There have been several constant themes throughout this year. A surprising one has been the question of how we tax capital and whether we should have a capital gains tax. Throughout the year there have been a steady stream of stories on the topic. Meanwhile the Labour Party is currently reviewing its tax policy, and whether it’s going to go with a wealth tax or a capital gains tax.

A place where talent does not want to live

Intriguingly, Inland Revenue has added to this mix right at the end of the year with the release of an issues paper on the effect of the Foreign Investment Fund (FIF) rules on immigration.

Earlier this year I discussed a New Zealand Institute of Economic Research report called The place where talent does not want to live, which looked at the impact of the FIF rules on migrants to New Zealand. The NZIER report concluded that the FIF rules were acting as a hindrance to investors, particularly those migrants coming here who have previously invested in offshore startup companies.

The report also discussed an issue I’ve encountered fairly regularly of the impact of the FIF rules for American citizens. Even though they may have been resident in New Zealand for many years, because they are American citizens they still have to file U.S. tax returns. As a result, a mismatch arises for them between the FIF rules, which basically act as a quasi-wealth tax, and the realisation basis of capital gains tax that applies in America.

Inland Revenue policy officials have been aware of this issue for some time. In fact, I spoke to several officials earlier this year about the issues and potential options. The topic was highlighted as an option for review and was included in the Government’s tax and social work policy programme released last month. This report has therefore come out quicker than I expected which is a pleasant surprise.

The problem with the FIF rules

The problem is set out very clearly in paragraph 1.5 of the issues paper.

“Migrants will generally have made their investments without awareness of the FIF rules and may not be organised so that they can fund the tax on deemed rather than actual income. This is particularly a problem for illiquid investments acquired pre migration…. Because the FIF tax is imposed in years before realisation and on deemed rather than actual income, FIF taxes paid may not be creditable against foreign taxes charged on the sale of the investment.“

This highlights a key point about the FIF rules – they’re highly unique by world standards. When I’m discussing them with overseas clients and advisers, to make them more understandable I tend to explain them from the viewpoint that they’re a quasi-wealth tax. As the quote above notes problems also emerge whether the tax paid under the FIF rules can be fully utilised in the United States, for example.

Fixing the problem – taxing the capital gains?

The paper canvasses several options for reform, including one of simply increasing the current $50,000 threshold above which the FIF rules automatically apply. A key proposal is that maybe the investments subject to the FIF rules should be taxed on what is called revenue account. That is only dividends received and any gain in the value of those investments attributed to New Zealand on disposal would be taxed. In other words, an investor would be taxed on dividends and then when the investment was disposed of, a capital gains would be become payable.

Now to buttress this option the paper proposes that there should be an exit tax. In other words, if someone elects to use the revenue account method, but then decides no, actually New Zealand isn’t working out for us for whatever reasons, and they become a non-tax resident, this migration would trigger an exit charge. I’ve seen this in other jurisdictions and current FIF rules do have a provision covering it. This approach should be pretty understandable to investors coming here.

Maybe a deferral basis?

Another alternative is a so-called deferral basis, is where the FIF rules would apply on a realisation basis. This would be achieved in a way similar to how withdrawals on foreign superannuation schemes are currently taxed when the tax charge arises on withdrawal or transfer into a New Zealand based Qualifying Recognised Overseas Pension Scheme.

The taxable amount would be based on a deemed 5% per annum income from the date of their migration, with an interest charge for deferral. Again, this would be buttressed by an exit tax.

What happens overseas?

Picking up on what I was saying at the start about the question of taxation of capital, most other jurisdictions don’t encounter this issue to the same extent as we do because they usually have a capital gains tax regime that applies to comprehensive capital gains. Actually, in paragraphs 2.3 and 2.4 I find there’s some intriguing commentary from Inland Revenue on this issue.

“Because New Zealand does not tax capital gains without the FIF rules, no New Zealand tax would ever be paid on an investment in a foreign company that paid no dividends and was sold for a capital gain.”

This is an interesting insight to the issues caused by non-taxation. In effect without the FIF rules the Government is forsaking potential revenue. I always thought the expansion of the FIF rules in 2006 was really a sidestep around the difficult issue of taxing capital. And of course, despite having kicked the capital gains tax can down the road back in 2006, it’s still there.

Tax driven behaviour, or just a rational investment choice?

The issues paper goes on, quite controversially in my view, to argue that without the FIF rules in New Zealand, residents have a tax driven incentive to invest in foreign companies that enjoy low effective tax rates and do not pay significant dividends. Speaking with 40 years of tax experience, yes taxes do drive investment behaviour.

But this argument sidesteps a huge criticism, which is still valid, of the current FIF rules. When they were introduced in 2006, many of the submissions against them argued that the New Zealand stock market is so small in global terms that investors would be unwise to be fully invested here, and therefore should be spreading their risk by diversification and investing in offshore markets.

That is as valid a criticism of the FIF rules now as it was back in 2006. And of course, memories of the 1987 stock market crash, which was actually quite catastrophic by world standards, still run deep in many areas. We now have this scenario here where the FIF rules were designed because the Government wanted some revenue. It saw tax driven behaviour happening offshore, but it ignored a key fact, the importance of diversification. And if you don’t tax the capital but you want the revenue, where do you go from there?

Backdating the introduction of the changes?

Anyway, the whole paper is a very worthwhile read. It has one further highly interesting suggestion that changes could be back dated to take effect from 1st April 2025 and the start of the next tax year. Such a swift law change doesn’t happen with issues papers. Normally there’s usually another year or so before legislation is introduced and then comes into effect.

This option is actually very encouraging for migrants. I have had a number of inquiries on this issue, and I know of clients who have backed away from New Zealand because of the FIF rules. So, they will be looking at the proposals with great interest.

The paper also canvasses whether it should apply to new migrants or to existing New Zealand tax residents. That’s a good question it should certainly apply to migrants who can reorganise their affairs in anticipation, but I believe it should also apply to U.S. citizens who still have to file U.S. tax returns and are very disadvantaged by the current FIF rules.

Worth noting that although this is largely a tax measure it’s important to the Government because the existing FIF rules are seen (as the NZIER report noted) as a hindrance to attracting high quality migrants. Changing the law is seen as a priority as part of the Government’s general economic programme,

Submissions are open now and continue until 27th of January. I urge everyone interested in this topic to submit. We will be submitting a paper on this ourselves. We will also be contacting clients on this matter as it’s quite a welcome Christmas present.

The year in review

Moving on, its been a very busy year in tax. And I guess the biggest story in many ways was the Budget on 30th May, with the promised increase in tax thresholds finally being enacted with effect from 31st July. That was certainly the most eagerly anticipated one, and according to my data reads, it was the most read transcript over the year.

The tax cuts which weren’t

These tax cuts as they were called (which they’re not because they’re only inflation adjustments) also highlighted a big and continuing problem with our tax system, which the politicians apparently don’t want to address. The threshold adjustments only factored in inflation from 2018. They therefore effectively locked in the inflationary effect of the non-adjustment between 1st October 2010 (the last time the thresholds were adjusted) and the 2018 baseline.

On the other hand, in order to help pay for these adjustments which will reduce government revenue, the threshold on Working for Families which has been at $42,700 since 1st July 2018, was not increased. This means that families with income above that threshold have their Working for Families credits abated at 27.5%. Consequently, they face some of the highest effective marginal tax rates in the country.

And as I have repeatedly said in past podcasts, our politicians are very much less than transparent about the impact of what’s called fiscal drag. That is, as wages increase with inflation, they pull taxpayers up into higher tax brackets. We have a particularly big problem around the now $53,500 threshold where the tax rate jumps from 17.5% to 30%, the biggest single jump in the whole tax scale.

To bang a drum already beat repeatedly, this hinders a discussion around what is happening with our tax system? How much revenue have we really raised because politicians have been happy to use fiscal drag to quietly increase the tax take.

But the main effect is that the burden of tax falls on low to middle income earners who face significantly higher marginal tax rates because of the effect of abatements on people receiving social support, such as Working for Families.

So overall, those tax threshold adjustments were welcome. They were overdue, but they were one step forward and two steps sideways and half a step back because there’s no comprehensive commitment to ensuring that we have regular threshold adjustments.

If America can do it, why not here?

Just as an aside, in America all thresholds are automatically index-linked. Countries vary on their treatment of inflation and thresholds. And in low inflation periods, you can get away with not needing to do it every year, but you can’t leave such adjustments for 14 years without finally having to do something.

A year of anniversaries

2024 was quite a big year for me personally. I started working in tax 40 years ago in Britain and it so happened that the British budget on 30th October had several announcements which have huge significance not just for UK migrants who have moved here but also for many Kiwis. So, I find myself, somewhat ironically, still doing a lot of work on the impact of British taxation.

It’s also been 20 years since I started Baucher Consulting and as I said in the podcast much has changed, and yet in some ways little has changed. One constant which hasn’t really changed is the behavioural impact of tax- this week’s discussion of the FIF regime is the latest example. I’d like to thank everyone who’s supported me over the these past 20 years.

Our fantastic guests

Looking at some other highlights of the year in terms of the podcast, we had a lot of great guests this year and my thanks again to all of them. My particular favourite episode was the Titans of Tax with Sir Rob McLeod, Robin Oliver and Geof Nightingale. Many thanks to Sir Rob, Robin and Geof for giving up their time. It was a fantastic discussion and very, very enjoyable. It was extremely well received all around. It was fascinating to just sit back and listen and to three experts who’ve been very heavily involved in the last three major tax working groups.

