flies but in that time, we’ve had two big events. The first being COVID, which we just talked about and clearly that’s having an impact.

But the other thing that was just happening when I last spoke to Chris in December 2019 was Inland Revenue’s Business Transformation programme. And that was, as you know, a huge project that was carried out and came in on time and under budget. How has Business Transformation played out from your perspective?

Matt Obviously, my perspective is slightly different coming in after that project was completed, I think Inland Revenue has done an incredible job of digital transformation when you frame that up under the context of the complexity that they’re dealing with and the legacy nature of tax collection. I think when you look at Inland Revenue they’ve done a great job with that.

But I think from my perspective, what’s very interesting with my interactions with them, they’re still extremely open minded and extremely motivated to continue to make their function, which is tax collection, essentially more and more efficient. And what’s super interesting about that is they very much see this now as an ecosystem place.

How do we make the tax system more efficient for everyone? And when you look at where the technology is going and our ability to connect directly with Inland Revenue and their ability to connect directly with us from a technology point of view, there is the potential to make the function of collecting tax easier, more efficient, less burdensome and costly for business.

The potential there is still significant and that excites me because that’s really what I do and what I enjoy doing. But what probably excites me more is Inland Revenue’s openness to actually pushing this further and further. And the fact that they accept that it is an ecosystem, especially from a technology point of view.

And if we work together on that, we can really make a more efficient system. Although the transformation project itself may be over, we continue to work with them on what I would argue is pretty exciting stuff from a technical point of view.

Liaising with Inland Revenue

TB This is where your experience in the fintech sector is absolutely crucial. You’re touching on that you would have regular contact with Inland Revenue. You’d actually be meeting the senior officials there and talking these matters through as well, because there’s a specifically dedicated unit within Inland Revenue that manages tax pooling. But apart from the people there, you’re also meeting the senior honchos.

Matt Yes.

TB And how frequent are those meetings, and what insights have you gained?

Matt Yes, we speak to the most senior officials and Inland Revenue on a regular basis. There are probably two angles that takes. One is more from a framework point of view. How can we take tax pooling and actually enhance what that’s doing for business and enhance what it’s doing for Inland Revenue?

Although I won’t go into details of that now, we’ve got some pretty interesting stuff that we’re working with now. To use tax pooling I suppose to try and help businesses through this period. I would argue that that touches closer to policy. So we speak to them regularly from a policy point of view which is very interesting.

And then we have a totally other side of the equation where we’re talking to them specifically about the technology the digital side. So, there’s two tranches there and you’re quite right, it’s quite interesting you know, without naming names, the people we speak to are the top people at Inland Rrevenue. So there’s good communication channels there, direct access and they’re very open to that, which means we can do cool stuff.

Comparisons with the UK

TB How does that compare with your experience in the UK? Did you have, or need to have such interactions with HM Revenue and Customs?

Matt No, that’s very interesting. The chances of sitting down with the executive team at HRMC in the UK and discussing this stuff from the UK context would be very, very unlikely. So, one of the cool things about New Zealand is that I can pick up the phone and speak to the Commissioner of Inland Revenue if I need to. It also means that we can do cool stuff. So that’s completely different to the environment that you had in the UK.

So yes, it’s a real upside that New Zealand has right. As a smaller country we all sort of quasi know each other which is quite an interesting difference between things in the UK and New Zealand.

TB Yes. Mind you, I think I’d take a call if I knew that person was holding $10 billion in tax.

Matt Well, that’s probably not the way we sell it, but yes, I know.

Looking ahead

TB You’ve now had 12 months under the under the hood looking around, and you’ve come from this background and clearly you’ve got things in progress. Without revealing any state secrets or anything, what improvements or changes do you think you you’d like to see?

Matt It’s an interesting perspective. Obviously I’ve come into this with completely different eyes to the people that have traditionally been running tax pooling. You know Chris and I’m sure you’ve met Ian before; you know these guys are very experienced career tax people.

