Last week I discussed the Green Party’s wealth tax proposals, and commented about how what makes New Zealand an outlier in world tax terms is not so much that we don’t have a capital gains tax, but we also don’t have an estate tax, gift tax, land taxes (other than rates), stamp duties and taxes on wealth or wealth transfers, which exist in many other jurisdictions.

This prompted reader kiwikidsnz to respond as follows

It’s a really interesting comment and thank you for that, because it gets to the heart of the issue around tax and how it changes people’s behaviour. Tax is regarded in economic literature as a deadweight cost. Any tax is therefore distortionary, but we have taxes because they pay for things that people like, such as roads, schools, hospitals, infrastructure and pensions, and a whole heap of other services. Accordingly, a key purpose of taxation is to raise the maximum amount of revenue without producing too many distortions and disincentives.

International Monetary Fund on productivity “a significant challenge”

kiwikidsnz’s comments coincided with a report issued by the International Monetary Fund (the IMF) on New Zealand’s productivity challenge. This paper was prepared following the IMF’s visit here in late February and early March as part of their annual review of the New Zealand economy and it does not make for good reading.

As the paper’s opening paragraph notes:

“Weak productivity growth poses a significant challenge for New Zealand’s long-term prospects. Low productivity growth partly reflects structural factors, including New Zealand’s remote geography and small markets, as well as the relatively large role of the tourism and agricultural sectors. However, it also reflects costs and incentives for investment and innovation, which are in turn shaped by features of the business environment and limited financing options.”

Tax is a part of the business environment and as mentioned above the question arises about the distortionary effect of tax. Now the report, and I recommend reading it, is relatively short, but it’s very thorough. But as I said, it’s pretty grim reading because

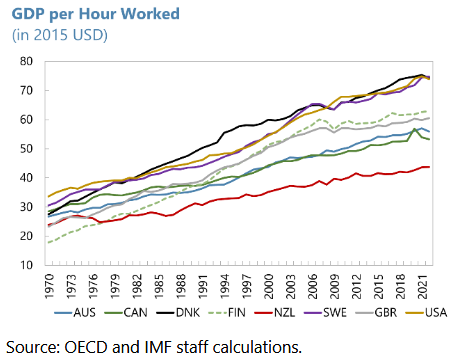

“Over the past five decades, labor productivity growth in New Zealand has lagged that in peer advanced economies, resulting in a widening gap between New Zealand’s GDP per hour worked and that in peers. As a result, by 2022, GDP per hour worked was well below levels in comparable economies.”