My thanks also to all my other guests this year, including the four finalists for this year’s Tax Policy Charitable Trusts Scholarship. Again, thank you so much for your input. Very interesting to talk to you, and the future of tax policy is in good hands.

Inland Revenue goes full throttle on compliance work

One of the big themes for the year, and less of a surprise, was Inland Revenue’s ramping up its enforcement approach. One of our guests very early in the year (and thanks again) was Tracy Lloyd, service leader of Compliance Strategy and Innovation at Inland Revenue. Tracy’s podcast was a really interesting one looking at what tools Inland Revenue is using and how it’s ramping up its investigative activities.

We’ve seen Inland Revenue’s more aggressive approach constantly through throughout the year. It has made announcements about cracking down on the construction sector, looking at liquor stores. Pretty much every week there’s a media release that another tax fraudster has been jailed or received substantial fines or home detention. In addition Inland Revenue is making use of information received through the Common Reporting Standards on the Automatic Exchange of Information.

These things will continue to come through. Inland Revenue got $116 million over four years to beef up its investigation activities and to improve its tax collection. As part of this we’re seeing a crackdown on student loan debt, which is a much more problematical issue mainly because the biggest portion of debt is held by persons overseas. It’s therefore not so easy to collect.

Inland Revenue’s activities will continue to ramp up but I think it may start to find there’s increasing push back as it clamps down. I think it’s previously been slow in responding, and during the COVID pandemic that was understandable. But right now, the faster it responds to debt issues developing, the better for all of us. Zombie businesses which linger on are no good to anyone.

The surprising continuing debate over capital gains

But the other big thing this year has been a surprising one. It’s the question of the shape of the tax system and persistent media stories about whether we should have a wealth tax or capital gains tax. This is a topic I don’t see going away. I see the pressure mounting on it because as, the Government’s main agency, Treasury, is pointing out we have ongoing demographic pressures in relation to superannuation and funding health.

And as I keep pointing out, we also have the question of climate change. We have insurers withdrawing cover and I think that means the Government will be expected to step in. And that means sharing the burden, which means ultimately some form of tax increases. All this means the composition of the tax base will continue to be a matter of debate.

Of course, we have options like capital gains tax, wealth taxes, or as Dr. Andrew Coleman suggested (another one of the fascinating podcasts this year) maybe we should rethink our issue of Social Security taxes, where again we’re a unique jurisdiction in that we don’t have them. We used to have such taxes way back from the early 1930s through until late 60s, before they were finally abolished,

So overall lots to discuss this year. I’d like to thank all my guests again, and all the listeners, readers and all those who chip in and comment away. Your comments are read and always welcome. And on that note, everyone have a very happy festive season. We’ll be back with what’s new in the tax world in January 2025.

One of the unseen revolutions in international tax over the last decade has been the adoption of the automatic exchange of financial account information. Also known as the Common Reporting Standards https://www.ird.govt.nz/crs this was developed by the Organisation of Economic Cooperation and Development, the OECD, in conjunction with G20 countries. It requires the automatic exchange of information on financial accounts – which is bank accounts, other investments held by taxpayers outside their jurisdiction. Financial institutions are required to provide information on such accounts to their respective tax authority which then sends that information to the jurisdiction in which that taxpayer is resident.

This project began in 2017. For the latest year, the tax authorities from 111 jurisdictions have automatically been exchanging information on financial accounts. And as I said, it’s a very broad range of investments, not just bank accounts. It’s all forms of investments. By and large, the public is pretty unaware of what’s happening here even though the numbers are significant.

€130 billion in tax interest and penalties so far

According to the latest peer reviewfrom the OECD, information from over 134 million financial accounts was exchanged automatically in 2023, and that covered total assets of almost €12 trillion. As a result, over €130 billion in tax interest and penalties have been raised by the jurisdictions through various voluntary disclosure programmes and other offshore compliance programmes.

Now the interesting thing here is that as a consequence of the introduction of the CRS, financial investments held in international finance centres or tax havens have decreased by 20% since the introduction of CRS in 2017. That’s a significant change. It means investments are moving into jurisdictions where they will be taxed. Over the long term that’s going to be quite significant for increased tax revenue around the world.

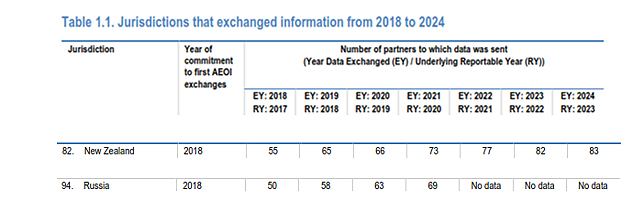

The full OECD report, which also discusses methodologies, runs to 248 pages, but the bulk of what people will be interested in is covered in the first chapter. Table 1.1. gives a summary of how many jurisdictions have been exchanging information, starting in 2018. According to the latest report the time of this report, 118 jurisdictions including New Zealand have started exchanging information.

Now the interesting thing to notice is the steady growth in the number of partners to which data has been sent. For example, the tax haven Anguilla in 2017 sent data to four countries but by 2023, it’s up to 67. The Cayman Islands, another key tax have sent data to 83 jurisdictions.

CRS and New Zealand

New Zealand began swapping data in 2018 when it sent information to 55 partners. For the latest year that’s grown to 83. Based on the early data exchanges Inland Revenue began a review programme in late 2019 which was then interrupted by COVID. However, it has now resumed its review programme, and I have one case at the moment which involves the taxpayer making the relevant disclosures after Inland Revenue enquiries based on data received through CRS. They won’t be the only one.

I was rather amused to see that Russia began exchanging data in 2018 when it sent data to 50 jurisdictions. But for the last three years no data is available. Wonder what’s happened there.

By the way the United States is not part of the CRS. That’s because it has something called the Foreign Account Tax Compliance Act, which basically was the model on which the current global CRS was built, and so it reports data separately.

How much data is Inland Revenue sharing?

I’ve tried unsuccessfully to obtain more detailed information on the data exchanges using the Official Information Act (the data exchanges are outside the OIA because of international treaty obligations which is fair enough). Notwithstanding this the impression I have is there are some huge numbers involved.

You have been warned…

What people should be aware of is that there’s a massive amount of data being circulated by tax authorities around the world right now. Many people may be oblivious to what’s going on. The likelihood is if you have an overseas financial account and you haven’t declared it for whatever reason, then it is quite likely that you will soon be asked a few questions about that by Inland Revenue.

Speaking about Inland Revenue, earlier this year they asked for consultation on their proposed long-term insight briefing (LITB). To quickly recap, LITBs are

“…future focused think pieces that government departments produce every three years. They provide information on long term trends, risks and opportunities that could affect New Zealand in the future, and policy options for responding to these matters. Their purpose is to help us collectively think about and plan for the future. They are developed independently of ministers and are not current policy.”

Back in August Inland Revenue proposed that its next long term insight briefing will explore what would be a suitable structure of the tax system for the future, and invited submissions by early October.

Inland Revenue has now published a summary of those submissions. In total, there were 35 submissions from 12 groups and 23 individuals. Most submissions were generally supportive of the topic. The rest, either suggested something completely different or were either ambivalent about it or did not actually specify whether they supported the project or not.

Seven themes in feedback

Inland Revenue’s picked out seven themes that came through from those submissions. Firstly, the fiscal pressures arising from superannuation and healthcare are a key trend and that’s one of the reasons behind Inland Revenue wanting to do a long term insight briefing on this topic. Most agreed with that, but several also added the question of increasing fiscal pressures arising from climate change.

My belief is its climate change that’s going to be the trigger point around changes to the tax system because that’s happening right now. And as damage from the floods grows and costs and insurers look increasingly wary about insurance, people will be looking to the Government for support.

The second theme was keeping flexibility in the tax system. In its submission EY commented

“We agree improvements to system flexibility should be the focus for this LTIB. In particular, working through options for system integrity in the context of tax rate increases is in our view, important.”

The devil is in the detail

A third theme was the analysis needs to consider policy design details and looking at first principles. Chartered Accountants of Australia and New Zealand made the comment that “Sometimes it is the detail that can make things unworkable. The framework should consider the merits of expanded tax bases with different design parameters”.

Another theme – and this is something I think I would endorse – the analysis needs to consider the tax and transfer system interaction. There were a few submissions pushing very strongly on that point.

A fifth theme proposed considering corrective taxes. The Young International Fiscal Association Network suggested that environmental taxes would fit well with Inland Revenue’s proposed topic because of the long term environmental trends.

The impact of technology

Another theme was the question of technological change and how that will affect the sustainability of tax bases. Earlier this year an IMF report on the impact of artificial intelligence suggested changes to tax systems could be needed.

Some submitters emphasised that it was important to consider how the tax system impacts a wider range of social outcomes. These included Doctor Andrew Coleman who was broadly in support of what was in the proposed LTIB. He suggested that they need to look at a wider range of retirement savings reforms, which would be no surprise to anyone who listened to the podcast with Gareth Vaughan and myself earlier this year. Several other submissions suggested how tax system could support productivity.

Finally, there were suggestions about considering progressive consumption taxes, which hasn’t really been looked at in any detail in New Zealand.

How Inland Revenue will proceed

Following this feedback Inland Revenue has said the LTIB will discuss the arguments for lower taxes on savings and the question of the tax treatment of retirement savings as part of a discussion about social security taxes. This is an interesting development because as the consultation noted generally, most jurisdictions have social security taxes which represent somewhere around 25% of total tax revenue. Whereas we don’t have them at all. This was a point Dr Coleman made in the podcast so it’s good to see Inland Revenue will be looking at that.

