New rules about Provisional Tax when you haven’t previously been a provisional taxpayer

Late last week, the OECD released its fourth edition of its corporate tax statistics. These are becoming pretty essential reading about the corporate tax world. They’re particularly important because as the introduction to the report says, “the database is intended to assist in the study of corporate tax policy and expand the quality and range of data available for the analysis of the impact of base erosion and profit shifting” (the BEPS initiative).

This latest edition has information about corporate tax revenues and trends over the past 20 years. But it also looks beyond headline tax rates at the effective corporate income tax rates. There are particularly interesting sections on R&D tax incentives and on the anonymised and aggregated statistics collected via the country-by-country reporting, which is something that came out of the BEPS initiative. These are an absolute gold-mine for corporate tax statistics.

The primary data analysed here is for the year ended 31st December 2019. The average corporate tax revenues as a share of total tax revenues in that year was 15%, compared with 12.6% in in 2000. And similarly, the average corporate tax revenues as a percentage of GDP have risen from 2.6% in 2000 to 3.1%.

How does Aotearoa New Zealand stack up and compare to those general measures? Well, as a share of total tax revenues and corporate tax revenue in 2019 it was 12.4% of the total, which is below the overall average of 15% but above the OECD average of 9.6%. However, Aotearoa is still well below the Asian Pacific average of just over 18%.

On the other hand, as a share of percentage of GDP, at 3.9% it’s well above the OECD average of 2.98% and the Asia Pacific average of 3.26%.

Quite an interesting dichotomy there, it could be said that corporate tax take is quite low. But when you look at it in the context of as a percentage of GDP, it seems relatively strong.

The report notes on corporate income tax rates that they had have fallen considerably for most jurisdictions since 2000. 97 jurisdictions, for example, had lower tax rates in 2022 than in 2000. Another 14 had the same, but only six including China have a higher rate.

On average, these rates have been declining. The average combined rate across the 117 jurisdictions covered is now 20% compared to 28% in 2000. Our current 28% is near the top of the pile. Australia is also quite high up with its 30% rate, although that is about to reduce. In 2000, the percentage of jurisdictions where the statutory corporate tax rates were greater than or equal to 20% was 85%. For this year, it’s down to 60%.

But as I’ve said in the past elsewhere and the report notes, the trend has been starting to reverse. The infamous Trussonomics budget was going to reverse corporate tax. Increases proposed for next year. In the wake of that complete disaster those tax increases have been reinstated. And that’s quite a significant change in direction.

The report also examines what is the effective average tax rate across the jurisdictions. This is seen to be a much more accurate tax policy indicator than statutory tax rates. For 2021 the average effective average tax rate across the 77 jurisdictions covered is 20.2% which is 1.2 percentage points lower than the average statutory tax rate of 21.4% for the same year.

Here in Aotearoa-New Zealand, the statutory effective statutory tax rate is 27.1%, which is not far short of our statutory rate of 28%. And that reflects the lack of distortions and special incentives we have in our tax system. In fact, when you examine effective marginal tax rates, we’re in the top ten of all countries at 20.1%. By comparison with many other jurisdictions, such as Finland, which was in the news this week, its effective marginal rate is 15%. Also in the top 10 are Australia with a rate of 16.9% and Japan at 17.2%. Incidentally, Argentina has the top effective marginal tax rate of 29.2%.

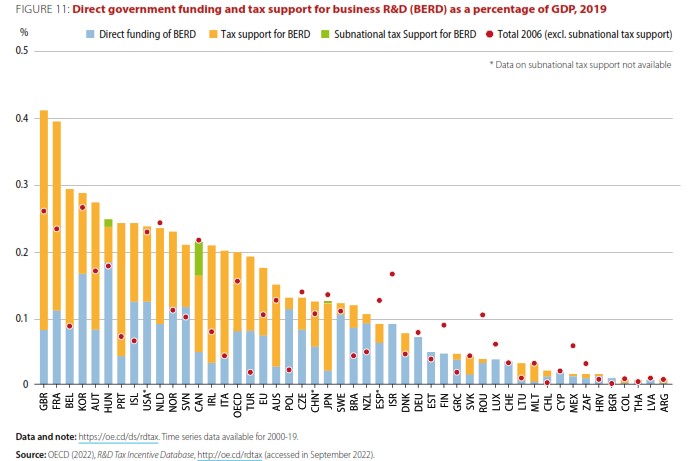

The database looks at tax incentives for research and development, and the total of direct government funding and tax support for business R&D as a percentage of GDP in 2019. Across the OECD it was 0.2%. Aotearoa-New Zealand is well down the field at just over 0.1%. What I thought was quite interesting is more than 80% of it comes from direct funding from the government. A very small proportion, barely 20% of that 0.1% is for tax support and that’s actually amongst the lowest across all the OECD.

And it seems to me that points to the concerns which are continually raised about productivity. If we’re not investing in R&D, should we be looking harder at why investment in R&D is so low and what can we do to boost it. Has the government been doing too much or not enough and what part of role businesses playing in that?

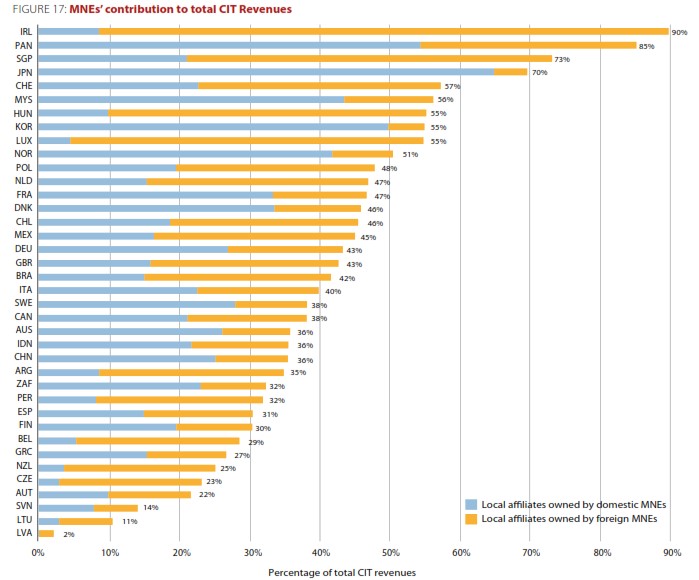

Another thing that caught my eye which I thought was potentially quite concerning was the contribution of multi-national enterprises (MNEs) to total corporation income tax revenues. At the top is Ireland where 90% of the corporate tax take comes from foreign multinational enterprises.