A productivity growth challenge across the economy

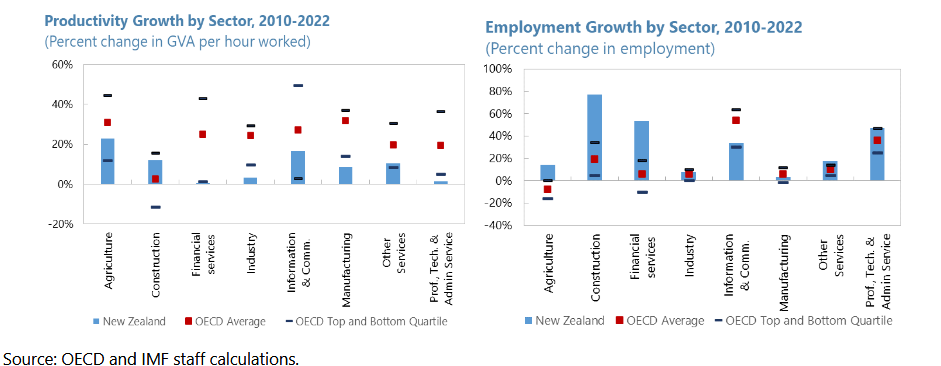

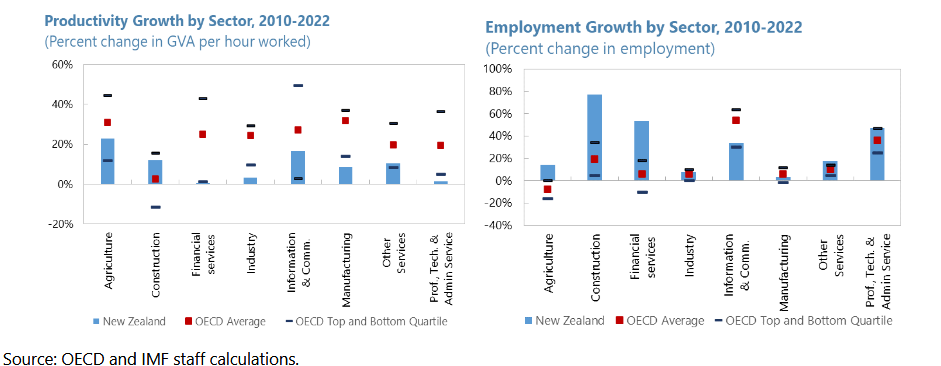

The paper examines this why this has happened and it’s not good reading. A part of the paper that really jumped out at me was paragraph 8 Productivity at the Sector Level. According to the paper labour productivity growth from 2010 to 2022 was below the OECD peer average in agriculture, information and communication (ICT) and some service sectors. In fact

“Productivity growth in New Zealand was in the bottom quartile among OECD peers for financial services, industry, manufacturing and professional and technical service sectors over the same period. The only sector where productivity growth in New Zealand was above the OECD average over this period was the construction sector. New Zealand’s productivity growth challenge thus does not appear to be confined to a few sectors, but to reflect broader issues across the economy.”

Basically, it appears our high immigration has been masking the low GDP per capita growth. ”New Zealand’s workforce has not witnessed the same efficiency gains as workforces in AE [advanced economy] peers (has not been ‘working smarter’), but it has compensated for this with adding more workers at a faster pace.”

Not enough gazelles and too many in the wrong sectors

Another damning part of the report is Section B In Search of New Zealand’s Gazelles. Gazelles are young high growth firms that see 20% growth in sales over at least one three-year period when they are under 10 years, from a base of at least USD100,000. Basically, we don’t have enough:

“Since the Global Financial Crisis, birth rates of gazelles in New Zealand, as a share of all new firms established, have been below the median observed in peer advanced economies. At around 13% gazelle birth rates in New Zealand were below levels observed in Australia, Finland or Sweden, but above levels observed in the Netherlands or Denmark.”

Paragraph 14 of the report I think, gets to where the real problems within our economy have arisen, and where tax may have played a very significant part. It notes young, high growth firms in New Zealand have been concentrated in a few sectors:

“Over 2008 to 2018 new gazelles in New Zealand were primarily concentrated in the financial and real estate sectors. The share of new gazelles in this sector was higher in New Zealand than in most peers, even as the sector saw lower overall productivity growth. At that same time, the share of new gazelles in ICT and professional and technical services, which include hi-tech product, high-productivity sectors dependent on innovation, has been lower in New Zealand than in peers. These trends suggest investment and innovation incentives may be misaligned between sectors in New Zealand. Trends could also be a symptom of the high propensity to save in real estate.”

This is where I think the issue of our lack of capital gains tax and a general lack of capital taxation comes home to roost. The incentives to invest in businesses have been trumped by the investment and lending practises in real estate. I think it was a particularly telling comment here about how those new gazelles, which are a very important part of productivity growth, are primarily concentrated in the financial and real estate sectors.

Replacing one set of disincentives with another

To pick up the issue that kiwikidsnz raised, economic efficiencies do arise from tax policies. Removing incentives such as 66% tax rates and a whole pile of distortionary tax incentives that are given because a government is trying to promote particular behaviour is a good move. But there’s also the disincentives to divert capital if you do not tax something, and it’s is becoming clearer and clearer to me that this is the biggest single problem with not taxing capital gains comprehensively. Coupled with bank lending practices what has happened is we’ve diverted resources into real estate resulting in lower productivity growth and less efficient use of our limited capital. That’s a policy issue that all parties need to consider.

