Last week I discussed the Green Party’s wealth tax proposals, and commented about how what makes New Zealand an outlier in world tax terms is not so much that we don’t have a capital gains tax, but we also don’t have an estate tax, gift tax, land taxes (other than rates), stamp duties and taxes on wealth or wealth transfers, which exist in many other jurisdictions.

This prompted reader kiwikidsnz to respond as follows

It’s a really interesting comment and thank you for that, because it gets to the heart of the issue around tax and how it changes people’s behaviour. Tax is regarded in economic literature as a deadweight cost. Any tax is therefore distortionary, but we have taxes because they pay for things that people like, such as roads, schools, hospitals, infrastructure and pensions, and a whole heap of other services. Accordingly, a key purpose of taxation is to raise the maximum amount of revenue without producing too many distortions and disincentives.

International Monetary Fund on productivity “a significant challenge”

kiwikidsnz’s comments coincided with a report issued by the International Monetary Fund (the IMF) on New Zealand’s productivity challenge. This paper was prepared following the IMF’s visit here in late February and early March as part of their annual review of the New Zealand economy and it does not make for good reading.

As the paper’s opening paragraph notes:

“Weak productivity growth poses a significant challenge for New Zealand’s long-term prospects. Low productivity growth partly reflects structural factors, including New Zealand’s remote geography and small markets, as well as the relatively large role of the tourism and agricultural sectors. However, it also reflects costs and incentives for investment and innovation, which are in turn shaped by features of the business environment and limited financing options.”

Tax is a part of the business environment and as mentioned above the question arises about the distortionary effect of tax. Now the report, and I recommend reading it, is relatively short, but it’s very thorough. But as I said, it’s pretty grim reading because

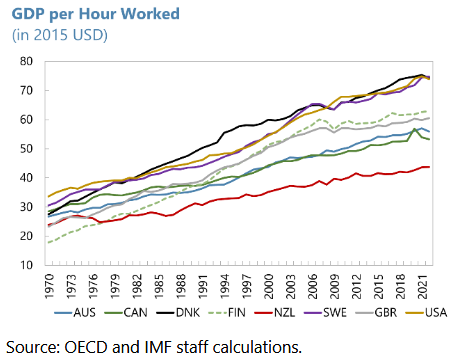

“Over the past five decades, labor productivity growth in New Zealand has lagged that in peer advanced economies, resulting in a widening gap between New Zealand’s GDP per hour worked and that in peers. As a result, by 2022, GDP per hour worked was well below levels in comparable economies.”

A productivity growth challenge across the economy

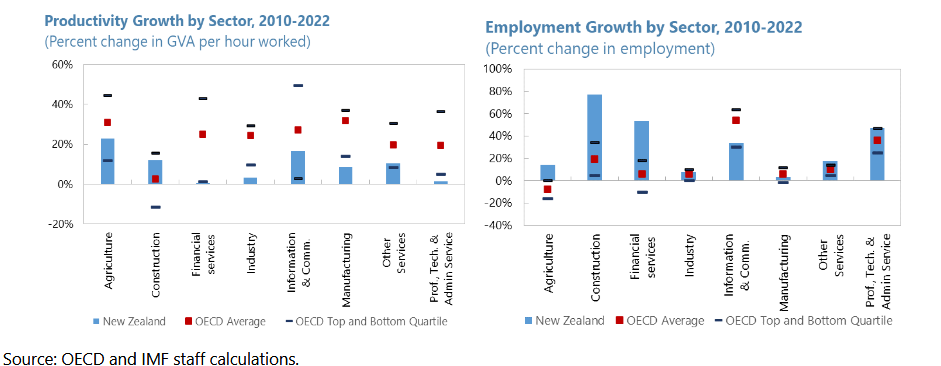

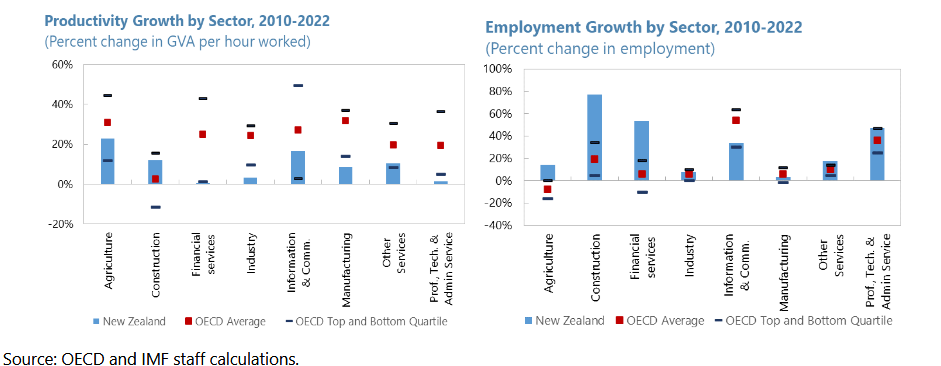

The paper examines this why this has happened and it’s not good reading. A part of the paper that really jumped out at me was paragraph 8 Productivity at the Sector Level. According to the paper labour productivity growth from 2010 to 2022 was below the OECD peer average in agriculture, information and communication (ICT) and some service sectors. In fact

“Productivity growth in New Zealand was in the bottom quartile among OECD peers for financial services, industry, manufacturing and professional and technical service sectors over the same period. The only sector where productivity growth in New Zealand was above the OECD average over this period was the construction sector. New Zealand’s productivity growth challenge thus does not appear to be confined to a few sectors, but to reflect broader issues across the economy.”

Basically, it appears our high immigration has been masking the low GDP per capita growth. ”New Zealand’s workforce has not witnessed the same efficiency gains as workforces in AE [advanced economy] peers (has not been ‘working smarter’), but it has compensated for this with adding more workers at a faster pace.”

Not enough gazelles and too many in the wrong sectors

Another damning part of the report is Section B In Search of New Zealand’s Gazelles. Gazelles are young high growth firms that see 20% growth in sales over at least one three-year period when they are under 10 years, from a base of at least USD100,000. Basically, we don’t have enough:

“Since the Global Financial Crisis, birth rates of gazelles in New Zealand, as a share of all new firms established, have been below the median observed in peer advanced economies. At around 13% gazelle birth rates in New Zealand were below levels observed in Australia, Finland or Sweden, but above levels observed in the Netherlands or Denmark.”

Paragraph 14 of the report I think, gets to where the real problems within our economy have arisen, and where tax may have played a very significant part. It notes young, high growth firms in New Zealand have been concentrated in a few sectors:

“Over 2008 to 2018 new gazelles in New Zealand were primarily concentrated in the financial and real estate sectors. The share of new gazelles in this sector was higher in New Zealand than in most peers, even as the sector saw lower overall productivity growth. At that same time, the share of new gazelles in ICT and professional and technical services, which include hi-tech product, high-productivity sectors dependent on innovation, has been lower in New Zealand than in peers. These trends suggest investment and innovation incentives may be misaligned between sectors in New Zealand. Trends could also be a symptom of the high propensity to save in real estate.”

This is where I think the issue of our lack of capital gains tax and a general lack of capital taxation comes home to roost. The incentives to invest in businesses have been trumped by the investment and lending practises in real estate. I think it was a particularly telling comment here about how those new gazelles, which are a very important part of productivity growth, are primarily concentrated in the financial and real estate sectors.

Replacing one set of disincentives with another

To pick up the issue that kiwikidsnz raised, economic efficiencies do arise from tax policies. Removing incentives such as 66% tax rates and a whole pile of distortionary tax incentives that are given because a government is trying to promote particular behaviour is a good move. But there’s also the disincentives to divert capital if you do not tax something, and it’s is becoming clearer and clearer to me that this is the biggest single problem with not taxing capital gains comprehensively. Coupled with bank lending practices what has happened is we’ve diverted resources into real estate resulting in lower productivity growth and less efficient use of our limited capital. That’s a policy issue that all parties need to consider.

The Australian counter-example

It’s worth talking about the long run implications of the Rogernomics reforms that happened starting in 1984. In October 1985 Australia was also going through its reform period but taking a more measured approach. One of the things it did was to introduce a comprehensive capital gains tax with effect from October 1985. We actually therefore have 40 years of examples to look at what happened around productivity.

Now productivity growth in Western advanced economies has been an issue, but Australia has seen higher productivity over the past 40 years. It has a capital gains tax. We have had lower capital productivity growth, and we don’t have a capital gains tax. Now, correlation is not causation, but there’s 40 years of examples there to make everyone think very hard that maybe in this case correlation does equal causation.

Interestingly, around the whole question of the 1980s idea of supply side economics and cutting taxes to generate economic growth, generally now seems to have run its course, and it probably was always going to do that. Simply because if you’re starting in the 1980s, individual tax rates were then at 60-70% and even more, in some cases. If you’re cutting rates down to 30-40% that’s a significant move and you’re bound to see something happen. But once rates get down to 30%-40%, the impact of tax cuts is less clear.

