the first ever sentencing for possession of tax evasion tools.

Inland Revenue’s draft long-term insights briefing currently out for consultation has generated quite a bit of debate. The paper discusses the future shape of the system and how to fund the rising cost of superannuation and related health costs.

Sir Roger Douglas has now entered the chat as he, together with Professor Robert MacCulloch of Auckland University, have released a paper titled How to change the welfare state from a taxation to a savings-based model. In some typically bold thinking from Sir Roger, the proposal is to dramatically change the tax system, and instead of trying to raise additional tax to meet these costs, take a completely different approach.

A tax cut or something else?

Sir Roger and Professor MacCulloch suggestion is for the first $60,000 of income to be tax free. Based on current tax rates, that’s at least a $10,000 tax cut for everyone with income of at least $60,000. Instead, those taxes would be directed into mandatory savings accounts for health, pensions and other risk cover. These would then be supplemented by employer contributions (effectively a social security tax, although not specifically described as such) with the trade-off for these contributions being a cut to the corporate income tax rate.

They’ve released a short paper outlining their proposal (there’s also a more detailed paper that Sir Roger and Professor MacCulloch produced in 2020). The paper starts with an analysis of the forthcoming rise in health and superannuation costs and the need to take a long-term view on addressing this issue. Sir Roger and Professor MacCulloch take the view that the conventional approach, raising taxes to meet these costs isn’t going to cut it. Something more dramatic is needed.

Taking the axe to corporate welfare

In addition to the proposed mandatory savings accounts, Sir Roger and Professor MacCulloch propose cuts to what they call corporate welfare and grants to high earners. The cuts include the removal of screen production grants, ending accelerated depreciation allowances for industries such as forestry, fishing and bloodstock, withdrawing winter energy payments to wealthy households and KiwiSaver subsidies to higher earners. They also propose ending the “favourable tax treatment to owners of rental housing” but this isn’t defined. I’d be very intrigued to know more about what exactly they’re driving at there. All up Sir Roger and Professor MacCulloch suggest these could save over $12 billion annually.

Yeah, but…

This is quite a radical proposal which would be quite a shock to the system, and I’d be very interested to see what other economists think of it. One hurdle I see is with the proposals aimed at introducing competition into the provision of health services. This is a perennial problem for our economy. We are just 5.2 million people and 2,000 kilometres away from the nearest neighbour. Competition in that context is always going to be difficult but it’s an issue we need to address, not just in this context but across the economy as a whole, because I think it’s a major problem for our economy.

Overall, you can never say that Sir Roger Douglas would die wondering. As a RNZ report noted it’s a bold plan and I recommend reading the summary paper. Bear in mind some of what it proposes in terms of removing subsidies such as the Government’s KiwiSaver contribution for high-income employees are now actually happening.

What about increasing GST?

On a more conventional approach Inland Revenue’s briefing paper includes a discussion about the implications of raising GST from 15% to 18%. Last Thursday I spoke with Wallace Chapman of RNZ’s The Panel about this proposal.

The Inland Revenue briefing paper notes the suggested GST increase could raise $5.5 billion of tax annually. This is because, as I explained to Wallace and his panellists, GST is an enormously efficient tax. It does meet the classic broad based low-rate approach. You broaden the basis as widely as possible so you can have as low rate as possible. Furthermore, because we have no exemptions, our GST is enormously efficient. So really if you were thinking of increasing taxes your first point of call would be to raise GST.

A regressive tax

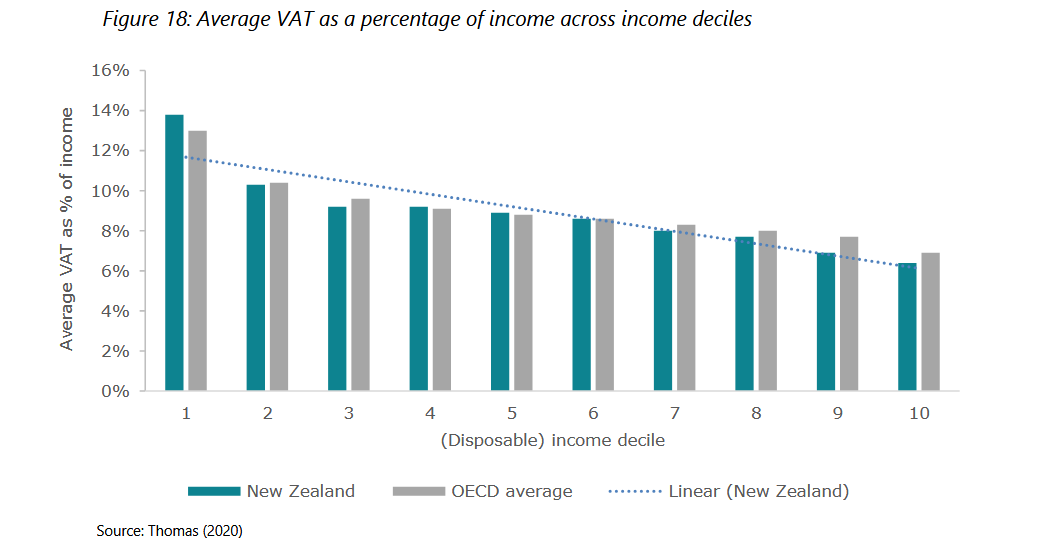

The problem is though, as Inland Revenue pointed out and as Holly Bennett, one of Wallace’s guests immediately jumped on, GST is a regressive tax. There’s quite an interesting analysis of this in the Inland Revenue briefing paper. The paper notes that GST or VAT (value added tax) is regressive relative to income.

According to the organisation of Economic Cooperation and Development (the OECD), the average GST to income ratio declines from 10.4% in Decile 2 to 6.9% in Decile 10. We follow a similar profile with our GST to income ratio declining from 10.3% in Decile 2 to 6.4% in Decile 10.

