The New Zealand Tax Podcast year-end special.

- Proposed changes to FIF regime

- A look back at the highlights in tax in 2024

There have been several constant themes throughout this year. A surprising one has been the question of how we tax capital and whether we should have a capital gains tax. Throughout the year there have been a steady stream of stories on the topic. Meanwhile the Labour Party is currently reviewing its tax policy, and whether it’s going to go with a wealth tax or a capital gains tax.

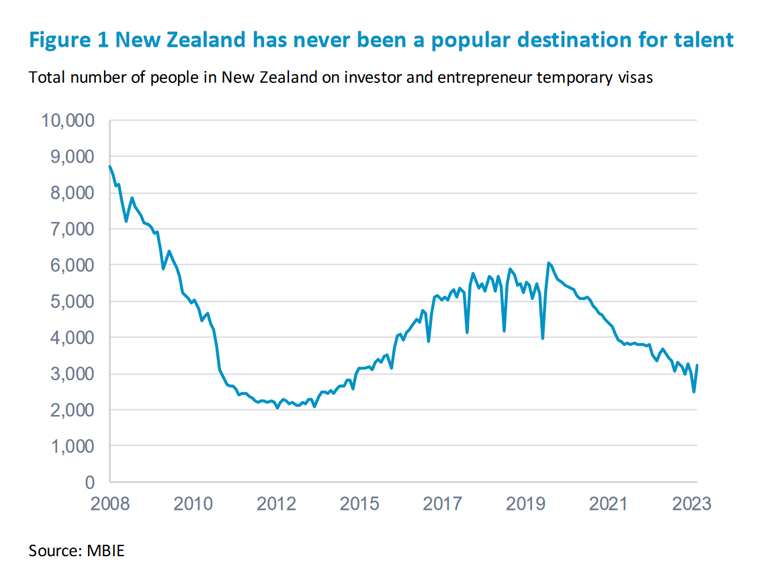

A place where talent does not want to live

Intriguingly, Inland Revenue has added to this mix right at the end of the year with the release of an issues paper on the effect of the Foreign Investment Fund (FIF) rules on immigration.

Earlier this year I discussed a New Zealand Institute of Economic Research report called The place where talent does not want to live, which looked at the impact of the FIF rules on migrants to New Zealand. The NZIER report concluded that the FIF rules were acting as a hindrance to investors, particularly those migrants coming here who have previously invested in offshore startup companies.

The report also discussed an issue I’ve encountered fairly regularly of the impact of the FIF rules for American citizens. Even though they may have been resident in New Zealand for many years, because they are American citizens they still have to file U.S. tax returns. As a result, a mismatch arises for them between the FIF rules, which basically act as a quasi-wealth tax, and the realisation basis of capital gains tax that applies in America.

Inland Revenue policy officials have been aware of this issue for some time. In fact, I spoke to several officials earlier this year about the issues and potential options. The topic was highlighted as an option for review and was included in the Government’s tax and social work policy programme released last month. This report has therefore come out quicker than I expected which is a pleasant surprise.

The problem with the FIF rules

The problem is set out very clearly in paragraph 1.5 of the issues paper.

“Migrants will generally have made their investments without awareness of the FIF rules and may not be organised so that they can fund the tax on deemed rather than actual income. This is particularly a problem for illiquid investments acquired pre migration…. Because the FIF tax is imposed in years before realisation and on deemed rather than actual income, FIF taxes paid may not be creditable against foreign taxes charged on the sale of the investment.“

This highlights a key point about the FIF rules – they’re highly unique by world standards. When I’m discussing them with overseas clients and advisers, to make them more understandable I tend to explain them from the viewpoint that they’re a quasi-wealth tax. As the quote above notes problems also emerge whether the tax paid under the FIF rules can be fully utilised in the United States, for example.

Fixing the problem – taxing the capital gains?

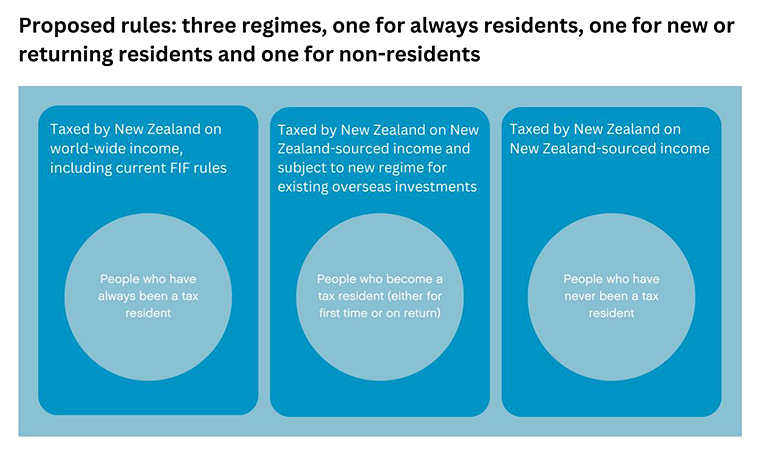

The paper canvasses several options for reform, including one of simply increasing the current $50,000 threshold above which the FIF rules automatically apply. A key proposal is that maybe the investments subject to the FIF rules should be taxed on what is called revenue account. That is only dividends received and any gain in the value of those investments attributed to New Zealand on disposal would be taxed. In other words, an investor would be taxed on dividends and then when the investment was disposed of, a capital gains would be become payable.

