The Greens announced their tax proposals a week ago, last Sunday.

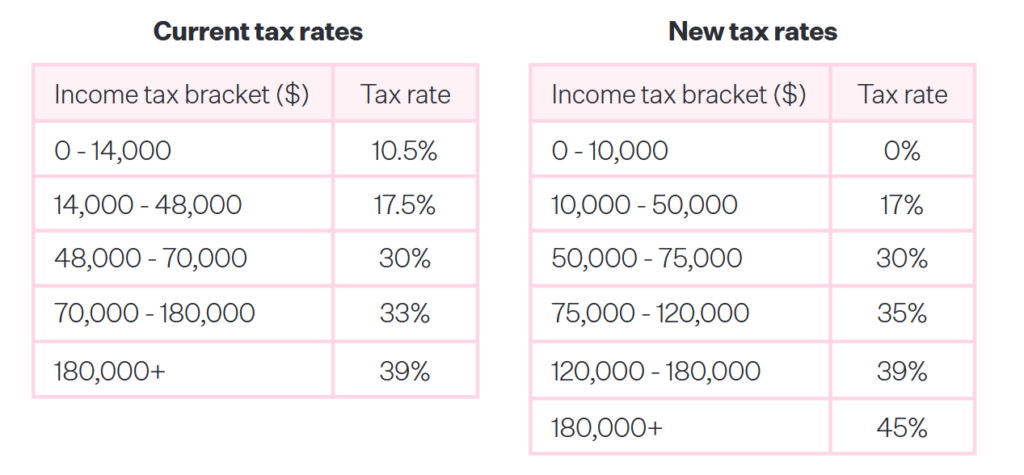

And my reaction was, “These are very bold.” They proposed major tax cuts at the lower end, meaning 95% of taxpayers will be better off under the Greens. Those cuts are paid for by increasing the top tax rate to 45% and increasing the 33% tax rate to 35% as well. These increases are part of the trade-off for the proposed nil rate band of $10,000, which no doubt will be very popular. As is well known, many other jurisdictions have something similar and given the fact that nothing has been done in relation to indexation of thresholds for well-nigh 13years now, it’s unsurprising that the pressure is built up, particularly at the lower end, to change the tax rates.

But most of that got swept away by the Greens controversial wealth tax proposal. In summary, there are two parts to it. Any individual whose net assets, net of mortgages for example, exceed $2 million will be subject to a wealth tax of 2.5% on the excess. For family trusts there is no nil rate band or threshold at all. It’s a flat 1.5% which is a deliberate anti-avoidance mechanism.

Latest Inland Revenue data on trusts

Trusts were used to avoid the impact of estate and gift duties in the past and are used in other jurisdictions to mitigate the impact of wealth and estate duties. So, the Greens have targeted this avoidance. Coincidentally, last Saturday the New Zealand Herald published a piece including details of the trust tax return filings made to Inland Revenue for the year end 31st March 2022 which indicated the value of assets held in trusts. The net assets of the 201,100 trusts which reported, was just over $300 billion. So at 1.5%, theoretically that’s $4.5 billion dollars straight up there.

Incidentally, what that Inland Revenue report doesn’t show is the non-reporting trusts, those are likely to be quite significant. We really don’t know how many trusts there are in New Zealand, the best estimates are somewhere between 500,000 and 600,000. Many of the non-reporting trusts don’t do so because they have no income, but they hold assets such as the family home. So, family homes that have been held in trusts may now be subject to the Greens’ proposal.

Now this kicked off quite a storm, which I watched with a little bemusement because the Greens first of all have to put themselves in a position of such leverage that its coalition partners, almost certainly Labour and Te Pati Māori, agree to the proposal. And then somehow between 14th October, the date of the election, and 1st April next year, the legislation to introduce all of this is drafted and passed through Parliament. So ,it’s a big challenge ahead.

But it caused quite a stir, and I fielded several calls from people concerned about what they saw here, trying to get an understanding about it and my views on it. At our Accountants and Tax Agents Institute New Zealand’s regional meeting on Tuesday we had a very lively debate around the question of this wealth tax. Normally, a lot of the time we’re talking about what’s in the legislation and whether Inland Revenue ever answer their phones again. All this I think shows the impact of the proposals, even though in theory they affect only a small group of people, the top 1%.

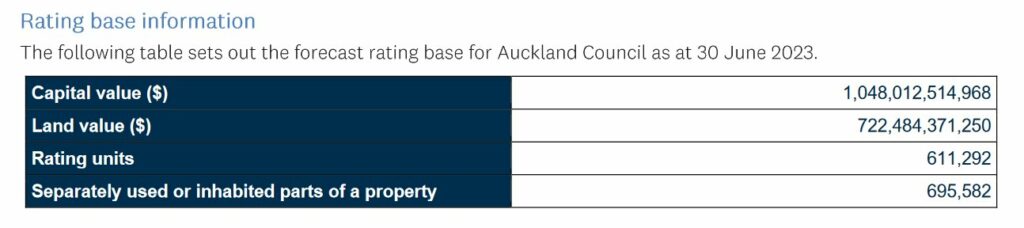

But there is substantial wealth locked up in property. We know that from digging around the official figures. For example, Auckland Council estimates the rateable value for all property within the Auckland Council region will be over one trillion dollars as of 30th June. Obviously, not all of those would be subject to a wealth tax.

