The Government introduces a surprise fringe benefit tax exemption

The potential implications for New Zealanders from the UK’s Spring Budget

Inland Revenue has now formally launched its campaign to improve tax compliance in the construction industry, which I first mentioned a couple of weeks back. Under the heading, “Take the stress out of tax” it is promoting a tax toolbox for tradies.

This is intended to provide the rules, resources and tools to enable people to get their tax position correct. Proclaiming “We’re here to help”, there’s a series of pre-recorded online seminars covering the most common topics, such as an introduction to business, a GST workshop and employers’ responsibilities. There’s also offers for more direct contact, such as a business advisory or social policy visit. And then there’s a reminder that people can also talk to tax agents or use accounting software to, “take the pressure off.”

The background notes released comment that 42% of construction industry taxpayers who are behind either in tax payments or in filings have a tax agent. So, the role of tax agents is seen as important and obviously Inland Revenue is hoping that the role of agents will expand.

There’s also a reminder that Inland Revenue has access to data, which, as it puts it, means “We have a good handle on what happens in the construction industry”, adding it’s never too late to do the right thing. And it goes on to suggest people should come forward if they’ve forgotten some income of past tax returns or maybe have overinflated their expenses.

This is a welcome initiative by Inland Revenue. The phrasing of the campaign “Take the stress out of tax” is a classic example of speaking softly but carrying a very big stick. My view is that too many people either underestimate or are unaware of just how much data is available to Inland Revenue. This campaign phrasing also touches on something of a paradox I’ve experienced when dealing with clients with tax arrears. They’re often relieved to discover after discussing the matter the position is nowhere near as bad as they had feared, and they can now sleep easier. And I expect I’m not the only tax agent to have observed that.

It will be interesting to see the outcomes from the campaign. And as always, we’ll keep you updated with developments.

Exemption from FBT for bicycles, e-bikes, e-scooters … and mobility scooters

Now, two weeks back, I discussed the so-called apps tax. This is part of the Finance and Expenditure Committee report back on the Taxation Annual Rates for 2022-2023 (Platform Economy and Remedial Matters) Bill (No.2). The updated bill included some provisions around the proposals to charge GST on services supplied by the likes of Uber and Airbnb. The bill also included clarifications to a proposed fringe benefit tax exemption for the use of public transport.

As part of the bill, over 400 submitters, including myself, made submissions proposing some form of FBT exemption for e-bikes and e-scooters. The officials report declined the submissions commenting,

“Our overall conclusion is that a specific FBT exemption for bicycles would increase the distortion between the taxation of transport benefits and other fringe benefits, reducing the overall fairness and coherence of the tax system and giving rise to integrity risks, impacting on the fiscal cost.

If Parliament wanted to increase the uptake of cycling to help achieve improved health outcomes and assist New Zealand to achieve emissions reductions, it would instead recommend a more transparent and potentially targeted subsidy specifically designed to achieve considered policy outcomes.”

This is Inland Revenue’s boilerplate for “Nah, go away. We don’t like subsidies and special tax exemptions.”

That was then. But in what has become something of a pattern following Chris Hipkins’ elevation to Prime Minister, this week the Government has released a Supplementary Order Paper for the bill, which now introduces an exemption from FBT for bicycles, e-bikes, e-scooters and mobility scooters.

According to Revenue Minister David Parker the Government “considers that there is a public good to be gained from encouraging low emission transport” and “This measure will support New Zealand’s shift to more sustainable transport options and encourage employers to provide further sustainable and climate-friendly transport options for their staff.”

The bill includes a regulation making power which would specify the maximum cost of the exemption and the specifications to qualify. When I made my submission, I suggested a cap of about $4,000 should apply. It will be interesting to see what will be the maximum available under the exemption and how many employers make use of it, which will come into force on 1st April.

An English Budget and why it’s interesting here

On Wednesday night, the British Government unveiled its Spring Budget. This is a far less dramatic affair than the Autumn Statement last September, just after the Queen died, which led to the downfall of Liz Truss. This time the Chancellor of the Exchequer (Finance Minister) Jeremy Hunt has gone for something rather more cautious in its approach with one or two twists.

I was actually surprised there weren’t any moves around restricting the availability of non-residents to make use of the Personal Allowances exemption, or just generally increase the taxation of non-residents. That’s something I’ve seen other countries do. Australia is a very good example of where that happens. A cynic might say that’s because some of those non-residents are Conservative Party donors. But cynicism aside, given the financial pressures that the British government faces, not kicking over the stone and looking, is a bit surprising,

For example, there weren’t any changes to the controversial non domiciled or “Non-dom” scheme which gives a tax advantage on foreign income for people who are not tax-domiciled in the UK (including Prime Minister Rishi Sunak’s wife). (Most New Zealanders would qualify for this exemption).

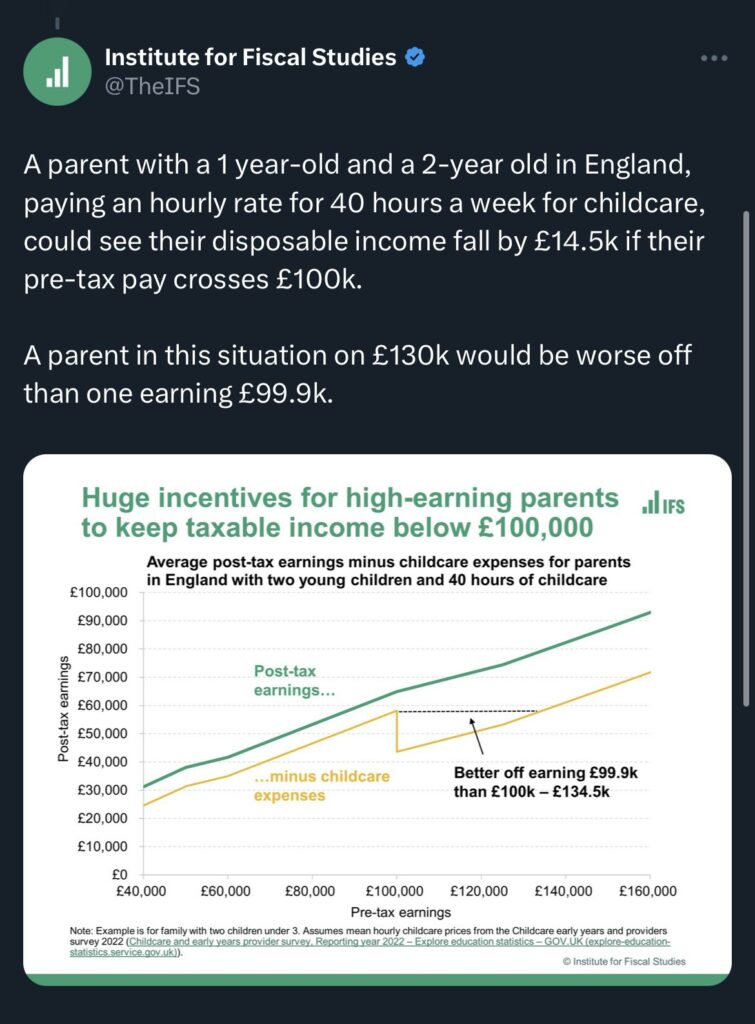

But what has perhaps attracted a fair bit of interest here was an excellent proposal, to provide and support up to 30 hours each week of free childcare support for working parents with children now aged between nine months and three years. Basically, free childcare will be available from between the ages of nine months and when children go to school. The National Party has recently announced proposals boosting childcare access.

There is a kicker to this in that it’s not available to anyone whose adjusted income is above £100,000. Basically, if someone earns more than £100,000, then all of those childcare costs they might have received are clawed back. Essentially, they don’t get back into the same net position until their income rises to £191,000. A 100% effective marginal tax rate will apply.

Now, you might well say, and I have to agree with you, that income of over £100,000 is a nice problem to have. However, it highlights a similar issue we have in our tax system in relation to clawback of Working for Families tax credits that effectively people on what modest incomes face higher than expected marginal tax rates. The clawback kicks in at a rate of 27 cents per dollar of income above $42,700.

