We’re racing towards the end of the current tax year. And naturally, at this time of year, tax advisors will be planning ahead and considering what elections we might need to make before 31st March, whether to bring forward taxable income into this year or, if we can, defer taxable income into a later tax year because we are aware that in that new year a lower tax rate will apply.

Right now, I’m discussing these timing options with a number of clients who are thinking about transferring or withdrawing funds from their UK pension schemes. Such transfers/withdrawals are taxable under the foreign superannuation scheme transfer provisions in Section CF3 of the Income Tax Act 2007.

Long-term followers will know that I am not a fan of this regime, but it’s now been in place since 2013. One of my major criticisms with the regime is that it triggers a tax liability for the transferor, even though that person may not be able to access the funds in the scheme to pay the tax. This wasn’t really grasped by most of the industry until after the reforms were put in place.

The Scheme Pays solution

Subsequently, there’s been a long period of consultation between industry specialists and Inland Revenue, and then between Inland Revenue and HM Revenue and Customs (HMRC) to find an answer to this issue. Fortunately, and finally, that answer has now been found and will become effective from 1st April. It’s known as the ‘Scheme Pays’ option, under which the transferring scheme, the receiving scheme (which for UK purposes is known as a qualifying recognised overseas pension scheme or QROPS) will pay the tax on behalf of the transferor, the transfer scheme withdrawal tax.

The benefit of the Scheme Pays option is twofold. Firstly, the tax may be paid from the funds that are transferred. The problem that had existed previously was that HMRC could have treated a withdrawal to pay the tax as an ‘unauthorised withdrawal’ for UK tax purposes, which could come with a 55% tax charge on it. Working through a solution which was mutually acceptable to HMRC and Inland Revenue took some time.

Secondly because a QROPS is a portfolio investment entity the tax rate payable is capped at 28%. The option that now becomes available for people considering a transfer into a QROPS is If they do so, they will pay tax at 28%, which if they’re a higher rate taxpayer – 39% – is a very attractive option.

When to transfer?

The issue now under consideration is whether a person transfers a scheme before 1st April, be taxed at the usual personal tax rates and is therefore responsible for meeting the tax personally. Alternatively, defer the transfer until on or after 1st April and into a QROPS. The deferral will increase the amount of taxable income, but the trade-off is a flat 28% tax charge. There are some clients where that’s an extremely attractive option, and we’re talking about saving tens of thousands of dollars as a result.

There is an argument, in my view, that the tax rate for all transfers like this should have been 28% or linked to the top prescribed investor rate all along, because basically part of the rationale for this regime is countering people getting a benefit from investing offshore.

The transfer scheme withdrawal tax

The individual making the transfer is still liable for determining the taxable amount of the transfer. For example, if it’s $100,000, the receiving QROPS will withhold 28% or $28,000 from the amount transferred and pay it to Inland Revenue. The transferring taxpayer has got 10 working days from the point at which the funds reach the scheme to ask the scheme to pay the tax (‘Transfer Scheme Withdrawal Tax’) on your behalf.

The taxpayer can calculate the taxable amount using either the ‘Schedule Method’, or the ‘Formula method’ if it is available. For many people who are transferring defined benefit schemes, such as UK teachers’ pensions or UK police pensions, they must use the Schedule Method.

It may have taken a long time to resolve but the Scheme Pays option is a good alternative. As I said, it has the potential to save thousands of dollars for some taxpayers. So if you’re considering transferring your UK pension you should get in touch with your local tax advisor.

Changes to banking taxation ahead?

Moving on, in my last podcast I mentioned in passing that the Minister of Finance had made comments about a potential banking review. Subsequently there’s been a couple of stories in the New Zealand Herald and Business Desk on this matter, in particular, Inland Revenue are preparing a consultation document entitled Changes to Tax Rules for Foreign-Owned New Zealand Banking Groups.

the document outlines a series of technical proposals aimed at improving the integrity of the tax system. Apparently, the changes would affect offshore banks that have branches in New Zealand (about 6% of the banking sector by assets according to 2024 figures) rather than locally incorporated banks with which the vast bulk of Kiwi households and businesses engage. While the proposed changes could see banks pay a bit more tax, they aren’t aimed at generating material amounts of additional tax revenue for the Crown.

Although it’s interesting to see this issue under consultation, it represents one of the group of technical issues that Inland Revenue is always mulling over particularly because being the banking sector, there’s possibly quite some large sums involved.

A banking levy surprise in the Budget?

Dileepa Fonseka in Business Desk wondered, whether in fact, there might be some form of banking levy introduced as part of the budget on 28th May. He considered whether such a levy could possibly be tied to the recently established Depositor Compensation Scheme (DCS).

Dileepa notes that in Europe, 17 countries and the United Kingdom have introduced bank levies or financial stability contributions in the years following the Global Financial Crisis. Many were levied on the liabilities banks carry rather than profits and are designed to ensure financial stability and to cover the cost of insuring bank deposits.

It’s possible anything which taxes banks more might be a bit of a vote winner, even if, as experts note, there’s a chance that such levies might ultimately be passed through to customers. Dileepa also makes an interesting comparison with a similar levy which was a surprise sprung by Scott Morrison in 2017 when he was the Australian Treasurer (Finance Minister).