We’re near the bottom with 25% of total corporation tax revenues come from multinationals. So that’s a surprisingly low figure. But what I thought was particularly concerning was the breakdown of this. What the report does it splits the reporting between local affiliates owned by overseas MNEs and local affiliates owned by domestic multinationals. In our case the proportion from domestically owned multinationals is under 5% which appears to be amongst the lowest in the OECD. I think only the Czech Republic and Lithuania have a lower percentage. I wonder whether that points to a lack of diversity in expansion overseas in by our corporate sector.

Some of this information comes from aggregated Country-by-Country Report (CbCR) data which has been collected from almost 7,000 MNEs with turnover exceeding 750m Euros. The data analysed from 47 countries including ourselves indicates “evidence of misalignment between the location where the profits are reported and the location where economic activities occur”

For example, the median value of revenues per employee in jurisdictions with a corporate income tax (CIT) rate of zero is USD 2 million as compared to just USD 300,000 for jurisdictions with a CIT rate above zero. Moreover, in investment hubs, related party revenues account for 35% of total revenues, whereas the average share of related party revenues in high-, middle- and low-income jurisdictions is around 15%. “While these effects could reflect some commercial considerations, they are also likely to indicate the existence of BEPS.”

I think Inland Revenue and other tax authorities will be reviewing this data with interest. Anyway, lots to consider in these statistics, particularly about increasing R&D and the role of overseas export focused multinationals.

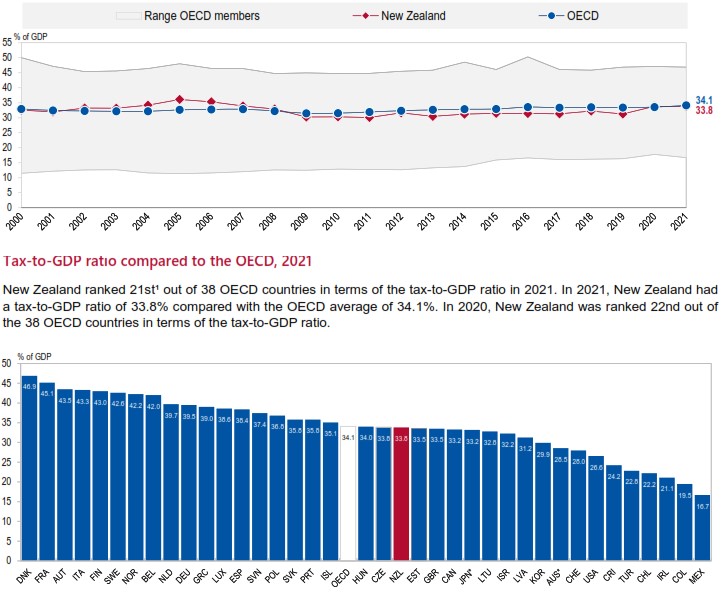

Coincidentally, on Wednesday the OECD also released its Revenue Statistics 2022 edition. This shows how tax revenues bounced back in 2021 as OECD economies recovered from the initial impact of the COVID-19 pandemic. In fact, the OECD average tax-to-GDP ratio rose by 0.6 percentage points in 2021, to 34.1%, the second-strongest year-on-year increase since 1990.

Tax-to-GDP ratios increased in 24 of the 36 OECD countries for which 2021 data on tax revenues was available, declined in 11 and remained unchanged in one. That one country was Aotearoa-New Zealand where the ratio staying at 33.8%, below the OECD average of 34.1% and ranks 21st out of 38 OECD countries.

What the Crown Accounts tax data reveals

It was a busy week for tax data as the Government published its financial statements for the four months to 31st October. The total tax receipts of $35.6 billion for the period is actually $122 million below forecast, which in the scheme of things doesn’t seem too bad. We are seeing fairly strong wage growth from PAYE or source deductions. The forecast was for $14.4 billion but in fact, it was $628 million above that at just over $15 billion. Company income tax was also $302 million above forecast.

However, GST at $9 billion was $945 million below forecast which is a very significant shortfall. Because of the Government extending its cuts to fuel excise duty and road user charges they were 30% lower than forecast, a shortfall of $185 million.

What does all this mean? Firstly, we can see the effect of fiscal drag, which we’ve talked about endlessly. That is the impact as people’s salaries increase and take them across the thresholds, most notably the $48,000 threshold where the tax rate jumps from 17.5% to 30%. We can still see the impact of that, and that’s a factor in the strong growth in PAYE receipts.

To give you an example of the overall effect, the PAYE receipts for the four months to 31st October 2021 were $13.3 billion. But in the four months just ended, these were $1.5 billion or 11% higher at $15 billion. So that’s the effect of fiscal drag which is an issue which isn’t going to go away before next year’s election so expect to see plenty of political posturing and manoeuvring around that issue.

When Bright-line taxes are payable – maybe surprises for some

And finally Inland Revenue have released a draft consultation on the question of provisional tax and the impact on salary of wage earners who receive a one-off amount of income without tax deducted. This scenario could arise where a salary earner realises a gain from the sale of a property subject to the bright-line test. Other instances include shares released under an employee share scheme or one I’ve seen quite frequently, the tax liability arising on the transfer of/or withdrawal from a foreign superannuation scheme.

Typically, when this happens because the taxpayer is on PAYE, they weren’t a provisional taxpayer in the previous tax year as their residual income tax, or RIT, was under $5,000 in the year prior to the receipt of the untaxed sum.

Under the draft consultation, if the tax on the untaxed income is over $5,000 the taxpayer will be deemed to be a provisional taxpayer. But, so long as the total amount of tax payable ends up as being less than $60,000 then the use of money interest exposure will be only start running from the terminal tax date, typically, this would be 7th February following the tax year end of 31st March. This is pretty reasonable and reasonably well understood.