I would hope whoever’s in Government will look seriously at this question of the clawback, the amount applicable and the threshold.

Of more direct interest to some New Zealanders is a change to what is known as the Lifetime Allowance Charge. Now, this is a controversial move that was brought in some years back because Britain has generous tax exemptions for pensions contributions. Consequently, some had accumulated very substantial pension pots tax free. To counter this, the Lifetime Allowance Charge was introduced, which imposed a charge which could be as high as 55% where the accumulated funds were above a threshold (£1,073,100).

The Lifetime Allowance Charge will be removed from 6th April and will be abolished in a future finance bill. Apparently up to 1.4 million people were caught by this. I know of several clients within this group. So they were considering their options about when and how to withdraw funds from their UK pensions. The removal of the charge means they may wish to reconsider their options.

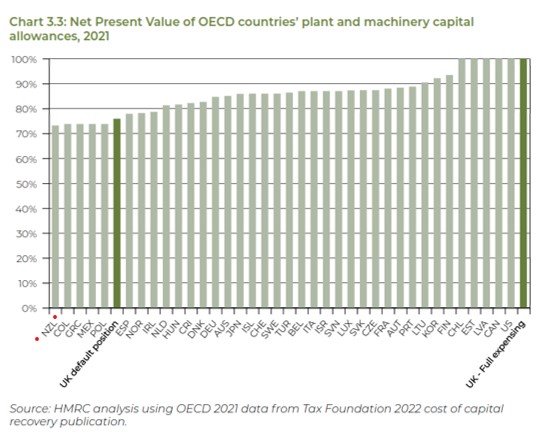

But the other thing that was particularly interesting to me is, and I think for our economy at wide was the decision to allow full expensing for capital assets acquired up to £1 million per year. Under this “Investment Allowance”, a first year allowance of 100% will be available up to the £1 million threshold. The idea is to encourage investment.

This is a topic that comes up in discussions down here. But what caught my eye was a graph produced as part of the background papers showing the net present value of all OECD countries plant and machinery capital allowances as of 2021.

As you can see under the present previous tax treatment, the UK would have been 33rd in the OECD. By going to full expensing, it moves up to be jointly top of the OECD. However, what caught my eye is that New Zealand is bottom of the OECD.

The question therefore arises whether we ought to be looking at our capital allowances regime. A similar type of initiative would be expensive, there’s no doubt about that. That’s one of the main reasons cited against such initiatives. But on the other hand, Britain has made this move because it wants to boost productivity and we know we’ve got problems with productivity.

So, here’s another challenge for the Finance Minister, Grant Robertson, to be considering right now. How do you boost our productivity? Is something similar to the UK investment allowance worth considering? We will see how that plays out in the UK. I see speculation about what might be in our budget in May is already emerging. Increasing capital allowance deductions is something I’m sure is under consideration. However, I’m also, to be honest, sceptical that we’ll see anything in the Budget.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Plenty to consider in Inland Revenue’s latest Interpretation Statement on tax avoidance

Working from home allowances updated

GST and Donation Tax Credit fraudsters convicted

Last year, I covered the Supreme Court decision in Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. To recap, Frucor had entered into a series of arrangements mainly for the benefit of its overseas parent. However, in the eyes of the Commissioner these arrangements represented tax avoidance. By a majority of 4 to 1, the Supreme Court ruled that the arrangements did indeed represent tax avoidance, and they also met the threshold for the imposition of shortfall penalties totalling $3.8 million. What was also of particular note here was the very strong dissenting judgement from Justice Glazebrook, which was completely at odds with the majority opinion.

Following the Supreme Court decision, Inland Revenue have now released an updated Interpretation Statement IS23/01 Tax avoidance and the interpretation of the general anti avoidance provisions of sections BG 1 and GA 1 of the Income Tax Act 2007. This 138-page Interpretation Statement is accompanied by a nine-page fact sheet and two Questions We’ve Been Asked covering income tax scenarios on tax avoidance, which amount to another 50 pages or so. A fair amount of material to work through.

The statement sets out the Commissioner’s approach to the application of Section BG 1 and then explains how under the related section J1 the Commissioner may act to counter it. And counter any tax advantage that a person has obtained from a tax avoidance arrangement. This Interpretation Statement is also relevant to the general anti-avoidance provisions in section 76 of the Goods and Services Tax Act 1985. This Interpretation Statement also replaces the previous Interpretation Statement is 13 zero one issued on 13 2nd June 2013.

The statement sets out the Commissioner’s approach to applying section BG1 and then explains how under the related section GA1 the Commissioner may act to counteract any tax advantage that a person a obtains from a tax avoidance arrangement. The Statement is also relevant for the general anti avoidance provision in Section 76 of the Goods and Services Tax Act 1985. It replaces the Commissioners previous Interpretation Statement IS13/01 issued on 13th June 2013

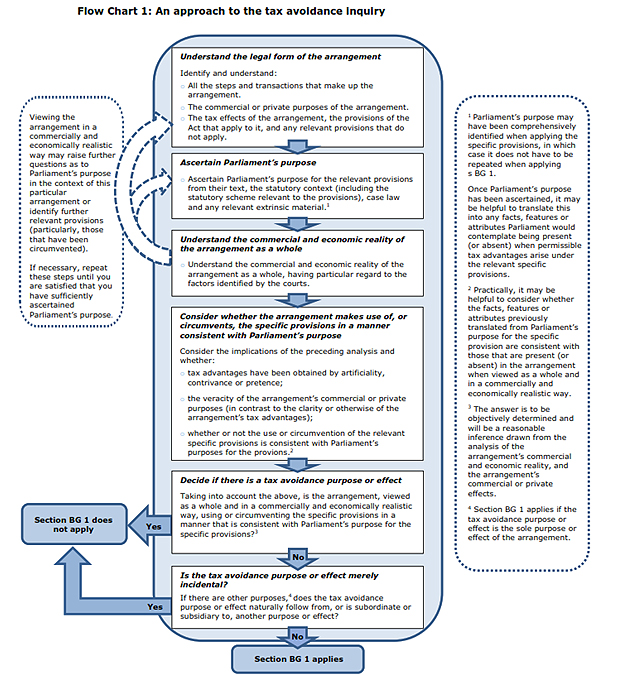

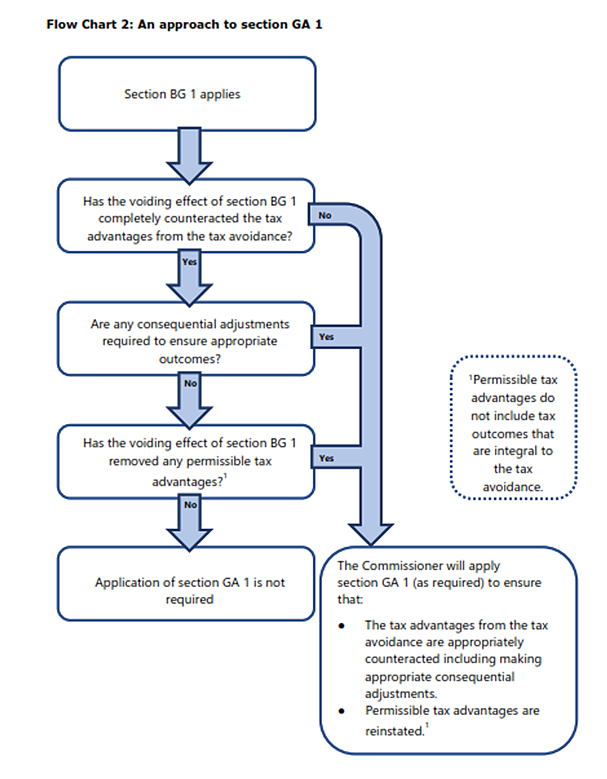

For those unfamiliar with these provisions, section BG1 is the main anti avoidance provision in the Income Tax Act. If applicable it will void a tax avoidance arrangement for income tax purposes. The related section GA1 then enables the Commissioner to make adjustments where an arrangement voided under section BG1 has not “appropriately counteracted” any tax advantages arising under the tax avoidance arrangement.

