Facebook and Google’s results indicate scale of BEPS issue

Is the just announced Government voluntary buyout of 700 unliveable homes a harbinger of things to come?

Last week when discussing the new tax bill, which includes the proposal to lift the trust income tax rate to 39%, I mentioned that Example 20 in the accompanying commentary had raised a number of concerns amongst tax agents and advisers. It seemed to be endorsing the option of trusts distributing income to beneficiaries with lower tax rates, leaving us all wondering, is that really correct?

It transpires Inland Revenue picked up on those concerns and then released the following statement.

“We are also aware that one of the examples used in the Bill commentary and factsheet has caused some confusion. The example noted that trustees could distribute income to a beneficiary, who may then decide to resettle it on the trust. We agree that there is some uncertainty under existing law about the tax treatment of such a settlement and we will be undertaking consultation on this. To avoid creating that doubt we have changed the example in those documents.”

The accompanying commentary has been updated and re-released. This shows the area is not as cut and dried as people might imagine. Obviously, Inland Revenue and advisers alike would like to have as much certainty as possible. So, it’s good that Inland Revenue picked up on this issue. But you do wonder how it managed to slip into the commentary in the first place without someone realising it might actually be a bit of an issue.

Rate misalignment problem solved? Not quite

Separately another advisor (Aman Chand of Bentleys Chartered Accountants) has picked up an interesting comment in the Regulatory Impact Statements (“RIAs”) which are issued alongside new legislation. RIAs discuss the purpose of this legislation, the alternative options and which one was chosen and why.

The issue the increase in the trustee tax rate to 39% addresses is one of rate misalignment between trustee income being taxed at 33% and individual personal income being taxed at a top rate of 39%. This issue was well understood at the time of the introduction of the reintroduction of the 39% tax rate in 2021. In fact, Inland Revenue and Treasury both said the trustee rate should rise to 39% at the same time. And now that’s what’s happening.

But for some time, there’s also been a rate misalignment between the corporate tax rate of 28%, the portfolio investment entity (“PIE”) rate, which is also 28%, and the then top individual personal rate of 33%. Inland Revenue had been looking at this for some time and had noted that there was starting to be a steady accumulation of undistributed income in companies. This rate misalignment issue was something that had been on its radar which it had started to make moves towards addressing.

What Aman spotted is that the RIA on the increase in the trustee rate does discuss this existing misalignment issue. The RIA notes Ministers have decided to progress increasing the trustee tax rate to 39% “while considering PIE and company shareholder misalignment issues on a longer timeframe”. Even if the trustee tax rate is aligned to the top personal tax rate, there will continue to be opportunities to circumvent that rate by substituting trusts with companies or PIEs. This is something that is going is obviously has been on the Inland Revenue’s radar and will remain so.

And even if there’s a change of government following the election in October as a result of which the top rate, 39% rate will no longer apply, the issue of a current rate misalignment between 28 and 33%, assuming that remains the top personal tax rate, will remain. Inland Revenue is working on this, and the RIA has some interesting details about potential options.

Don’t be banking on a change of Government

Accordingly, people hanging their hat on a change of government to defer this particular issue of a trustee income tax rate increase to 39% should still be aware that it’s likely that Inland Revenue may well introduce or recommend the introduction of other type of tax avoidance rules to tackle rate misalignment in the future. The issue is on their radar, and it still may well be something we will encounter regardless of whoever forms the government after the election.

Facebook, Google and BEPS

Last week I mentioned Facebook. New Zealand had released its results for the year ended 31st December 2022. And coincidentally last week we also covered the Government’s proposals for the global anti base erosion rules, the Pillar two proposals which are designed to help tackle the issue of base erosion and profit shifting (BEPS), where the New Zealand tax base is being eroded by profits shifting out of here to lower tax jurisdictions.

Facebook reported gross advertising revenue of over $154 million, but its net profit before tax was $3.3 million. And that’s because over $149 million was paid to a related company Meta Platform Ireland Ltd for the purchase of services during the year. Ireland’s corporate income tax rate is 12.5%, compared with ours at 28%. Withholding tax may be applied to some of these payments if they are treated as royalties, but you still have an idea of the scale of the issue.

It so happens that last Friday, after we recorded the podcast, Google New Zealand released its results for the year ended 31st December 2022. And in this case, it paid over $870 million in service fees to offshore affiliates. Mostly, it appears to the Singapore based Google Asia Pacific Pte Ltd. You shouldn’t be surprised to hear Singapore has a preferential tax regime. Incidentally, MasterCard and Visa New Zealand appear to route their payments through Singapore.

To put everything in context about the scale of the issue being faced by ourselves and other countries, if you look at Facebook and Google New Zealand’s 2022 results they paid more than $1 billion in service fees to overseas affiliates for the year. In theory, at a corporate income tax rate of 28%, that represents over $319 million in potential tax.

So, the Government and other governments are keen to see Pillar Two and Pillar One hopefully come into play and deal with this issue of tax and profit shifting. But as the commentary to the bill which introduced the Pillar Two legislation notes the benefit is likely to be about $40 million annually.

The impact of the GloBE rules is therefore not terribly significant. The issue of profit shifting still remains. It will always be there, by the way, because it is only appropriate that the tech companies charge for the use of their valuable IP in New Zealand. So, it’s not a question of we’re just going to disallow $1.1 billion of deductions and bingo, we’ve got $319 million. That is never going to happen.

But the difficulty with transfer pricing is really determining the value on that and just how much of it can be kept in New Zealand. And that’s going to be an ongoing struggle, whether or not Pillar One and Pillar Two actually proceed.

Cheque please

Finally, this week the government announced that in the wake of Cyclone Gabrielle, 700 homes around the country are considered unlivable.

And so homeowners will be offered a voluntary buyout through a funding arrangement between the Government and councils. Apparently, another 10,000 homes will require investment in flood mitigation around them so they can be protected when the next severe weather event hits. Note the word “when”, I think we are now in the midst of climate change.

I mention this because it reinforces the point we’ve been hammering away at for some time. Climate change is here and it’s going to have an impact on homeowners all around the country. It doesn’t differentiate between suburbs. The likelihood is that we are going to have to start thinking seriously in some cases about managed retreat, that there will be more and more houses that are unlivable. The insurers are already pricing it in, so some houses may become uninsurable over time.

The question really coming to the forefront now is who’s going to pay for this buyout and managed retreat? Councils, for example, may have allowed properties to be built in areas where they should not have been built. Auckland Mayor Wayne Browne has already spoken about this. By the way 400 of those 700 unlivable properties are in the Auckland region.

At a time when next year’s Auckland Council budget is going through a very controversial process, having to fund in some way the buyout of people from 400 properties at a time when the average price house price in Auckland is $1,000,000 is quite a significant hit to the bottom line even if the Government chips in.

This all reinforces what I’ve been saying for some time; the impact of climate change plus the demographic changes that are happening with the ageing population means that we really do have to think a lot harder about how much tax we are going to need. Either that, or what services we’re going to reduce. And the question of the taxation of capital is going to become ever more important. The politicians keep kicking it down the road, hoping it just will go away. It won’t.

The climate change bills are now starting to come in and will continue to mount. We will wait and watch to see who of the politicians in the main parties is going to grasp that nettle and say, “Hey, guys, this is this is the deal. If you want us to help you mitigate the impact of climate change, we have to spread the tax burden wider.”

