controversial Inland Revenue proposals for shareholder loans hit a major roadblock

The Finance and Expenditure Select Committee has reported back on the Taxation (Annual Rates for 2025-2026, Compliance, Simplification and Remedial Matters) Bill. This Bill contained measures in relation to changing the tax treatment of non-resident visitors who are working remotely while visiting New Zealand, introducing the new Revenue Account Method for calculating foreign investment fund income, plus the usual host of other amendments tidying up various issues.

The amendments to the tax treatment of New Zealand visitors are designed to encourage people to work here remotely without triggering too many adverse tax effects. One change proposed relates to disregarding the activities of a non-resident visitor present in New Zealand when determining whether a company is tax resident in New Zealand.

Watties, Heinz, tax and a Lions legend

This is a long-standing point and with Watties being in the news for all the wrong reasons, I recall an interesting point raised way back in the 1990s when Watties was acquired by Heinz, the international food manufacturing giant. Apparently, Tony O’Reilly, the former British Lion and then chairman of Heinz, was in the country at the time the deal was being finalised. Did this mean Heinz had a permanent establishment in New Zealand because key decision makers were here?

Tony O’Reilly in action against the All Blacks in 1959

That was a somewhat mischievous question. But it is an example of where key personnel being in a country may trigger unintended and adverse tax consequences. The Bill tidies up a number of issues relating to this as well as clarifying the treatment of remote working by non-residents.

No major changes to the Revenue Account Method proposal

When the bill was introduced, much fanfare was made of the proposed Foreign Investment Fund (FIF) Revenue Account Method. This allowed an eligible person’s FIFs to be taxed on a realised gains basis with a discount of 30% applied to the gain resulting in an highest effective tax rate of 27.3% (i.e. 70% of 39%).

This was seen as disappointingly high so many submissions on the Bill requested a higher discount to reduce the effective tax rate. These have all been knocked back on the basis that the maximum rate of 27.3% is broadly comparable to the 28% payable under the PIE regime.

But there are some minor mostly technical changes. For example, losses arising under the Revenue Account Method were initially to be ring-fenced and only available against future gains. Any such losses will now be available to offset against dividends from the same interests. So that’s a bit of a win.

And there is the ability also to allow taxpayers to sometimes use other method calculations which are required at present rather than and not lose their eligibility to apply the revenue account method to other interests. In other words, you can sort of split treatment on that. So generally, the rules are a progression, but I think you can read when you get into reading the fine printing, you sort of see the technical minutiae and issues that pop up because of the complexity involved.

There was an interesting, there’s also a proposal for essentially there’s a realisation tax on migration, and a point has now been clarified that If this happens, the calculation of any tax payable, because someone has used the revenue account method and then migrated out of New Zealand, they would use the market value of the interest at the time the person departs New Zealand, not the market value received when the interest is subsequently disposed of.

Quick example, a person leaves New Zealand when the market value of one of these interests is say, $500,000, subsequently sells it and realises the market value of $1,000,000. Any New Zealand tax payable will be based on the 500,000 being the market value at the time they left.

Don’t look the parents are squabbling…

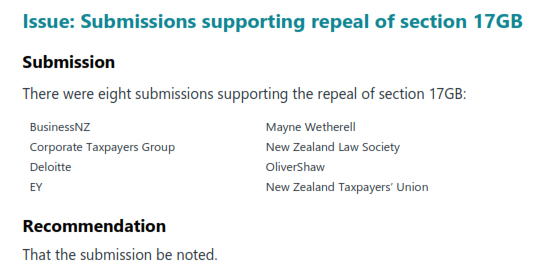

There was a nice little spat between the various parties on the committee over the proposal to repeal the Section 17GB of the Tax Administration Act 1994, which allows the Commissioner to collect information for the purpose relating to the development of policy for the improvement of the tax system. This was the measure introduced under the last Labour government, which was then used as the basis for finding the information for Inland Revenue’s controversial 2023 High Wealth Individual Review. Unsurprisingly Labour and the Greens opposed its repeal as did 202 submissions (including for the record Baucher Consulting, and the Chartered Accountants of Australia and New Zealand). Eight submissions supported the repeal.

Information sharing risks?

Labour was also opposed to the provision expanding the ability to allow Inland Revenue to share information about individual taxpayers with other government agencies more easily by way of Ministerial agreement. The Labour Party MPs made this very valid point,

“While Inland Revenue has strict rules about which employees may access information about individual taxpayers and it polices those rules rigorously, the same protocol may not apply in other agencies.”

Indeed, Inland Revenue, to the best of my recollection, has never had issues where someone has emailed out a spreadsheet full of confidential details which we’ve seen both the Ministry of Social Development and ACC to name a couple of culprits do. The Labour Party also noted “This is a significant change to the rules that protect the privacy of taxpayers’ information. We note the Office of the Privacy Commissioner has concerns about these proposals.” Despite this the provision is to go into effect.

Financial arrangements – three welcome surprises

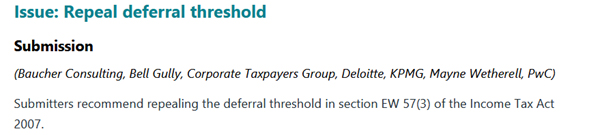

A big and welcome surprise relates to changes to the financial arrangements regime. Under the financial arrangements regime if certain thresholds are exceeded taxpayers must calculate income and expenditure on an accrual, or unrealised, basis rather than on a cash, or receipts, basis. These thresholds had not been increased since 1999, and the bill proposed to double them.

The regime also has a deferral threshold which means income and expenditure must be calculated on an accrual basis (unrealised) if the difference between calculating income on a cash (receipts) basis and the accrual basis exceeded $40,000 at any point. This applied regardless of whether a taxpayer’s total financial arrangements were under the $1 million threshold. Unsurprisingly, this deferral threshold frequently tripped up taxpayers (I even once saw advice from a Big Four firm which had overlooked its impact). I was one of several submissions recommending repeal of this threshold.

Inland Revenue has accepted our submission noting the deferral threshold

“…imposes a high compliance burden, requiring taxpayers to calculate income and expenditure on an accrual basis to compare it with a cash basis result and ensure that the difference is below a threshold. This is the same compliance burden that being a cash basis person is intended to avoid.”

This is an excellent result.