Meanwhile, in America, maybe not such a Big Beautiful Bill?

What’s really interesting is at the same time as the IMF report came out over the United States) someone who’s been described as the MAGA movement’s top economic guru, Oren Cass, has come out and been very critical of the latest President Trump backed tax cuts included in the Big Beautiful Bill (yes, it really is called that). Mr. Cass is the chief economist for the right leaning American think tank American Compass. He remains the leading proponent of conservative economic populism amongst allies of President Trump.

In talking about the Big Beautiful Bill and the tax cuts that have been included in that, Oren Cass has basically said that the ideas around the Laffer Curve and supply-side theories which have dominated tax policy thinking for the last 40 years have essentially run their race. After commenting “There’s much less confidence in the 1980s-style supply-side tax cutting” he went on

“The reality is we are not going to solve our economic problems if we do not get serious about the fiscal push and fiscal picture and actively reduce the deficit that’s going to require both reduced spending and raising revenue. If you’re not willing to do that, then I don’t think you can credibly say you’re addressing our economic problems.

…Whereas in the past you would have just said, “Well, this thing pays for itself,” This time there is a recognition that it does not pay for itself, — and we have a fiscal crisis — so we also need to explain how we’re at least partly going to pay for it.”

This is an absolutely astonishing admission to hear from a right wing think tank, and particularly in America, which is the home of the supply-side theory.

The thing to keep in mind about taxes, as I said last week, it’s all about politics. But taxes reflect economies and economies change. kiwikidsnz was right to make the comments that there were inefficiencies in our tax system in the 1980s and they were ripe for reform. But it is not a question of set and forget and that’s it, job done, we never have to change again. The dynamics of tax and economies change all the time. And our thinking around that needs to change and reflect that. As a few people pointed out in response to kiwikidsnz we may not have a capital gains tax but other countries do and they have also inheritance taxes, stamp duties, etc and in most cases those peers are wealthier than us. There is 40 years of evidence to suggest that non taxation of capital isn’t actually the economic Nirvana you might think, and it has distorted our economy, particularly our productivity as the IMF notes.

Dr Rod Carr on markets: “myopic, reckless and selfish”

On a related point there was a really interesting leader opinion piece by Dr Rod Carr in the Sunday Star-Times on 1st June. Dr Carr has had a hugely impressive career. He’s been previously chair of the Reserve Bank of New Zealand, worked at Treasury in the 1980s during the Rogernomics reforms and was the inaugural chair of the Climate Change Commission. In summary he has a vast wealth of knowledge about economic policy development in New Zealand over the past 40 years.

His topic was the role and influence of markets. Looking back, after completing an MBA in Columbia University in the mid-1980s, there was little doubt then that markets could allocate financial capital more efficiently than politicians and technocrats and corporate conglomerates. And he believes markets are still, “ruthlessly efficient at allocating privately scarce resources with a price.”

However, he continues markets are “myopic, reckless and selfish,” and understate future benefits and exclude or understate future costs. This results in

“…underinvestment in long-life infrastructure, the degradation of natural ecosystems and under investment in public health and education markets. Markets are reckless because we have created an asymmetry that sees profit accrue to those with private property, while costs are left to lie with the general public.”

He concluded “Markets should be a tool to enable us, not a mantra to enslave us.”

After 40 years, time to think again?

If you combine what Dr Carr said with the comments of Oren Cass and the IMF report on productivity, we’ve now had 40 years of results to look back at how our tax system has evolved and worked in relation to taxation and capital. In my view the long and the short of it is, it hasn’t gone according to plan. Maybe it’s time to look at the script all over again and rethink how we want to have our capital used if we want to start growing a few more gazelles, lift productivity and our living standards.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

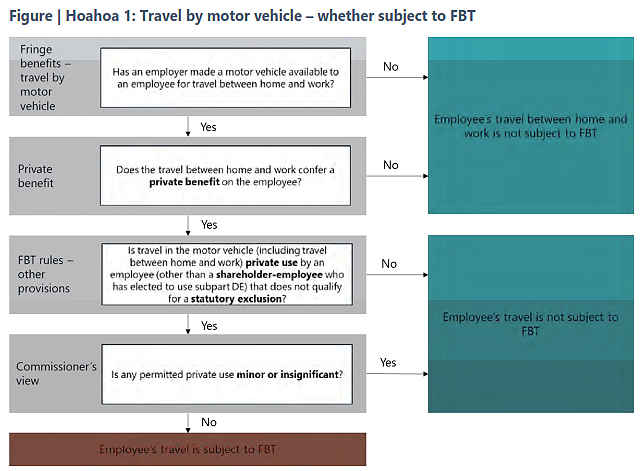

In the same week as Public Service Minister Nicola Willis directed department bosses to tighten up on working from home arrangements, it’s a little ironic to see Inland Revenue release a draft consultation on the topics of deductions for expenditure and travel by motor vehicle between home and work and when an employer provided motor vehicle is subject to fringe benefit tax (FBT) for travel between home and work.

These were released alongside some interesting commentary from Inland Revenue that it is currently reviewing FBT, so what is set out in the draft consultations may change, but as Inland Revenue note, it gets a lot of questions on the topic. With regard to this FBT review my understanding is we may see something relatively soon. I think given the outcome of the Inland Revenue’s regulatory stewardship review of FBT and what the Minister of Revenue has said previously, it’s likely this review with look at simplification measures.

There are actually two consultations which will replace the previous interpretation statement IS3448. The topic is quite involved, because the two draft consultations run to 111 pages of commentary and examples. Fortunately, as is now the common practise, each draft consultation is accompanied by fact sheets, each containing a very useful flow chart to help people work their way through the maze.

The deductibility of motor-vehicle travel between home and work

The first draft interpretation statement deals with the question of deductibility of travel by motor vehicle between home and work which is set out in Subpart DE of the Income Tax Act 2007. What that subpart does is limit deductions for motor vehicle expenditure to the business proportion of the expenditure. It generally applies to self-employed taxpayers and partners in partnerships, but it can also apply in some circumstances to close companies and look through companies.

The basic position is that a journey is deductible if it’s a business journey, but to be a business journey and deductible, the whole journey must be undertaken for the purpose of deriving income. This is actually slightly different from the general deductibility provision for tax, which allow deductions quote to the extent to which they are incurred in deriving gross income. By contrast, this the provisions in Subpart DE are very specific it’s got to be a business journey if it is to be deductible.

Four exceptions

Generally speaking, and it’s probably no surprise here, travel between home and work is viewed as private. But there are four exceptions as a result of case law. Firstly, where the vehicle is necessary for the taxpayer to transport goods and equipment that are essential for their work between their home and workplace and for use both at home and in their workplace.

Now secondly, the taxpayers work is itinerant, which means that the taxpayer works at different locations during the workday and the sequence of where they work and how much time they spend is unpredictable and varies. It’s therefore not practicable for them to carry out their work without the use of a vehicle.

The third case is where a taxpayer is responding to emergency call outs and does so from home. And finally, and this is increasingly relevant, the taxpayer’s home is a workplace or base of operations for the purposes of travel to and from work.

This latter point is where we’ll probably see a lot of discussions and arguments. In order for a home to be treated as a workplace or base of operations the role requires a significant proportion of a person’s work to be spent working at home. I think it’s most likely to apply to owners of businesses who may be working between two places, but senior employees who might be required to make international calls in the evening, they may will be covered.

What’s a business journey?

A business journey is one primarily carried out for business purposes. Case law allows an overall journey to be treated as two journeys if there is a stop in between. It’s possible that one part represents a business journey, and the other part is private.

Furthermore, case law also said that some incidental private use does not mean a journey is prevented from being a business journey. Under the draft Inland Revenue consider that insignificant private use can’t exceed either approximately 5% of the total journey and approximately two kilometres.

The consultation also deals with the issue of what if vehicles are taken home for security purposes or, as is now more common, it’s an electric vehicle taken home to be recharged. Either of those circumstances are not sufficient in themselves to make the relevant journey between home and work a business journey. There have to be other factors at play, such as the exceptions we’ve previously mentioned or that home represents a workplace.

When does a fringe benefit arise?

The second interpretation statement and supporting fact sheet considers the question of when a fringe benefit arises when an employer provided motor vehicle is used for travel between home and work. The position is pretty straightforward: if a vehicle has been provided for private use, FBT will apply. In this context private use would include the use of the vehicle for travel between work and home and work. If a employee has a employer provided vehicle and travels to between home and work in that, then fringe benefit will apply.

There are three statutory exclusions from FBT which would cover travel between home would work. These exclusions apply to work related vehicles (a topic the subject of a whole another interpretation statement;

Emergency calls affecting health, life or the operation of essential machinery and services; and

business trips of more than 24 hours.

