Plus big changes to the retirement landscape she helped initiate.

She also explains why she was one of the first of the 97 signatories on the Open Letter on Tax.

During her time as Retirement Commissioner, she also helped develop a national strategy for financial literacy that incorporated practical strategies such as the excellent sorted.org website, multimedia campaigns and education in schools.

More recently, Diana was the chief executive of the Wellington Free Ambulance and is presently chair of the Lifetime Retirement Income and several charities. She is also one of the initial 97 signatories of last month’s Open Letter on Tax.

Ki Ora Diana, welcome to the podcast. Thank you for joining us.

Diana Crossan Ki Ora Terry, thank you for having me.

TB Oh, not at all. Enormous privilege and thank you. I’m really fascinated. You’ve got an incredibly distinguished career there. But I’m most fascinated by your time as Retirement Commissioner. Because when I was researching/writing Tax and Fairness and looking at the superannuation savings regime, as it was in 2002, prior to when you took over, it was pretty much ground zero. There was practically little or no incentives to save.

And we know that the numbers of superannuation schemes had basically collapsed from where the numbers that prior to the removal of insane tax incentives in 1988, they had fallen quite dramatically, to I think barely 13% of the workforce was covered about 2002.

So, you come onto the scene, you’re appointed Retirement Commissioner. It must have been quite daunting. What were your thoughts when you volunteered for that?

Diana Crossan You’re right, it was a bit overwhelming initially. And I was the second Retirement Commissioner, the first one was Colin Blair, who was a tax specialist. So, when the government set up the retirement commission, they thought that they were helping the nation. Hopefully they were because we had a superannuation, or a retirement savings system that was very different from the rest of the world, or the OECD world really.

We had New Zealand super, which is of course brilliant, and should be protected and we had private saving. The Retirement Commissioner was supposed to be there to help people understand that they needed to save for their own retirement. That was why it was set up.

And what we discovered – the Retirement Commission was just on to this when I arrived – was that the advertisements and the encouragement and all of the messages they were sending out to people were getting to people who were already looking for it. It was preaching to the converted, really.

And the average age of people they were talking to at that point was about 45 to 50, and the Retirement Commission recognised that that wasn’t going to work. That starting to save at that late stage in your career didn’t work. So that’s how it came about. The recognition that maybe in the 2000s at the beginning of this century, we had to do something very different.

So, they stopped all paper brochures and television interviews and things that focussed on brochures. And the team introduced Sorted https://sorted.org.nz/ and I came in just at that time. And so the focus on financial literacy and on getting to people earlier was the most important thing I picked up when I first arrived.

TB And that’s been a huge transformation there, I take.

Diana Crossan Yes, absolutely. We started off by thinking, how do we do this? You know, this is new. I thought it was very brave of the group just before I arrived. You talked about the national strategy for Financial Literacy.

We were one of the first countries to do that because we recognised that if the government was (and we kept talking to government about other things as well) going to stick with this policy of having a New Zealand super, which was very basic as we know, somewhere between 30 and 40% of New Zealand population live on New Zealand super alone. So first of all, it was that and then it was up to you to say we needed to find ways of talking to people about what to save, how to save, how safe is it. All of the issues in our trustworthy financial services sector, we needed to talk about that. We need to talk about government policy that didn’t get in the way.

So until KiwiSaver came along, we were different from the rest of the world. The countries that we tend to look up to like Australia, Canada, US – well, the US is unusual – the UK and parts of Europe because we didn’t have the middle pillar which is about supported saving by government.

TB Yes, some countries do that by means of very generous tax incentives which were abolished under Roger Douglas in late 1988. So, you were closely involved in the development of KiwiSaver?

Diana Crossan Yes, Michael Cullen approached me to join the team. So, it was an interesting group of people from a variety of government organisations and his statement was “We are going to have a savings scheme. I don’t want this group to come back and say it’s not a good idea because we’re going to have it while I’m in government. What I do want you to do is tell me how to develop that.”

And just before I came into the Retirement Commission role, I had been funded by a businessman and business family in Auckland who asked me to look at how we could help New Zealanders go to university and polytechnic, tertiary education. There were high fees and high interest rates for university students at that time.

So, we had done four years of work about a children’s savings scheme. Therefore, when I was asked to join the KiwiSaver group by Michael Cullen, I was able to take all that work to that. So that included the kick start and included thinking about other ways of doing things.

TB Yes, it’s been enormously successful. Even the FMA Financial Market Authority’s June 2022 report now says that we have $90 billion in KiwiSaver as of 30th June 2022 and over 3.17 million members. And that’s not even 20 years. It’s 15 years max. It’s been transformative.

Diana Crossan It is, however, there are issues with that. As you know, there are a lot of people who don’t know where their money goes or know what kind of fund they’re in. And they might be young and in a fund that’s quite conservative and they could do better to be in the balanced or growth funds, and they don’t understand that.

So that’s what the financial literacy was about. Also, many of them have very low savings in KiwiSaver. And while it will be helpful when they get to retirement, we want people to put more in now so that they have a better retirement when they retire.

TB How do we achieve that? The Tax Working Group in 2018 made a number of recommendations around that. It was suggesting that perhaps we should increase for example, a KiwiSaver member on parental leave would receive a maximum member tax credit even if they didn’t make the full $1042 contributions. And we saw something in the last month’s Budget for that alongside that. But that’s not enough, is it really?

Diana Crossan No. And one of the recommendations I would have made, which was too bold, I think, is that if we want women to have children, and I think we do, and if we want women to have equal opportunity through their career and their retirement, that we do, then maybe we should be thinking about how we help women to keep their KiwiSaver going. We do it with ACC. We keep it going at 80%, so what about keeping KiwiSaver going?

You know, there’s lots of ways of thinking about it, but I think we have to be quite bold in that area because not only are women having time out to have children, but they’re also earning less on average. And so we need to find ways to reduce both of those things. And one would be while you’re on parental leave, your KiwiSaver is put in by the government to even things out. And the other one would be let’s keep pushing for equal pay.

TB Absolutely.

Diana Crossan It makes a difference in retirement.

TB Well, yes, because the thing about retirement is a dollar saved 20 years ago is worth exponentially much more than one saved with ten years to go to retirement. It’s that sort of thing. It’s just volume of savings steadily each year, year in, year out.

Diana Crossan So we’re not good at this, though, because we had a government – I think it closed in 1991 I think – a government savings scheme, a superannuation scheme for its staff. And what was interesting was of course women had unequal pay until the 1960s and some of those women who had unequal pay, when equal pay came in, there was no adjustment in the super.

So they lived out their lives on those savings that were made in relation to the pay at the time. And there was an attempt to tell government that this was completely unfair. Other countries, when they made equal pay rules and legislation, changed the super at the same time so that the women who’d retired by that stage got a better income.

TB Yes, that is still a perennial problem, and it shouldn’t be. As you say, equal pay is closing that gap, which is, what, 13% now?

Diana Crossan Yes, about that.

TB Give or take. Still, closing that gap is vitally important. And we all hear plenty of stories about the shortage of workers and experience. So I think, “Well, guys, we need to address those issues and retirement issues.” And looking at the Tax Working Group, what I liked about what it said in relation to proposal tax incentives, was they were focussed on the lower end.

Because to pick up your point earlier on when you became Retirement Commissioner, the people who should be saving knew they should be saving, were saving anyway. It was getting to those people who weren’t as aware as they needed to be about what they could do.

And so helping that group was what I liked about the Tax Working Group’s suggestions. For example, removing the employer superannuation tax charge on employer contributions below the $48,000 threshold at the moment. What do you think about the tax treatment of KiwiSaver and savings?

Diana Crossan I’m not a tax expert as I said earlier I think. It’s not something I have spent a lot of time on. I think my reason for signing up to the letter was much more about getting more tax, rather than tinkering with what we’ve got at the moment.

You might think, paying women when they’re on parental leave is tinkering. But it’s dear to my heart.

TB I don’t think it’s tinkering. I think it’s something we should be doing.

