This report was commissioned by the tax advisory firm OliverShaw and has been released ahead of two reports coming out next week, one from Inland Revenue on the tax and effective economic income of high wealth individuals in New Zealand and the other from Treasury on the effective tax rate of New Zealanders across the income and wealth distributions.

As you may recall, the Inland Revenue project reviewing the net wealth of the 400 richest families in New Zealand has been highly controversial and generated quite a bit of pushback from the outset. There were mutterings about court actions to prevent the proposal going ahead, although as far as I’m aware, none of those have ever eventuated.

Nevertheless, the controversy prompted OliverShaw to commission a report because, as they say in the Foreword of the report:

“From what has been said about the methodology of the Inland Revenue study, it seems that the Inland Revenue and Treasury studies may use different methodologies. A comparison of two different studies using different methodologies could easily produce a misleading and confusing picture of our tax system.

Moreover, the Inland Revenue methodology seems inconsistent with OECD and academic effective tax rate studies….We therefore considered it important to have a study that uses a more consistent approach to estimate the effective tax rates that are imposed on the incomes of low, medium and high wealth households rather than just high wealth individuals.”

That’s the rationale that OliverShaw gave for the project. Incidentally the Oliver in OliverShaw, is Robin Oliver, a former Deputy Commissioner of Inland Revenue and a member of the last Tax Working Group. So, he speaks with a lot of authority. You will also recall Oliver was one of three members of the Tax Working Group who produced a dissenting opinion on the proposal for a comprehensive capital gains tax.

Worth keeping in mind, however, that Oliver and the other two dissenters, Kirk Hope and Joanne Hodge did agree with the rest of the group in extending the taxation of residential investment properties. This probably should be kept in mind amongst all controversy the Sapere Research Group report has produced.

The report, to put it mildly, is massive, it runs to a total of 267 pages, in three parts. There’s a foreword from OliverShaw, followed by a detailed outline of the report. And finally, the report itself, which breaks down into five sections, an introduction, an overview of New Zealand’s tax and benefit systems, the effective tax rates estimates, section four then interprets and applies these effective tax rate estimates. And finally, there is the conclusion in section five.

So it is colossal and to be honest, I haven’t yet got my head around all that’s in here. It’s certainly, as I’ve heard one or two other experts say, a report that merits rereading as often is the case when you’re processing this much data. As far as I can recall nothing like this was prepared for the Tax Working Group. (No doubt some will correct me if I’m wrong on that).

It’s an extensive piece of research and its conclusions are a little controversial, because in essence, they appear to be saying that the average effective tax rate paid by the wealthy is not far off that paid by other middle-income earners.

By the way, the classification of what is middle-income is something that perhaps might provoke some pushback. Low income is seen as under $48,000, which is the threshold at which the income tax rate increases from 17.5% to 30%. Medium-wealth households are described as those that derive annual net real economic incomes between $48,000 and $500,000. High wealth, high income households are those deriving net real economic incomes in excess of $500,000.

That medium-income upper threshold of $500,000 seems pretty high to me. But no doubt the statisticians and others have got a reasonable background on it.

As I said, there’s so much in this report to digest that it’s possibly the reason why there’s a fair bit of confusion about what it is really driving at. In summarising the report’s conclusions Robin Oliver commented;

“One of the questions asked is whether the very wealthy pay taxes at the same or higher rate than middle income earners…This research shows clearly that, whether you consider taxable income or other measures, such as economic income, the answer is: ‘Yes, they do.’ “

That certainly raised a few eyebrows around the place, including that of Craig Elliffe, another member of the last tax working group. And if you want a good critique of the report and where some of the issues are going to be explored further, The Spinoff has a very good article in which they spoke to Craig Elliffe at length on the matter.

For myself I’m still digesting the report. As I said, it’s massive and a significant amount of data to absorb. So, I’m not so keen to rush to judgement. Certainly, that conclusion that Robin Oliver cited surprised me. On the other hand, when he was interviewed for Newstalk ZB, he did point out that there’s a real problem with the tax rate jumping from 17.5% to 30%, around the $48,000 threshold.

Indeed, one of the conclusions of the report is arguably the highest effective tax rates are paid by those on the lowest incomes once you take into consideration the impact of abatement of benefits.

Getting your retaliation in first?

The report has generated a lot of controversy, which appears to be the deliberate intention of OliverShaw. It certainly follows the motto adopted by the 1974 Lions captain Willie John McBride when they were about to play the Springboks “Let’s get our retaliation in first”.

I’m therefore going to withhold further comment on the report until I’ve seen the reports from Inland Revenue and Treasury. We’ll then be looking at three very comprehensive reports and I’m sure a clearer picture will emerge as from these reports once they’re considered as a whole.

Still, it’s good to see tax in the news. I think generally we don’t talk seriously enough about tax. Politicians will fence around the topic talking in slogans, but the nature of what we tax, and how we tax is incredibly important. As I’ve said repeatedly in the past, I am concerned that we’re facing significant fiscal challenges from climate change and changing demographics. Our tax system has to be seen to be robust enough to meet those demands.

Does that mean, as the economist Cameron Bagrie suggested recently, we may need to be raising taxes? All of that is up for consideration. So, a debate around what’s taxed and who pays what is very good to see. And I look forward to engaging more in that debate.

Lessons from FATCA?

Moving on, as noted above, one of the controversies about the Separe report and in general, is over the question of the true economic income of the highest net worth New Zealanders. And the controversy really arises because we don’t know very much. Data is scarce on this topic and that generally bedevils tax policy and tax revenue authorities around the world and has done for a long period of time.

A report from the United States this week looks at the data obtained as a result of the highly controversial Foreign Account Tax Compliance Act, or FATCA.

If you recall, this was introduced in the wake of the Global Financial Crisis, and it required banks and financial institutions in overseas jurisdictions to provide data to the United States Internal Revenue Service (“the IRS”), regarding foreign wealth held by United States citizens in those foreign jurisdictions.

To recap, the United States requires all its citizens, whether or not they are living in the United States, to file tax returns. As part of those filings, they are required to provide details of all overseas financial bank accounts. FATCA is an incredibly important piece of legislation, probably one of the most important pieces of tax legislation in the last decade, because it became the genesis of the OECD’s Common Reporting Standards on the Automatic Exchange of Information.

Following the introduction of FATCA. Other jurisdictions thought, “Well, if our financial institutions have to supply this information to the United States, it would be handy if we also knew exactly which of our citizens and tax residents had wealth overseas.” So that was the genesis of the Common Reporting Standards (“the CRS”).

The IRS, together with the United States National Bureau of Economic Research, have just released a report which pulls together all the data so far provided to the IRS since 2015, when FATCA took full effect.

This has enabled the IRS and therefore the United States government to get a clearer handle on what wealth is held offshore and by whom.

According to the report, around 1.5 million US taxpayers hold foreign financial accounts. The total value of those is around US$4 trillion as of the year ended 31st December 2018.

Just for comparison, the total financial assets of the US households amounted to roughly US$80 trillion in 2022. What is of particular interest to the IRS is about one in seven of these overseas accounts are held in jurisdictions usually considered tax havens such as Switzerland, Luxembourg and the Cayman Islands, but those accounts total nearly US$2 trillion. The report’s authors conclude that this indicates accounts in tax havens are, on average, larger.

Another point of interest is the ratio of tax haven assets to GDP is estimated to be about 10%. That was higher than previously estimated. The implication is that financial assets in tax havens may have grown significantly faster than the overall U.S. economy since 2007, which is that baseline for that previous estimated ratio of tax havens wealth to GDP.

The FATCA data is enabling the IRS to get a better idea of who holds overseas assets. It appears that more than 60% of the individuals in the top 0.01% of the income distribution in the United States own foreign accounts, either directly or indirectly. What also happens is that the proportion owning offshore accounts rises as the incomes deciles rises. This apparently ties in with literature, which says that there's a strong correlation between the wealthier a person is, the more wealth is held offshore.