The problem is, though, if the RIT is over $60,000 then the person is meant to pay the tax due on the third provisional tax instalment date, that is 7th of May following the tax year end. If not made, use of money interest starts to apply. Many people affected probably haven’t quite realised that’s when their tax liability is due rather than on the terminal tax date, so it’s good to get clarity on this.

It’s particularly important because Inland Revenue has just announced that use of money interest rates are to rise with effect from 17th January. The rate of underpaid tax will rise to 9.21% with the rate on overpaid tax also increasing to 2.31%. I have to say that that 6.9 percentage point gap is frankly a bit of a laugh, and at odds with some of the somewhat pointed comments made by the Government to banks about social licence and assisting customers during hard times.

The Green Party quotes Margaret Thatcher with approval

The Australian Tax Office’s latest corporate tax transparency report

The latest from the OECD on the carbon pricing of greenhouse gas emissions

Last week, the Green Party released a discussion document on what it’s called an excess profits tax. This is part of its “commitment to a progressive and fair taxation system.” What it is saying is that an excess profits tax or windfall tax is required to level the playing field so that, “big businesses are not able to profit to excess when so many people are struggling”.

The proposal comes on the back of data showing that in the 2021 financial year, corporate profits reached $103 billion, up $24.5 billion on the previous year. And you’ll recall that the corporate tax take for the year to June 2022 was almost $20 billion. The Green Party are saying we’ve got several matters going on at the moment. It believes there are excess profits being earned at a time of hardship. There’s also a need to address the impact of the unprecedented transfer of wealth that happened in response to the COVID 19 pandemic.

The discussion document points out that windfall taxes are common in other countries. It notes that the EU is implementing an excess profit tax in the energy sector. Spain has an excess profit tax on the energy sector and banks. Interestingly, the paper then uses the example of Britain under Margaret Thatcher in 1981, when the Conservative government introduced a windfall tax on banks. This was raised the equivalent of about £3 billion in today’s money and represented about a fifth of the profits banks were pocketing at the time.

That obviously attracted quite a lot of controversy back in 1981. The 1981 British budget is one of the most controversial I can recall in my time. But Thatcher was unrepentant about what she did. In her memoirs The Downing Street Years, she responded

“Naturally, the banks strongly opposed this, but the fact remained that they had made their large profits as a result of our policy of high interest rates rather than because of increased efficiency or better service to the customer.”

So, I guess we live in strange times when the Green Party is quoting Margaret Thatcher with approval, but that is a fair point. And bear in mind ANZ reported a net profit of $2 billion for the first time.

So, windfall taxes are not uncommon elsewhere in the world. They are uncommon under the New Zealand tax framework and haven’t really been used for a very long time. They were used during both world wars but apparently, they weren’t entirely successful.

It’s good to get this discussion going because sometimes I feel that the tax debate in New Zealand is very narrowly circumscribed. We’re living in unusual times so is a windfall tax something that could be done? Even if it was, in my view it would have to be a one-off, such taxes shouldn’t be part of the regular tax take. Incidentally, this is a point I’ve seen discussed elsewhere notably in Ireland following the release of a report about its tax system.

The Green’s proposal suggests a windfall tax could have some retrospective effect. This would be highly unpopular and rightly so, for companies, because it would mean there’s no certainty around their planning. Companies might budget for a 28% tax rate but then suddenly find that in fact it’s been increased to 33%. So businesses would find that hard to deal with, but if they knew there was a possibility it would be interesting to see how pricing might play out.

Overall it’s good to see this discussion going on and no doubt it’ll attract a lot of controversy and you can make your own submission on the idea to the Greens. Next year is an election year so who knows what’s going to happen afterwards? But as I said, windfall taxes are used elsewhere in the world. And if they were good enough for Margaret Thatcher, well, who knows?

Aussie ‘transparency’

Moving on, over in Australia, the Australian Tax Office, (the ATO) has just published its eighth annual report on corporate tax transparency. What this does is look at the amount of tax paid by large corporates for the year to June 2021. According to the report, the over A$68 billion paid during that year by large corporates is the highest since reporting started. It’s up A$11 billion or 19.8% on the previous, COVID-19 affected year. Apparently, rising commodity prices were a key driver for the increase in corporate tax.

The report notes that Australia has some of the highest levels of tax compliance of large businesses in the world, with 93% of tax paid voluntarily. This rises to 96% after the ATO has asked a few questions.

The ATO has been running what it calls the Tax Avoidance Taskforce for some time. According to the report since 2016, the ATO has raised tax liabilities of $29 billion and Tax Avoidance Taskforce funding being responsible for $17.2 billion of that amount. (It’s worth remembering “raised liabilities” doesn’t necessarily mean that they’ve been collected). In last week’s Australian Budget there’s an extra $200 million per annum to help expand the focus of the Tax Avoidance Taskforce. This brings the total funding for the Tax Avoidance Taskforce to A$1.1 billion over the next four years.

Now, this report covered 2,468 corporate entities, more than half of which were foreign owned with income of A$100 Million or more. 529 or about 20% were Australian owned private companies with an income of $200 million or more, which is an indication of the size and scale of the Australian economy. Interestingly, there’s a note that the percentage of entities which pay no income tax was 32%.

It’s interesting to see what other jurisdictions do with their tax data. I feel Inland Revenue should do a lot more in this space with the data it receives, but it’s very reluctant to do so at this point. It’s currently not part of its brief, but such a report and other statistics gives us a better understanding of the scale of the economy and what’s happening in it. I would like to see Inland Revenue produce something similar.

Energy, taxation and carbon pricing

Finally, this week, overnight the OECD released its latest report on pricing greenhouse gas emissions. This looks at how carbon prices, energy prices and subsidies have evolved between 2018 and 2021. This is part of a database the OECD is developing to track what’s happening on energy, taxation and carbon pricing.

This report covers 71 countries (including New Zealand) which together account for approximately 80% of global greenhouse gas emissions and energy use. There’s a summary report by country as well. Overall, more than 40% of greenhouse gas emissions in 2021 were covered by carbon prices and that’s up from 32% in 2018. And the average carbon price from emissions trading system schemes and carbon taxes more than doubled to reach €4 per tonne of CO2 equivalent.