What’s being suggested by other parties?

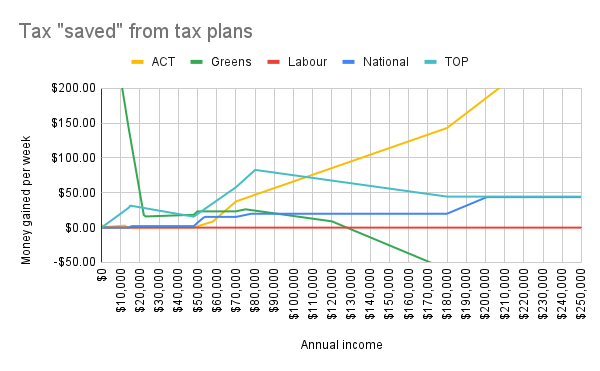

But I thought it was interesting that people are taking the Green’s proposals very seriously. The income tax shift to 45% on income over $180,000 won’t be terribly popular. But at present, the proposals that they’ve put out for the income tax cuts would affect many more people and benefit many more people, all those earning under $125,000, which is something like just over 4 million people. This has a broader impact than either National or Act’s proposals.

It’s quite interesting now as the election comes ever closer, we can start to see the tax policies of the various parties taking shape. The Greens are raising a substantial amount of tax to deal with poverty. Act is proposing tax cuts and it’s taking the ideologically opposite approach of substantial cuts to spending in order to achieve its top rate of 28%.

TOP, The Opportunities Party, are putting out a policy which has a land value tax, and they also propose tax increases at the higher end together a nil rate band and also substantial tax cuts at the lower end.

We haven’t yet heard from Labour on what they would do. Over on Twitter @binkenstein put together a graph comparing the various parties’ proposals so far.

So, the debate has ramped up quite a bit. Obviously, the Greens wealth tax is the most controversial part of it, but the other part which really got very little commentary but is equally controversial, was a proposal to raise the income tax rate for companies from 28% to 33%. More than most of the Greens’ proposals, that would probably produce a certain frisson of tension amongst multinationals. They may look and think “Maybe we might not increase our activities in New Zealand” or they may ramp up what they try and do under profit shifting.

Anyway, it all made for a very lively discussion all round. As I told people, wait and see. But it is interesting to see the pressure point for those are likely to be affected around a wealth tax.

What does the IMF think?

With almost impeccable timing, the IMF, the International Monetary Fund, were in town and it suggested that maybe it was time for a capital gains tax.

The Concluding Statement of the 2023 Article IV Mission noted:

Well-designed tax reform could allow for lower corporate and personal income tax rates by broadening the tax base to other more progressive sources, such as comprehensive capital gains and land taxes, while also addressing fiscal drag and improving efficiency.

It’s not the first time the IMF has suggested changing the tax system. They did so in 2021. In fact, there’s a regular pattern of the IMF and/or the OECD coming here looking around saying, “Well, guys, the country is in good shape, generally government policy is pretty sound, but you need to do something about capital gains taxes.” Regardless of whichever party is in power the Government’s reaction is quite funny. They like the bit about everything being under control. But at the mention of capital gains tax, they all throw up their hands in horror. And yet, as we know all around the world, capital gains taxes are a common feature of tax policy.

The Crypto-Asset Reporting Framework, the latest expansion of the Common Reporting Standards

Now, the Greens wealth tax proposal will probably be music to the ears of the French economist Thomas Piketty, who has proposed a global wealth tax, as one of the core points of his monumental work, Capital in the 21st Century. And at the time of publication in 2014, the opportunities for that global wealth tax to ever eventuate were probably just about zero or maybe marginally above zero.

But since then, we’ve had the introduction of the Common Reporting Standards which I think is actually revolutionising the tax world quietly because an enormous amount of information sharing is now happening on. We know from what’s been reported under the Automatic Exchange of Information that there’s something like €11 trillion held in offshore bank accounts. The Americans have got their FATCA, the Foreign Account Tax Compliance Act, and as a result of that, they know that American citizens have got maybe US$4 trillion held offshore.

Now, the latest part of the Common Reporting Standards is extending the framework to crypto-assets and I talked about this last year when the proposals first came out. Those proposals have now been finalised and the Crypto-Asset Reporting Framework is now in place. There have also been some amendments to the Common Reporting Standards. I’m going to cover all these changes in a separate podcast because I think they’re worth looking at in a bit more detail.

The tightening noose of information exchange

But the key trend in international taxation that’s going on, which I think is going to have a long-term impact around the world, and particularly for tax havens, is this growing interconnectedness, the sharing of information that goes on between tax authorities through mechanisms such as the Common Reporting Standards. I asked Inland Revenue about what information they had been supplied under the CRS in relation to the numbers of taxpayers and the amounts held in overseas bank accounts. Inland Revenue turned down my Official Information Act request on the basis that much of this is obviously confidential, but also would be compromising to the principles under which the information is shared.