Diana Crossan In terms of why I signed up and why I’m interested in this issue, is I just don’t think we’ve got enough money. And I know it’s as basic as that. We have one of the lowest tax rates, as you know, in the OECD. Why do we do that? Why don’t we tax? We want the same schools, the same health services. We want housing for everybody. We want the same services as they have in France or as they have in Germany or Canada or Australia. But we all pay less tax. That’s just madness to me.

TB As I heard someone put it “We want Scandinavian levels of [‘free’] service, but American levels of tax” and the two are incompatible.

Diana Crossan There is strong evidence that investing in health and education outcomes leads to productivity and economic well-being. There’s strong evidence that if you focus on health and education in a nation that there will be an increase in productivity and an increase in economic well-being. Why don’t we do it?

TB Well, yes, because the way I do see it as an economic issue. Because if we have poor outcomes for lower income groups and Pasifika and Māori etc., that’s an economic anchor on the rest of us. We pay more for our health care.

And I know from my time when I was coaching rugby in South Auckland, players didn’t get the ACC treatment that we wanted them to get to have the injuries looked after because they couldn’t afford the little surcharge. That was only $5/$10. Some people, I think $5/ $10, that’s nothing. When you’re on minimum income, it’s a lot. And so you could see players, you could see from their injuries, that had never been properly treated, that there’s a shortage of funds there. And so longer-term health issues develop from that.

Diana Crossan And you’ll be aware that we’ve had underspend for a long time, so it is catch up time and that’s why I signed this letter. Yes, let’s get out there and say for those who can afford it, and we’re not talking about the stinking rich, we’re talking about people who could pay a little bit more. I mean, if we went to Australia, we’d be paying 45% and we’re paying 39% at the top and mostly 33%.

TB Yes, our tax rates are not high by world standards. To me, the big issue that we have in our tax system when we talk about income tax rates, is that low to middle income earners pay a lot more, the $48,000 threshold which it goes from 17% to 30% has not been lifted since 2010.

And how that’s been allowed to develop – politicians then come along and like snake oil salesman said, ‘Oh, we’re giving you a tax cut’. And I’m thinking, ‘No, you’re just simply restoring a position that shouldn’t have existed in the first place.’

So, there’s enormous pressure there, and then we’re on to the question of wealth. Last week, when I talked about how the Greens tax proposal for a wealth tax caused a lot of conniptions amongst people. So politically I think it’s going to be a hard push. But we have this aversion, it seems, to taxing capital, which I’m not sure where that’s developed. Is that something you’ve seen over time? Has it come up in discussions about broadening the tax base?

Diana Crossan What I’ve seen, Terry, I think there’s two things. One is people get nervous. It’s almost NIMBY, isn’t it? Let’s find a way of doing it in somebody else’s backyard but don’t let me pay more, let others do it somehow.

And I think there’s a lot of ignorance about what capital gains or wealth tax might be and that people are concerned they’re going to pay millions somehow. Yet not paying capital gains seems blatantly unfair. I would say if we could have a poll, I think we’d find more people would be for capital gains tax than those who are against it. And they were hoping that this government, when it had its huge mandate, would have done that. Maybe the ones against it are more vocal. But I think overall the people I meet, the ordinary people, understand that it’s fairer.

TB There’s an awful lot of misinformation that goes on around this now and watching the debate at the time. It was certainly the squeaky wheel squeaking a lot back in 2018/2019, happened to be those that would have been most affected by it.

Naturally someone who sits on substantial unrealised capital gains and property or whatever, of course they’re going to say, ‘Well, this is going to hurt, so I don’t want it’. And I don’t have a problem with people saying that. I know we need to look at the bigger picture.

Diana Crossan If you have enough money to get into the property market and you manage it well, you can make quite a lot of money.

TB On leveraging the gains, when you look at how generous our tax system was until this current Labour government came in, it was extraordinary generous. You could offset your losses against your other income, you’re able to leverage it. And one of the key parts of the return, the capital gain was untaxed, until the changes around Brightline tested all yanked that scenario.

So now we have a de facto capital gains tax applicable to one asset class, a residential property. You know, for me I have great fun explaining to people who want to migrate here from overseas. “Yes, we’ve got about five different tax treatments because we don’t have a general capital gains tax.” Now that keeps me in work, but I can hear the brains whirring away trying to understand the intricacies of the various regimes in place, thinking what is the problem here? Broadening the base means we can lower the tax rates. We may not need a 45% tax rate if we broaden the base.

Diana Crossan I’m not suggesting a 45%. Even if we went to 40%. My understanding is that the tax take brings in $113 billion. And if we had another $20 to 30 billion, we would be able to do the things we need to do in housing and health. And I can also hear people who might be listening saying “We can be more efficient, we waste money”. Well, my understanding is that yes, we can be more efficient, but we can’t make $20 to 30 billion out of efficiencies.

TB Yes, that’s the key issue. What was surprising, the Greens were proposing $10 to $12 billion of tax increase, a 10% tax increase to tackle it. That is a substantial tax increase. But it gives you an idea of the scale of the problem. But no one’s really talking about that. They were focussed on this wealth tax, which was probably the most ambitious part of the proposal and the least likely to actually come into force. Because that would require a lot of political balls to drop in the right place for that to happen.

Diana Crossan I think one of the things about the TOP party and the Green Party is their tax proposals didn’t increase the tax take a lot because they also were dealing with supporting the low income. That was more about making it fairer. I’m all for making it fairer too. But I think, we need more money. I know we need more money.

TB I keep harking on about the climate change costs. 700 properties were rendered unliveable by Cyclone Gabriel. That is probably the thick end of a billion dollars. And that’s just this year. 400 are in Auckland. Another 300 are along the Hastings, Napier, Tairawhiti-Gisborne and Wairoa districts, none of whom by the way have the funds. You can see from their rating base. So, it’s a communal responsibility.

Climate change doesn’t distinguish between postcodes. It’s coming and we’re dealing with it right now. And I think the crunch point will be the insurers. They’re already starting to say, “Well, we’re not going to insure you if you build there. We’re not going to give you that.”

Last week I got a call from someone who was down in Christchurch and they’re still arguing with the insurers over the earthquakes. We don’t want that scenario repeated across the whole of the country in relation to climate change.

Diana Crossan We certainly don’t. And while I’ve focussed on housing, education, child poverty and health – the whole issue of being prepared for what’s coming – we’ve had a taste of it and it’s not going to go away quickly.

We need to work hard for ourselves, but we can’t stop it all, so we’re going to have, I think we all agree, having weather we’ve never had before, and we’re going to have more weather we’ve never had before. And so we need more money. I just keep saying we need more money.

TB And a little a lot goes a long way.

Diana Crossan And people have asked why the signatories of the letter don’t just put their hands in their pockets and pay up and give more to education and health and poverty.

And what I know, of course, is that quite a few people I knew who signed the letter are already doing that. But some of them, of course, rightly said, “I’d be much happier if everybody was doing it and it was fairer across the board so that it wasn’t just philanthropists. We weren’t just relying on charity.”

TB Yes, that was my philosophy as well. And we are actually a generous nation in that. And what’s notable is often it is relatively low-income people are very generous, as a proportion of income given to charities.

Diana Crossan When I was working at Wellington Free Ambulance, it was collecting in the street. It was always very interesting who gave money, and it was people who you would think wouldn’t be able to afford to. But people are generous and that’s good. But I think it’s so much better for housing, health, even ambulance, I believe, should be part of our government funded services. And that’s what we want. And we just need to pay more even if I sound like a broken record, Terry.

TB Well, Dame Diana Crossan, that seems to be a very good place to leave it, broken record or not. I think it’s something we need to be hearing.

Thank you so much for being part of this podcast. It has been fascinating to talk to you and hearing the story of your back involvement with the Retirement Commission and the changing landscape, which has changed considerably for the better. Thanks for your efforts. It’s been a pleasure having you on the podcast. Thank you so much.

Diana Crossan Sure. Thank you for having me.

TB That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Greens announced their tax proposals a week ago, last Sunday.