If any of these exclusions apply the whole day is excluded from the calculation of FBT.

As noted above Inland Revenue is in the course of reviewing FBT, so maybe some of this might change within the next couple of years or so. In the meantime, it’s good to have this draft guidance. Consultation on this is open until 6th November.

Meanwhile progress on the international tax deal continues

Moving on, we’ve talked regularly about the G20/OECD international tax agreements on base erosion and profit sharing. This week, several jurisdictions signed a multilateral treaty which will to help the Pillar Two subject to tax rule. But the other thing that’s important which was concluded in the last few days, was a Model Competent Authority Agreement on the Application of the Simplified and Streamlined Approach to Amount B of Pillar One. This agreement will provide a framework to enable jurisdictions to comply with what’s expected to be the final format of the rule of the Pillar One and Pillar Two agreements.

However, progress has slowed right down since October 2021 when 135 jurisdictions announced that they were accepting the two-pillar solution. With tax, the devil is in the detail and there is a lot of detail and devil to work through.

I think the other thing that should be kept in mind is that the US Presidential and Congressional elections happening in November will determine how much further progress will happen. As previously noted, the likes of Meta and Alphabet are none too keen on what’s proposed here and their lobbyists have the ears of plenty within Congress. We’ll just have to wait and see. But in the meantime, the deal seems to be inching forward.

“The time has arrived for a capital gains tax”

Last week I covered the report from Victoria University of Wellington about comparing tax rates between New Zealanders and taxpayers in nine other jurisdictions. This week things got spicier than I would expect in this sort of debate after the CEO of ANZ Bank Antonia Watson said in the course of her RNZ interview with Guyon Espiner “the time has arrived for a capital gains tax.” This in turn provoked a strong response from both the Prime Minister and the Minister of Finance. I found this a little surprising. I would have thought they’d just let Ms Watson make her comments and move on, but it certainly adds to the headlines.

CGT the most likely option

Following on from Antonia Watson’s remarks, I spoke to RNZ’s The Panel on Wednesday evening about the question of a capital gains tax. Put on the spot I said I could see it happening. To expand on my answer, it seems to me that a CGT is the most likely option if we do expand the tax base, because CGTs are common in other jurisdictions and the concepts are broadly well understood. And as Antonia Watson also noted, wealth taxes on unrealised gains are deeply unpopular with those that would be affected.

The interview with Antonia Watson is well worth listening to. One of the things I found quite interesting was that a couple of times she mentioned the impact of adverse weather effects. This wasn’t anything to do with tax, but she was explaining that our vulnerability to such events was a factor in why we have higher interest rates than Australia.

This circles back to the point that I made last week and again on The Panel, that the discussion around the question of capital gains tax or expanding the taxation of capital base is really around the question of how do we pay for the forthcoming costs of climate change and an ageing population? Are we raising enough tax revenue right now? If not, what are the options on the table?

What does Inland Revenue think?

Inland Revenue currently have their proposed long-term insights briefing for next year out for consultation. Susan Edmunds of RNZ picked up on this in a story on Thursday. The consultation finishes Friday 4th October, and I really do recommend reading and submitting on it.

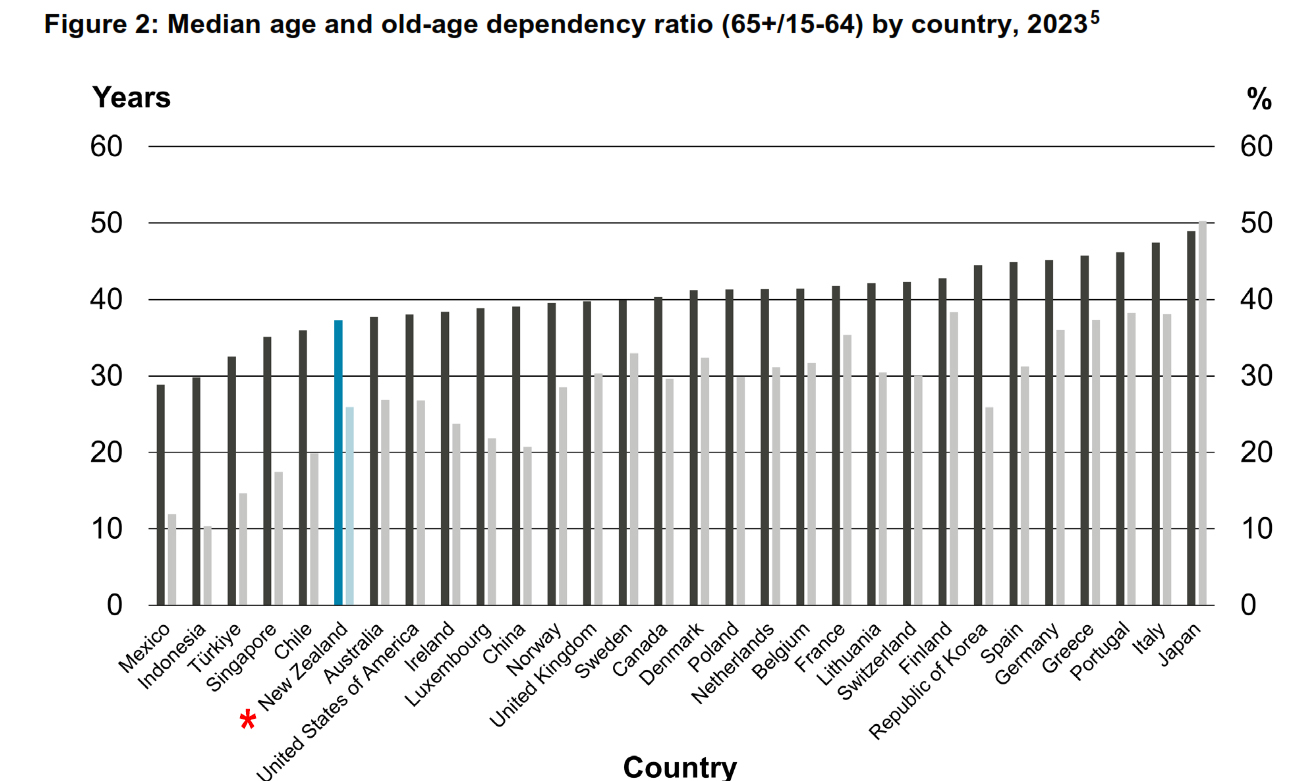

On the question of the forthcoming actual fiscal pressures, Dominick Stephens, the chief economic adviser for the New Zealand Treasury (and former chief economist for Westpac), delivered a speech on Wednesday titled Longevity and the Public Purse, which I’d recommend reading. It includes plenty of graphs illustrating the difficulty that we are facing. Our population is ageing, which is well known and the median old age dependency ratio is rising, although as the speech notes thanks to strong population growth it’s not as bad as other jurisdictions which means we are at the lower end of that range.

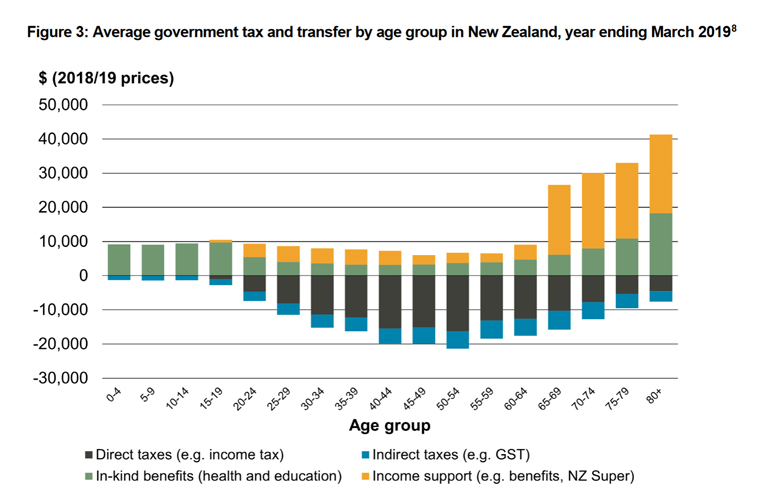

There’s a particularly telling graph about the average government tax and transfer by age group in New Zealand, for the year ended 31 March 2019

As can be seen above for the 65 and over age groups the transfers from Government rise significantly. These are the age groups which is where the debate about sustainability arise, as Dominick Stephens comments:

“Since 2006, the Treasury’s Long-term Fiscal Statements have repeated the message that our fiscal settings are not sustainable over the long run given the impact of population ageing.”

Over the period since 2006 some interesting developments have somewhat ameliorated the potential impact. Interest rates, for example, have been lower than were predicted in 2006, while population growth has been higher.