Now this data is prepared for the United States and comes out of FATCA, but I expect Inland Revenue would be mining the data it’s receiving through the Common Reporting Standards.

And it might be that we might see some of those findings reflected in next week’s reports. It doesn’t surprise me, by the way, that the wealthier a person is, the more wealth is likely to be held offshore because wealthier persons will seek to diversify their asset holdings.

That’s a natural response and shouldn’t necessarily be seen as being sinister. But whatever the reason, it’s interesting to see what the IRS has gathered so far from its data.

And of course, it will be interesting to see how they respond to that data. Of course, they’ll certainly get pushback from the Republican Congress on that. But that’s politics and taxes, they go hand in hand. I’m curious to see what, if any, reference to CRS data comes out of next week’s Treasury and Inland Revenue reports.

New Inland Revenue guidance on the bright-line test and family transactions

And finally, this week, and also connected to our main story, Inland Revenue has released some guidance in relation to the bright-line test and family transactions. Now this particular Interpretation Statement IS 23/02 is very specific.

It applies to the application of the five year bright-line test, that is where the land was purchased between 29th March 2018 when the bright-line test period increased from 2 to 5 years and, 27th March 2021 when the bright-line period was further extended to ten years. As is now usual, the interpretation statement is accompanied by a useful six-page fact sheet.

The Interpretation Statement covers scenarios where parents are assisting children or other close relatives with buying first homes, a partner is added to the title of residential land and where land is inherited under a will which is then on-sold to other beneficiaries.

Generally speaking, if you sell residential land to a family member or partner within the bright-line period, that potentially will trigger a taxable charge. That may also be the case if the land is gifted or sold below market value. On the other hand, if residential land inherited under a will is sold to other beneficiaries under that will, that sale would be exempt from the bright-line test. However, any subsequent sale by those recipients to a third party within the relevant bright-line period would be taxable.

Inland Revenue have promised to release separate guidance on this issue of transactions between family members in relation to the ten-year bright-line period, and that will be considerably more involved.

Something which comes up repeatedly and lies at the heart of the controversy surrounding the Sapere report are the implications of the lack of a comprehensive capital gains tax. At the moment, it results in distortions where someone’s economic wealth rises without being subject to tax, whereas in other cases an equivalent rise in value may be taxed because of a different set of circumstances. The various iterations of the bright line test are a good example of this frankly, incoherent approach.

That’s all for this week. Next week we’ll be looking in detail at the Treasury and Inland Revenue reports on tax and economic incomes of New Zealanders and how their conclusions and methodologies compare with those in the Sapere report.

Until then, I’m Terry Baucher and you can find this podcast on my website or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Happy new tax year and welcome to the 2023-24 tax year and as is often the case the start of a new tax year it means newly enacted legislation is now in place.

However, some of the same old issues are still with us.

The Taxation (Annual Rates for 2022-23, Platform Economy and Remedial Matters) Bill (Number 2) finally received the Royal Assent on 31st March. Apparently this bill had nearly 200 new clauses, which between them had some 42 different application dates. So, it was a surprisingly complex bill. But remember, its most controversial proposal to standardise the treatment of GST on fund management firms was removed.

As noted, the bill has got quite a considerable amount of new provisions in it, and we’ll pick up several over the next few weeks. But I want to start by looking at the new fringe benefit tax (FBT) exemptions for bikes and public transport. As you may recall, the bill originally had an exemption for public transport, but at the last minute an FBT exemption for bikes was introduced. That actually covers bikes and “low powered vehicles”, so obviously covers scooters, e-scooters, e-bikes. The exemption from FBT applies where you are travelling between home and work. There’s going to be a maximum cost for the low-powered vehicles, which is yet to be confirmed by regulation shortly.

Watch out for the hook in the FBT exemption for bikes and public transport

But the key point to keep in mind is that the bike or scooter must be used mainly for travelling between home and work. Therefore, where that isn’t the case, FBT would still apply. This together with the maximum price cap on the exemption should rule out people buying high end bikes, e-bikes or e-scooters and then using them mainly for private use hoping that it’s exempt from FBT.

Now the exemption is from FBT, there is no equivalent exemption for PAYE. What that means is, it is very important for employers to consider how they provide that benefit and don’t make the mistake of assuming “Well, the FBT exemption applies so nothing to worry about.” The issue that arises is where the employer purchases the bike or scooter directly, then the FBT exemption should apply. However, if the employee chooses and purchases a bike personally and is then reimbursed, then PAYE will apply and there’s no exemption.

This principle also applies to the exemption around the use of public transport or vehicle shares, such as Uber and similar apps. Again, the employer must incur the cost for the exemption to apply. As some have noted that’s actually administratively quite awkward. It seems likely quite a few employers will accidentally trip up on this by reimbursing the employee rather than incurring the costs directly. The hope is that this particular anomaly can be quickly resolved and therefore ease the compliance involved.

Now, the new act also contained a permanent exemption from the interest limitation rules for build to rent dwellings. This exemption will apply where there are at least 20 connected dwellings, and the landlord must offer a fixed term tenancies of at least ten years. By the way, for the purposes of the interest limitation rules, as of 1st April, only 50% of the interest is now deductible unless one of the exemptions, such as a new build or build to rent, applies.

Interest limitation rules and short-stay accommodation – don’t get mucking fuddled

Coincidentally, last week, Inland Revenue released a draft interpretation statement for consultation on the interest limitation rules and short-stay accommodation. The interpretation statement considers how the interest limitations will apply and then also explains what other income tax rules may be relevant depending on the circumstances. The draft interpretation statement runs to 79 pages and is now common practice, it’s accompanied by a fact sheet.

It says much about the complexity of the rules in this area that the fact sheet runs to 13 pages. That’s because not only are the interest limitation rules applicable owners of short-stay accommodation must also take into consideration the potential application of the mixed use asset rules which have been around for over ten years now, as well as the ring fencing rules.

For the purposes of the draft interpretation statement, short-stay accommodation is defined as accommodation provided to paying guests for up to four consecutive weeks. The interpretation statement covers five scenarios where such accommodation is provided:

either in a holiday home; in a person’s main home; in a separate dwelling on the same land as the main home; in a separate property used only for short-stay accommodation; and on a farm or lifestyle block.

Within each of those five scenarios, the interpretation statement will explain if and how the interest limitation rules will apply, what apportionment rules apply, and whether ring fencing rules apply. There are also variations within these scenarios. If there’s a new build involved, for example, a person’s holiday home is on new build land, then the interest limitation rules will not apply. However, the deductibility of interest is still subject to the other apportionment rules, such as those contained in the mixed-use asset provisions and the ring-fencing rules will still apply.

As can be seen, there’s a great deal of complexity now involved, and this is partly the result of the somewhat ad hoc approach adopted by the Government in tackling what it sees as the preferential treatment of residential property investment. It also reflects generally incoherent policy resulting from the lack of a comprehensive capital gains tax. Whatever, the key lesson to watch out for is that the short-stay accommodation rules are now incredibly involved, so proceed with great care.

The taxation of capital is a longstanding issue and one which in my opinion, will need to be addressed sooner rather than later. Not only because of the tensions it creates within the tax system, but also because of the need to find additional revenue to meet the demands of an ageing population and the impact of climate change, which we’ve spoken about previously.

We like New Zealand Superannuation – but how are we going to pay for it?

And three reports this week highlighted this ongoing tension around meeting future liabilities. Firstly interest.co.nz covered a study coming out the University of Otago regarding New Zealand Superannuation. The study surveyed almost 1300 people in 2022 asking them what they felt about the age of eligibility, means testing and the willingness to increase both current and future taxes to pay for New Zealand Superannuation.