No to considering financial transaction taxes

As part of managing the whole scope of the LTIB Inland Revenue believes it “could reduce the discussion of some tax bases are less likely to be subject of significant public discussion such as financial transaction taxes.” This makes sense. Financial transaction taxes or Tobin Taxes are something that pop up in discussions about tax reform. I’m ambivalent about whether in fact they will achieve what people make out for them. I think they would add complexity and they would drive all sorts of different behaviour.

They’re not going to do a full review of the interaction of the tax and transfer system. And to be fair to Inland Revenue, I think that would be an entire long-term insight briefing of itself. But their chapter on consumption taxes discussed using transfers to offset GST rate increase somewhat similar to what Andrew Paynter proposed last week. (Just to repeat Andrew’s proposal is his alone and does not reflect any Inland Revenue policy). According to Inland Revenue the tax regimes chapters “will largely focus on how to make our main tax bases more flexible to rate changes, including considering options to support system coherence and integrity.”

Providing an analytical base

In summary Inland Revenue’s intention

“…is to provide an analytical base to provide further consideration of these issues in the future. For example, our focus on tax bases is on understanding the relative costs of taxing different underlying factors and what the overlaps and differences are in those tax bases. Our focus on tax regimes is on exploring how to make our tax based main tax bases more flexible to rate changes without undermining equity or efficiency goals.”

All of this seems perfectly reasonable to me.

From here there will be a future opportunity to provide feedback when Inland Revenue releases a draft of its briefing for public consultation in early 2025. It will then be finalised and given to Parliament in mid-to-late 2025.

Sir Roger Douglas’s radical proposals

Inland Revenue have also published all the submissions, from those who gave permission to do so, adding up to 175 pages of submissions, from individuals and organisations alike. It’s interesting to dip in and see what is being suggested on the topics. Sir Roger Douglas was one of the submitters and as you might expect, the old warrior is still looking for something radical.

Part of his proposal is a tax-free threshold of $62,000. But the trade-off is most of that gets put into retirement and health accounts. With the proposed retirement account, he’s probably reflecting the thinking of Andrew Coleman about the need for the current generation to start saving in earnest because of the various pressures coming towards us. Can’t say I agree fully with Sir Roger’s proposal but full marks for boldness.

Feedback on Andrew Paynter’s proposal

And finally, this week, to pick up a little bit from last week’s podcast with Andrew Paynter and his proposal to increase GST by 2.5% points to 17.5%, but then with a rebate for low- and middle-income earners. The transcript has been very well read and generated a phenomenal number of comments, over 150 at last count, and I thank all the readers and commenters for that.

What about the self-employed?

One commenter asked a question which we didn’t cover off during the podcast; how would Andrew’s proposal apply to the self-employed? The answer is it would use something similar to the provisional tax system. A person’s income would be uplifted from last year and if you’re in the range then you qualify for the proposed payments.

Last week Tax Management New Zealand and the Young International Fiscal Association network ran a joint presentation for the two winners, Andrew and Matthew to come and present their proposals. If you recall, Matthew proposed expanding the withholding tax regime to contractors. Andrew and Matthew both made excellent presentations to a very engaged crowd, and I can see why the judges had a difficult time splitting the pair. So well done again.

Left-to-right Matthew Seddon, Terry Baucher and Andrew Paynter

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week the ninth edition of the OECD’s Tax Policy Reforms was released. This is an annual publication that provides comparative information on tax reforms across countries and tracks policy developments over time. This edition covers tax reforms in 2023 for the 90 member jurisdictions of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

Reversing the trend

It’s a fascinating document which tracks trends of what’s happening around the tax world at both a macro and micro level. The report has three parts: a macroeconomic background, then a tax revenue context, and then part three is the guts of the report with details of tax policy reforms around the world.

There is an enormous amount in here to consider and the executive summary lays out the ‘balancing act’ issues pretty clearly.

“Policymakers are tasked with raising additional domestic resources while simultaneously extending or enhancing tax relief to alleviate the cost-of-living crisis… On the one hand, governments further protected and broadened their domestic tax bases, increased rates, or phased out existing tax relief. On the other hand, reforms also kept or expanded personal income tax relief to households, temporary VAT [GST] reductions, or cuts to environmentally related excise taxes.”

A key observation for 2023 was a trend towards reversing the responses to the COVID-19 pandemic. Instead, as the report notes “2023 has seen a relative decrease in rate cuts and base narrowing measures in in favour of rate increases and base broadening initiatives across most tax types.”

“A notable shift”

This includes “A notable shift occurred in the taxation of business, where the trend in corporate income tax rate cuts seems to have halted with far more jurisdictions implementing rate increases than decreases for the first time since the first edition of the Tax Policy Reforms report in 2015.”

This is a pretty significant change. I think actually when you consider last week’s speech by Dominick Stephens of Treasury, it was setting out the context for why having got over the crisis of responding to the pandemic, countries are realising they’ve got to deal with the demographic issues of ageing populations and funding superannuation.

Climate considerations

Beyond these concerns, there is the immediate impact of climate change and its growing effects. The executive summary picks up on this issue:

“Climate considerations are also increasingly influencing the design and use of tax incentives, with more jurisdictions implementing generous base narrowing measures to promote clean investments and facilitate the transition towards less carbon intensive capital.”

And on that point, I hope all the listeners and readers down in Dunedin and Otago are safe and well at the moment.

Paying for superannuation

The other thing picked up is that in referencing that point I made a few minutes ago about population ageing. There has been a growing trend amongst countries to increase Social Security contribution taxes. Alongside Australia, and to a lesser extent Denmark, we are unique in that we don’t have social security contributions. However, elsewhere in the OECD social security contributions raise increasingly significant amounts of revenue.

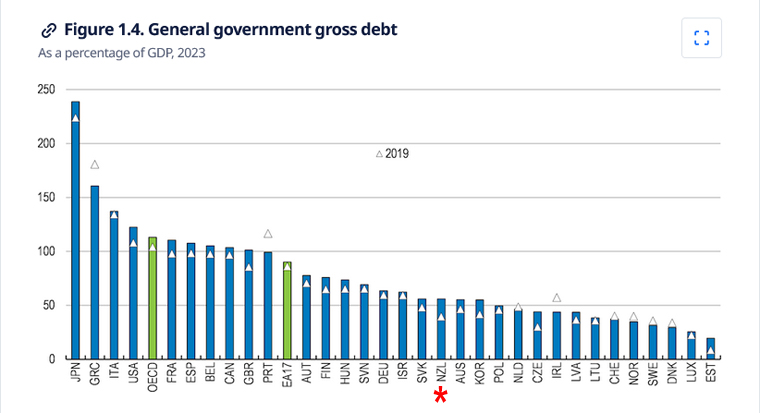

The report begins with a macroeconomic background. It notes that for the OECD as a whole in 2023 government debt rose by about nine percentage points, reaching 113% of GDP. For context, New Zealand’s debt-to-GDP ratio is just over 50%.

As the macroeconomic summary notes after generally decreasing in 2022 Government deficits increased again in 2023 following the energy crisis triggered by the war in Ukraine. Consequently,

“As debts and interest rates increased, interest payments have started to rise as a share of GDP. Even so, in 2023 they mostly remained below the average over 2010 to 2019, except notably for Australia, Hungary, New Zealand, the United Kingdom, and the United States.”

In short, we definitely have issues to deal with in terms of debt management and rising costs.

Responding to growing deficits

The report then notes that responses to growing deficits have been to start at increasing taxes. In general tax revenue terms,