But wait, it gets better

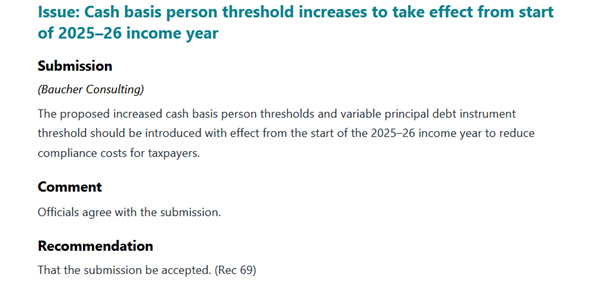

Under the Bill the increased thresholds were due to take effect from the start of the 2026-27 income year (1st April for most people). Adopting the principle of you don’t ask, you don’t get, I also submitted the threshold changes should be effective as of the start of current tax year (i.e. 1st April 2025). This would reduce compliance costs for the taxpayers, one of the key objectives of the Bill.

To my great surprise and delight, that was accepted as well, which is another excellent result.

But wait, there’s more…

KPMG made a very sensible submission that foreign currency loans used as mortgages over property should be removed from the financial arrangements rules and calculations. Exchange rate fluctuations can mean the deferral threshold is breached making any unrealised foreign exchange gains taxable. This once happened to one of my clients resulting in a tax bill of over $100,000.

Although Inland Revenue did not accept KPMG’s submission in full, it proposed instead “limiting the effect of foreign exchange fluctuations for the absolute value threshold”. This would be achieved by testing the absolute value threshold (now $2 million) is tested using the principal amount converted at a set date, for example, the first day of the financial arrangement, and ignoring subsequent foreign exchange fluctuations. If the principal amount changes for non-foreign exchange rate, reasons i.e. increases or decreases in borrowing, the financial arrangement should be reassessed for the threshold.

A bit late for my client perhaps but still a good result. The three change are also good examples of the Generic Tax Policy Process in action resulting in sensible law changes.

Controversial shareholder loan proposal halted

Moving on, late last year, Inland Revenue dropped what I described as a bombshell, with a consultation proposal for significant changes to the treatment of shareholder loans. Inland Revenue proposed that shareholder loans above a certain threshold would instead be treated as dividends, similar to the treatment for Australian and UK taxation purposes.

These proposals have hit a major roadblock with opposition from Winston Peters and New Zealand First together with the ACT Party. The end result is that the proposals as put forward in December will not be proceeding. Instead, Inland Revenue will continue to review the issue of the treatment of outstanding shareholder loans when a company goes into liquidation owing tax.

The proposals were quite controversial but the same time there was something of a tacit acceptance that yes, perhaps something needed to change. Simultaneously, there were concerns that Inland Revenue was perhaps muddling two issues. One of the issues was that companies that went under often sometimes owed substantial sums by shareholders, and in some cases, this meant Inland Revenue was missing out because funds were paid to shareholders instead.

John Cantin, former guest of the podcast, and also the independent advisor to the Finance and Expenditure Committee on the current tax bill has made public his submission to Inland Revenue on the shareholder loan proposals. His view is that more information is needed on the interaction between outstanding shareholder loans and company failures and the composition of the tax debt of such companies. If it is mostly GST and PAYE? Then yes, maybe that is something to be considered. He also thought there was merit in looking at changing the tax treatment of what happens on liquidation.

The upshot is we’ll be going back for round two of consultation. It’ll be interesting to see what comes out of this. Like John I think changes around what happens when a company is put into liquidation are sensible and also around keeping records of what we call available capital distribution amounts and available subscribed capital.

Property flippers – what about the tax impact?

And finally, an interesting story from RNZ about a complaint to the Real Estate Authority about a rise in so-called ‘property flippers’ making six-figure returns from unwitting vendors. Property data firm Cotality has noted a rise in significant rise in what’s called contemporaneous sales, with the number happening last year was almost double the total for 2024.

In a contemporaneous settlement, a property flipper makes a purchase offer with a long settlement period and then finds another buyer to purchase the property on the same day the property flipper has to settle their purchase. If it all goes to plan the property flipper makes a quick gain.

According to iFindProperty co-founder Maree Tassell who has complained to the Real Estate Authority about the practice:

“It’s quite common that there are some deals out there where people are making over $100,000-plus on contemporaneous settlements, getting a property under contract. The poor old vendor, and even often the vendor’s agents will think ‘oh this is a real purchaser’. …It’s quite deceptive to the vendors and quite deceptive sometimes to the agents.”

Although tax isn’t actually discussed in this story, these transactions would be considered a taxable trading activity even if they are not specifically within the bright-line test rules. It’s the sort of activity Inland Revenue should be watching with great interest. Property flippers should therefore beware, you may be making a quick buck, but Inland Revenue will be tracking these transactions. If you are not declaring the income, then you could find yourself with a big please explain somewhere down the line.

And on that note, that’s all for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

Inland Revenue uncovers over $150m from property sector.

Five suggested changes to the tax system compliance.

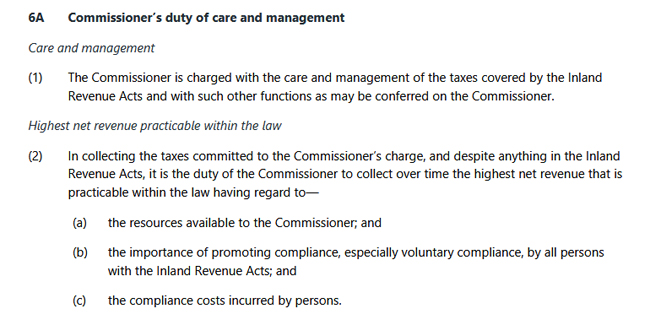

Early last month, Inland Revenue issued a draft interpretation statement The Commissioner’s duty of care and management under Section 6A of the Tax Administration Act 1994. This is a largely unchanged update of the previous interpretation statement issued in 2010.

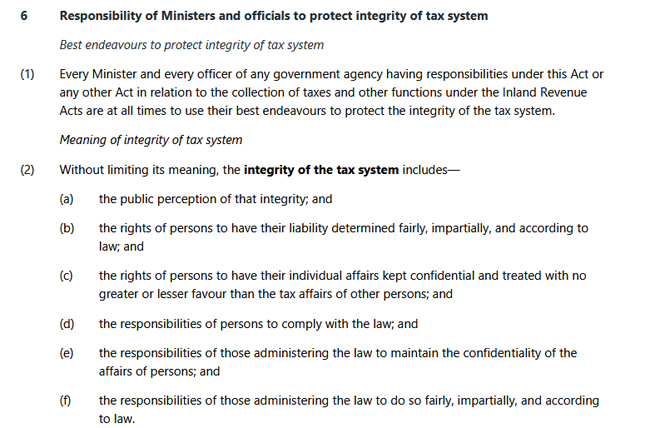

This might sound a little arcane, but Section 6A, and the related section 6 of the Tax Administration Act are, in my mind, two of the most important sections in the tax legislation. As the interpretation statement puts it, “these are important provisions governing the day-to-day operation of Inland Revenue and the exercise of the Commissioner’s power of the under the Inland Revenue Acts.”