The key case relating to these anti avoidance provisions is the Supreme Court decision in Ben Nevis Forestry Ventures Limited in 2008. In that decision the Supreme Court adopted the principle of Parliamentary Contemplation in determining how the anti-avoidance provisions were to be applied. In brief Parliamentary Contemplation requires deciding whether the arrangement when viewed as a whole and in a commercially and economically realistic way makes use of or circumvents specific provisions in a manner consistent with parliament’s purpose. If not, the arrangement will have a tax avoidance purpose or effect. Subsequent to the Ben Nevis decision this principle of Parliamentary Contemplation was applied in the well-known Penny and Hooper case, and again in the Frucor decision.

It would be foolish to think these tax avoidance provisions only apply to major corporates. as I’ve just mentioned the principles were relevant in the Penny Hooper decisions and at last week ATAINZ conference the point was made that section BG1 could be applied in circumstances where a person’s lifestyle appears to rely on payments and distributions from a trust because it is in excess of that person’s reported salary.

Just as an aside, apparently in March 2021, almost $11 billion in dividends were paid prior to the increase in the top personal tax rate to 39%, with effect from 1st of April 2021. Now, that is more than four times greater than the usual amount of dividends paid at that time of year. I understand Inland Revenue is discussing the pattern of distributions with some tax agents.

The issue tax agents, advisers and clients should be aware of is where there is no regular pattern of distributions, even though profits were available, but suddenly there’s a very big distribution in this particular year. You could be vulnerable to Inland Revenue looking at that and saying, “Well, you paid a big dividend in March 2021, but you haven’t paid similar dividends in March 22 or March 23. Why is that? Nothing to do with the new 39% personal tax rate?” So just to reinforce these tax avoidance provisions, the case law may generally involve large corporates, but they are very relevant to small and medium enterprises.

Fortunately, there’s some good examples accompanying the Interpretation Statement and give you guidance as to where the Inland Revenue think the boundary might apply. For example, and this is a very common scenario, a company is wholly owned by a family trust. Over some years the trust has advanced $1 million to the company as shareholder advances on an interest free repayment on demand basis. The company has then used these funds to finance its business operations for the purpose of deriving assessable income.

The trustees decide to demand repayment of the full amount of the loan. In order to make that repayment the company borrows $1 million from a third-party lender at market interest rates secured over the assets of the trust. The $1 million loan is then used to repay the shareholder advances. The company deducts the cost of borrowing from its income. Meanwhile, the trustees have used the funds to purchase a holiday home for the trust’s beneficiaries.

As I said, this is a not uncommon scenario. But does it represent tax avoidance? No, according to the Commissioner. Which is a relief but be careful of relying on that particular set of circumstances, there may be a little twist in your tale, which may interest the Commissioner.

Another example is where a taxpayer with a marginal rate of 39% invests in a portfolio investment entity where the maximum prescribed investor rate is 28%. This would not constitute tax avoidance because the tax advantage of the maximum prescribed investor rate of 28% is within Parliament’s contemplation.

On the other hand, an example is given of an investor whose tax rate is 39%. He borrows funds from a bank to invest in a Portfolio Investment Entity (PIE) sponsored by the same bank. The policy of this PIE is to invest all funds in New Zealand dollar interest-bearing two-year deposits with the bank.

In this situation, this arrangement would represent tax avoidance. The key facts being the somewhat circular nature of the investment, but critically the fact the return is less than the cost of borrowing, resulting in a pre-tax negative, i.e. a loss position, but a post-tax positive net return. Once you look at the interest earned and the tax rate 28% tax rate, there’s a deduction available to the investor at 39% effectively. But the PIE income is only taxed at 28%.

This got me thinking because it suggests the well-known practice of negative gearing to purchase investment properties might in some circumstances represent tax avoidance. Now, this is less likely following the introduction of the loss ring-fencing rules and interest limitation rules in 2019 and 2021, respectively. But it’s another case where you ought to think carefully about how Inland Revenue might view a particular transaction.

As you can see, there’s a considerable amount of material and reading to work through including some useful flow charts (see below). At a minimum, I would suggest reading the Fact Sheet and the two Questions We’ve Been Asked which accompanied the Interpretation Statement.

You can also find some excellent commentary by the Big Four accounting firms. They’re always worth reading on these matters as they’ve got the resources to really go in and consider what these Interpretation Statements might mean. (And no doubt it’s particularly relevant for their clients).

Like some, I have my reservations about the Parliamentary Contemplation test. I think it was Rodney Hide who remarked about the principle “When I was in Parliament, most of the time I was contemplating what I was going to have for dinner”. Joking aside, I feel we should be approaching the test with some caution. I also think Justice Glazebrook’s dissent in Frucor raised valid concerns about how these provisions would apply. As I mentioned at the time, she comes from a very experienced commercial and tax background which is one reason why her dissent was raised a few eyebrows in the tax world.

Notwithstanding all of that, the Frucor and Ben Nevis cases are the law. And with the release of this Interpretation Statement and related material, taxpayers now should have a clearer idea where the boundaries lie. More examples from Inland Revenue around where they see the boundaries applying would be a great help in continuing to clarify the position. As always, we’ll bring you developments as they emerge.

Reimbursement for working from home

Now, moving on, we’ve discussed in the past how the impact of the pandemic and the resulting shift to more people working from home meant Inland Revenue had to quickly reconsider the treatment of reimbursing payments made to employees who work from home and for using their own phones and other electronic devices as part of their employment. Inland Revenue released a series of determinations giving some guidance as to the appropriate level of reimbursement.

Inland Revenue has just issued an updated determination which will, once it’s gone through consultation, apply from 1st April. It basically updates these previous determinations and gives a little bit more leeway in terms of the amounts allowed. The reimbursement allowance for employees working from home has increased from $15 per week to $20 per week. The previous limit of $5 per week for person use of telecommunications tools is now $7 a week. I feel these amounts are on the low side, but at least Inland Revenue is revisiting the matter and updating them to take account of inflation. So that’s welcome.

Jail for tax fraud

And finally this week news about convictions involving tax fraud. Firstly, a former developer who apparently lived in Manhattan before he migrated here in 2016 on an entrepreneur residency visa, has just been jailed for tax fraud relating to $1.5 million in fraudulent GST refunds. He had bought a vineyard in Canterbury and then filed fraudulent GST returns between April 2017 and April 2021 in relation to the purchase and operation of this vineyard. He received over $1.3 million in GST refunds, but a further $175,000 was withheld once Inland Revenue realised what was happening in April 2021.

He’s been jailed for a total of three years and seven months. One other thing of note is Inland Revenue has taken court action to recover what was fraudulently obtained. Unusually it also took a high court freezing order out and had a receiver appointed over the assets of the vineyard owning company. So good move from Inland Revenue. That’s what we expect them to be doing.

The case does raise an issue though, because it was four years before Inland Revenue detected this fraud. And so, again, you just wonder that hopefully this was because during this period it was going through its Business Transformation program. So, you would hope that now Inland Revenue, with its enhanced capabilities, is picking up on these frauds much quicker.

In a related release, five members of the Samoan Assembly of God Church in Manukau have been sentenced to community detention and ordered to repay the money they received after they made false donation tax credit claims worth almost $170,000. They apparently used not only false donation credits for themselves, but also asked other individuals, usually members of their own congregation for personal information, including their IRD numbers. They then using these details issued a series of false donation receipts. The fraud was detected by Inland Revenue and the five were charged. All have pleaded guilty and received various sentences mostly involving community detention but also reparations and repayment of the funds claimed.

I often see a lot of feedback around the charitable exemption particularly in relation to businesses. It’s a touchy point. One of the areas where the Tax Working Group had concerns was about whether the donations once received were actually being applied for charitable purposes.

Now, I don’t know whether this particular case is just one of those scenarios where Inland Revenue came across it and acted or it’s part of a general operation where it’s looking more closely at what’s happening with charitable donations and whether in fact, they’re being applied to charitable purposes. We’ll find out in due course.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Inland Revenue clarifies the GST treatment of a professional director’s fees

Treasury’s suggestions for financing the effects of climate and demographic change

The cyclone recovery efforts continue with the announcement of how $25 million of relief for the Tairāwhiti-East Coast and Hawke’s Bay regions are to be distributed. We are still waiting to hear about specific tax measures but I am aware that similar suggestions to those discussed in last week’s podcast have been made by other parties. It’s a question of wait and see so we will keep you informed of developments.