In the meantime, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

One of the odd things about the budget process for me is that tax really doesn’t feature very much. In fact, I know some very experienced tax practitioners who don’t go to the Budget Lockup because of this. Most of the Budget and the accompanying analysis focuses on the exciting stuff – where the money being spent and the winners and losers from that funding. The source which provides most of that spending is almost an afterthought unless as in 2010 and again in 2017 tax cuts are a centre piece of the Budget mix.

In part, that’s because, unlike Australia and the United Kingdom, the legislation relating to various technical amendments to the Taxes Act is usually introduced separately. It was therefore a bit of a surprise last week when after the budget lockup period ended at 2 p.m., I discovered that there had been not one, but two tax bills published. Other than the announcement of the increase in the trustee tax rate to 39% the budget documents had not indicated there would be many significant measures.

In fact, as the bill’s title explains, The Taxation (Annual Rates for 2023–24, Multinational Tax, and Remedial Matters) Bill, it primarily relates to the introduction of the relevant legislation to support the OECD’s Pillar Two global minimum tax proposal. You may recall the Australian Budget two weeks ago included similar measures. It would have been surprising if we had not followed Australia’s lead although neither the Revenue Minister nor the Finance Minister made much reference to the proposals last week.

Introducing the global minimum tax rate

The intention behind Pillar Two is to impose a global minimum tax of 15% for all those multinationals with annual revenue exceeding €750 million, these are the so-called global anti base erosion (“GloBE”) rules. The legislation and commentary include a heap of new tax acronyms including DIIR (Domestic Income Inclusion Rule), POPE (Partially Owned Parent Entity) and QDMTT (Qualified Domestic Minimum Top-up Tax), which a rather cynical overseas tax advisor has suggested should be pronounced Q-Dammit.

The commentary to the tax bill explains the legislation will only take effect once a “critical mass of countries” has adopted the GloBE rules. This is thought to be “very likely, though is not certain”. If that critical mass is reached, then the rules will be phased in starting from 1 January 2024.

Assuming Pillar Two does proceed then how much will it raise? Not much. According to the Regulatory Impact Statement (RIS) released with the tax bill the GloBE proposals should be worth $25 million annually with another $16 million coming from taxes on amounts which would have otherwise been shifted to lower tax jurisdictions. The RIS explains this “modest amount” is because of a number of factors including that only 20-25 multinationals will be affected.

Now earlier this week. Facebook’s New Zealand’s accounts were public. And despite earning gross advertising revenue over $154 million its reported profit before tax was just $3.3 million, and it just ended up paying just over $1,000,000 in tax. That’s because it paid over $149 million for the purchase of services to a related company, Meta Platform Ireland Ltd. The GloBE rules are intended to counter this. But don’t expect that they will raise significant sums of money.

Raising the Trustee tax rate to 39%

The headline measure and tax measure in the budget was the proposed increase in the trustee tax rate to 39%, with effect from 1st April next year. Now, this is a conceptually logical move, and as noted last week was one that both Treasury and Inland Revenue recommended should have happened when the personal income tax rate was increased to 39% on 1st April 2021.

The commentary for the tax bill provides some more detail around the introduction of the measure, and a couple of points stand out. One of Inland Revenue’s examples appears to suggest that it would not automatically see allocation of beneficiary income by a trust to someone whose tax rate was below 39% as constituting tax avoidance. At least this appears to be implication from example 20 in the commentary, and that’s caused a few comments from other tax advisers as to whether Inland Revenue is signing off on tax avoidance.

Example 20: Mitigating over-taxation

Amy (an air traffic controller) and Anthony (a builder with his own company) have settled some income-generating assets on a discretionary family trust for the benefit of themselves, their children (both minors under the age of 16) and future grandchildren. Amy, Anthony and their accountant are the trustees.

2024–25 income year

Anthony has personal income of $70,000 and Amy has personal income of $180,000. Their trust has income of $40,000.

If the income is retained as trustee income, it will be taxed at the proposed 39% trustee tax rate. Any income allocated to their children as beneficiary income will also be taxed at 39% under the minor beneficiary rule.

However, by allocating the income to Anthony as beneficiary income, it can be taxed at his personal tax rate. This amount can be credited to Anthony’s current account, available to be called upon at any time, or he can settle it on the trust if he wishes to do so.

2025–26 income year

Barry, the older of Amy and Anthony’s children, has turned 16, so he is no longer a minor. Barry has no personal income. Anthony again has personal income of $70,000, and Amy has personal income of $180,000, while the trust has income of $50,000.

Since Bary is no longer a minor, he is not subject to the minor beneficiary rule. Income can be allocated to Barry as beneficiary income and taxed at his personal tax rate (for example, up to $14,000 at 10.5%, over $14,000 and up to $48,000 at 17.5%).

If the trustees do not want to distribute this income to Barry, it can be credited to his current account, available to be called upon at any time, or a sub-trust arrangement can be set up so that Barry’s interest in a portion of the trust assets is recognised and protected.

On the other hand the legislation specifically counters attempts to distribute income to certain corporate beneficiaries. The benefit here obviously being that instead of trustee income being taxed at 39% it would be taxed at the corporate income tax rate of 28%. The bill aims to negate potential distributions being made to closely controlled family companies.

The bill will not apply to deceased estates but only in respect of trustee income derived within 12 months of the deceased persons date of death. Based on personal experience and discussions with lawyers that 12-month period is too short, 18 to 24 months seems more appropriate

There is also an exemption for disabled beneficiary trusts which are defined as having only one beneficiary other than any residual beneficiaries who may benefit on the death of the disabled person. Critically the trustee must not allow any further beneficiaries apart from residual beneficiaries to be added. I expect that this may mean a number of existing trusts may have to be amended or be re-settled in order to comply.

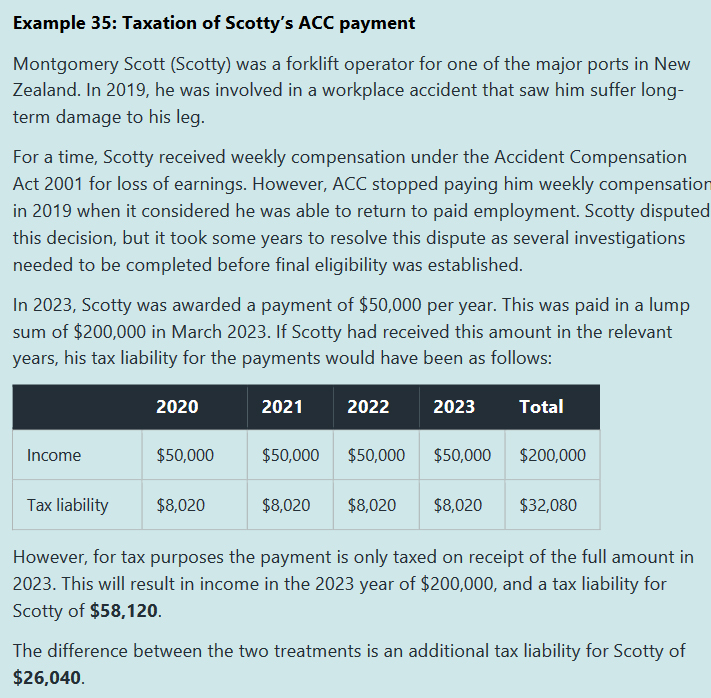

A end to over-taxation of ACC lump sums

Moving on and some good news. I’ve previously covered the situation where Accident Claims Compensation Corporation has paid a backdated lump sum, representing several years compensation after the claim was initially denied before being accepted on appeal. Now, as I was explained in the past, such payments often result in over taxation relative to the tax that would have been payable if the payments had been made at the correct time. The commentary gives an example of this where the claimant would have an additional tax liability of $26,040 as a result.