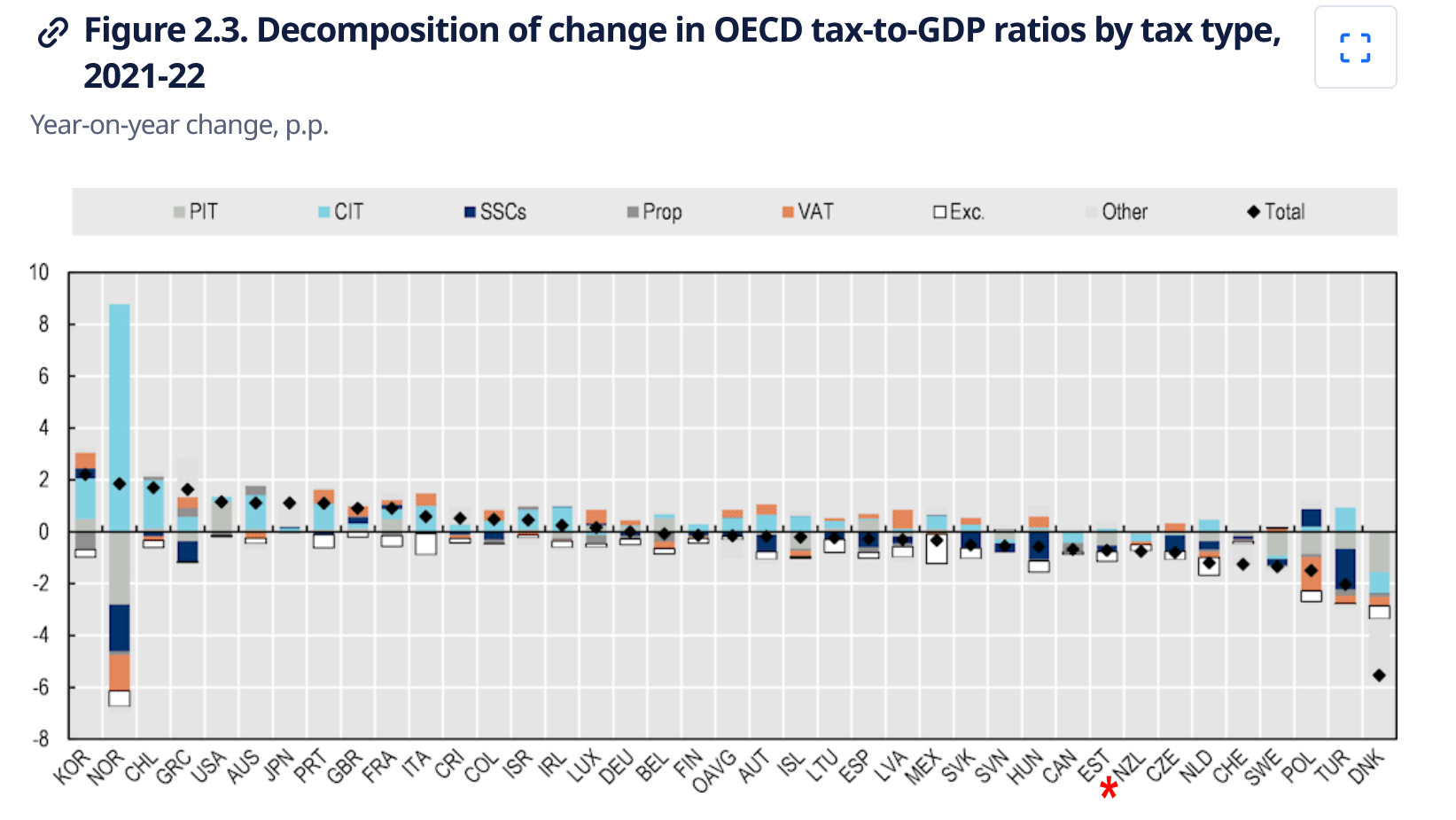

“From 2020 to 2021, the tax-to-GDP ratio rose in 85 economies with available data for 2021, fell in 38, and stayed the same in one. In more than half of these economies, the change in the tax-to-GDP ratio was under one percentage point, whereas 22 economies saw shifts greater than two percentage points in their tax-to-GDP ratio.”

Denmark saw the most significant drop of 5.5 percentage points, with New Zealand’s tax-to-GDP ratio falling by three-quarters of a percentage point, well above the OECD average fall of .147 percentage points. (Norway’s dramatic corporate income tax take increase of 8.775% is the result of “extraordinary profits in the energy sector”.)

Composition of tax base

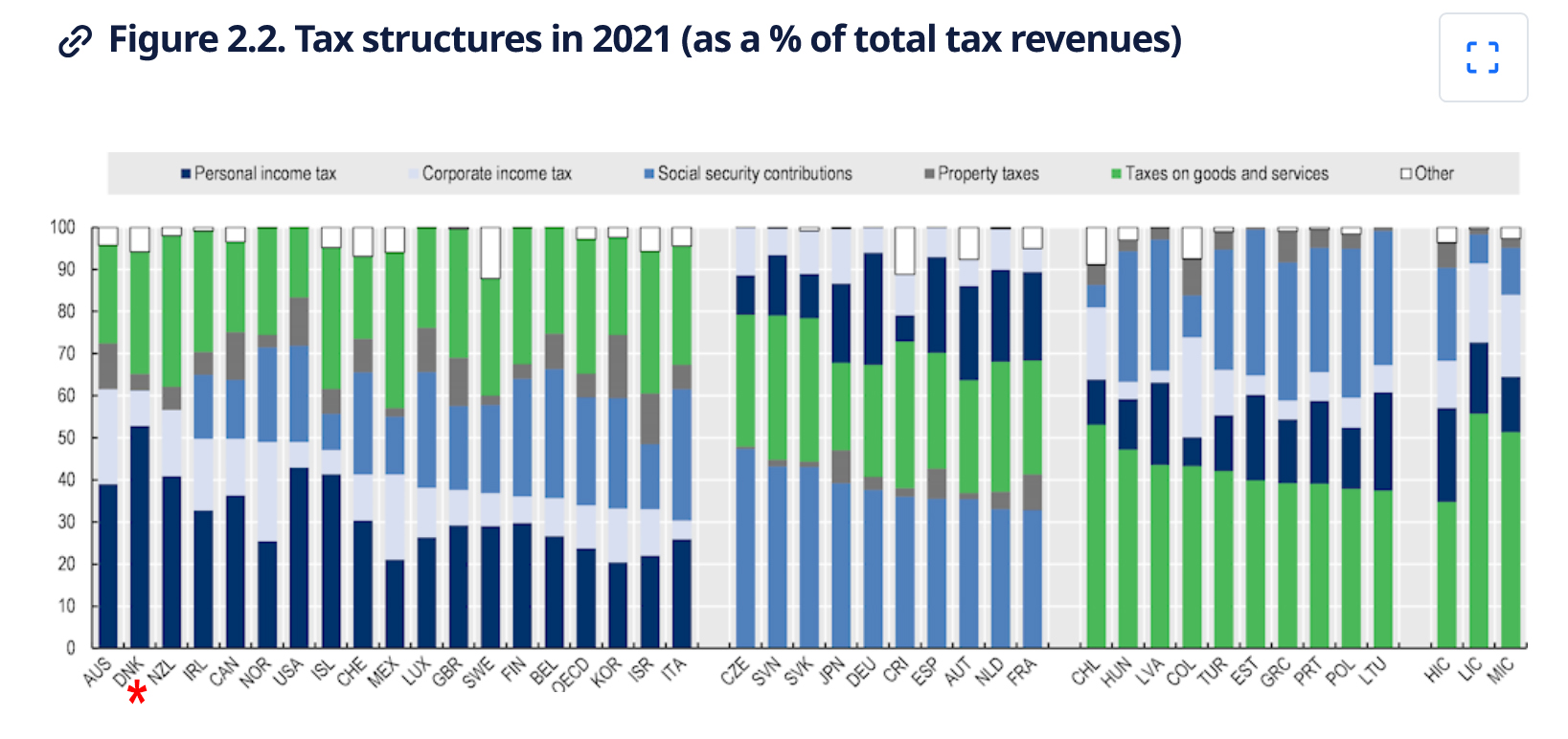

With regards to the composition of tax, 18 OECD countries (including New Zealand) primarily generate their revenues from income taxes, including both corporate and personal taxes. Ten OECD countries relied most heavily on Social Security contributions, and another 10 derived the majority of the revenues from consumption taxes, including VAT, (GST). Notably, taxes on property and payroll taxes contributed less significantly to the overall tax revenue mix in OECD countries during 2021.

Drilling into the detail

Part 3, of the report looks at the detail of the tax policy reforms adopted during 2023. This part has an introduction, then looks at five separate categories of taxes beginning with personal income tax and Social Security contributions, followed by corporate income tax and other corporate taxes, taxes on goods and services, environmentally related taxes and finally taxes on property.

As I mentioned previously, there was “a marked increase in the number of jurisdictions that broadened their Social Security contribution bases and raised rates”. Generally speaking, for high income countries personal income tax and social security contributions represent 49% of total tax revenue. Across the OECD personal income tax represented 24% and social security contributions 26% on average.

Here about 40% of all tax revenue comes from personal income tax. That’s one of the higher proportions around. Around the globe there was a bit of tinkering around personal income tax reforms mainly targeting lower income earners. This is an area where I think we need to focus any future reforms.

We have just (partly) adjusted thresholds for inflation and interestingly, I see that during 2023 quite a few jurisdictions did increase thresholds for inflation. For example, Austria updated its automatic inflation adjustment mechanism to counteract inflation, pushing workers into higher brackets. Meanwhile Australia increased its threshold for its Medicare levy to ensure low income households continue to be exempt, given that inflation has led to higher normal wages.

Corporate income tax rates are on the rise

Substantially more corporate income tax rate increases and decreases were announced or legislated by jurisdictions in 2023. Six jurisdictions increased their corporate tax,four of those did so by at least two percentage points. Türkiye increased all its corporate tax rates by five percentage points.

Whenever there are discussions about reforming our tax system, the issue of reducing our corporate tax rates will come up. With a 28% rate we are at the higher end of the corporate tax rate scale. There is potentially some scope, but as economist Cameron Bagrie has noted any such decrease needs to be part of a broader range of changes.

An example of such a change was the introduction of a general capital gains tax by Malaysia for all companies, limited liability partnerships, cooperatives and trusts from 2024.

Picking out of the details something which I know businesses here would look at with a certain amount of envy is more generous depreciation allowances. The UK, for example, has permanent full expensing for main rate capital assets as it’s called and a 50% first year allowance for special rate assets. Australia has also increased its thresholds for effectively fully expensing items for small businesses. Around the world there’s a whole range of incentives for R&D and environmental initiatives.

We have just limited the limits for residential interest deductions but it’s interesting to see that Italy abolished its allowance for corporate equity provision. Meantime Canada has new restrictions on net interest and financing expenditure claimed by companies and trusts.