It’s interesting to see the stories circulating in this space. We’ll get more details on the Inland Revenue consultation when it is publicly released, and we’ll discuss it then. Meantime, as I said in the first podcast of the year, we could expect to see a bit of electioneering around a potential bank levy.

Foreign Investment Funds and transitional residents

Finally, this week, there’s an interesting Inland Revenue Technical Decision Summary, TDS 26/01, regarding the opening value of foreign investment funds. It relates to a transitional resident, a person who has either not previously been resident in New Zealand or has been non-resident for at least ten years. Transitional residents generally are eligible for a 48-month exemption from New Zealand income tax on their overseas investment income. But what happens when that exemption period expires?

The taxpayer in the TDS also requested a 31st December balance date, which had been approved by Commissioner. In other words, without saying so specifically, this client is probably an American who must file US tax returns to 31st December. And as the TDS notes, a 31st March balance date means there are high compliance costs because the person has to calculate income for US tax purposes to 31st December and then for our purposes to 31st March.

The taxpayer’s last day of his transitional residence exemption period was actually 31st December 2024. He requested a change of balance date for his tax year from 31st March to 31st December to align with his US filing period. Inland Revenue agreed to the request which means that balance date could be used for calculating hi FIF income. Which is good because that is very handy for many American clients, because of the dual reporting they have to do.

But the other point is that the TDS agreed the opening value for each FIF interest for the purposes of the income year ending 31st December 2025 would be nil, not the value as of 31st December 2024. That means that when applying the fair dividend rate, which is 5% of the opening value and any quick sales adjustments, the opening value would be NIL. Therefore, for the year to 31st December 2025, only the quick sales adjustment calculation will apply in relation to the FIF interests acquired and disposed of during that tax year.

This is an interesting little summary. It confirms a point that some of us had thought was the case, that clients required to file American tax returns could switch to a 31st December year end to help ease compliance. The taxpayer still has to request a change but this TDS indicates Inland Revenue should accept the request.

Still on foreign investment funds, we should hear this week about the final form of the proposed change, allowing taxpayers required to file US tax returns to adopt a quasi-capital gains tax or “revenue account” approach to their foreign investment fund interests, i.e. being taxed on a realisation basis. The Finance and Expenditure Committee is due to report back on 10th March on the Bill and we’ll bring you that news next week.

And on that note, that’s all for this week, I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

a new report on how the tech companies minimise their tax.

and tax agents rate Inland Revenue.

Recently we discussed the Taxation (Annual Rates for 2025−26, Compliance Simplification, and Remedial Measures) Bill which coincided happily with the New Zealand Law Society’s annual tax conference.

Making compliance with the financial arrangements regime easier

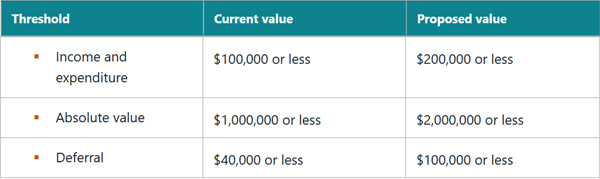

Amidst all the excitement, I overlooked a fairly critical measure in relation to the financial arrangements regime. As regular readers will know, the financial arrangements regime is highly complex, and little known to the average taxpayer. A major issue with the regime is that once certain thresholds are breached unrealised gains and losses must be included in taxable income, i.e. on an accrual basis.

These thresholds have not been amended since 1999 which was the last time there was a serious review of the financial arrangements regime. It’s therefore very welcome news to see a proposal to significantly increase the three key thresholds allowing persons to be treated as a ““cash basis person” and therefore able to return income or expenditure from a financial arrangement on a cash (realised) rather than an accrual (unrealised) basis.

However, Robyn Walker of Deloitte has pointed out the continued existence of the deferral threshold remains problematic. At present, even if the other two thresholds are met, income may still have to be returned on an accrual basis if the difference between income and expenditure calculated on an accrual basis and that under the cash basis exceeds the deferral threshold. In other words, in order to comply with the cash basis method taxpayers are required to calculate and track income and expenditure under the accrual basis.

As Robyn notes the deferral threshold just needlessly complicates matters. (The anecdotal evidence is that its effect is often not realised). She is therefore campaigning for the repeal of the relevant provision requiring the deferral threshold calculation. I fully support her suggestion as bringing about a much-needed simplification. As an aside my personal preference would be for the new thresholds to have retrospective effect from 1st April 2025, rather than 1st April 2026 as proposed.

PepsiCo and Big Tech

One of the papers at the recent New Zealand Law Society tax conference reviewed the Australian PepsiCo case involving what’s called an “embedded royalty”. In this case the Australian Tax Office (“ATO”) said that a bottling agreement for concentrate agreement between PepsiCo and Schweppes Australia Pty Limited involved an embedded royalty and therefore withholding tax was due on a portion of the payments under the agreement.

The ATO won in the initial court case in March 2023, but on appeal and a majority of the Full Federal Court ruled in favour of the taxpayers in March 2024. The case then went to the High Court of Australia which has just ruled 3:2 in favour of Schweppes Australia/PepsiCo.

That would appear to be the end of the matter in Australia but as the paper and session at the New Zealand Law Society tax conference noted, the case remains of interest here. In particular, could our non-resident withholding tax and non-resident contractor’s tax rules apply to part of any payments made to an offshore related party by a New Zealand company.