I’ve come in from completely the other angle. The big challenge that I’ve thrown down is, as I said earlier in our conversation, why are all businesses not using tax pooling? Even if that is simply just paying their tax into the tax pool and then transferring that tax to Inland Revenue.

There really is no reason that all businesses shouldn’t be doing that. The fact is, when you look at it, I roughly think, 40 or 50% of New Zealand business still don’t use tax pooling in in any way.

It’s also probably worth saying that I’m agnostic as to whether they use TMNZ or another tax pooling company from a high level. I just want every business to use tax pooling because of the benefits.

So when I ask myself “well, how do I address that challenge?” This gets into the strategy off running the business. How do I help all businesses to use tax pooling. When you stand back and look at it there’s inertia in a lot of instances to actually using tax pooling.

Some of that’s technology, some of it’s a reliance on a tax advisor or an accountant being able to advise on how your business can use it. And you know there’s two things there as well. That advisor needs to be able to charge for their advice, obviously. But they also need to have the knowledge themselves, and it’s quite interesting when you look into the market. I think of tax pooling all day, so I assume everyone understands it to the level that I do.

Making tax pooling accessible

Matt That’s simply not true, even within the accounting fraternity. So the real challenge is how do we make this accessible and simple to all New Zealand businesses so they can all use it.

Now if we want to look for an analogy, if you consider a credit card, a mortgage, an overdraft facility or a bank account or insurance. Most people don’t understand the intricacies that go on behind providing those financial services. Almost nobody is going to read their hundred-page mortgage contract from end to end and analyse every point in that although maybe perhaps they should,

I don’t think we’ve got to that stage with tax pooling. From my point of view, it’s a case of how can we bring this product to market in an easy-to-understand way, where you don’t need to understand it, just like you don’t need to understand the intricacies of how a credit agreement behind a credit card actually works.

I think at the moment that’s the piece that’s missing. How do I make it easier for an advisor to take tax pooling to their client? How do I make it easier for a client to understand how tax pooling works? How do we make this more transactional? Probably what I’m saying is, I think if we can answer that question, I think we’ll rapidly see higher adoption through New Zealand businesses using tax pooling and obviously there can only be a win for business and for Inland Revenue.

Tax pooling an essential cash flow tool

TB I totally agree with that and to reiterate here, because of the flexibility tax pooling provides, it is an essential cash flow tool.

Matt It is and interestingly, when you get into it, and this is I guess, where we diverge between the way I think about it and the way I view the industry, and the way perhaps the tax advisor would view the industry, this is our cash flow smoothing tool, that’s essentially what it is.

You can almost dismiss the tax element to a level and say, “hey, you’ve got an obligation to pay money at a certain date that’s not aligning perfectly with your business model.” And let’s be honest, if you look at provisional tax payments, they’re set up under a model where you pay three times a year. There you go. Your business matches that. The reality is that there’s businesses out there that in extreme circumstances make all their revenue within two weeks. That sort of pay tax model versus the reality of your business model.

The chances of those aligning perfectly are quite slim, so it isn’t really about tax from that point of view, it’s about cash flow smoothing.

So, if you have an obligation and I can say to you, “ Terry, you can simply pay X amount per month and your obligation is settled. Or pay nothing for this quarter or pay nothing for next quarter depending on what you need.”

So that is the real USP. Save money on use of money interest, save money on penalties. These things are fundamental to what we’re doing. But at the end of the day, this this is a cash flow smoothing tool and it’s a source in certain instances of capital for business or capital at a rate that’s in most circumstances, especially in SME, that’s significantly cheaper than the cost of accessing other types of capital.

TB That’s a really significant point. How our provisional tax filing dates developed is a whole other story but the long and the short of it, it was driven very much by the big end of town and that that’s they wanted the payments to align.

Matt Yes.