It so happens that the Accountants and Tax Agents Institute of New Zealand (ATAINZ) to which I belong was due to hold its annual conference in Napier this weekend. Despite the best efforts and will of everyone involved that was not possible. Instead ATAINZ organised a one-day online workshop on Friday.

The opening session presentation by Tony Morris, currently Inland Revenue’s acting Deputy Commissioner for customers and compliance had quite a number of interesting insights about the current state of Inland Revenue and its immediate and long term objectives.

Inland Revenue’s recently completed Business Transformation programme has given it a great foundation for its future operations. As Tony explained, its enhanced capability is now a real asset for the Government which means it is being asked to do more across government. An example would be the proposed income insurance scheme which would have been Inland Revenue’s responsibility if it had proceded. The Cost of Living payments is another example. On the other hand, responding to Government initiatives required Inland Revenue staff to be directed away from its core role.

Although COVID-19 continues to impact thousands of New Zealanders each week, Inland Revenue is now moving on from the immediate urgency of responding to the pandemic. Tony did observe that although demand for government services increased as a result of the pandemic, trust in Inland Revenue and other good government departments has fallen. Rebuilding that trust is a key objective.

“Restarting compliance”

Notwithstanding this, and the ongoing demands of the cyclone recovery, Inland Revenue is getting back to its core role and as Tony put it, “restarting compliance.” This month it is launching an initiative focused on the construction sector. Apparently 50,000 taxpayers in this sector, about half of whom are individuals, have some form of arrears either being behind in filing of returns or owe tax. Inland Revenue’s new campaign launching this month will focus on this group, obviously with the aim of ensuring that they get up to date with their filing and payment obligations.

Inland Revenue is currently also re-establishing its strategy for the next 10 years now that the Business Transformation programme is complete. No doubt we will hear more about this over the coming months, and I will bring you developments as they happen. For now those in the construction sector can expect to be hearing more from Inland Revenue very soon.

Objecting for the sake of it? because its election year?

Moving on, the Taxation (Annual Rates for 2022–23, Platform Economy, and Remedial Matters) Bill (No 2) was reported back to Parliament this week. This bill has hit the news headlines after the National Party came out objecting to what it called the “App tax”. This proposes GST will apply to services such as Airbnb and Uber which are provided via an offshore resident platform. Some minor changes have been made to the proposals by the Finance and Expenditure Committee, which are intended to take effect from 1 April 2024. However, National has indicated it would not proceed with these changes if it is elected later this year.

It would be interesting to see if National actually did overturn these changes because conceptually there is little difference between what is proposed and the imposition of GST on other services supplied by offshore providers such as Netflix, a change introduced in 2016 by the last National government.

Incidentally, the Green Party also had a dissenting view about the bill, this time in relation to the decision to not include active transport vehicles and services, such as e-bikes, scooters, and sharing schemes, used for travel to and from work in the exemption from FBT. Over 400 submissions also called for a FBT exemption for the provision of bicycles, including e-bikes. The Greens supported widening the exemptions as part of meeting the targets in the Transport Emissions Reduction Plan. “Nothing doing” was the response although the FBT exemption for public transport was clarified and widened in scope.

Not to be left out, the ACT Party opposed the bill on the basis “the tax rates set, and methodology are not agreeable to ACT as it is a regressive tax package and does not drive productivity or growth and continues to solidify our country as a high tax per GDP/capita.”

As I said in my first podcast of the year, it’s an election year so the politics of tax is more often in play. The Government has the numbers to pass the bill regardless of what National, ACT and the Greens might say.

Despite the disruptions of the Auckland Anniversary Weekend floods and Cyclone Gabrielle, Inland Revenue’s technical teams have been issuing a series of technical papers on a variety of issues. These include an important interpretation statement on tax avoidance which has been updated following the recent decision in Frucor. This interpretation statement came up as part of the ATAINZ workshop and I will discuss it in more detail next week.

GST on director/board fees

In the meantime, Inland Revenue has released three binding rulings discussing the GST treatment of directors’ fees and board members’ fees. These binding rulings have attracted interest because Inland Revenue has now determined that generally speaking, directors’ fees and board members’ fees are not subject to GST. This is a change from what has been generally thought to be the position. Inland Revenue’s now consider a person who provides only directorship (or board member) services is not eligible to be registered for GST.

The binding rulings are accompanied by an operational position on the question of professional directors and board members who are incorrectly registered for GST. In summary those persons who have incorrectly registered for GST will not be required to retrospectively deregister. However, any directors who are not carrying on a taxable activity must deregister with effect from 30 June 2023.

The group most likely to be affected are those professional directors who never had a separate taxable activity (for example as a consultant, lawyer or accountant). There may be other directors currently registered who did correctly register for GST because they were carrying on a separate taxable activity other than their professional directorships but who have subsequently ceased to carry on that other activity. If their only taxable supplies are from directorship fees they should now deregister.

As a colleague noted this hardly seems the most urgent of issues particularly when as we know Inland Revenue has been stretched because of the demands of the pandemic, cost of living and now Cyclone Gabrielle. However, it’s good to have this position clarified and a practical exit strategy for those incorrectly registered.

Preparing for major demographic change

Last week I discussed Te Hirohanga Mokopuna, Treasury’s combined statement on the long-term fiscal position and long-term insights briefing released in September 2021. To recap, Treasury outlined the fiscal challenges ahead for governments and projected the gap between expenditure and revenue will grow significantly as a result of demographic change and historical trends, in the absence of any offsetting action by governments. So, what “offsetting action” did Treasury suggest was possible.

One of the fiscal pressures is the rising cost of New Zealand Superannuation which is projected to grow from 5% of GDP now to 7.7% of GDP by 2061. That’s actually reasonably manageable compared with other OECD countries, but still represents a challenge. Treasury suggest a couple of options – raise the age of eligibility from 65 to 67 or reduce the rate at which New Zealand Superannuation grows, by linking it to inflation rather than wages.

Treasury also looked at a report prepared by Susan St John and Claire Dale in 2019 for the Commission for Financial Capability’s 2019 Review of Retirement Income policies. This proposed a tax-based clawback system. In essence this would be an updated version of the former Superannuation Surcharge which applied between 1985 and 1998. Under the proposal other gross income earned by pensioners would be subject to an alternative tax regime that has higher than usual tax rates. Consequently, there would be a break-even point above which it would not be financially advantageous to take New Zealand Superannuation. Depending on the tax rates applied this could be between $112,000 and $140,000. It’s interesting to see Treasury discussing this proposal, it indicates it’s now viewed as a serious policy alternative.

Section 2.5 of the Statement considers some alternatives for raising tax revenue. It notes “None of the options are enough on their own to fully address the fiscal challenges explored in earlier chapters.” The Statement noted that tax revenue might have to rise by 8% of GDP (or almost 25%) to meet the fiscal pressure. An increase of this size the statement notes

“…may not be desirable or even feasible to raise this much revenue within our current tax structure. Instead, tax changes of this size may require a more fundamental review of the structure and integrity of the tax system as a whole.”

Quite an understatement there, but at some point, just as happened after 1984, that fundamental review will have to happen.

Anyway, the Statement focuses on options around either increasing revenue from the existing tax system, broadening the tax base, or introducing new kinds of taxes.

Treasury modelled policy scenarios around raising additional revenue from personal income tax, either by increasing all personal income tax rates by one percentage point, or ten years of ‘fiscal drag’, where income tax thresholds are kept at their nominal value rather than rising with wage inflation. Fiscal drag means that more taxpayers and taxable income would be taxed in higher tax brackets over time.

Raising personal income tax rates by one percentage point (while thresholds rise with wage growth) would raise around 0.6% of GDP (currently about $2 billion) per year while 10 years of fiscal drag would build up every year it operates and raise around 1.0% of GDP (currently over $3.3 billion) annually.