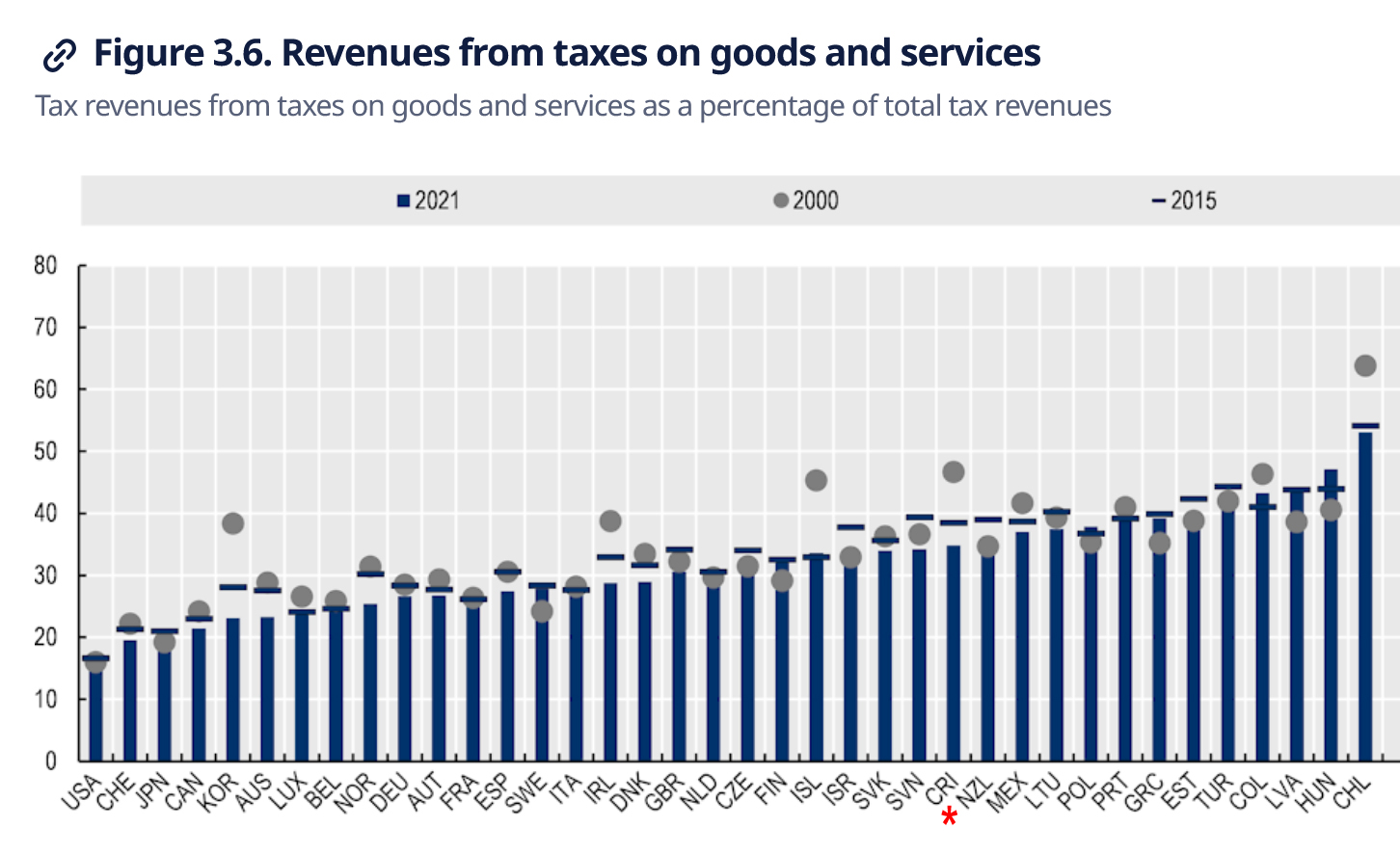

Taxes on goods and services (VAT/GST)

In the VAT/GST space, in terms of revenue from taxes on goods, although we have one of the most comprehensive GST systems in the world, New Zealand was only twelfth in the OECD for the percentage of tax revenue from goods and services as a percentage of total tax revenues. GST raises just over 30% of total tax revenue here, whereas Chile raises over 50%. This is quite interesting given how comprehensive our GST system is. It might mean that there is scope to expand the the rates of GST further. (Six countries including Estonia, Switzerland and Türkiye did so in 2023). But any government doing so should do so as part of a total tax switch package.

We discussed GST registration thresholds a couple of weeks back. During 2023 seven countries increased or planned to increase their VAT registration threshold. I was very interested to discover that Ireland has a split VAT registration threshold treatment: the registration threshold for the sale of goods is €80,000. But for the provision of services, it’s €40,000. I’ve not seen this split before. Meanwhile Brazil is undertaking the introduction of VAT/GST, which is a huge step forward.

A stable tax policy or just less tax activism?

There’s a lot to consider in this report more than can be easily covered here. Overall, it’s incredibly interesting to see what’s going on around the world. Many of the reforms discussed here involve threshold adjustments but there are plenty of new exemptions and incentives introduced. We generally don’t get into this space, that’s possibly a reflection of a very stable tax policy environment, but also perhaps a less activist philosophy by New Zealand governments which hope market incentives will work. Whatever, the approaches it’s interesting to see what’s going on around the world and I recommend having a look at this very interesting report.

ACC crackdown

Moving on, ACC has been in the news when it emerged that it has been chasing thousands of New Zealanders for levies on income they earned while working overseas.

According to the RNZ report, ACC sent 4,300 Levy invoices for the 2023 tax year to New Zealand tax residents who had declared foreign employment or service income in their tax return. The issue is that the person was often overseas at the time the income was earned and in some cases the the person has probably incorrectly reported the income in their return.

It’s an interesting issue and coincidentally, it so happens that I’ve just come across a couple of similar instances. My initial view is there seems to a bit of a mismatch between the relevant income tax legislation and the legislation within the Accident Compensation Act 2001. Watch this space on this one because I’m not sure the matter is entirely as cut and dried as ACC considers.

Inland Revenue responds to social media criticisms

A couple of weeks back, we covered criticism of Inland Revenue for providing the details of hundreds and thousands of taxpayers to social media platforms. It had done so as part of various marketing campaigns targeting people who owed taxes and Student Loan debt in particular.

Inland Revenue has now responded by putting up a dedicated page on its website, referring to customer audience lists.

In its words “social media is just one channel we use to reach customers. It is very effective at reaching people where they are.” As I said in the podcast Inland Revenue’s dilemma is it has to go to where the people are which is on the social media websites. In order to reach out to them it’s going to have to provide certain data. To reassure people the new page explains how it uses custom audience lists and what data is provided.

They do upload a list of identifiers such as name and e-mail addresses, which is then ‘hashed’ within Inland Revenue’s browser before being uploaded to the social media platform. This is where I think the tech specialists have raised concerns that the hash technique is not as secure as Inland Revenue thinks.

Australia – the Lucky Country again

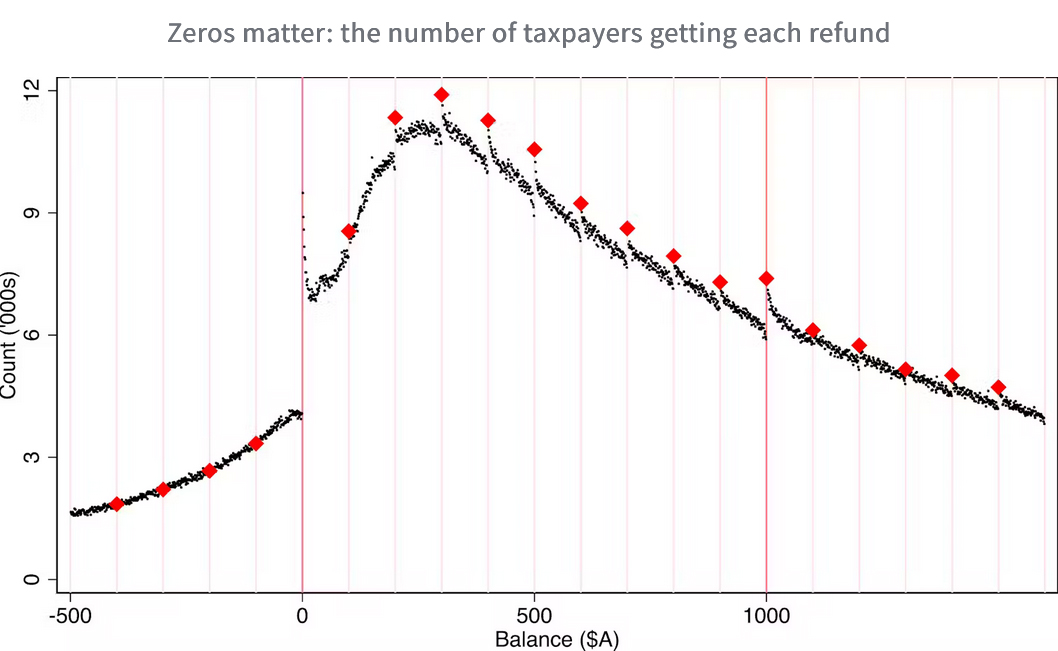

And finally, an interesting story from Australia about tax refunds. A research team at the Australian National University’s Tax and Transfer Policy Institute discovered a “striking” number of returns generating round number refunds (basically any digit ending in zero). The unit examined 27 years of de-identified individual tax files and found far more refunds of exactly $1,000 than of $999 or $995.

The unit concluded these returns are more likely to be driven by efforts to evade and minimise tax and are costly for the Australian Tax Office to audit such as work related expense deductions. Unlike New Zealanders, Australians can claim deductions on their tax returns. Somewhat concerning to me as a professional is that zeros in tax returns prepared by agents were twice as common as those prepared by taxpayers.

What this article is driving at is that some of the complexity of the Australian system results in the system getting gamed. Back in February you may recall Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue was a guest on the podcast. Based on our discussion and my own observation I would have confidence that Inland Revenue would not get caught out the same way thanks to the Business Transformation programme. As Tracy recounted, Inland Revenue can track live changes and they can see people just trying to square the return off to what they regard as an acceptable number.