Now to buttress this option the paper proposes that there should be an exit tax. In other words, if someone elects to use the revenue account method, but then decides no, actually New Zealand isn’t working out for us for whatever reasons, and they become a non-tax resident, this migration would trigger an exit charge. I’ve seen this in other jurisdictions and current FIF rules do have a provision covering it. This approach should be pretty understandable to investors coming here.

Maybe a deferral basis?

Another alternative is a so-called deferral basis, is where the FIF rules would apply on a realisation basis. This would be achieved in a way similar to how withdrawals on foreign superannuation schemes are currently taxed when the tax charge arises on withdrawal or transfer into a New Zealand based Qualifying Recognised Overseas Pension Scheme.

The taxable amount would be based on a deemed 5% per annum income from the date of their migration, with an interest charge for deferral. Again, this would be buttressed by an exit tax.

What happens overseas?

Picking up on what I was saying at the start about the question of taxation of capital, most other jurisdictions don’t encounter this issue to the same extent as we do because they usually have a capital gains tax regime that applies to comprehensive capital gains. Actually, in paragraphs 2.3 and 2.4 I find there’s some intriguing commentary from Inland Revenue on this issue.

“Because New Zealand does not tax capital gains without the FIF rules, no New Zealand tax would ever be paid on an investment in a foreign company that paid no dividends and was sold for a capital gain.”

This is an interesting insight to the issues caused by non-taxation. In effect without the FIF rules the Government is forsaking potential revenue. I always thought the expansion of the FIF rules in 2006 was really a sidestep around the difficult issue of taxing capital. And of course, despite having kicked the capital gains tax can down the road back in 2006, it’s still there.

Tax driven behaviour, or just a rational investment choice?

The issues paper goes on, quite controversially in my view, to argue that without the FIF rules in New Zealand, residents have a tax driven incentive to invest in foreign companies that enjoy low effective tax rates and do not pay significant dividends. Speaking with 40 years of tax experience, yes taxes do drive investment behaviour.

But this argument sidesteps a huge criticism, which is still valid, of the current FIF rules. When they were introduced in 2006, many of the submissions against them argued that the New Zealand stock market is so small in global terms that investors would be unwise to be fully invested here, and therefore should be spreading their risk by diversification and investing in offshore markets.

That is as valid a criticism of the FIF rules now as it was back in 2006. And of course, memories of the 1987 stock market crash, which was actually quite catastrophic by world standards, still run deep in many areas. We now have this scenario here where the FIF rules were designed because the Government wanted some revenue. It saw tax driven behaviour happening offshore, but it ignored a key fact, the importance of diversification. And if you don’t tax the capital but you want the revenue, where do you go from there?

Backdating the introduction of the changes?

Anyway, the whole paper is a very worthwhile read. It has one further highly interesting suggestion that changes could be back dated to take effect from 1st April 2025 and the start of the next tax year. Such a swift law change doesn’t happen with issues papers. Normally there’s usually another year or so before legislation is introduced and then comes into effect.

This option is actually very encouraging for migrants. I have had a number of inquiries on this issue, and I know of clients who have backed away from New Zealand because of the FIF rules. So, they will be looking at the proposals with great interest.

The paper also canvasses whether it should apply to new migrants or to existing New Zealand tax residents. That’s a good question it should certainly apply to migrants who can reorganise their affairs in anticipation, but I believe it should also apply to U.S. citizens who still have to file U.S. tax returns and are very disadvantaged by the current FIF rules.

Worth noting that although this is largely a tax measure it’s important to the Government because the existing FIF rules are seen (as the NZIER report noted) as a hindrance to attracting high quality migrants. Changing the law is seen as a priority as part of the Government’s general economic programme,

Submissions are open now and continue until 27th of January. I urge everyone interested in this topic to submit. We will be submitting a paper on this ourselves. We will also be contacting clients on this matter as it’s quite a welcome Christmas present.

The year in review

Moving on, its been a very busy year in tax. And I guess the biggest story in many ways was the Budget on 30th May, with the promised increase in tax thresholds finally being enacted with effect from 31st July. That was certainly the most eagerly anticipated one, and according to my data reads, it was the most read transcript over the year.

The tax cuts which weren’t

These tax cuts as they were called (which they’re not because they’re only inflation adjustments) also highlighted a big and continuing problem with our tax system, which the politicians apparently don’t want to address. The threshold adjustments only factored in inflation from 2018. They therefore effectively locked in the inflationary effect of the non-adjustment between 1st October 2010 (the last time the thresholds were adjusted) and the 2018 baseline.

On the other hand, in order to help pay for these adjustments which will reduce government revenue, the threshold on Working for Families which has been at $42,700 since 1st July 2018, was not increased. This means that families with income above that threshold have their Working for Families credits abated at 27.5%. Consequently, they face some of the highest effective marginal tax rates in the country.