The PepsiCo decision coincides with the release of a report from Tax Justice Aotearoa entitled Big Tech Little Tax – Tax minimisation in the technology sector. This report examines the publicly available records of the major tech companies in New Zealand to determine how much income tax they are paying and how they are structuring their affairs.

There’s a lot to pick apart in this report. It notes the Government has decided to withdraw the bill introducing a Digital Services Tax (DST) given the Trump administration’s plain declaration that any form of DST would be viewed unfavourably. Inland Revenue had estimated a DST would have been yielded perhaps $100 million in annual revenue.

Targeting the tech giants

The purpose of the paper (written by ex HMRC/Inland Revenue international tax specialist) is

“…to identify practical options to capture a greater proportion of income, including through the application of existing legislation. It argues, for example, that applying the 5% withholding tax stipulated in the New Zealand US double tax aggregation agreement to the service and licence fees of Google, Facebook, Amazon Web Services and Microsoft would have yielded withholding tax revenue of $130 million.”

The paper analyses the various types of fees paid by the New Zealand subsidiaries of companies like Google, Facebook, Amazon Web Services, and Microsoft, and explores whether some of these payments might, in substance, constitute royalties and therefore subject to non-resident withholding tax of 5%. This is where the PepsiCo case becomes particularly relevant, as it provides insight into how such payments might be classified.

The paper analyses the tax practices of the tech giants and their three primary models of tax minimisation: the service fee model, the inflated licence fee model, and the service company model. Facebook, Google and Amazon Web Services appear to use the service fee model involving substantial “service fees” to related offshore companies.

Oracle New Zealand and Microsoft New Zealand use the inflated licence fee model, under which the local subsidiary pays a large percentage of their revenue to offshore subsidiaries for the licensed use of certain intellectual property rights. According to the report in 2024:

“Oracle New Zealand earned revenue of $172.7m but paid licensing fees of $105.3m to an Irish related party, leaving taxable income of just $5.3m. In previous years, the company has disclosed royalties, which, at that time, made up between a third and three-fifths of total revenue.

Microsoft New Zealand earned revenue of $1.32bn but paid $1.075bn in “purchases” to an Irish related party, leaving taxable income of $62.8m.”

It so happens that Oracle in Australia is currently in the middle of litigation with the ATO regarding the sub-licensing of software and hardware from Oracle Ireland to Oracle Australia and whether these should be treated as a royalty. This is a major case as apparently at least 15 other multinationals are facing a similar dispute with the ATO. Inland Revenue (which tends to follow Australia’s lead on transfer pricing issues) will be watching with interest.

A lack of transparency

The paper also discusses MasterCard, Visa and Netflix where we really don’t know what’s going on because there is no publicly available information. At present all three companies meet the requirements to be exempt from publishing financial statements. The paper surmises the three companies utilise the service company model under which “the local subsidiary operates only as a marketing and support service to an overseas group company, while sales or service revenue is booked offshore.”

I agree with the paper’s recommendation that the Companies Act reporting requirements are changed “to require all local subsidiaries of overseas-headquartered companies to file accounts publicly.” The numbers are reportedly quite large for MasterCard and Visa; it’s the commission on $49.5 billion of credit card payments. In the case of Netflix, if it has 1.2 million subscribers in New Zealand then its expected subscription revenue should be approximately $250 million a year.

Overall it appears there is substantial potential profit shifting happening through the use of various fees, some of which could be subject to non-resident withholding tax. As noted above there is significant litigation happening in Australia on the issue and I don’t think the ATO is going to back off on the matter. I do wonder where Inland Revenue is on this and I expect that we will see more chatter and more discussion of this topic.

Tax agents survey results

Finally, what do tax agents think of Inland Revenue? Quite a few times it depends on what we receive in the morning mail and how our clients react. Joking aside Inland Revenue regularly surveys tax agents and it has just published its Tax Agents Voice of the Customer survey results for the just ended 2024/25 financial year.

According to Inland Revenue tax agents “continue to report strong satisfaction with our services. Some of these results are at their highest levels so far:

92% of tax agents are satisfied with their overall experience

95% found it easy to get what they needed, which is a significant improvement

88% trust Inland Revenue.”

Those are all fantastic numbers and very encouraging.

The benefits of answering the phone

Inland Revenue considers these results “reflect our improved responsiveness” which includes that “Over the past six months, many of you have noticed it’s now easier to talk to us on the phone.” Not being able to get through and speak with someone at Inland Revenue has been a sore point for many tax agents.

The reality is that although Inland Revenue would prefer tax agents and the general public interacted online with it, sometimes there is no substitute for a phone call. This is the swiftest way of sorting out any issues resulting from Inland Revenue not processing a transaction correctly. Often a tax agent will come under pressure from a client to resolve an issue swiftly. I think Inland Revenue doesn’t always appreciate that when it drops the ball, we as tax agent cop the flack for it because something we’ve said is going to happen hasn’t been done. It’s therefore encouraging that phone response times have improved.

Tax agent satisfaction with responsiveness on web messages is now 74% up from 70% for the year ended 30th June 2024. I think that’s too low it should be at least 80% in my view. To be fair I think Inland Revenue would want to reach this level too. Satisfaction with consistency of Inland Revenue’s advice was 76% for the year which is down from 79% for the 2024 year. As Inland Revenue notes consistency of advice is important but remains a challenge.