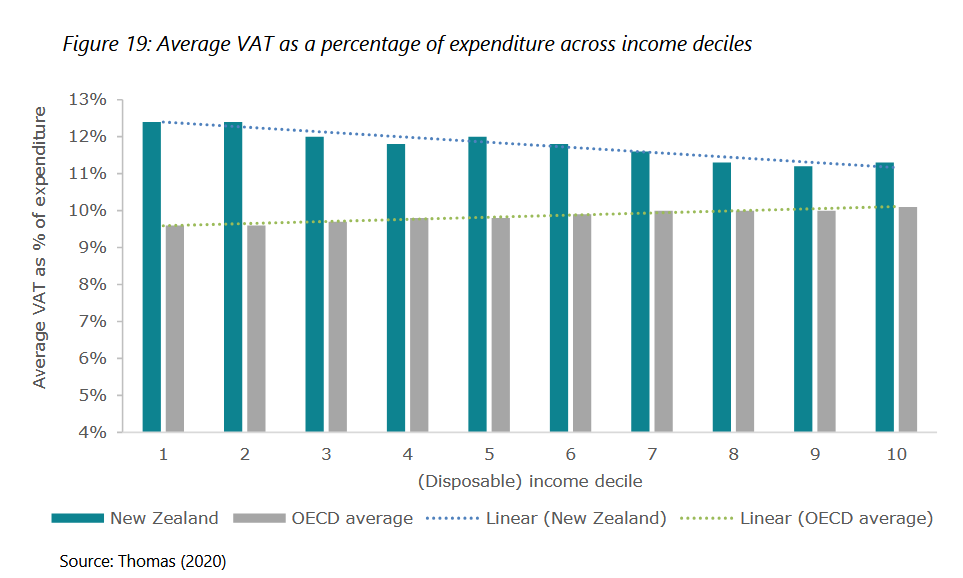

The Inland Revenue paper also considers the effect of GST relative to expenditure. In this instance GST or VAT is slightly progressive for most OECD countries because of the exemption of tax of necessities such as food and some sanitary products and various other Items which make up a very large proportion of the consumption basket of lower income households. However, our GST, because we don’t have any such exemptions, is mildly regressive.

Increasing poverty?

As Holly Bennet (one of Wallace’s panelists) was quick to also point out, an effect of GST increases is to increase the poverty headcount. According to Inland Revenue, based on the 2015/2016 Household Expenditure Survey GST “increased the imposition of GST in New Zealand increased the poverty headcount by 4.7%, the poverty gap by 1.7%, and the squared poverty gap by 0.8.” What’s worse is that the effect of those increases is higher than the OECD averages of 3.1%, 0.7%, and 0.3% respectively, again, because we have no exemptions.

The GST dilemma

So, raising GST results in the dilemma that it would raise a lot of revenue very quickly but hit lower income families harder. The suggestion in Inland Revenue’s paper is that there should be a compensation increase in welfare benefits for low-income families. They suggest that would probably cost maybe $440 million a year in total.

Readers and listeners may recall that last year a guest was Andrew Paynter, one of the Tax Policy Charitable Trusts co-winners. We discussed his proposal of raising GST to 17.5 % and introducing a GST refund tax credit for low- and middle-income earners.

Coincidentally or not, Andrew works for Inland Revenue, but there’s a worldwide trend looking at this particular issue. For example, the International Monetary Fund released a paper last year Designing a Progressive VAT which suggested a point of sale credit for low-income families. As the Inland Revenue paper notes Canada and Thailand have point of sales/refund credits for low-income earners.

Some form of capital taxation also needed

If you were adopting a conventional approach to addressing the rising expenditure gap, then raising GST is the most likely approach. My personal view is we also need to have some form of capital taxation because as I explained to the Panel, not only do we have rising health and superannuation costs, the cost of dealing with the impact of climate change, is rapidly accelerating.

This week Forsyths Barr and the Insurance Council released data that showed that over 40 years, the average annual cost of dealing with weather related events was $203 million. However, in the latest 10 years those costs had risen to $606 million annually and the five-year average is now $952 million per annum. Currently Tasman is spending $500,000 a day repairing its roads in the wake of the recent floods.

So climate change is having a huge impact now and there are a huge number of properties – 220,000 in total – presently worth over $180 billion, which are located within coastal inundation and inland flood zones. More than a quarter of those are in the Canterbury, Tasman, Gisborne, West Coast and Nelson regions. Those last four of which have all had severe weather events in the last year.

A quid pro quo

Protection against climate events will be another growing demand, particularly since for most people their property is their principal capital asset. This is where I think some form of capital taxation/capital gains tax is perhaps appropriate because if the Government and local councils are expected to spend more to protect capital assets, the quid pro quo must be that those capital assets become taxable.

Working for Families – a correction

Moving on, last week I talked about the changes to FamilyBoost and I noted that there had been no change to the threshold for Working for Families. That was actually incorrect. A kind reader from Inland Revenue pointed out that the Working for Families threshold will increase to $44,900 with effect from 1st of April next year its first increase since July 2018. Thanks for getting in touch and apologies for my error.

I’ll just simply add that on an inflation adjusted basis, that threshold should have gone up to something like $54,650 so it’s still way short of where it should be.

In any case the effect of the increase in the threshold from$42,700 to $44,900, which remember is for a family’s income, is mitigated by the increase in the abatement rate went up from 27.5 cents per $100 to 28 cents per $100.

Furthermore, the other point I made last week was about the focus of the FamilyBoost towards higher income families. That point doesn’t change just because the threshold for Working for Families has been (slightly) increased.

A New Zealand first

A recurrent theme this year is how Inland Revenue has increased its focus on chasing non-compliance. The latest example is the Auckland man who has become the first person in New Zealand to be convicted and sentenced for aiding and abetting his company’s possession of the electronic sales suppression tools.

Now these sales suppressions tools basically alter the Eftpos record so they’re very much about suppressing income and basically trying to defraud the taxpayer. In this case, Gurwinder Singh has been sentenced to seven months home detention on tax evasion charges, including the charge of aiding and abetting this company for possessing electronic sales suppression tools for the purpose of evading the assessment and payment of tax.

All up, Singh’s tax evasion amounted to $198,500. Apparently one of the things he was also doing was although he had four employees, including himself, he was only reporting PAYE returns for two staff. So, some obvious and not so obvious tax evasion was going on here. Anyway, this is the first time the new law in relation to electronic sales suppression tools has been applied. Would-be fraudsters have been warned.

The pitfalls of schedular payments

As often mentioned, Inland Revenue turns out vast amounts of very interesting and helpful material. Once such source are its Technical Decision Summaries about issues or rulings that Inland Revenue has encountered.

One TDS released this week is a private ruling in relation to the application of the schedular payment rules.

This involved a company wanting to make use of offshore personnel to act as directors in New Zealand. The question of interest here is a reminder that if you are making payments to overseas persons, they may, even if they are contractors, be subject to non-resident withholding taxes/schedular payments.

That’s why this one is useful. This ruling explained why those provisions would not apply. But typically, if they do apply then 15% withholding tax can be deducted which can come as a shock to some overseas persons. This is a useful ruling on a point which we often encounter but is one of those cases where I suspect the compliance isn’t always as diligent as it could be.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

And reveals results of increased audit activities.

Is GST really a tariff?

It’s been a busy week in tax. Right at the start of the tax year, Inland Revenue has launched a public consultation on a review of the fringe benefit tax regime which is now 40 years old. The 75 page issues paper titled Fringe benefit tax – options for change reviews the current status of FBT, focusing on issues Inland Revenue has identified. It puts forward a number of proposals aimed at simplification of these rules and a reduction in compliance costs, a long standing issue with major employers. There’s plenty to digest here but there’s a summary of the proposals on pages 6-8 of the paper if you want to get a quick handle on the proposals.