Now, I’m not entirely sure about that. I think the more openness we have about what is being shared, the better the likelihood of tax enforcement once people cotton on to what’s happening. They will not think “Yeah, well, I’m just going to leave it over in the UK or the US or wherever, and Inland Revenue will never find out.” My view, as I tell my clients, is they always find out and they know much, much more than you can imagine.

And outside of the CRS there appears to be a regular exchange of information about property purchases between the United States Internal Revenue Service and Inland Revenue here. So be advised, the Crypto-Asset Reporting Framework is just the latest in a building block of international information exchange.

The Auckland Budget – what about climate change?

And finally, the Auckland budget got signed off last week. I’ve been in the press disagreeing with the sale of any part of the Auckland airport shares, and I still stand by that. I think it’s a short-term fix for a long-term problem, but that’s now done and we move on.

What I did think was quite surprising as you delve into the budget is some of the numbers that come out. As I mentioned earlier, the rating base for Auckland and according to the Auckland Council’s documents is over $1 trillion.

But the thing that really surprises me, which wasn’t addressed in the budget so we’re going to have to address it next year, is the question of climate change. Towards the end of the process, the Government announced that in the wake of Cyclone Gabrielle 700 homes around the country are too risky to rebuild. The Government and councils will offer a buyout option to those property owners.

400 of those are in the Auckland region and apparently it doesn’t also take into account what is going to have to happen out at Muriwai because of the slips and the dangerous cliffs over there. As Deputy Mayor Desley Simpson pointed out, “If you say it’s 400 [Auckland homes] times $1.2 million, give-or-take just like the average house price, you’re talking half a billion dollars.”

The question arises how is that split between Auckland ratepayers and the rest of the country? Yet there was nothing in the Auckland budget about this, and that’s just this year’s damage. What happens if we get another Cyclone Gabrielle, next year?

We’ve got an interesting scenario developing where we’re talking about reducing emissions and we’ve got a distant horizon 2030 or whatever farmers and other parties want to extend it to. But in the meantime, we are picking up the bill now for increased damage and we don’t seem to be thinking in terms of how does that affect our taxes and rates? And this is going to be an ongoing issue. So, the question of paying for that, whether it’s a wealth tax, capital gains tax, whatever, is going to become ever more present, in my view.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

When a post COVID-19 world dawns, there’ll be plenty of options for new taxes. Photo: Terry Baucher.

Terry Baucher on rising tax rates, the taxation of capital, environmental taxes, a rising corporate tax take and increasing power and reach of tax authorities

1) In the short-term tax rates will rise.

The initial shock to government balance sheets is enormous. To compound the problem, many governments are still recovering from the effect of the Global Financial Crisis in 2008. Here in New Zealand, the Government’s books were in good order coming into this crisis. But with projections of a potential doubling of net government debt in a matter of months the Government’s finances will undoubtedly come under strain.

In case you missed it, not only will there be a huge hole in the Government’s books as a result of this pandemic, but the inexorably rising cost of New Zealand superannuation remains. As is the not so small matter of responding to climate change. Remember, it was barely three months ago that smoke from Australia was affecting our atmosphere here.

The tax system was going to have to change to adapt to those two issues, and those changes will accelerate in the wake of the COVID-19 pandemic. The first sign of how those issues will be addressed will be in next month’s Budget.

My guess is that next month’s Budget was going to include an adjustment of the tax thresholds probably targeted, as the Tax Working Group recommended, at low to middle income earners. I think that will still happen because putting money in people’s pockets in a recession would be a reasonable measure at this stage. It will however, be the last such adjustment for quite some time.

Medium-term, maybe within a couple of years, personal income tax rates are likely to rise, at least for high earners. It’s worth keeping in mind that the top individual tax rates in those countries we compare ourselves with, are several percentage points higher than New Zealand. In Australia and the United Kingdom, it’s 45%, the United States top rate is 37% and across the EU-28 it averages 39.4% with Sweden and Denmark the highest at 55%. A move higher seems inevitable, if not back to the 39% rate which prevailed between 2000 and 2009.

During the 1970s and early 1980s the Robert Muldoon led National Government responded to a series of economic shocks with several ad-hoc measures. These were increasingly ineffective and were swept away during the reforms of the 1984-1993 period. However, desperate times call for desperate measures and Grant Robertson or his successor might be tempted to follow the overseas examples of special levies.

Australia also had a Budget Repair Levy of 2% on incomes over A$180,000 between 1 July 2014 and 30 June 2017. It was replaced by a permanent increase in the Medicare Levy to 2.5% for those with income over A$180,000.

Separate from special levies, the ugly combination of the inexorably rising cost of New Zealand Superannuation, a significantly damaged economy and weaker government finances, means the continued universality of New Zealand Superannuation will be increasingly debated.

Options might include means testing, or a reintroduction of the deeply unpopular New Zealand Superannuation Surcharge, which applied in the 1990s. An alternative to these might be the proposal made by Susan St. John, for a special tax to apply to recipients of New Zealand superannuation who are earning above a certain threshold. This proposal at least has the merit of fitting in with the principles of a progressive tax system as it targets those whose income indicates that they are not really in ‘need’ of New Zealand Superannuation.

However, the TWG noted that GST is seen as a regressive tax for low-income earners. It’s also worth noting that increasing the rate of tax for a consumption tax such as GST could slow down spending, which is contrary to what’s going to be required in order to help restart the economy.