The study found there was widespread opposition to financial barriers for receiving superannuation. Means testing was not popular, but the support for keeping the retirement age at 65 has increased, with almost a quarter ranking the age of 65 as most important aspect of New Zealand super compared with a fifth back in the 2014 survey. 61% of those surveyed ranked raising the retirement age to 67 as the worst policy. The general response was they would prefer universal superannuation.

The New Zealand Super Fund, which has been established to help spread the cost of superannuation was popular. Although there was opposition to increases in current taxes to pay for New Zealand Superannuation, a majority of respondents still support higher current taxes to reduce the size of future increased tax increases given plausible investment returns.

A day earlier independent economist Cameron Bagrie told Newshub he had concluded New Zealand might need to introduce tax increases to have to deal with the impact of climate change and what he called an “infrastructure mess.” In his view, taking into consideration climate change, infrastructure and superannuation “If I step back, though, and think about tax rates in general over the next ten years, where do I think they’re going to be headed? I think they’re going to be biased up as opposed to down.”

Climate change will cost “multiple billions” under ALL scenarios

Bagrie will probably be reinforced in his view by the Climate, Economic and Fiscal Assessment for 2023 released last week by the Treasury and Ministry for the Environment. This report concluded,

It is clear that the size and breadth of the economic and fiscal costs of climate change to New Zealand will be large. The physical impact of climate change and the choices the country makes to transition to a low emissions future will affect every aspect of the economy and society for generations. These impacts will have flow on implications for the Crown’s fiscal position.

What particularly seems to be concerning the Treasury and the Ministry for the Environment is that at present in the planning to help meet our climate targets there is an assumption that we will be purchasing offsets from offshore. As the report notes,

The cost of purchasing offshore mitigation to achieve New Zealand’s [commitments] presents a significant fiscal risk. For all scenarios considered, our analysis estimates this cost to be multiple billions over the period 2024 to 2030.

Multiple billions in this case could range from a low-end estimate of around $7.7 billion to perhaps as high as $23.7 billion. Apparently, the costs involved represent between 3.9% to 28% of the new operating expenditure that will be made available in each budget. Therefore, if climate change is swallowing up to 28% of the new operating expenditure that puts pressure on other areas such as education and health.

The report also discusses the potential tax implications. As noted at the start of section 6 on Fiscal Impacts, “Climate change will create multiple cost pressures for the Crown and is likely to negatively affect its tax base through changes to economic activity.” This presents a big question for policymakers and politicians – how do we have enough revenue to square the circle between meeting the demands for health and superannuation, and our climate change commitments? So that is why, like Cameron Bagrie, I think there is an inevitable pointer towards tax changes.

And on that bombshell, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Friday was the final day of the 2022-23 tax year for most taxpayers. One of the more important tasks to achieve that day was filing any outstanding tax returns for the 2021-22 tax year. March 31st is the latest due date for taxpayers with a tax agent and most tax agents, including myself, were busy filing tax returns to meet this deadline.

A key reason the deadline is important is because under the Tax Administration Act, Inland Revenue have four years after the end of the tax year in which a tax return is filed to open any investigation into that return. This is what we call the time bar period. For example, Friday was the last day for Inland Revenue to open a review of a tax return for the year ended 31st March 2018, which was filed during the year ended 31st March 2019. The four-year time bar period expired on 31st March 2023. If the deadline isn’t met and you’re late, even by a day, then effectively you give Inland Revenue an extra year in which to review a return.

But there are circumstances in which Inland Revenue can reach back beyond this four year period. And a Technical Decision Summary released this week is a good illustration of when that might happen. Technical Decision Summaries come out of disputes which have gone before the Adjudication Unit of Inland Revenue. They’re not formal decisions, but they’re very good indicators of the type of cases Inland Revenue has been reviewing and how it would approach a case.

The background is that an individual taxpayer had a business and got into a dispute regarding the treatment of deposits made to bank accounts owned by the taxpayer and associates during the 2010, 2011, 2012, and 2016 tax years. Did these deposits represent assessable income. If they were, was the taxpayer liable for a tax evasion shortfall penalty Inland Revenue was also looking for an increase in that shortfall penalty for obstruction. And that last point is not something we’ve seen very much of before.

But before Inland Revenue get to that, the question that had to be decided was whether they were entitled to amend the assessments to increase the amounts, because the years in question were outside the four-year time bar period I just mentioned. Now, this is the most interesting part of this whole case because it is a good background of when Inland Revenue can amend to increase income in a tax return. It’s also worth remembering they may also go past the time-bar to decrease an amount of a net loss.

As noted, all the disputed periods 2010, 2011, 2012 and 2016 would have been time barred unless one of these exceptions applied. And the relevant exceptions are where Inland Revenue or the Commissioner of Inland Revenue, to be exact, is of the opinion that a tax return provided by a taxpayer is “fraudulent or wilfully misleading,” or does not mention income of a particular nature or derived from a particular source.

A key point here is that it is sufficient for the Commissioner to honestly believe on the available evidence and on the correct application of the law that the tax return in question meets the requirements for these exceptions to apply. And if you’re going to challenge the Commissioner, that will only succeed if the Commissioner did not honestly hold that opinion or misdirected himself as to the legal basis on which the opinion was formed, or his opinion was not one that was reasonably open to the Commissioner on the available information.

A decision to re-open a time-barred tax return is what we call a disputable decision so it can go before the courts. But the burden of proof rests with the taxpayer to show on the balance of probabilities that a decision made by the Commissioner to reopen time-barred years is wrong.

The adjudicator at the Tax Counsel Office went back to basics in examining the case because it’s a fairly serious matter if you’re going to reopen tax years. The Tax Counsel Office concluded on the evidence that the taxpayer knew they were breaching their tax obligations by not returning rental and business income. This was also apparent from and could be inferred from the taxpayer’s business experience. Furthermore the taxpayer went so far as to proactively provide misleading information about the requirement to file during a phone call with Inland Revenue. The Tax Counsel Office therefore formed the view the taxpayer’s returns were fraudulent and wilfully misleading.

However, the Tax Counsel Office also considered there wasn’t enough proof to show evasion for the 2011 year. But they did say there should be a gross carelessness shortfall, penalty of 40%. The taxpayer was held to have evaded tax in the other years so Inland Revenue went for tax evasion penalties, which are 150% of the tax evaded (discounted by 50% for previous good behaviour). Bear in mind, use of money interest will also be running on the tax evaded.

What Inland Revenue also did, which I haven’t seen much of before, is the shortfall penalties were increased by 25% for obstruction. This was done because the taxpayers continued and undue delays, misleading statements, clear diversion of income into other relatives’ bank accounts and repeated failure to be forthcoming about with information about deposits and bank accounts delayed and made it more difficult for the Inland Revenue to carry out the audit. This obstruction affected the 2011, 2012 and 2016 years and for each of those years, the shortfall penalty was increased by 25%.

The case illustrates when Inland Revenue can bypass the four-year time bar. Although it felt it was dealing with a case of tax evasion, the Tax Counsel Office also concluded the four-year time bar didn’t apply because no return had been provided and no declaration had been included of income, then the second leg was also available. The 25% increased shortfall penalty for obstruction is one of the first cases where I’ve seen it applied. In summary, this is a classic example of where the taxpayer screwed around and got found out and would have paid quite a considerable penalty.

Interest deductibility and thin capitaisation

Moving on, earlier this week, an article popped up over whether or not landlords are in business, and on the face of it they are. But landlords have been complaining that they are not treated like other businesses and are subject to more rules and regulations. One of the sore points for residential property landlords is the question of the interest deductibility, which is restricted.

According to Property Investors Federation vice-president Peter Lewis, he made the case that it is a business and the interest deductibility compared with other businesses is an example where they’re treated differently, however. And Brad Olsen, the Infometrics chief executive and economist, agreed with him on that.