The Bill proposes to change this by allowing a tax rate to be used when a backdated lump sum payment is paid to be based on the recipient’s average tax rate for the four years prior to the tax year in which they receive the backdated lump sum payment.

There will also be provisions relating to lump sum payments made paid by the Ministry of Social Developments and those will eliminate any potential further tax liability for recipients.

According to the accompanying regulatory impact statement, the effect of this over taxation is roughly about $9 million a year. This is great news, and one I’m personally pleased about because I’ve been lobbying in the background for Inland Revenue for some time to make this change.

These new rules will take effect from 1st April 2024. Personally, I’d like to see them in effect, from 1st April this year, and I’ll submit on that. But don’t hold your breath on that one.

There’s a number of other measures in the bill, including a proposal for the Government to pay a 3% KiwiSaver contribution on the amount of paid parental leave received by a KiwiSaver member. The this will be made providing the recipient also pays the 3% employee contribution. The idea is to help increase the KiwiSaver balances of paid parental leave recipients, many of whom are women and whose ability to save has been disrupted because they take time out of the workforce to raise children. This is a welcome measure.

As usual there’s a whole heap of technical amendments as well. Submissions on the Bill are now open and the closing date is 30th of June.

A taxation principles bill – putting the politics into tax?

Now, the other bill, which was a big surprise, was the Taxation Principles Reporting Bill. This bill is intended to “increase the public’s understanding of the tax system and promote informed debate and discussion about its future”. The Bill does this by proposing a set of generally accepted tax principles and then requires the Commissioner of Inland Revenue to report on how the tax system is tracking against those principles.

The idea is that “regular reporting will help the public better understand how our tax system is performing and over time, informed public consultation process on tax policy proposals.” The hope is tax policy is developed in line with “values which society considers desirable in a tax system.”

The tax principles set out in the bill such as horizontal and vertical equity efficiency, revenue, integrity, certainty and predictability, flexibility and adaptability and compliance and administration costs, are all well accepted principles, and they’ve been used in various tax reviews, both here and abroad.

There’s a framework by which Inland Revenue will be reporting annually then every three years it will provide a more thorough review. And the implication would appear to be that the Inland Revenue would be expected to be doing regular surveys of the type that just was carried out on the high wealth individuals. That at least is one interpretation of these reviews.

The Bill will take effect from 1st July this year, which means that there’s going to be little time for consultation. In fact, the closing date submissions will be 9th June, just two weeks ahead. This is an incredibly political bill – is it a harbinger of a wealth tax, capital gains tax, whatever? We shall see. It will be interesting to see how this plays out and of course, its future will be very dependent on the Election.

In the meantime, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

an increase in the trustee rate but no action, yet, on tax rates and thresholds

The big tax surprise in the Budget is that there is no tax surprise. Surprisingly, well to me at least, the Government included no changes to income tax and other thresholds and there is little indication of any such changes ahead in the Budget documents.

The destruction wrought by the January floods and Cyclone Gabrielle may have interrupted plans for such changes. Of course, the Government could be keeping its powder dry for the coming election campaign. No doubt we will find out when the campaigning begins in earnest.

On the other hand, the increase in the trustee tax rate to 39% with effect from 1 April 2024 should not have come as a surprise. Inland Revenue recommended the trustee rate should also be increased to 39% when the top personal income tax rate of 39% was introduced in 2021. It was only a matter of time before the trustee rate rose and the publication of Inland Revenue’s High Wealth Individual Research Project provided a clear opportunity for the Government to do so.

In the accompanying press release announcing the measure Minister of Revenue David Parker noted that new Inland Revenue information shows a near 50% increase in trust income taxable at the trustee rate from $11.4 billion in the 2020 tax year to $17.1 billion in the 2021 tax year. The top 5% of trusts with taxable income accounted for $13.3 billion or 78% of all trustee income in the 2021 tax year.

As a tax policy measure, it is logical and is expected to raise $350 million annually. (There will be some exemptions for disabled and deceased estates).

I expected an announcement about the OECD’s Base Erosion and Profit Shifting international tax rules similar to the initiatives included in last week’s Australian Budget. There was no such move although the forecasted tax revenue for the June 2027 includes an estimate of $25 million as the initiative takes effect. Asked about this in the Budget Lockup, Grant Robertson specifically ruled out a Digital Services Tax.

Nor did we see any moves for increased or targeted depreciation measures as was also in the Australian Budget, although the new 20% rebate for game development studios matches an Australian measure. The gaming industry is exactly the sort of low-emissions, high wage, high growth export industry we need, so the move is welcome.

Looking at the numbers, tax revenue is projected to rise from $114.6 billion for the June 2023 year to $122.6 billion for the June 2024 year. About a billion dollars of the increase is the effect of fiscal drag where wage rises crossing tax thresholds mean higher average taxes for earners. Resident Withholding Tax on interest has almost doubled to an expected $1,659 million for the current year to June 2023, a direct effect of the dramatic increase in interest rates over the past year. Proof, perhaps, that every interest rate rise cloud has a silver lining, for the Government at least.

There are a few interesting snippets from digging through the Vote Revenue Estimates of Appropriations. Last year’s Cost of Living payments were budgeted as costing $706 million, but according to the Appropriations the final cost was $50 million lower at $656 million.

Inland Revenue’s funding appropriation for June 2024 shows a $23.2 million or over 20% boost from $110.6 million to $133.8 million for its investigation, audit and litigation activities. Debt management gets a significant increase too, although the provisions for impairment and debt write off totalling $931 are actually down from the estimated $985 million for the current year.

Overall, from a tax perspective this was a surprisingly quiet Budget especially considering it’s an election year. Grant Robertson was quick to brush off questions about electioneering but on the tax front at least I think we can expect to see more in the coming months. The debate over tax rates, tax thresholds and capital gains taxes are all to come.

In my view, the leaky building saga is an underappreciated factor in how our housing market got so expensive. At a time when population growth was accelerating, builders and resources had to be diverted to remediation work on buildings, many of which were fewer than 10 years old. These are expensive and time-consuming processes for all involved, and a major question has always been are these costs tax deductible where the building being remediated is being used for deriving rental income?

Inland Revenue doesn’t have a specific measure dealing with leaky buildings, but instead it’s covered in the general analysis under Interpretation Statement IS12/03 Income tax deductibility of repairs and maintenance expenditure general principles. Generally speaking, each case is really looked at on its merits.

That’s what makes a Technical Decision Summaryfrom the Inland Revenue’s Adjudication Unit released this week quite interesting.

The background is that the taxpayer owned a rental property which was part of a block of six units. This block of six was a freestanding building within a larger complex. Units within the block were connected by inter-tenancy walls. The block was largely clad with monolithic cladding but required remediation work to resolve weather tightness issues.

The work was carried out by the body corporate, and they levied special levies payable by each unit holder calculated by reference to their expected portion of the total expenditure. While the remediation work was being done, the unit was unoccupied, so the taxpayer independently organised for internal painting to be done during that time.

The question was whether this expenditure was deductible. The taxpayer, not unreasonably, claimed the levies were repairs and maintenance, as were the separate costs he paid for painting the unit. Inland Revenue didn’t agree, and the dispute finished up before Inland Revenue’s Adjudication Unit. It determined the levies paid for the remediation were capital, however, the painting was deductible.