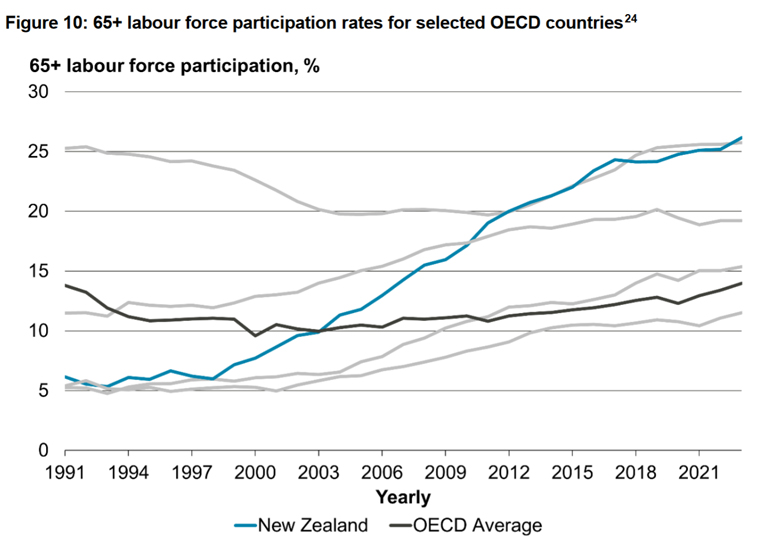

One of the more extraordinary developments since 2006 is labour force participation for 65 plus age groups has dramatically increased. Consequently, we’ve gone from being amongst the lower labour force participation rates to one of the highest.

All things being considered, there are difficult choices to be made and the question of whether more revenue is necessary is a question which isn’t going to go away.

“There is no silver bullet: none of the policy options we modelled in 2021 was large enough to stabilise debt on its own. This means that governments will need to likely draw on multiple expenditure and revenue changes to close the fiscal gap.

Some savings can be made from a greater preventative focus and reducing inefficiencies but making substantive savings is likely to require some tough choices around entitlements. This would have come with trade-offs, particularly for groups of the population who already face challenges accessing health services.”

Governments could also choose to raise additional revenue, in fact as Dominick remarked “successive increases in taxes over time would be required unless actions were also taken to manage demographic expenditure pressures.”

So tough fiscal choices ahead. I note in the comments on last week’s transcript some noted ‘well, wait a minute, why don’t we try and reduce expenditure?’ That’s certainly a driver for the current Government. But I think what Dominick Stephens and Treasury are saying, addressing the fiscal pressures will be a two-part process. We will need to both reduce costs and raise revenue. So, this debate over capital taxation isn’t going to go away soon and will continue. I expect I’ll be asked plenty more times to comment.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

What makes a good tax system and where does New Zealand presently sit?

The current broad-base, low rate approach is under strain. How do we address that? What can we do to keep/ preserve that as far as possible? And more.

Terry Baucher: It is my very great privilege this week to be joined by three of the titans of tax in New Zealand, Rob McLeod, Robin Oliver and Geof Nightingale.

Rob, or more correctly Sir Robert McLeod, KNZM is one of THE gurus of New Zealand tax, has been involved in tax policy at the highest levels since the 1980s. A former chair of EY, he was chair of the 2001 McLeod Tax Review and was also a member of the 2010 Victoria University of Wellington Tax Working Group. He’s currently a consultant, although still very much involved in the tax policy world. He was knighted in 2019 for services to business and Māori. Kia Ora, thank you for joining us.

Robin Oliver, another of the gurus of New Zealand tax, until he retired from Inland Revenue, was Deputy Commissioner of Inland Revenue and head of Tax Policy where he advised the 2001 and 2010 tax working groups. He is now a partner in tax consultancy Oliver Shaw and was a member of the last Tax Working Group. Robin was made a member of the New Zealand Order of Merit in 2009.

Geof Nightingale recently retired from PwC, and when he’s not cycling the length of the South Island, is an independent tax consultant. He was a member of both the 2010 and 2019 tax working groups. Thank you again to all of you for joining us.

What makes a good tax system and where does New Zealand presently sit?

We’ll begin with what was asked at this year’s International Fiscal Association Conference. The three of you spoke on the topic of what makes a good tax system. What does make a good tax system and where does New Zealand presently sit? Rob, would you like to lead off?

Rob Mcleod (RM) Thanks, Terry. Well, I think at its core tax is mainly about raising revenue to finance government programmes. It’s true that tax has peripheral tasks as well, like you know, correcting for market failure. If we think about carbon taxes, the primary purpose of that kind of tax is really to moderate adverse behaviour in the economy, which is not is not really a revenue raising objective. Some would also argue that taxes are there to achieve redistribution goals, transfer income to those that are in need. That too is not so much a revenue raising goal.

“At its core tax is mainly about raising revenue to finance government programmes”

But if you go to the real reason why income tax exists in countries, it’s actually to raise revenue for governments. If governments didn’t need revenue, you wouldn’t have taxes. And chances are you wouldn’t have such a major regime doing these other two things, like corrective taxation, like carbon taxes, or trying to redistribute income without the agenda of raising revenue. I would argue that we wouldn’t have tax systems on the scale that we have them doing those other things. So, I believe that raising revenue is the primary goal of a good tax system and doing it at least cost would be my formulation.

Robin Oliver (RO) I agree with Rob, even more so, that a good tax system is one that works. It raises money for the government. That may seem obvious to people, but you can’t have taxes which fail to raise money. Margaret Thatcher’s poll tax failed to raise money. It was a failure.

“You’ve got to really focus on raising money at least cost”

So it has to raise money at least cost to society and that’s admin costs, compliance costs, but overall economic costs. The cost of disincentivising people from work and savings and so forth. People think that’s “blah blah blah blah” but the estimates in New Zealand and Australia, and used by the Australian Treasury, is that twenty cents in every dollar of tax is lost in economic costs. In other words, not quite, but basically lost output, lost wealth for the country. So, you’ve got to really focus on raising money at least cost.

Rob mentioned redistribution. I think redistribution’s got nothing to do with a good tax system. Government raises money to do good things – health, education, welfare. We’ve lost focus on what tax is about. We’ve got diverted into all sorts of ideas that it could be used for. No, it’s about raising money, at least cost. Every tax proposal should be looked at “Is this the way we could raise some money, effectively, at least the cost to society.”

TB Thanks, Robin. Geof, I think you have a slightly different take on the redistribution issue and I note that the IMF was talking about redistribution in one of its papers recently

Geof Nightingale (GN) Well, Terry, I’d largely, and violently agree with Rob and Robin that the primary function of a good tax system is to raise the revenue that government needs. But it’s how it goes about that where I might differ.

There’s a couple of backgrounds, opening points I’d like to make, and the first is I think it seems, really uncontroversial that our modern democratic states with tax systems and, you know, rule of law-based things. They’ve done more than anything that’s ever been tried to lift living standards. So, broadly, I think they are a good thing that the tax status policy people might call it is a good thing.

“You can only tax by consent”

The second point is, that in those democracies, it’s really important for tax policy people to acknowledge that you can only tax by consent. I mean we impose taxation through the rule of law and through enforcement. But in the end people vote on taxes and people vote governments in and out and tax is often a key election thing. So you can really only tax by consent.

So, whatever the theory may tell you, you have to – I’ve learned over many years now – bring the public with you. That’s the job of the politicians, not the policy people. The policy people have to accept. That general consent point is really important when you start talking about the future of tax in New Zealand.

And then the third thing is there’s no such thing as a perfect tax system and as Robin pointed out, we navigate it, every tax policy choice is a bunch of trade-offs, and we navigate those trade-offs with some well-established principles. You know, equity efficiency, administration etcetera. And those principles can never be applied scientifically. In the end, they come down to, in my view anyway, value judgments at the margin, and that’s where the politics comes into the tax system as it as it should be.

So what is a good tax system? Well as Rob and Robin said, primarily one that raises revenue with the least cost to society. And there are secondary objectives, and those are the distributional impacts. I think those are important for policymakers to take into account. And I think they feedback around into the consent of citizens to be taxed and and the fundamental democratic process actually. and. Most OECD countries, in fact all I think, have progressive tax systems by and large and general voting patterns suggest that that’s the majority view of life across OECD democracies.

The problem with behavioural taxes

Other secondary objectives that Rob and Robin mentioned with behavioural changes, carbon taxes and things and those are very specific instruments of public policy, and they might raise some short term revenues. But they shouldn’t be relied on for long term revenues and it’s almost a different category of taxation to the general tax system because if they work – those behavioural taxes – the revenues will often dry up, will be reallocated into the areas that they’re trying to change.

TB That’s something we’re actually seeing with the tobacco excise duty. It worked and now revenues are falling and now that’s sort of a hole in the finances.