Instead what may happen over the medium-term is that GST may be extended to apply to financial services, something the TWG recommended be investigated. This could happen in the wake of overseas changes in this area. Globally I expect to see a fierce debate emerge on the matter of expanding the ambit of GST, with countries looking to withdraw or tighten current exemptions around food and financial services.

2. The taxation of capital.

Aside from short-term measures a longer-term implication will be increasing the tax on capital. This will also be a global issue.

Inevitably, here in New Zealand that will mean the reignition of the debate over whether New Zealand should introduce a comprehensive capital gains tax. That’s already begun with former Prime Minister Bill English raising the possibility in a briefing to private investors.

In the short term I suggest the answer will still be “no” for the simple reason it would do enormous damage to the Prime Minister’s reputation (and re-election hopes) for her to repudiate what she said little under a year ago that there would be no CGT while she was leader of the Labour Party.

Putting that aside, we can expect Inland Revenue to ramp up its enforcement of property disposals. It’s even possible New Zealand First might be persuaded to abandon its opposition to making all residential property investment subject to a CGT.

One of the key drawbacks to CGT is that it is a transactional tax – the tax only arises on disposal. If people aren’t buying and selling, no tax rises and there’s always been great concern about what they call the ‘lock in’ effect of a CGT. That is, people will not sell because they do not wish to trigger a tax liability. This means CGT revenues can be either a feast or a famine for governments who prefer more regular tax streams such as PAYE and GST.

Given the politics around CGT other alternatives may be considered. Globally, the idea of a wealth tax has been gathering momentum since Thomas Piketty raised the idea in his monumental work Capital in the 21st Century. A wealth tax is part of Senator Bernie Sanders’ platform. Here in New Zealand, the TWG dismissed a wealth tax as “a complex form of taxation that is likely to reduce the integrity of the tax system.”

Re-examining the role of a wealth tax in the wake of the COVID-19 pandemic seems likely. The 5% fair dividend rate applying as part of the foreign investment fund regime is a de-facto wealth tax which could be adapted for this purpose (although at a much lower percentage, maybe a maximum of 2% as Piketty suggests). The fair dividend rate had its origins in the suggestion of the MacLeod Tax Working Group in 2001 of a applying risk-free rate of return methodology to the taxation of investment property.

The TWG also rejected the idea of a land tax, noting Maori concerns and its terms of reference. But maybe a land tax could be introduced for non-resident landowners only. This would be in line with a trend I see repeatedly in overseas jurisdictions of either taxing non-residents more heavily than locals or restricting the available exemptions. For example, in Australia non-residents do not qualify for the 50% discount for assets held for more than 12 months. Together with higher income tax rates the result is the tax rate on property disposals can be as much as 45%. Similarly, in the United Kingdom and the United States estate taxes of up to 40% apply to assets situated there. Expect to see these issues debated both here and abroad over the coming decade.

3. Environmental taxes will be more important.

Like the cost of New Zealand Superannuation, addressing the cost of climate change will soon push its way back up the tax agenda once the immediate COVID-19 pandemic crisis is past.

As part of this, the importance of environmental taxes to the tax base will rise. The TWG final report noted that according to the OECD, New Zealand ranked 30th out of 33 OECD countries for environmental tax revenue as a share of total tax revenue in 2013.

The TWG’s reference to the growing importance of environmental taxes was something that got drowned out last year with the debate over CGT. In his briefing at the launch of the TWG’s final report, Michael Cullen stressed the need to initially recycle revenues to help those farmers most affected transition to a greener economy.

What we will see emerge is a range of short-term tactical actions with immediate application allied to longer-term measures all intended to encourage a switch to a greener economy.

Tackling emissions in the transport sector could involve the use of congestion charging, putting more money into public transport including rapid electrification of trains and buses. Charging vehicle emissions could be part of this, perhaps allied with subsidies to get older cars off the road, replacing them with newer, more fuel efficient cars as an interim measure. This could achieve three benefits: it lowers emissions, reduces costs for families who are dependent on cars to move around and finally improves road safety because newer cars are safer. It would be a better use of funds than subsidising the purchase of electric cars.

The TWG recommended increasing the Waste Disposal Levy, currently $10 per tonne at landfills that accept household waste. The TWG noted the effect of increases in the equivalent levy in the United Kingdom as illustrated by the following graph:

Landfill tax rates and waste volumes in the United Kingdom

Other initial measures which would also raise revenues and simultaneously encourage behavioural change would be to remove fringe benefit tax on the use of public transport and, as in the United Kingdom, tie FBT to the level of emissions of the vehicle. (The coming clampdown on the non-compliance around FBT on twin-cab utes might have the indirect effect of taking these high emission vehicles off the road).

Tax is power. And maybe once matters have settled down, one of the most significant effects will be a shift in the power of taxation back towards the state and democracies. This will reverse the trend of the past 30 years ago or so, where lobbyists for corporates and special interests have been able to drive down corporate tax rates. This trend has been most noticeable overseas but as the CGT debate last year revealed New Zealand is not immune to the same influences.

