The Government’s tax and social policy work programme is announced.

- more on Inland Revenue’s crackdown on student loan debt

- and why we might need to pay more tax

At an event for the Young International Fiscal Association, the Revenue Minister, Simon Watts announced the Government’s Tax and Social Policy Work Programme. These work programmes are a working document updated frequently so that after a change of government they reflect the new government’s priorities in tax policy and social policy areas.

According to the speech made by the Revenue Minister, the work programme under the current government is designed to support rebuilding of the economy and improve fiscal sustainability by simplifying tax, reducing compliance costs and addressing integrity risks.

There are six areas of priorities going forward: economic growth and productivity, modernising the tax system, social policy, the integrity of the tax system, strengthening international connections and other agency work.

Out with the old, in with the new

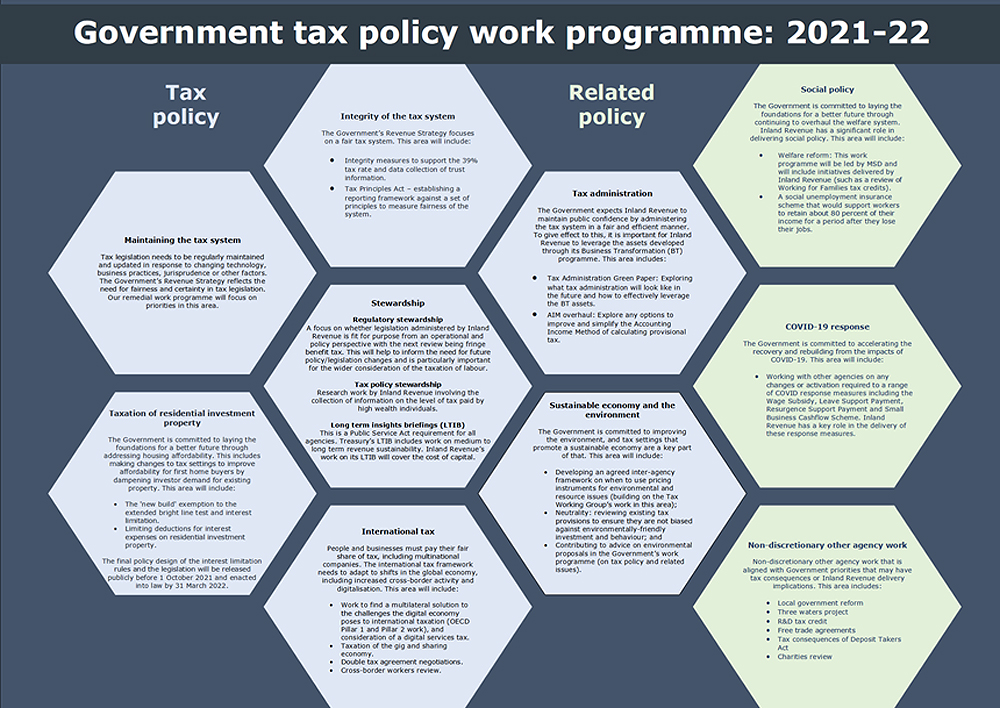

It’s interesting to have a look at what changes have been made since the programme was last officially updated back in 2021-22.

There under the Labour Government, there were 10 work streams of tax policy and related policy matters some of which overlap with the updated programme. Social policy integrity of the tax system, maintaining the tax system were all part of the 2021-2022 work programme and they’ll be part of every work programme going forward.

On the other hand, the COVID-19 response and the taxation of residential investment property were two major areas back in 2021-22 which are no longer there. As is well known the current government when it came in repealed all the work in relation to changes to the taxation of residential investment property.

Tax policy changes already happening

Drilling into the latest workstreams, some of them are already underway such as improvements to employee share schemes, implementation of the Crypto-asset Reporting Framework, simplification of the Approved Issuer Levy reporting including allowing retrospective registration and changes to inward pension transfers. All these are in the current tax bill before the House.

The other interesting things they’ve added in here, which we’ll watch with some interest, are exploring compliance cost reductions, including improving tax compliance with small businesses. Now you recall last week in my review of Inland Revenue’s annual report one of the areas Inland Revenue felt that business transformation hadn’t delivered as much as had been hoped for, was in reducing compliance costs for small businesses.

I totally support what Inland Revenue are doing, but the issue that they’ve run up against is that sometimes it has to accept the trade-off between good tax policy and the risk of tax seepage around the margins. If a policy allows a deduction or other benefit for taxpayers such as SMEs that meet certain criteria, you get certain deductions, Inland Revenue is always concerned about people exploiting that. The question that arises is does the wish to reduce compliance costs outweigh the risk that some of those measures might be abused?

A place where talent wants to live?