RO But if that works, yeah, it’s the same as environmental taxes. You know you have taxes on degradation of the environment. And if you don’t degrade the environment, you get no money. And it’s perfectly fine. They work, but back to Geof’s point. I totally disagree that redistributions got anything about it. You clearly have to have a democracy; in a democracy you have to have consent. I agree with that. You have to have consent to make the tax system work because of voluntary compliance and all that.

Poll taxes – efficient but unworkable?

But the purpose of tax is to raise the money in the most cost-effective way. And I give the example of that is the poll tax, Margaret Thatcher’s poll tax. I mean poll taxes are loved by economists because it’s thought of as being efficient. But it doesn’t work. I mean if you want to raise New Zealand’s government revenue by poll tax you’ve got to raise about $30,000 per individual. You’re not going to go out to people in South Auckland, a family household, and demand $100,000 from them please. I mean, they don’t have it. And there’s no point in demanding money, which people just don’t have.

And that’s why even an efficient tax system, inevitably given the level of government expenditure we have, will need to be progressive. Because you know the lower income earners just don’t have money to pay the tax that the government needs. But again, the point is, you’re really trying to raise money to spend on health, education and welfare and you want to do it at least cost. And forget about trying to have a secondary objective of redistributing income, that just leads you into bad taxes. And that’s led us from having a good tax system to one which is now pretty awful or going that way.

TB It’s a hell of a topic that. I mean, there is always a redistributive effect of tax, and the recent Treasury paper on the fiscal incidence of taxation was quite interesting in that regard.

RO Yes, good paper.

What about ring-fencing taxes for certain objectives?

TB The Treasury paper showed health and education benefits going to different deciles. They’re essentially redistributed within the system. So just a quick thought about these behavioural taxes Do you actually see much of a role for ring fencing? Tax takes such as, for example, environmental taxation that we raise these, we’re trying to encourage better behaviour, but the funds don’t go into the general pool but are used to mitigate the impact of climate change. Is there a role for that Rob?

RM Yes, I think I think there is. We call this hypothecation and we’ve had hypothecation in the area of fuel taxes for example, which are put on road users and then reinvested back on to roads at various times. But over time, you know, I think that money was ultimately then sent to the consolidated fund.

RO I mean, money is fungible. And therefore, putting it in one pot versus many pots, you can have an argument about whether that’s effective. I think ultimately if governments ensure there is a correlation between how they apply the funds and the taxes they raise, and hypothecation is a solid principle to get that correlation. But I think that the more recent view of governments has been that they can be relied on to effectively finance it all out of a consolidated pot. So yes, hypothecation is certainly there, and we’ve got examples of it.

Economists hate hypothecated taxes, because it ends up government spending money wastefully and low priority areas, because that’s where the money is. But it does serve a purpose, it provides the right incentives. There’s a case for it you know road user charges, Rob said was a good case in point. And you can make other cases like how do we control the level of health expenditure? Well, you could hypothecate GST to health and if people want to spend more on health, GST goes up and everybody has to pay it, so you can end up with arguments for hypothecated taxes. But the economists really hate them.

GN At the risk bringing distributional effects back onto the table, hypothecated taxes can also be highly regressive, so yes, I’ll just leave that there.

TB Yes, a common hypothecated tax around the world, which we don’t now have but once did, was Social Security. You see that many other jurisdictions had that and we’d had that until the late 60s. I think it was Rob Muldoon who decided stuff this we’ll just get rid of it because it was, as Rob described, was just going into the consolidated fund. But looking way back, it was a quite significant part of tax revenues if you look track the history of tax.

The problem with social security taxes

RO And very important in Europe in particular, and the United States of America. And we are very lucky not to have them. Australia and New Zealand, one of the few OECD type countries not to have Social Security payroll taxes, which are linked with the benefits. The reason for that is it results in peoples’ old age pensions, or whatever you call them – New Zealand super being linked with past earnings.

And that means that the poor are really poor, when they are elderly. And that’s the case in the UK. Everybody gets the same in New Zealand which in my view is absolutely a much better system than using your tax system to provide benefits linked with wages. Which means particularly women who are not always in the workforce, but child rearing, skills get really done over. I think we’ve got a much more equitable system of expenditure on welfare because we don’t have that.

The incidence of tax – who is actually bearing the tax burden?

RM Terry, can I just perhaps take us back to redistribution, I think there’s one important point about redistribution which unfortunately is a bit of a technical point. But it’s one that is overlooked not only by lay persons, you know, people not familiar with technical stuff, but also the tax profession itself. Which is the issue of incidence.

So if you just start with the GST as an example, most New Zealanders wouldn’t accept, and rightly, that the GST is not imposed on them. And yet, if you have a look at who pays the GST, they don’t pay it. The consumers do not send cheques to Inland Revenue. The tax is actually imposed on businesses. As a matter of imposition. When we talk about redistribution, we’re inclined to assume that the tax impact is where the law imposes it, but the key principle that’s demonstrated by the GST example is the market actually takes that tax and spreads it around, arguably like margarine, to all of the stakeholders and sometimes non stakeholders, and the and the contract to be affected.

These are such things as gross ups, if you go and slap a tax on somebody and they’ve got market power, they’ll put the price up of what they’re supplying to others. And in so doing, they’ll pass that tax burden on to others. And this is completely ignored in my view, when people are talking about redistribution, because there’s the assumption that the taxes that are actually imposed by the government, is actually borne by the people who send cheques to Inland Revenue Department, is utterly false. And if you try and unravel that mathematically and work out who actually is bearing the tax, the best you can get to on most of it is estimates including the dead weight loss of the 20% that Robin is talking about, it’s there’s a lot of estimation going on to get to those numbers.

There’s no argument that that economic effect is real, and for me that’s a big undercut of why I don’t buy all the redistribution argument, because it tends to proceed on the assumption that the way the government’s levying the tax will ultimately shape and determine the burden of it.

RO We don’t know a lot about the incidence of tax. But what we do know, it’s almost never born entirely by the person paying it. So, you end up with these studies, like the awful IRD study on high wealth, totally ignoring this fact, just totally ignoring it.

And the classic example of economics in the United States is that you have local body bonds, the interest rate is tax free. It’s a subsidy to like City Councils or what, and the federal government doesn’t tax them.

The high wealth individual – the person on the very high rates – ends up owning all these municipal bonds. They don’t pay any tax. But they’re getting a lower interest rate because they’re bidding up the price of these bonds, which is what’s intended and the local City Council get cheap money. And then along comes a bunch of officials measuring their tax burden and finding it zero. Disastrous. Horrible. Well, in fact, they’re paying it through the lower interest rates on it.

And this happens all the time, all through the tax system. You put taxes up on foreigners, that’s a good idea. Foreigners we don’t like, they’re not voting, and we put big tax on foreigners. They just simply demand a higher rate of return or don’t invest here. We end up with lower productivity, lower wages and the economics is absolutely clear. Put your tax on your non-resident investor, it ends up coming out in lower wages. And that’s exactly Rob’s point. The incidence is always shifting and yet we totally ignore this. The political debate just assumes the world is not what it is.

TB Robin, I think we’re going to see more and more of that. Sorry, Geof, you were about to say something.

GN I totally agree with Robin and Rob on incidence, it’s critical. But it comes back to my opening point that you can only tax through consent, eventually. If incidence is not well understood, policymakers – and it’s very hard and very slippery getting your hands on the concept – but policymakers need to think about it. But if you can’t convey that to voters, then it becomes kind of irrelevant.

I remember Sir Rob’s MacLeod committee and the $1,000,000 tax cap for individuals. I thought was a was a great idea because of that sort of argument that we’d be better off with $1,000,000 than not. But that policy is too easy to attack politically from an equity and a sort of a fairness sense. And that’s what happens in the real world as we all know and that’s why we end up in political arguments around the secondary purposes of the tax system, as opposed to really discussing the primary purpose of the tax system Which is least cost revenue raising for government policy. So, I agree with their incidence comments, but it works both ways, I think.

RM Can I just jump in on that one and just observe that in the McLeod Review where we did recommend that to be honest, I think it’s politicians that say that say no to those sorts of things than not, as opposed to public sentiment. Muldoon made the famous quote that Joe Blog, the average person on the street, wouldn’t know fiscal deficit if he tripped over one. And I think that’s a long way back and things weren’t as sophisticated then as perhaps they are now.

But if you think about the complexities of tax and you think about the extent to which the public is actually engaged with that complexity, I think that you are apt to over egg that interaction. Because ultimately politicians and officials and people like ourselves, there is a leadership role we play and the public follows that leadership.

I think you can observe that in history. The differences between countries and the qualities of their tax system often reflect the differential qualities of officials, politicians, et cetera, that’s going on in those countries. So, while I agree that in the concept of democracy, there’s a public underbelly in debate and voting terms, there’s one hell of a space for leadership and tax policy. Otherwise, we might as well pack our bags and go home. And I think that that is very influential and that’s why these debates and these principles of incidence and so on are important and need to be approached in the way we’re doing it.