When I was asked this question, my response was it’s not technically correct to say no other business is denied interest deductibility. Landlords are not unique in that sense. That’s because of the thin capitalisation rules which apply to New Zealand companies with overseas parent companies. Under these rules, if the debt to asset ratio exceeds 60% then interest deductions above that threshold are restricted.[i] (As an aside, I thought that when it was clear the Government was considering changes to residential rental property, adopting the thin capitalisation regime, which has been in place since 1995, would have been one option. But as we know, they went a different route).

The other point I made is that residential property investors have the ability to leverage quite significantly, and they also seem to get away with expectations of a lower return. In my view that’s partly an expectation of the capital gain which drives this behaviour. Brad Olsen probably was coming from the same point where he said the gains should be taxable.

On the other hand, you get do have investors with maybe ten or more properties. Then you quite clearly are running a business. If you are trying to level the playing field, then the question is perhaps whether the restrictions around interest deductibility should apply or rather maybe these investors are a group that are probably more appropriate for the thin capitalisation regime.

You may recall when John Cantin was on the podcast and we talking about interest restrictions, he made the point perhaps there always should have been some form of interest apportionment would not be remiss because there is a clear expectation of some non-taxable capital gain. As we will find out in the next item, interest is generally deductible to the extent it’s incurred in deriving gross income. And if capital gains aren’t gross income, why should you get a full deduction?

In my view, when thinking about regulations, while you’re in business, you just have to accept they are a fact of life. Some businesses are regulated more than others. For example, food manufacturers and restaurants, have a fair number of regulations imposed on them for the better health of the public at large.

Anyway, the argument over the treatment of interest deductions isn’t going to go away. Landlords may feel aggrieved about their treatment at this point in relation to interest, but they’re not entirely unique in my view, because the thin capitalisation rules apply to other businesses. It’s always worth remembering that if a property does become taxable because of the bright line test or some other provision, generally speaking, interest deductions incurred in relation to that property will become deductible on the disposal.

Capital expenditure?

And finally, this week in a slightly related matter, an interesting story out of the U.K. from the BBC after it emerged an OnlyFans creator had claimed a tax deduction for breast enhancement surgery.

Titillation aside this caused a bit of a stir in the U.K. because the deduction rules in the U.K. around self-employed are actually much more restrictive than here. On the face of it, the deduction seems to be a bit generous. The lady in question incurred the expense because she wanted to boost her appearance and drive up her income from the OnlyFans subscription-based website.

Titillation (ahem) aside, the reason why UK advisers looked a little bit sideways at this case is because the general rule for self-employed deductibility is it must be “wholly and exclusively incurred”. In theory, if there’s a private element no deduction would arise, and there would appear to be at least some private element in any breast enhancement.

By comparison as I just mentioned a few minutes ago, the relevant provision in New Zealand allows a deduction to the extent to which the expenditure is incurred in deriving assessable income or in the course of carrying on a business of deriving assessable income. It’s quite clear that for New Zealand tax purposes, a deduction of some of that breast enhancement expenditure would be allowed.

So, if you’re thinking about the end of the tax year and maximising your deductions, remember expenditure is deductible to the extent it’s incurred in deriving gross income and therefore some form of apportionment is available. The question here in New Zealand comes down to determining what proportion is deductible. However, a fellow tax specialist did wonder whether in this case breast enhancement might be capital expenditure and therefore subject to depreciation.

Well, on that bombshell, we’ll leave it there. We’re going to take a short break for Easter next week, so we’ll be back in a fortnight. In the meantime, I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

[i] In some circumstances the thin capitalisation rules also apply to New Zealand resident investors with offshore investments

The end of the tax year on March 31st is fast approaching. This is a time of year where myself and other tax advisers are frantically tidying up outstanding tax returns and advising clients on steps they should be taking to make sure there are no unwelcome tax surprises for them. So here are a few common tips that we are passing through to clients.

Firstly, go through your debtor ledger and write off any bad debts. A bad debt deduction is only allowable if the debt is written off in the tax year in question. In doing this you really need to take a hard eyed look at your debtor ledger and tell yourself, realistically, are these debts going to be paid? Factor in how long the debt has been outstanding, the credit history of the client and what you know about how the client’s business is going. You can always write these debts off, take the deduction, and then if fortunately the cash comes through, then you write it back the following year. But the key thing is you can’t take a bad debt deduction until you write it off. And my recommendation is always to err on the side of caution on this one. So that’s my main tip.

My number two tip is one we see a lot of in our business and that is overdrawn current accounts. These happen when the shareholders/owners have often taken out more money than they’ve been paid through the salaries or are likely to receive. Where a client has an overdrawn current account there are a couple of options to offset against the overdrawn current account, an increased salary or a dividend.

If neither of those are possible because there are no reserves or the company has not been profitable, then what you will be faced with is having to charge interest on the overdrawn amount. The rate applicable is the fringe benefit tax prescribed rate of interest and for the quarter beginning 1st January 2023 it’s 6.71%. You calculate an interest charge based on the current account balance throughout the tax year. Keep in mind the rates have been rising, back on 1st April 2022, they were 4.5% and it’s due to rise again on 1st April to 7.89%.

This is an issue we commonly see, and we don’t often get to hear about it until it’s too late and often before remedial steps can be taken. A common reason for its occurrence is people take out too much money or the company has realised a capital gain and they’ve helped themselves to the capital profit without realising that actually it’s not as easy as that, that there are proper processes to be followed for distributing capital. This is a common issue most accountants will encounter and you need to take action, preferably before 31st March, to mitigate the impact.

Still on companies, a key area you’ve got to keep an eye on is what we call the shareholding continuity provisions. That is making sure that the relevant percentage of shareholders doesn’t drop below certain thresholds. For example, if it drops below 49% a company which has accumulated tax losses could potentially lose those tax losses. More critically, if it drops below 66%, then any imputation credits that have been accumulated will be lost. This will affect the distribution of dividends and lead to an effective double tax charge.

So again, check shareholding percentages very carefully. If there have been any changes, you need to make sure that they will not affect any tax losses or imputation credits a company may have.

Another important area is fixed assets. Where the fixed asset cost less than $1,000 check to see you have been taking an immediate tax deduction for the full amount. You should also go through assets that have been on the fixed assets ledger for some time, and just consider whether, in fact, they are in use anymore. If not, write them off and tidy up the balance sheet at that point.

A little pro tip here. You get a full month’s deduction for depreciation purposes regardless of when you purchased depreciable asset during the month. So, if you purchase an asset on 30th March, you will get the relevant full month’s depreciation deduction for that asset. So, if you are considering purchasing assets and they don’t fall within that low value asset write off limit of $1,000, you can maximise in a temporary way the depreciation deduction.

The final tip is to make sure that you’ve got all your elections filed on time. For example, if you’re considering, electing to join the look through company regime, those elections must be filed before the start of the new tax year (unless you’ve got a startup company). There are also some residual elections around in respect of qualifying companies. We don’t see so many of those now because that regime was abolished more than ten years ago.

Filing elections on time is crucial because if you missed the deadline you’ll have to wait a year. Inland Revenue, although it does have some discretion around late elections, very, very rarely will exercise that discretion. There may be some relief where it has been quite apparent that the recent cyclone and flooding events have disrupted a business.

You should also be trying to file all tax returns due by the end of the tax year. Otherwise, what we call the time bar provisions effectively get extended there – in effect Inland Revenue has another year to re-open prior year tax returns.

So that’s a few tips on how to get ready for tax year end and the most common areas we encounter. There are some good checklists around, including this comprehensive one from BDO.

The key thing is to be aware and get in front of your accountant or tax agent as soon as possible, don’t leave it until the 31st to ask these questions. We work miracles a lot of the time, but not every day.