An interesting one that caught my eye was their plan to review the Foreign Investment Fund rules. This is something that was mentioned in passing by the Minister of Revenue at the recent New Zealand Law Society Tax Conference. This looks to address the issues raised by the report The place where talent does not want to live in relation to the problems the Foreign Investment Fund regime causes for investors migrating here.

Another interesting one is reviewing the thin capitalisation rules for infrastructure. That’s almost certainly tied up to the desire to have public/private partnerships help build infrastructure in the country. What it would almost certainly mean is that the current thin capitalisation rules (which basically limit interest deductions for international multi-nationals, which have more than 60% debt asset ratio) would almost certainly be relaxed.

In terms of other agency work Inland Revenue is considering, is an improved information sharing agreement with the Ministry of Business and Innovation and Employment, student loans, the question of final year fees free and overseas based borrower settings, the highly topical Treaty of Waitangi settlement, Local Water Done Well and supporting the all-of-Government response to organised crime. (Organised crime often represents tax evasion so it will always fall in the ambit of Inland Revenue).

Changes to the taxation of the Super Fund?

A big work programme, probably in terms of modernising the tax system, would be exempting the New Zealand Superannuation Fund from income tax. This would be quite significant as the New Zealand Superannuation Fund probably contributes $1 billion a year in company income tax. On the other hand, the Government will probably then be able to dial back completely its contributions to the scheme. In other words, the fund would now be expected to be self-funding going forward, which is quite possible now it’s reached a near critical mass of at least $70 billion in value.

The document’s fairly light on detail, just a one pager, but it gives you an insight as to where the priorities are right now. There are no real big surprises and we’ll watch and bring developments as these policies mature and are brought to fruition.

Student loan debt – Inland Revenue ups the ante

Moving on, last week I talked at some length about Inland Revenue’s actions around the collection of student loan debt and it so happened that yesterday Inland Revenue’s Marketing and Communications Group Manager Andrew Stott appeared on RNZ’s 9:00am to Noon with Catherine Ryan. They discussed what Inland Revenue is doing with its extra $116 million of funding over the next four years. This Includes an additional $4 million for recovering overdue student loan debt.

Quite a lot of interesting commentary came out of this interview. One of the first surprises was that many young people going overseas don’t know that their student loan debt, once they leave the country, starts to accrue interest. Therefore, they get behind surprisingly quickly. As is known, only 29% of overseas based borrowers are making repayments at the moment, and the student loan debt is now up to $2.37 billion, $2.2 billion of which is owed by overseas borrowers. A substantial number of whom are based in Australia.

So that’s now obviously a focus both operationally and in the latest work programme. I’m particularly interested to know more about what is planned in the overseas based borrower settings. What does Inland Revenue consider it needs to improve its ability to collect debt under the student loan scheme?

Inland Revenue has been allocated $4 million in funding to get cracking on recovering debt and it’s expected to produce a four to one return this year, which is expected to rise to eight to one next year. It will meet those targets pretty comfortably I’d say. Apparently in the first quarter of its new financial year – 1st July to 30th September this year it’s already collected $60 million in overdue debt up 50% from last year.

A surprising statistic

I guess the big surprise that came out of the interview was when Mr. Stott noticed that most of the debt is owed by people in their 40s or 50s who had never got round to repaying Inland Revenue. These people had been much younger when they went overseas with student loan debt which then accumulated as interest and penalties were added. This does beg the question that if people went overseas in their 20s and we’re now chasing them in their 40s and 50s, what was Inland Revenue doing in between?

As I said in last week’s podcast, relying on late payment and interest charges for enforcement just doesn’t work. We know from research in other areas when a person’s debt blows out (and probably the threshold is as low as $10,000), people will put their head in the sand and not take action because the matter feels too big to manage. Mr Stott mentioned that there’s several debts running into tens of thousands. I have seen one where it’s over $100,000. The average debt owed is about $17,000, but it’s the old overseas debtors, obviously larger debts, that Inland Revenue is going to be targeting.

As part of this it is talking to anyone who returns to New Zealand who has a debt of at least $1,000. They can now identify such persons thanks to the information sharing that goes on between New Zealand Customs and Inland Revenue.

Inland Revenue also have the ability to detain/prevent someone from leaving until they have a conversation about payment of debt. According to Mr Stott the group being targeted are those who have persistently not engaged with Inland Revenue. They have not responded to Inland Revenue at all. They’ve simply just said now go away, I’m not going to talk to you and ignored them. They will be fined and will find themselves having an extra stay at the airport just prior to departure.

Deducting debts from overseas salaries?

Inland Revenue has the ability to issue deduction notices requiring amounts to be withheld from payments to Inland Revenue debtors. (According to an Official Information Act response I got from Inland Revenue, it issued over 42,000 such notices in the year ended 30th June 2024).