And obviously the report goes into what’s happening across the across the globe. There’s been a rise in the amount of greenhouse gas emissions now covered, and that is as a result of the introduction or extension of explicit carbon pricing mechanisms notably in Canada, China and Germany.

What’s termed carbon net prices are rising further in 2021 as have permit prices under emission trading schemes. There’s steady changes in carbon taxes, with new carbon taxes introduced, together with increases in carbon tax rates or the phasing out of carbon tax exemptions.

As for New Zealand, 44.1% of all greenhouse gas emissions are now subject to a positive ‘Net Effective Carbon Rate’ which has not changed since 2018. The report also notes that fuel excise taxes, which are described as an implicit form of carbon pricing cover 23.8% of emissions. Again, that’s unchanged since 2018. So, looking at this, we appear to be stalling a bit on this and I do wonder whether next year’s report might show that because of the cut in fuel excise duty, we’ve gone backwards. However, other countries have also been cutting fuel taxes because of the high inflation in the wake of the war in Ukraine.

Although the level of coverage of greenhouse gases covered by carbon pricing hasn’t changed since 2018, the average carbon price has risen. For example, fuel excise taxes in 2021 amount to €19.73 per tonne of CO2 equivalent. That’s up by +9.4% relative to 2018, which is probably below inflation, though. However, once adjusted for inflation the average Net Effective Carbon Rate on greenhouse gas emissions has increased by +39% since 2018

There’s a lot to consider in this report, more than I’ve had a chance to go through right now. But again, it reflects a constant theme of this podcast about the increasing role of environmental taxation and the scope for opportunities in this space.

What we do with those funds is the other side of the equation. It’s one thing to say we need more taxation. What isn’t always debates is what we do with those taxes. I’ll repeat my longstanding view that funds coming out of environmental taxation in the form of new taxes or the existing emission trading scheme should be used to mitigate the impact of climate change.

There was a report earlier this week identifying 44 communities in great risk of environment impact from climate change which are unprepared for the flood risk. No doubt they will be looking for assistance. In the meantime, Nick Smith, Nelson’s new mayor (and former Environment Minister) has requested government assistance with dealing with the impact of the recent flooding. No doubt there will be plenty more to come on this topic.

This week we take a close look at Inland Revenue’s Annual Report for the year ended 30th June 2022. It begins with an overview of how Inland Revenue “has contributed to the well-being of New Zealanders”. There’s a summary of the highlights and key results for the year including a summary graphic illustrating the composition of the $100 billion of tax revenue raised during the year and the areas in which it was spent. The highlights note that Inland Revenue exchanged financial account information with more than 70 countries and has information sharing arrangements with more than 17 agencies. This is something that people always need to keep in mind just how much information Inland Revenue has access to and how much it shares.

The overview declares “we interact with a range of customers on tax and provide payments that are critical to people’s wellbeing.” You’ll note the use of the word “customers”. In fact, “customer” or “customers” is used over 660 times in the report, compared with a mere 30 mentions of “taxpayers”.

I have great reservations about describing taxpayers as customers. I can appreciate there are some benefits from this approach in terms of helping Inland Revenue staff understand the need to provide better service to taxpayers. But the repeated use of the term customers implies a voluntary transactional relationship and ignores the power dynamic. Actually, tax is compulsion. We are compelled to pay tax and we can’t exactly say to the Inland Revenue, ‘Your service is terrible. I’m switching providers to the Australian Tax Office’.

Whatever the description, Inland Revenue considers it’s dealing with three groups of customers; individuals, families and businesses. This, however, overlooks the important role of tax agents who interact with Inland Revenue on behalf of these groups daily. However, tax agents are only mentioned nine times throughout the whole report. It’s a long-standing complaint of myself and other tax agents that the Business Transformation process underestimated the important role of tax agents in enabling the smooth running of the tax system. Accidentally or not this summary of who Inland Revenue sees as its customers rather reinforces our point.

Anyway, moving on, the next section within the report expands on Inland Revenue’s story for 2021-2022 outlining the benefits of its transformation of the tax and social policy system. After a brief look at the year ahead, we then get into the detailed analysis of how Inland Revenue performed against key measures and indicators, its organisational capability, and finally the departmental financial statements. Lots of juicy stuff here, in fact too much for one podcast.

Inland Revenue’s major achievement for the year is the completion of its Business Transformation programme, which was officially closed on 30th June this year. The project was completed on time and under budget and as a result, Inland Revenue is on track to save $100 million in administration costs annually. Furthermore, at the end of the Transformation Project, Inland Revenue handed back $458 million to the Crown. The programme was initially budgeted at $1.5 billion and came in at just over $1 billion. Given the notorious history of some I.T. projects such as Novapay, this is a significant achievement. So well done, Inland Revenue.

Business Transformation, of course, has enabled Inland Revenue to proceed with its auto-assessment process. As the report notes, previously, approximately 1.4 million people who were potentially eligible for a tax refund never applied. This year tax refunds were sent to 1.65 million taxpayers and as of 30th June, $602 million had been refunded. Apparently, it now costs on average $1.35 to process a tax return, compared with $2.33 back in 2015-2016. So that’s a significant improvement.

Business Transformation has also meant that many taxpayers now use Inland Revenue myIR portal to communicate with Inland Revenue and handle their tax affairs. There were over 60 million user sessions in the June 2022 year, and that’s a growth of 140% since 2019. Overall, 80% of taxpayers say they find it easy to deal with Inland Revenue, which is about the same as last year.

Although Inland Revenue encourages the use of its digital platform, it is aware that not everyone has ready access to computers. It’s good to see that this year it has been working with the likes of the Citizens Advice Bureau to ensure that those who are at risk of being digitally excluded always have a chance to engage with Inland Revenue. That’s something to be applauded and we hope that will continue.

There’s some interesting commentary on the impact of Business Transformation for small businesses. The report notes that approximately 90% of businesses in Aotearoa New Zealand have five or fewer employees. Inland Revenue’s hope was that this group would especially benefit from Business Transformation. However, the compliance effort for this group has not reduced as much as Inland Revenue had hoped.