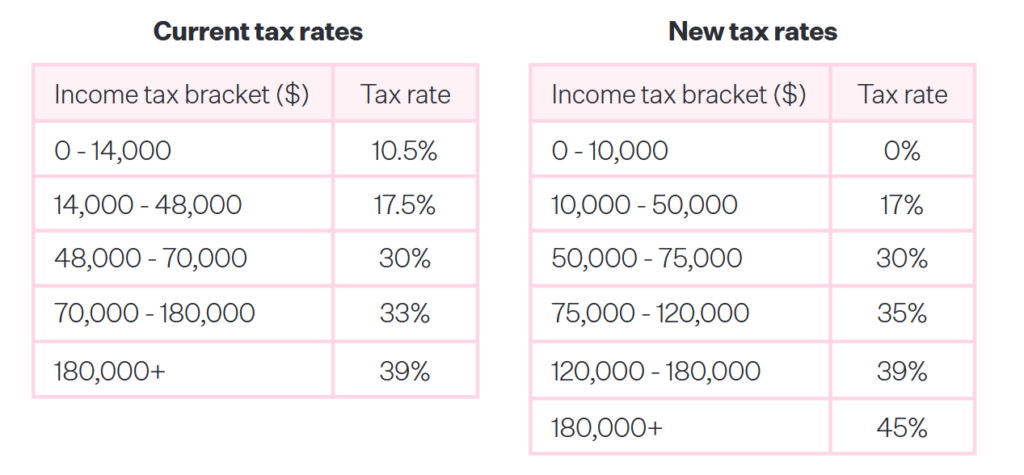

And my reaction was, “These are very bold.” They proposed major tax cuts at the lower end, meaning 95% of taxpayers will be better off under the Greens. Those cuts are paid for by increasing the top tax rate to 45% and increasing the 33% tax rate to 35% as well. These increases are part of the trade-off for the proposed nil rate band of $10,000, which no doubt will be very popular. As is well known, many other jurisdictions have something similar and given the fact that nothing has been done in relation to indexation of thresholds for well-nigh 13years now, it’s unsurprising that the pressure is built up, particularly at the lower end, to change the tax rates.

But most of that got swept away by the Greens controversial wealth tax proposal. In summary, there are two parts to it. Any individual whose net assets, net of mortgages for example, exceed $2 million will be subject to a wealth tax of 2.5% on the excess. For family trusts there is no nil rate band or threshold at all. It’s a flat 1.5% which is a deliberate anti-avoidance mechanism.

Latest Inland Revenue data on trusts

Trusts were used to avoid the impact of estate and gift duties in the past and are used in other jurisdictions to mitigate the impact of wealth and estate duties. So, the Greens have targeted this avoidance. Coincidentally, last Saturday the New Zealand Herald published a piece including details of the trust tax return filings made to Inland Revenue for the year end 31st March 2022 which indicated the value of assets held in trusts. The net assets of the 201,100 trusts which reported, was just over $300 billion. So at 1.5%, theoretically that’s $4.5 billion dollars straight up there.

Incidentally, what that Inland Revenue report doesn’t show is the non-reporting trusts, those are likely to be quite significant. We really don’t know how many trusts there are in New Zealand, the best estimates are somewhere between 500,000 and 600,000. Many of the non-reporting trusts don’t do so because they have no income, but they hold assets such as the family home. So, family homes that have been held in trusts may now be subject to the Greens’ proposal.

Now this kicked off quite a storm, which I watched with a little bemusement because the Greens first of all have to put themselves in a position of such leverage that its coalition partners, almost certainly Labour and Te Pati Māori, agree to the proposal. And then somehow between 14th October, the date of the election, and 1st April next year, the legislation to introduce all of this is drafted and passed through Parliament. So ,it’s a big challenge ahead.

But it caused quite a stir, and I fielded several calls from people concerned about what they saw here, trying to get an understanding about it and my views on it. At our Accountants and Tax Agents Institute New Zealand’s regional meeting on Tuesday we had a very lively debate around the question of this wealth tax. Normally, a lot of the time we’re talking about what’s in the legislation and whether Inland Revenue ever answer their phones again. All this I think shows the impact of the proposals, even though in theory they affect only a small group of people, the top 1%.

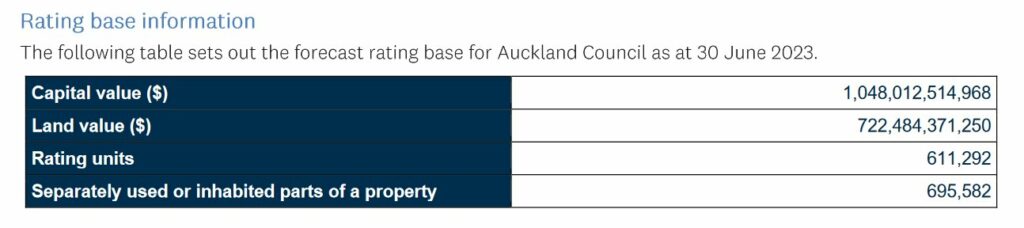

But there is substantial wealth locked up in property. We know that from digging around the official figures. For example, Auckland Council estimates the rateable value for all property within the Auckland Council region will be over one trillion dollars as of 30th June. Obviously, not all of those would be subject to a wealth tax.

What’s being suggested by other parties?

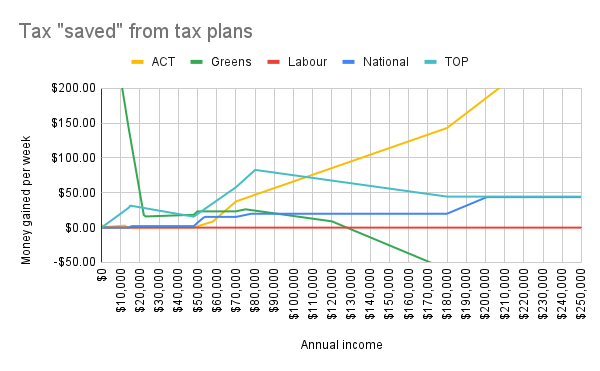

But I thought it was interesting that people are taking the Green’s proposals very seriously. The income tax shift to 45% on income over $180,000 won’t be terribly popular. But at present, the proposals that they’ve put out for the income tax cuts would affect many more people and benefit many more people, all those earning under $125,000, which is something like just over 4 million people. This has a broader impact than either National or Act’s proposals.

It’s quite interesting now as the election comes ever closer, we can start to see the tax policies of the various parties taking shape. The Greens are raising a substantial amount of tax to deal with poverty. Act is proposing tax cuts and it’s taking the ideologically opposite approach of substantial cuts to spending in order to achieve its top rate of 28%.

TOP, The Opportunities Party, are putting out a policy which has a land value tax, and they also propose tax increases at the higher end together a nil rate band and also substantial tax cuts at the lower end.

We haven’t yet heard from Labour on what they would do. Over on Twitter @binkenstein put together a graph comparing the various parties’ proposals so far.

So, the debate has ramped up quite a bit. Obviously, the Greens wealth tax is the most controversial part of it, but the other part which really got very little commentary but is equally controversial, was a proposal to raise the income tax rate for companies from 28% to 33%. More than most of the Greens’ proposals, that would probably produce a certain frisson of tension amongst multinationals. They may look and think “Maybe we might not increase our activities in New Zealand” or they may ramp up what they try and do under profit shifting.

Anyway, it all made for a very lively discussion all round. As I told people, wait and see. But it is interesting to see the pressure point for those are likely to be affected around a wealth tax.

What does the IMF think?

With almost impeccable timing, the IMF, the International Monetary Fund, were in town and it suggested that maybe it was time for a capital gains tax.

The Concluding Statement of the 2023 Article IV Mission noted:

Well-designed tax reform could allow for lower corporate and personal income tax rates by broadening the tax base to other more progressive sources, such as comprehensive capital gains and land taxes, while also addressing fiscal drag and improving efficiency.

It’s not the first time the IMF has suggested changing the tax system. They did so in 2021. In fact, there’s a regular pattern of the IMF and/or the OECD coming here looking around saying, “Well, guys, the country is in good shape, generally government policy is pretty sound, but you need to do something about capital gains taxes.” Regardless of whichever party is in power the Government’s reaction is quite funny. They like the bit about everything being under control. But at the mention of capital gains tax, they all throw up their hands in horror. And yet, as we know all around the world, capital gains taxes are a common feature of tax policy.