The Australian counter-example

It’s worth talking about the long run implications of the Rogernomics reforms that happened starting in 1984. In October 1985 Australia was also going through its reform period but taking a more measured approach. One of the things it did was to introduce a comprehensive capital gains tax with effect from October 1985. We actually therefore have 40 years of examples to look at what happened around productivity.

Now productivity growth in Western advanced economies has been an issue, but Australia has seen higher productivity over the past 40 years. It has a capital gains tax. We have had lower capital productivity growth, and we don’t have a capital gains tax. Now, correlation is not causation, but there’s 40 years of examples there to make everyone think very hard that maybe in this case correlation does equal causation.

Interestingly, around the whole question of the 1980s idea of supply side economics and cutting taxes to generate economic growth, generally now seems to have run its course, and it probably was always going to do that. Simply because if you’re starting in the 1980s, individual tax rates were then at 60-70% and even more, in some cases. If you’re cutting rates down to 30-40% that’s a significant move and you’re bound to see something happen. But once rates get down to 30%-40%, the impact of tax cuts is less clear.

Meanwhile, in America, maybe not such a Big Beautiful Bill?

What’s really interesting is at the same time as the IMF report came out over the United States) someone who’s been described as the MAGA movement’s top economic guru, Oren Cass, has come out and been very critical of the latest President Trump backed tax cuts included in the Big Beautiful Bill (yes, it really is called that). Mr. Cass is the chief economist for the right leaning American think tank American Compass. He remains the leading proponent of conservative economic populism amongst allies of President Trump.

In talking about the Big Beautiful Bill and the tax cuts that have been included in that, Oren Cass has basically said that the ideas around the Laffer Curve and supply-side theories which have dominated tax policy thinking for the last 40 years have essentially run their race. After commenting “There’s much less confidence in the 1980s-style supply-side tax cutting” he went on

“The reality is we are not going to solve our economic problems if we do not get serious about the fiscal push and fiscal picture and actively reduce the deficit that’s going to require both reduced spending and raising revenue. If you’re not willing to do that, then I don’t think you can credibly say you’re addressing our economic problems.

…Whereas in the past you would have just said, “Well, this thing pays for itself,” This time there is a recognition that it does not pay for itself, — and we have a fiscal crisis — so we also need to explain how we’re at least partly going to pay for it.”

This is an absolutely astonishing admission to hear from a right wing think tank, and particularly in America, which is the home of the supply-side theory.

The thing to keep in mind about taxes, as I said last week, it’s all about politics. But taxes reflect economies and economies change. kiwikidsnz was right to make the comments that there were inefficiencies in our tax system in the 1980s and they were ripe for reform. But it is not a question of set and forget and that’s it, job done, we never have to change again. The dynamics of tax and economies change all the time. And our thinking around that needs to change and reflect that. As a few people pointed out in response to kiwikidsnz we may not have a capital gains tax but other countries do and they have also inheritance taxes, stamp duties, etc and in most cases those peers are wealthier than us. There is 40 years of evidence to suggest that non taxation of capital isn’t actually the economic Nirvana you might think, and it has distorted our economy, particularly our productivity as the IMF notes.

Dr Rod Carr on markets: “myopic, reckless and selfish”

On a related point there was a really interesting leader opinion piece by Dr Rod Carr in the Sunday Star-Times on 1st June. Dr Carr has had a hugely impressive career. He’s been previously chair of the Reserve Bank of New Zealand, worked at Treasury in the 1980s during the Rogernomics reforms and was the inaugural chair of the Climate Change Commission. In summary he has a vast wealth of knowledge about economic policy development in New Zealand over the past 40 years.

His topic was the role and influence of markets. Looking back, after completing an MBA in Columbia University in the mid-1980s, there was little doubt then that markets could allocate financial capital more efficiently than politicians and technocrats and corporate conglomerates. And he believes markets are still, “ruthlessly efficient at allocating privately scarce resources with a price.”

However, he continues markets are “myopic, reckless and selfish,” and understate future benefits and exclude or understate future costs. This results in

“…underinvestment in long-life infrastructure, the degradation of natural ecosystems and under investment in public health and education markets. Markets are reckless because we have created an asymmetry that sees profit accrue to those with private property, while costs are left to lie with the general public.”