‘Serious design issues’

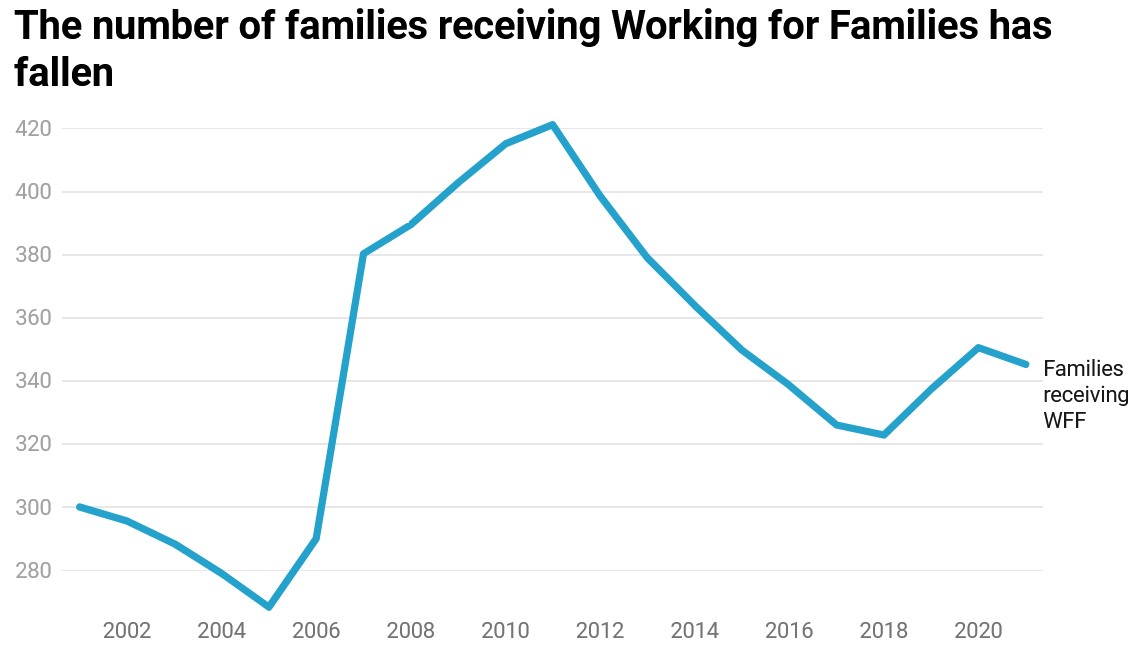

Moving on, earlier this week, there was a report that a major review of the Working for Families scheme is currently under consideration by Social Development Minister Carmel Sepuloni.

The report has “found serious design issues” in the way some of the tax credits are applied. It highlights a number of factors which I’ve talked about for several years now, such as the increasing impact of the low abatement threshold.

Just as a refresher, the abatement threshold for Working for Families kicks in at $42,700. If your family income is above that threshold, then for every dollar of taxcredit you receive, $0.27 is abated, which means effectively that’s a 27% tax on that income.

Now, you’ll note that $42,700 is below the threshold of $48,000, where the tax rate increases from 17.5% to 30%. So as this report notes, the abatement threshold kicks in at relatively low incomes and not far below what someone on the minimum wage from 1st April will be receiving. So the whole system is due for a thorough review.

This issue was raised by the Welfare Expert Advisory Group and the Child Poverty Action Group, have been hammering away at the inequities of the Working for Families system for years now. Last week I talked about the interesting initiative in the UK budget for childcare to be provided to basically every child over the age of nine months. But that came with a sting in the tail that there was a very, very penal abatement regime once you crossed a threshold even though that threshold was quite high.

But the point stands that thresholds and abatements can produce some very unwelcome outcomes, and one of which is that people may no longer have the incentive to work because they just look through the numbers and decide once the extra tax and the abatement is taken into consideration, they are no better off.

And one of the interesting things that this report shows is the number of families receiving Working for Families has fallen from about 420,000 in 2011 to just over 340,000 in 2021. When you consider the population growth in that time, that’s quite a significant fall in relative terms.

Another issue which requires resolution is that more and more families are falling into debt because they were overpaid Working for Families tax credits during the year. Apparently 57,000 families now owe debts worth $250 million, which includes $71 million of penalties and interest. Almost certainly most of these families are at the low income, so digging their way out of debt is a real problem.

It’s good to see that a report is being considered as major changes are needed. I have a sense that this year’s budget is going to tackle some of those issues, not least of which would be increasing the abatement threshold. A point of interest about the abatement threshold is that when Working for Families was introduced, the abatement threshold was $35,000, but the abatement rate was 20 cents on the dollar.

Not only has the threshold not kept up with inflation since its introduction in December 2005 (based on inflation to the December 2022 quarter it should be $52,700) but also abatement applied now is 27 cents on the dollar, quite a significant increase. So there’s a lot of strain in this situation and it’s something I’m glad to see the Government is considering actively.

Low compliance option for tiny cash businesses

And finally, this week, something else from last week’s British budget, which again, I think has relevance for New Zealand, and that is consulting on expanding the so-called cash accounting regime, a simpler tax regime for smaller businesses.

The British initiative recognises that there are businesses which are not significant enterprises. They’re often one person operations, so they don’t derive significant amounts of income. But under present tax policy, they would have to prepare normal full accrual accounting. However, most of the time these operations are too busy running their businesses and operate everything basically on a cash basis.

So, ten years ago the UK introduced a low compliance regime for cash businesses, which said that those self-employed persons with income under £150,000 could drop into this regime. Under the regime income is taxable on receipt and expenses deductible when paid. There is no need to accrue for income and expenditure. Incidentally, the regime doesn’t worry itself too much about the niceties of depreciation. Basically, you can take a full deduction for capital assets. Last week’s UK Budget is planning to extend this regime.

I think something like this is well worth considering in the New Zealand context. It was something we talked about when I was on the Small Business Council. Inland Revenue has fenced around this issue for some time. I’ve also had intermittent discussions with Inland Revenue policy officials about a similar scheme.

Inland Revenue’s concerns centre on the fiscal costs and whether it could be too generous. On the other hand, how much free time would such a regime free up for those businesses who are often run by some pretty stressed individuals? I am sceptical that the fiscal cost is as great as Inland Revenue imagines. Its duty is to maintain the integrity of the tax system so its approach is not unreasonable.

Anyway, it’s something worth considering. In Britain, it’s only applicable to unincorporated businesses. But I think it’s easily adaptable for smaller enterprises, for example those with turnover below $500,000 per annum who are eligible for six-monthly GST filing.

To address some of Inland Revenue’s concerns, it could also introduce something like fixed deductions on the principle “You can drop into this regime, but here are the fixed amounts of deductions because we know in your type of business these are type of deductions we see and the average amount of expenditure in respect of those items.” It should have the data to support this approach.

I’ve occasionally spoken to Inland Revenue policy officials on this topic but progress on these sort of initiatives often gets interrupted when something like a pandemic or a flood turns up. At which point Inland Revenue’s attention rightly gets diverted to more immediate matters. Anyway, this is something for further consideration and I’ll be watching closely to see how it pans out in the UK. Maybe we might see something similar in New Zealand eventually.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

The Government introduces a surprise fringe benefit tax exemption

The potential implications for New Zealanders from the UK’s Spring Budget

Inland Revenue has now formally launched its campaign to improve tax compliance in the construction industry, which I first mentioned a couple of weeks back. Under the heading, “Take the stress out of tax” it is promoting a tax toolbox for tradies.

This is intended to provide the rules, resources and tools to enable people to get their tax position correct. Proclaiming “We’re here to help”, there’s a series of pre-recorded online seminars covering the most common topics, such as an introduction to business, a GST workshop and employers’ responsibilities. There’s also offers for more direct contact, such as a business advisory or social policy visit. And then there’s a reminder that people can also talk to tax agents or use accounting software to, “take the pressure off.”