The COVID-19 pandemic has almost certainly put paid to any idea of corporate income tax cuts. But the TWG noted that there was little justification for lowering corporate tax rates and a background paper prepared for it noted:

“…the two recent reductions in the company tax rate in New Zealand (from 33% to 30% on 1 April 2008 and from 30% to 28% on 1 April 2011) did not cause a surge of FDI into New Zealand. Nor did it show up in New Zealand’s level of FDI increasing relative to Australia’s.”

How the backlash against corporates will initially manifest itself will be in the adoption of the OECD’s international tax initiatives such as Base Erosion and Profit Shifting, or BEPS, and the recently launched Global Anti-Base Erosion Proposal (“GloBE”) – Pillar Two. The OECD estimates aggressive tax planning by multinationals costs US$240 billion annually.

Late last year, prior to the outbreak of coronavirus, these initiatives looked in danger of stalling after the United States indicated it might not adopt the measures. This appeared to be the result of lobbying by American multinationals. However, the US Government’s finances like those of every other country have been devastated by the pandemic.

So, for a brief moment, I can see the OECD and the US government’s intentions aligning, resulting in a relatively quick agreement on the changes to multinational taxation.

Notwithstanding the OECD measures, social media tech companies might find themselves hit with advertising levies as a means of supporting local media. India raised 939 crores (about $207 million) for the year ended 31st March 2019 from a digital advertising levy. Expect to see other countries follow suit (it could be one way of supporting New Zealand journalism and media which is in crisis as the collapse of Bauer Media shows).

This may now be the time to implement a global financial transactions tax. However, in order for an FTT to be effective, it must be universal. The European Union outlined a possible FTT back in 2013 but has been unable to reach agreement on its introduction. Without that universal agreement, an FTT is effectively inoperable because it is too easily avoided. Adopting the principle of never wasting a crisis, it will be interesting to see if the objections to an FTT are overcome by governments’ need for new sources of revenue.

5. The power and reach of tax authorities will increase.

The final trend that will accelerate is one which has been happening very quietly over the past 10 years since the GFC. That is the swapping of data between tax authorities through initiatives such as FATCA and the OECD’s Common Reporting Standards or the Automatic Exchange of Information.

According to Inland Revenue, since the CRS exchanges started in 2018 it has “received more than 1.5 million records on New Zealand tax residents from 74 jurisdictions.” These records relate to approximately 80,000 New Zealanders. Inland Revenue apparently intends to contact all those for whom it has received information and confirm they have met their obligations.

Separately Inland Revenue has used information sharing agreements with Australia to collect $46 million of overdue child support for the year ended 30th June 2019. In the same year it sent the Australian Tax Office details of 149,031 student loan debtors for matching and obtained contact information for 81,875.

The scale of this information sharing is unprecedented and has happened with very little public debate on the matter. Furthermore, exchanges under CRS are separate to specific information sharing which can happen as part of a double tax agreement between New Zealand and another jurisdiction. No specific data on those information exchanges is made public but anecdotally it is significant.

A little-known feature of the multilateral agreement under CRS is that all signatories agree to undertake to assist in the collection of unpaid tax. Prior to CRS such agreements were negotiated individually as part of a double tax agreement. Under CRS Inland Revenue can now assist any of the other 68 jurisdictions with which it has activated the CRS Multilateral Competent Authority Agreement.

As Inland Revenue’s Business Transformation upgrade continues its data analytic capabilities will increase. My understanding is that the latest upgrade will now enable it to automatically assimilate information it receives under CRS and automatically connect it with taxpayers. This information will only be available to Inland Revenue who can then monitor the taxpayer’s compliance against the data it holds. A question then arises as to the extent Inland Revenue is using artificial intelligence and how that use is being monitored.

Information sharing and the growing use of AI by Inland Revenue and other tax authorities will be a trend about which we should see increasing discussion over the next 10 years. For the moment, citizens appear to be paying little attention to what is happening. How much longer will that inattention will continue? And what are the implications for privacy and democracy? Or is it a case of the ends of higher tax collections justify the means?

Writing about the Easter 1916 Uprising a couple of years before Lenin’s alleged aphorism, Irish poet, W.B. Yates wrote “All changed, changed utterly.” It is indeed all changed, changed utterly and the extent and impact of those changes to the tax landscape will only become clearer over the coming years.

ANALYSIS: Who killed the capital gains tax proposal and why? What did that decision cost us? And is it really dead or just resting?

Tax is inherently political, so when looking at who killed the capital gains tax (CGT), the answer is straightforward: it was New Zealand First in the Beehive with its veto. Firmly slapping down Simon Bridges’ attempts to claim credit for the decision, Winston Peters declared: “We’ve heard, listened, and acted: No Capital Gains Tax.”

Curiously, one of Peters’ justifications for NZ First’s veto was that a CGT would unfairly penalise those who had been “forced” to invest in property following the stock market crash in 1987. It’s worth remembering that even if a CGT had been introduced those historic gains would not have been taxed. (This crucial fact was often rather conveniently overlooked during the debate.)

New Zealand First’s decision had the backing of a number of transparently self-interested groups such as the NZ Property Investors Federation but also many smaller businesses who were concerned about the potential impact.