Anyway, it’s an interesting story. It shows the differences between our tax system and that of Australia, but it does seem a little rich that not only can you earn more in Australia, but you get bigger refunds.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Should the New Zealand Superannuation Fund become tax exempt? Inland Revenue is under scrutiny for its use of social media.

A bad week for Apple and Google in the European courts.

Inland Revenue releases an intriguing consultation on GST and management services supplied to managed funds.

In the past few weeks, the question of taxing capital has reappeared on the agenda featuring across a number of news stories. It probably kicked off initially when Inland Revenue’s long term insights briefing consultation document raised the question of whether the tax base should be expanded to meet what is the anticipated growing fiscal costs of superannuation, health and climate change.

“New ways of generating revenue”

Then a couple of weeks back, the outgoing chief executive and Secretary to the Treasury, Caralee McLiesh, commented to the New Zealand Herald that New Zealand needs new ways of generating revenue and cutting expenditure. She suggested a capital gains tax and a more efficient superannuation scheme.

Labour leader Chris Hipkins has been in the news talking about the Labour Party’s internal discussions around the question of taxing capital. And then at the start of the week, Bruce Plested billionaire co-founder of Mainfreight, raised the idea of wealth tax. Understandably he caveated it with a question around whether the funds raised would be spent wisely.

But the point is, across the whole spectrum the question of taxing capital is back on the agenda. It never actually goes away to be perfectly honest. Like spring it comes around at least once every year. Anyway, it’s interesting to see this debate carried on. I think a driving factor is a growing recognition that the present tax base probably isn’t sufficient to meet the coming demands of rising superannuation, rising health costs and climate change. Sure, managing government expenditure more efficiently will help, but it will only go so far.

The Treasury has talked about a structural deficit of 2% of GDP which is $8 billion. That’s a fairly sizable sum, and with the best will in the world, cuts in government spending aren’t going to fill that gap. So, a discussion has to be had on how this gap is to be filled.

Given we will need to find extra revenue, taxation of capital is the obvious point. We should be considering whether it’s a wealth tax, land tax, capital gains tax or even restoration of estate and gift duties, which were once quite a substantial part of the New Zealand tax base. It could be a combination of all or some of those, but the debate isn’t going away.

Time to make the New Zealand Superannuation Fund tax exempt?

Moving on, and talking about the rising cost of superannuation, the New Zealand Superannuation Fund (NZSF) was established more than 20 years ago by Michael Cullen, to help smooth the cost of superannuation. It has been an enormous success. The NZSF has now grown to well over $70 billion and along the way it has been paying tax.

This is quite unusual for sovereign wealth funds because most are tax exempt. New Zealand has two other sovereign wealth funds, ACC and the Reserve Bank of New Zealand, and neither of those are taxed. They have between them another $60 billion of assets. But when the NZSF was established back in 2003, the decision was taken that it would pay tax. Part of the reason for doing so was to provide a commercial incentive so the NZSF made decisions around investments on strong commercial grounds, rather than because of a tax-exempt status.

But this has created a sort of slightly odd money-go-round. The government would contribute capital to it based on a formula, and then the NZSF would then pay part of that back in the form of tax. This is before its designated drawdown date, which is coming up towards the latter part of this decade, when it’s expected that regular withdrawals will be made to start funding superannuation.

For the period to June 2024, the Super Fund received contributions of roughly $1.6 billion overall and paid nearly $1.5 billion in tax. It is by far and away the largest single taxpayer in the country, a reflection, by the way of our Foreign Investment Fund regime rules. Finance Minister Nicola Willis is now seeking advice as to whether in fact it should become tax exempt, on the basis now that its tax bill is beginning to outgrow crown contributions.

Now that the Government has contributed $16.9 billion after accounting for $9.6 billion in tax paid since the fund was set up, the Finance Minister will be thinking whether it’s now time the Government can wind back the contribution. Ultimately, this should have the same effect as also removing its taxable status. We shall see how this develops, but it’s interesting to see the discussions in this space, which are also a by-product of the question of how do we fund superannuation?

Inland Revenue under fire

Moving on, Inland Revenue is in a little bit of hot water after it emerged that it’s giving hundreds of thousands of taxpayers’ details to social media platforms as part of its various marketing campaigns. These campaigns are intended to target taxpayers who might owe taxes.

Unpaid student loans are one particular area that that pops up here. The controversy revolves around the anonymisation tool which is used to ensure that whatever information the social media companies get, the details are minimised as far as possible to protect the privacy of the taxpayers involved.

The question has been raised as to whether that tool is sufficient.

The horns of a dilemma

There are two issues here. One is the technical question about how effective is the anonymisation tool. But the bigger question is whether Inland Revenue should be doing that. It faces a problem that if it wants to reach out to the general public – or certain sectors of the public – to remind them about their tax obligations. The best outreach method is through social media platforms. Inland Revenue is on the horns of a dilemma.

I will say this, that in my 20-30 years’ experience watching and working with Inland Revenue, it has an exemplary record around disclosure of private details. It has strong processes in place, and I cannot recall over that time a data breach scenario similar to those we’ve seen with both ACC and MSD where private data of taxpayers has been emailed to persons outside the agency.

Notwithstanding Inland Revenue’s record, the practice seems questionable because of the fact that social media sites are constantly under attack from hackers. Supplying private information to social media companies, no matter how laudable the intentions, puts that data at risk. It would be interesting to hear from the Privacy Commissioner on this.

Then there is the huge irony that these social media companies are amongst the most aggressive exponents of tax planning in in the world. For the year ended 31st December 2023 Facebook New Zealand, for example, reported taxable income of $9.1 million, but we know from its accounts that it paid over $157 million offshore to related entities. And Google’s numbers are even bigger. The extent of the advertising now going offshore has absolutely gutted local media and the implications of this loss of revenue for our media landscape are still being worked through.

Inland Revenue has to work through the dilemma as to how far it should go with providing information to social media companies. Ideally, you’d say it should not. But if you want to reach out to taxpayers about their obligations, you have to go where you might find those taxpayers. And at the moment that’s the social media companies.

Apple and Google lose bigly in Europe

Speaking of the big tech companies, over in Europe, Google and Apple had a week to forget. The European Union’s top court the Supreme Court of the European Court of Justice (the ECJ) ruled that Google must pay a €2.4 billion fine for abusing its market dominance of its shopping comparison service. This fine had been levied by the European Commission in 2017, and Google has been fighting it since then but has now lost in the ECJ, the highest court in Europe.

But that news was overshadowed by a major tax decision by the ECJ the same day, ordering Apple to pay Ireland €13 billion. That’s an eye watering $23.3 billion the equivalent of just over 12. 5% of Ireland’s total tax revenue for 2023.

What’s particularly interesting about this case is that Ireland was also a defendant alongside Apple. Ireland had been accused by the European Commission of having given Apple illegal tax advantages in the form of state support. The European Commission ruled the state support was illegal in 2016. Apple appealed and won in the lower court of the ECJ in 2020. But now the ECJ’s Supreme Court Justice has ruled that there was illegal state support which must be repaid.

A major transfer pricing decision

This is going to be a key transfer pricing case which will be analysed for many years to come because it revolves around the way profits generated by two Apple subsidiaries based in Ireland were treated for tax purposes. The ECJ ruled these arrangements were illegal because only Apple was able to benefit from them. Other companies based in Ireland could not.

This is just the latest instalment of the general crackdown that Europe is going through right now about transfer pricing and other profit shifting mechanisms led by the European Commission. The decision is an enormously important case in the transfer pricing world.

It actually leaves Ireland in a little bit of an embarrassing case because, as I said, it’s an enormous sum of money, so people will be naturally saying, well, what are we going to do with this? The Irish Treasury has warned against using this for anything other than perhaps a one-off major capital project or debt repayment.

But the Irish also appear to be quite concerned about how their low tax regime (they have a corporate tax rate of 12.5%) will be perceived by other companies who would like to invest in Ireland which has pursued a long-term policy of attracting investment. Its industrial strategy was shaped in the late 50s, but really only started to come to fruition once Ireland joined the European Economic Community in 1973.

I would be very interested to see how this massive decision plays out in other jurisdictions and what lessons are taken by transfer price practitioners.

GST and managed funds – round two?

Finally this week, Inland Revenue has been busy releasing a number of draft consultations on a range of subjects, including Commissioner of Inland Revenue’s search and information gathering powers, the income tax treatment of short stay accommodation, arrangements involving tax losses carried forward under the business continuity rules, and a big paper on the income tax company amalgamation rules.

However, the one that’s got me a little bit intrigued because of its back story is a consultation on the GST treatment of fees paid in relation to managed funds. If you recall back in August 2022, the then Labour government introduced a tax bill which included a measure which would impose GST on management services supplied to managed funds.

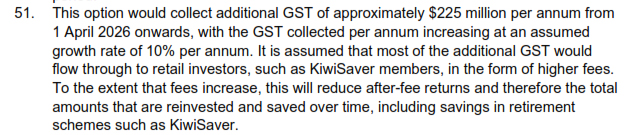

According to the supporting Regulatory Impact Statement that measure was to tidy up an anomaly that had been identified by a GST issues paper released by Inland Revenue In February 2020, just before COVID arrived. It was projected to bring in an estimated $225 million a year starting from 1 April 2026.

A furore erupted after the same regulatory impact statement noted that was according to modelling by the Financial Markets Authority, the impact of imposing GST on management fees would mean that the amount available for KiwiSaver investors would be reduced by an estimated $103 billion by 2070. For context, it’s worth pointing out that the KiwiSaver funds were projected to be valued at nearly $2.2 trillion. In an unprecedented move, Labour backed down and withdrew the bill within 24 hours.