Outside of survey bodies such as the Accountants and Tax Agents Institute of New Zealand, the Chartered Accountants of Australia and New Zealand, and the New Zealand branch of CPA Australia all regularly discuss service delivery and operational matters with Inland Revenue officials. Overall, the survey is a pass mark for Inland Revenue, but areas for improvement remain and it’s good to see it acknowledging this.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week, as part of its continuing drive to increase compliance, Inland Revenue released an updated property tax decision tool.

What this does is help people work out when a property might be taxable under any of the land taxing rules, including the bright-line test. It’s been updated to take account of the bright-line test changes which took effect on 1st July this year.

The growing issue of helping families into housing – what are the tax implications?

Generally speaking, since 1st July, the bright-line test only applies where the end date for sale as determined under the rules is within two years of when the property was deemed to have been acquired. The aim of the tool is to work through all the various scenarios that might apply. So that’s something worthwhile, and I think we’re going to see more of people wanting to make more use of this because of a developing trend around shared home ownership where people who are not necessarily couples are coming together to purchase properties. There are also families wanting to help elderly parents.

We’re seeing some very interesting scenarios develop as a result. One of those scenarios was the subject of last week’s Mary Holm’s column for the New Zealand Herald.

“We’ve bought my wife’s parents’ house. They had a small mortgage on it, with no income, just super, coming in. They didn’t have enough money to keep paying the mortgage, hence they were going to start a reverse mortgage to keep things afloat.

If they sold the house they would’ve struggled to get into a retirement village and stay near family etc. So we bought the house so they don’t ever have to leave – so let’s say they will be there for at least another 10 years.

They pay us $750 rent per week. We took out a 30-year $800,000 mortgage, with just the interest on it at $1977 a fortnight, so we are topping up mortgage payments as the rent does not cover it. We also pay the rates, insurance and any maintenance costs.

How do we treat this in terms of any possible tax or claims as such?”

Mary asked Inland Revenue and me for comment. Notwithstanding that a net loss was foreseeable, my advice was you never always know what the full story is as there may be a detail which for whatever reason, the correspondent has overlooked. The basic approach I took was you should report it. Inland Revenue were much of the same view but noted that any excess deductions would be ring fenced.

As I mentioned to Mary, I think we’re going to see a lot more of this. Because they’re coming from both ends of the generational spectrum. In this case we’ve got the elderly parents wanting to stay near family and then at the other end, young people trying to get on the housing ladder.

Is shared home ownership an answer to housing affordability?

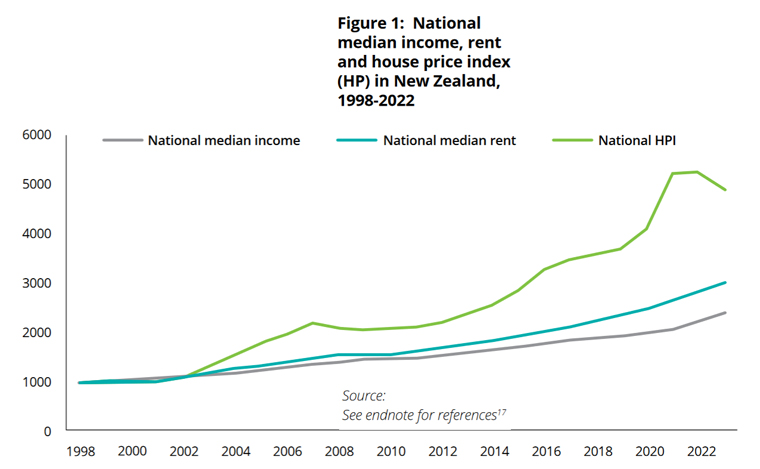

Over the last 20 years or so I’ve seen the practice develop quite rapidly of parents, grandparents and other relatives helping their children or grandchildren get their foot on the property ladder. This was the subject of an interesting report on shared home ownership released by Westpac called Next Step Forward. The report notes that the housing market is increasingly difficult, and “the home ownership dream is increasingly out of reach for some New Zealanders”. The report’s analysis is that shared home ownership will become increasingly common and how might that develop.

The report describes the housing market as “distorted”. To give you some idea of the scale of the problem, the report notes “As of February 2024, the median house price was 6.8 times the median income compared to 5.4 times in 2004 and roughly 2.3 times in 1984.” So over 40 years, the median house price relative to median income has practically trebled.

