- New Digital Services Tax Bill

- National’s tax policy launched

It’s been a busy week in the tax world. The Taxation Principles Reporting Bill passed its third reading in Parliament and very shortly will receive the Royal assent. Now this was the bill introduced at the time of the May Budget, the purpose of which was to provide a statutory reporting framework and required the Commissioner of Inland Revenue to provide the Minister of Revenue with an annual report on the operation of the tax system.

This report would outline aspects of the tax system against a set of tax principles such as equity, efficiency and certainty. As commentary provided by Inland Revenue to the Finance Expenditure Committee noted. “These principles are often considered when designing changes to a tax system”.

Tax being political the Government also wants this bill to

…help improve the public’s understanding of the tax system and encourage informed debate about its future. New Zealand has seen several Tax Working Groups and Committees over the last 20 years, with the most recent being the 2019 Tax Working Group These reviews have offered useful insights into the operation of the tax system and suggestions for improvement. These reviews have also highlighted areas of the tax system where information is lacking, which makes a fully informed debate on some aspects of the tax system more difficult.

The bill requires the Commissioner of Inland Revenue to prepare and publish an annual report which considers the tax system measured against the principles included in this bill.

Generally speaking, the principles in the bill are well established. The Inland Revenue commentary references the tax principles made in all three of the reports this century, the McLeod Report in 2001, the Victoria University Tax Working Group Report in 2010, and finally the most recent Tax Working Group in 2019. They all used and refer to basically the same principles of taxation.

What will happen is Inland Revenue will produce a short form report annually with a full report every three years. The first full report will be produced in 2025 with the shorter version reports produced in the interim years starting later this year. The intention is to align the requirement for this report to be produced the second calendar year of each parliamentary term.

There’s been some discussion around whether we need this bill and how does it sit within the Generic Tax Policy Process (GTPP)? You could say it’s an extension of the GTPP and of course, it does mean that we can have a look at some of the tax policies that have been put out by the various parties and compare them against the principles set out in this bill. And I’ll be doing that a little later on. The politicians may find this new bill is something of a double edged sword.

A Digital Services Tax just in case…

It so happens a digital services tax bill was introduced on the last sitting day of this parliamentary term which is a bit of a surprise. Digital services taxes (DST) have been talked about for some time but have generally not been brought into effect. They’re obviously not favoured by the targets, the digital giants such as Google and Facebook. But they are a tool that many governments around the world have been considering implementing.

The ongoing OECD Pillar One and Pillar Two negotiations are intended to eliminate the need for these taxes. In fact, it’s a condition of the introduction of the OECD model that any digital services tax in effect would be repealed.

The Government’s actually been looking at a DST for some time. There was a discussion document back in 2019 on the topic. That said, it still was a bit of a surprise to see this bill pop up at this particular time. Arguably, you could see it as a bit of politicking. The key thing is the Government is already committed to not introducing a DST until 1st January 2025 at the earliest. Now Inland Revenue and Treasury have said it will be handy to have the legislation ready just in case the OECD deal falls over. So that’s a reason given for this bill being introduced now.

The DST would target multinational multinationals with global revenue in excess of €750 million per year from digital activities and New Zealand revenue from these activities which exceeds $3.5 million per year. The DST taxes the revenues rather than the profits, because then it doesn’t require trying to establish a connection with a multinational’s physical presence in New Zealand. The rate to be proposed is 3%, pretty standard compared with others around the world.

This bill is a more fallback measure and it’s interesting to see where it stands that they’ve made this move now. But many countries have DSTs, Britain is one, France another and India is probably the biggest exponent of them. And as I said, the Government’s basically saying, ‘We want this in our back pocket in case the OECD Pillar One and Pillar Two deals fall over.’ These are still very much up in the air for discussion, as we’ve mentioned in previous podcasts.

National unveils its tax policy

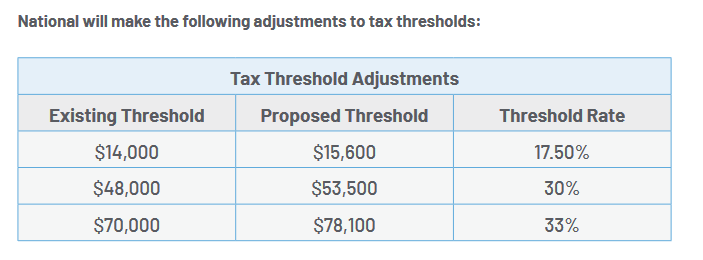

But the big news this week would have been the launch of the National Party’s tax policy on Wednesday, and it landed with quite a thump and contained quite a few surprises. National had already signaled well in advance that it proposes to increase thresholds by 11.5%. As regular listeners to this podcast will know my view is tax threshold increases are long overdue.