TB And fair enough for you are paying 80-90% of the tax. That’s not an unreasonable suggestion to make. The thing is, you’re only 10% of the businesses and the rest of us are all in this position.

Like you said, there are businesses that have two weeks to make their money and then there are businesses where things go quiet and suddenly, ”oh, January, I’ve been on holiday. Oh, I’ve got a provisional tax payment.”

I’d be interested to know if you see a lot of requests around the January 15th payment, the provisional tax and GST is quite a quite a thump.

The problems with paying tax in January and how TMNZ can help

Matt For want of a better example let’s pick an industry. Let’s assume you’re in retail and Christmas is an important time for you. So ,you’ve just gone through that Christmas period and done a lot of trading. You’ve got a big GST payment coming up and then you’ve also got a provisional tax date sitting there. So in January it’s rough times, right?

Business has been falling through the floor because you’re through Christmas and suddenly you’ve got these two big tax payments coming, or May 7 could be another example of this.

So this is where the creativity and the ease of access is important. You’ve got GST and you’ve got a provisional tax payment owing on the back of that. So pay your GST that’s important. Always pay your GST because, and fair enough to GST, as a tax you’ve collected it’s not your money essentially, it’s Inland Revenues.

TB Always pay your GST, folks.

Matt Finance your provisional tax The rate that you pay on net finance for most businesses apart from the very top end of town is going to be significantly less than what you can use in your overdraft or short-term funding facility or however you’re funding your business. There’s a way we can smooth out that that cash flow quite significantly, and can do it at a rate that’s very, very competitive. From a business cash flow perspective, it’s perfect, instead of exiting all of that cash out of your business at one time. You remain a compliant taxpayer; and you pay a rate on that that’s very competitive compared to the other cost of capital.

But one of one of the frustrating things about the industry is what I’ve just described there. If we go out into the street and ask how many people are aware of this, the gulf is big and the number of businesses sitting out there that will using an overdraft facility that they could be paying 12/13/14/15% interest, to do this is significant.

When you think of the implications of that, in New Zealand we need economic growth. We’ve got a structure of problems in the country; we need to invest money into New Zealand. There’s a massive piece of capital that potentially goes back into the market that grows that business. The business gets bigger and employs more people, who pay more tax in the long run, so it’s a real win/win situation. That’s what excites me about it. It’s not necessarily about the provisional tax payment element of it, it’s about what this can actually do for New Zealand business.

What are the potential savings?

TB Alright. That sounds fantastic and I totally agree with that strategy. It’s sometimes a difficult sell because you’re up against inertia. But potentially what sort of savings could we be seeing by adopting that approach?

Matt It’s greatly circumstantial, Terry, obviously, so it’s very difficult to say “hey, X is the savings.” So you can’t really take it from that point of view. If you consider a very basic situation, “ hey, look, I’ve fallen behind an income tax, I’ve got some income tax owing, and I want a solution for that.”

Depending on the amount of tax, you could be saving anywhere between 15 or 25% on what the cost implication would be if you choose not to use tax pooling. If, as we discussed earlier, you’re looking at a long-term reassessment situation then, obviously those savings could be considerably and materially higher. You know you may be getting into 30 or even 40% saving on what it’s otherwise going to cost you.

The other thing as well that’s worth pointing out when we talk about savings is you’ll save money, and you know I’m a businessman. And if I save a dollar, I think that that’s a job well done.

Saving money and staying compliant

Matt So the savings will always be there. But I think the other thing that we shouldn’t lose sight over is that you also remain a compliant taxpayer. That’s a thing that we don’t focus on enough. So you save money, and you remain a compliant taxpayer. I think that’s an important thing for the business, and I also think it’s a very important thing for the people advising that business to ensure that they remain in that category.