Reimagining FBT

The paper also addresses the separate issue of general compliance with the regime. A particular source of grief amongst compliant taxpayers is the treatment of the ubiquitous twin cab ute and the application of the work related vehicle exemption. Overall, the purpose of the paper is to

“…to review how FBT is assessed now, highlight current issues we are aware of with FBT and then outline some new concepts for how we could think about a reimagined FBT regime that is less complex and more targeted…”

The paper has 12 chapters, beginning with an introductory chapter, with Chapter 2 setting out the aims of the review. Chapter 3 explains how FBT is currently assessed. Chapter 4 picks up the FBT regulatory stewardship review from August 2022 which is really one of the initiators of this project. Chapter 5 then provides some comparisons with international FBT regimes.

Chapter 6 has an interesting discussion about FBT’s connection with remuneration. We tend to forget FBT was mainly introduced to ensure that all types of remuneration were brought into scope. Back in the 1980s, before FBT was introduced and the top personal tax rate was 66% it was common practice to give employees non-cash benefits such as company vehicles. Countering this was a key driver behind the introduction of the FBT rules in 1985.

Chapters 7 and 8 look at FBT and motor vehicles and considers options for change. Chapter 9 considers one of the areas of complexity, the treatment unclassified benefits. Chapter 10 discusses the option of applying FBT on entertainment expenditure, a proposal which will probably surprise a few people. The paper notes that entertainment regime also attracts a great deal of controversy and complaints about the compliance costs involved. Finally, chapter 11 looks at miscellaneous issues before Chapter 12 looks at data filing and integrity.

Why such a tight submission deadline?

There’s a lot to consider in this paper but submissions are due by 5th May, which means between Easter and Anzac Day there’s barely 4 weeks in total to review the paper and make submissions. The Minister of Revenue, Simon Watts, has repeatedly expressed a wish to simplify the FBT rules so he is keen to get this moving. My understanding the reason for the tight timeline is a desire to have the relevant legislation ready to be part of this year’s main tax bill, which will be introduced around late August or early September.

Proposed changes to FBT on motor vehicles

I expect many will focus on the proposals for motor vehicles. An interesting proposal is to increase the weight limit for vehicles subject to FBT from 3,500 kg to 4,500. Given the weight limit for a person with a full individual drivers’ license is 6,000 kg, my view is the FBT limit should tie into that threshold. Another proposal is to exempt vehicles that are used for providing emergency services.

A key change is removing the tax book value based option for calculating the fringe benefit value of a vehicle. Something worth considering is the suggestion for an optional valuation basis based on the fuel source for the vehicle i.e. electric, hybrid or petrol and diesel.

As part of re-connecting FBT with remuneration the paper suggests the FBT value of the motor vehicle could be calculated by reference to external sources such as remuneration consultations or maybe the AA calculations of vehicle running costs. The paper suggests regular revaluations, maybe every four years. One of the reasons why the tax book value option was introduced was that if people are not changing their vehicles regularly, then there’s an issue that the vehicle may be overvalued for FBT purposes. The proposal would address this issue.

However, the Lord giveth, and the Lord taketh. The paper proposes the following new rates for calculating the fringe benefit value of a vehicle based on its cost:

standard rate: 26% annual or 6.5% quarterly

hybrid vehicles: 22.4% annual or 5.6% quarterly, and

electric vehicles: 19.4% annual or 4.8% quarterly.

Availability vs actual use

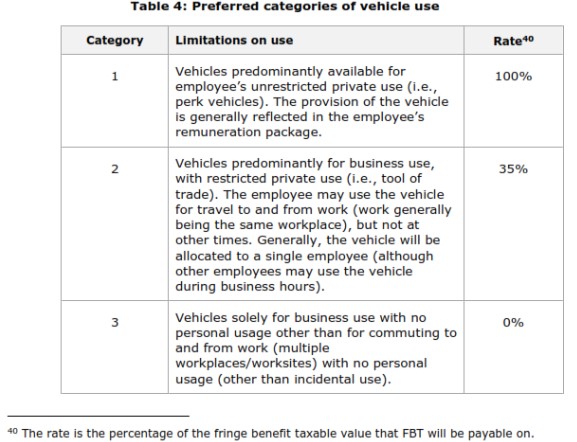

As part of the intention to simplify FBT, the suggestion is to no longer require taxpayers to maintain logbooks to determine the days the vehicle is available for private use. Instead, the focus will shift towards the actual extent of private use the vehicle is available for (for example, is it limited to home to work travel?).

The paper suggests the following categories of vehicle use:

As part of this change, the paper proposes excluding “incidental travel” to ensure that one-off private use of a vehicle can be ignored for FBT purposes. Behind this idea is a “close enough is good enough” approach.

A key proposal is to remove the current work-related vehicle exemption which as the paper says, is a “most misunderstood” exemption. The changes should address the issue of double-cab utes supposedly qualifying for the work related vehicle exemption and avoiding FBT entirely.

Changes to the entertainment regime

The other major proposal of note is integrating the entertainment regime into the FBT regime. Again, the idea behind this is to simplify quite a number of issues that currently exist in relation to the entertainment rules which have never been very popular and compliance is also a problem. As the paper notes many employers are taking a close enough is good enough approach to entertainment expenditure.

The interaction of the entertainment and FBT regimes can be confusing. For example, if an employer takes an employee out to a restaurant that is subject to entertainment rules. However, if the employer gives a voucher for that restaurant to an employee to use whenever they want, then that’s subject to FBT. Another example one would be if an employer pays for employees to participate in a front run, and then then provides a BBQ for staff staff at the finish line. Is the cost of the fun run subject to FBT but the BBQ represents entertainment? Integration of the two regimes is intended to address these issues.

Overall, this is a welcome review and as previously noted pretty timely given it’s now 40 years since FBT was introduced. Just remember you’ve got to get your skates on to submit by the deadline of 5th May.

Inland Revenue ramps up its audit activities with good results

At the start of last week Inland Revenue announced some of the results of its “noticeably increased” compliance activity. For the period from 1st July to 31st December 2024, it opened 3,600 audits 50% up on the same period in 2023. According to Inland Revenue’s Segment Lead for Significant Enterprises, Tony Morris, “Inland Revenue has found $600 million of additional tax that should have been declared.”

Morris went on to add “We’ve had a strong focus on the largest businesses in New Zealand and it’s worth noting that half of that additional tax came from less than 10 audits.” In other words 10 audits yielded $300 million.

Furthermore, Inland Revenue screened over three million returns as part of its annual year-end auto-assessment process. 30,000 of those, or about 1% were selected for review which resulted in a further $859 million of tax revenue. That’s a pretty good bang for buck on the additional funding it got in last year’s Budget.

Inland Revenue has also been focusing on debt and I thought this particular comment was of interest

“We’ve been in touch with 200 business owners and told them we know they have multiple properties – some in a company name, some in trusts, some personally. We believe they should be able to refinance to pay their debts to us and told them so.