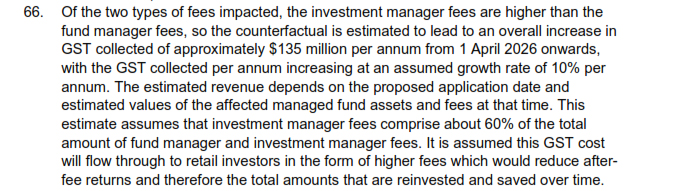

Against that background, it’s interesting to see Inland Revenue’s final consultation on the same topic. And this is where I’m intrigued to know a little bit more about what’s changed. Basically, it seems that Inland Revenue is going back to a default position where manager fees are treated as exempt, but investment manager fees become subject to 15%. The proposal in 2022 was all fees become subject to GST at 15%.

An intriguing counter-factual

What intrigues me is that the 2022 Regulatory Impact Statement noted as the counterfactual that this would probably result in something like an overall increase in GST collectible of approximately $135 million per annum from 1 April 2026 onwards. That’s not an insignificant sum of money.

Although Inland Revenue’s job is to provide interpretation and guidance, my thoughts on this are if this is a sum that’s going to potentially raise $135 million dollars of tax annually, maybe that’s something that Parliament should legislate.

There is also a subsidiary issue here which is a long-standing issue in our tax system at the moment. It is surprising, given that this was a controversial point, that this issue had not reached the courts, or that no one has taken a test case.

So, although Inland Revenue is doing its job, given the sums apparently involved I think that is something that should be put into legislation and go through the Select Committee process. But for the moment though, Inland Revenue is consulting on the issue until 25th October. As always, we will bring you any news and developments as they emerge.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The one thing that wasn’t in there, which I was expecting, was a move by Inland Revenue to restrict the use of portfolio investment entities with a maximum rate of 28%. These are increasingly being used by trusts and individuals subject to the 39% top tax rate. I’ve had a feeling for some time that this might be something that Inland Revenue was looking at, and maybe this bill would see some action on that part. But nothing, so far.

Preparing for emergency events

Instead, there’s a number of key initiatives and a lot of remedial measures. The first key measure relates to developing a generic response to emergency events. This sounds pretty mundane but what’s intended here is to enable Inland Revenue to be quicker in responding to provide tax relief following any emergency events.

What’s proposed is to build in tax relief measures into the legislation, which then can be activated by an Order in Council. This has been something that Inland Revenue has had to do rather a lot recently. As the commentary to the bill notes there have been three national emergencies declared in the last 15 years, where Inland Revenue’s basically had to apply some discretion to provide some measures of tax relief. Those were the February 2011 Christchurch earthquake, the COVID-19 pandemic and then the flooding in the wake of Cyclone Gabrielle last year. Cyclone Gabrielle came hot on the heels of the Auckland Anniversary weekend flood. Then there was also a huge earthquake in Hironori Kaikoura in 2016, which was a local emergency.

This bill proposes to introduce primary legislation which will enable Inland Revenue in the wake of an emergency event to use an Order in Council to activate these measures so it can respond to the emergency event.

I think it’s a good move. The COVID response in particular, showed that there was a need for greater discretion for Inland Revenue in certain areas, and in fact the Finance and Expenditure committee suggested last year that some form of this measure was needed.

It’s a fact of the times that we need such a measure, and incidentally also supports my long-standing view that it’s climate change which is going to hit the balance sheets first, and we need to be responding to that.

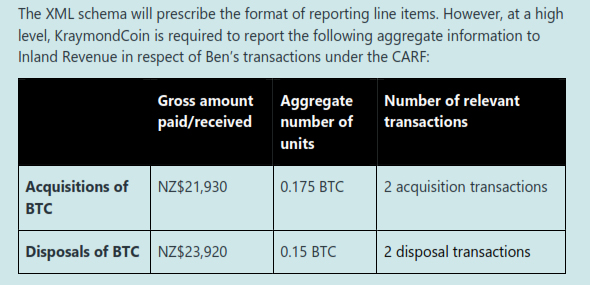

Crypto-asset reporting framework

The Bill also introduces the legislation required to implement the Crypto-Asset Reporting Framework (CARF), an OECD initiative, which is planned to take effect from 1st of April 2026. From that date New Zealand-based reporting crypto-asset service providers would be required to collect information on the transactions of reportable users that operate through them. The providers would then need to report any information for the year ended 31st March 2027 to Inland Revenue by 30th of June 2027. And then Inland Revenue would exchange this information with other tax authorities to the extent that it did come across information that a user of a platform in in New Zealand was actually resident elsewhere.

(Example of information reporting required)

As the commentary to the Bill notes, the market for crypto assets has grown enormously and there are now more than 22,000 crypto assets with a total market capitalisation of that is now close to NZ$4 trillion. This is up from barely US$17 billion back in 2017. According to the commentary between 6% and 10% of New Zealanders own some crypto-currency and Inland Revenue analytics show that 80% of crypto-asset activity by New Zealanders is undertaken through offshore exchanges.

There are some interesting notes in the accompanying Regulatory Impact Statement that once this is all up and running, Inland Revenue expects to be gathering about $50 million a year from it. In the meantime, a colleague has told me about a client who was using the Binance platform who has received some queries from Inland Revenue. The CARF initiative once implemented will boost Inland Revenue’s audit activities in this area.

Foreign superannuation scheme transfers – a good fix for a bad policy?

The next couple of measures relating to foreign superannuation scheme transfers and the Approved Issuer Levy are good to see, but also raise some interesting policy questions.

Under our current foreign superannuation scheme rules, if you transfer a foreign superannuation scheme into New Zealand or withdraw funds from the scheme (the money doesn’t necessarily have to reach New Zealand), you trigger a liability.

What has been an issue all along, particularly for Britons, is if they transfer their overseas scheme into a Qualifying Recognised Overseas Pension Scheme – or QROPS – they trigger a tax liability but may have no access to the funds, because they’ve not reached the age in which they’re allowed to do so under UK pension law. Any attempt to do so would trigger what’s called an unauthorised payments charge which could be up to 55%.

This was a problem that was identified with the legislation when it was first proposed back in 2013. Thanks in part to COVID, it’s taken this long to come up with a workable solution which is to kick in from 1st April 2026. From that date there will be a “Scheme Pays” option, under which the receiving scheme will calculate the tax due and pay that on behalf of the transferring client. The receiving scheme will do so at a flat rate of 28%, which is the prescribed investor rate. Transferring clients will have the option to fund the tax liability out of their own pockets, presumably because their marginal tax rate is 10.5% or 17.5%.

As I said, it’s a solution to a long standing problem. I am not a fan of the foreign superannuation scheme rules. It seems to me that we are taxing the importation of capital. People are bringing capital into the country and yes, they have benefited from an overseas tax regime. Conceptually, what we do ties in with our tax policy and in particular, the Foreign Investment Fund regime.

A ‘highly problematic’ regime?

But those of you who have been reading Dr Andrew Coleman’s recent articles will know our tax regime in relation to the taxation of savings is quite unique. I think in this area it’s highly problematic. People are bringing overseas savings and currency, into the country and we are essentially taxing them for that. Now looking at the bigger macroeconomic picture, that doesn’t seem to make a lot of sense to me. It’s conceptually correct from our taxation perspective, but it seems nonsense. This has always been my view, and I’ve still not received a satisfactory explanation other than “Well, that just fits in with our tax regime.”

My second point here is with the proposal for schemes to apply the prescribed investor rate at 28%. The Regulatory Impact Statement notes that on average the tax rate transfers is about 29%. Now the reason we tax foreign superannuation scheme transfers is so that people who have overseas pension schemes don’t have an advantage relative to their New Zealand counterparts, who would be in KiwiSaver funds, which as prescribed portfolio investment entities have a maximum prescribed investment rate of 28%.

Over taxation of transfers?

This begs the question as to why these transfers have been taxed at a person’s marginal tax rate which in some cases would be 39%. Surely if we are saying we’re looking to try and prevent a disadvantage, the top rate that should have been applied was 28%. That’s not discussed in the commentary or the Regulatory Impact Statement. But I will raise it in my submission to the Finance and Expenditures Committee and see what develops of it.

I was also interested to see the numbers of people that are affected by this seem to have been dropping off. According to the Regulatory Impact Statement, 2,700 individuals reported a foreign superannuation scheme withdrawal or transfer in the 2022 income year. For 2023 the number was 458 with 113 reporting the amount was mainly sourced from the UK. That’s quite a drop off.

The “Schemes Pay” solution has taken a long time to get here. I’ve been involved as part of the group that’s worked with Inland Revenue on this policy measure, so I’ll give it a qualified pass. But I still think the bigger issue as to why we are taxing these transfers in the first place really should be addressed properly.

Changes to the Approved Issuer Levy – fixing a problem but not addressing the cause?

Another good measure which also resolves a long-standing issue, involves the Approved Issuer Levy regime. Where a person pays interest to a non-resident lender, the payer is required to withhold non-resident withholding tax (NRWT). Alternatively, if the interest payments are being made to non-associated lenders, then you can register to apply to register the loan and instead deduct the 2% Approved Issuer Levy (AIL) and that’s what most people do.

According to the Regulatory Impact Statement about 1200 taxpayers are filing AIL returns paying AIL totalling $153 million for the year ended 30th June 2023. This represents annual interest of approximately $7.7 billion subject to the 2% AIL.