So, what are these provisions? As you can see Section 6 requires Ministers and officials to “protect integrity of tax system” including “the public perception of that integrity.”

Section 6A then sets out the Commissioner’s duty of care and management.

What does “care and management” mean and why are these provisions here? The opening two paragraphs of the interpretation statement explains it as follows:

“A reality of modern tax administration is that the Commissioner must operate the tax system with limited resources. This means the Commissioner cannot always collect every last dollar of tax owing in every case. As a result, the Commissioner must decide how to best use his resources to maximise the taxes collected and to foster the integrity and effective functioning of the tax system.

The Commissioner’s resource allocation and management decisions can affect the integrity of the tax system, including taxpayers’ perceptions of that integrity. What one taxpayer may consider as flexibility that achieves a practical and sensible outcome, others may consider as inconsistency or favouritism.”

What has this got to do with Mickey Mouse?

Setting out the history as to how this section gets here is very interesting, and that’s where Mickey Mouse comes into play. It might be no surprise to find out the actual origins of Mickey Mouse’s involvement in our tax system go back to the UK and a case known as the Fleet St Casuals[i] case.

This was a decision by [the British] HM Inspector of Taxes to reach a settlement with casual workers in the Fleet Street printing industry who had not been compliant with meeting their tax obligations. Instead the workers had “engaged in the process of depriving the Inland Revenue of tax due on their casual earnings.”

As part of this the casual workers had falsified their identities and addresses when collecting their pay so that HM Inspector of Taxes could not assess and collect tax due. Apparently, Mickey Mouse of 1 Sunset Blvd was a regular worker and there were several similar such aliases employed. When the HM Inspector of Taxes investigated, they found there was around 6,000 workers who had not been compliant at all, and many of them had provided false addresses. Chasing down every amount of tax due was impracticable. So, a settlement was reached.

When this became known it attracted the ire of the National Federation of Self-Employed and Small Businesses, and they took a case against the Commissioner of Revenue, on the basis that they were being unfairly discriminated against. The Federation sought out a writ of mandamus to basically compel the Commissioner to assess and collect all taxes properly owed.

The case eventually reached the House of Lords, who held that the Commissioner had a “wide managerial discretion under Section 1 of the Taxes Management Act.” It was therefore within the exercise of the Commissioner’s care and management to reach settlements, even though not all the tax due would be collected.

The Organisational Review of Inland Revenue

Back in 1981, when the House of Lords decided the case, there was no such equivalent provision in New Zealand. During the overhaul of our tax system in the 1980s and early 1990s, the Valabh Committee concluded that a similar measure was needed. Subsequently an organisational review of Inland Revenue was carried out by a committee chaired by Sir Ivor Richardson, the late great tax jurist. This was a highly important review if now somewhat lost in the mists of time.

The Organisational Review’s 1994 report concluded a similar discretion to that of the UK was needed and this led to the introduction of sections 6 and 6A of the Tax Administration Act. (The Organisational Review also prompted a substantial overhaul of the dispute process which is another story).

The thrust of Section 6 and 6A is Inland Revenue has some discretion about how far it can use its resources to collect tax, but in doing so it is bound by keeping the perceptions of the integrity of the tax system. A key point that is repeatedly made clear is that discretionary care and management does not mean that Inland Revenue can override or ignore tax law that exists. Nor do sections 6 and 6A give the Commissioner of Inland Revenue the ability to issue what might be called extra statutory concessions.

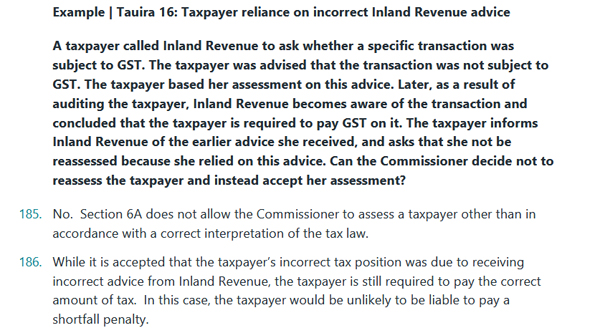

The interpretation statement includes a useful appendix setting out the history of the provisions. There’s a separate handy reading guide accompanying it as well for those who want to avoid wading through the full 59-page consultation. As is now common, the interpretation statement contains 17 examples illustrating how the Commissioner might use his discretion. This example will sound familiar.

The response given in the above example is what I would expect to see. Although it addresses the issue of a shortfall penalty, what about use of money interest? Would the Commissioner have discretion to remit that interest? The example doesn’t cover that, but it’s something that a taxpayer might raise an objection about. Obviously, everything is fact dependent and Inland Revenue may be able to point out that key facts were not provided at the time of the initial inquiry.

As I said, this is a highly important document. Even though the practical effects on day-to-day taxpayers may not seem significant, it’s good to see it updated.

What about Inland Revenue mistakes?

On the other hand, I have to say that the emphasis on Section 6A does overlook the question of whether operational practices of Inland Revenue may be a breach of Section 6. In other words, Inland Revenue does something operationally, which may be correct under the law, but actually is highly disruptive to taxpayers because it failed to process matters promptly or incorrectly.

What happens then, and also regarding the matter of costs that are incurred by the taxpayer? How does that affect the integrity of the tax system or taxpayers’ perception of the integrity of the tax system?

This is an interesting area and one where I think we ought to see more case law involved. But as this updated paper points out, there have only been four tax cases since 2010 where there has been some reference to section 6A, so it is yet to be tested. Consultation is open until 26th May

Inland Revenue’s clampdown on the property industry

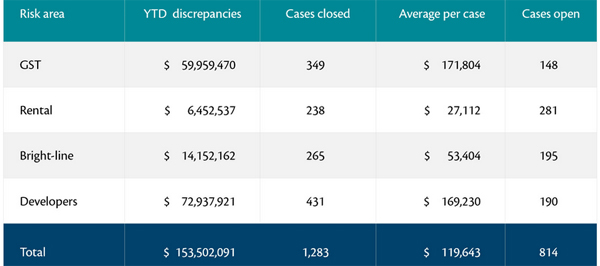

Speaking of Inland Revenue and reassessments, last week Inland Revenue released a press release proclaiming its latest success in the clamp down on under-declared income and GST.