“…These 200 people had $14 million of debt between them, but within a month more than $10 million had been paid or put under arrangement.”

Inland Revenue’s data gathering around property transactions is second to none and people would be wise to not underestimate this. It has been identifying transactions in this area for quite some time. A colleague recently told me of an audit that he was involved in where the client was saying, ‘Oh well, a number of property transactions were simply renovations of my main home’. That is until Inland Revenue investigators presented a “ream sized folder” full of property transactions for this taxpayer. From that point, the question wasn’t about rebutting Inland Revenue’s proposition that he was actually a property trader but trying to mitigate the damage. You have been warned.

“This is Baycorp calling on behalf of Inland Revenue”

However, something that does concern me is Inland Revenue’s announcement on 10th April it would be “running a six month pilot program in partnership with Baycorp to improve our debt collection process.”

Inland Revenue warned taxpayers that during this pilot, “you may be collected, may be contacted by representatives from Baycorp. Please be assured that these contacts are legitimate and part of our authorised programme.”

That’s as may be, but I’m not so sure given everyone’s growing concern about scams, not too many people are going to accept calls from Baycorp saying ‘you own Inland Revenue money pay up.’ I therefore doubt the pilot is actually going to be as effective as hoped even if Baycorp show the taxpayer incontrovertible proof that they have a debt due to Inland Revenue.

This is just the latest push by Inland Revenue to improving debt collection. As we noted in our last podcast given the rise in GST debt in particular, it’s basically no surprise that Inland Revenue is putting resources into debt collection. And as I’ve said previously, I expect there will be more funding given to it in next month’s Budget.

Is GST a tariff?

Meanwhile, around the world there has been large scale turmoil in the financial markets as everyone tries to work out what exactly is happening with the tariffs proposed by President Trump’s administration. As part of this he has indicated that value added tax (VAT) is now seen as a tariff. There’s been a huge pushback against this with the basic counterargument being that tariffs are only imposed on imported goods and services, whereas GST/VAT applies regardless of source of the goods or services

If you want more a bit more detailed analysis of why GST/VAT isn’t a tariff, I suggest this interesting post by Dan Neidle of Tax Policy Associates. He considers the issue using the example of beer, which is always handy, and the implications of the policy.

Removing GST from fruit and veg – “a well-known solution to every human problem”

The American writer HL Mencken was the source of the quote “There is always a well-known solution to every human problem – neat, plausible and wrong.” This often comes to mind in relation to the frequent proposal to remove GST from fruit and vegetables. It so happened the Prime Minister was asked about this suggestion on TV1’s Breakfast Show. He responded that it was far more complex than people imagined.

I subsequently appeared on Wednesday’s show to discuss the issues involved in removing GST from fruit and veg. To be fair following Mencken’s dictum about the policy being ‘wrong’ would be a bit harsh. This is an extremely well meant suggestion based on the precept if you wanted to try and help people struggling with the cost of living then removing GST is an option or step and no doubt would provide some assistance.

But as I explained it is complex and definitional issues lead to extreme examples such as the UK Mega-Marshmallows which enabled me to sneak in a reference to The Princess Bride. Furthermore, well-meant though it is, the proposal is not perhaps the right solution for the problem you’re trying to deal with, which is people with low income who are struggling with rising costs. A targeted response is more appropriate.

The Tax Working Group’s view

This was also the analysis of the 2018-19 Tax Working Group which also addressed a key complaint about GST, that it’s seen as regressive for those on low incomes. In response to addressing regressivity by perhaps reducing the rate of GST or introducing a GST exception for food the TWG commented “there are more effective ways to increase progressivity than a reduction in the rate of GST.”

Instead, the Tax Working Group suggested

“…increases in welfare transfers would have a greater impact on low income households. Changes to personal income tax can also have a greater impact on low and middle income earners. GST exceptions are complex, poorly targeted for achieving distributional goals and generate significant compliance costs, and furthermore, it is not clear whether the benefit of specific GST exceptions are passed on to customers.”

I agree with that analysis. It’s also supported by research carried out by Tax Policy Associates on the impact of VAT(GST) changes in the UK, where VAT has been removed from several products again for very well meant reasons. Examples include a reduction in the VAT rate for tampons and other menstrual products and the zero-rating of e-books. In both cases, the analysis carried out by Tax Policy Associates identified little or no benefit going to final consumers. In fact, in the case of e-books, no benefit passed through to consumers, costing the UK £200 million.

A complex and ineffective solution

In sum removing GST from fresh fruit and veg is complex and leads to boundary definitional issues. UK cases such as Mega-Marshmallows or the older Jaffa cake case involving the UK’s zero-rating of food are very, very good examples of the sometimes absurd distinctions that arise. Even although accounting systems are much improved the fact remains there are irreducible minimum compliance costs involved. These will fall most heavily on smaller operators such as dairy owners who already have a fairly heavy compliance burden with GST.

Much as I can see why people would want to suggest zero-rating fresh fruit and vegetables, ultimately, you’d have to consider whether the benefit of such a change is actually going to flow through to those who you want to benefit? Remember, if you do apply an exception, everyone benefits from it. As the Tax Working Group noted wealthier deciles spend more on food and fresh fruit and vegetables so would probably benefit disproportionately.

This isn’t a matter that’s going to go away. My view remains in line with that of the Tax Working Group. Look at what the real issue is, and it’s some families don’t have enough income. The best approach is therefore to give them more income. But we’ve got an election coming up next year and no doubt the proposal together with other well-meaning but inefficient ideas will be put forward.

And on that note, that’s all for this week, we’ll take a short break for Easter and be back for the ANZAC Day weekend. In the meantime I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day and Happy Easter.

The debate over international taxation and the so-called Two Pillar proposals has been driven largely by the G20 and the Organisation for Economic Cooperation and Development, (the OECD). But in recent years the United Nations has started to flex its muscles in this space. This is unsurprising, because the UN represents the wider world view outside the 40-odd countries which make up the G20/OECD.

All of this is behind the story that RNZ ran at the start of the week about the United Nations Committee on Economic, Social and Cultural Rights statement on tax policy. The RNZ ran this statement under the banner headline “UN Report questions fairness of GST”, in which it pointed out that GST can be regressive for low-income earners.

In fact, the UN Committee statement went much further than GST. It noted the terms of reference to the United Nations Framework Convention on International Tax Cooperation, which had been adopted by the General Assembly,

“This development represents an important opportunity to create global tax governance that enables state parties to adopt fair, inclusive and effective tax systems and combat related illicit financial flows.”

“regressive and ineffective tax policies”

The key paragraph to the UN Committee statement is paragraph 4, which refers to “regressive and ineffective tax policies”, having

“…a disproportionate impact on low-income households, women, and disadvantaged groups. One such example is a tax policy that maintains low personal and corporate income taxes without adequately addressing high income inequalities. In addition, consumption taxes such as value added tax can have adverse effects on disadvantaged groups such as low-income families and single parent households, which typically spend a higher percentage of their income on everyday goods and services. In this context, the Committee has called upon States Parties to design and implement tax policies that are effective, adequate, progressive and socially just.”