The wider business concerns were a reason why three members of the Tax Working Group (TWG) — Joanne Hodge, Kirk Hope and Robin Oliver — disagreed with the group’s recommendation of a comprehensive CGT. The three considered any potential benefits would be outweighed by increased efficiency, compliance and administrative costs.

However, the TWG was unanimous that there was a “clear case” for greater taxation of residential rental investment properties.

Robin Oliver, a former Inland Revenue deputy commissioner, presented some interesting insights into the failure of the CGT when he and fellow TWG member Geof Nightingale spoke at the Chartered Accountants Australia & New Zealand (Caanz) tax conference last November.

Oliver commented on the visible lack of political support for a CGT, which was in marked contrast to how Roger Douglas and Trevor de Cleene had promoted the introduction of a goods and services tax (GST) in 1985.

Oliver also noted the proposed design was probably too uncompromisingly pure. In his view the politics were always going to be difficult and compromises would be needed to cross those hurdles.

For example, Oliver suggested that instead of adopting the proposed “valuation day” approach (taxing the gains from a specific date), it might have been more palatable to follow Australia’s example and exclude assets acquired prior to the introduction of the CGT.

Incorporating some form of inflation adjustment was another potential compromise. This is common in jurisdictions with a CGT. Australia, Canada, South Africa and the United States all do not tax the full amount of a gain. Instead, the gross gain is reduced by between 40 per cent and 50 per cent, with the net amount then taxed as if it was income.

The United Kingdom does tax the full amount of the gain but applies a different tax rate linked to the taxpayer’s total income. Interestingly, that tax rate can be higher if the gain relates to property.

Neither of these compromises were ever floated and so the CGT was effectively left to wither and die.

WHAT WAS THE COST?

What did the decision to shelve the CGT cost? For starters, the TWG modelled four revenue-neutral scenarios for redistributing the $8.3 billion a CGT was projected to raise over the first five years.

For many people, the decision not to adopt a general CGT meant they lose out on lower income taxes. However, a cynic might say that for residential rental investment property owners the continuing benefit of untaxed gains far outweighs any such benefit.

The decision not to adopt a general CGT does nothing to break New Zealand’s long-running pattern of over-investment in residential property.

The decision also does nothing to break New Zealand’s long-running pattern of over-investment in residential property, which means little real progress can be made on addressing housing affordability. There is therefore likely to be an ongoing cost for those Millennials and Generation Zers wanting to own their own property.

There’s a wider concern that funds which could be used for productive investment will be increasingly diverted into residential property, particularly in the wake of the increased capital holding requirements for banks.

DING DONG THE WITCH IS DEAD – OR IS IT?

New Zealand therefore remains an outlier in world tax terms in not having a generally applicable CGT. But it is not as if no capital gains are currently taxed. The tax system has nearly 30 separate provisions taxing some form of capital gain.

This includes a general provision which will tax any gains made from disposals of personal property if the property was acquired “for the purpose of disposing of it”. Critics of a CGT also ignored that it would have brought a certainty of treatment to all transactions.

In the absence of that certainty, taxpayers cannot always be certain that a property sale will be non-taxable. Tighter enforcement of the existing rules by Inland Revenue is very likely.

As a sign of this, I have recently become aware Inland Revenue is reviewing property transactions from as far back as 2012. Although these disposals pre-date the introduction of the bright-line test in October 2015, it appears they would have been taxable if the test had existed at the time of sale. The spectre of CGT therefore remains.

Robin Oliver concluded his comments at the Caanz tax conference by noting that although he remained opposed to a general CGT, he did not consider the present under-taxation of residential rental investment properties was sustainable in the long run.

Nightingale supported that assessment. Both were undecided as to whether a CGT was the best means of addressing the issue of under-taxation. An alternative might be to apply the deemed return approach used to tax overseas shares in the foreign investment fund regime.

It’s therefore wise to assume that CGT is not dead but merely resting. My expectation is that the debate will emerge in force towards the end of this decade as the rising cost of superannuation and health costs for the elderly puts increasing pressure on government finances.

By then inter-generational frustration with housing affordability may mean voters are ready to back change. We shall see.

Why did the Tax Working Group’s CGT proposal fail?

Transcript

This week, an update on Inland Revenue’s Common Reporting Standard initiative, the Future of Tax and what went wrong with introducing a capital gains tax.

I spoke recently of Inland Revenue’s new initiative on the Common Reporting Standard on Automatic Exchange of Information or CRS as it’s commonly referred to. This is where Inland Revenue has received details of upwards of 700,000 accounts from overseas tax authorities. It is now working its way through that list of information it’s received and has started to send out some letters to people where it considers there has been either under declaration or non-declaration of income.

I’ve found out a bit more about what’s going on with this initiative, and it’s a little bit concerning how it’s being approached. So far Inland Revenue has sent out approximately 4,000 letters to various individuals with the latest batch of letters going out in the last couple of weeks, in fact.

But it seems to be slightly indiscriminate in its approach, I’m hearing reports of transitional residents who don’t have to report overseas income, receiving such letters and then having to spend time on it.

The information that’s been sent is for the period to 30th June 2018, and there’s another set of information coming for the period to 30th June 2019 very shortly. And apparently Inland Revenue is asking people to reconcile the numbers it’s received with what’s in their tax returns, because there are sometimes big discrepancies.