According to the press release, it has uncovered more than $150 million in undeclared income tax and GST from the property sector. This initiative is part of the additional $116 million funding given to Inland Revenue in last year’s budget. According to the press release, the $153.5 million discrepancy for the first nine months of the current financial year is almost the same as the total $156.8 million figure for the whole of the year ended 30th June 2024.

Now, there are four risk areas identified here. GST, rental, bright line and developers. The majority of the discrepancies relate to GST and developers.

Defaulting developers under increased scrutiny

The press release also revealed Inland Revenue is focusing on defaulting developers because

“…we’re also seeing a pattern of property developers claiming significant refunds as they incur costs upfront but then failing to file and pay once properties sell.

Where we expect a GST payment from a property sale and we don’t see the sale in the return, we contact the developer to make enquiries.

If there is no response or no return filed, we will take enforcement action quickly.”

This is unsurprising and will be an ongoing project. As noted above, Inland Revenue got $116 million over four years in last year’s budget. I would expect it to get more in this year’s budget, but who knows at this point?

Five proposals to improve the tax system

Last month I had the very great privilege of speaking to Inland Revenue’s Policy Advice Division. They asked me to present to them some of my insights about the tax system and on communicating tax policy. It was a fascinating session around those wide-ranging topics. The Q and A session was particularly interesting and entertaining. Again, my thanks to Inland Revenue for inviting me along. It was an enormous privilege to speak to you all. I thoroughly enjoyed it, and I hope you did too.

Now, one of the questions was “if you’re in charge of tax policy for a day, what changes would you propose?”. I put forward the following five proposals.

Number one – introduce a capital gains tax

Firstly, I would introduce a capital gains tax, and I would do so as much for economic efficiency and clarity as for raising revenue. I don’t accept the argument that it’s too complex. Anyone who looks at the Foreign Investment Fund and financial arrangement regimes, both of which trip up experienced taxpayers and practitioners, can’t honestly be saying a CGT would be too complex.

At present there’s a large part of our tax system, particularly in relation to property transactions, that contains some rather subjective definitions around a person’s intent or work of a minor nature. Those are subjective terms and perhaps unsurprisingly, in my experience non-tax specialists people tend to think tax should be pretty much cut and dried. It is therefore surprising for them to discover there is so much potential subjectivity involved.

But I also think that when you consider how our economy has developed over the last 40 years leading to over investment in property (in my opinion and that of economists such as Bernard Hickey and Associate Professor Susan St John), then trying to shift the allocation of capital away from investing in property would be a good thing. I’m not saying capital gains tax would solve that issue overnight, but it would be a start.

Number two – time for the “Fair Economic Return”

My second suggestion would be the fair economic return (FER), which is something that I’ve talked about before which I’ve developed alongside Susan St John. How it operates is that above a certain threshold, a set percentage will be applied to the net value of a person’s residential property. I see this alongside a capital gains tax as a twin track approach to address the issue of better allocation of capital.

Furthermore, as the Tax Working Group noted in its discussion of the deemed return method (on which FER is based), it would initially raise more revenue than a CGT, and we need to raise revenue. The Government’s books are clearly under strain, and this will increase. That was something I talked to Inland Revenue Policy about where I saw the strains manifesting. Cost cutting is part of managing the books, but in my view, tax increases are inevitable.

Number three – mandatory indexation of income tax thresholds

The suggestion I have, and this has been a bugbear of mine for quite some time, is automatic indexation of income tax thresholds. To me, this is primarily about transparency and addressing the issue of fiscal drag (when inflation pushes taxpayers into higher tax brackets).

Fiscal drag has been a tool which governments of both hues over the past 30 years have been very happy to use to disguise the actual tax take. It led to the position we saw last year, where in the first threshold adjustment since 2010, the adjustment was limited to inflation since 2017. In other words, a lot of inflation gains were locked in.

I think there’s a lack of transparency about this process and it doesn’t just extend to income tax thresholds. It also extends to other income tax thresholds, in particular around the financial arrangements regime which have not been adjusted since 1999. It doesn’t apply to GST, however, because I think there are different issues involved with the GST threshold.

These thresholds wouldn’t need to be changed annually as happens in the United States, but they could be changed no more than three yearly or when a threshold, say 5% inflation, has been breached. The key thing is these threshold changes would happen automatically unless the government of the day specifically legislated otherwise. If a government decides not to increase thresholds this decision goes through the regular Parliamentary legislative process and the government must then explain its decision.

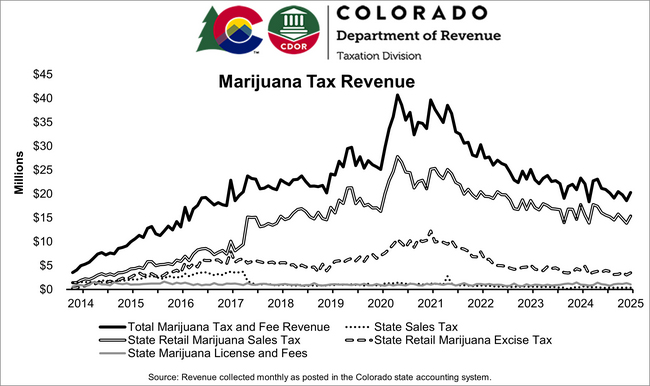

Number four – legalise and tax cannabis

I don’t smoke, but around the world there has been a trend to legalising/decriminalising cannabis. The present criminal status of marijuana enables its supply to be captured by organised crime syndicates and those of you who know crime history will know that it was tax evasion that got Al Capone busted.

I think legalisation of cannabis is something that should happen and could be a useful revenue raiser. To give an example, Colorado, a state of about five million people, legalised cannabis in February 2014 and since then, its total tax collected has been over US$2.9 billion, roughly NZ$5 billion. In the year to December 2024, it collected US$255 million, about NZ$440 million.

Granted, the tax take from marijuana in has been falling in recent years. But that’s because other states are legalising it as well. If I was Nicola Willis, I’m not sure I’d want to leave a potential $400 million plus per year lying around.

Number five – time for a Tax Ombudsman

Finally, I would establish a tax ombudsman and a tax advocate for small businesses and small taxpayers. This is a more administrative issue, but it’s based on a report I was lucky enough to prepare for the Tax Working Group in 2018.