It’s the reference to consumption taxes that was picked up by RNZ. The regressivity of GST is well known and was noted by the last Tax Working Group. The general approach we’ve taken here to that issue is to try and ameliorate the impact by benefits or transfer payments such as Working for Families and Accommodation Supplement to lower income families.

The thing is though, as Alan Bullôt, of Deloitte noted in the RNZ story, GST is a very effective tool for the government to raise a large amount of money relatively easy. In fact, GST represents about 25% of all tax revenue a point I repeated when I discussed the whole story on RNZ’s The Panel last Monday.

Principles of a well-designed tax system

But the Committee statement is interesting beyond the GST issue because it goes on in paragraph 6 to set out what it regards as the principles of a well-designed tax system. It suggests, for example,

“…ensuring that those with higher income and wealth, in particular those at the top of the income and wealth spectrums, are subject to a proportionate and appropriate tax burden.”

That can be clearly interpreted as a call for a capital gains tax or some form of capital taxation, a point I made to The Panel.

The Committee also fires a few shots over international tax, stating

“The Committee has observed situations in some States where low effective corporate tax rates, wasteful tax incentives, weak oversight and enforcement against illicit financial flows, tax evasion and tax avoidance, and the permitting of tax havens and financial secrecy drive a race to the bottom, depriving other States of significant resources for public services such as health, education and housing and for social security and environmental policies.”

That clearly targets tax havens, but it’s also a shot across the likes of Ireland, for example, with its low corporate tax rate.

A global minimum tax

The Committee also calls for a “global minimum tax on the profits of large multinational enterprises across all jurisdictions where they operate and to explore the possibility of taxing those enterprises as single firms based on the total global profits, with the tax then apportioned fairly among all the countries in which they undertake their activities.”

That’s quite the statement even if probably forlorn given the Trump administration’s recent declarations. It’s probably what the less developed world is after, because they’re quite concerned they’re losers under the current system. This is going to lead to wider clashes over the G20/ OECD proposal, which I think to be frank, is probably dead. In any case, I thought it was always noteworthy that Pakistan, the World’s fifth most populous country and Nigeria, the sixth most populus country and also Africa’s largest economy, both refused to sign up for Two Pillars.

Now economically, that was not highly significant because the economies are small relative to the giant economies of the developed world. However, I think this refusal points to existing issues and this statement underlines there’s global tensions ahead on this question of international tax.

As I said, the Trump administration basically is saying no go. But I think you will see countries attempting to find ways of taxing what they regard as their part of the international multinationals’ income. So, plenty ahead in this space.

Rising GST debt

Now moving on, another RNZ report picked up that there had been a substantial growth in GST debt. Allan Bullôt, of Deloitte raised a concern this could be creating zombie companies. In particular he noted the amount of GST collected but not paid to the Government, has risen from $1.9 billion in March 2023 to $2.6 billion by March 2024.

As mentioned earlier, GST represents 25% of tax revenue. It also represents just under 40% of all tax debt and has been rising sharply. That’s a reflection of the economic slowdown and the cash flow crunch that’s happening to a lot of businesses.

Even so, this is a matter where Inland Revenue has a number of resources it can deploy, and one Alan mentioned is the power to notify credit reporting agencies about tax debt. According to the Inland Revenue, it only did that three times in the year ended 20 June 2024 and not at all during the June 2023 year.

This means that people were trading and doing business with companies without realising the potential risk. What that might mean is that you provide services to a company which is struggling with GST debt, and lo and behold, you suddenly find you’ve got a bad debt on your hand.

Creating zombie companies?

This is a major issue and as Allan put it,

“That’s grown and grown. I get very nervous we’re creating zombie companies … if you’re three or four GST returns behind, it’s incredibly unlikely if you’re a retail or service business that you’ll ever come back. If you’re three of four GST payments behind, it’s incredibly unlikely that your retail or service business will ever come back.

Maybe if you’re a property developer who’s got big assets that you sell and settle your debt. But if you’re a normal business, a restaurant or something like that, you go belly up.”

This is an area where Inland Revenue has information which is not available to the general public and maybe it should be making that more widely available. There’s a question here to my mind, of what proportion of debt you would report. The Inland Revenue I think has every right to say this person owes X amount of GST, or is behind on GST, but bear in mind in some cases the debt is inflated by interest and penalties. Or in some cases there may have been estimated assessments.

Notwithstanding this Allan is right to raise concerns and I expect we will see more money being granted to Inland Revenue in this year’s Budget to chase this debt.

Meanwhile, jam tomorrow in the Australian Budget

It was the Australian budget on Tuesday night our time in which the ruling Australian Labor Party promised modest tax cuts starting in July 2026, with a further round in July 2027. Under the proposed cuts, a worker on average earnings of A$79,000 per year (about NZ$86,800) will receive A$268 in the first year and that will rise to A$536 in the second year. In addition, there will be a A$150 energy rebate payable in A$75 instalments.

Otherwise, there weren’t many other tax measures to report. That was hardly surprising because two days later, Prime Minister Anthony Albanese announced that the Federal Election would be held on 3rd May. The Budget was therefore what you might call a typical pre-election budget, promising jam tomorrow if you vote for the ALP.

One tax measure of note was that the Australian Tax Office is getting further funding for dealing with tax avoidance and tax evasion. I think that’s a pretty standard pattern we’re seeing around the world. The British had what they call their Spring Statement this week, the half yearly report by the Chancellor of the Exchequer or Finance Minister.

No new tax measures were announced. But like the ATO, HM Revenue and Customs was allocated more money to target tax evasion, with the expectation that it would achieve about a billion pounds a year in additional revenue, which seems very light given the scale of the UK economy.

Mega Marshmallows food or confectionery?

Finally, this week, a couple of years back, we discussed the Mega Marshmallows Value Added Tax (VAT) case from the United Kingdom. Basically, it involved the VAT treatment of large marshmallows. If deemed to be food they would be zero-rated for VAT purposes, but if they were confectionery, they would be standard rated which at 20% means quite a significant sum is at stake.

I will cite this and its very well-known predecessor the ‘Max Jaffa’ case involving Jaffa Cakes from the 1990s, when people make suggestions about maybe reducing the GST on food to help with the cost of living, particularly for lower-income families. It’s a well-meant policy except the practical issues you run across lead to absurdities at the margins. My view on this topic is if you want to assist people at the lower end of the income scale, it’s better give them income rather than try and fiddle with the GST system because there are unintended consequences, and this mega marshmallow case is a classic example.

The case involves unusually large marshmallows. The recommendation by the manufacturer is that they should be roasted as they’re marketed as part of the North American tradition of roasting marshmallows over an open fire. Except it’s not clear in fact, if that actually happens.