The Technical Decision Summary has a good analysis of how Inland Revenue goes through the process of determining whether the expenditure is capital or deductible. This analysis is based on the Privy Council decision in the Australian case of BP Australia Limited v Commissioner of Taxation. Based on that case there are three key elements:

Whether the work done resulted in the reconstruction, replacement, or renewal of the asset, or substantially the whole of the asset.

Whether the work done had the effect of changing the character of the asset.

Whether the work was part of one overall project or was a series of projects that merely happened to be undertaken at the same time.

Whether the work was part of one overall project or was a series of projects that merely happened to be undertaken at the same time.

Overlaying that case is another Privy Council case, this time involving Auckland Gas from 1999, which suggests a two-stage process to determine whether the expenditure is of a revenue or capital nature. You first identify the asset being repaired and then analyse the nature and extent of that work.

In relation to the painting, the Adjudication Unit considered it wasn’t part of the overall repair project for the block of units, and it was therefore considered separately. Ultimately, they concluded it was a repair and deductible.

As for the remediation work, this is quite interesting because they saw that it was a block of six units all under repair. But there’s also a discussion about whether the fact that several other blocks in in the complex also required remediation work, whether the complex should be seen as the total asset. They discounted this in the end because although the units within each block were physically connected to each other, the blocks were not. Therefore, the block of six units represented an asset, but the complex of blocks overall did not.

This case, I think, might go further because over here the Adjudication Unit said although there was extensive work done the remediation did not result in the reconstruction, replacement or renewal of the block or substantially the whole of the block. The work was not so significant it could constitute reconstruction. However, they did consider the scale of the work was such that it changed the character of the block, because the cost of the remediation was high, around 20% of the value of the unit in the complex. (There are no numbers quoted in this TDS, they do that because of these are meant to be anonymous). And there were some significant improvements to the affected areas, and in the Adjudication Unit’s view, these were structurally significant and important to the operation of the asset.

There’s a comment here that in addition the remediation of the block was necessary to prevent water ingress and protect the overall structural integrity and income earning capacity of the unit in the rest of the block. My view on that would be that’s very true. But it’s also true of any building and buildings are built with that in mind. So, enabling it in the first place, or making sure that doesn’t happen, seems to me it’s more of a repair.

But I do wonder whether this might be taken further by the taxpayer. We shall see. Anyway, it’s a useful case. It’s good the way it runs through the principles involved. The taxpayer will not be entirely happy about that, I daresay, and my own view is the remediation issues around leaky buildings are one where erring on the side of deductibility would longer term be a good policy. But we are where we are at the moment, and we’ll just have to see what turns up in other decisions.

Moving on, last Tuesday night it was the Australian budget and that first of all produced a surprise. There was a small surplus, apparently the tax take was above expectations. The Australians are actually going to proceed with the so-called Stage Three, tax cuts package. This is controversial because they are weighted to benefit the top end earners above A$120,000.

From a New Zealand perspective looking at the Australian budget, there are a few interesting snippets in there. They’re going to give extra funding to boost skilled migration.

Part of this is they’re increasing the temporary skilled migration income threshold of A$70,000 and additional places for the so-called Pacific Australia Labour Mobility Scheme, for workers in priority sectors for the Pacific and Timor-Leste regions. I think that’s interesting because putting it in context, we’re not the only country looking for skilled migrants.

There’s a huge increase in rent assistance and I wonder whether we might see something in that. It’s the largest in nearly 30 years. And there’s also moves to encourage investments in build-to-rent projects. We’ve seen something similar to this because of our interest deductibility rules. The depreciation rate for build-to-rents has increased from 2.5% to 4% per annum. By contrast, residential buildings over here do not attract depreciation.

There’s also a measure to support small businesses, including what they call a small business instant write off. This enables small businesses with an annual turnover of less than $10 million Australian to be able to immediately deduct eligible assets, which cost less than $20,000 for a one-year period starting 1st July 2023. Now, that’s something that’s often called for here.

There’s a small business energy incentive, as well as more tax breaks to help small and medium businesses electrify and save on energy bills. And these target businesses with an annual turnover of less than $50 million. They get special depreciation claims.

Interestingly, a couple of things have happened in relation to international tax. More work on anti-avoidance is happening and they’re implementing a global and domestic minimum tax – the two pillars international tax solution.

Basically, from 1st January 2024 large Australian multinationals and the Australian operations of large foreign multinationals will pay an effective tax rate of at least 15%. And then from 1st January 2025, Australia will also be able to tax the foreign operations of large foreign multinationals that operate in Australia to ensure they’ve paid at least 15%. This is following through from the international measure.

Then there’s changes around tax breaks for the superannuation scheme system. This is something I’m seeing all around the world actually. Governments are looking at dialing back some of the generous tax relief they’ve given. In Australia from 1st July 2025, earnings on super funds balances exceeding $3 million will be taxed at 30%, whereas those earnings and balances below $3 million will continue to be taxed at the concessional 15% rate.

As always with the Australian budget, because they have a bigger economy and a more interventionist approach there’s a lot of little details where they’re happy to tinker around the edges with the tax system.

Budget predictions

Our Budget is this Thursday. Now generally speaking, there are typically very few tax measures in a budget. You could always rely on Bill English sneaking in a tax increasing measure normally in the form of non-indexation. But another example would be introducing superannuation withholding tax on KiwiSaver employer contributions from 1 April 2012.

On the other hand, Grant Robertson seems almost averse to mentioning the word tax. That said, because this government and the last National government have done nothing about tax thresholds since October 2010, there is a huge amount of pressure for something to happen in that space. Robertson’s problem is that he’s also trying to manage inflation, and reducing taxes isn’t generally seen as a positive inflation fighting move.

For all that, my guess is that we might see some action directed at lower income families. That might include some changes to thresholds especially for those earning around the $48,000 threshold. We might also see some changes in the Independent Earner Tax Credit and adjustments to the Working for Families thresholds and possibly abatement rates.

Businesses have long called for higher thresholds for instant write-offs as has just happened in Australia, but I don’t see that happening. There might be some Cyclone Gabrielle related reliefs, perhaps an extension of the Small Business Cash-Flow scheme or a temporary reinstatement of the ability to carry back tax losses to earlier years.

Whatever, I sense it is going to be a more interesting budget than usual. And as usual, we will be in the Budget lockup, and you’ll have our views on it soon after 2 p.m. this Thursday.

In the meantime, I’m Terry Baucher and you can find this podcast on my website or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

At the end of last week, the Government announced a surprise tax measure for North Island businesses hit by recent flood damage. The measure means that they will not have to pay tax on insurance or compensation they might receive for any damaged buildings or plant or equipment.

As the Revenue Minister David Parker pointed out, generally speaking such payments are treated as taxable income. Recognising another tax bill is the last thing any businesses affected by the floods needs, the Government has decided to adopt a measure which was used previously following the Canterbury earthquakes and the Hurunui-Kaikoura earthquakes. It essentially allows a deferral of the tax on the compensation payments received to replace damaged or lost buildings and plants and equipment.

What happens is instead of a depreciation recovery (income) happening because you’ve received a payout, there’s a rollover relief which will defer the recognition of that income on the basis that there is a commitment to rebuild or replace the destroyed buildings or plant. There is a key difference here as to the measures used previously for the earthquakes, and that is there is no requirement for any replacement buildings to be located in the same region. This is because in some cases managed retreat is now being considered. For example, where a building which is in the Hawkes Bay has been destroyed or severely damaged by Cyclone Gabrielle, the business owner may decide to relocate to a different region. In this case the rollover relief would apply an exemption.

This is a good measure to see. The formal legislation will be introduced shortly probably around the time of the Budget, I might imagine, along with the other budget measures.