According to an Inland Revenue survey in 2021, SMEs said they spend an average of 31 hours a year on meeting their tax obligations. Now, this is five hours fewer than in the survey’s baseline year of 2013. But the introduction of mandatory pay day finding from 1st April 2019 means that businesses spend as much time complying with PAYE obligations now as they did in 2013. Overall, though, 60% of small business owners felt that the time their business spends on tax matters was acceptable and that’s up from 55% in the previous survey.

The core role of Inland Revenue is the collection of tax. And this is the first year the total tax take has exceeded $100 Billion, up 7.3% on 2021. However, the overall amount of tax debt increased by 10.5% to $4.8 billion at 30th June 2022. And there are some concerning numbers in here. As of June 2022, 55,888 people who received Working for Families were in debt, which is a 27% increase on the June 2021 year.

Overdue student loan debt has also increased by 17.6% to $2 billion. This is apparently mostly due to only 24.5% of the overseas based student loan borrowers making their required repayments this year.

Inland Revenue wrote off $688 million of debt during the year. That’s down from the $812 million written off in 2021. Write offs of GST and individual income tax debt made up 58.8% of that total value.

Now the report admits that “The total amount written off is lower this year, due in part to Inland Revenue prioritising COVID-19 support work over proactive debt collection work.” The report then notes that “overdue tax debt grew at a comparable rate to tax revenue. It was 4.6% of tax revenue, compared to 4.5% in 2020–21 and 4.5% in 2018–19. This is a good result, considering how difficult the environment has been.” That’s probably fair comment. Inland Revenue has had to deal with an enormous amount of other projects such as the COVID 19 Resurgence Support Programme as well as getting ready for the cost of living payments, which happened after the end of the year.

But what action is it taking about trying to collect all this debt? Well, during the year $2.38 billion of debt was put under instalment arrangements involving approximately 120,000 taxpayers. As of 30th June, $491 million has already been repaid in full. And it’s then also started a programme in November 2021 targeting those with bigger debts. This involves around 1,350 businesses with debts totalling $356 million. And that’s apparently generated about $90 million of repayments so far.

It also pulled out the big stick and commenced the liquidation process against 759 companies, resulting in 163 companies being liquidated through the High Court. Another 592 companies went into liquidation, owing tax debt after the Inland Revenue initialised the process. Now some of these liquidations are inevitable, to be frank. Although Inland Revenue is trying to work hard in this area I definitely think there’s room for further improvement.

One of the key metrics I’m always interested in is Inland Revenue investigations activity. There’s an admission that it …

0 of 15 secondsVolume 0%

“…didn’t undertake as many interventions as usual as we didn’t want to put more pressure on customers during a difficult year. We paused some investigation activity and focused on ensuring the integrity of our COVID-19 support products.”

Consequently, Inland Revenue only met one of its four measures for investigations category. Whereas last year it achieved three out of four.

One measure is the ‘Percentage of customers whose compliance behaviour improves after receiving an audit intervention.’ The target is 85% but the actual measurement achieved this year was 69.6%. I don’t quite know how they’ve measured that, but it’s a little bit concerning because pretty much my experience is if someone from Inland Revenue turns up and there’s an audit, behaviour generally improves afterwards. I think this measurement may be a by-product of overdue debt existing.

On the other hand, it did meet the measure for ‘Discrepancy identified for every output dollar spent.’ Now the target is $7 per dollar but Inland Revenue achieved a return of $9.88. “We have assessed additional tax or protected the integrity of the tax system to the value of $1.12 billion. This has exceeded expectations.” Although I find the phrasing of that a little opaque.

Intriguingly, that measure has been retired and is not being used in the current year. I’m not sure why, but we will watch with interest as we won’t know what the new measure is until next year’s report is released.

As part of its usual compliance activity Inland Revenue ran a number of compliance campaigns for specific sectors and compliance issues. For example, it ran campaigns about tax residency, disclosing offshore income and basically ensuring people meet their international tax obligations. According to the report, these campaigns targeted some 7,000 taxpayers and their tax agents and resulted in voluntary disclosures totalling $100 million in omitted income in the past two years. That’s not $100 million of tax, the best-case scenario would be maybe $40 million of tax. But anyway, still a good return for Inland Revenue.

I think we can see more of this campaign. Inland Revenue, as I mentioned earlier, shares information with 70 countries. This is an area it was starting to pay attention to before the Pandemic and is now returning to this area with the launch of a new offshore tax programme in June 2022. So, watch this space.

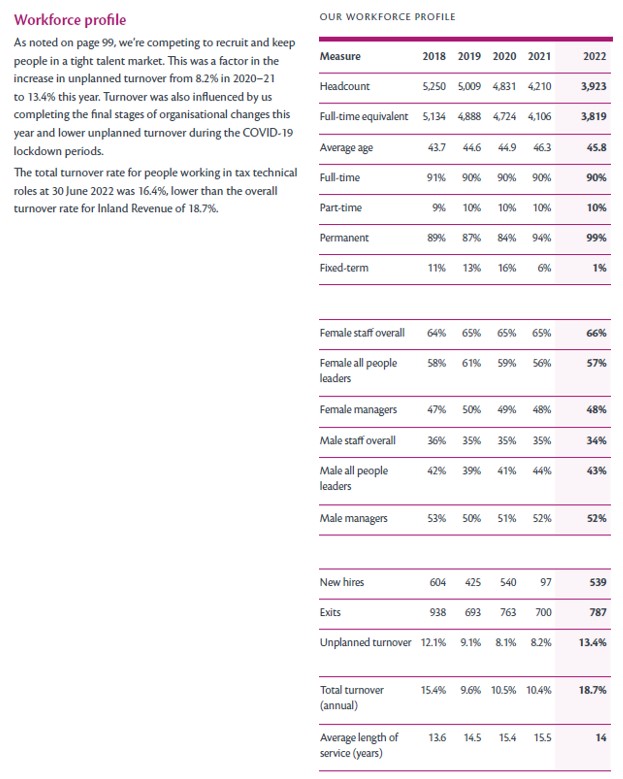

Now the key to any organisation is its people. And Inland Revenue has been through a massive amount of change in the past five years. As of 30th June, its workforce is now 3,923, which is down 1,327 or 25% since June 2018.