What about Working for Families abatement?

National has an identical proposal to that of Labour to increase the Working for Families In-Work Tax Credit by $25 to $97.50 per week starting next April. There’s a commitment that the current $42,700 abatement threshold for Working for Families will rise to $50,000 from 1st April 2026. This is also a Labour Party commitment. But as I said to a number of media outlets, the problem is that the Working for Families abatement threshold already kicks in at very low level and in fact if they had been adjusted for inflation since the last adjustment in July 2018, it would now be $51,800.

Both parties promising to raise the threshold to $50,000 in three years’ time is frankly a little off in my view. It just compounds the problem these families at the lower end of the income scale face with what we call high effective marginal tax rates because of the abatement level of 27 cents per dollar above the $42,700 threshold. This issue isn’t being addressed but instead the can has been kicked down the road.

But on the other hand, there is the proposed FamilyBoost childcare tax credit, which is worth up to $150 per fortnight for couples with childcare costs. This will be no doubt welcome, but the trade-off is the loss of the proposed extension of the Early Childhood Education subsidy that Labour included in its May Budget.

All good but how are you paying it?

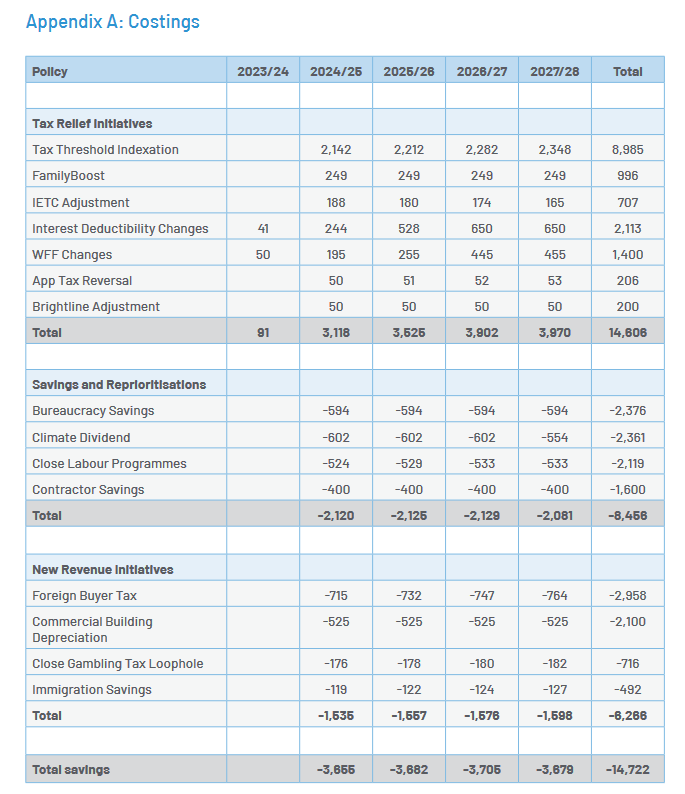

In fact, the controversy around National’s plan has broken out over how it’s going to fund this program and of these proposed tax adjustments. There are several surprises here, the first of which was this proposed foreign buyer tax. Currently no one who does not have permanent residency can buy property. National are proposing to keep that in place for properties worth less than $2 million, but to allow properties worth more than $2 million to be purchased. But that would be subject to a 15% tax, which sounds a bit like a stamp duty. We haven’t had stamp duty, by the way, since 1999.

The controversy is around the numbers involved, which do seem very optimistic. Revenue of $700 million a year would imply sales of at least $6 billion in property. I’ve seen a report in the New Zealand Herald which suggests that actually something like 60 to $65 million is more reasonable. But the proposal also runs up against questions that certain of our double tax treaties and trade agreements have clauses that would not allow such a clause to be a tax to be introduced, notably Singapore and Australia.

But now it’s been pointed out that what we call non-discrimination clauses in double tax agreements may apply to this. In which case these income assumptions of tax revenue would be well short.

There is a proposal to close an online casino gambling tax loophole as its described. This would require offshore operators to pay GST and register and report their earnings for tax purposes. The suggested penalty for non-compliance would be IP geo blocking of services. It subsequently emerged that the Government got $38 million in online GST for the year ended 31st March 2023. This is a result of the so-called “Netflix Tax” which, ironically, was introduced by the National Government in 2016.

National assume the measure will raise $180 million, and I admit I raised my eyebrows when I saw that suggestion. This seemed high to me particularly when I considered that the proposed DST I mentioned earlier is expected to raise about $55 million a year. Online gambling would seem to be a similar type of activity, if not quite identical, so assuming they’re going to raise 2 to 3 times as much as a DST struck me as optimistic.