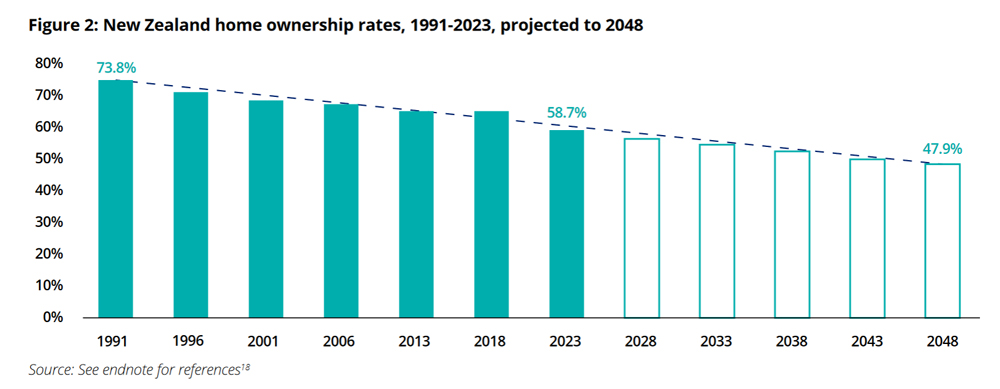

The report also notes that home ownership rates in New Zealand have been declining steadily since peaking in 1991 at 73.8%. They’re down to 58.7%, so a 15 percentage point drop over 30 years is pretty substantial. But the report projects that within 25 years, the proportion of homeowners will have dropped to 47.9%. (The report notes the outlook is even worse for Māori and Pacific peoples, where the home ownership rate is lower, at 47% and 35%, respectively, as of 2023).

What are we going to do about this? Well, as the report suggests shared home ownership is going to become more common. This in turn is going to trigger all sorts of tax issues. Which is why something like Inland Revenue’s property tax tool is handy. The report, incidentally, doesn’t really discuss tax other than mentioning tax free capital gains do play a part in people’s investment decisions and may have an impact on the housing market

There’s no real short answer to this issue. Raising incomes would be one thing, freezing or slowing the rate of house prices would be another, and building more homes would be a vital third factor. Pulling all this together is a huge problem and each solution comes with secondary effects.

International tax deal in trouble?

Moving on, an equally complicated scenario and one we’ve been covering for several years, is the question of the taxation of multinationals. Back in 2021, the OCED/G20 declared a breakthrough international tax deal over the taxation of the largest multinationals in the world. The deal proposed a Two-Pillar solution over the question of taxing rights. Ultimately this is where the idea of a minimum corporate tax rate of 15% emerged.

Agreeing in principle was one thing, but the negotiations have been going on since then and increasingly it seems to be that they’re running into difficulty. A key 30th June deadline has now passed, and it appears that some governments are starting to lose patience with the whole process.

One of the ideas behind the agreement was to head off the implementation of digital services taxes (DSTs). As part of the process these DSTs were put on hold by several jurisdictions, including the UK, Austria, India and others. In the meantime, as negotiations have dragged on, other countries such as Canada have said “Well, we’ve had enough of this, we’re going to go ahead and impose a digital services tax.”

Meantime, the United States whose companies such as Alphabet and Meta are at the heart of the issue have threatened retaliatory tariffs on countries imposing DSTs. Nobody wants a trade war, but someone has to blink in terms of getting a deal past this impasse. So, they’re continuing to negotiate, even though the deadline theoretically has expired.

Time to go back to first principles?

On the other hand, as Will Morris, PWC’s Global Tax Leader points out in this short video. Maybe we should just go back to first principles instead of trying to hammer out a deal through the existing Pillar 1 process which some consider is not really fit for purpose.

It’s not a bad idea but it would delay further progress in the matter, and I think that’s where governments who’ve got elections to win may not be prepared to wait much longer. I think generally the public is a bit antsy about the question of corporate taxation. As I noted last week, when we looked at the OECD’s latest corporate tax statistics, statutory corporation tax rates have pretty much stabilised after 20 years of falling.

However, there are still substantial gaps in public finances as a result of first the Global Financial Crisis, then the pandemic and increasingly we’re having to deal with the impact of climate change as well. When the insurers are leaving the market, who picks up the tab? In my view, that’s going to be we the taxpayers.

There will be pressure to get some sort of deal across the line, but I also think although we may see corporate tax rates elsewhere in the world rise, I think with our 28% rate, we haven’t really got much room for manoeuvre for an increase at this point.

A place where talent does not want to live?

Finally, the New Zealand Institute of Economic Research released a fascinating report on Thursday. Provocatively titled The place where talent does not want to live, it looks at the question of New Zealand’s immigration policy and how that sits alongside our international tax regime.

The report was prepared for the American Chamber of Commerce in New Zealand, the Auckland Business Chamber, the Edmund Hillary Fellowship and the NZUS Council. It’s a fascinating document because it pulls together points, we don’t always hear discussed when we’re looking at immigration policy, how does our tax system interact with that policy?

The report notes that conceptually, we have developed tax rules which make sense in a tax context. However, they lead to wider issues once they start operating in a broader context. In particular the report really focuses on the Foreign Investment Fund (FIF) regime which it considers disadvantages many investors who come here hoping to use their skills and their capital to help build the economy and the tech sector in particular.

I’ve seen comments on this topic previously from entrepreneurs, and it’s easy perhaps to be cynical and say, “Well, they’re speaking out of self-interest” but 40 years of tax experience also tells me that behavioural responses to tax are very observable and policymakers should pay attention to such responses.

An in-depth examination of the Foreign Investment Fund regime

What makes this report particularly interesting are the authors, Julie Fry and Peter Wilson. Julie is a dual New Zealand and U.S. citizen who in her bio notes that “her location and financial decisions have been impacted by the tax rules covered in the report.” Peter was Manager of International Tax at the New Zealand Treasury from 1990 to 1997 and then Director of Tax Policy from 1998 to 2002. As such “He was responsible for advising the government on many of the tax issues contained in this report.” Consequently, outside of anything prepared for a tax working group, this report is one of the most in-depth examinations we’ve seen of our international tax regime and FIF regime.