A tax ombudsman is common in other jurisdictions. For example, when preparing my report for the Tax Working Group, I spoke to the then Inspector-General of Taxation and Tax Ombudsman of Australia. It could be a standalone office, or it could be part of the Ombudsman’s office. Either way, it would give taxpayers a second right of complaint against improper practises as they see it, by Inland Revenue. In that way it ties into our main story this week about Inland Revenue’s duty to preserve the integrity of the tax system.

The tax advocate together with changes to the dispute process would redress the imbalance between Inland Revenue and smaller taxpayers. Something I raised in my presentation to Inland Revenue, is that for a very litigious subject, we actually don’t have many tax cases going through the courts (something Supreme Court Justice Glazebrook has also noted). I consider in many cases Inland Revenue wins because it is playing with a loaded deck. This is the result of the changes following the Organisational Review Committee. I think 30 years on from that review its time we had another look.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

This week, Inland Revenue published a reminder aimed at tax agents that clients must have a taxable activity in order to be registered for GST.

The notice said if your client is filing regular GST refund returns with expenses consistently more than their income, it may suggest they are not carrying out a taxable activity or have errors in their GST returns.

Inland Revenue then notes that clients “may receive a letter if they have filed regular GST refund returns from registration.” Tax agents are advised to “please review the refund returns filed and if required take any necessary action”. Inland Revenue then add that letters may be sent to clients who have been filing regular GST refund returns in the last 36 months.

If anyone receives such a letter their response will be expected to include one or more of the following:

a description of the taxable activity or activities undertaken and an explanation for the regular GST refunds.

A voluntary disclosure to correct any errors in the GST returns,

Cancellation of the GST registration if they are no longer carrying out a taxable activity. The final GST return should be filed with the required adjustments.

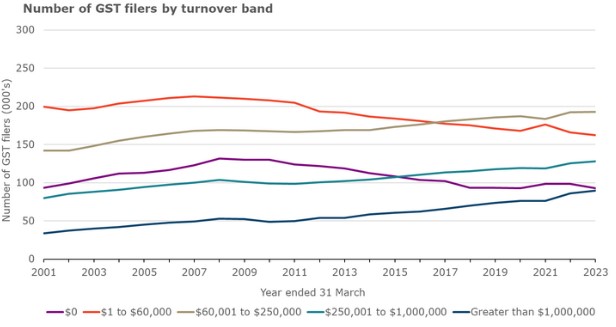

Inland Revenue are clearly about to run a campaign on this issue. Based on Inland Revenue’s statistics during the year ended 31st March 2023 there were just under 100,000 GST registered persons with nil turnover. (About the same number as have turnover exceeding $1 million). There’s another 160,000 or so who have a GST turnover of between $1 and $60,000.

According to Inland Revenue the net GST refund paid to GST registered persons with turnover below $60,000 has increased from $463 million in the March 2001 year to $1.473 billion in the March 2023 year.

Clearly Inland Revenue has looked at this and thought “How genuine are some of these GST registrations?” It will probably be looking at some of the lifestyle blocks that I’ve encountered with some grazing income, but the expenses of running outweigh the grazing income. Inland Revenue looks to be gearing up for a campaign to review those such clients in some detail. We’ll track to see what happens on this and give you updates as and when information emerges

When is a subdivision project a “taxable activity” for GST purposes?

Moving on and still on the matter of GST, and actually on the question of carrying on a taxable activity, Inland Revenue has just released a draft Question We’ve Been Asked (QWBA) for consultation on when is a subdivision project a taxable activity for GST purposes.

Following the 1995 Court of Appeal decision in Newman, Inland Revenue had issued a Policy Statement on this issue.

Under the Policy Statement whether a subdivision project is a taxable activity for GST purposes depends on the facts of each case. Determining this takes into consideration factors such as the scale of a subdivision, the level of development, work time and effort involved, the amount of financial investment and the commerciality of the transaction. Based on this the general view was if a person carried out a subdivision involving three or four sections, it was likely to not represent a taxable activity for GST purposes.

28 years on, it’s not unreasonable for Inland Revenue to come back and look at the matter again. In the draft QWBA the Commissioner considers most of these factors are still relevant when considering whether a subdivision is a taxable activity. However, the draft clarifies and, in some respects, differs from the previous Policy Statement.

According to the draft QWBA in determining whether a subdivision represents a GST taxable activity “the most relevant factor will generally be whether the activity is carried on continuously or regularly. This Question We’ve Been Asked focuses on this factor.”

Following on from this, paragraph 29 of the draft states,

“Generally, the Commissioner considers the level of development work involved in the construction and sale of a single house or other residential dwelling as part of a subdivision is not on its own enough for an activity to be considered carried on continuously or regularly.”

On the other hand, the construction and sale of multiple residential dwellings or a large commercial building is more likely to be continuous or regular. This is an interesting change in tone since 1995. But also, when you think about it, the change reflects how generally speaking, it has become easier to subdivide. Certainly, in Auckland if not necessarily everywhere, it has become easier to subdivide.

Clearly, Inland Revenue is seeing a lot of activity in this space. And the question is then arising, well, at what point does a simple subdivision become a GST taxable activity? Hence this updated QWBA.

As I mentioned a few minutes ago, there was always a sort of general conclusion from Newman that maybe three or four lots carved off would not be a taxable activity. But as the draft notes, there’s no specific number of lots created that determines whether a taxable activity exists. Our case law indicates that where a subdivision activity involves the creation and sale of multiple lots, it MAY be a taxable activity. But it doesn’t necessarily mean a subdivision involving creation and sale of multiple lots will always be a continuous activity because, for example, a subdivision is so straightforward that the number of lots sold is not significant, but it does in revenue.

But…a single section could be a taxable activity

Paragraph 32 of the draft notes although an activity leading to the supply of only one section will not usually be considered an activity carried on continuously or regularly, “this does not mean an activity leading to one supply can never be a taxable activity”. It could be that if other factors are sufficiently present, such as the scale of the subdivision or the level of development work. This will be this will indicate the activity is continuous, even if it leads to only one supply. For example, the construction and sale of a single commercial building on subdivided land would be an activity carried on continuously and regularly.

Changes from previous policy

The previous policy referred to the commerciality of the project as a factor but Inland Revenue have now decided that commerciality is no longer significant. In addition, there was an example in the previous Policy Statement where the construction and sale of a tea shop on subdivided land would represent a taxable activity. However, this draft QWBA now considers that building a tea shop would not normally involve more activity at work than that involved in constructing a residential building and therefore would not meet the criteria to be a taxable activity.

No GST, but what about income tax?

The draft also adds a reminder that although it is focused on GST, even if a subdivision activity is not a taxable activity for GST purposes, the resulting sale may still be subject to income tax. This might perhaps be under the bright line test. But there are other provisions that specifically deal with subdivisions carried out within ten years of acquisition. A useful reminder that although a transaction might not be within the GST net, it could well still be subject to income tax.