He concluded “Markets should be a tool to enable us, not a mantra to enslave us.”

After 40 years, time to think again?

If you combine what Dr Carr said with the comments of Oren Cass and the IMF report on productivity, we’ve now had 40 years of results to look back at how our tax system has evolved and worked in relation to taxation and capital. In my view the long and the short of it is, it hasn’t gone according to plan. Maybe it’s time to look at the script all over again and rethink how we want to have our capital used if we want to start growing a few more gazelles, lift productivity and our living standards.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Last week The Post published a story about Roger and Shaun Nixon, father and son landlords who by The Post’s calculation owned at least 111 residential and lifestyle properties either in person or through a combination of trusts and companies. (In total across various entities and including commercial, industrial and retail properties the pair apparently own over 300 properties across the length of the country from Kaitaia to Invercargill, including properties on Waiheke Island and Omaha, where former Prime minister Sir John Key had a holiday home).

The story was produced as part of The Post’s Mega Landlords series, and I spoke to journalist Ged Cann on the question whether many of the homes in this property empire would ever re-enter the market for sale. As I explained, at the moment there are no tax incentives such as a capital gains tax or an inheritance tax (what we used to call Estate Duties), which could force the break-up of the Nixon’s holdings.

Estate and Gift Duties were first introduced in the 1890s, and were in part designed to provide a relatively good source of revenue for the Government, but they were also a means of breaking down large estates. The Liberal government of the time was concerned about accumulation of excess wealth and the related issue of inequality which drives a lot of discussion in this area. Inequality will exist in any society, no matter what the tax setting settings are. I think it’s a by-product of any modern capitalist society. Some people are extremely able to use their advantages of natural and inherited capital to make fortunes. And by and large, I don’t have a problem with that at all.

The question we should be addressing is how far we are prepared to accept inequality and what strains it puts on our social system. It’s a difficult question to answer. We have seen a rise in inequality since the 1980s and the end of the post-war consensus where higher taxes were seen as means of equalising society. And I spoke to Ged about one of those tax tools used, Estate Duty which disappeared just over 30 years ago.

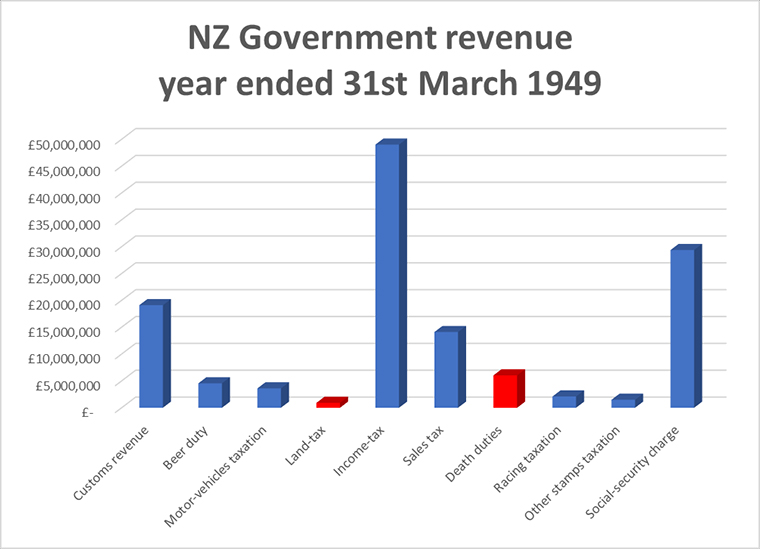

Estate and Gift duties were quite a substantial part of the tax revenue for New Zealand governments for a long period of time after the 1890s, right up until probably the turning point with the election of the First National Government in 1949. For the year ended 31st March 1949 the total amount of land tax, estate and gift duties amounted to just under £7 million of the government’s £130 million revenue. In other words, it was the equivalent of 5.3% of the total tax take for that year. If you were to project that forward, it would be the equivalent of $5.7 billion using the June 2022 numbers. So, these taxes were a very significant proportion of past governments’ revenue.

Whatever happened to Estate Duty?