But some people haven’t registered the loan for AIL and the current rules are that they can’t register for AIL until they’ve paid the NRWT. The loan cannot be registered retrospectively. There’s an example in the Regulatory Impact Statement that one borrower had to pay $2 million in NRWT as a result. The proposal is to enable Inland Revenue to allow retrospective registrations.

Paying withholding tax on your mortgage interest

What has also emerged as an issue is that there are a number of individuals with overseas mortgages. They have moved here, but they’ve kept their overseas property and usually rented it. The UK and Australia are the two most common examples I’ve encountered. These persons are paying interest to the UK/Australian located banks on UK/Australian located properties because they have mortgages. These payments are also subject to AIL and NRWT but practically speaking it’s very hard to explain why AIL/NRWT is payable particularly when the payments are being made from an account situated in the UK/Australia.

This AIL proposal will deal with some of the problems around retrospective registration. But the question has not been asked as to whether in fact individuals in those circumstances that I’ve just described should in fact be within the scope of the regime, because that’s not why the AIL scheme was introduced.

It’s intended to help lower the cost of capital for New Zealand borrowers. As mentioned above in my view taxing foreign superannuation schemes seems to be taxing the importation of capital. This is contradictory to the purpose of the AIL regime. Both those positions can’t be correct in my view if we want to make it easier to access capital. In my view we should be changing the approach in relation to foreign superannuation schemes.

Rant aside, allowing retrospective AIL registration is actually a welcome move. The bigger question still remains as to whether in fact individuals with overseas mortgages should be within the regime. As the Regulatory Impact Statement notes, we don’t really know what’s the impact for individuals. It’s pretty near minuscule overall and there’s probably more non-compliance than the Regulatory Impact Statements acknowledge.

A hefty dose of remedials…

Another policy measure is to increase the exempt employee share scheme threshold. The maximum value of market shares that can be offered will be increased from $5,000 to $7,500 with effect from 1 April 2024. Finally, there are a large number of remedial measures relating to GST, trustee tax rate changes, partnerships, land tax rules, international tax and sundries. These often pop up in tax bills, just tidying up inconsistencies in legislation.

Submissions are now open and close on 18th October.

Insights from ten years of Inland Revenue’s transfer pricing questionnaires

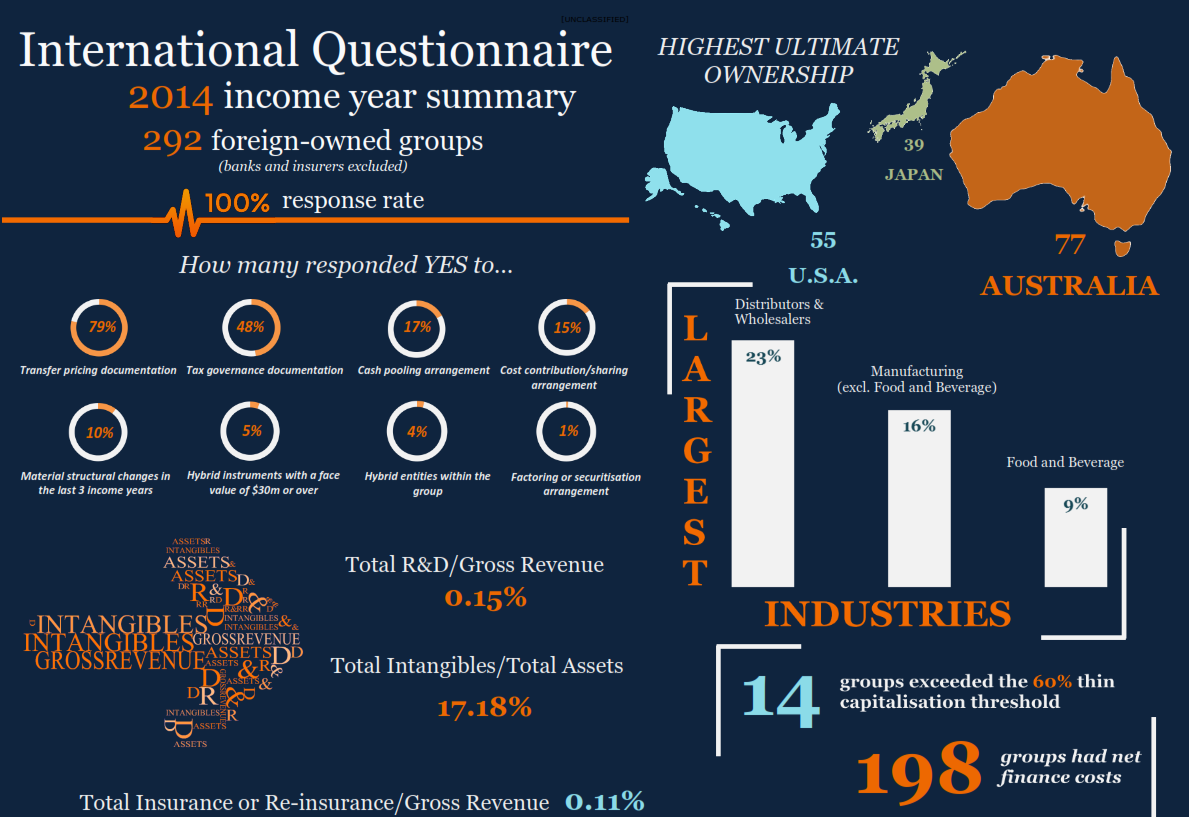

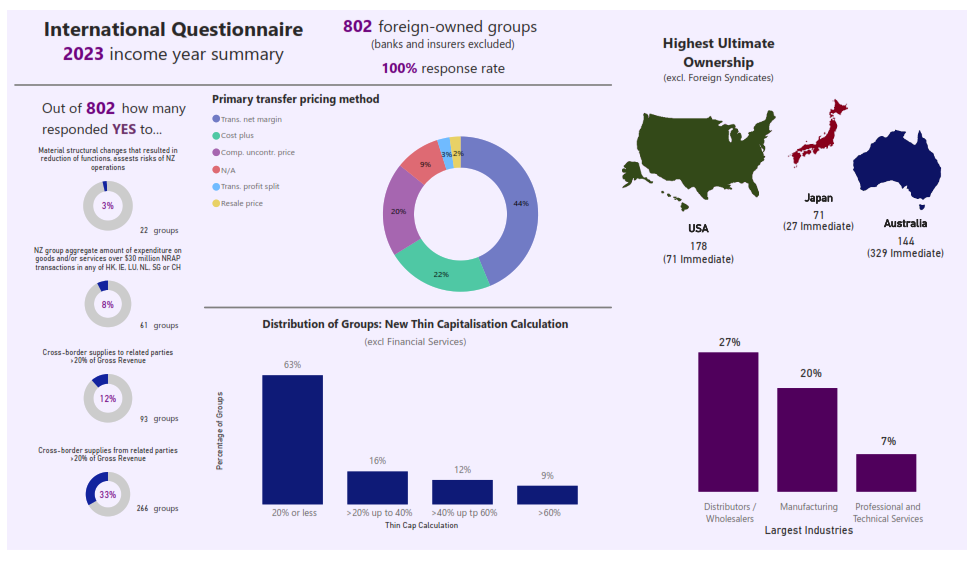

Every year Inland Revenue issues an international questionnaire designed to collect key information about financing debt and transfer pricing issues in regard to foreign owned businesses in New Zealand. The data request for 2023 was sent out in February 2024 and responses were required by 15th April 2024. These questionnaires generally target foreign owned groups with turnover exceeding NZ$30 million.

What’s happened is Inland Revenue’s now published a summary of the answers it received covering the10 years from 2014 to 2023 inclusive. There are some interesting little details in here. In both 2014 and 2023 years, the three countries with the highest ultimate ownership were Australia, Japan and the United States. In 2014 there were 292 foreign owned groups (excluding banks and insurers), 77 had ultimate ownership in Australia, 55 in the USA and 39 in Japan.

Flip forward to 2023 and there are now 802 groups. The top three were still the same, but the order has changed. In that now the United States with 178 groups is the country with the highest ultimate ownership Australia has 144 and Japan 71.

There’s also questions about how many groups are subject to our thin capitalisation rules which kick in where the debt to asset ratio exceeds 60%. In 2023, nine percent of the groups – that’s about 75 – would be subject to some form of interest restriction.

Back in 2014, that was much smaller. Only 14 of the 198 groups that had net finance costs were subject to thin capitalisation. That’s quite interesting because it shows that more debt has been taken on board by foreign owned groups over the ten year period.

I’m always interested to see data like this from Inland Revenue as it gives us insights into the shape of our economy.

“Who’s that knocking on the door?”

And finally, this week a reminder that Inland Revenue has upped the ante in terms of debt collection and just general enforcement across the board. I mentioned earlier on about the taxpayer who had received an inquiry in relation to their Binance account. This week RNZ ran a story about instances where Inland Revenue have actually been out door-knocking and making physical visits to people who owe them debt. It’s something we haven’t seen for about five years. Inland Revenue seemed to have dropped off using this practise prior to COVID and obviously COVID then had a huge operational impact.

Inland Revenue re-engaging in this process is to be honest welcome. You do get the sense that certain taxpayers just push the envelope and think they’ll get away with it. So, it probably was a big shock for them that Inland Revenue can actually turn up on their doorstep and say “Hey, we’d like to talk to you about your debt.” As I’ve said before we’re going to see more of this increased enforcement.

Coincidentally, but I haven’t time to cover it this week, Inland Revenue also released drafts for consultation, updating its operational statements in relation to the use of its (very) extensive search powers. That’s probably something maybe I’ll get a chance to cover later, but for now, that’s all for this week.

I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.