The Crypto-Asset Reporting Framework, the latest expansion of the Common Reporting Standards

Now, the Greens wealth tax proposal will probably be music to the ears of the French economist Thomas Piketty, who has proposed a global wealth tax, as one of the core points of his monumental work, Capital in the 21st Century. And at the time of publication in 2014, the opportunities for that global wealth tax to ever eventuate were probably just about zero or maybe marginally above zero.

But since then, we’ve had the introduction of the Common Reporting Standards which I think is actually revolutionising the tax world quietly because an enormous amount of information sharing is now happening on. We know from what’s been reported under the Automatic Exchange of Information that there’s something like €11 trillion held in offshore bank accounts. The Americans have got their FATCA, the Foreign Account Tax Compliance Act, and as a result of that, they know that American citizens have got maybe US$4 trillion held offshore.

Now, the latest part of the Common Reporting Standards is extending the framework to crypto-assets and I talked about this last year when the proposals first came out. Those proposals have now been finalised and the Crypto-Asset Reporting Framework is now in place. There have also been some amendments to the Common Reporting Standards. I’m going to cover all these changes in a separate podcast because I think they’re worth looking at in a bit more detail.

The tightening noose of information exchange

But the key trend in international taxation that’s going on, which I think is going to have a long-term impact around the world, and particularly for tax havens, is this growing interconnectedness, the sharing of information that goes on between tax authorities through mechanisms such as the Common Reporting Standards. I asked Inland Revenue about what information they had been supplied under the CRS in relation to the numbers of taxpayers and the amounts held in overseas bank accounts. Inland Revenue turned down my Official Information Act request on the basis that much of this is obviously confidential, but also would be compromising to the principles under which the information is shared.

Now, I’m not entirely sure about that. I think the more openness we have about what is being shared, the better the likelihood of tax enforcement once people cotton on to what’s happening. They will not think “Yeah, well, I’m just going to leave it over in the UK or the US or wherever, and Inland Revenue will never find out.” My view, as I tell my clients, is they always find out and they know much, much more than you can imagine.

And outside of the CRS there appears to be a regular exchange of information about property purchases between the United States Internal Revenue Service and Inland Revenue here. So be advised, the Crypto-Asset Reporting Framework is just the latest in a building block of international information exchange.

The Auckland Budget – what about climate change?

And finally, the Auckland budget got signed off last week. I’ve been in the press disagreeing with the sale of any part of the Auckland airport shares, and I still stand by that. I think it’s a short-term fix for a long-term problem, but that’s now done and we move on.

What I did think was quite surprising as you delve into the budget is some of the numbers that come out. As I mentioned earlier, the rating base for Auckland and according to the Auckland Council’s documents is over $1 trillion.

But the thing that really surprises me, which wasn’t addressed in the budget so we’re going to have to address it next year, is the question of climate change. Towards the end of the process, the Government announced that in the wake of Cyclone Gabrielle 700 homes around the country are too risky to rebuild. The Government and councils will offer a buyout option to those property owners.

400 of those are in the Auckland region and apparently it doesn’t also take into account what is going to have to happen out at Muriwai because of the slips and the dangerous cliffs over there. As Deputy Mayor Desley Simpson pointed out, “If you say it’s 400 [Auckland homes] times $1.2 million, give-or-take just like the average house price, you’re talking half a billion dollars.”

The question arises how is that split between Auckland ratepayers and the rest of the country? Yet there was nothing in the Auckland budget about this, and that’s just this year’s damage. What happens if we get another Cyclone Gabrielle, next year?

We’ve got an interesting scenario developing where we’re talking about reducing emissions and we’ve got a distant horizon 2030 or whatever farmers and other parties want to extend it to. But in the meantime, we are picking up the bill now for increased damage and we don’t seem to be thinking in terms of how does that affect our taxes and rates? And this is going to be an ongoing issue. So, the question of paying for that, whether it’s a wealth tax, capital gains tax, whatever, is going to become ever more present, in my view.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Australian Tax Office ruling on residency – time for a clearer statutory definition?

Applying for Australian citizenship? Watch out for the sting in the tail.

Submissions closed Friday on the Tax Principles Reporting Bill. Now for a bill that doesn’t actually increase the tax rates this has been a surprisingly controversial bill, mainly because it’s actually perceived as being highly political in its ambit in introducing reporting on tax principles. The speed with which with which it has been rushed through is also controversial because normally tax legislation is developed through what we call the generic tax policy process (GTPP). The GTPP is very well regarded around the world.

But every so often, for whatever reason, the process is bypassed. Sometimes as during the COVID emergency because things need to be done immediately. It’s a framework through which New Zealand tax policy has operated for the better part of nearly 30 years. And it means changes of tax policy and of the particular tax treatment of certain items are developed over time through consultation.

Controversy around the Tax Principles Reporting Bill

In this case, the Tax Principles Reporting Bill came out of left field. There’s been very little consultation about it. In fact, we’ve only had barely three weeks between its introduction alongside the Budget and today. So that’s part of the controversy around it.

The other question is what it really is setting out to do. I think most objections will centre around this question of why is this here? The idea of setting out some ideas about what tax principles might be is not unreasonable in itself. But criticism of the Bill is focusing on whether it’s very clear about what it’s trying to do. For example, Inland Revenue is required to report on certain effective principles and whether there are inconsistencies in the tax system with these principles. But then, as several tax advisors have asked, what action will be taken at that point. There is also no acknowledgement that tax policy ultimately involves trade-offs between principles and politics. To be frank, tax is politics.

I’ve seen one or two interesting comments about which agency should be reporting under the Bill. Inland Revenue or maybe Treasury? There are a whole heap of things to consider about the Bill. Although it comes into effect on 1st July, if there is a change of government, it will almost certainly be repealed.

It’s an interesting Bill because it’s attempting to clarify the basis on which we design and operate a tax system. But it’s also flawed because I don’t think it’s has actually achieved that. We’ll see plenty of pushback and I’ll be interested to read the submissions on the bill. (Shortly after the podcast was recorded, John Cantin published his submission).

Australian tax residency

Moving on, I frequently deal with issues of tax residency. It’s a core part of what I do because tax residency determines what sources of income will be taxed in Aoteaora-New Zealand. There are also rules set out in double tax agreements, and one pretty basic principle wherever you go in the world is that if you have property situated in the country, that country gets what we call the primary taxing rights to it.

But individual tax residency is a matter of great practical importance. If a person is resident in the country, then that country can tax them on their world-wide income, and that can have quite significant implications.

The Australian Tax Office (ATO) has just updated and released a tax ruling TR 2023/1, on income tax residency tests for individuals. Australia deems a person to be tax resident in Australia if they reside in Australia under what they call the ‘ordinary concepts’ test, and that includes a person whose domicile in Australia, unless they’re satisfied that they have a permanent place of abode outside Australia.

A person is also resident if they have actually been in Australia continuously or intermittently during more than half of the year of income, unless they’re satisfied that they have a usual place of abode outside Australia and they do not intend to take up residency in Australia. There’s also another series of tests, which I’ve not come across, relating whether or not they’re a member of a superannuation scheme or are covered under the Commonwealth Fund.

When you look at these tests you can see there are quite a few value judgements involved. And so there have been calls for the Australian tax residency test to be put on a more statutorily defined basis, most notably by the Australian Board of Taxation. “The Board’s core finding is that the current individual tax residency rules are no longer appropriate and require modernisation and simplification.”

Now it’s of interest here obviously for people going across to Australia, but also because our own residency test is twofold. The primary test, and this is often forgotten, is a person is tax resident in New Zealand if they have a permanent place of abode in New Zealand. You’ll note that phrase, “permanent place of abode” is actually also used in Australia.

Failing that, there’s the days present test where a person is deemed to be resident in New Zealand if they are physically present in New Zealand for more than 183 days in any 12-month period. There’s a subtle difference there between our days present test and many other jurisdictions in that it is based on a rolling 12-month period rather than a tax year. On the other hand, when you get down to defining a permanent place of abode, that involves quite a number of value judgements.