During the year, 787 people left Inland Revenue and it hired 539. Over the past five years, some 3,881 people have left Inland Revenue, which is 74% of the workforce as of July 2017. That is a massive churn and I have concerns about that.

The average length of service in years has dropped this year to 14, compared with last year’s 15.5 years. A lot of people have left and Inland Revenue’s staff turnover this year was 18.7%. Rather worryingly, the total turnover rate for people working in tax technical roles at 30th June 2022 was 16.4%. Although that’s lower than the 18.7% for the whole organization, it is well up on last year’s 1.3%.

Inland Revenue staff are actually very highly valued outside the public sector. My understanding is Inland Revenue is pretty competitive on wages. Seeing so many gamekeepers turning into poachers is not something we really should see. hence my concerns about what’s going on.

Page 100 onwards in the report looks at the state of morale and health in the report in Internal Revenue, and it’s very mixed. Some of the metrics are better than the public service generally. For example, 96% of staff can work remotely, which is well above what the rest of the public sector.

The report has a breakdown of employee ethnicity and the proportion of roles held by people with different ethnicities. Now, actually, Inland Revenue pretty much reflects the diversity of modern-day Aotearoa. 66% of its staff are European, compared with 70% of the population generally, 12% are Māori, which is below the 16.5% of the general population.

A bit more concerning though is looking at the proportion of leadership roles. When you get up to senior management, 96.4% are held by Europeans. Even the team leader and general management roles are all over 80%. So, there’s work to be done there.

But something which really caught my eye and is a matter that needs to be discussed more widely is a disclosure under Schedule 6 of the Public Service Act 2020. This requires Inland Revenue to report on situations where the Commissioner has delegated any of the Commissioner powers outside the public service. In other words, it said to people, ‘You can act in our capacity’.

In previous years the disclosure has involved Westpac and Callahan Innovation. But this year, for the first time, it includes Madison Recruitment Ltd. The disclosure reads

“Inland Revenue engaged Madison Recruitment Ltd to provide contingent labour to help with the introduction of the Cost of Living Payment and to provide additional support with other specific tasks due to the ongoing impact of COVID-19. The first Madison personnel began undertaking their engagement in June 2022. To enable the Madison personnel to fully undertake the engagement, the Commissioner delegated some powers to those Madison personnel. This delegation has been operating as intended in line with the contractual arrangements with Madison Recruitment.”

I have major reservations about this because it shows that Inland Revenue is perhaps under-resourced if it is taking on temporary labour. I don’t believe an organisation such as Inland Revenue with the powers available to it, should be taking on temporary contract labour. I can see there might be a business case for doing so, but as I said earlier there’s an issue with mounting overdue debt and the drop off in investigations activity.

We also have this staff churn that’s going on at Inland Revenue. Losing 75% of your workforce over five years, is not something I think is healthy for an organisation. Staff changes are inevitable and healthy. But 75%, I’m not so sure about that. So, this one of the major concerns I have coming out of this report.

Summing up the report is a mixture of the good, the not quite so good and the concerning. One of the not quite so good is a rather bumpy relationship with the tax agents, as I mentioned previously. But I understand the new commissioner Peter Mersi has been meeting with representatives of the professional bodies and no doubt this point has been discussed. In fairness, the ongoing huge challenge of dealing with a pandemic and its aftermath have not helped.

My great concern is the level of staffing and the state of morale at Inland Revenue. As I mentioned, there’s been considerable turnover of staff in the past five years, and I don’t believe the delegation of powers to Madison Recruitment is acceptable. I think it threatens Inland Revenue very well-deserved for reputation, for privacy and security of taxpayer information. It may be a temporary measure in order to help handle the Cost of Living payments, but judging by the report overall, I think Inland Revenue should be consider whether its current staffing levels are sufficient.

Overall, I would give Inland Revenue a pass mark for what has been another difficult year. The impression I have is an organisation right now in transition and under understandable stress. It could not have handled the many COVID-19 related issues it’s faced in the past two years without the benefit of Business Transformation. So, getting that project finished on time and under budget is a massive achievement. At the same time, the Pandemic and the continuing cost of living crisis has pointed to some ongoing weaknesses, which I think the new Commissioner will need to address urgently. We will be watching with interest.

A scoop by Rebecca Stevenson revealed Inland Revenue had collected an extra $33 million from multinational firms as part of a campaign to keep COVID-19 wage subsidy payments in New Zealand.

During 2020 a total of 376 multinationals (those with annual turnover in excess of $30 million) received a total of $830 million in wage subsidies. Inland Revenue’s transfer pricing unit saw there was a possibility that although the wage subsidy was meant to ensure employment in New Zealand, multinationals could take the opportunity to transfer these funds overseas.

It therefore met with advisers of the Big Four accountancy firms to brief them on its views about this and then wrote to 436 multinationals, “setting out the expectation that all of the Government’s wage subsidy assistance should remain within the New Zealand economy.” Subsequently, some $33 million of wage subsidy monies was repaid voluntarily by multinationals.

Each year, Inland Revenue Transfer Pricing Unit sends out an annual survey to approximately 750 international firms. These are updated each year and this year’s survey included two new COVID 19 questions relating to the impact of the pandemic on multinationals. These are in addition in addition to more typical transfer pricing type questions about the “intensity and effect” of related party transactions which Inland Revenue wants to undertake so it can “refine its risk profile on firms with cross-border arrangements”.

According to Inland Revenue’s International Revenue Manager John Nash, who incidentally is part of the OECD Base Erosion and Profit Shifting (BEPS) initiative, Inland Revenue also liaised with the Australian Tax Office and with the OECD Secretariat to ensure that its approach to transfer pricing in this matter was consistent with transfer pricing regulations internationally. And the word that came back that it was.

Apparently not all multinationals are happy with Inland Revenue’s interpretation of the transfer pricing rules. And therefore, when it comes to looking at 2021 and 2022, Inland Revenue may expect experience and pushback as a result. This is unsurprising, but it is interesting to see how proactive Inland Revenue was on this issue.