Fiscal drag has in fact been the default option applied since 2010 when the last adjustment was made to tax rates and thresholds (other than the introduction of the 39% tax rate on 1st April 2021). It’s more than a little ironic to see Treasury go on to comment

“a significant period of fiscal drag could lead to a high proportion of individuals paying tax rates previously paid only by higher-income earners, which could undermine perceptions of fairness in the tax system.”

In my view for those earning around the average wage the failure to adjust tax rates for inflation for more than 10 years has undermined perceptions of fairness in the tax system.

What about introducing new taxes, for example increasing GST? To raise the equivalent of one percentage point on all personal income tax rates (0.6% of GDP) would require an increase in GST of roughly 1.5 percentage points that is to 16.5%. However, GST is seen a regressive tax for those on lower incomes. Furthermore, any rate rise would increase pressure to exempt certain goods from GST and therefore undermine the integrity of GST. On balance, Treasury, Inland Revenue and tax experts would probably put maintaining the integrity of GST ahead of exemptions and rate rises.

Treasury calculates that company income tax rates would have to rise by 6 percentage points to 34% to raise 0.6% of GDP. Given that the current headline tax rate of 28% is already quite high by international standards, such an increase would as Treasury notes be “likely to have relatively large economic effects, particularly to the extent that they lead to multinational companies restructuring profits away from New Zealand or reductions in investment and the capital stock.” So not really a viable alternative.

The Tax Working Group proposed a comprehensive capital gains tax which it estimated could raise around 1.2% of GDP a year. That estimate is probably too high given the subsequent increases in the bright-line test to 10 years. On the other hand, a CGT

“…could improve the allocative efficiency of saving and investment by ensuring more economic income is taxed neutrally, would be progressive, and would improve the integrity of the tax system.”

Higher effective tax rates for those on average earnings is one of the unfortunate by-products of the failure to introduce a CGT and one which was glossed over back in 2019. But as Treasury notes the issues around perceptions of the fairness of the tax system remain.

As is well known, The Opportunities Party has long promoted a land tax for the reasons Treasury acknowledges – “annual taxes on the unimproved value of land are generally considered to be highly efficient, simple to administer, and difficult to avoid.”

The briefing suggests 0.7% annual levy would raise 1% of GDP. New Zealand has had land tax in the past, but extensive lobbying by interested groups meant that over time exemptions were added and then increased gradually withering the tax take to insignificance. I think any tax reform will need to look at some form of land taxation but as we saw with the Tax Working Group’s CGT proposals there will be fierce pushback.

A net wealth tax is also discussed but as Treasury notes although “highly progressive, these taxes tend to be subject to a high level of avoidance and exemptions, and raise relatively little revenue” (between 0.1% and 1.1% of GDP in those OECD countries with such taxes – Switzerland is the country with the most comprehensive wealth tax).

An alternative might be the restoration of gift and death duties. These were once a significant source of taxation – in 1949 they represented 4.6% of the tax collected. Post 1949 however a series of National party governments increased the exemptions until like land tax it withered away. As Treasury notes “although such taxes often come with significant exemptions and integrity risks, their economic cost is likely to be relatively low although they do raise questions of fairness for those affected.” OECD countries with these taxes raise between 0.1% and 0.7% of GDP from them. The United Kingdom’s Inheritance Tax collected over £6 billion last financial year, double the amount from 10 years previously.

There’s a discussion about the impact of digital services taxes and the proposed OECD deal on multinational taxation but the tax raised once implemented is likely to be small. Far more opportunities exist with better compliance and as I said at the start of the podcast we can expect Inland Revenue to pick up its efforts here.

Finally, there’s environmental taxes. We raise less from such taxes than other OECD countries. It was just 1.3% of GDP in 2019, well below the OECD average of 2.1%. However, as Treasury notes

“Given that these taxes can induce changes in behaviour that reduce the tax base (and are often applied to activities that are in decline), they may not offer a substantial or sustainable additional source of tax revenue in the long term. They could, however, have broader benefits including supporting the accumulation of natural capital (by preventing environmental harm) and improving the wellbeing of the natural environment”.

This is a reasonable analysis which is why I believe any environmental taxes should be ring-fenced and recycled back to help climate change mitigation and adaptation.

To repeat Treasury’s key point – some form of fiscal adjustment involving a change in the tax base to spending will be required. None of the options suggested by Treasury will sound attractive to politicians seeking election but, in my view, making hard calls is part of the territory. I would hope that between now and the election the leaders and finance spokespersons for the main parties are interrogated in detail about the long-term issues identified by Treasury and how they propose to deal with them. I’ll be honest, I won’t be holding my breath but as always, we’ll bring you developments as they emerge.

That’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

what more can be done for victims of the recent bad weather disasters

thinking more broadly about the climate and demographic challenges ahead

The relief effort for the areas affected by Cyclone Gabrielle has picked up this past week. The government announcing a $50 million package for affected businesses, plus additional funding for the repairs of the roading network damaged by the cyclone.

Included in those reliefs is a temporary exemption from the Credit Contracts and Consumer Finance Act 2003 requirements, relaxing the requirements for banks to provide credit. This applies to the Gisborne, Hawke’s Bay and Tararua regions and enables banks and other lenders to quickly provide up to $10,000 in credit to affected businesses and individuals.

In terms of specific tax reliefs, as we mentioned last week, Inland Revenue has the ability to remit late payment penalties and also use of money interest for late payments on tax payments. The exemption for use of money interest runs through until 30th June. And then there is the Income Equalisation scheme we mentioned last week. That’s obviously going to be important for those eligible to use it, such as farmers and others with agricultural businesses on land. Just to reiterate, deposits for the March 2022 income year can now be made until 31st May, and withdrawals may also now be made on application.

Now, other things you can do if you want to help is making charitable donations to approved organisations. And there’s also the opportunity for businesses to gift trading stock as well and not be taxed for disposing of it below market value. This is something I think supermarkets, restaurants and farmers are already making use of this provision which was introduced as part of the COVID 19 response. It was due to expire on 31st March but an order has now been issued to extend it until 31st March 2024. Now that will be fairly useful in the short term.

Just to repeat a point I made last week, when you’re dealing with Inland Revenue, the best approach is to get in contact early and let them know what’s happening. Unfortunately, at the moment Inland Revenue’s offices in Napier and Gisborne are still closed. But if you’re in the affected areas, your best option is to call Inland Revenue on their dedicated helpline 0800 473566. Or you send a message via myIR using the key word “flood”.

That’s the main reliefs available although we don’t quite know how the $50 million business relief is to be distributed just yet but at least some help is on the way. What other things could be done from a tax perspective? I got some insights into that from a colleague, Stephen Diedericks, a tax agent in Hawke’s Bay. Based on the personal experiences of himself and other tax agents in the area he’s come back with some feedback on what’s going on and what could be done.

As he said, the issues they face are really numerous. First and foremost, positive cash flow is drying up. Then there are the seasonal farm workers who may have had jobs cancelled or they’re on the way here and have no accommodation to go to. I see there’s some changes to visa requirements underway which may be useful. There’s an enormous amount of damage to farm equipment and there are delays in obtaining new equipment. Even if you get a quick insurance pay out, getting replacement equipment may not be that easy. For example, Stephen mentions how one farmer placed an order this past week but will only receive delivery in 2024.

Then how do businesses support staff who’ve lost everything? Napier, as we know, was hit very hard. It so happened Cyclone Gabrielle coincided with Art Deco week, which is a big, big event for the region, and that’s not happening. As Stephen notes, volunteers have come and helped out and maybe some form of payment could be made to them? In his words, “rural farms are under water, crops are damaged. It could be more than one season for the land to recover.” And an unsurprising knock-on effect from that is food and vegetable prices for city-dwellers are likely to increase.

In terms of suggestions. Stephen and his colleagues believe there should be a six-month moratorium on all purchases and personal debt for those who have lost everything. He suggests providing easy access to KiwiSaver which is perhaps controversial, but can be done in cases of hardship. This would appear to be one of those situations, I would think. Basically, the point keeps being repeated. Cash injections to help businesses trying to get back on their feet and help the staff who may have had their homes destroyed or severely damaged.