The background notes released comment that 42% of construction industry taxpayers who are behind either in tax payments or in filings have a tax agent. So, the role of tax agents is seen as important and obviously Inland Revenue is hoping that the role of agents will expand.

There’s also a reminder that Inland Revenue has access to data, which, as it puts it, means “We have a good handle on what happens in the construction industry”, adding it’s never too late to do the right thing. And it goes on to suggest people should come forward if they’ve forgotten some income of past tax returns or maybe have overinflated their expenses.

This is a welcome initiative by Inland Revenue. The phrasing of the campaign “Take the stress out of tax” is a classic example of speaking softly but carrying a very big stick. My view is that too many people either underestimate or are unaware of just how much data is available to Inland Revenue. This campaign phrasing also touches on something of a paradox I’ve experienced when dealing with clients with tax arrears. They’re often relieved to discover after discussing the matter the position is nowhere near as bad as they had feared, and they can now sleep easier. And I expect I’m not the only tax agent to have observed that.

It will be interesting to see the outcomes from the campaign. And as always, we’ll keep you updated with developments.

Exemption from FBT for bicycles, e-bikes, e-scooters … and mobility scooters

Now, two weeks back, I discussed the so-called apps tax. This is part of the Finance and Expenditure Committee report back on the Taxation Annual Rates for 2022-2023 (Platform Economy and Remedial Matters) Bill (No.2). The updated bill included some provisions around the proposals to charge GST on services supplied by the likes of Uber and Airbnb. The bill also included clarifications to a proposed fringe benefit tax exemption for the use of public transport.

As part of the bill, over 400 submitters, including myself, made submissions proposing some form of FBT exemption for e-bikes and e-scooters. The officials report declined the submissions commenting,

“Our overall conclusion is that a specific FBT exemption for bicycles would increase the distortion between the taxation of transport benefits and other fringe benefits, reducing the overall fairness and coherence of the tax system and giving rise to integrity risks, impacting on the fiscal cost.

If Parliament wanted to increase the uptake of cycling to help achieve improved health outcomes and assist New Zealand to achieve emissions reductions, it would instead recommend a more transparent and potentially targeted subsidy specifically designed to achieve considered policy outcomes.”

This is Inland Revenue’s boilerplate for “Nah, go away. We don’t like subsidies and special tax exemptions.”

That was then. But in what has become something of a pattern following Chris Hipkins’ elevation to Prime Minister, this week the Government has released a Supplementary Order Paper for the bill, which now introduces an exemption from FBT for bicycles, e-bikes, e-scooters and mobility scooters.

According to Revenue Minister David Parker the Government “considers that there is a public good to be gained from encouraging low emission transport” and “This measure will support New Zealand’s shift to more sustainable transport options and encourage employers to provide further sustainable and climate-friendly transport options for their staff.”

The bill includes a regulation making power which would specify the maximum cost of the exemption and the specifications to qualify. When I made my submission, I suggested a cap of about $4,000 should apply. It will be interesting to see what will be the maximum available under the exemption and how many employers make use of it, which will come into force on 1st April.

An English Budget and why it’s interesting here

On Wednesday night, the British Government unveiled its Spring Budget. This is a far less dramatic affair than the Autumn Statement last September, just after the Queen died, which led to the downfall of Liz Truss. This time the Chancellor of the Exchequer (Finance Minister) Jeremy Hunt has gone for something rather more cautious in its approach with one or two twists.

I was actually surprised there weren’t any moves around restricting the availability of non-residents to make use of the Personal Allowances exemption, or just generally increase the taxation of non-residents. That’s something I’ve seen other countries do. Australia is a very good example of where that happens. A cynic might say that’s because some of those non-residents are Conservative Party donors. But cynicism aside, given the financial pressures that the British government faces, not kicking over the stone and looking, is a bit surprising,

For example, there weren’t any changes to the controversial non domiciled or “Non-dom” scheme which gives a tax advantage on foreign income for people who are not tax-domiciled in the UK (including Prime Minister Rishi Sunak’s wife). (Most New Zealanders would qualify for this exemption).

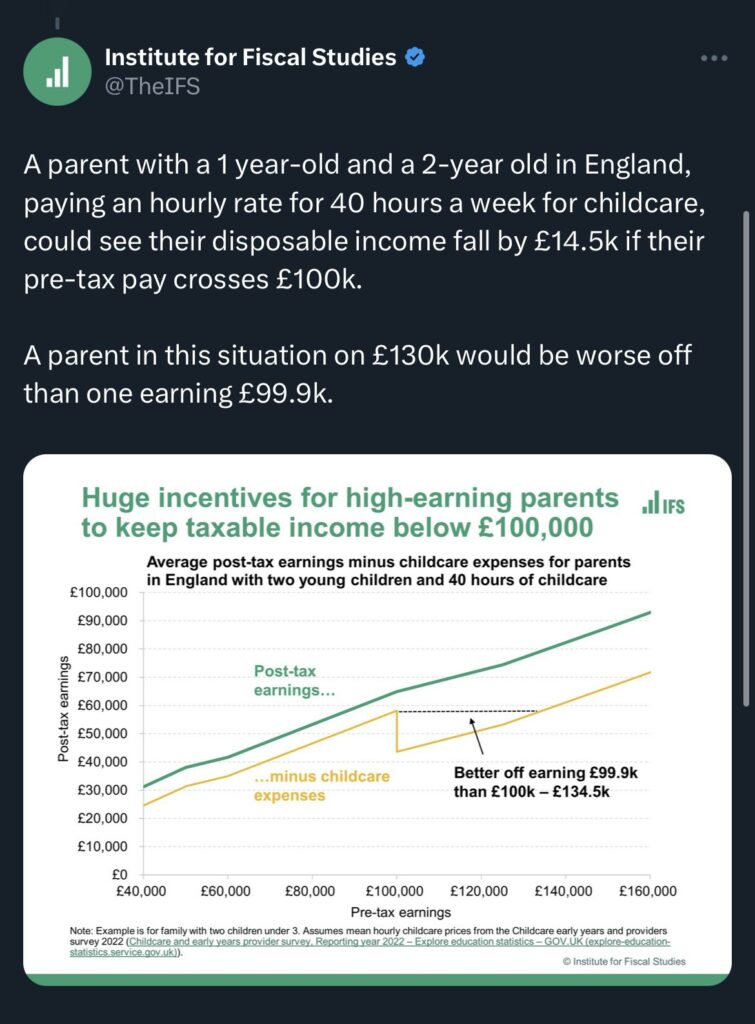

But what has perhaps attracted a fair bit of interest here was an excellent proposal, to provide and support up to 30 hours each week of free childcare support for working parents with children now aged between nine months and three years. Basically, free childcare will be available from between the ages of nine months and when children go to school. The National Party has recently announced proposals boosting childcare access.

There is a kicker to this in that it’s not available to anyone whose adjusted income is above £100,000. Basically, if someone earns more than £100,000, then all of those childcare costs they might have received are clawed back. Essentially, they don’t get back into the same net position until their income rises to £191,000. A 100% effective marginal tax rate will apply.

Now, you might well say, and I have to agree with you, that income of over £100,000 is a nice problem to have. However, it highlights a similar issue we have in our tax system in relation to clawback of Working for Families tax credits that effectively people on what modest incomes face higher than expected marginal tax rates. The clawback kicks in at a rate of 27 cents per dollar of income above $42,700.

I would hope whoever’s in Government will look seriously at this question of the clawback, the amount applicable and the threshold.

Of more direct interest to some New Zealanders is a change to what is known as the Lifetime Allowance Charge. Now, this is a controversial move that was brought in some years back because Britain has generous tax exemptions for pensions contributions. Consequently, some had accumulated very substantial pension pots tax free. To counter this, the Lifetime Allowance Charge was introduced, which imposed a charge which could be as high as 55% where the accumulated funds were above a threshold (£1,073,100).