Starting with the election of the First National Government the exemptions from Estate Duty were widened. This started to undermine the theory we’ve often discussed here and which I strongly support, of a broad based, low-rate approach to taxation. The broader the tax base, the lower the tax rate you can apply. And to a large extent this was the case with estate and gift duties.

But what happened was that exemptions for Estate Duties (and Land Tax) began to be expanded. And therefore, as the exemptions expand, the tax base is narrowing and then the tax take starts to fall away. And gradually, over time, the numbers diminished to the point of insignificance. Land tax was abolished in 1990 and Estate Duty reached its end point in 1992. Gift duties, for whatever reason, lingered on until 2011, before they went on the not on reasonable grounds that the barely $2 million revenue collected was far outweighed by the compliance costs.

The question that should come up is whether, in fact, the abolition of Estate and Gift Duties was a wise move on two points, firstly for maintaining a broader tax base. And secondly around this question of inequality, because Estate Duties are something that can hit estates very, very hard particularly where perhaps too much is tied up in illiquid assets, such as property. This is something I’ve seen quite a lot in the UK with the effect of what is now called Inheritance Tax.

To repeat a point I have made before, the absence of Estate and Gift Duties makes our system unusual because we don’t have a capital gains tax. (We’ve also removed stamp duty although by and large, tax theory has that stamp duties are pretty inefficient taxes. Still, they linger on everywhere else). So, we have no taxes which could be part of breaking down large estates. We have to accept whether that’s a good or bad thing.

Following IAG’s move do we need to broaden our tax base to deal with climate change?

My view is that we ought to be thinking about the question of broadening our tax base. And in that context, I’ve been thinking quite a bit on this question of estate and gift duties, because this week there was another reminder of an issue I keep raising – the growing costs of dealing with climate change.

The insurer IAG announced this week it will not offer ongoing insurance for properties in Category 3 of the Government’s Land Categorisation framework for regions affected by the floods earlier this year.

The cost of the property damage this year by those events is currently several billion and climbing. Of course, property owners are the persons that are most closely affected.

One of the doubts I have about National’s proposed foreign buyers tax is about the type of properties foreign buyers are likely to be purchasing. In Auckland, there is a growing number of suburbs where the average price is $2million. But foreign buyers aren’t necessarily wanting to buy a rundown villa in Grey Lynn or Devonport, they’d probably be looking at flashier properties in coastal areas. However, these coastal properties could now be more exposed to climate change which could be a factor in them deciding not to purchase.

Of course property owners, maybe including the Nixons, have already been affected by climate change and if they are struggling to insure their properties, they will be looking to the Government for assistance with this. And so it seems to me we are rapidly reaching a break point because we’re not taxing capital and property in particular. This is going to create a huge issue between those on one hand who have property and want government assistance when their property is flooded out or damaged beyond repair and insurance is limited or not available. On the other hand, there is a group who don’t have property and can’t get onto the ladder, who will, through their taxes end up paying for the former. This dichotomy sets up a whole social strain, which I don’t think we really want.

To repeat, the thing about this story of the megalandlord Nixons is how it illustrates to me this dilemma we have created around the taxation of capital and the preference for property as an asset class.

So why is the New Zealand Super Fund taxed?

There were some very interesting responses to last week’s commentary about the New Zealand Superannuation Fund’s (“the Super Fund”), retiring CEO Matt Whineray’s remarks on the fund’s tax status. (Thank you again to all my readers and listeners for your contributions). The question was asked, ‘Well, why does it pay tax?’ The answer, as I indicated in last week’s podcast, it was designed as such when the Super Fund was being set up prior to when it actually started investing 20 years ago this month.

“There are two main issues surrounding the tax status of the proposed super fund. The first of these is the tax avoidance opportunities that would be created if the fund was tax-exempt. The second is whether poor incentives would be created regarding investment behaviour.

…By making an entity tax exempt, the government effectively gives it an asset that it can trade with taxable entities. Current tax-exempt organisations such as charities have engaged in complicated schemes to take advantage of this kind of opportunity. …

We consider that making the fund tax exempt will create an opportunity for this kind of avoidance activity.”