What happens if you rent a room to a flatmate?

Moving on, Inland Revenue has released an interesting draft Questions We’ve Been Asked consultation on how the bright-line test might apply to where a person rents out a room in their home to a flatmate. Alongside that there’s another Draft Questions We’ve Been Asked relating to the extent to which a person can claim deductions for expenditure incurred in deriving the rental income, when they’ve rented a room to in their home to a flatmate.

As always, there’s a bit of detail in these, but in summary, in relation to claiming deductions or costs incurred in renting a room out to a flatmate, the draft consultation concludes that deductions can be claimed to the extent that they’re incurred in deriving gross income. The rental income will be assessable and the amount of expenditure needs to be apportioned between private use living in the house and income earning use, rental income from a flatmate.

The draft consultation suggests that apportionment, based on the use of physical space, is a reasonable basis on which to determine what represents an income earning component of expenditure and therefore calculating the deduction available.

Interestingly, the interest limitation rule will not apply, if the land is used predominantly for the person’s main home. Similarly the residential ring fencing rule won’t apply if more than 50% of the land is used for most of the income made by the person as their main home.

The general rule here is that it’s a matter of fact, whether the dwelling is the person’s main home. You must consider all the circumstances. But the fact that you are renting out a room in, in your home to a flatmate while you are living there will not preclude the home being the person’s main home. And on that basis, the interest limitation and residential ring-fencing rules should not apply.

Which leads on to the second question as to whether then the bright-line test might apply. If so, would a person who is living in a home and rents out a room to a flatmate, qualify for the main home exclusion.

This draft consultation concludes that, yes, that person should qualify for the main home exclusion. Again, whether it’s a home is a matter of fact, and you consider where the person resides and has a fixed presence. Just a reminder, though, that there is a slight twist in for land acquired between 29th March 2018 and 26th March 2021. The main home exclusion applies where for most of the days in that bright-line period, the land is mainly used as a residence by the person.

But there may be situations where that in fact is actually incidental to the main purpose of carrying on rental activity. I think one of the questions there would be if you are starting to rent out more than one room if say there are four bedrooms and you’re renting three out. The question might then start to arise as to whether the main home exemption would be available. Anyway, it’s good to see some guidance on this as this question no doubt is going to pop up from time to time.

It’s provisional tax payment time

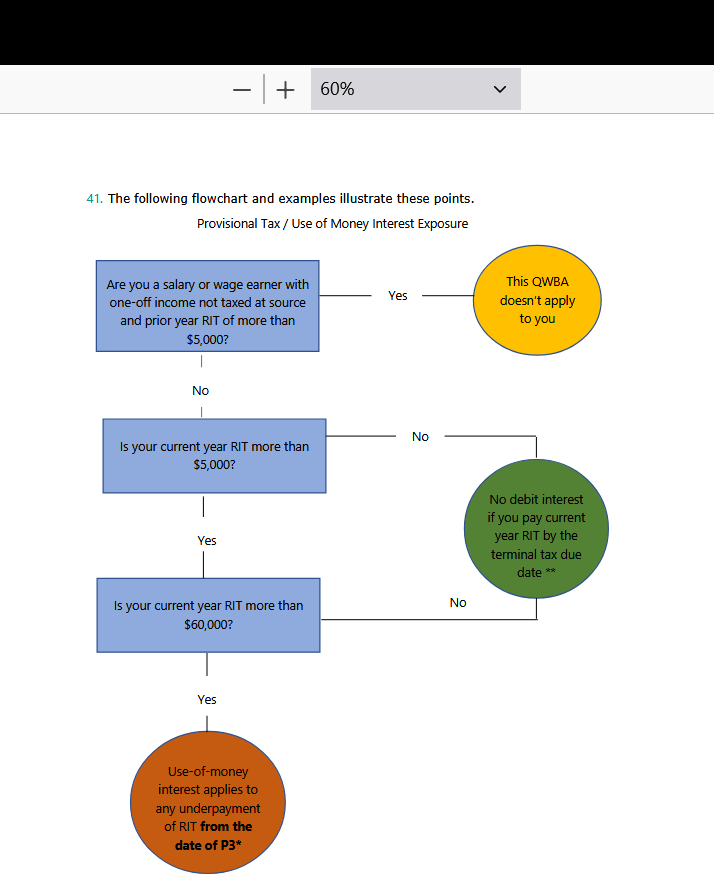

Monday is the due date for payment of the final instalment of Provisional tax for the March 2023 income year. The key thing to keep in mind here is if you think your residual income tax for the year to 31st March 2023 is going to exceed $60,000, then you need to make the full payment on Monday. Otherwise, use of money interest will apply on the unpaid provisional tax.

Incidentally, the interest rate on tax paid late rises to 10.39% with effect from Tuesday. Also, bear in mind, in some cases, you may also face late payment penalties, an initial 1% on the tax paid late. And then if it’s not paid in full within seven days, a further 4% is levied. Use of money interest continues to apply on top of these penalties. So, paying your tax late is an expensive proposition.

I’ve been dealing with Provisional tax for almost 30 years now, and it’s still something that confuses me from time to time. But the key point to always keep in mind about the latest iterations of these rules is that if your residual income tax is going to exceed $60,000 for a tax year then you need to pay the liability in full on the third provisional instalment date.

Not self-employed? You might still have to pay provisional tax

Usefully, Inland Revenue have released a Question We’ve Been Asked QB 23/05 on the impact of provisional tax for salary and wage earners who receive a one-off amount of income without tax deducted.

For example, this sort of income could be the gain from the exercise of shares granted under an employee share scheme, or from the transfer of a pension from overseas or a gain from a sale subject to tax under the bright-line test.

The general provisional tax rules are if your prior year residual income tax was less than $5,000, then this question you’ve been asked doesn’t apply. However, if it it’s more than $5,000, then you will be liable to pay terminal tax. No interest will run on that tax if it’s paid by the terminal tax due date, which is typically the 7th February following the end of the tax year for those without a tax agent, or the following 7th April for those with a tax agent.

As always in tax there’s a but, and the big but is what I mentioned a few minutes ago. What happens if your residual income tax exceeds more than $60,000? Then use of money interest at 10.39% will apply to any underpayment from the date of the third instalment, typically 7th May.

This is a really critical point if you have an untaxed gain such as those I mentioned, a gain under the bright-line test, transfer of a foreign superannuation scheme or as a result of exercising shares under an employee share scheme, and your tax liability exceeds $60,000, then you’re into the provisional tax payment regime straightaway and you have pay the tax in full on the third instalment date, typically 7th May, or this year, Monday 8th May.

Provisional tax does trip up a lot of people and but generally speaking, unless you’ve made a big gain, in which case you probably should have the funds available (or at least I’d hope so), you’ve got until the terminal tax date to meet those requirements.

One thing you need to do, by the way, if you are a salary earner and you have realised one of these untaxed gains, you should notify Inland Revenue as soon as possible before it starts its auto calculation assessment process. Otherwise, what might happen then is that they calculate you may be due a refund. They will make that refund and then you will have to repay the refund and the correct amount of provisional tax.

More feedback on taxing wealth

And finally, the controversy continues to around the Inland Revenue High Wealth Individual Research Project and the various related reports such as the Sapere report. There’s some fairly interesting commentary flying around on the topic. I thought Damien Venuto in the New Zealand Herald was on point when he said whether we like it or not, there is a reckoning coming around how we deal with tax.