However, as former tax working group member Professor Craig Elliffe noted, there is a potential for quite a significant dispute given that the amount involved is $830 million. As Craig commented “It is a hugely sensitive matter. You feel as a New Zealander there’s no moral justification for multinationals taking a difficult approach here.” This is shaping up to be a classic example of the clash between the technically legal correct approach and the morality of the multinationals’ approach. We will watch with interest.

Transparency for reporting crypto transactions?

Last week I discussed the OECD’s proposed Crypto Asset Reporting Framework, and thank you for all the feedback that generated. This week it’s the launch of the Asia initiative, an idea proposed in 2021 by Indonesia’s Minister of Finance Sri Mulyani Indrawati and the President of the Asian Development Bank (ADB), Masatsugu Asakawa.

The Asia Initiative will be “focused on setting tailored solutions to ensure the implementation of tax transparency standards across Asia.”

So far, 13 countries have signed up to the initiative, but these include all the major economies of the region India, China, Japan, Indonesia, Malaysia and Pakistan. The initiative is just the latest example of the agenda discussed previously all for international cooperation on information sharing and thus best exemplified by the Common Reporting Standard and the proposed Crypot-Asset Reporting Framework.

It so happens that the OECD Secretary General Mathias Cormann also reported back last week to the 14th Plenary meeting of the OECD/G20 inclusive framework on BEPS. He gave them an update on progress on the two-pillar international tax reform. In short, some progress, but plenty of hard work ahead. The intention is to finalise a new multi-lateral convention for implementation of Pillar one by mid-2023, and that is going to be for entry into force in 2024.

And again, as I’ve said previously, politics will get in the way here. It will be interesting to see what plays out, particularly in the wake of the upcoming US midterm elections.

Just a note that during that plenary meeting, Mongolia became the 100th jurisdiction to join the current multilateral BEPS convention, which now covers around 1850 bilateral tax treaties worldwide. This the level of international cooperation will continue to grow. There were more than 500 delegates from over 135 countries and jurisdictions at that plenary meeting.

Stuck with a questionable decision

Following on from the recent Supreme Court decision in Frucor, Tax Guru and past podcast guest John Cantin has done a deep dive on the decision.

As you’d expect from John it’s measured and insightful. He rightly points out that criticisms of the majority judgement are irrelevant – the case is now the law. He sees little prospect of this being changed either by a future Supreme Court decision or by a legislative change to the anti-avoidance provisions which he thinks would be a difficult piece of legislation to write.

In summary his view is

“Practically, taxpayers need to consider and prove the commercial, tax and the economic effects of what they do to counter a tax avoidance charge. They need to be able to explain what they did to persuade the court that the desired tax effects are achieved. Findings of fact are important and likely to be persuasive for future arrangements.”

John’s full note on the case is well worth a read. As I said we can expect to see more analysis of the case but although I expect there will be criticism of the decision, as John said for now it is the law.

Others are addressing fiscal drag

I’ve frequently discussed here and across other media the effect of fiscal drag because of non-indexation of thresholds, not just for income tax but for Working for Families and student loan repayment thresholds. So I had a bit of a wry smile when I read about the United States Internal Revenue Service inflation adjusting more than 60 tax provisions, including tax rate schedules and another tax changes as part of getting ready for the 2023 US tax year.

As Shamubeel Eaqub told Newshub, the failure to regularly index thresholds is really quite cynical politics by both major parties. It’s a view I share and which I discussed with Sharon Brettkelly as part of The Detail podcast last week.

Don’t mess with tax simplification

Finally, a quick note on the astonishing events in the UK. One of the measures announced in former Chancellor Kwasi Kwarteng’s mini-Budget was the abolition of the Office of Tax Simplification. In the wake of his resignation and now that of Prime Minister Liz Truss, UK tax guru Dan Niedle of Tax Policy Associates tweeted

“Let this be a lesson to future politicians to not abolish the Office of Tax Simplification”

The OECD proposes a crypto-asset reporting framework

New levy proposal for farmers’ greenhouse gas emissions;

TOP’s bright idea about tax rate

Last week, the OECD launched its Crypto-Asset Reporting Framework (CARF). This is a response to a G20 request that the OECD develop a framework for the automatic exchange of information between countries on crypto-assets. In other words, it is going to be a development of the existing Common Reporting Standards on the Automatic Exchange of Information or CRS. The CARF was presented to G20 Finance Ministers and Central Bank Governors for discussion at their meeting this week in Washington D.C.

The proposed rules cover four areas:

the scope of crypto-assets to be covered,

the entities and individuals subject to data collection and reporting requirements,

the transactions subject to reporting as well as the information to be reported in respect of such transactions and

the due diligence procedures to identify crypto-asset users and controlling persons and to determine the relevant tax jurisdictions for reporting and exchange purposes.

CARF is intended to complement the CRS and mean that crypto-assets will be subject to automatic exchange of information reporting. Now the reason that that has come up is unsurprising really. Individuals holding wallets which are not affiliated with any current financial institution or service provider, and are therefore then able to transfer crypto-assets across jurisdictions. As the OECD report notes:

“this presents the risk that relevant crypto-assets are used for illicit activities or to evade tax obligations. Overall, the characteristics of the crypto asset sector have reduced tax administrations visibility on tax relevant activities carried out within the sector, increasing the difficulty of verifying whether associated tax liabilities are appropriately reported and assessed”

This is a very long way of saying there’s probably a lot of tax evasion going on in the crypto-assets sector.

CARF is therefore an obvious response. It is also part of the huge ongoing trends in the modern tax world of the acceleration in reporting and exchange of information between jurisdictions. This is a very, very significant development in the tax world that happened in the wake of the Global Financial Crisis and has largely gone unreported in the wider press although it appears to be generally accepted by the public. When you align this alongside what’s happening with the Pillar One and Pillar Two proposals, then the days of tax havens where money can be parked outside the tax net of major jurisdictions, are numbered.