RO We can see that with GST. We’ve got a flat rate, a good GST system, world class.

I remember back in the 80s Sir Robert Muldoon, the proposals was put to him about that. And he said, “You mean we’re going to tax water?” And he chuckled, “No way.” We put GST on doctor’s bills. People overseas think that’s just totally astonishing. Yet there’s broad support for what we have in GST, a non-progressive tax. Bizarrely we legislated to make it regressive, but it does meet those economic principles and it’s got widespread support. I mean, politicians keep on arguing for GST on no food, but those proposals get put up and get rejected every time.

Rob McLeod’s suggested alternative to a capital gains tax

TB Rob in your review, you raised the possibility of the risk-free rate of return method (RFRM) as an alternative to a capital gains tax. And we’ve seen that in the Foreign Investment Fund regime. Are you still keen on the idea?

RM The RFRM, the McLeod Review, came largely out of the debate around taxing housing. And this was in a discussion document, by the way. It wasn’t the final recommendation; it was abandoned because of what Robin said. Michael Cullen’s switchboard was blown up by the complaints of from telephone callers and we knew that was a pretty strong signal that no government was ever going to support it.

So, we pulled the plug. But basically, the problem with taxing assets that produce, that give sort of imputed income like your motor car or your house or your washing machine, there’s no cash flow to really measure the income. It’s economic income, but it’s hard to measure. And so, the beauty of the RFRM is that you calculate it effectively as a wealth tax, which is applying a percentage, I think we had 4%, against the market value of the of the equity in the asset. It’s quite important. That’s one feature of the RFRM is you’ve got to work out what you’re going to do with debt, debt funding of the asset. And we came to the conclusion we’re best to deal with that by narrowing the tax onto the equity, which is the total value of the asset minus debt associated with it. Which brings in problems because people then start to plan with where they load their debt, right?

But it was simplicity. If we could have made the income tax work on that kind of asset that’s a superior way of going, if you can make it work. I think the only reason you go to RFRM in substitution is there’s easier compliance and administration for taxpayers and the Inland Revenue. The F|IF regime I think Terry came out of the international regime As the child of the CV, the mark-to-market option.

I think you’re thinking of the FDR [fair dividend rate] in today’s terms is probably the most relevant analogy. Fixed dividend rate which I think did come from a an RFRM logic, although it’s a bit screwy because FDR, the RFRM tax principle is you should apply it at the riskless rate of return, and not at the risky rate of return, which is the way FDR works. And also, no deductions which FDR doesn’t abide by in its various option formats. So the concept is much the same but quite different in detail.

What’s surprising in the tax world now?

TB Is there anything in the tax world that surprises you right now?

RO I would say the wealth tax coming on the table, totally unworkable. According to the papers the last government almost legislated for a wealth tax in the last budget, ??? funding and massive reductions in income tax rates. And that wealth tax was completely unworkable and would never get off the ground. It was a total nuclear bomb on our tax system. The fact that people are seriously talking about totally impractical things is a serious concern.

We’ve got to be adults here. There is no fairies at the bottom of the garden. There is no pot of gold at the end of the rainbow. Grow up. Taxes have to be pragmatic and have to be workable, and trying to measure everybody’s wealth on a comprehensive basis every year is not.

GN I remain surprised by the continued acceptance by middle New Zealand of what I consider to be really high effective tax rates on labour income through the combination of GST and [tax] rates. And I remain surprised when you look at their voting patterns, their general resistance to extending taxation into capital income to address that, so not raising taxes as a percentage of GDP, but recycling revenue, shifting the instance of where slightly where that tax is paid, and it continues to surprise me. I think that message came through the high net worth survey that came out last year, but it was obfuscated by the complexity and some of the methodology problems and the way that survey was done. That’s what I’m still surprised at.

TB I think there’s a general lack of awareness of what effective marginal tax rates are and how they interact and how high they are at relatively low incomes. The 30% rate, $48,000 is a real problem threshold.

RM I suppose I am a bit surprised that the fundamental features of what’s been great for the New Zealand tax system, reappear as controversies, in the political realm particularly. Like the high tax rate. The problem is that Europe’s got high tax rates and Australia’s got high tax rates. New Zealand trying to wave the flag in favour of the low tax rate component of the BBLR has been a challenge. And I think it’s actually been because our neighbour has high marginal rates. And Europe has been very influential on people like Robertson and so on in my opinion in the sense that they buy into the idea that we can have government spending and taxes at 50% plus of the GDP. I should say that I’m therefore not surprised by it. But I think that’s been the big disappointment, that our rates structure has been allowed to sort of get up, and in a sense it’s part of narrow base, high rate [NBHR] thinking. They don’t realise that with those high rates comes the NBHR concept.

The other thing I just touched on is I kind of worry about the international – the OECD and the EU – devices through which large countries bully other countries. And the treaty networks and the BEPS regime and all that sort of stuff is typically a mask for powerful big countries grabbing money off other countries. And the more that happens, that’s a source of corruption and cancer for me and can ripple down and reach these national tax systems. And we’ve had more of that in the last five years than we’ve ever had before.

RO The OECD stuff is probably more two big elephants fighting, the US versus Europe and we get squashed in the middle.

TB I think that’s why the Global South is pushing back and trying to get the UN involved led by Nigeria and Pakistan which are small economies globally, but giant populations, you’re talking over 400 million people between them. They’re not buying into Pillar two. There seems to be pressure building in that area.

What one proposal from your respective tax working groups would you like to see implemented?

RM That’s a that’s a good question. Sorry to be boring, but I think I came back to the broad-based low rate. For Geof and Robin who know me well, I am a bit of a bore-a-thon drum beater on base principles, and the thing that I’ve seen is the base principle lose a bit of its grip in New Zealand in the last decade. We’ve taken our personal and our trust rate to 39%, which I do not like.

It’s the fiscal stuff that’s that this government is arguing that I don’t accept that it’s necessary for that, but that’s another big debate point about understanding how balance sheet management in government needs to be separated from profit and loss account management. I don’t think that those two aspects of the debate are properly worked through. We should take the longer road and the longer term to fix our debt issues, obviously try and avoid them from happening in the first place. But debt is not necessarily needed to be paid immediately. And not to be factored immediately into tax rate design in my opinion, which is a mistake that we’re currently going through.

GN I’ll be boringly repetitive, but I think the extension of income tax to more realised capital gains on a realisation basis and then using that revenue to recycle, I think that’s got equity efficiency benefits. And I also think it helps in some ways to resolve those high effective marginal tax rates around our productive sector of our economy, labour productivity. So that’s still what I would do if we were able to do one thing.

RO Oh, I still like Rob’s RFRM on residential rental and get rid of all these bright lines, interest deductions and ring-fencing rules. The other one Geof raised was seriously considered by the Labour government under Michael Cullen, was that you pay a million bucks worth of tax and you’ve done your bit and go away. An anathema now, times have changed. That was acceptable then it seems, but not now.

It was seriously considered by the caucus at the time. The idea is you get someone come and live in New Zealand and pay a million bucks and fund a Children’s Hospital. Doesn’t seem to me to be a bad idea.

RM Like a hypothecated tax, Robin?

RO I wouldn’t mind if it was hypothecated for good healthcare for children. I think that would be good.

TB Well, I think we’ll leave it there. I want to thank my guests this week, Sir Robert McLeod, Robin Oliver and Geof Nightingale. It’s been fantastic talking with you all. Thank you so much for being part of this.

[This is an edited part of the full podcast which readers are encouraged to download and listen to at the link at the top of this page.]

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

IMF and Climate Change Commission suggest changes to the Emissions Trading Scheme are needed.

Like a never-ending Groundhog Day, every International Monetary Fund report on the New Zealand economy suggests tax reforms would promote efficiency. For example,

“There is a sense that the asset allocation in New Zealand households has a bit too much emphasis on housing versus other investments. We think a capital gains tax at the margin would help.”

That was IMF Mission Chief Thomas Helbling in 2017.

“…tax policy reforms are needed to promote investment and productivity and growth increase, increase the progressivity of income tax and mobilise additional revenue in response to long term fiscal challenges. To achieve these objectives, reforms should combine comprehensive capital gains tax, land value tax and changes to corporate income tax.”

And invariably the IMF’s conclusions are usually followed by a fairly dismissive response from the Minister of Finance of the day.

In 2002 it was the late Sir Michael Cullen responded to that year’s report: “The IMF’s credibility is not assisted by the fact that it tends to apply the same policy template regardless of the country’s circumstances”. This year Nicola Willis’s retort was “There are some things that are certain in life, death, taxes and the IMF recommending a capital gains tax.”