The current residency test is now over 30 years old. As noted above the Australian Board of Taxation suggested that really the Australian test perhaps should be more clearly defined in statutory legislation. And I’m coming around to the view that maybe that’s what we need to do in New Zealand as well. I’ve seen at least one academic article in the past year that’s picked up on this point.

“You can check out any time, but you can never leave”

Now, why we don’t do that is explained in the Inland Revenue Interpretation Statement on residency. Right now the permanent place of abode test does make it easy for someone to be defined as tax resident, but difficult to lose that.

Notably, the Interpretation Statement does not have an example of a time period of how many years must a person be overseas before Inland Revenue would consider that someone has lost their permanent place of abode.

So, this makes residency a very open-ended issue, which is not terribly good in terms of certainty for taxpayers. It’s become more of an issue in the past 30 years since we introduced the permanent place of abode test in 1989 because as we have seen in the last three or four years, the world’s got a lot more mobile with people moving and working around the world.

This issue of being tax resident here, perhaps inadvertently, is actually something that individuals are concerned about. They obviously want to minimise their tax obligations as far as legally possible. On the other hand, governments know that if you set out very specific tests then people will play to the letter of those rules by watching carefully the number of days present in a country.

A British alternative?

The British residency test, the statutory residence test, actually deals with this day count issue pretty well by specifying what it calls “ties”. Depending on how many ties to the UK you have, whether you’ve been tax resident beforehand and how many days you spent in the previous tax years, then the number of days you can spend in a in the UK in a tax year before you become resident drops.

It’s therefore not as simple as you can spend 182 days and then you’re okay. Each year it drops off quite dramatically and basically at its tightest definition you can only spend 16 days in the UK. Obviously, people will still try and manipulate their timing within these limits but the UK test is much more specific and it gives a great deal of clarity.

And I think in our case, just as the Australian Board of Taxation considers, it’s not an unreasonable objective to be looking at a statutory definition of residency which addresses the concerns Inland Revenue rightly has about people trying to game the system, but it provides certainty for people.

Becoming an Australian citizen – beware the potential tax trap

Still on Australia, there was good news recently that there’s now a pathway for Australia and New Zealanders who live in Australia to become citizens. This is very important for the huge numbers of New Zealanders over there, well over half a million. There is, however, a potential sting in the tail.

People will be aware that New Zealand has what we call a transitional residents exemption, which applies to new migrants or people who have returned to here and have not been tax resident for ten years. Under this exemption their non-New Zealand sourced investment income for the first 48 months is generally not taxable here.

Australia has a similar test if it applies to what they call temporary residents and it applies to most New Zealanders living in Australia. The sting in the tail is that if you apply for citizenship in Australia, you are no longer a temporary resident. What that means in particular is your New Zealand assets here become subject to Australian tax, including capital gains tax. The impact of Australian capital gains tax on New Zealand assets is often overlooked. It’s an issue I deal with regularly.

So that’s the trade off on Australian citizenship. Overall, it’s a good news and it puts people who have contributed significantly to the Australian economy on a level footing. But there is a wee sting in the tail for some. So, approach with caution.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week I’m joined by Shamubeel Eaqub, a partner at the boutique economic consultancy Sense Partners.

Shamubeel is a regular commentator on economics and is the author of several books including Generation Rent.

Terry Baucher (TB): Kia ora Shamubeel, welcome to the podcast. It’s been an interesting week, we’ve had three major reports on the true tax rate paid by the wealthy on their economic income. What have you made of all this? Are we any the wiser after these three reports?

Shamubeel Eaqub(SE): I think we are much wiser. I think we’ve all always suspected that the rich were not required to pay tax on a lot of their incomes. But we didn’t know how much income or how much wealth there was. So, the report by IRD in particular, I think was really useful to get a much better understanding of the survey of high wealth individuals and families. Just how rich they were and just how much income they were earning from wealth alone. The report that came out the previous week from Sapere and OliverShaw Consulting I think was really poor.

I think the official report laid bare those conjectures and I think fairly largely lobbying efforts that was done in the Sapere report.

(TB): Yes, the Sapere report was something, I’ve described it elsewhere as fairly indigestible. You had the complete difference in the conclusions the Sapere report reached that broadly speaking the wealthy were paying a fair amount of tax in line with middle income New Zealand. By contrast the reports from Treasury and Inland Revenue which show a completely different picture, with Inland Revenue concluding the median income tax rate on economic income was 8.9%, I think that raised a lot of eyebrows.

SE: It did. I mean the reports from Inland Revenue and Treasury didn’t show that the rich are not paying tax on the income that is taxable. What it showed was our tax system simply does not ask rich people to pay tax on the income that they earn. Most of the income earned, of course, is from capital. Wealth begets wealth and that huge amount of income, almost all of the income comes from that. You know, the wealthy becoming wealthier and they’re not paying tax on it because we don’t ask them to.

I think there was a sort of misconception that somehow the wealthy are sneaking around and not paying tax on what’s required of them. Although we suspect that they might do that as well. This report wasn’t really about that. But, you know, tax minimisation is a thing. There’s a whole profession that’s out there to help rich people do it very well, people like you, Terry. And then there was the other bit, which is, I think, a bigger and more pertinent question, which is “What counts as taxable income, and should that be taxed?”

TB: Yes, and that’s at the heart of this whole thing. It’s not controversial to be looking at the question of the distinction between economic income and taxable income, because I’ve seen other jurisdictions consider the same issues. On Wednesday, I was on Radio New Zealand’s The Panel. A panelist argued bringing in economic income into the equation isn’t right, because it’s not taxed and we’re also talking about gains not realised. But as you know, we do tax certain instruments on an unrealised basis. But broadly speaking, there is no controversy about looking at the economic value to determine what is a fair or what is a true rate of tax.

SE: There isn’t. And I think the norms will change over time as well. And at a particular point in time, income taxes were thought to be ridiculous, but they’re now the norm. There is nothing to say that there is no one form of income or wealth or a taxable base that we can’t tax. To me, it feels a little bit strange to think that just because we’ve got a system now, which defines taxable income as a particular way, that’s the only thing that we can possibly tax. That’s not true, as you know, when it comes to, for example, things like foreign shares, we have a foreign shares deemed rate of return regime, and that actually works pretty well because it takes a lot of the complexity away and you pay tax on the return that you’re likely to make on the asset that you have invested overseas.

We do tax [unrealised gains] already, it’s not like we don’t. We also do it on things like rates, which is calculated by reference to the value of our houses. So, it’s not like there is any reason why we should think that there can be no connection between wealth or the income earned and wealth. This whole thing that somehow it’s terrible we’re taxing unrealised wealth. As if these are poor people and they can’t afford to pay a tiny amount of that wealth by selling some of those assets or borrowing money or deferring it to a future point. There are so many ways we could design a system that would work quite well.

But to me, these [arguments] are just distractions. But these distractions are going to be really coordinated and very powerful because you know what? There’s a lot of money on the line.

TB: Were there any surprises for you in the numbers that came out?

SE: No, it wasn’t surprising. I think for most New Zealanders, the surprise would be just how rich the rich are.

TB: Yes. I figured that we might see something around the 10% mark because we knew other overseas jurisdictions had seen that. There’s that White House report from America where they actually have a capital gains tax and an estate tax and a gift tax. And they still think that the true tax rate on the economic income of the top 400 families in America is 8.2%, which is quite astonishing, really. Again, it illustrates the effect of what we tax and what we don’t tax although, the American system is riddled with particular exemptions. I do think you’re right, the scale of the wealth at the top end of these 300 odd families being collectively worth about $85 billion, I think that did take a few by surprise.

SE: Yes. I mean, it’s an extraordinary sum of money. And, you know, that is well beyond the conception of what any normal New Zealander could hope to have. And I think quite often when you think about the proposition to people when it comes to tax policy, particularly any taxes on wealth, they think that one, their wealth is going to be targeted or two, they might one day become wealthy.

But we’re not talking about that. We’re talking about, you know, a scale of wealth that there is very little chance that any normal New Zealander will ever achieve that kind of wealth.