A very important point also is some form of certainty with rent. Stephen’s view was that some form of rent holiday is required. The response by landlords in the wake of the pandemic was, shall we say, a little bit uneven. Some landlords, including my own, by the way, were willing to accommodate tenants who were affected, others less so. But I agree putting a rent moratorium in place would be very useful.

Then there’s the opportunity of reactivating the wage subsidy scheme. I know the Prime Minister has mentioned that this is a possibility. This is an off-the-shelf response we can embrace. My only caveat to using the wage subsidy is that, as we saw with the payments made during the COVID 19 response, some organisations took it who didn’t need it and then didn’t repay it. And then there were other organisations that took the payments but didn’t pass them on to employees. Personally, I favour getting payments directly to employees and as quickly as possible.

Anyway, notwithstanding the criticisms of the scheme, it was set up incredibly quickly paying promptly and was absolutely vital in that crunch period in March and April 2020. It’s there and it’s something we’ve done before, so we should be able to activate it again pretty easily.

Now in terms of specific tax responses, Stephen and his colleagues have a very good suggestion, which I totally endorse and that is to increase the low value asset limit. This is where this is the amount below which you can immediately depreciate the full cost of an item. Stephen and his colleagues suggest raising the threshold temporarily from its current $1,000 limit to $20,000. If you recall, back in 2020 it was increased to $5,000 for 12 months, and that was a welcome move. It helps businesses get replacement equipment, and that’s important at this stage.

Stephen is also supportive of the measures already taken by Inland Revenue about interest and penalty waivers. He suggested perhaps provisional tax payments could be suspended for the current tax year ending on 31st March and maybe also for the year to March 2024. But the key priority is to get cash in the hands of businesses immediately. “Just put it into the bank accounts. What’s needed is cash to pay bills.” And that’s the most important thing of all, is whatever is decided has to be done quickly. Everyone needs government assistance to happen as quickly as possible.

Other suggestions that might be made is obviously the wage subsidy. But I would think that the Government doesn’t want to use the wage subsidy, then the Small Business Cashflow Scheme, which was also hugely successful, is another mechanism still in place. It should be possible to open it up immediately to for affected businesses.

What I would suggest is that the amounts available are substantially increased. Under the scheme set up in 2020, there was a limit of an initial $10,000 plus up to $1,800 dollars per full time employee, up to a maximum of 50 full time employees. I think you need to more than double those limits because whereas COVID-19 was an event which interrupted businesses with Cyclone Gabrielle we’re talking about business interruption and physical destruction of property. Businesses affected will need more than $10,000 to get back on their feet as quickly as possible. I think, for example, you could lift the limits to say an initial $25,000 plus, say $4,500 per full time employee.

Another tax measure which we’ve used in the past is tax loss carry-back. If you remember, these rules were introduced temporarily in 2020, and allowed losses for the year ended 31st March 2021 to be carried back to the March 2020 year. There was some work done on making these a permanent part of the Income Tax Act, but work on that stopped I understand because of fiscal pressures.

Again, we’re facing something that needs immediate action and here’s something off the shelf we can use. All it would require is a Supplementary Order Paper to reintroduce the section for the current tax year and maybe the next year as well. I actually expect Inland Revenue is probably working on this at the moment.

Another possible mechanism that could be used again would be a variation on the Cost of Living payments. I know they were controversial because some payments went to the wrong people. But again, Inland Revenue ought to have the data to say, “Well, we know all these people live in the affected regions. So here’s $500 to every adult in that region.” An immediate cash drop to help.

And so, as I said, those are some of the options we can consider. And no doubt people will have some other ideas. And the key thing here is none of what I’ve mentioned is revolutionary or requires completely designing something from the ground up. They’re all mechanisms we’ve used previously and not so long ago and therefore should be able to reactivate. This is a major event, and we need to get relief to those affected as quickly as possible.

Thinking more broadly …

Now moving on, the debate has already begun about how to pay for this assistance and also further climate adaptation, which is now going to be required. It’s interesting to see a shift in thinking very rapidly on this stage. Now, in my view, this is a debate we should have been having for some time now. There are plenty of official reports which have alluded to the issue of the cost of dealing with climate adaptation and how to fund it.

And one I want to talk about for the rest of this podcast is Te Hirohanga Mokopuna in 2021, which is Treasury’s combined statement on the long-term fiscal position and long-term insights briefing. Treasury is required to produce these reports every four years. It was due in 2020 but got delayed to 2021 because of COVID. Obviously, when Te Hirohanga Mokopuna was released in September 2021, the effects of COVID 19 were high on the agenda.

But as the executive summary noted, “it is not only the COVID 19 pandemic that we must consider other economic and societal matters such as climate change and population ageing must also be factored into the long-term fiscal position of New Zealand.” These reports may take a very long-term view, looking at 40 years or more.

Treasury’s conclusion about COVID 19 response was quote.

“While the fiscal response to the COVID 19 pandemic has caused net debt to increase significantly, the Treasury views this response and current debt levels to be prudent. In any event, the Government’s fiscal response has helped prevent a deeper and longer lasting recession, which could have had long-term impacts on New Zealand’s wellbeing.”

After dealing with the immediate impact of COVID 19 the briefing then pivots to talk about climate change, which it notes

“… will impact the fiscal position through both the physical impacts of a changing climate, such as more frequent and severe weather events, and the transition to a net zero emissions economy by 2050. Climate change has started to impact New Zealand today, but the long-run effect is highly uncertain at this stage.

More frequent and severe extreme weather events and the gradual increase in temperature and sea levels will have economic and fiscal impacts in the future, which adaptation policy today could reduce.”

So, there you have it. In September 2021 Treasury pointed out the climate change scenario which we just encountered in the past three weeks firstly in Auckland with the Anniversary weekend floods and now with Cyclone Gabrielle was already happening. It’s here and we have to deal with it.

To be fair, it’s not just climate change the report is concerned about. It then discusses the impact of an ageing population, noting that 26% of the population is expected to be over 65 years old by 2060, compared with 16% by in 2020. Now what does that mean? Increased superannuation expenditure and rising health care costs. Treasury projects “the gap between expenditure and revenue will grow significantly as a result of demographic, demographic change and historical trends, in the absence of any offsetting action by governments.”

Treasury sees net debt increasing rapidly as a share of GDP by 2060. Its judgement is “there is currently no immediate need to reduce debt, but policy action will be necessary to reduce, achieve and maintain a sustainable debt trajectory over time. This will ensure that New Zealand is resilient to future shocks and future generations do not face an unduly large burden of debt.”

In my view we’ve arrived at the point where policy action is required right now. The Briefing then notes “Governments will need to decide how large an adjustment is necessary and at what time.” [My emphasis]. Now “adjustment”, and the word is used quite a bit in this report, is Treasury speak for tax increases and expenditure reductions.

The executive summary concludes.

“Changing tax rates or restricting expenditure growth can help close the growing gap between revenue and expenditure. However, analysis in this Statement shows that one policy change by itself is unlikely to stabilise debt over the long run. This means that future governments will likely need to draw on multiple levers and can consider trade-offs across different policy options in responding to our fiscal challenges.”

In other words, we’re going to need both tax increases and expenditure cuts.

This, by the way, was a point noted by the last Tax Working Group, which recommended a capital gains tax to help meet these pressures. The pressures identified in 2021 were much the same as those noted in Treasury’s 2016 briefing, which featured heavily in the thinking of the Tax Working Group about what changes to the tax system was needed.

Now, as we know, a capital gains tax was rejected in 2019, and we also know that the Government was not keen to see this relitigated in its long-term insights briefings from Inland Revenue. So what options does Treasury see as viable in its 2021 briefing? Well, we’ll examine those suggestions next week.

That’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

It’s been a very sombre week hearing the news and seeing the images of utter devastation from the cyclone and related flooding. My thoughts and best wishes go out to all my listeners, readers and fellow tax agents affected by Cyclone Gabrielle, particularly those in Hawke’s Bay and Tairāwhiti East Coast. I hope that you are safe and that you are getting all the assistance you need.