Associate Minister of Finance David Seymour also weighed in commenting. “I see the IMF again saying, oh, you need a capital gains tax. Every country has one. The only countries that don’t have one are New Zealand and Switzerland. But I say let’s be more like Switzerland.”

However, I’m not so sure that this was quite the zinger he hoped because as someone mischievously pointed out on Twitter, Switzerland has a wealth tax and a $59 per hour minimum wage in Geneva.

Deputy Prime Minister and former Treasurer Winston Peters was apparently not available for comment.

A de-facto capital gains tax – the bright-line test

Now, amidst all of the commentary about the IMF’s suggestions, one of the things that came up time and again is that in many ways, we do have a de-facto capital gains tax, except we don’t call it that. The bright-line test is an example of the approach that we’ve adopted, which has been ad hoc and responsive based on the government of the day’s policies at the time.

As you may recall the bright-line test was brought in with effect from 1st October 2015 by the National Government and it then applied to disposals within two years. In March 2018 the Labour Government introduced a five-year period and in 2021 it was increased a 10-year period. And so, a quite confusing scenario has developed as to which bright-line test applies because some of the exemptions have changed over time as well, particularly in relation to the main family home.

In one way, therefore, the reduction of the bright-line test back to two years again from 1st July is to be welcomed because it is clarifying and simplifying what has become an incredibly complicated area.

Tax Red Flags: More than just the bright-line test to be considered

The bright-line test and taxation of land has plenty of red flags when together with the excellent Shelley-ann Brinkley and Riaan Geldenhuys and moderator Tammy McLeod, I made a presentation about tax red flags on Tuesday to the Law Association. (Formerly the Auckland District Law Society). My thanks again for the invitation to present and to my excellent co-presenters, we had a very lively session talking around this.

In short when you drill into our current land taxation rules, they are very incoherent. The bright-line test is a backup test. It applies if none of the other land taxing provisions apply. And this is something that tripped up people before the bright-line test was introduced and will continue to do so even now it’s been reduced down to two years.

For many people, the particular issue to watch out for is the question of subdivision. If you own a property and undertake a subdivision within 10 years of acquisition it may still be caught under the existing rules, outside of the bright-line test. And in some cases, you may be caught by the combination of the provisions with the associated persons test which deem transactions to be taxable if at the time you acquired the land you were associated with the builder, dealer, or developer in land.

Sometimes the tax charge can be triggered way past the 10-year timetable since acquisition. That’s particularly the case in relation to a disposal of property where building improvements have been carried out. That particular provision, section CB 11 of the Income Tax Act, deems income to arise if a person disposes of land and

“within 10 years before the disposal”, the person or an associate of the person completed improvements to the land and at the time the improvements were begun, the person or an associated person carried on a business of erecting buildings. Note, the reference to “within 10 years before the disposal.” So, you may have owned that land for considerably longer than 10 years and yet still be subject to the provision.

Just a pro tip for anyone thinking ‘Great, with a two year bright-line test coming in, I can now sign a sale and purchase agreement, make sure settlement takes place after July 1st and it’s not going to be subject to the bright-line test.’ That’s not the case. The sale point for the bright-line test in that case is when the sale and purchase agreement is signed and not when settlement happens. I had at least one client get caught by that very provision because they went for a long settlement thinking that got past the two year period. It didn’t, and it is another case of always seek advice on transactions involving land, because as I’ve just outlined, the provisions are complicated.

Could a capital gains tax be ‘simpler?’

And this was the point we reinforced during our seminar. There is a lot of complexity already in our tax system around the taxation of land and in my view, in some ways a capital gains tax would actually clear away a lot of that uncertainty. It’ll become clearer that, broadly speaking, if you buy something, and you sell it subsequently, any gain will be taxable.

Now, how the gain is calculated and the rate at which it’s taxed are two different things. But often in the debate around the capital gains tax, those two things get conflated to run as an argument against the taxation of capital gains.

In my view, the point still remains that we have a confusing hotchpotch approach to taxing capital gains and at some point, grasping the nettle with a CGT as suggested by the IMF and also the OECD, would ultimately perhaps be a better approach.

Incidentally, doing so would be consistent with the well-established principle we have of the broad-based low-rate approach. There’s nothing to say that by broadening the tax base, we could not hold tax rates at current levels or even lower. Bear in mind that the when the last tax working group recommended the capital gains tax, it was intended to keep to help keep the top tax rate at 33%.

Watch out for trustees on the move across to Australia

One of the other issues that came up in our Tax Red Flag Seminar was the question of trustees, and beneficiaries and settlors moving cross-border, particularly to and from Australia. That is something all three of us are seeing quite a bit of and it is something to watch out for as a key red flag.

The IMF on how to tax wealth

If there is a certain repetitiveness to the IMF’s discourse about taxing capital, it’s part of a global discourse on the topic. Earlier this month the IMF released a How to Tax Wealth note. These how to notes are “intended to offer practical advice from IMF staff members to policy makers on important issues.” And this this was a very interesting read as you might expect.

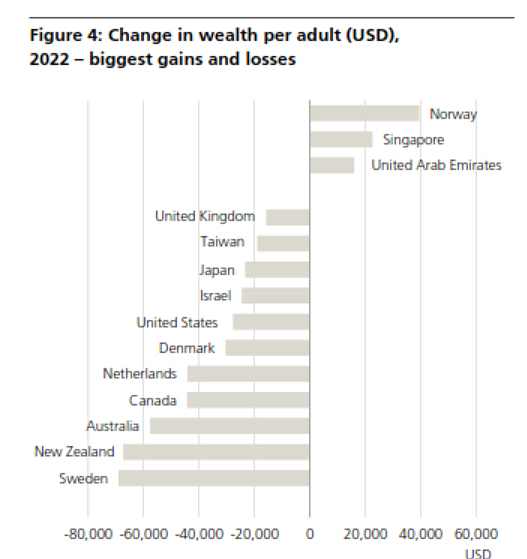

The IMF’s How to Tax Wealth note neatly coincided with the release of the UBS/Credit Suisse, Global Wealth Report for 2023. According to the report, in 2022 New Zealand ranked sixth in the world with an average wealth of US$388,760 per adult. On the basis of median adult wealth per adult, again in U.S. dollars, we ranked 4th behind Belgium, Australia and Hong Kong, with a median wealth of US$193,060.

Incidentally, these rankings were after a very sharp fall from 2021 levels, where New Zealand was only behind Sweden in the biggest loss in wealth per adult.

I am genuinely very surprised to see New Zealand rating so highly for both average wealth and median wealth. On the other hand this Credit Swisse/UBS report is another example of why there’s a great debate going on around the taxation of wealth not just here, but globally.

And this IMF How to Tax Wealth note is instructive in its approach. It starts by making a very obvious point, how much to tax wealth is a distinct question from how to tax wealth. The note argues that:

“returns to capital generally should be taxed for equity and possibly efficiency reasons. and that in many countries, wealth inequality and better tax enforcement strengthen the case for higher effective taxation than in the past.”

Now the IMF doesn’t make any particular proposal about a specific level of tax, the note is basically about ‘here are things you should consider.’ But on the question of wealth taxes, it does come down pretty much against them noting,

“Improving capital income taxes tends to be both more equitable and more efficient compared with replacing them with net wealth taxes. Countries hence should prioritise improving capital income taxation over considering the introduction of wealth taxes”.

Then it talks about – in terms of strengthening capital taxes – addressing loopholes, notably the under taxation of capital gains in many countries. There’s a passing comment, that perhaps you can use a one-off net wealth tax or maybe apply it to very, very high wealth levels.

Time for inheritance tax?

But the Note also concludes “taxing capital transfers through gifts or inheritance provides another opportunity to address wealth inequality.” The IMF comments that the efficiency costs of such taxes are modest, and notes that “inheritance taxes are better aligned with redistribution than estate taxes, since exemptions and rate structures can account for the circumstances of the heirs.”

What really makes the New Zealand tax system unique is not the absence of a capital gains tax because, as David Seymour pointed out, other countries don’t have that, namely Switzerland. It’s the complete absence of taxes on the transfer of wealth, which has been the case now since 1992. That’s what makes New Zealand unique – we have no general capital gains tax together with no estate or gift or wealth taxes.

And this is an area where I think a lot more consideration needs to go into because as the IMF noted, we’ve got fiscal challenges ahead, and where might the revenue be raised from to meet those challenges.

The IMF and Climate Change Commission suggest changes to the ETS

And finally, back to the IMF again. It concluded its mission report by noting that “New Zealand’s ambitious climate goals call for major reforms,” and it referenced the Emissions Trading Scheme, having helped limit net emissions by encouraging robust reductions and removals, particularly from afforestation.

But the IMF then went on to say that “significant reforms” are going to be needed to meet domestic and international targets, and these include reducing the number of available units in the ETS, pricing agricultural emissions and strengthening the incentives for gross emissions reductions within the ETS. The IMF finally note that given the ambition of New Zealand’s first nationally determined contribution under the Paris Agreement, the use of international mitigation i.e.; buying credits from offshore, is likely to be required.