The story so far is that after HM Revenue and Customs lost in the First-Tier Tribunal, it appealed to the Upper-Tier Tribunal which basically said, “Nope, we’re not hearing it.” So HMRC appealed again to the Court of Appeal which has now issued its ruling. The Court of Appeals determined it was not absolutely clear whether in fact these marshmallows can only be eaten if they are cooked, in which case they must be food, or they can be eaten with the fingers, in which case they are confectionery.

Accordingly, the key issue is whether they are normally eaten with the fingers. This is a question of fact about which the first-tier tribunal has not made a finding. In some cases, it will be obvious from the nature of the product whether it is normally eaten with the fingers or in some other way. But that is not clear with this particular product.

The Court of Appeals therefore sent the case back to the First-Tier Tribunal to decide on this question of fact. Are these mega marshmallows mostly eaten with the fingers? If so they’re confectionery and subject to VAT at 20%. Alternatively, are they mostly cooked as supposedly intended, and therefore zero-rated food.

Time for the UK to apply VAT to food?

This case came to my attention through the UK tax thinktank Tax Policy Associates which is run by the estimable Dan Neidle, a former tax partner at the mega law firm Clifford Chance. Commenting on the Court of Appeal’s decision, he pointed out the sheer absurdity and costs involved and questioned why this was so. “Why do we have a horribly complicated set of rules that mostly benefit people on high incomes (because they spend more on food)? “

His solution – scrap zero-rating on food, in other words, adopt the approach we have here in New Zealand and tax everything. He estimates that would raise about £25 billion which could be used to reduce the standard rate of VAT from 20% to 17%.

Warming to his theme Dan thinks a better idea would be “Cut the rate to 18% and use the remaining [money] in benefit increases and tax cuts targeting those on low incomes, so they’re not out of pocket from the loss of the 0% rate.”

It’s the first time I can recall a British commentator suggest this. I doubt it will happen, but it’s just a reminder that although our GST is highly comprehensive, we don’t have these absurd but entertaining cases involving marshmallows of unusual size.

But a comprehensive GST is regressive, and I think a better approach is to address that by means of transfers to lower incomes rather than tinkering with exemptions. You never know, there may be something in this space in the Budget, we’ll find out next month.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Lessons from the largest known GST fraudster – could it happen again?

Corporate tax cuts – who benefits and what does the public think?

The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year’s tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it’s often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They’ve therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock.

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

the asset was acquired before 1st of April 2023; and

it was not acquired for the principal purpose of making taxable supplies; and

it was not used for the principal purpose of making taxable supplies; and

a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don’t pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don’t necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you’re registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called “time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn’t entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I’d like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken’s release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn’t always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there’s been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they’d have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I’ve heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it’s interesting to marry that along with the public’s general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

My guest this week is Andrew Paynter, a policy advisor at Inland Revenue and co-winner with Matthew Seddon of this year’s Tax Policy Charitable Trust Scholarship. The Tax Policy Charitable Trust was established by founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa.

Andrew Paynter’s proposal is to increase the rate of GST to 17.5% and introduce a GST refund tax credit for low-and middle-income individuals.

I should make it clear here that everything in Andrew Paynter’s proposal and what is in this podcast represents his views and not those of Inland Revenue. Kia ora Andrew Paynter, congratulations on your win and welcome to the podcast. Thank you for joining us.

Andrew Paynter Thank you. That’s very kind. And yes, it’s great to be here and I’m really excited to have a chat with you.

TB Me too, it is a very interesting proposal. And so how do you land on choosing this? There is a pretty free rein in choosing topics for the scholarship. But what drew you to this particular proposal? .

The background

Andrew Paynter Yes, sure. For me, something I’ve been interested in ever since I’ve worked in the tax space is the New Zealand Crown’s long term fiscal position. And we know from the New Zealand Treasury’s most recent long-term insights briefingHe Tirohanga Mokopuna 2021 that as we look into the future, the Crown is going to be spending at quite a higher rate than it is getting revenue.

And for me, I think that puts New Zealand in quite a weak position to manage its daily societal needs. But also to manage future disasters, pandemics and economic shocks. And we know that these things are going to happen more often and probably at a greater severity than they have in the past. So that was sort of my starting point. I guess that was the thing I was interested in, and I wanted to try and develop some form of solution to that.

TB Yes, I mean, this is something long-time listeners to the podcast keep hearing me banging on about Treasury’s statement on the long term fiscal position. I also note in its briefing to the new Finance Minister, Treasury says there is a structural deficit of 2.4% of GDP. So we have a fiscal gap already, according to Treasury. I mean people talk about reducing expenditure, but that will only take you so far, particularly when expenditure is going up faster than you can reduce it, to be blunt. So why did you land on GST?

Why increase GST?

Andrew Paynter I think there’s quite a few reasons that I landed on GST. I guess the two main points are about finding a revenue raiser that embodies good taxation principles.

And then the second part is trying to find a revenue raiser that I think has better impacts than other revenue raisers, particularly in relation to effectiveness and efficiency.

So, on that first point, embodying good taxation principles. It’s really important that any revenue raisers that we choose are aligned with broad-based low rate, and that’s ensuring that we maintain f broad-based low rate at an entire tax system level, and at a regime level.

Of course, when we look across the New Zealand tax system, I think we can all agree that one regime in particular stands out as being super broad-based and that’s GST. We know GST has few exemptions and exclusions, but it also has the highest value added tax revenue ratio score in the OECD by quite some margin.

TB Yes, that’s quite a stat. In fact I think only Chile raises a higher proportion of tax from GST than ourselves?

Andrew Paynter I’m not entirely sure if that’s correct, but I do know for the revenue ratio score, I think Luxembourg has the second highest score in the OECD. But we outscore Luxembourg by quite some mark. And I think we have double the OECD average in New Zealand. So, it’s quite a difference.

GST – the broad base, low rate exemplar

TB That’s taxing everything. It’s as you say, it’s the exemplar in the system of the broad-based low rate. Even if you’re you’re proposing to raise it to 17.5%, even then, that would still be below the OECD average, isn’t that right?

Andrew Paynter Yes. The OECD average rate is 19.2%, so 17.5% is still nearly 2% below the average.

TB How much would that raise? This is the thing the politicians say. OK, how much would we get if we increased it by 2.5 percentage points. What’s the potential take?

Andrew Paynter Yes, I think obviously it depends on a huge raft of dynamic factors like inflation and consumption patterns. If the rate was applied in the 2023 tax year it would have raised an additional $4 billion in revenue. So that gives like a proxy for what’s possible.

TB Wow. I mean, that’s one percentage point of GDP. So that is a significant amount. But the question is, as I said, why GST? There’s a lot of debate around capital taxation as well, wealth taxes, capital gains tax and occasionally, not so much though, estate duty/death duties/inheritance tax. In your paper, you talk about GST being a one-off taxation on the wealthy. Can you elaborate on this?