The driving force of this paper was concern that giving the Super Fund tax exempt status would give it poor incentives. And so, the fund was set up on that basis. (It’s also interesting to note that the paper assumed the Super Fund would be contracting out most of its fund management activity. However, as we know, the Super Fund is now one of the largest fund managers in the country).

Changing the FIF rules

Back when the Super Fund was being established the tax treatment under the foreign investment fund regime was very different. There was what we call a “Grey list” that applied to investments in several countries such as the US, Australia, UK, Germany, Japan and others. Investments here were only taxed on dividends and capital gains would be taxed under the normal rules, similar to those we have now for investing in Australia and New Zealand. The amount of tax payable on these investment would not have been quite significant under those rules.

However, in 2006, proposals were introduced establishing the current Foreign Investment Fund regime which took effect from 1st April 2007. Now, the interesting thing is that I cannot see any commentary or submission to the Finance and Expenditure Committee by the New Zealand Super about the changes, although there’s plenty of commentary from the Corporate Taxpayers Group and others. As I mentioned last week, some 3,400 submissions opposed the changes, and only two were in favour. So of course, the measure went ahead.

From that point the New Zealand Super Fund started to pay a lot more tax. (In the year to June 2008 the fund had a loss of $704 million but had a net tax bill of $164 million because of the changes to the FIF regime). The effect of the FIF regime was described in a submission the New Zealand Super Fund made in 2018 to the last Tax Working Group. It said it would like to be tax exempt because as I noted earlier it’s the only sovereign wealth fund in the world which is taxed. Its tax status also creates some issues when it is investing overseas. In support of tax exempt status, the submission (signed off by then acting CEO Matt Whineray) noted.

“The fund’s tax position can be volatile depending on the performance of the fund and the contributors to that performance. This is often illustrated by our effective tax rate. For example, our effective tax rate was 3% in 2015, 96% in 2016 and 20% in 2017. The main driver of this volatility is how our physical global equities are taxed under the fair dividend rate regime. In simple terms, this means that in any given year, if our return in global equities exceeds 5%, then our tax rate will be lower than 28%. And if our returns are less than 5%, then our tax rate will be higher than 28%.”

Another interconnected issue for the Super Fund is that as so often is the case, I think Governments rather like the tax revenue from the Super Fund. However, as the Fund’s Tax Working Group submission noted if it was tax exempt it would not be forced to sell assets to pay “the Government provisional tax with the Government then turning around to pay the Fund contributions, thereby removing the need for practical work arounds in terms of offsetting provisional tax”.

As I said, way back in 2000 when they were considering the tax status of the New Zealand Super Fund, the FIF regime was very different. And I wonder whether if they had foreseen the impact of the FIF regime that was introduced from 2007, whether they might have rethought the decision to tax the Fund.

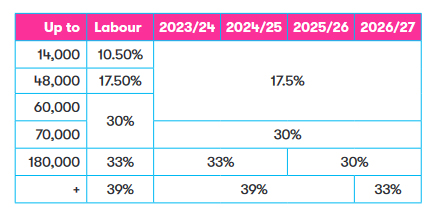

Act is now accepting that cannot happen but instead the top rate from 2026 will be 33%. What it has also said, and this is interesting, is that the top 39% rate will remain until then.

One of the proposals in ACT’s “Alternative Budget” is the Government will stop making contributions to the New Zealand Super Fund. But what won’t change, however, is the tax status of the fund, and it will still be taxed.

Now the ACT numbers are quite detailed, and they note that the expected tax revenue from the New Zealand Super Fund will actually drop by about $100 million over the three years to June 2027 period because of lower Government contributions. (Incidentally, in measuring debt-GDP ratio ACT’s Alternative Budget excludes the $65 billion value of the NZSF which rather unfavourably distorts the ratio).

ACT also proposes winding back the KiwiSaver member’s tax credit (the Government contribution you receive if you make contributions of at least than $1,043 a year), for higher income earners. Instead, it will be capped at 5% of a participant’s taxable income. The maximum subsidy amount will reduce by 3% per dollar of income above $48,000, reducing to zero by around $65,000.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.