My last podcast was actually recorded four weeks ago before we went overseas. And it’s fair to say a lot has happened in that time, beginning, beginning with the weather bomb and related flooding over the Auckland Anniversary weekend and now Cyclone Gabrielle. So, this week we will focus on what help is available from Inland Revenue for those affected by these weather events. And hopefully we’ll get back to a more regular routine next week.

At present, Inland Revenue offices in Napier, Gisborne and Takapuna are closed, although I would expect the Takapuna office to open shortly. For those in the affected areas, communications permitting, your best option is to call Inland Revenue on their dedicated helpline on 800 473566 or send a message via myIR using the key word “flood “.

2022 terminal tax payments for many would have been due on 7th February. But the extent of the Auckland anniversary weekend flooding in the Northland, Auckland, Waikato and Bay of Plenty Regions led to Cabinet declaring it an emergency event on 8th February for the purposes of use of money interest remission. https://www.ird.govt.nz/updates/news-folder/emergency-event—heavy-rain-and-flooding-in-the-upper-north-island What that means is Inland Revenue have advised for those significantly infected by the weather, late payment penalties will be waived once any taxes due are paid in a reasonable time. Furthermore, use of any interest charged up to 30th April will also be removed, which, given the interest rate is currently 9.21%, is actually quite a relief.

As always with Inland Revenue, the key is to get in contact as soon as possible and they do accept that there will be delays for many people given the state of the communications in the affected areas. And this advice also applies to those thousands of GST payments coming up for the 31st January GST return period which will be due at the end of the month.

It also includes forestry businesses. And I have to say, I can’t say I’m terribly impressed by how the forestry industry has handled the issue of its slash by product, which appears to have wrought considerable damage in Tairawhiti East Coast and Hawke’s Bay.

That aside, eligible businesses are able to use the Income Equalisation scheme to even income fluctuations by spreading their gross income from year to year – I have had one or two clients use this. Under the scheme eligible persons can pay income into a special account which earns interest at 3% if it’s left on deposit for more than 12 months. The payment is tax deductible in the year for which it is made.

Typically, deposits must be made within six months of the tax year end. However, as an Adverse Event has been declared, late, deposits for the March 22 income year can now be made until 31st May.

Now any withdrawals, including interest from the scheme, are usually assessable and are counted as taxable income in the year businesses apply to withdraw them. Typically, amounts may not be withdrawn unless they have been on deposit for at least 12 months. This restriction has now been lifted and applications for withdrawals must be made in writing and will take approximately 20 days to process. I think you can expect Inland Revenue will give these a priority and try and move them through more quickly than that. https://www.ird.govt.nz/income-tax/income-tax-for-businesses-and-organisations/income-equalisation-scheme/discretionary-relief

These discretionary Income Equalisation Scheme reliefs become available whenever Cabinet makes the relevant declaration. They also cover droughts as well as floods and storms. By my reckoning, the declaration on 8th February, which is before Cyclone Gabrielle turned up, is the eighth such declaration in the past 12 months, two of which already related to the Tairāwhiti East Coast and Hawke’s Bay areas. As you can see, they’ve taken a tremendous hammering already.

I expect that the Ministry of Social Development will also be making special benefits and reliefs available. I do wonder whether some consideration could be given to extending the Small Business Cashflow Scheme to help small businesses affected in the area. Certainly, there’s plenty of opportunities for some creative thinking in this space and I think we’re going to need to see it because the scale of this event is scarcely credible. It’s certainly the biggest such natural disaster to hit us since the Canterbury earthquakes.

To summarise, basically what Inland Revenue can do at the moment is help with late payments and those who qualify for the income equalisation schemes now have some more discretion about payments and withdrawals. And as I just mentioned, we might see some special reliefs become available through other agencies in due course.

I mentioned in my last podcast He Tirohanga Mokopuna 2021, the Treasury’s combined statement on the long-term fiscal position and Long-Term Insights briefing released in September 2021. https://www.treasury.govt.nz/publications/ltfp/he-tirohanga-mokopuna-2021-html This raised the specific issue of the fiscal impact of climate change – and unsurprisingly this is now front and centre in the news. I’ll take a closer look at what Treasury had to say in next week’s podcast.

In the meantime, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week, for all those affected, Kia Kaha. Stay strong.

Terry Baucher discusses three major trends that could have an impact on tax policy, along with his hopes for 2023

Welcome back. This week, we’re going to take a look ahead to what I expect will happen this year and also what I’d like to see happen in the tax world.

And let’s begin with the elephant in the room. It’s an election year and the politics of tax in an election year are always greatly magnified. We can therefore expect to see and hear quite a lot about the tax proposals of the main parties.

However, as some political commentators have already pointed out, this year’s election is likely to be tight, which means that the policies of the Act and Green parties may have more influence when the major parties get down to negotiating coalition agreements after the election.

I expect most of the public debate and announcements from the main parties will centre around providing relief to the squeezed low- and middle-income earners. This is the group that’s been most affected by the impact of fiscal drag over the past years as where the non-indexation of tax threshold has resulted in increasing the large number of people on relatively modest incomes being pulled into the 30% tax bracket.

This then has flow on effect for those who may be claiming Working for Families, tax credits and the impact of abatement, results in very high effective marginal tax rates for that group, sometimes close to 60%.

The respective policies that we’ll see between the left and the right blocs will come down to a choice between broad based tax cuts or tax relief, whichever phrase they wish to use, which will benefit greater numbers or more targeted policies aimed at the low- and middle- income earners I just mentioned.

Now, what the respective parties’ policies are will become clear in the run up to the election, but I would expect that we would see Labour’s proposals announced in the Budget, which should take place probably on either 18th or 25th May.

Now, given the demonstrated preference for targeted assistance as shown by last year’s Cost of Living payments, I would expect we might see changes to the Working for Families abatement regime and maybe also the Independent Earners Tax Credit. Certainly the group earning at the top of the 17.5% tax threshold at the moment will be the target there.

Now invariably lots of big numbers will be bandied around about tax that year and we’ll have claim and counterclaim. It’s my almost certainly vain hope that the politicians of whatever hue give a clear indication of how they propose to fund the coming fiscal challenges which we face around the impact of demographic change and the implications of that on the funding of New Zealand superannuation, health care and the fiscal impact of climate change.

Now, as previously mentioned, those were issues that were all addressed in Treasury’s combined statement on the long-term fiscal position and Long Term Insights briefing. It was released in September 2021, which seems like an age ago. But keep in mind that a key driver of the Tax Working Group’s proposal for a comprehensive capital gains tax was partly to address concerns identified by Treasury in the 2016 long term fiscal position about a growing funding shortfall.

The Tax Working Group noted that if nothing changed, according to Treasury forecasts, then the Government was going to be running large deficits starting as soon as 2030. Now, whatever opponents of capital gains tax may say, those fiscal concerns that were identified by Treasury in 2016 and again in 2021 remain and will need to be addressed in one form or another as far as we can see.

Neither of the main parties want to specifically address this critical issue. It’s the minor parties, the ACT party and the Green Party who have proposals in the tax space. They may be ideologically diametrically opposed. But the point is, they are looking at these issues and saying, hey, how are we going to pay for superannuation, health care, and climate change?

Last year it was the Nelson region that got battered by storms. So far, it’s been Tairawhiti East Coast, which has taken a tremendous pounding from Cyclone Hale and other weather events.

Amidst all the noise of what will be, I regret to say, a quite fractious debate this year, I hope everyone keeps their eyes on the main objectives that whatever we decide is the level of tax we’re raising, it is meeting the objectives we want of maintaining services such as health care, superannuation and also addressing road maintenance, infrastructure, housing, climate change, to name but a few.

It’s hard work corralling cats who are beholden to big business lobbyists

Moving on, the second trend will be no surprise at all for long time listeners of this podcast, and that is ongoing international tax reform, the so-called Pillar One and Pillar Two proposals.

Now, since the big breakthrough was announced in October 2021, Governments and tax agencies have been working through, with varying degrees of success, as to how those proposals will be implemented. They all looked to have stalled last year in the face of the European Union’s failure to agree unanimously on accepting the Pillar One and Pillar Two proposals. But fortunately, that obstacle was overcome late last year, so we expect to see further progress in this area.