And as I have repeatedly said in past podcasts, our politicians are very much less than transparent about the impact of what’s called fiscal drag. That is, as wages increase with inflation, they pull taxpayers up into higher tax brackets. We have a particularly big problem around the now $53,500 threshold where the tax rate jumps from 17.5% to 30%, the biggest single jump in the whole tax scale.

To bang a drum already beat repeatedly, this hinders a discussion around what is happening with our tax system? How much revenue have we really raised because politicians have been happy to use fiscal drag to quietly increase the tax take.

But the main effect is that the burden of tax falls on low to middle income earners who face significantly higher marginal tax rates because of the effect of abatements on people receiving social support, such as Working for Families.

So overall, those tax threshold adjustments were welcome. They were overdue, but they were one step forward and two steps sideways and half a step back because there’s no comprehensive commitment to ensuring that we have regular threshold adjustments.

If America can do it, why not here?

Just as an aside, in America all thresholds are automatically index-linked. Countries vary on their treatment of inflation and thresholds. And in low inflation periods, you can get away with not needing to do it every year, but you can’t leave such adjustments for 14 years without finally having to do something.

A year of anniversaries

2024 was quite a big year for me personally. I started working in tax 40 years ago in Britain and it so happened that the British budget on 30th October had several announcements which have huge significance not just for UK migrants who have moved here but also for many Kiwis. So, I find myself, somewhat ironically, still doing a lot of work on the impact of British taxation.

It’s also been 20 years since I started Baucher Consulting and as I said in the podcast much has changed, and yet in some ways little has changed. One constant which hasn’t really changed is the behavioural impact of tax- this week’s discussion of the FIF regime is the latest example. I’d like to thank everyone who’s supported me over the these past 20 years.

Our fantastic guests

Looking at some other highlights of the year in terms of the podcast, we had a lot of great guests this year and my thanks again to all of them. My particular favourite episode was the Titans of Tax with Sir Rob McLeod, Robin Oliver and Geof Nightingale. Many thanks to Sir Rob, Robin and Geof for giving up their time. It was a fantastic discussion and very, very enjoyable. It was extremely well received all around. It was fascinating to just sit back and listen and to three experts who’ve been very heavily involved in the last three major tax working groups.

My thanks also to all my other guests this year, including the four finalists for this year’s Tax Policy Charitable Trusts Scholarship. Again, thank you so much for your input. Very interesting to talk to you, and the future of tax policy is in good hands.

Inland Revenue goes full throttle on compliance work

One of the big themes for the year, and less of a surprise, was Inland Revenue’s ramping up its enforcement approach. One of our guests very early in the year (and thanks again) was Tracy Lloyd, service leader of Compliance Strategy and Innovation at Inland Revenue. Tracy’s podcast was a really interesting one looking at what tools Inland Revenue is using and how it’s ramping up its investigative activities.

We’ve seen Inland Revenue’s more aggressive approach constantly through throughout the year. It has made announcements about cracking down on the construction sector, looking at liquor stores. Pretty much every week there’s a media release that another tax fraudster has been jailed or received substantial fines or home detention. In addition Inland Revenue is making use of information received through the Common Reporting Standards on the Automatic Exchange of Information.

These things will continue to come through. Inland Revenue got $116 million over four years to beef up its investigation activities and to improve its tax collection. As part of this we’re seeing a crackdown on student loan debt, which is a much more problematical issue mainly because the biggest portion of debt is held by persons overseas. It’s therefore not so easy to collect.

Inland Revenue’s activities will continue to ramp up but I think it may start to find there’s increasing push back as it clamps down. I think it’s previously been slow in responding, and during the COVID pandemic that was understandable. But right now, the faster it responds to debt issues developing, the better for all of us. Zombie businesses which linger on are no good to anyone.

The surprising continuing debate over capital gains

But the other big thing this year has been a surprising one. It’s the question of the shape of the tax system and persistent media stories about whether we should have a wealth tax or capital gains tax. This is a topic I don’t see going away. I see the pressure mounting on it because as, the Government’s main agency, Treasury, is pointing out we have ongoing demographic pressures in relation to superannuation and funding health.

And as I keep pointing out, we also have the question of climate change. We have insurers withdrawing cover and I think that means the Government will be expected to step in. And that means sharing the burden, which means ultimately some form of tax increases. All this means the composition of the tax base will continue to be a matter of debate.

Of course, we have options like capital gains tax, wealth taxes, or as Dr. Andrew Coleman suggested (another one of the fascinating podcasts this year) maybe we should rethink our issue of Social Security taxes, where again we’re a unique jurisdiction in that we don’t have them. We used to have such taxes way back from the early 1930s through until late 60s, before they were finally abolished,

So overall lots to discuss this year. I’d like to thank all my guests again, and all the listeners, readers and all those who chip in and comment away. Your comments are read and always welcome. And on that note, everyone have a very happy festive season. We’ll be back with what’s new in the tax world in January 2025.