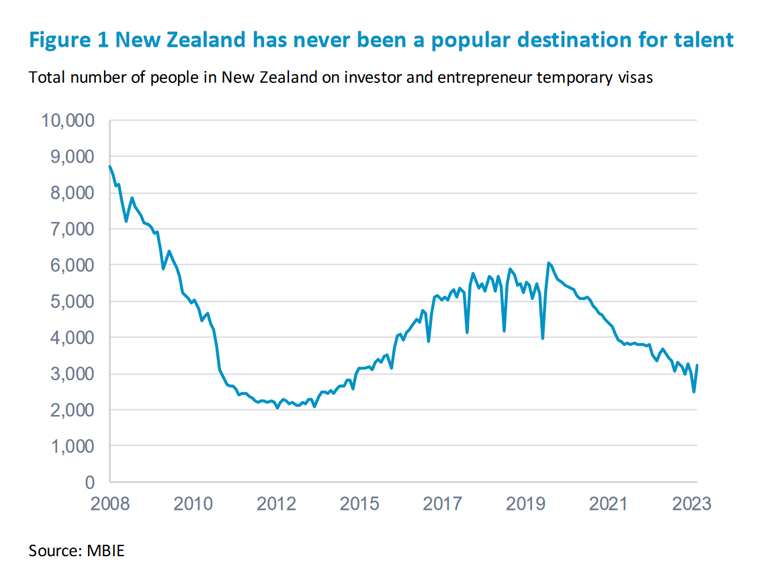

The report notes that although we have a fairly open flow of migrants, “New Zealand has never been a particularly popular destination for talented people”. (Interestingly, we have no data on how long people on the various investor and entrepreneur visas stay).

As the report notes there’s a competition for global talent and New Zealand is not attracting as many as we would like. We should therefore be thinking hard about the implications of this.

The report hones in on the FIF regime as being a particular problem for many investors because of the way that it taxes unrealised gains. This creates a problem of a funding gap where an investor is expected to pay tax on an investment which very often isn’t producing cash because as a growth company cash is being reinvested. (By the way, this is often a common argument against wealth taxes).

As the report notes, “New Zealand’s tax rules were not designed with the idea of welcoming globally mobile talent in mind.” For example, as Inland Revenue’s interpretation statement on residency makes clear it’s deliberate policy to make it’s easy to be deemed tax residency in New Zealand, and hard to lose. This has long term flow implications because as the report points out, people who would perhaps want to commit to New Zealand are reluctant to do so because of the tax consequences of doing so.

Chapter Three is the very, very interesting section of the report as it explains the development of our current international tax regime and the rationale for the various FIF regimes and their design. The overall objective was to protect the tax base, but they didn’t really think about what was happening with migrants. As Ruth Richardson and Wyatt Creech then the respective Minister of Finance and Minister of Revenue explained in 1991:

“The objective of the FIF regime, where it applies, is to levy the same tax on the income earned by the FIF on behalf of the resident as would be levied if the fund were a New Zealand company. Because the FIF is resident offshore with no effective connection with New Zealand, the only way of levying the tax is on the New Zealand holder.”

This is conceptually correct from a tax perspective but as the report keeps pointing out, it doesn’t really take into account what happens with migrants who made investment decisions long before they arrived in New Zealand only to find their accumulated savings are being taxed here under the FIF regime. I have a similar problem with the taxation of foreign superannuation schemes. Although the tax treatment conceptually ties in with our system, it seems to me we are effectively taxing the importation of capital and this paper is basically saying the same thing in relation to FIF.

How much tax does the FIF regime raise?

Section 3.5.1 on page 26 of the report has an interesting analysis of how much revenue the FIF regime raises. Because our tax reporting statistics aren’t very detailed, the answer is we don’t really know. The report concludes

“The high-level finding is that the level of overseas investment is small compared to total financial assets at the national level. Portfolio foreign investment is, in some years, one-thousandth of domestic investments. This suggests that the current FIF tax base is likely only to make a minor contribution to direct revenue.”

A suggested reform

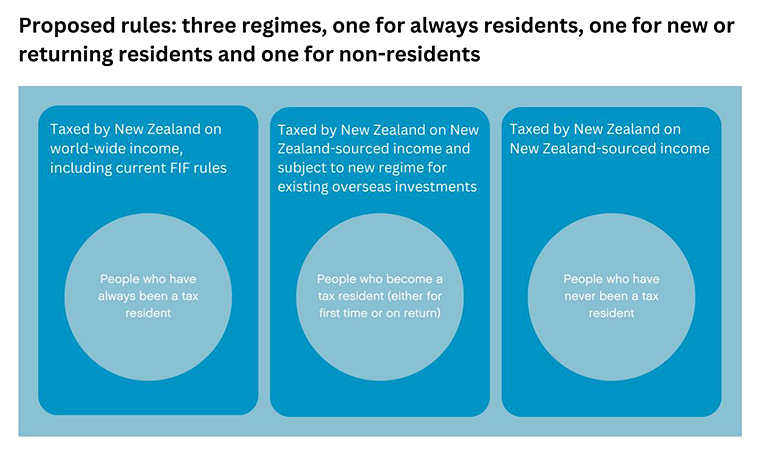

The report concludes that in an international context where we were trying to attract the right talent, maybe we should be looking at the FIF regime. What it suggests is to separate the tax treatment of people who have always been tax resident from those of new and returning tax residents. The existing FIF rules would continue to be applied to those have always been New Zealand tax resident. Meantime a new regime should be designed for new and returning tax residents.