Interestingly, the OECD has a new director of its Centre for Tax Policy Administration, Manal Corwin. She’s actually pretty well known in the international tax community, has held senior tax policy positions with two US administrations. In fact she was previously a delegate and then vice chair of the OECD Committee on Fiscal Affairs and was a delegate to the Global Forum on Tax and Transparency.

She’s got over 30 years of experience, so on the face of it, is exceptionally qualified for this particular area. I understand she takes up the role with effect from 1st of April.

Now, like the previous director, Pascal Saint-Amans, she’ll be very busy driving this change and basically trying to herd a lot of cats towards an agreement on international tax.

There’s quite a lively debate going on in this space at the moment around how well the new rules will play out, when and to what extent it will be implemented and what will be the implications.

And throughout the coming year, I hope to have some guests on the podcast to talk in more detail about these international tax developments.

Information sharing targets crypto

Now, for most taxpayers, these proposals, which are directed at corporate taxpayers, don’t really have a great degree of impact, except to the extent that you feel that multinationals should pay more tax, which of course is at the core of these reforms.

But many people are more affected by international tax cooperation. And surprisingly, this is an area which has seen remarkably little public commentary on the matter. This is the information sharing that goes on between the various tax agencies.

As we’ve explained previously, this is happening at a much greater extent than the general public realises and probably appreciates. And I expect to see initiatives such as the Common Reporting Standards and the Automatic Exchange of Information continue to be expanded. And we talked last year about the new proposed reporting free framework for crypto assets. And again, we’ll see that a push through into implementation probably later this year. So that’s a major step.

More audits coming

That major trend will continue, and it ties in to the third trend I see happening, which is Inland Revenue ramping up its investigation and audit activity. Now that Inland Revenue has got past dealing with COVID and cost of living payments, it probably will be focusing on what it sees at its core role, preserving and maintaining the tax system’s integrity. And part of that will be driven by the information it’s receiving through the various international information sharing agreements that I have mentioned previously.

Inland Revenue, for example, last year put out an informative booklet on offshore taxation, and it’s setting out where it expects to see greater compliance in this space. And only a couple of weeks back, it is now sending out letters to those three groups of people it’s identified who receive cost of living payments where their eligibility was unclear.

The three groups identified by Inland Revenue are those who had only negative PIE income and therefore should not have received a payment. Those are others whose eligibility is unclear because they might be overseas or were overseas at the time of receipt. And finally, the other group didn’t meet eligibility for other reasons.

Anyway, it’s interesting at this point, it’s sent out the letters directly to recipients, on the basis that the cost-of-living payments were not linked to tax agents. And normally, if you are linked to a tax agent, they will receive the correspondence.

So Inland Revenue have decided to go straight to the recipients. They’ve estimated there may be as many as 80,000 people involved here. And so right now, that group of people are working through with Inland Revenue as to whether they were eligible and if not, how are they going to repay? What are the consequences of that and options for repayment.

That’s just the first initiative we know we’ve seen in the launch this year. I expect we’ll see more and particularly in the area around the cash economy and invariably around the property sector, which has always been a reasonably fruitful area for Inland Revenue.

Seek relief early

At the same time, Inland Revenue will also be dealing with businesses and taxpayers coming under increasing strain as the economy slows down. And so, it will be interesting to see how it responds to requests for relief in that space. Just to repeat what we’ve said previously, if you do run into difficulties in the area, the best approach is to contact Inland Revenue as soon as possible to make arrangements about paying in instalments where possible. They are generally sympathetic where taxpayers take the initiative and come forward.

I suspect this time around they are going to be less sympathetic where taxpayers have started defaulting on payments, such as PAYE and GST. It’s always taken the view that these payments are held in trust by employers, businesses and should not be used for any other purpose. Many of the prosecutions we see Inland Revenue take involve non-payment of PAYE and GST. So, expect a harder line to emerge on that potentially. Again, watch this space and as always, we’ll keep you tuned with developments.

Looking ahead

Now, what would I hope to see going forward? I will keep it realistic. I know we constantly talk on this podcast about the need to address the taxation of capital. I think the current treatment is unsustainable in my view and is putting increasing strains on the tax system.

Things like the bright-line test and the interest limitation rules are by-products of not addressing that particular issue. But that’s not going to happen this year because for the politicians of the main parties it’s a topic they don’t really want to go near because they both see political downsides in doing so. So, I’ll focus on what things I think could happen realistically and what I’d like to see happen.

For example, I’d like to see some really good proposals coming forward to deal with a scenario I mentioned earlier about the taxation of low to middle income earners and these high effective marginal tax rates that trap them when they cross the threshold and the effective abatement on of benefits, whether it’s indexation of thresholds, or perhaps reshaping the thresholds as they haven’t been looked at properly since 2008.

I’d like to see something more than temporary targeted relief. This is an ongoing issue. It is a fault in the system and needs to be addressed otherwise we’re slapping a band aid on the matter and in another three to five years the same issues will re-emerge.

I personally have struggled for a long time to understand why New Zealand politicians seem to be very averse to the idea of automatically indexing tax thresholds. I think it’s because for a long time they’ve been able to proclaim changes to that as a tax cut and also, on the quiet, it gradually enables more revenue to be gathered through the impact of fiscal drag.

But automatic indexation happens in many tax systems around the world. The American tax system where the IRS is basically held together with bits of sticking plaster and string, can manage to index quite a substantial number of thresholds every year. Our system does index for ACC thresholds, and I don’t see why we can’t be doing that more in the income tax space.

There will also be plenty of talk this year, election year, about reducing the compliance burden, no doubt. And we’ll expect to hear that a lot from the ACT and National parties. And there’s no doubt that the compliance burden for small business is pretty high. And so, I’d like to see some thoughts put into making changes to make it easier for small and micro-businesses, those with five or fewer employers where they really do feel a strain. Personal declaration here – that’s a group I represent.

For example, one of the things I might think about is allowing for fixed deductions. Say that if you’re a self-employed contractor or something, there’s a standard amount of deductions claimable. You can claim these and you don’t have to worry about keeping records because in Inland Revenue’s experience, this is the sort of total expenditure that would happen generally. This would be something to help to simplify the tax system.

Changes to provisional tax would also help small businesses. Looking at the timing, for example. I mean, we just had a provisional tax payment on 16th January, which isn’t ideal timing, to be perfectly frank, and maybe we should rethink that date. Incidentally the changes resulting in the current timing of provisional tax payments were really made to suit larger taxpayers.

Now they might say, “Well, we pay most of the tax”. That’s true, but we have to follow your rules as small businesses and it doesn’t work for us, and there’s more of us than you.

Then, for example, there’s the financial arrangements regime which is horrendously complex and catches more people than it was ever envisaged to do when it was implemented in the mid-eighties. Some of the thresholds that apply in the financial arrangements regime have not been changed since 1999, so updates there would be helpful.

There’s also another quite irksome burden around paying non-resident withholding tax on mortgage interest paid to an offshore lender. And this often happens with for example, you’ve got a rental property overseas and you’re using the rental income from overseas to pay an offshore bank.

Under our present rules, technically you should be paying non-resident withholding tax or the Approved Issuer Levy on all such interest payments. Now, conceptually, you’re making payments to a non-resident, which is understandable, but it’s a lot of administration and practically the effect is minimal. But it’s one of those areas where I think Inland Revenue perhaps needs to have a think about whether it’s achieving what’s intended from the non-resident withholding tax rules.

And then I’ve mentioned earlier about fixed deductions. Maybe this should be a fixed allowance for home office space, again, making it easier for small business and employees. Overall, if you go into that space and you’re prepared to accept that there are swings and roundabouts and some people might push the margins, which is always what Inland Revenue worries about, there are definitely opportunities to reduce the compliance burden for small businesses here. I hope that politicians come forward with some realistic proposals in this area.

Well, to summarise, it’s going to be another busy year in tax and as always, we will keep you updated with developments throughout the year. That’s all for this week.

NOTE – this podcast was originally recorded on 19th January before I went overseas and was broadcast on 3rd February. Obviously, a LOT has happened since then.

e Tabacos de Filipinas v. Collector of Internal Revenue