A few examples

There are some good examples at the end of the draft QWBA. It’s just worth repeating again that the material being put out by Inland Revenue is much more accessible than it was in previous years. The draft contains a good example about a basic subdivision then, which would not be a taxable activity because it’s not carried on continuously and regularly.

Example four illustrates the GST issues where a subdivision is part of an existing taxable activity. Now this is a question that does pop up quite regularly in my experience. In this case, Loammi and Marissa are GST registered as a partnership with a taxable activity of residential property development. They buy dilapidated houses and renovate them to sell for a profit.

In this example they realise they could make a larger profit on a particular piece of land by subdividing before sale. And therefore, even though the subdivision and sale would not be a taxable activity on its own, in this case the sale of the subdivided land is a taxable supply because it was done in the course of furtherance of their existing taxable activity

Overall, this draft QWBA is probably a good warning for anyone considering subdividing property, maybe carving off two, three or four sections, and thinking that that would not represent a GST taxable activity. This view is no longer so clear cut. Like much of tax it’s fact dependent. It’s also another good example where it pays to get good advice beforehand, otherwise a nasty GST surprise could be awaiting.

Foreign Investment Funds – a welcome change of heart from Inland Revenue

Finally, a few weeks back I discussed an interesting Inland Revenue Technical Decision Summary about which methodologies must be used to calculate income under the Foreign Investment Fund (FIF) regime. Under the FIF regime individuals and trusts may switch between the fair dividend rate, which applies a flat 5% to the opening value of a persons FIFs or the comparative value, which looks at the gains, losses and income during the year.

However Inland Revenue had suggested this could not happen where people were making voluntary disclosures of FIF income for prior tax years, something I see quite frequently. Inland Revenue’s proposal was this ability to change methodologies was not available and all taxpayers making voluntary disclosures would be required to adopt the fair dividend rate.

This prompted a fair bit of pushback from quite a number of advisors, including myself. I’m pleased to say that Inland Revenue has now issued an updated draft QWBA on this matter. The updated QWBA notes the Commissioner accepts that taxpayers have a choice of methods to calculate income, even if they fail to declare the income in a tax return and later file a voluntary disclosure or fail to file a tax return by the due date and later provide one including the FIF income.

This updated QWBA is another example of the Generic Tax Policy Process working with Inland Revenue taking on board feedback from advisers. It’s a good result for taxpayers. I was concerned that if Inland Revenue adopted a harsh approach on this, then people would just simply stay in the undergrowth and hope that Inland Revenue never noticed them. And that’s not good for the tax system at all, where you’ve got people who are become compliant and feel that they are unfairly penalised for doing so. Meanwhile other non-compliant persons see this and decide to just take a chance on not being caught in the first place. This is never a wise approach in my view.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

New Zealand has undoubtedly entered a slowdown economically and that’s flowing through to lower tax receipts leading to claims this week of the Governments being in a big fiscal hole. According to the Companies Office’s latest statistics for the quarter ended 30th June 2023, there were 461 liquidator appointments in the quarter.

That’s 47.8% up on the 312 for the same quarter last year.

As Professor Lisa Marriott noted in an article late last week, the ripple effect of companies going into liquidation is considerable, particularly for unpaid suppliers and employees. Her research suggests that Inland Revenue could be doing a lot more to share information about businesses that are failing. According to Professor Marriott Inland Revenue is actually less proactive than some comparable overseas government agencies such as the Australian Tax Office.

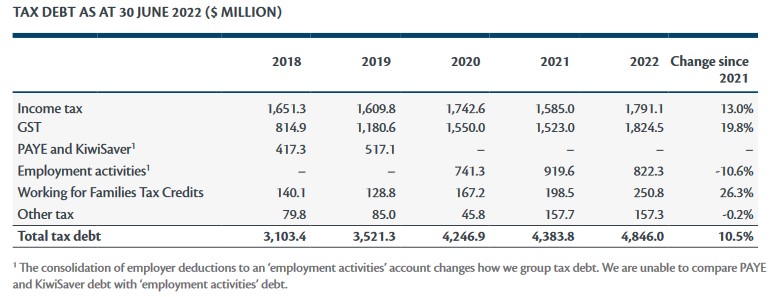

Inland Revenue initiates more than 60% of liquidations in the average year, and that sometimes happens after quite a considerable period of non-payment of key taxes such as GST and PAYE. For example, $2.6 billion or over 54% of the $4.8 billion owed to Inland Revenue as of 30th June 2022 represented GST and what it terms “employment activities” (i.e. PAYE and KiwiSaver contributions).

(Inland Revenue June 2022 Annual Report)

Professor Marriott’s research points to non-payment of these particular taxes as being a very early warning sign of businesses running into trouble. Picking up overseas initiatives she suggests three particular responses could be adopted here to help businesses be aware that a particular business they may be dealing with may represent a credit risk.

For example, in Ireland, Revenue Ireland produces a quarterly list of tax defaulters which identifies the name, address, occupation and the amount of tax owed. This is triggered when the debts exceed €50,000 or approximately $90,000.

Another option would be as the Australian Tax Office does, to advise credit rating agencies that a business has tax debts. This happens if the amount owed exceeds A$100,000 and is more than 90 days overdue.

A third option and one the Tax Working Group looked at, is following another Australian initiative and making business directors personally accountable for unpaid tax through Director Penalty Notices. These are issued in relation to the Australian equivalent of PAYE, GST and KiwiSaver. Once a Director Penalty Notice has been issued, it can only be cancelled by full payment of the tax debt within 21 days or some other action such as commencing winding up proceedings. If no action is taken, then the director becomes personally liable, effectively sidestepping creditor protection and limited liability issues.

These are sensible suggestions, but in my view perhaps another thing Inland Revenue could do would be to be much more proactive in managing debt, particularly in relation to GST and PAYE. I occasionally get involved with helping taxpayers who have fallen behind with their tax payments. And there’s invariably a couple of common points in every case.

Common problems with tax debt

Firstly, Inland Revenue’s present policy of charging interest and late payment penalties doesn’t seem particularly effective to me. In fact, arguably, I’d say it counterproductive.

Debt builds up very quickly and consequently, at a remarkably low level somewhere between $10 and $20,000, the taxpayers often just feel defeated and basically give up. At this point they haven’t engaged with Inland Revenue and all they see is just the amount owed going up and up and up resulting in a sort of death spiral procrastination spiral.