The report does touch on the question of a general capital gains tax regime (which could be an answer) but considers the development of a comprehensive CGT is a long term political consensus building project.

In discussions I’ve had with other colleagues on this matter we’ve noted how our American clients in particular are very affected by the current FIF regime. As American citizens they are required to continue to file American tax returns and are therefore subject to capital gains tax. This creates a mismatch between when they pay New Zealand income tax and the final US tax liability on realisation. Although the FIF regime creates foreign tax credits for US tax purposes, clients are frequently not able to utilise the foreign tax credits.

As people told the report authors this is extremely frustrating and there is no doubt that people are upping sticks and moving because of it. (I’ve also seen other clients switch into property investment instead).

Overall, this is a very interesting and highly recommended report considering the intersection of tax driven behaviour with wider economic issues.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week, the OECD/G20 announced a new multilateral convention had been agree in relation to Amount A of Pillar One of the international tax agreement.

Pillar One is the part of the international agreement which allocates the taxing rights to market jurisdictions with respect to the share the profits of the largest and most profitable multinational enterprises which are operating in that jurisdiction’s markets, regardless of whether or not the multinational has a physical presence.

This multilateral convention is also intended to ensure the repeal and prevent the proliferation of digital services taxes and other similar measures. Based on 2021 data, the OECD/G20 estimate that this should result in about US$200 billion of profits being reallocated each year. This should represent an approximate additional corporate income tax of about between US$17 and 32 billion.

Although the convention has been signed, we’re still working forward towards the actual final detail and agreement on the application of Pillar One and for that matter, we’re also working forward on the application of Pillar Two. This multilateral convention, by the way, extends to perhaps 800 pages so you can see the level of detail involved.

Yeah, but are we getting there?

You may think we’ve heard this sort of announcement before, and we have. What’s happening is the framework of how the final international agreements will operate is being put into place very slowly. But, and it’s a big but, are we actually going forward and is an agreement on the cards? And that’s where a fair bit of scepticism is starting to develop amongst those in the international tax community who deal with international tax issues day in, day out. (I have to be honest that most of this stuff involving the multinationals is way above my pay grade).

There was a particularly interesting article this week on the matter by Rasmus Corlin Christensen, a political economist at the Copenhagen Business School.

In short, he is highly sceptical of exactly what progress is being made on this and whether, in fact an agreement is as close to agreement as is being touted by the OECD/G20.

His blog post discusses the history of the Pillar One and Pillar Two process from when it started about ten years ago. He notes the tensions that have arisen around the agreements, like all tax, comes down to politics. As he explains, the initial drive for an agreement came from the French, and the Americans have been pushing back because it’s their multinationals that are most likely to be taxed. Although, as he rather wryly notes, Ireland has a big part to play in this because that’s where quite a bit of the profits from larger multinationals such as Apple, for example, are centred.

It’s a good read explaining the whole topic and but he thinks ultimately what will happen is that various pressures will build on the topic as the political posturing and manoeuvring goes on between the Americans and Europeans. But Christensen also points out that emerging nations, in particular Nigeria, the largest economy in Africa, are starting to push back wanting to see some progress.

The concern is if no agreement is reached then the Americans have already indicated as they did so under President Trump, that they will deploy trade weapons and tariffs. No one wants a trade war and that’s where Christensen thinks that this may force the issue bringing about some form of agreement.

Quite apart from the Europeans and Nigeria he also noted that Canada has broken ranks by going forward with a digital services tax. You may recall that just before Parliament rose for the election, the Labour government introduced a digital services tax. This is a fallback in case the Pillar One and Pillar Two negotiations don’t proceed.

But if you’re reading between the lines here, from what Rasmus Corlin Christensen is saying, it’s quite possible that we’re going to need that. And as he notes,

“But there’s really nothing puzzling about Canada’s move, or the proliferation of digital taxes globally. International corporate tax policy has risen to the top of national and global political agendas, with governments individually and collectively asserting their authority against the forces of globalization – a significant shift from years past.”

And this, by the way, fits in with how I see tax policy internationally developing, the era of low taxation globally and corporate tax in particular is over. Governments’ balance sheets and finances, including our own, are under strain. Everyone is looking under all available rocks as to what funds might be available.

Christensen’s article is well worth a read with a different perspective on international tax away from the sort of “rah rah rah it’s all great” messaging coming out of the OECD/G20. He focuses on the politics, but doesn’t necessarily see that this deal isn’t going to happen, it just may happen in a different way than is presently planned.

Good news on the Foreign Investment Fund front?

Still on the subject of international tax, Inland Revenue released an interesting Technical Decision Summary in relation to the ability to change foreign investment fund (FIF) calculation methods. This is a private ruling where the applicant has interests in a number of foreign trusts, unit trusts and companies subject to the FIF rules and the attributable FIF method. The taxpayer hadn’t filed a tax return at this point and they wanted to apply for a ruling as to whether in fact they could change methodologies under the FIF rules.