The Lifetime Allowance Charge will be removed from 6th April and will be abolished in a future finance bill. Apparently up to 1.4 million people were caught by this. I know of several clients within this group. So they were considering their options about when and how to withdraw funds from their UK pensions. The removal of the charge means they may wish to reconsider their options.

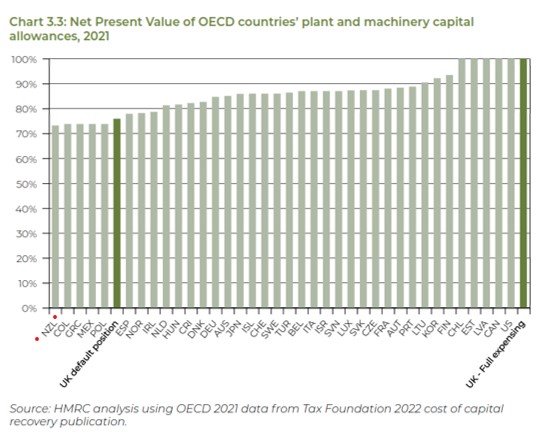

But the other thing that was particularly interesting to me is, and I think for our economy at wide was the decision to allow full expensing for capital assets acquired up to £1 million per year. Under this “Investment Allowance”, a first year allowance of 100% will be available up to the £1 million threshold. The idea is to encourage investment.

This is a topic that comes up in discussions down here. But what caught my eye was a graph produced as part of the background papers showing the net present value of all OECD countries plant and machinery capital allowances as of 2021.

As you can see under the present previous tax treatment, the UK would have been 33rd in the OECD. By going to full expensing, it moves up to be jointly top of the OECD. However, what caught my eye is that New Zealand is bottom of the OECD.

The question therefore arises whether we ought to be looking at our capital allowances regime. A similar type of initiative would be expensive, there’s no doubt about that. That’s one of the main reasons cited against such initiatives. But on the other hand, Britain has made this move because it wants to boost productivity and we know we’ve got problems with productivity.

So, here’s another challenge for the Finance Minister, Grant Robertson, to be considering right now. How do you boost our productivity? Is something similar to the UK investment allowance worth considering? We will see how that plays out in the UK. I see speculation about what might be in our budget in May is already emerging. Increasing capital allowance deductions is something I’m sure is under consideration. However, I’m also, to be honest, sceptical that we’ll see anything in the Budget.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Plenty to consider in Inland Revenue’s latest Interpretation Statement on tax avoidance

Working from home allowances updated

GST and Donation Tax Credit fraudsters convicted

Last year, I covered the Supreme Court decision in Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. To recap, Frucor had entered into a series of arrangements mainly for the benefit of its overseas parent. However, in the eyes of the Commissioner these arrangements represented tax avoidance. By a majority of 4 to 1, the Supreme Court ruled that the arrangements did indeed represent tax avoidance, and they also met the threshold for the imposition of shortfall penalties totalling $3.8 million. What was also of particular note here was the very strong dissenting judgement from Justice Glazebrook, which was completely at odds with the majority opinion.

Following the Supreme Court decision, Inland Revenue have now released an updated Interpretation Statement IS23/01 Tax avoidance and the interpretation of the general anti avoidance provisions of sections BG 1 and GA 1 of the Income Tax Act 2007. This 138-page Interpretation Statement is accompanied by a nine-page fact sheet and two Questions We’ve Been Asked covering income tax scenarios on tax avoidance, which amount to another 50 pages or so. A fair amount of material to work through.

The statement sets out the Commissioner’s approach to the application of Section BG 1 and then explains how under the related section J1 the Commissioner may act to counter it. And counter any tax advantage that a person has obtained from a tax avoidance arrangement. This Interpretation Statement is also relevant to the general anti-avoidance provisions in section 76 of the Goods and Services Tax Act 1985. This Interpretation Statement also replaces the previous Interpretation Statement is 13 zero one issued on 13 2nd June 2013.

The statement sets out the Commissioner’s approach to applying section BG1 and then explains how under the related section GA1 the Commissioner may act to counteract any tax advantage that a person a obtains from a tax avoidance arrangement. The Statement is also relevant for the general anti avoidance provision in Section 76 of the Goods and Services Tax Act 1985. It replaces the Commissioners previous Interpretation Statement IS13/01 issued on 13th June 2013

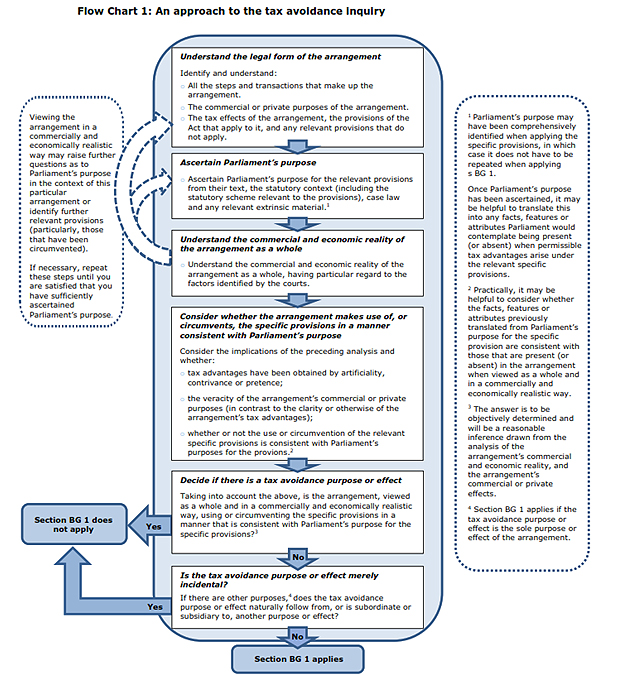

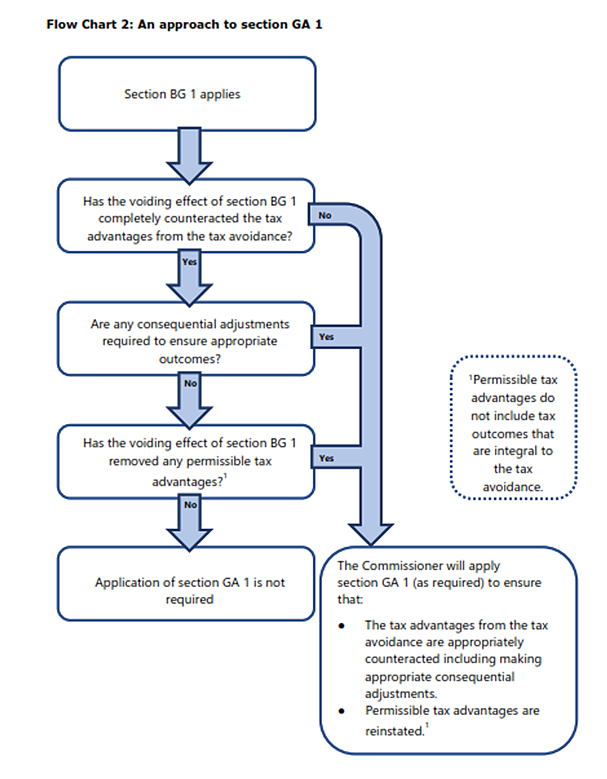

For those unfamiliar with these provisions, section BG1 is the main anti avoidance provision in the Income Tax Act. If applicable it will void a tax avoidance arrangement for income tax purposes. The related section GA1 then enables the Commissioner to make adjustments where an arrangement voided under section BG1 has not “appropriately counteracted” any tax advantages arising under the tax avoidance arrangement.