The DomPost has an article by Susan Edmunds, which wasn’t online at the time of the podcast, talking about what was happening here and getting the views of Robyn Walker of Deloitte. Previous podcast guest John Cantin, as always, has some very insightful commentary. I think John makes an interesting comment about how the Sapere report and some other commentary brings in the question of benefits paid to taxpayers to provide an overall economic view. And he thinks that rather confuses the matter.

We don’t tax unrealised gains? Think again.

I want to repeat a point I made last week in the podcast and on RNZ’s The Panel. We currently do tax unrealised gains. The Foreign Investment Fund regime is the very best example of that. The taxation of pension transfers is another. When someone transfers an overseas pension to New Zealand, they’re not always realising it. In some cases, people are taxed on the value of the pension transfer but they can’t access it until they reach age 55. So that’s not really a realised gain. There are the financial arrangements rules which tax unrealised foreign exchange gains and losses. Overseas, estate taxes in essence tax unrealised gains. So, the concept is not unusual.

I remember looking at the various commentary reports from the 1980s and early 1990s when New Zealand was overhauling its tax system. There was a real debate going on around whether it was practical to have an accrual-based capital gains system. Wisely, the reports concluded that much as that might be economically accurate, it simply was practically impossible. Wealth taxes, quasi do that in a way, but a capital gains tax on an unrealised basis is, to all intents and purposes, a non-starter.

So, the debate will continue, and we’ll see a lot of politicking around that. Like Damien Venuto I’d like to see some hard answers on this from politicians about how they are going to address the issues of demography, demographic change and climate change.

And on that bombshell, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week I’m joined by Shamubeel Eaqub, a partner at the boutique economic consultancy Sense Partners.

Shamubeel is a regular commentator on economics and is the author of several books including Generation Rent.

Terry Baucher (TB): Kia ora Shamubeel, welcome to the podcast. It’s been an interesting week, we’ve had three major reports on the true tax rate paid by the wealthy on their economic income. What have you made of all this? Are we any the wiser after these three reports?

Shamubeel Eaqub(SE): I think we are much wiser. I think we’ve all always suspected that the rich were not required to pay tax on a lot of their incomes. But we didn’t know how much income or how much wealth there was. So, the report by IRD in particular, I think was really useful to get a much better understanding of the survey of high wealth individuals and families. Just how rich they were and just how much income they were earning from wealth alone. The report that came out the previous week from Sapere and OliverShaw Consulting I think was really poor.

I think the official report laid bare those conjectures and I think fairly largely lobbying efforts that was done in the Sapere report.

(TB): Yes, the Sapere report was something, I’ve described it elsewhere as fairly indigestible. You had the complete difference in the conclusions the Sapere report reached that broadly speaking the wealthy were paying a fair amount of tax in line with middle income New Zealand. By contrast the reports from Treasury and Inland Revenue which show a completely different picture, with Inland Revenue concluding the median income tax rate on economic income was 8.9%, I think that raised a lot of eyebrows.

SE: It did. I mean the reports from Inland Revenue and Treasury didn’t show that the rich are not paying tax on the income that is taxable. What it showed was our tax system simply does not ask rich people to pay tax on the income that they earn. Most of the income earned, of course, is from capital. Wealth begets wealth and that huge amount of income, almost all of the income comes from that. You know, the wealthy becoming wealthier and they’re not paying tax on it because we don’t ask them to.

I think there was a sort of misconception that somehow the wealthy are sneaking around and not paying tax on what’s required of them. Although we suspect that they might do that as well. This report wasn’t really about that. But, you know, tax minimisation is a thing. There’s a whole profession that’s out there to help rich people do it very well, people like you, Terry. And then there was the other bit, which is, I think, a bigger and more pertinent question, which is “What counts as taxable income, and should that be taxed?”

TB: Yes, and that’s at the heart of this whole thing. It’s not controversial to be looking at the question of the distinction between economic income and taxable income, because I’ve seen other jurisdictions consider the same issues. On Wednesday, I was on Radio New Zealand’s The Panel. A panelist argued bringing in economic income into the equation isn’t right, because it’s not taxed and we’re also talking about gains not realised. But as you know, we do tax certain instruments on an unrealised basis. But broadly speaking, there is no controversy about looking at the economic value to determine what is a fair or what is a true rate of tax.

SE: There isn’t. And I think the norms will change over time as well. And at a particular point in time, income taxes were thought to be ridiculous, but they’re now the norm. There is nothing to say that there is no one form of income or wealth or a taxable base that we can’t tax. To me, it feels a little bit strange to think that just because we’ve got a system now, which defines taxable income as a particular way, that’s the only thing that we can possibly tax. That’s not true, as you know, when it comes to, for example, things like foreign shares, we have a foreign shares deemed rate of return regime, and that actually works pretty well because it takes a lot of the complexity away and you pay tax on the return that you’re likely to make on the asset that you have invested overseas.

We do tax [unrealised gains] already, it’s not like we don’t. We also do it on things like rates, which is calculated by reference to the value of our houses. So, it’s not like there is any reason why we should think that there can be no connection between wealth or the income earned and wealth. This whole thing that somehow it’s terrible we’re taxing unrealised wealth. As if these are poor people and they can’t afford to pay a tiny amount of that wealth by selling some of those assets or borrowing money or deferring it to a future point. There are so many ways we could design a system that would work quite well.

But to me, these [arguments] are just distractions. But these distractions are going to be really coordinated and very powerful because you know what? There’s a lot of money on the line.

TB: Were there any surprises for you in the numbers that came out?

SE: No, it wasn’t surprising. I think for most New Zealanders, the surprise would be just how rich the rich are.

TB: Yes. I figured that we might see something around the 10% mark because we knew other overseas jurisdictions had seen that. There’s that White House report from America where they actually have a capital gains tax and an estate tax and a gift tax. And they still think that the true tax rate on the economic income of the top 400 families in America is 8.2%, which is quite astonishing, really. Again, it illustrates the effect of what we tax and what we don’t tax although, the American system is riddled with particular exemptions. I do think you’re right, the scale of the wealth at the top end of these 300 odd families being collectively worth about $85 billion, I think that did take a few by surprise.

SE: Yes. I mean, it’s an extraordinary sum of money. And, you know, that is well beyond the conception of what any normal New Zealander could hope to have. And I think quite often when you think about the proposition to people when it comes to tax policy, particularly any taxes on wealth, they think that one, their wealth is going to be targeted or two, they might one day become wealthy.

But we’re not talking about that. We’re talking about, you know, a scale of wealth that there is very little chance that any normal New Zealander will ever achieve that kind of wealth.

TB: Yes, you’d have to have bought thousands of Bitcoin back in 2010 to match some of the numbers we’ve seen here. What do you think about the fact the median age of the respondents was 67? I think that was a little older than I was expecting to see. What can we read into that?

SE: I think it shows people who have made it, who worked hard, got lucky because luck and hard work are the two things that are the key ingredients for becoming quite wealthy. And sometimes intergenerational as well. I think it shows there was a bunch of people who came through that period of the economic reforms which made some big winners and losers, and some of them did spectacularly well.

And we see that, right. We know we know some of these individuals who are out there in that kind of age group. They’re quite visible and well known. It doesn’t detract from all the work they might have done. It’s more that I think they lived through a period of time which created opportunities that were quite unusual.

TB: Is that a moral, do you think, then, going forward for all of us, just come back to your point a few minutes ago, that people say “Well, so-and-so has made X and we can as well.” Or are we different economy, different times?

SE: Well, I think we will mint new billionaires and multimillionaires over time. They will be the Rod Drurys, and the Peter Becks, as well as the Stephen Tindalls and other people.