The second common factor in dealing with clients in this scenario is that the situation has been allowed to carry on and develop over a long period of time. These businesses have been going through a slow decline before Inland Revenue finally steps in and decides either to liquidate it or impose some other form of action to recover the outstanding amounts.

One of those actions is the use of “Deduction Notices”. These enable Inland Revenue to go to a customer of a defaulting taxpayer and require them to withhold a certain percentage of any payment they may make to the defaulting taxpayer, and instead pay it over to Inland Revenue. Most often Deduction Notices are issued to employees and often in relation to unpaid child support. But they can be used in other circumstances. In one case I saw a Deduction Notice applied was 100%, although I’m not entirely certain what was meant to be achieved by issuing such a notice.

Adopting the measures suggested by Professor Marriott would take some time to go through the full consultation and legislative process. Although these are tools Inland Revenue perhaps could consider adopting, given the current rise in liquidations, I consider it needs to be taking action sooner rather than wait for these additional options.

Harden up Inland Revenue?

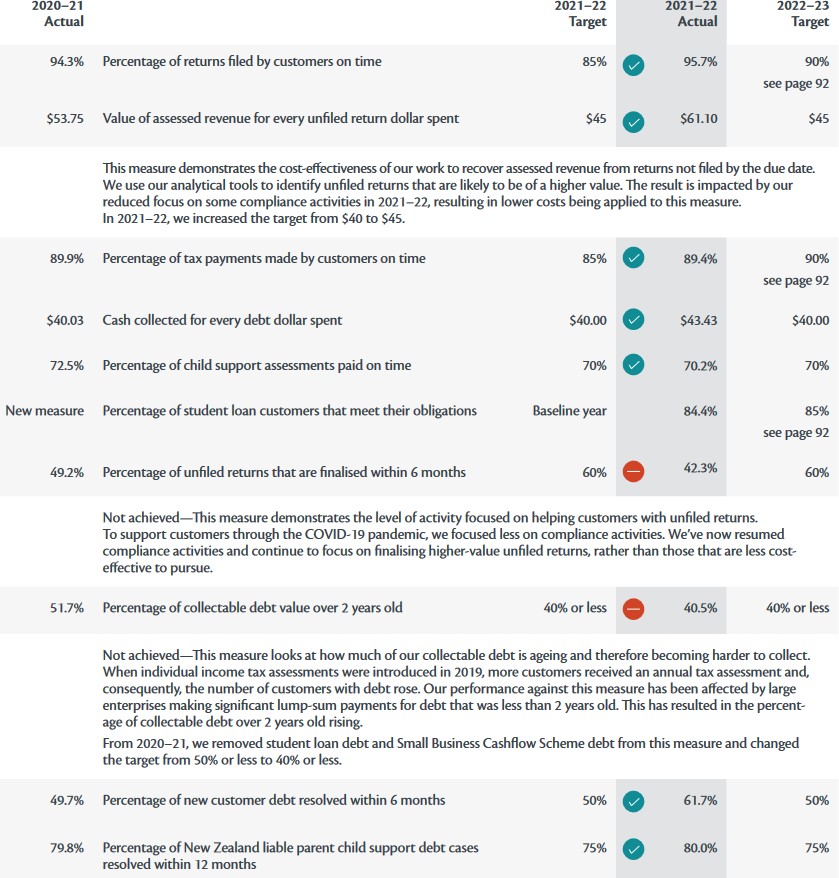

One of the things it ought to do is toughen up its own performance measures in relation to the management of debt. Each year in its annual report Inland Revenue will publish its performance measure results broken down by various sectors. For the year ended 30th June 2022, it achieved seven out of nine measures that it set in relation to the management of debt and on file returns.

But critically, one of the measures where it fell down was the percentage of collectable debt over two years old. The target for the year was 40% or less and in fact it achieved 40.5%, just above its target. That, by the way, was a considerable improvement on the 51.7% achieved for the year to June 2021.

But I would suggest that the 40% target is actually too generous. Inland Revenue really should be looking to drive that down to 20% or less. In fact, looking at this measure, it used to include student loan debt and Small Business Cashflow Scheme debt, but they were taken out and the debt target was then reduced from 50% to 40%.

(As an aside, student loan debt is a particular problem where I think Inland Revenue inaction has allowed very large sums of debt built up with people going overseas as the main issue here. But Inland Revenue, to my mind, has not been quick enough to develop the tools it needs to keep on top of that particular issue, which means often applying to overseas tax agencies for details of defaulting taxpayers.

I think it’s picking up its efforts in this space, but the scenario perhaps shouldn’t be allowed to develop to the extent it did. I’ve recently come across a case where the taxpayer left over 20 years ago but basically Inland Revenue has only now really started to take action to collect the outstanding debt.)

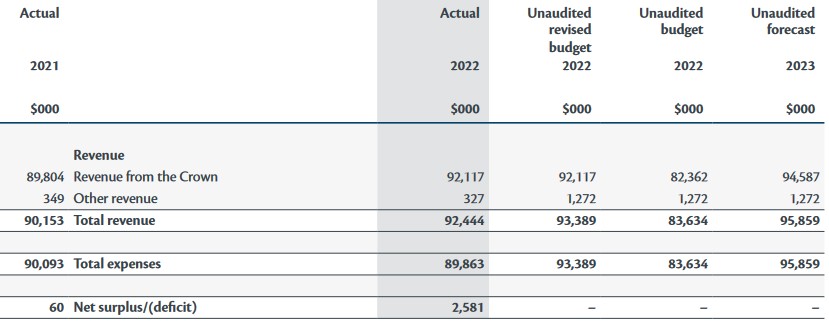

The other thing that’s also noticeable from Inland Revenue’s June 2022 annual report is that it did not actually spend the full amount allocated to it from the relevant budget appropriations.

Some questions for Inland Revenue

The amount allocated was just over $92 million, but in fact Inland Revenue underspent by $2.5 million for the year. A couple of questions I have about this are how did that happen and what’s being done to improve the performance and make sure that the funds allocated are effectively used? (I note that for the year to June 2023, there was an increase in the appropriations.)

It will be interesting to see how that’s played out when we see the annual report later this year. This debt management issue, by the way, points to something I’ve mentioned in previous podcasts – has Inland Revenue’s Business Transformation program deprived it of some capacity in key areas? Inland Revenue has reduced its staffing by more than 25% of your staff and not all of that might be dead wood no longer needed because of the upgrade. I think vitally important staff have gone from key areas such as investigations. And it may be that debt management is another area where key personnel have been allowed to go and the gap has been allowed to develop as a consequence.