National Party documents seem to be saying this is essentially a corporate income tax. In which case, it appears this particular tax could also be caught by the anti-discrimination articles in double tax agreements. And that could mean a $140 million shortfall in National’s projections.

Good news for singletons…ironically

On the other hand I do think the proposal to increase the Independent Earner Tax Credit threshold to $70,000 from its current $48,000 is a good initiative. I’ll be honest, I was a bit surprised that Labour didn’t think to do something similar as part of its budget earlier this year. But there is actually a little bit of an irony in that this Independent Earner Tax Credit was actually going to be abolished by National under the last budget it published in May 2017. But that measure never went through because of the change of government later that year.

A counter-productive proposal and more irony

But I think one of the measures that should attract more controversy, is the proposal to remove depreciation for commercial property which includes factories. Now this is something that Labour have also proposed to pay for the proposed removal of GST on fresh and frozen fruit and vegetables.

This is a counterproductive move in my view. The proposal refers to “commercial building” but the depreciation deduction covers all sorts of property such as factories, farming sheds etc. These all depreciate. It was recognised by the last tax working group, that depreciation on commercial and industrial buildings should really be re-introduced, introduced and is actually quite common around the world.

A measure that takes it away seems to be counterproductive particularly if we’re talking about encouraging investment in productive assets. There’s also the added irony that this would be the second time that a National government had removed that depreciation to pay for tax cuts.

Overall there’s an awful lot to pick apart here and the devil is always in the detail. This does seem to point to the revenue forecasts being on the optimistic side, certainly in relation to the foreign buyer online gambling taxes.

Good news for landlords…mostly?

On the other hand, there was also no surprise about the reintroduction of interest deductibility for residential properties. But what is interesting about this move is that’s it’s not simply being fully restored as of a change of government. What’s proposed is for it to be brought back in over a two-year period from 1st April 2024. At present the proportion which would become non-deductible is due to rise to 75%. Instead it will stay at 50% non-deductible and then starting 1 April 2025 the non-deductible proportion will year drop down to 25% before becoming fully deductible with effect from 1st April 2026.

Reducing the bright-line test back down to two years will be welcome for a lot of people. The unintended consequences arising from the extension of the period to first five and then ten years were giving me and plenty of other advisors a lot of work as we try to unpick where the boundary was, and what transactions were caught. So that’s probably quite welcome.

On the other hand, there’s a surprise that nothing has been said about allowing losses from residential property investment (“loss ring-fencing”) to again be offset against other income. This hasn’t been allowed since 2019. It also appears that the proposed increase in the trustee tax rate to 39% will still go ahead. I had heard whispers to that effect, and although there’s been plenty of pushback on the proposed increase it will be interesting to see what eventually emerges.

Now about those Tax Principles…

Having just got a new Tax Principles Reporting Act in place, it is interesting to compare the principles set out in there against these policies. You’d have to say for now, not entirely a big pass. Indexing the thresholds is a reasonable measure, as I said, but that’s a minor point. The tax on foreign homebuyers probably could be said to be questionable in terms of equity. Why should one group of people suddenly get a far higher tax charge than other groups of people in reasonably similar circumstances.

The removal of depreciation for commercial and industrial buildings doesn’t seem to fit with the tax principles. And since we’re talking about things that wouldn’t pass that bill, I’d have to say removing GST on fresh and frozen fruit and vegetables wouldn’t pass muster either.

Sucks to be a student…and an Auckland ratepayer?

But to summarise, tax is politics, so we can expect plenty of politicking. There’s no doubt that the tax relief in terms of the changes in the thresholds will be welcome, but there’s going to be quite a few losers as well. Following the announcement I spoke to a student radio station in Christchurch who were wondering about the impact for students. The answer was not very much and if the proposal to remove the 50% discount on public transport goes ahead, students would be worse off as a consequence.

Auckland ratepayers are also probably worse off with the proposed abolition of the Auckland Regional Fuel tax. Mayor Wayne Brown has already said that could mean a $2 billion funding shortfall. How is that gap going to be funded?

Overall National’s proposals are very much a sort of the Lord giveth and the Lord taketh. And where you sit on that spectrum depends on how well you end up. If you’re a landlord and high-income earner, and you don’t use public transport, you’ll be reasonably okay.

On the other hand, if you’re on lower incomes, perhaps receiving Working for Families income and you do use public transport, you’re going to be worse off. But this is politics, the electorate will decide in six weeks exactly which tax policy is fair.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.