TB: Yes, you’d have to have bought thousands of Bitcoin back in 2010 to match some of the numbers we’ve seen here. What do you think about the fact the median age of the respondents was 67? I think that was a little older than I was expecting to see. What can we read into that?

SE: I think it shows people who have made it, who worked hard, got lucky because luck and hard work are the two things that are the key ingredients for becoming quite wealthy. And sometimes intergenerational as well. I think it shows there was a bunch of people who came through that period of the economic reforms which made some big winners and losers, and some of them did spectacularly well.

And we see that, right. We know we know some of these individuals who are out there in that kind of age group. They’re quite visible and well known. It doesn’t detract from all the work they might have done. It’s more that I think they lived through a period of time which created opportunities that were quite unusual.

TB: Is that a moral, do you think, then, going forward for all of us, just come back to your point a few minutes ago, that people say “Well, so-and-so has made X and we can as well.” Or are we different economy, different times?

SE: Well, I think we will mint new billionaires and multimillionaires over time. They will be the Rod Drurys, and the Peter Becks, as well as the Stephen Tindalls and other people.

So there are different ways and some people are at the right point at the right time with the right skills and all those bits that make that magic. But the reality is, in a country of five million people, not all five million of us will have that magic.

TB: Indeed.

SE: A vanishingly small number of us will ever have that. So, I don’t think it’s a model that’s replicable, per se. It’s, of course, nice to have that aspiration that we should try and improve ourselves. We should start businesses; we should try and do well. We should create jobs. But actually, for most of us, we’re not going to achieve and attain those kinds of numbers, that kind of wealth.

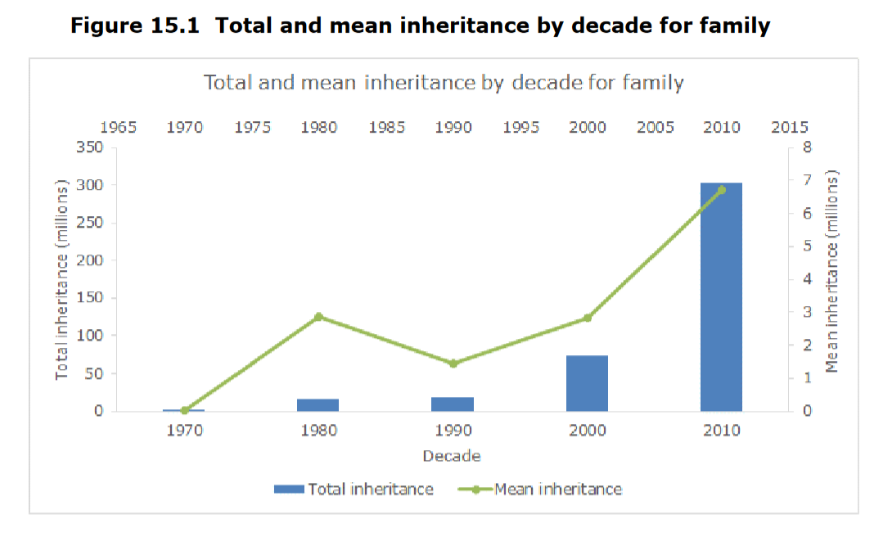

TB: Actually on wealth one of the things that I was intrigued to see Inland Revenue had looked at was the impact of inheritances. And this saw $411 million that had been transferred in what they call sizeable gifts, which is more than $25,000. But that was over a 50-year period, which isn’t terribly significant. I think that if memory serves right, half of that happened in the decade between 2010 and 2020.

What do you make of that? We’re not talking about old money being passed down from generation to generation, are we? Or maybe the money is still locked up in trusts. Did that surprise you? Because it was a surprise to me. I was expecting to see bigger numbers than actually popped up.

SE: Yes, I think there are now a lot of family offices for the truly wealthy families. It doesn’t make sense to give the money away. It’s much easier to keep it locked up because you get the economies of scale from running a family office, which gives you the ability to create even more wealth for future generations.

So, I wasn’t super surprised because there was no great incentive to dilute your wealth and to give that money away. I’m not really clear on what the definitions were in terms of those inheritances. Was it really money being gifted or was it the returns that are given to family members? There are lots of different ways that you could think about that. But my sense is that there is no great tax incentive for [the wealthy] to give the money away. There is no kind of reason for why you shouldn’t have the trusts and structures going on in perpetuity.

So was Thomas Piketty right?

TB: I see that Thomas Piketty has been quoted on Newshub about the report.

We know that Piketty is David Parker’s favourite economist or one of his favourites. Do you think this vindicates what Piketty has been saying?

SE: But I think it confirms what we know to be true, wealth begets wealth. To be very rich, it’s very helpful to begin by being very rich. And we also know that because of the way that our tax system is designed, it is designed for the many rather than for the few.

So, you know, inevitably you’re going to see the critique that this is the politics of envy and all that kind of stuff. But actually, when you jump back and ask the question ‘What is income and what should be taxed?’ it does take you away from that idea of envy. And actually, your income is very large and you’re not paying the same share as everybody else. Why is it that because you are wealthy, you are exempt from this income that you earning?

I think this was the core fundamental of the kinds of things that Piketty has been arguing for, why is this unearned income, this accident of birth? Why is it that you have some God given right to keep that protected from the rest of society? Why is it that that wealth, that income is not part of the wider taxation system in a society that you choose to participate in?

TB: I guess a response to that would be, well, we pay most of the tax anyway. It’s a small group, the numbers being pushed say the top 2% or 3% pay 26% of the tax. So the probable counter might be, ‘Well, we are paying enough anyway. We are paying our share.’ What would you say to that? Again, I guess it’s a question of how we define income, isn’t it?

SE: I think so. And I think, it’s also entirely possible to counter that with saying, ‘Well, if you also pay 20% like the rest of us, then, in fact, that future reality might be that all of us pay 15%.’

TB: The broad base, low-rate approach, broadening the base and lowering the rate. Yes.

SE Exactly. So, the alternative features are not just that they pay more. It might be that they pay more and the rest of us pay less. And again, this still goes back to the fundamental question of what is income and what we choose to define as taxable income.

And I think that’s really what came through that entire work. It wasn’t really about wealth. I mean, for me, it was really about asking the question of what do we actually consider to be income? And why is it that our tax system deliberately and specifically excludes some forms of income? Just because they happen to be the domain of the rich.

A ground-breaking report

TB: The report has been described as groundbreaking and not because of its methodologies, because those are fairly common. We were talking earlier that there seem to be three different methodologies and Treasury got down to nine different calculations of effective average tax rate, which I think was testing the patience of even the most dedicated of us.

What marks this report out as groundbreaking in my view, is we’ve actually got really good hard data, to work on for a change. And so it’ll be interesting to see how this plays out around the world.

SE: As you know, Terry, this is not new in the sense that there’s been other countries, particularly the US, where they’ve really kicked this off trying to find out what’s going on, because, you know, the domain of the very rich is quite opaque.

They can keep things opaque because they’re very rich and they have very good lawyers and very good accountants. And also, people are private because they don’t want people to know how much money they’ve got. But the groundbreaking nature of this study was very much that now we have real data based on an extraordinarily high rate of response.

TB: I think it was 93%. And, you know, fair’s fair, to be honest when the project was announced, there was a lot of immediate pushback on this. But 93% compliance, I think, is something I would expect that’s actually better than Inland Revenue were hoping for at the start of the project.

SE: I think it’s excellent. I mean, we know that there is a large enough population to give us a really good understanding of what this group of people look like. But I think it also speaks to something about it’s not like these people are necessarily trying to hide things, right?

When you see these kinds of numbers come out, there’s always a tension that all the rich are trying to hide things or they’re not trying to pay their fair share.

My sense is that that’s not really what the high rate of participation shows. I think what it shows is that people are relatively open. I mean, of course, there’s always a risk of not complying with Inland Revenue’s requests. But to me, it shows that even the very rich families, they do feel there’s a civic responsibility participating in society, that they want to be part of New Zealand and a tax system that is fair and transparent.