So there are different ways and some people are at the right point at the right time with the right skills and all those bits that make that magic. But the reality is, in a country of five million people, not all five million of us will have that magic.

TB: Indeed.

SE: A vanishingly small number of us will ever have that. So, I don’t think it’s a model that’s replicable, per se. It’s, of course, nice to have that aspiration that we should try and improve ourselves. We should start businesses; we should try and do well. We should create jobs. But actually, for most of us, we’re not going to achieve and attain those kinds of numbers, that kind of wealth.

TB: Actually on wealth one of the things that I was intrigued to see Inland Revenue had looked at was the impact of inheritances. And this saw $411 million that had been transferred in what they call sizeable gifts, which is more than $25,000. But that was over a 50-year period, which isn’t terribly significant. I think that if memory serves right, half of that happened in the decade between 2010 and 2020.

What do you make of that? We’re not talking about old money being passed down from generation to generation, are we? Or maybe the money is still locked up in trusts. Did that surprise you? Because it was a surprise to me. I was expecting to see bigger numbers than actually popped up.

SE: Yes, I think there are now a lot of family offices for the truly wealthy families. It doesn’t make sense to give the money away. It’s much easier to keep it locked up because you get the economies of scale from running a family office, which gives you the ability to create even more wealth for future generations.

So, I wasn’t super surprised because there was no great incentive to dilute your wealth and to give that money away. I’m not really clear on what the definitions were in terms of those inheritances. Was it really money being gifted or was it the returns that are given to family members? There are lots of different ways that you could think about that. But my sense is that there is no great tax incentive for [the wealthy] to give the money away. There is no kind of reason for why you shouldn’t have the trusts and structures going on in perpetuity.

So was Thomas Piketty right?

TB: I see that Thomas Piketty has been quoted on Newshub about the report.

We know that Piketty is David Parker’s favourite economist or one of his favourites. Do you think this vindicates what Piketty has been saying?

SE: But I think it confirms what we know to be true, wealth begets wealth. To be very rich, it’s very helpful to begin by being very rich. And we also know that because of the way that our tax system is designed, it is designed for the many rather than for the few.

So, you know, inevitably you’re going to see the critique that this is the politics of envy and all that kind of stuff. But actually, when you jump back and ask the question ‘What is income and what should be taxed?’ it does take you away from that idea of envy. And actually, your income is very large and you’re not paying the same share as everybody else. Why is it that because you are wealthy, you are exempt from this income that you earning?

I think this was the core fundamental of the kinds of things that Piketty has been arguing for, why is this unearned income, this accident of birth? Why is it that you have some God given right to keep that protected from the rest of society? Why is it that that wealth, that income is not part of the wider taxation system in a society that you choose to participate in?

TB: I guess a response to that would be, well, we pay most of the tax anyway. It’s a small group, the numbers being pushed say the top 2% or 3% pay 26% of the tax. So the probable counter might be, ‘Well, we are paying enough anyway. We are paying our share.’ What would you say to that? Again, I guess it’s a question of how we define income, isn’t it?

SE: I think so. And I think, it’s also entirely possible to counter that with saying, ‘Well, if you also pay 20% like the rest of us, then, in fact, that future reality might be that all of us pay 15%.’

TB: The broad base, low-rate approach, broadening the base and lowering the rate. Yes.

SE Exactly. So, the alternative features are not just that they pay more. It might be that they pay more and the rest of us pay less. And again, this still goes back to the fundamental question of what is income and what we choose to define as taxable income.

And I think that’s really what came through that entire work. It wasn’t really about wealth. I mean, for me, it was really about asking the question of what do we actually consider to be income? And why is it that our tax system deliberately and specifically excludes some forms of income? Just because they happen to be the domain of the rich.

A ground-breaking report

TB: The report has been described as groundbreaking and not because of its methodologies, because those are fairly common. We were talking earlier that there seem to be three different methodologies and Treasury got down to nine different calculations of effective average tax rate, which I think was testing the patience of even the most dedicated of us.

What marks this report out as groundbreaking in my view, is we’ve actually got really good hard data, to work on for a change. And so it’ll be interesting to see how this plays out around the world.

SE: As you know, Terry, this is not new in the sense that there’s been other countries, particularly the US, where they’ve really kicked this off trying to find out what’s going on, because, you know, the domain of the very rich is quite opaque.

They can keep things opaque because they’re very rich and they have very good lawyers and very good accountants. And also, people are private because they don’t want people to know how much money they’ve got. But the groundbreaking nature of this study was very much that now we have real data based on an extraordinarily high rate of response.

TB: I think it was 93%. And, you know, fair’s fair, to be honest when the project was announced, there was a lot of immediate pushback on this. But 93% compliance, I think, is something I would expect that’s actually better than Inland Revenue were hoping for at the start of the project.

SE: I think it’s excellent. I mean, we know that there is a large enough population to give us a really good understanding of what this group of people look like. But I think it also speaks to something about it’s not like these people are necessarily trying to hide things, right?

When you see these kinds of numbers come out, there’s always a tension that all the rich are trying to hide things or they’re not trying to pay their fair share.

My sense is that that’s not really what the high rate of participation shows. I think what it shows is that people are relatively open. I mean, of course, there’s always a risk of not complying with Inland Revenue’s requests. But to me, it shows that even the very rich families, they do feel there’s a civic responsibility participating in society, that they want to be part of New Zealand and a tax system that is fair and transparent.

At least for me, the signals were very positive that these very high net worth individuals and families, they wanted to share that information so that we could have an open conversation about what is it that we want to do. Because the reality is that if we make changes on things like capital gains or wealth taxes, it’s not going to be just those families that will be affected, it will be a wider group of people. And having that transparency and openness does make it easier for us to have those conversations.

I think the study is really helpful because those studies give us real data and also just showed us the distribution of New Zealand. You know, the 99% of New Zealanders will live very different lives to that top 1%.

So how did the rich get rich?

TB: Yes, indeed. Just on the distribution in the report was there anything of interest to you about the range of the sources of that wealth? There’s some property, new technologies. Anything stood out for you in that data?

SE: Well, I mean, to me it was more that there was such a variety. I think that’s cool, right? It shows that to be filthy rich, there isn’t a common formula. There’s lots of different ways people have become filthy rich. Some of it because of, you know, like just being at the right time, at the right place in the right industry or having the right whatever. But it wasn’t all property. It wasn’t all one thing.

TB: Now the property thing is really interesting. I think on average each of the 311 families held 22 properties. But the analysis and modelling by Inland Revenue showed the capital gains weren’t all from property, they represented a range of things, portfolio investments, but mainly their own businesses that they had built up.

And that actually was something I thought was quite encouraging because you take that and the fact that we did not see a lot of inheritances being passed down and you got the impression that there were people who could come in and start at the bottom and have huge success. You mentioned Peter Beck earlier. Rod Drury of Xero would be another example of that. Stephen Tindall with The Warehouse, three different types of industries there. None of those are traditional industries, by the way. They’re not farming, or forestry related, but they’re all very wealthy people as a result of that. I guess people might say it shows a more diverse economy and the opportunity existing in that. So, I was encouraged by that.

SE: I think so. I think for most New Zealanders, the story of wealth creation kind of goes to a housing type story, right? Actually, there are a lot of people who’ve made a lot of money by starting businesses, selling businesses, or keeping businesses and growing them. And that to me is what creates economic vitality. That’s what creates a better New Zealand, right? That’s what creates more jobs.