In certain situations, taxpayers can change their FIF calculation methodology between the fair dividend rate and the comparative value. However, in other circumstances and other entities a taxpayer must apply the fair dividend rate. This is an interesting ruling because it gives clarity around this issue and that and on the basis of these facts, and everything is always be very fact specific, you can change methodologies.

The big caveat I would add here is that a critical fact may well be that they hadn’t actually filed returns because there’s been a bit of controversy about Inland Revenue saying that if a return has been filed adopting one methodology, then you can’t adopt a subsequent change in methodologies in most circumstances. And I just wonder whether that was a factor in this ruling. It’s not a formal Inland Revenue ruling, so it may well be converted to one subsequently. But still, it’s interesting to see some guidance on an area where there’s a bit of controversy developing.

Is a Financial Transactions Tax really worthwhile?

Early in the week, I spoke about how the New Zealand Loyal party had campaigned on a financial transactions tax (FTT) as a replacement for income tax and GST. The last Tax Working Group had looked at the question of a financial transaction tax and come down against it. Generally speaking, no one is overly sold on the idea, but it is something that frequently pops up in discussions or when I’m in public forums. It’s sometimes called a Tobin Tax after the economist who dreamed up.

The idea behind a FTT is the fact that there are vast sums of money flushed through financial systems and on the basis of the good old principle of broad base, low rate, a very small charge on this could raise significant sums of money.

It so happened in reading on the topic, I came across a new working paper by Gunther Capelle-Blancard of the University of Paris’ Centre for Economic Studies of the Sorbonne. The paper takes a fresh look at the whole question of financial transactions tax and particularly looks at what happened with Sweden’s tax which failed badly, and that of France which introduced one in 2012. The French financial transactions tax hasn’t gone as well as expected, but even so, it’s still raising close to €2 billion after nearly ten years of implementation.

The French and Swedish experience

Two main objections to a FTT are firstly, it will encourage displacement, people will take their activity and trade elsewhere outside that jurisdiction. Secondly, people will reduce the volume of transactions to mitigate potential charges. According to the paper there certainly appears to have been a reduction in the volume of transactions happening.

But the displacement activity, which was a big problem for the Swedish financial transaction tax, so much so it was abandoned, doesn’t appear to be the same issue for the French because it’s better designed on that. The key difference being that under the French system it is the nationality of the company that issues the shares, which is subject to the to the financial transaction tax and not that of the counterparties or intermediaries carrying out the transaction. In Sweden, it seems what happened was the activity which would have been done by Swedish stockbrokers, was instead performed outside the country and therefore no financial transaction tax applied.

What about Stamp Duty?

But the other thing that I thought was very interesting and I hadn’t actually considered it beforehand was that Capelle-Blancard has also looked at the example of Stamp Duty on financial transactions. This still applies in the UK at a rate of 0.5% on all share transactions. When you take a broader view, stamp duty is a financial transactions tax. It doesn’t apply as broadly as those proponents of a FTT would want, but it still applies. In the case of the UK stamp duty on share transactions has applied since 1694 and raised £4.37 billion for the year ended 31st March 2022. We repealed stamp duty in 1995 if I recall correctly.

This is an interesting paper, well written and quite understandable, which takes a different perspective on a topic which has been pooh poohed on reasonably strong grounds. But a FTT may actually not be as impractical as has been mooted. What I would say is even if it’s more practical to implement than people have said there is no way that it would ever replace income tax and GST, as the New Zealand Loyal party promoted and many people think it can do, because you would have to impose quite a high charge on transactions. And you would then very definitely see a large displacement/reduction in activity.

The paper notes some absolutely eye watering numbers about the growth in the level of financial transactions “Since the 1970s, global GDP has multiplied by 15 times, market capitalisation by 50, and the amount of stock market transactions by 500.” In France, for example, the total amount of transactions in the Paris Stock Exchange has grown from €3.5 billion in 1970 to over €2,000 billion today.

These absolutely eye watering numbers are why people think a FTT could raise a lot of money. The paper estimates a FTT could raise perhaps as much as between €156 and €260 billion annually, based on a nominal rate of 0.3 or 0.5 per cent. I think people will still look at the idea with some scepticism, but in fact as the paper notes, and I didn’t realise, FTTs are more widely spread than many might realise.

The Election’s over, now what?

Finally, the Election is over, and we’re now waiting to see the exact composition of the Government and what involvement Winston Peters and New Zealand First may have. What does that mean for tax? Well, we will have to wait and see. The expectation is there will be some form of tax threshold adjustments coming up starting from 1st April next year and obviously rollback of the rules around interest limitation for residential property landlords.

But I would just point everyone to the example of the New Zealand First National Coalition Agreement in 1996. National went into that election having already implemented a set of tax cuts which took effect from by sheer coincidence of course, on 1st July 1996, just before the election. There was another round of tax cuts to follow shortly afterwards. But under the agreement that was eventually hammered out, which made Winston Peters, Treasurer/Finance Minister, the second round of tax cuts was delayed for a year.

I’m therefore just wondering whether Winston and New Zealand First might just have a look at the books and say, “Ah, maybe not this time”. And of course, you’ve also got Act on the other side saying, “We want to see some movement on this pretty quickly.” So ,the new Government and the expected Prime Minister, Mr. Luxon, have got some negotiations ahead, which might turn out to be trickier around this issue than we’d all first imagined.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.