How GST represents a one-off tax on the wealthy

Andrew Paynter Two interesting parts to that really. I was again looking to this future fiscal deficit and trying to think of revenue raisers that suited that future context. And one thing that we know is underpinning part of the deficit (obviously it’s not the whole thing, but part of it) is having this ageing population. And so, is there a way to leverage revenue from an ageing population? Of course, as the population gets older, a higher percentage of the population is earning less taxable income, but they are consuming often more than the means of their income as they’re drawing down on savings. So, increasing the rate of GST becomes in a way an effective one-off taxation on all the current and future wealth that exists in New Zealand so long as that wealth is then consumed in New Zealand on taxable supplies.

TB So if the ageing population skips off to spend its money overseas that is outside the GST net. But the likelihood is, as you say, they’ll consume more and more of it in New Zealand effectively because their income has declined.

Andrew Paynter Yes.

TB This means the GST relative to what their income as a proportion of the total tax they might pay, will rise on under this measure. Yes, so interesting analysis there but we don’t have a lot of evidence.

Andrew Paynter That’s correct, yes.

TB Maybe we don’t have as much statistical evidence as we would like. The empirical evidence to talk about, the behavioural impacts of this. But GST’s not really subject to the same behavioural impacts as other taxes, because you can either spend it in New Zealand or spend it offshore. And as we said, your opportunity to do that has become limited because physically you may not be able to travel, or it becomes too expensive to travel.

Andrew Paynter Yes, that’s right. Some interesting analysis is that when you do increase GST or just a VAT or consumption tax in general you do get potential behavioural responses. You know, substitution effects, price elasticity responses, etc. But some of the academic analysis I found was that when you introduce a rate increase alongside a compensation measure, those behavioural responses are often quite muted. So you don’t actually get the same response that you would if you just did a GST rate increase by itself. And obviously, this proposal does have a compensation measure aspect to it.

What about inflation?

TB Yes, we’ll come to that in a minute. One of the other things that may come into play around a GST increase, is it’s potentially inflationary. How do you deal with that effect, how have you calculated that potential effect and how long would it last?

Andrew Paynter It’s quite interesting. I think we have some precedent in New Zealand that we can look to. For the 2010 GST rate increase, the government of the day had modelled that the inflationary response would be about 2% immediately after the introduction of the new rate. That was reflecting an immediate 2.5% price increase on all taxable suppliers, and then some form of future and lagged response on non-taxable supplies like rents, but those are a lot harder to quantify.

So, you certainly do get a significant inflationary impact, but I think that because the Reserve Bank has the discretion to look through temporary inflation shocks in the way that it sets its monetary policy, in theory it shouldn’t have very significant economic consequences. And again, I think, we can look back to 2010 and see that.

TB Yes, we want to avoid that horrible double whammy – prices have gone up and then interest rates go up, that is a real nasty spiral.

Andrew Paynter Yes, that’s right.

TB And as we mentioned before, GST is as incredibly efficient tax. Businesses were collecting it and everything fell into place very smoothly. I’ve been around long enough to remember that after the 2010 increase things fell into place pretty smoothly.

But the big downside though for GST, (and the last Tax Working Group touched on this) and the taking GST off food was a partial response, is that GST is actually a regressive tax. Particularly for the lower- and middle-income earners. And the second part of your proposal deals with that. What are you proposing there?

Ensuring equity through a targeted GST refund tax credit

Andrew Paynter As we noted before, the inflationary impacts of a GST rate increase means that businesses are passing on the full cost of the GST rate increase to final consumers.

And so that means prices are going to immediately increase relative to incomes. That’s obviously a problem. We have relatively high levels of inequality in New Zealand, so low to middle income New Zealanders don’t necessarily have the means needed to absorb that price impact.

Then on top of that, as you mentioned, GST is regressive. I know it’s argued that it’s not necessarily regressive over an entire lifetime, but I think the fact that it’s regressive, at least at a point in someone’s life, it can impact on their economic position, which can then have lifelong implications on them economically. To address that I’m proposing that a targeted GST refund tax credit should be introduced to offset that impact.

TB How would that work?

Andrew Paynter It’s a very good question. We were touching on it in a conversation we were having off-air earlier, with all social policy initiatives when you’re choosing a compensation measure or when you’re just designing that compensation measure, it’s all about trade-offs and deciding on what values and objectives you value more than others and what you’re trying to achieve.

We can discuss the design parameters for the credit in a second, and I’m sure we will. But I guess I just wanted to highlight that this is just one way to do it. It’s not necessarily the only way and it’s not necessarily the only “right” way to do it. It really depends on what you’re trying to achieve.

TB Because there’s quite a bit of interest around this sort of mechanism around the world, isn’t it? The IMF released a working paper in April just as you were writing your initial proposal. But that was completely different. And that was a refund that comes through as point-of-sale credit. You mentioned in your paper that Canada has been doing it.

Andrew Paynter Yes, that’s right.

TB So, similar to what you’re doing?

Andrew Paynter Yes. As you said, the IMF compensation measure is completely different to a tax credit like I’ve proposed. Whereas Canada’s example is a tax credit, as they call it, the GST/HST refund tax credit but the design parameters reflect the realities of the governmental and tax systems in Canada so it’s quite complicated.

Although we could look to these examples for some inspiration, I think that the parameters that we select for the New Zealand context should be rooted in the realities of our government structures, and also our transfer system and our tax system.

Resolving the problem with abatements and marginal tax rates

TB You note in the paper that transfer payments have been sliding lower relative to median incomes over time. Then what you’re driving at is that one alternative might be “let’s increase the alternative transfer payment”. But they all come with heaps of abatements as you point out.

I was reviewing Inland Revenue’s annual report before today’s podcast and a stat that jumped out at me on this point was that only 22% of people receiving Working For Families credits do not have an abatement. That threshold is $42,700, which means 78% are being abated, and that’s at 27.5%.

So, you want to avoid that because it just increases this whole problem of effective marginal rates. How do you intend to do that? You’re taking what they call a fiscal cliff approach. Is that right?

Andrew Paynter Yes. Part of the design of the credit that I’m proposing is to use a cliff face approach. As you touched on, abatement is where your entitlement, whatever that may be, is decreased by a specified percentage for each dollar you earn over whatever the threshold is.

So, when you compare that to a cliff-face approach (which is where your entitlement just ends once you hit the threshold) you don’t get the same impact on effective marginal tax rates.

You still get work incentive impacts, but those are a lot sharper and shorter. So given as you say, there’s lots of interacting abatement payments in the New Zealand context, for those reasons I’m proposing that the credit utilise the cliff face approach.

TB Yes, you’ve also said it’s to be individual, so it’s not calculated like Working for Families on a collective family unit. It’s on an individual basis because the evidence shows you wouldn’t be getting much potential abuse of the credit. Why an individual credit rather than a family credit?