[Sometimes] the reasons for those discrepancies are because the taxpayer has returned income under a special regime, such as the foreign investment fund regime or the financial arrangements regimes. The financial arrangements regime, as you may recall, deals with income on an accrual basis and brings into account unrealised foreign exchange gains.

So naturally, there are going to be significant differences between what’s reported [to Inland Revenue], the actual amount of interest paid by an overseas financial institution and what’s been reported a taxpayer. So, it’s a little bit disconcerting to hear Inland Revenue taking that approach.

One other thing that has emerged is that Inland Revenue is expecting where someone has not been compliant, [that is] has not disclosed income for whatever reason, people to make disclosures for what’s called the open years, or not time barred [tax years]. This is usually four income tax years prior to the current year to 31st March 2019 for which a return is due. So that means that someone will have to be filing income tax returns covering the period from 1st of April 2014 onwards.

Just an aside on that. If Inland Revenue does feel that there’s been deliberate evasion, where someone was receiving, say, substantial amounts of income and they really should’ve known they ought to have been returning this, it always has the right where there is tax evasion or fraud at stake to go further back than the usual four year period.

I’ll keep you up to date on this developing story, as they say in the news. There’s going to be some confusion. If you have been compliant it’s not a problem. But it is a bit of a headache trying to find out exactly what Inland Revenue is after. And if you’ve not been compliant, come forward and get it sorted out.

It’s always interesting to see the developing trends in tax and catch up with colleagues. Several papers have been very, very interesting talking about the future of tax. Incidentally, because the larger organisations such the Big Four accounting firms and larger law firms that dominate attendance at this conference there’s a fairly international tax and transfer pricing aspect for many of the sessions.

But because of the OECD’s recent tax initiatives I talked about last week, there’s very some interesting papers to be seen on this topic. Something one presenter talked about was that in some ways this development towards a global minimum tax rate may not be the sort of silver bullet to put an end to aggressive tax planning by multinationals some people might think it does. It does represent, as the present pointed out, a threat to the tax sovereignty of jurisdictions around the world. And that is something that hasn’t really been talked about too much.

Traditionally each country had its own taxing rights for activities [carried out] within the jurisdiction. Of course, the digital economy has just basically demolished that old precept which was designed almost one hundred years ago. Essentially, they’re basically now obsolete. But what’s coming and is still being debated may mean that countries have to accept that because of the way economies are now structured the taxing rights are going to change.

And here’s the thing, New Zealand is a small economy basically at the edge of the world on these matters. And to a large extent we will have little say as to what happens, how we can apply tax rules and what our cut, so to speak, of this digital economy tax take will be. And that’s something to really think about.

On the other hand, New Zealand tax officials are actually quite heavily involved in [this OECD process]. The Minister of Revenue and Minister of Finance both spoke at the conference. They gave an interesting political take on matters (they took questions as well).

Both of them singled out Carmel Peters of Inland Revenue for her work within the OECD. Carmel is in fact recognised as one of the top 100 most influential women in the tax community worldwide. This is a fantastic achievement when you consider how small New Zealand is for someone to be held in that regard.

This is a by-product of New Zealand’s Generic Tax Policy Process which is regarded very well worldwide and how co-operative tax professionals and Inland Revenue are in developing and implementing tax policy. So that’s encouraging. We may yet be effectively getting some crumbs at the table, but maybe we’re going to be helping set the table, so to speak.

Another paper that caught my eye, which is very interesting and something I’ve also talked about in past podcasts, is what’s happening in indirect taxes, and GST in particular. The guts of it is governments are really moving to basically disintermediate the tax professionals. That is, they’re going to cut out the middleman.

In some jurisdictions – China, India were mentioned – they are setting up a GST system or its equivalent where GST registered persons can only operate if they basically have a central government approved software where all transactions are automatically recorded and sent back up to and through this software to the tax authority. So, there’s no longer a question of gathering information, preparing a tax return and then filing it after a certain period time. Basically, everything’s going real time. And that’s actually not surprising given the way the Cloud technology is developing.

But it has put Inland Revenue and the Australian Tax Office at a little bit of a disadvantage compared to these other jurisdictions and the likes of Sweden, where, as I’ve previously mentioned, all credit and cash registers are centrally linked. The ATO and Inland Revenue are a little bit behind the game on this, but as the presenter noted, although they may not be pursuing this trend at the moment, on the other hand they’re probably ahead of many of the new jurisdictions in their ability to analyse the data they do receive.

And that’s something people should always be aware of, that Inland Revenue now has greatly enhanced capabilities. And it is almost certainly running its eye over the data it’s receiving, watching for the transactions which a café may not be ringing through.

By the way, this presenter was from Australia and after he paid in cash for a coffee, he wasn’t given a GST receipt even though he requested one, which as he rather wryly said “I didn’t know that New Zealand’s GST system operated like that”. But what’s going on there is almost certainly a case of tax evasion.

And finally, Robin Oliver and Geof Nightingale who were both on the Tax Working Group gave their views on went wrong with the attempted introduction of a capital gains tax.