Now the IMF report was a week after the Climate Change Commission, and pretty much said the same thing, and advised the coalition government they should halve the number of ETS units on offer in each of the next six years. The last ETS auction did not go brilliantly. That has a flow on effect in that by reducing the amount of income from emission trading unit sales, it’s going to limit crown revenue for tax cuts.

Vale Rod Oram

It’s interesting to see a confluence of opinion happening here and an appropriate time to remember the late Rod Oram someone who was a very strong environmental journalist. I was fortunate enough to know him all too briefly after we met at a panel discussion. We’d planned on him appearing as a guest on the podcast. Sadly, with his passing that will never happen now, and our thoughts go out to his family and friends.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Plus big changes to the retirement landscape she helped initiate.

She also explains why she was one of the first of the 97 signatories on the Open Letter on Tax.

During her time as Retirement Commissioner, she also helped develop a national strategy for financial literacy that incorporated practical strategies such as the excellent sorted.org website, multimedia campaigns and education in schools.

More recently, Diana was the chief executive of the Wellington Free Ambulance and is presently chair of the Lifetime Retirement Income and several charities. She is also one of the initial 97 signatories of last month’s Open Letter on Tax.

Ki Ora Diana, welcome to the podcast. Thank you for joining us.

Diana Crossan Ki Ora Terry, thank you for having me.

TB Oh, not at all. Enormous privilege and thank you. I’m really fascinated. You’ve got an incredibly distinguished career there. But I’m most fascinated by your time as Retirement Commissioner. Because when I was researching/writing Tax and Fairness and looking at the superannuation savings regime, as it was in 2002, prior to when you took over, it was pretty much ground zero. There was practically little or no incentives to save.

And we know that the numbers of superannuation schemes had basically collapsed from where the numbers that prior to the removal of insane tax incentives in 1988, they had fallen quite dramatically, to I think barely 13% of the workforce was covered about 2002.

So, you come onto the scene, you’re appointed Retirement Commissioner. It must have been quite daunting. What were your thoughts when you volunteered for that?

Diana Crossan You’re right, it was a bit overwhelming initially. And I was the second Retirement Commissioner, the first one was Colin Blair, who was a tax specialist. So, when the government set up the retirement commission, they thought that they were helping the nation. Hopefully they were because we had a superannuation, or a retirement savings system that was very different from the rest of the world, or the OECD world really.

We had New Zealand super, which is of course brilliant, and should be protected and we had private saving. The Retirement Commissioner was supposed to be there to help people understand that they needed to save for their own retirement. That was why it was set up.

And what we discovered – the Retirement Commission was just on to this when I arrived – was that the advertisements and the encouragement and all of the messages they were sending out to people were getting to people who were already looking for it. It was preaching to the converted, really.

And the average age of people they were talking to at that point was about 45 to 50, and the Retirement Commission recognised that that wasn’t going to work. That starting to save at that late stage in your career didn’t work. So that’s how it came about. The recognition that maybe in the 2000s at the beginning of this century, we had to do something very different.

So, they stopped all paper brochures and television interviews and things that focussed on brochures. And the team introduced Sorted https://sorted.org.nz/ and I came in just at that time. And so the focus on financial literacy and on getting to people earlier was the most important thing I picked up when I first arrived.

TB And that’s been a huge transformation there, I take.

Diana Crossan Yes, absolutely. We started off by thinking, how do we do this? You know, this is new. I thought it was very brave of the group just before I arrived. You talked about the national strategy for Financial Literacy.

We were one of the first countries to do that because we recognised that if the government was (and we kept talking to government about other things as well) going to stick with this policy of having a New Zealand super, which was very basic as we know, somewhere between 30 and 40% of New Zealand population live on New Zealand super alone. So first of all, it was that and then it was up to you to say we needed to find ways of talking to people about what to save, how to save, how safe is it. All of the issues in our trustworthy financial services sector, we needed to talk about that. We need to talk about government policy that didn’t get in the way.

So until KiwiSaver came along, we were different from the rest of the world. The countries that we tend to look up to like Australia, Canada, US – well, the US is unusual – the UK and parts of Europe because we didn’t have the middle pillar which is about supported saving by government.

TB Yes, some countries do that by means of very generous tax incentives which were abolished under Roger Douglas in late 1988. So, you were closely involved in the development of KiwiSaver?

Diana Crossan Yes, Michael Cullen approached me to join the team. So, it was an interesting group of people from a variety of government organisations and his statement was “We are going to have a savings scheme. I don’t want this group to come back and say it’s not a good idea because we’re going to have it while I’m in government. What I do want you to do is tell me how to develop that.”

And just before I came into the Retirement Commission role, I had been funded by a businessman and business family in Auckland who asked me to look at how we could help New Zealanders go to university and polytechnic, tertiary education. There were high fees and high interest rates for university students at that time.

So, we had done four years of work about a children’s savings scheme. Therefore, when I was asked to join the KiwiSaver group by Michael Cullen, I was able to take all that work to that. So that included the kick start and included thinking about other ways of doing things.

TB Yes, it’s been enormously successful. Even the FMA Financial Market Authority’s June 2022 report now says that we have $90 billion in KiwiSaver as of 30th June 2022 and over 3.17 million members. And that’s not even 20 years. It’s 15 years max. It’s been transformative.

Diana Crossan It is, however, there are issues with that. As you know, there are a lot of people who don’t know where their money goes or know what kind of fund they’re in. And they might be young and in a fund that’s quite conservative and they could do better to be in the balanced or growth funds, and they don’t understand that.

So that’s what the financial literacy was about. Also, many of them have very low savings in KiwiSaver. And while it will be helpful when they get to retirement, we want people to put more in now so that they have a better retirement when they retire.

TB How do we achieve that? The Tax Working Group in 2018 made a number of recommendations around that. It was suggesting that perhaps we should increase for example, a KiwiSaver member on parental leave would receive a maximum member tax credit even if they didn’t make the full $1042 contributions. And we saw something in the last month’s Budget for that alongside that. But that’s not enough, is it really?

Diana Crossan No. And one of the recommendations I would have made, which was too bold, I think, is that if we want women to have children, and I think we do, and if we want women to have equal opportunity through their career and their retirement, that we do, then maybe we should be thinking about how we help women to keep their KiwiSaver going. We do it with ACC. We keep it going at 80%, so what about keeping KiwiSaver going?

You know, there’s lots of ways of thinking about it, but I think we have to be quite bold in that area because not only are women having time out to have children, but they’re also earning less on average. And so we need to find ways to reduce both of those things. And one would be while you’re on parental leave, your KiwiSaver is put in by the government to even things out. And the other one would be let’s keep pushing for equal pay.

TB Absolutely.

Diana Crossan It makes a difference in retirement.

TB Well, yes, because the thing about retirement is a dollar saved 20 years ago is worth exponentially much more than one saved with ten years to go to retirement. It’s that sort of thing. It’s just volume of savings steadily each year, year in, year out.

Diana Crossan So we’re not good at this, though, because we had a government – I think it closed in 1991 I think – a government savings scheme, a superannuation scheme for its staff. And what was interesting was of course women had unequal pay until the 1960s and some of those women who had unequal pay, when equal pay came in, there was no adjustment in the super.

So they lived out their lives on those savings that were made in relation to the pay at the time. And there was an attempt to tell government that this was completely unfair. Other countries, when they made equal pay rules and legislation, changed the super at the same time so that the women who’d retired by that stage got a better income.

TB Yes, that is still a perennial problem, and it shouldn’t be. As you say, equal pay is closing that gap, which is, what, 13% now?

Diana Crossan Yes, about that.

TB Give or take. Still, closing that gap is vitally important. And we all hear plenty of stories about the shortage of workers and experience. So I think, “Well, guys, we need to address those issues and retirement issues.” And looking at the Tax Working Group, what I liked about what it said in relation to proposal tax incentives, was they were focussed on the lower end.

Because to pick up your point earlier on when you became Retirement Commissioner, the people who should be saving knew they should be saving, were saving anyway. It was getting to those people who weren’t as aware as they needed to be about what they could do.

And so helping that group was what I liked about the Tax Working Group’s suggestions. For example, removing the employer superannuation tax charge on employer contributions below the $48,000 threshold at the moment. What do you think about the tax treatment of KiwiSaver and savings?

Diana Crossan I’m not a tax expert as I said earlier I think. It’s not something I have spent a lot of time on. I think my reason for signing up to the letter was much more about getting more tax, rather than tinkering with what we’ve got at the moment.

You might think, paying women when they’re on parental leave is tinkering. But it’s dear to my heart.

TB I don’t think it’s tinkering. I think it’s something we should be doing.