Andrew Paynter It’s various factors. I think one point is again touching on that Canadian example. In Canada, I believe you can file as a family or as a couple. Whereas in New Zealand, all of our filing is individualised. The administrative realities are that unless you’re in a regime like Working for Families, you don’t necessarily have those connections within the tax system to your partner.

Individualising the credit therefore aligns with the individualised nature of New Zealand’s tax system. It means that you don’t need information from your partner in order to get the credit. Which means that you can automate it because you don’t have to have an application process that says, this person’s my partner and this is their income. On top of that I was looking at the Household Economic Survey and it really looks like consumption patterns don’t vary greatly between one person household consumption data versus two person households. Consumption is quite an individualised thing.

TB That’s encouraging, because the simpler this is, the better in my view.

Andrew Paynter 100% agree.

What’s the threshold?

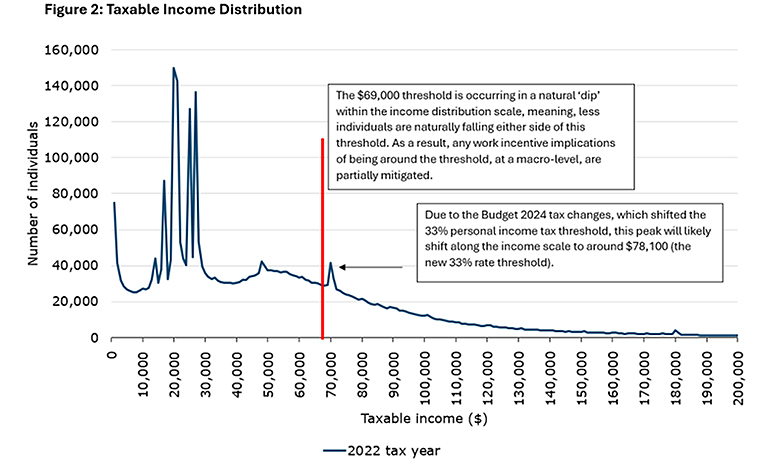

TB And so, the threshold you were talking about would be about $69,000.

Andrew Paynter Yes, I’m proposing that the threshold for the payment is $69,000, which is the median income from salary and wages. Obviously, it can be quite hard to define what we mean by low to middle income. But I think choosing this middle point makes sense for this notion of low to middle income.

You have less people naturally falling in that $69,000 space comparative to other parts of the income scale. And that means that those work incentive impacts that we talked about, are affecting less people, which I think is quite important from a macroeconomic perspective when compared to other parts of the income scale where you could put the threshold.

TB Yes, we see distortions around thresholds all the time. It’s quite blatant actually. You can see spikes in your graph at $70,000 and then $48,000. Don’t know what they have to do with it other than threshold increases.

Andrew Paynter Yes. That’s right.

How frequently?

TB This credit though, it would be payable quarterly. Is that correct?

Andrew Paynter Yes, I’ve chosen a quarterly model for paying and that quarterly model is full and final and that was to balance a few factors. It was to ensure that people are actually getting the credit close to the point in which they’re incurring the increase in GST, versus if you did a year, you might incur some form of increased cost towards the start of the year and you’re waiting quite a significant amount of time to get the payment. And again, given that this is targeted at low- or middle-income individuals, that sum of money is quite important.

Also, if you had a shorter time period, such as a week, it might be a bit more administratively difficult. For example, it’s hard to know how much people are actually getting paid as if a weekly model was chosen people’s pay periods might not align with that.

Having a quarterly full and final model also means that there’s a low demand for reassessments and that’s going to be important from an administrative perspective for Inland Revenue. Also, debt situations are avoided because you’re doing a lagged income model and that means people don’t have to guess what their income is going to be.

TB I think that’s incredibly important because when you see the stats, the debt’s building up. I mentioned earlier about the abatement issues for Working for Families and you say it’s full and final. So, in the quarter a person earns below the threshold, they get that payment and then for the next three quarters, they’re well above that.

But there’s no requirements to say, for example, they’re total income for the year was $80,000. But for the first quarter, they were within that $69,000, but that’s they received a final payment then and that’s it. No going back. No “backsies” from Inland Revenue to go back and re-assess.

Andrew Paynter Yes, that’s right.

TB And because as you say, the cliff face approach takes care of that because they get cut off, but hopefully their earnings have risen enough to mitigate the impact of the inflationary increase in GST.

Andrew Paynter Yes, that’s right.

TB I’m all for keeping it as simple as possible, otherwise the system gets bogged down with a lot of resources chasing relatively small sums of money. I think there are mechanisms to deal with that, and that’s the other part in here.

You’ve set out some different things you’re basically trying to automate as much as possible within Inland Revenue’s existing processes.

Definition of income?

Andrew Paynter Yes. Again, having the credit individualised as we touched on earlier, means you don’t need partner information. I also propose that the credit is based on a definition of taxable income, not something of a broader like economic income, which agencies like the Ministry for Social Development use for benefit payments. Inland Revenue already holds taxable income information in the course of its usual tax activities.

And then because it’s individualised and you don’t need partner information, it should in theory just be this really automated process where you know, me as an individual earns salary and wages and as long as I’m under the threshold for the quarter, as long as Inland Revenue has my bank account information, I will just get the payment.

TB I like that approach. Obviously you’ve got great feedback because you’ve won. But what feedback have you received from that? Is there a potential that your proposal might be taken further? Did Nicola Willis come up and say “ “Come and have a word with me I like this.”

Andrew Paynter Obviously everyone’s been very kind and very supportive, but whatever happens with my proposal, I’ve simply just come up with the idea. I’m obviously proud of my idea and all the work I put into it, and I have simply just put the idea out into the world.

TB That’s fantastic. Any final thoughts on what’s next?

Andrew Paynter What’s next? I’m not sure. A bit of relaxing I think. I guess one thing I would just say is if there’s any younger tax professionals listening to the podcasts or want to be tax professionals, it’s a really awesome competition and it’s a great opportunity to tackle some form of issue that you’re passionate about.

You’ve got the time and the space to develop a solution that you really care about and then you get to have it tested by leaders in the tax space. And I think that’s a really cool opportunity. So I heavily encourage anyone who meets the eligibility criteria to apply.

TB I thought the standard this year was extremely high and I’m very grateful to yourself, Matthew, Matthew and Claudia for all coming on and talking about your proposals

I think that seems to be a good point to leave it here. My guest this week has been Andrew Paynter, co-winner of this year’s Tax Policy Charitable Trust Scholarship, and we’ve been talking about his proposal to increase GST and have a refundable tax credit.

Andrew, it’s been a great privilege talking to you about that. Congratulations again. Have a well-deserved rest and onwards and upwards. I’ll watch with interest.

Andrew Paynter Thanks, TB. I really appreciate it. Thank you for having me on. It’s been great.

TB Not at all. Thank you. And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.