TB I couldn’t agree more with you on that point. Often, I’ve come across situations where I’ve explained to clients “Well, this is the scenario, and this is the tax due.” We’re not tactical magicians who wave a wand and the tax bill goes away. It doesn’t. What we’re often doing is we’re mitigating the impact, explaining and bringing taxpayers up to date. More frequently than people might realise, I’m told “Well, that’s just a huge load off my mind.” People want to be compliant and they’re worried if they’re not compliant. When they hear A – we can make you compliant and B – this is nowhere near as bad as you thought it was, there’s a huge relief you can see, and the strain lifts. Particularly in the SME sector, where it’s bloody tough.

Matt And you know, let’s be honest about it, you’re involved in tax every day. I’m involved in tax every day. So we think that the whole world revolves around tax, and of course, doesn’t.

But you know, particularly in SME land, the people running those businesses, they want to focus on running their businesses. And providing whatever goods or services those businesses provide at the highest level that that they can. And that’s what they should be doing.

Access to expertise

Matt They shouldn’t be sitting at home at night worrying about death and taxes as you say. And you know, to be able to provide a service to them that takes them away from that, I think it’s tremendously valuable. And the other thing, I don’t want to plug TMNZ services too much, I think it is worth the mention that ( I don’t count myself among these people) but the people we have working at TMNZ are tax experts. So often what looks like a very complex and very difficult situation can be worked through to a very advantageous outcome for the taxpayer or for the business owners.

That’s another thing that you get as a periphery benefit of using the tax pooling regime – you get access to those skills and that knowledge as part of the service, which again I think is something that along with remaining compliant, shouldn’t be lost sight of when we when we actually look at the service that we provide.

TB Yes, you’re dealing with provisional tax regime, and even for an experienced practitioners like myself, we’re always thinking “wait, what? Oh, hang on, that’s over $60,000. Oops.” It’s fantastic to be able to talk to your team and they’ll come back and show different ways of dealing with the issue.

That seems a good place to leave it there. This has been a very enjoyable and very insightful conversation. Thank you so much for taking the time to join us. Any final thoughts?

Matt No, it’s been my pleasure, Terry. Thank you for having me on. I know that my point of view is going to probably be quite a different to what you’re used to on the tax podcast. So, thank you for giving me the opportunity. It’s also been very fun from my point of view as well.

TB Excellent. That’s been great. Well, my guest today has been Matt Edwards, CEO of tax pooling company Tax Management New Zealand.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

And reveals results of increased audit activities.

Is GST really a tariff?

It’s been a busy week in tax. Right at the start of the tax year, Inland Revenue has launched a public consultation on a review of the fringe benefit tax regime which is now 40 years old. The 75 page issues paper titled Fringe benefit tax – options for change reviews the current status of FBT, focusing on issues Inland Revenue has identified. It puts forward a number of proposals aimed at simplification of these rules and a reduction in compliance costs, a long standing issue with major employers. There’s plenty to digest here but there’s a summary of the proposals on pages 6-8 of the paper if you want to get a quick handle on the proposals.

Reimagining FBT

The paper also addresses the separate issue of general compliance with the regime. A particular source of grief amongst compliant taxpayers is the treatment of the ubiquitous twin cab ute and the application of the work related vehicle exemption. Overall, the purpose of the paper is to

“…to review how FBT is assessed now, highlight current issues we are aware of with FBT and then outline some new concepts for how we could think about a reimagined FBT regime that is less complex and more targeted…”

The paper has 12 chapters, beginning with an introductory chapter, with Chapter 2 setting out the aims of the review. Chapter 3 explains how FBT is currently assessed. Chapter 4 picks up the FBT regulatory stewardship review from August 2022 which is really one of the initiators of this project. Chapter 5 then provides some comparisons with international FBT regimes.

Chapter 6 has an interesting discussion about FBT’s connection with remuneration. We tend to forget FBT was mainly introduced to ensure that all types of remuneration were brought into scope. Back in the 1980s, before FBT was introduced and the top personal tax rate was 66% it was common practice to give employees non-cash benefits such as company vehicles. Countering this was a key driver behind the introduction of the FBT rules in 1985.