Both were very clear that the political process of managing the introduction of a capital gains tax was badly handled right from the get-go. Furthermore, the design probably adopted a too purist approach. [Robin Oliver highlighted a few of the differences between the proposals and how Australia designed its CGT].

And the combination of an overly pure design, a poorly managed process in terms of selling a capital gains tax and its potential benefits meant that it really was quite a derailed process. As Robin noted the stars had to align for it come through. And they didn’t align at all, so it fell over badly.

What they also talked about is, well, what happens next? Fortunately, the government’s books are in surplus and the fiscal strains of superannuation and rising health care costs for the elderly are still some years down the path. But both thought that in 20 years’ time, the issue of capital gains tax will be back. And both Geof and Robin said that we have a significant asset class in land which is under taxed and that is not sustainable long term.

So that is a matter which will continue to be debated. We’ve got an election coming up and there was some commentary in the room about what is going to be the tax policy of the government going forward. There’s some talk, for example, about rejigging the rates and maybe increasing the top tax rate.

All that’s in the future. And we shall just have to wait and see.

And finally, just like a quick shout out to all the listeners and readers I’ve met at the conference so far. Thank you all for your kind comments and suggestions for topics and guests. Please keep them coming.

I’ll have more about the CAANZ tax conference next week. In the meantime, that’s it for The Week In Tax. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts, please send me your feedback and tell your friends and clients. And until next time have a great week. Ka kite āno.

So, no Capital Gains Tax to rule them all, not even a wafer-thin mint partial extension of the existing bright-line test to cover all residential investment property/holiday homes. I’m almost certainly not the only one who didn’t see that coming.

The other big surprise for me is the decision to not prioritise any new environmental tax proposals for now. When introducing the TWG’s final report Michael Cullen made much of using the funds from these measures to help farmers transition to a lower-carbon economy. That appears to have fallen by the wayside for the moment.

The Tax Working Group made a dozen recommendations regarding environmental and ecological outcomes. One of these was to develop a framework for taxing “negative environmental externalities” (i.e. pollution).

The TWG report noted that the approximately $5 billion of environmental taxes raised in 2016 represented about 6.2% of tax revenue. According to the OECD, New Zealand ranked 30th of 33 OECD countries for environmental tax revenue as a share of total tax revenue in 2013.

Surprising and a little disappointing

Accordingly, given our dependence on the environment for our agricultural and tourism sectors, it’s surprising and a little disappointing that the TWG’s recommendation for developing a framework is simply rated “Consider for inclusion in the 2019/20 tax policy work programme.” Furthermore, the Government has decided not to advance any new environmental tax proposals other than those within the current tax policy work programme.

The other eleven environmental proposals covered Greenhouse gases, water abstraction and water pollution, solid waste and transport. All are within the current tax policy work programme, but critically the Government has ruled out both resource rentals for water and the introduction of input-based instruments such as a fertiliser tax in this term of Parliament. Unlike CGT these issues are not completely off the table.

Although property owners in particular will be relieved by Wednesday’s decision, there will be far more losers as a result because the TWG’s suggested options for recycling the revenue raised from a CGT through reductions in personal income tax are off the table entirely. This would appear to include any changes to tax rates and thresholds which might come out of any proposals made by the Welfare Expert Advisory Group.

However, given the current tax rates and thresholds have not been adjusted since 2010, the issue of personal income tax reductions is not going away. Today’s decision probably increases the pressure on the Government to make some changes in next month’s Budget.

So which TWG recommendations has the Government marked out as high priority?

The most significant would be introducing measures to counter land-banking and land speculators. The TWG’s final report suggested residential vacant land taxes were best levied by local government. There are few other details so far apart from a direction for the Productivity Commission to include vacant land taxes into its enquiry into local government funding and financing.

The other high-priorities include the tax treatment of seismic strengthening work which frankly should already have been a priority; an interesting proposal from the New Zealand Superannuation Fund to develop a regime encouraging investment into nationally significant infrastructure projects; and a number of technical tax integrity items relating to loss-trading, and better tax collection.

Overall the TWG made 99 recommendations. Eleven have been deemed high priority for progression in the 2019/20 current tax policy work programme. The Government rejected 14 including CGT; another 14 such as the current rate of GST are current tax policy and will remain unchanged; work is already underway on considering 30 recommendations and the remaining 30 should be considered for inclusion in the tax policy work programme in due course. This last group includes business taxation changes aimed at reducing compliance and the TWG’s suggested changes for KiwiSaver. Given the well documented imbalance of tax treatment between residential property and KiwiSaver funds this is particularly disappointing.

‘Not healthy for a democracy for interest groups to wield such influence they can effectively exempt themselves from tax’

Finally, a note on the politics of the decision. I do not believe it is healthy for a democracy for interest groups, whether property owners, business owners or multinationals, to wield such influence that they can effectively exempt themselves from tax.

Over the past 50 years various working groups at regular intervals have reviewed the tax system, considered the merits or otherwise of a capital gains tax and then backed off. In between each review governments of both hues have steadily broadened the scope of taxation.

The Prime Minister may have said no this time, but the pressure for widening the scope of capital taxation still remains whether it’s from widening inequality or the continued tax-favoured status of property investment. We will therefore be re-litigating the issue of capital taxation within 10 years.