At least for me, the signals were very positive that these very high net worth individuals and families, they wanted to share that information so that we could have an open conversation about what is it that we want to do. Because the reality is that if we make changes on things like capital gains or wealth taxes, it’s not going to be just those families that will be affected, it will be a wider group of people. And having that transparency and openness does make it easier for us to have those conversations.

I think the study is really helpful because those studies give us real data and also just showed us the distribution of New Zealand. You know, the 99% of New Zealanders will live very different lives to that top 1%.

So how did the rich get rich?

TB: Yes, indeed. Just on the distribution in the report was there anything of interest to you about the range of the sources of that wealth? There’s some property, new technologies. Anything stood out for you in that data?

SE: Well, I mean, to me it was more that there was such a variety. I think that’s cool, right? It shows that to be filthy rich, there isn’t a common formula. There’s lots of different ways people have become filthy rich. Some of it because of, you know, like just being at the right time, at the right place in the right industry or having the right whatever. But it wasn’t all property. It wasn’t all one thing.

TB: Now the property thing is really interesting. I think on average each of the 311 families held 22 properties. But the analysis and modelling by Inland Revenue showed the capital gains weren’t all from property, they represented a range of things, portfolio investments, but mainly their own businesses that they had built up.

And that actually was something I thought was quite encouraging because you take that and the fact that we did not see a lot of inheritances being passed down and you got the impression that there were people who could come in and start at the bottom and have huge success. You mentioned Peter Beck earlier. Rod Drury of Xero would be another example of that. Stephen Tindall with The Warehouse, three different types of industries there. None of those are traditional industries, by the way. They’re not farming, or forestry related, but they’re all very wealthy people as a result of that. I guess people might say it shows a more diverse economy and the opportunity existing in that. So, I was encouraged by that.

SE: I think so. I think for most New Zealanders, the story of wealth creation kind of goes to a housing type story, right? Actually, there are a lot of people who’ve made a lot of money by starting businesses, selling businesses, or keeping businesses and growing them. And that to me is what creates economic vitality. That’s what creates a better New Zealand, right? That’s what creates more jobs.

I mean, of course we need homes. But you know what? It’s such a passive way to create wealth. Businesses are exciting because you’re creating jobs and changing lives through providing livelihoods. That, to me, is enormously more satisfying and exciting. Seeing a lot of that in the very high net worth individuals tax statistics, I think was very encouraging.

But it’s also true that not only do they make money by being in business, they continue to invest in businesses. So, it’s not like, there are these rich families that are sitting there with all this money sitting idle. We know they’re using that money all the time. They’re always looking for the next big opportunity. Of course, they don’t get it always right. But the reality is that, you know, I’ve been involved with businesses startups with these high net worth individuals, and they are the ones who back people. They’ll say ‘Here is a cheque for $1,000,000. I’m going to back you.’ And that is hugely powerful.

TB: That was something I came across when I was on the Small Business Council, the access to venture capital in New Zealand is surprisingly good. There is a fair amount available, and it is these wealthy people reinvesting in businesses. They go looking for the next Xero, the next Rocket Lab. And again, that’s encouraging.

What next?

So, what next? If you’re the Finance Minister or the Prime Minister, you’ve got this report and you say, ‘Right, here’s what we’re going to do.’ What would be the three things you would say to address the issues these reports have thrown up and improve our tax system?

SE: Well, if I were truly a politician in New Zealand, you know that I would have already sent out a poll asking a small group of people what they think about more taxes because we do politics by polling in New Zealand. And the polls will show that nobody, no New Zealander wants more taxes because they’re afraid that they might one day be rich, and they might be asked to pay tax on it.

So, you know that that the self-interest, that greed, that fear of missing out of a potential future, which is I think almost impossible, I think that would motivate most polls and they would show that people don’t want more taxes. And as Finance Minister, if I were truly in Cabinet today, I would see those polls and say ‘Bugger it, I’m not going to do anything. Bury this thing.’

That is the sad reality, it’s heartbreaking that we have seen very little action when it comes to tax policy in New Zealand for decades. Because you know what? We just don’t have the steel and the political consensus across the community to do anything different.

TB: Yes, I think that’s it in a nutshell. I mean, I think Jim Bolger’s ‘Bugger the pollsters’ is something that should be adopted when it comes to tax. Because the politicians, and it’s interesting, doesn’t matter which side, they run away from the issue.

I know I’m a broken record on this. I’m looking at what’s coming down the track, what the Tax Working Group saw was coming down the track. We’ve got demographics working against us with ageing, higher superannuation costs, greater health care demands and now climate change.

The Climate Change Commission in its report released yesterdaybasically said ‘We can’t buy our way out of reducing our emissions, we need to diversify.’ And that report, when it talked about tax, made repeated mentions of tax incentives for better investment to address these issues.

So, it seems to me that like it or not, politicians are going to have to address these facts or simply say, well, ‘You can’t have anything because we need to protect these unrealised gains.’

SE: You know, I was probably being overly pessimistic. But I think the thing is, in the current moment in time, the crisis still feels like it’s two or three or four or five political cycles away.

If you make changes on tax policy today, inevitably you will see whoever’s in power next undo them. So there will be no enduring tax policy because we don’t have consensus in New Zealand. Do we have a pressing need to shift our tax policy? Of course, we do because of demographics and because of climate change, because of large infrastructure deficits, we know that we need to change things. But we also know that New Zealand has an extraordinary reactionary political system. There is no leadership, it is reactionary. And so, unless there is a crisis, until something really breaks, we’re not going to change.

TB: So you don’t think Cyclone Gabrielle, or the Auckland floods are a breaking point?

SE: Not at all. I mean, they might cost the government, you know, a maximum of $15 billion in the scheme of things. That’s nothing spread over three or four years.

You know, the Government’s tax take per year is $100 billion. Those costs are at the margins. So that’s not enough. It’s when you’ve got Cyclone Gabrielle happening every year or every other year when people can’t get access to insurance, when we’ve got coastal properties that are being inundated, when we’ve got erosion that’s taking away what we’ve previously valued as multi-million-dollar bachs. That’s when you’re going to start to really strike those pressure points, because we haven’t actually planned for any of this stuff.

TB: Those are all happening right now, actually. I mean, Tairawhiti East Coast region, I think Cyclone Gabrielle was the fourth major event that warrants special tax treatment inside 12 months. But as just said, it’s now receding into the background. Maybe it’s not so much our politicians, it’s also our media cycle just isn’t adapted to that.

SE: I think it’s less about the media cycle, it’s also what we want to hear as citizens, as engaged people in politics, people who are engaged in the civics of the country. Are we actually engaged in grappling with these big structural issues? And the answer is no. And I think the conversations that we have on public policy in New Zealand are, by and large infantile.

You know, they are by and large led by people who are lobbyists and people who are actually biased with a huge amount of self-interest because it is a small group of people who do everything. There’ll be the tax experts who are providing expert advice to people to minimise their taxes and the same people who are going there to try and design a business tax system. Well, I don’t know, man can you really trust them?

TB: Well, reputational risk here, but yes, I think self-interest is a problem. But let’s just be bold, let’s say you’ve decided ‘Bugger the pollsters’ what would you do?

What tweaks would you do if you were looking at something that might take the population around along with you? What would be the first thing to do.

A tax switch?

SE: You know, I think one would be relatively easy in that you would do a tax switch. You would implement a land tax and you reduce something like GST. That switch would be quite immediate and it would create a much better balance in New Zealand. It wouldn’t capture the very high net worth because it’s not about that, but it would create the introduction of a wealth tax. We already have the mechanisms for that with things like the rating tools.

But, you remember with the Tax Working Group, the land tax was one of those things that was identified as a good tax to have, because we know that not only would it incentivise better use of our land that we have, but it’s also that one asset that can’t run away, like unlike many of the other types of assets that people hold. So that would be the big thing.

But fundamentally for me, it’s really around if you really want to change tax policy, you’re going to have to create consensus. And you know, we can’t do that until we have some kind of bipartisan agreement about, one, what the issues are, and two, that we fundamentally either need to have higher taxes or we simply cannot have all the services that we have promised ourselves.