As I said, it will be interesting to see the annual report later this year. But in summary, I’d have to agree with Professor Marriott, there’s plenty of room for improvement.

More interest rate rises…

Moving on, a key weapon for Inland Revenue in ensuring payment of tax debts is the ability to charge use of money interest on unpaid tax debt. The current rate is a fairly chunky 10.39%. But as of 29th August, the day after the next provisional tax payment date, the rate will increase to 10.91%. (Incidentally, the rate payable for overpaid tax will also rise, and that goes from 3.53% to 4.67%).

It is necessary for Inland Revenue to have a tool such as an interest charge for unpaid tax. Otherwise, people would just not take any action. But I think that is only one of the tools in its arsenal, as I just mentioned it really does need to back this up with greater enforcement and earlier interventions.

At the same time, Inland Revenue and tax advisers can all work together and let people know that when you take proactive steps on tax debt, you will find Inland Revenue is much more prepared to work with taxpayers in default than people might imagine. This has always been my experience. You front foot these issues with Inland Revenue, and you will find they will be prepared to work with you and your clients unless they are actually dealing with a serial defaulter.

For example, yesterday I was speaking with someone who’d run into some difficulties and had gone to Inland Revenue. They had been very pleasantly surprised by how proactive Inland Revenue had been in working with them on sorting out their unpaid tax. I could see clearly see that they felt a lot happier about the position. They still owed money, but they were in a position where they knew there was a way forward.

The key lesson is if you’re in trouble with Inland Revenue over unpaid debt, talk to it and your advisers and then you’ll hopefully get better results.

Incidentally, the rate of prescribed rate of interest for calculating fringe benefit tax on employer provided loans and some other measures is also being increased with effect from the quarter starting 1st October. From that date, the rate will rise from its current 7.89% to 8.41%.

Upstart Nation? Changing the tax system to boost startups

And finally this week, an interesting report called Upstart Nation from the government’s Start-Up Advisory Council.

This has been the business group looking at how to improve the rate of startups and develop more startups into major companies. On 1st August it released its report which included suggestions regarding changes to the tax system to help boost startups.

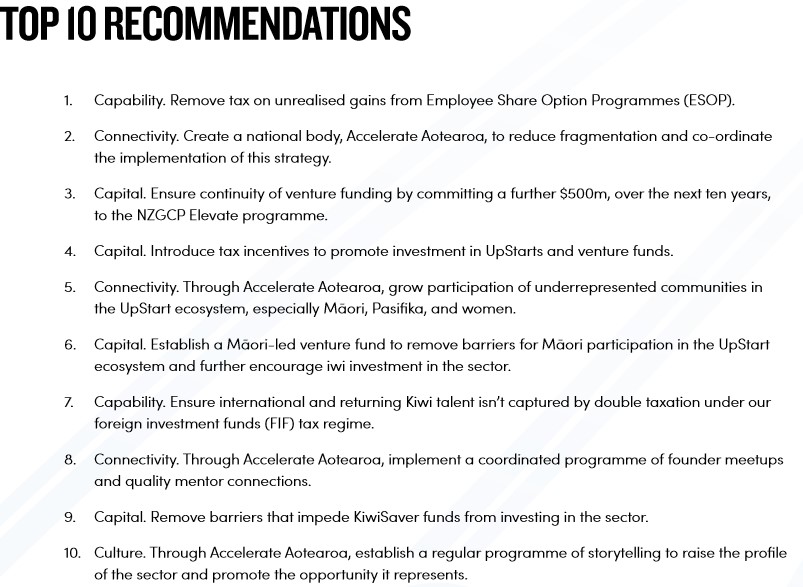

The report’s objective to “present a comprehensive strategy aimed at transforming New Zealand into a thriving hub for innovative UpStarts”. The Council identified four primary pillars as key: Capital Capability, Connectivity and Culture. Specific recommendations were made by the Council for each of those pillars to address identified gaps and leverage opportunities.

It had ten recommendations which it felt “will have the greatest impact on our ecosystem”.

Interestingly, three of those recommendations involve changes to the tax system. The first was wanting changes around the taxation treatment of share options and employee share option programs (ESOPs) in particular.

Generally, the current position is a taxable gain arises on the exercise of the options. The Council thinks it would be more appropriate to move that taxing point to when the underlying shares relating to those options are sold. ESOPs are intended to attract and retain investors and key employees as the business grows. Accordingly, hitting them with early tax charges ahead of when they actually can realise their position is a bit of an impediment. There are also questions around the compliance costs involved in getting accurate valuations in what is often an illiquid market. I hear this quite a bit.

Another was specific incentives to promote investment in UpStarts and venture funds in is some form of deduction for such investments. The Council recommends officials carefully review the Australian and UK tax concession schemes and develop something tailored to the New Zealand setting. In particular, they were looking at the Australian Early Stage Innovation Company scheme, which provides a deduction for an investment and a capital gains tax exemption.

The council suggests a deduction of maybe up to 30% of the capital invested directly in an UpStart or UpStart venture fund capped at $200,000 a year. That’s an interesting suggestion and one worth considering even though it probably won’t be accepted by fiscally prudent governments.

An urgent issue with the foreign investment fund regime

The third suggestion included in the top ten recommendations was to “Ensure international and returning Kiwi talent isn’t captured by double taxation under our foreign investment funds regime.” This issue almost exclusively affects American investors and employees with overseas investments. Once their four-year transitional residence exemption expires and the foreign investment fund (FIF) regime takes full effect, they are essentially taxed on an unrealised basis. At the same time, because America requires all its citizens to file tax returns, they are still subject to tax there and in particular capital gains tax.

This is something I’ve discussed with a number of clients. Although they can claim foreign tax credits in America in relation to the FIF tax payable, it often exceeds the equivalent amount of US tax payable on the realised gains. They are therefore accruing a tax liability, which in some cases they can never fully offset. In effect, they feel they are facing a double tax charge.

The Council recommended “this issue be investigated under urgency with a view to removing FDR on people caught under this double tax conundrum to ensure we can attract and retain them in New Zealand”.

I agree this needs reviewing. We hear frequently we are in the business of attracting talent here. In this particular case, we have an issue (somewhat ironically, a by-product of not having a comprehensive capital gains tax) which potentially hinders getting vitally important migrants.

You could argue that not this particular issue doesn’t just affect investors in the startup sector, but also any American citizen or returning New Zealanders who have acquired American citizenship or a Green Card and are among the groups of skilled migrants such as doctors or other specialist engineers, etc. This is a real impediment we need to consider.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.