I mean, of course we need homes. But you know what? It’s such a passive way to create wealth. Businesses are exciting because you’re creating jobs and changing lives through providing livelihoods. That, to me, is enormously more satisfying and exciting. Seeing a lot of that in the very high net worth individuals tax statistics, I think was very encouraging.

But it’s also true that not only do they make money by being in business, they continue to invest in businesses. So, it’s not like, there are these rich families that are sitting there with all this money sitting idle. We know they’re using that money all the time. They’re always looking for the next big opportunity. Of course, they don’t get it always right. But the reality is that, you know, I’ve been involved with businesses startups with these high net worth individuals, and they are the ones who back people. They’ll say ‘Here is a cheque for $1,000,000. I’m going to back you.’ And that is hugely powerful.

TB: That was something I came across when I was on the Small Business Council, the access to venture capital in New Zealand is surprisingly good. There is a fair amount available, and it is these wealthy people reinvesting in businesses. They go looking for the next Xero, the next Rocket Lab. And again, that’s encouraging.

What next?

So, what next? If you’re the Finance Minister or the Prime Minister, you’ve got this report and you say, ‘Right, here’s what we’re going to do.’ What would be the three things you would say to address the issues these reports have thrown up and improve our tax system?

SE: Well, if I were truly a politician in New Zealand, you know that I would have already sent out a poll asking a small group of people what they think about more taxes because we do politics by polling in New Zealand. And the polls will show that nobody, no New Zealander wants more taxes because they’re afraid that they might one day be rich, and they might be asked to pay tax on it.

So, you know that that the self-interest, that greed, that fear of missing out of a potential future, which is I think almost impossible, I think that would motivate most polls and they would show that people don’t want more taxes. And as Finance Minister, if I were truly in Cabinet today, I would see those polls and say ‘Bugger it, I’m not going to do anything. Bury this thing.’

That is the sad reality, it’s heartbreaking that we have seen very little action when it comes to tax policy in New Zealand for decades. Because you know what? We just don’t have the steel and the political consensus across the community to do anything different.

TB: Yes, I think that’s it in a nutshell. I mean, I think Jim Bolger’s ‘Bugger the pollsters’ is something that should be adopted when it comes to tax. Because the politicians, and it’s interesting, doesn’t matter which side, they run away from the issue.

I know I’m a broken record on this. I’m looking at what’s coming down the track, what the Tax Working Group saw was coming down the track. We’ve got demographics working against us with ageing, higher superannuation costs, greater health care demands and now climate change.

The Climate Change Commission in its report released yesterdaybasically said ‘We can’t buy our way out of reducing our emissions, we need to diversify.’ And that report, when it talked about tax, made repeated mentions of tax incentives for better investment to address these issues.

So, it seems to me that like it or not, politicians are going to have to address these facts or simply say, well, ‘You can’t have anything because we need to protect these unrealised gains.’

SE: You know, I was probably being overly pessimistic. But I think the thing is, in the current moment in time, the crisis still feels like it’s two or three or four or five political cycles away.

If you make changes on tax policy today, inevitably you will see whoever’s in power next undo them. So there will be no enduring tax policy because we don’t have consensus in New Zealand. Do we have a pressing need to shift our tax policy? Of course, we do because of demographics and because of climate change, because of large infrastructure deficits, we know that we need to change things. But we also know that New Zealand has an extraordinary reactionary political system. There is no leadership, it is reactionary. And so, unless there is a crisis, until something really breaks, we’re not going to change.

TB: So you don’t think Cyclone Gabrielle, or the Auckland floods are a breaking point?

SE: Not at all. I mean, they might cost the government, you know, a maximum of $15 billion in the scheme of things. That’s nothing spread over three or four years.

You know, the Government’s tax take per year is $100 billion. Those costs are at the margins. So that’s not enough. It’s when you’ve got Cyclone Gabrielle happening every year or every other year when people can’t get access to insurance, when we’ve got coastal properties that are being inundated, when we’ve got erosion that’s taking away what we’ve previously valued as multi-million-dollar bachs. That’s when you’re going to start to really strike those pressure points, because we haven’t actually planned for any of this stuff.

TB: Those are all happening right now, actually. I mean, Tairawhiti East Coast region, I think Cyclone Gabrielle was the fourth major event that warrants special tax treatment inside 12 months. But as just said, it’s now receding into the background. Maybe it’s not so much our politicians, it’s also our media cycle just isn’t adapted to that.

SE: I think it’s less about the media cycle, it’s also what we want to hear as citizens, as engaged people in politics, people who are engaged in the civics of the country. Are we actually engaged in grappling with these big structural issues? And the answer is no. And I think the conversations that we have on public policy in New Zealand are, by and large infantile.

You know, they are by and large led by people who are lobbyists and people who are actually biased with a huge amount of self-interest because it is a small group of people who do everything. There’ll be the tax experts who are providing expert advice to people to minimise their taxes and the same people who are going there to try and design a business tax system. Well, I don’t know, man can you really trust them?

TB: Well, reputational risk here, but yes, I think self-interest is a problem. But let’s just be bold, let’s say you’ve decided ‘Bugger the pollsters’ what would you do?

What tweaks would you do if you were looking at something that might take the population around along with you? What would be the first thing to do.

A tax switch?

SE: You know, I think one would be relatively easy in that you would do a tax switch. You would implement a land tax and you reduce something like GST. That switch would be quite immediate and it would create a much better balance in New Zealand. It wouldn’t capture the very high net worth because it’s not about that, but it would create the introduction of a wealth tax. We already have the mechanisms for that with things like the rating tools.

But, you remember with the Tax Working Group, the land tax was one of those things that was identified as a good tax to have, because we know that not only would it incentivise better use of our land that we have, but it’s also that one asset that can’t run away, like unlike many of the other types of assets that people hold. So that would be the big thing.

But fundamentally for me, it’s really around if you really want to change tax policy, you’re going to have to create consensus. And you know, we can’t do that until we have some kind of bipartisan agreement about, one, what the issues are, and two, that we fundamentally either need to have higher taxes or we simply cannot have all the services that we have promised ourselves.

Now, that’s a really hard conversation to have. You know, you look at the quality of our political leaders. They’re not engaged in any of that debate. You know, most of our political leadership is engaged in the politics of who’s going to do the least.

TB: It’s a very small target strategy.

SE: It’s sort of, if you ask me what needs to change, I think the change that needs to happen is not that you need to jump in and make lots of changes, because the reality is that the knee jerk reaction will be to reverse those through a change of government. I think the change that requires us to have is actually creating something like the Climate Change Commission that creates this conversation. Some of those public policy issues that take the politics out of it.

TB: So, are you saying there should be the equivalent of the Climate Change Commission, a Tax Policy Commission that alongside David Parker’s Tax Principles Act, but sits there and pushes out the reports and saying, ‘This is it, guys, this is what we can do.’ In other words, a semi-permanent tax working group.

SE: Except of course it must have powers and it must have the ability to hold the politicians to account. Quite often what we do with things like the Climate Change Commission is we give them the power to design, but we don’t give them the power to actually fund or hold the powerful to account.

It’s not going to be very hard, right, because no politicians want to give the power away to somebody else. There will be no independent body that they’re going to give the powers away. The only one that they’ve really done that with is the Reserve Bank, and I think they’ve been regretting it ever since.

TB: Yes, I was thinking of the Reserve Bank too. I think that’s probably as good a point as any to leave it there.

Shamubeel, thank you so much for being on the show. Really appreciate your insights on this. I hope I don’t feel so pessimistic, but to be frank, we probably have good reasons for people to be sceptical about what will change anyway.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week, kia pai to rā.