Now, that’s a really hard conversation to have. You know, you look at the quality of our political leaders. They’re not engaged in any of that debate. You know, most of our political leadership is engaged in the politics of who’s going to do the least.

TB: It’s a very small target strategy.

SE: It’s sort of, if you ask me what needs to change, I think the change that needs to happen is not that you need to jump in and make lots of changes, because the reality is that the knee jerk reaction will be to reverse those through a change of government. I think the change that requires us to have is actually creating something like the Climate Change Commission that creates this conversation. Some of those public policy issues that take the politics out of it.

TB: So, are you saying there should be the equivalent of the Climate Change Commission, a Tax Policy Commission that alongside David Parker’s Tax Principles Act, but sits there and pushes out the reports and saying, ‘This is it, guys, this is what we can do.’ In other words, a semi-permanent tax working group.

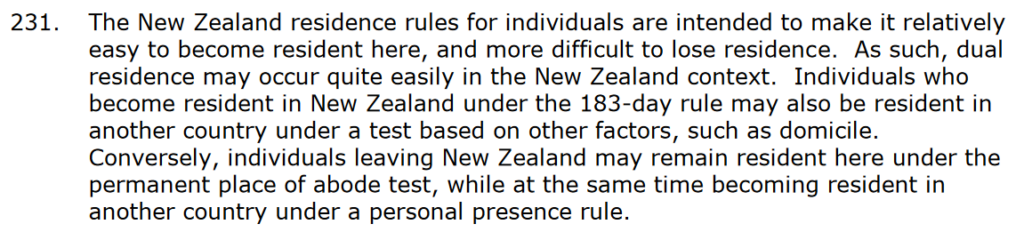

SE: Except of course it must have powers and it must have the ability to hold the politicians to account. Quite often what we do with things like the Climate Change Commission is we give them the power to design, but we don’t give them the power to actually fund or hold the powerful to account.

It’s not going to be very hard, right, because no politicians want to give the power away to somebody else. There will be no independent body that they’re going to give the powers away. The only one that they’ve really done that with is the Reserve Bank, and I think they’ve been regretting it ever since.

TB: Yes, I was thinking of the Reserve Bank too. I think that’s probably as good a point as any to leave it there.

Shamubeel, thank you so much for being on the show. Really appreciate your insights on this. I hope I don’t feel so pessimistic, but to be frank, we probably have good reasons for people to be sceptical about what will change anyway.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week, kia pai to rā.

Happy new tax year and welcome to the 2023-24 tax year and as is often the case the start of a new tax year it means newly enacted legislation is now in place.

However, some of the same old issues are still with us.

The Taxation (Annual Rates for 2022-23, Platform Economy and Remedial Matters) Bill (Number 2) finally received the Royal Assent on 31st March. Apparently this bill had nearly 200 new clauses, which between them had some 42 different application dates. So, it was a surprisingly complex bill. But remember, its most controversial proposal to standardise the treatment of GST on fund management firms was removed.

As noted, the bill has got quite a considerable amount of new provisions in it, and we’ll pick up several over the next few weeks. But I want to start by looking at the new fringe benefit tax (FBT) exemptions for bikes and public transport. As you may recall, the bill originally had an exemption for public transport, but at the last minute an FBT exemption for bikes was introduced. That actually covers bikes and “low powered vehicles”, so obviously covers scooters, e-scooters, e-bikes. The exemption from FBT applies where you are travelling between home and work. There’s going to be a maximum cost for the low-powered vehicles, which is yet to be confirmed by regulation shortly.

Watch out for the hook in the FBT exemption for bikes and public transport

But the key point to keep in mind is that the bike or scooter must be used mainly for travelling between home and work. Therefore, where that isn’t the case, FBT would still apply. This together with the maximum price cap on the exemption should rule out people buying high end bikes, e-bikes or e-scooters and then using them mainly for private use hoping that it’s exempt from FBT.

Now the exemption is from FBT, there is no equivalent exemption for PAYE. What that means is, it is very important for employers to consider how they provide that benefit and don’t make the mistake of assuming “Well, the FBT exemption applies so nothing to worry about.” The issue that arises is where the employer purchases the bike or scooter directly, then the FBT exemption should apply. However, if the employee chooses and purchases a bike personally and is then reimbursed, then PAYE will apply and there’s no exemption.

This principle also applies to the exemption around the use of public transport or vehicle shares, such as Uber and similar apps. Again, the employer must incur the cost for the exemption to apply. As some have noted that’s actually administratively quite awkward. It seems likely quite a few employers will accidentally trip up on this by reimbursing the employee rather than incurring the costs directly. The hope is that this particular anomaly can be quickly resolved and therefore ease the compliance involved.

Now, the new act also contained a permanent exemption from the interest limitation rules for build to rent dwellings. This exemption will apply where there are at least 20 connected dwellings, and the landlord must offer a fixed term tenancies of at least ten years. By the way, for the purposes of the interest limitation rules, as of 1st April, only 50% of the interest is now deductible unless one of the exemptions, such as a new build or build to rent, applies.

Interest limitation rules and short-stay accommodation – don’t get mucking fuddled

Coincidentally, last week, Inland Revenue released a draft interpretation statement for consultation on the interest limitation rules and short-stay accommodation. The interpretation statement considers how the interest limitations will apply and then also explains what other income tax rules may be relevant depending on the circumstances. The draft interpretation statement runs to 79 pages and is now common practice, it’s accompanied by a fact sheet.

It says much about the complexity of the rules in this area that the fact sheet runs to 13 pages. That’s because not only are the interest limitation rules applicable owners of short-stay accommodation must also take into consideration the potential application of the mixed use asset rules which have been around for over ten years now, as well as the ring fencing rules.

For the purposes of the draft interpretation statement, short-stay accommodation is defined as accommodation provided to paying guests for up to four consecutive weeks. The interpretation statement covers five scenarios where such accommodation is provided:

either in a holiday home; in a person’s main home; in a separate dwelling on the same land as the main home; in a separate property used only for short-stay accommodation; and on a farm or lifestyle block.

Within each of those five scenarios, the interpretation statement will explain if and how the interest limitation rules will apply, what apportionment rules apply, and whether ring fencing rules apply. There are also variations within these scenarios. If there’s a new build involved, for example, a person’s holiday home is on new build land, then the interest limitation rules will not apply. However, the deductibility of interest is still subject to the other apportionment rules, such as those contained in the mixed-use asset provisions and the ring-fencing rules will still apply.

As can be seen, there’s a great deal of complexity now involved, and this is partly the result of the somewhat ad hoc approach adopted by the Government in tackling what it sees as the preferential treatment of residential property investment. It also reflects generally incoherent policy resulting from the lack of a comprehensive capital gains tax. Whatever, the key lesson to watch out for is that the short-stay accommodation rules are now incredibly involved, so proceed with great care.

The taxation of capital is a longstanding issue and one which in my opinion, will need to be addressed sooner rather than later. Not only because of the tensions it creates within the tax system, but also because of the need to find additional revenue to meet the demands of an ageing population and the impact of climate change, which we’ve spoken about previously.

We like New Zealand Superannuation – but how are we going to pay for it?

And three reports this week highlighted this ongoing tension around meeting future liabilities. Firstly interest.co.nz covered a study coming out the University of Otago regarding New Zealand Superannuation. The study surveyed almost 1300 people in 2022 asking them what they felt about the age of eligibility, means testing and the willingness to increase both current and future taxes to pay for New Zealand Superannuation.

The study found there was widespread opposition to financial barriers for receiving superannuation. Means testing was not popular, but the support for keeping the retirement age at 65 has increased, with almost a quarter ranking the age of 65 as most important aspect of New Zealand super compared with a fifth back in the 2014 survey. 61% of those surveyed ranked raising the retirement age to 67 as the worst policy. The general response was they would prefer universal superannuation.

The New Zealand Super Fund, which has been established to help spread the cost of superannuation was popular. Although there was opposition to increases in current taxes to pay for New Zealand Superannuation, a majority of respondents still support higher current taxes to reduce the size of future increased tax increases given plausible investment returns.