Mr Stott was asked whether it could do the same in Australia? Can Inland Revenue ask the Australian Tax Office (ATO) to issue the equivalent to a deduction notice so that an employee working in Australia has part of their salary deducted to pay student loan debt. The answer is yes it can, but it’s not easily done. It’s termed a “garnishee order” in Australia and requires a court order. Consequently, Inland Revenue hasn’t really used such orders.

It seems to me that is something Inland Revenue really will need to look at closely, because if you’ve got 70% non-compliance and you’ve got an estimated 900,000 student loan debtors in Australia, it would be worthwhile establishing a process to enable garnishee orders to happen more frequently.

It may be that they have to ask the ATO to amend legislation, which would delay everything. But it would appear that they have the tools already, so it will be interesting to see if that’s employed more frequently.

Increased audit activity

The other thing Inland Revenue has ramped up is audit activities. It has apparently already launched 2,000 audits in the first quarter of its new financial year. This is up 50% on the previous year. Incidentally, 10% of those, are targeting the largest companies in the in the country.

As previously mentioned, Inland Revenue have recently targeted bottle stores and the construction industry. The next group of people that they’re going to be talking to now are vape stores, nail salons and hairdressers. Because in all cases they suspect cash income is not being declared, so these businesses will be the subject of unannounced visits.

The focus in Inland Revenue now is on enforcement and debt collection and there are more signs of it. So, I’ll repeat what I’ve said previously. If you have debt with Inland Revenue approach them to discuss it. You will find that if you take proactive action, it will be reasonable in most cases, unless you have a history of non-payment In which case good luck. Taking proactive action is the best approach, because tax debt is something you simply can’t put your head in the sand and hope it goes away. It won’t. Inland Revenue has got many more resources now, and the net is closing.

Why we might need to pay more tax

Finally, earlier in the week, I was one of several commentators Susan Edmunds of RNZ spoke to for a story on why we might need to pay more tax. Her story picked up the recent speech by the Treasury’s chief economic adviser Dominick Stephens which noted that the country appears to be running a fiscal deficit of 2.4% of GDP – that’s about $10 billion – and the pressure that’s building on demographic change, the ageing population, and rising healthcare costs. The article also referenced, Treasury’s 2021 Statement on the long term fiscal position He Tirohanga Mokopuna. I repeated that I think it is a matter of when, not if, the tax take has to rise when you put all these factors together.

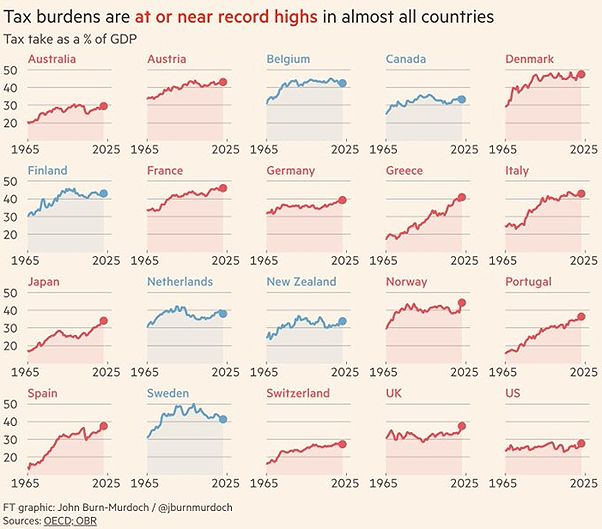

It’s also worth noting that the recent UK budget I covered a couple of weeks back increased taxes. Subsequently, the Financial Times had a very interesting graphic noting that tax burdens as a percentage of GDP for the last 50 years are at all-time highs in 14 of the 20 countries highlighted.

The pressure on tax revenues is a global problem, so we are not alone in trying to deal with these issues.

I think the break point, so to speak, will be the increasing cost of dealing with the damage as a result of extreme weather events. And I note that last week the Helen Clark Foundation released a report on the question of climate change and insurance premiums. My personal view is we need to get moving on this sooner rather than later, because that will help ease the transition.

Other jurisdictions we compare ourselves with, such as Australia and the UK, have a 45% top rate. And of course, in Europe the rates are much higher, still around 50% or so. I remain firmly committed to the broad-based low-rate approach, which means if we do broaden the base, we can hold tax rates down below these levels.

More tax, or less costs?

There was a nice to and fro in the comments on the LinkedIn post I put up with one commenter noting that we also need to reduce costs. Managing our expenses is part of what we have to do here, but if we’re talking about 2.4% of GDP, I think the pressures are too great for such a big gap to be easily closed just by better enforcement and cost management.

University of Auckland Professor in Economics Robert McCullough, thinks that this tax debate will define the next election in terms of “if we’ve got these expectations, how are we going to pay for everything?”

We shall see. And as always, we will bring you developments as they happen.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.