The key case relating to these anti avoidance provisions is the Supreme Court decision in Ben Nevis Forestry Ventures Limited in 2008. In that decision the Supreme Court adopted the principle of Parliamentary Contemplation in determining how the anti-avoidance provisions were to be applied. In brief Parliamentary Contemplation requires deciding whether the arrangement when viewed as a whole and in a commercially and economically realistic way makes use of or circumvents specific provisions in a manner consistent with parliament’s purpose. If not, the arrangement will have a tax avoidance purpose or effect. Subsequent to the Ben Nevis decision this principle of Parliamentary Contemplation was applied in the well-known Penny and Hooper case, and again in the Frucor decision.

It would be foolish to think these tax avoidance provisions only apply to major corporates. as I’ve just mentioned the principles were relevant in the Penny Hooper decisions and at last week ATAINZ conference the point was made that section BG1 could be applied in circumstances where a person’s lifestyle appears to rely on payments and distributions from a trust because it is in excess of that person’s reported salary.

Just as an aside, apparently in March 2021, almost $11 billion in dividends were paid prior to the increase in the top personal tax rate to 39%, with effect from 1st of April 2021. Now, that is more than four times greater than the usual amount of dividends paid at that time of year. I understand Inland Revenue is discussing the pattern of distributions with some tax agents.

The issue tax agents, advisers and clients should be aware of is where there is no regular pattern of distributions, even though profits were available, but suddenly there’s a very big distribution in this particular year. You could be vulnerable to Inland Revenue looking at that and saying, “Well, you paid a big dividend in March 2021, but you haven’t paid similar dividends in March 22 or March 23. Why is that? Nothing to do with the new 39% personal tax rate?” So just to reinforce these tax avoidance provisions, the case law may generally involve large corporates, but they are very relevant to small and medium enterprises.

Fortunately, there’s some good examples accompanying the Interpretation Statement and give you guidance as to where the Inland Revenue think the boundary might apply. For example, and this is a very common scenario, a company is wholly owned by a family trust. Over some years the trust has advanced $1 million to the company as shareholder advances on an interest free repayment on demand basis. The company has then used these funds to finance its business operations for the purpose of deriving assessable income.

The trustees decide to demand repayment of the full amount of the loan. In order to make that repayment the company borrows $1 million from a third-party lender at market interest rates secured over the assets of the trust. The $1 million loan is then used to repay the shareholder advances. The company deducts the cost of borrowing from its income. Meanwhile, the trustees have used the funds to purchase a holiday home for the trust’s beneficiaries.

As I said, this is a not uncommon scenario. But does it represent tax avoidance? No, according to the Commissioner. Which is a relief but be careful of relying on that particular set of circumstances, there may be a little twist in your tale, which may interest the Commissioner.

Another example is where a taxpayer with a marginal rate of 39% invests in a portfolio investment entity where the maximum prescribed investor rate is 28%. This would not constitute tax avoidance because the tax advantage of the maximum prescribed investor rate of 28% is within Parliament’s contemplation.

On the other hand, an example is given of an investor whose tax rate is 39%. He borrows funds from a bank to invest in a Portfolio Investment Entity (PIE) sponsored by the same bank. The policy of this PIE is to invest all funds in New Zealand dollar interest-bearing two-year deposits with the bank.

In this situation, this arrangement would represent tax avoidance. The key facts being the somewhat circular nature of the investment, but critically the fact the return is less than the cost of borrowing, resulting in a pre-tax negative, i.e. a loss position, but a post-tax positive net return. Once you look at the interest earned and the tax rate 28% tax rate, there’s a deduction available to the investor at 39% effectively. But the PIE income is only taxed at 28%.

This got me thinking because it suggests the well-known practice of negative gearing to purchase investment properties might in some circumstances represent tax avoidance. Now, this is less likely following the introduction of the loss ring-fencing rules and interest limitation rules in 2019 and 2021, respectively. But it’s another case where you ought to think carefully about how Inland Revenue might view a particular transaction.

As you can see, there’s a considerable amount of material and reading to work through including some useful flow charts (see below). At a minimum, I would suggest reading the Fact Sheet and the two Questions We’ve Been Asked which accompanied the Interpretation Statement.

You can also find some excellent commentary by the Big Four accounting firms. They’re always worth reading on these matters as they’ve got the resources to really go in and consider what these Interpretation Statements might mean. (And no doubt it’s particularly relevant for their clients).

Like some, I have my reservations about the Parliamentary Contemplation test. I think it was Rodney Hide who remarked about the principle “When I was in Parliament, most of the time I was contemplating what I was going to have for dinner”. Joking aside, I feel we should be approaching the test with some caution. I also think Justice Glazebrook’s dissent in Frucor raised valid concerns about how these provisions would apply. As I mentioned at the time, she comes from a very experienced commercial and tax background which is one reason why her dissent was raised a few eyebrows in the tax world.

Notwithstanding all of that, the Frucor and Ben Nevis cases are the law. And with the release of this Interpretation Statement and related material, taxpayers now should have a clearer idea where the boundaries lie. More examples from Inland Revenue around where they see the boundaries applying would be a great help in continuing to clarify the position. As always, we’ll bring you developments as they emerge.

Reimbursement for working from home

Now, moving on, we’ve discussed in the past how the impact of the pandemic and the resulting shift to more people working from home meant Inland Revenue had to quickly reconsider the treatment of reimbursing payments made to employees who work from home and for using their own phones and other electronic devices as part of their employment. Inland Revenue released a series of determinations giving some guidance as to the appropriate level of reimbursement.

Inland Revenue has just issued an updated determination which will, once it’s gone through consultation, apply from 1st April. It basically updates these previous determinations and gives a little bit more leeway in terms of the amounts allowed. The reimbursement allowance for employees working from home has increased from $15 per week to $20 per week. The previous limit of $5 per week for person use of telecommunications tools is now $7 a week. I feel these amounts are on the low side, but at least Inland Revenue is revisiting the matter and updating them to take account of inflation. So that’s welcome.

Jail for tax fraud

And finally this week news about convictions involving tax fraud. Firstly, a former developer who apparently lived in Manhattan before he migrated here in 2016 on an entrepreneur residency visa, has just been jailed for tax fraud relating to $1.5 million in fraudulent GST refunds. He had bought a vineyard in Canterbury and then filed fraudulent GST returns between April 2017 and April 2021 in relation to the purchase and operation of this vineyard. He received over $1.3 million in GST refunds, but a further $175,000 was withheld once Inland Revenue realised what was happening in April 2021.

He’s been jailed for a total of three years and seven months. One other thing of note is Inland Revenue has taken court action to recover what was fraudulently obtained. Unusually it also took a high court freezing order out and had a receiver appointed over the assets of the vineyard owning company. So good move from Inland Revenue. That’s what we expect them to be doing.

The case does raise an issue though, because it was four years before Inland Revenue detected this fraud. And so, again, you just wonder that hopefully this was because during this period it was going through its Business Transformation program. So, you would hope that now Inland Revenue, with its enhanced capabilities, is picking up on these frauds much quicker.

In a related release, five members of the Samoan Assembly of God Church in Manukau have been sentenced to community detention and ordered to repay the money they received after they made false donation tax credit claims worth almost $170,000. They apparently used not only false donation credits for themselves, but also asked other individuals, usually members of their own congregation for personal information, including their IRD numbers. They then using these details issued a series of false donation receipts. The fraud was detected by Inland Revenue and the five were charged. All have pleaded guilty and received various sentences mostly involving community detention but also reparations and repayment of the funds claimed.

I often see a lot of feedback around the charitable exemption particularly in relation to businesses. It’s a touchy point. One of the areas where the Tax Working Group had concerns was about whether the donations once received were actually being applied for charitable purposes.

Now, I don’t know whether this particular case is just one of those scenarios where Inland Revenue came across it and acted or it’s part of a general operation where it’s looking more closely at what’s happening with charitable donations and whether in fact, they’re being applied to charitable purposes. We’ll find out in due course.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!