So what crypto assets are covered? Well, the definition is pretty broad, it targets assets “that can be held and transferred in a decentralised manner and without the intervention of traditional financial intermediaries”, i.e. banks and other financial institutions. This includes stablecoins, derivatives issued in the form of crypto-assets and certain nonfungible tokens.

There are three categories excluded from what’s termed “Relevant Crypto-Assets”:

crypto assets, where have it’s been determined they cannot be used for payment or investment purposes,

Central Bank Digital Currencies which represent a claim in Fiat Currency on an issuing Central Bank or monetary authority, which function similar to money held in a traditional bank account,

Specified Electronic Money Products that represent a single Fiat Currency and are redeemable at any time in the same Fiat Currency. (Not sure I’ve encountered any of these myself, to be honest).

Reporting entities are any intermediary or service provider which is facilitating exchanges between relevant crypto-assets or between relevant crypto-assets and fiat currencies. Generally, they will be subject to the reporting requirements of the jurisdictions in which they are either tax resident or have a regular place of business or branch through which they carry out reportable transactions.

Keep in mind, CARF ties in with the CRS which is already hugely comprehensive and covers most of the main tax jurisdictions and tax havens. The ability for crypto asset service providers to slip out from underneath the CARF reporting requirements is going to be quite limited.

Three types of transactions are going to be reportable:

exchanges between Relevant Crypto-Assets and fiat currencies,

exchanges between one or more forms of Relevant Crypto-Assets, and

transfers of Relevant Crypto-Assets.

CARF has been developed to sit alongside CRS and in fact at the same time the OECD carried out its first comprehensive review of the CRS regime. It’s proposing some amendments to bring new financial assets, products and intermediates within the scope of CRS. The changes are also being made to try and avoid duplicate reporting with that which is expected to happen under CARF.

The entire CARF framework runs to over 100 pages. It should be signed off subject to any further work requested by the Central Bank Governors and Finance Ministers at their meeting this week. There will no doubt be some further tweaking, so it’s not yet all set to go. No doubt there will also be some lobbying for changes in the regime.

CARF is, as I said earlier, part of a growing trend for international cooperation on the sharing of information. When implemented it basically will probably mark an end, or certainly a restriction, on the use of crypto assets for tax evasion and other nefarious purposes.

Making farms pay

On Tuesday, the Government released its proposals for how to price agricultural emissions.

These are in response to the recommendations earlier this year from He Weka Eke Noa, the Primary Sector Climate Action Partnership, for a farm level pricing system. The Climate Change Commission, He Pou a Rangi, also provided separate advice on agricultural emissions.

The Government’s proposals try and integrate what He Weka Eke Noa and He Pou a Rangi have suggested. The intention is to price agricultural emissions at the farm level. But it comes with a big stick – if the sector cannot reach agreement by 1st January 2025, then agricultural emissions will be be priced under the Emissions Trading Scheme.

The key part of the proposal is a farm level split gas levy to price agricultural gas emissions. It will apply to farmers and growers who are GST registered and meet certain livestock and fertiliser use thresholds. There would be separate levy prices set for long lived gases and biogenic methane and these will be set up after advice from the He Pou a Rangi and in consultation with the agricultural sector and iwi and Māori.

The long-lived gases (basically carbon) price will be set annually and then linked to the New Zealand Emissions Trading Scheme unit price. There’s a separate biogenic methane levy which will be adjusted based on progress towards domestic methane targets. One of the feedback matters the Government is seeking is whether that methane levy price should be reviewed annually or every three years.

With regards to the revenue raised, the Government proposes it that the revenue is used to fund incentives and sequestration payments, with any remaining revenue to fund the administration of the pricing scheme and a joint government and Māori revenue recycling strategy. There’s a proposal for incentive payments for a range of on-farm emissions reduction technologies and practises. I fully endorse this policy of using funding from an environmental tax to help the transition.

But if you’ve been watching this, you’ll know it has taken a long time to get here. It’s almost 20 years since the infamous ‘Fart tax’ was first proposed and Shane Ardern MP drove a tractor up the steps of Parliament. So progress has been very slow on this, which I personally find very frustrating.

Here in the city, we need to be working on reducing our transport emissions. Rather ironically, on the same day of the Government announcement, Ruapehu Alpine Lifts went into voluntary administration. The ski field operation has clearly been affected not just by one very bad year and the effect of Covid. This is something that’s been building for some time.

We’ve also had the recent floods and damage reports coming out of Nelson where the insurance claims so far total $50 million. So change is happening all around us and my view is we are going to have to adjust to it and try and do something to reduce emissions as part of the global effort. We can’t rely on everyone else to do it for us.

TOP tackles tax bands

Finally, this week, there’s been a lot of talk about tax cuts ahead of next year’s General Election, particularly in the wake of the massive u-turn by the UK government over a proposed higher rate tax cut which has now resulted in the sacking of the Chancellor of the Exchequer (Finance Minister) Kwasi Kwarteng.

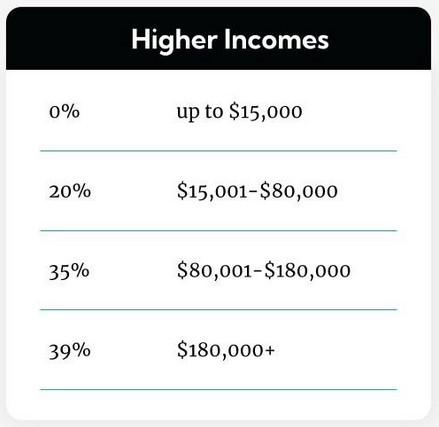

Amidst all of that chaos The Opportunities Party released its two-phase tax policy, phase one of which contains substantial tax cuts. But what caught my eye about TOP’s suggestion is their proposal to introduce a tax-free threshold of $15,000, together with adjusted tax thresholds.

Now tax-free thresholds are expensive, but they are seen around the world. Australia has one for the first A$18,200. The UK tax free personal allowance is £12,570 and America has a flat $12,000 exemption.

But what I thought is interesting about TOP’s proposal is they have looked at the question I’ve talked at length about what happens for low- and middle-income earners when their income crosses the current $48,000 threshold and the rate jumps from 17% to 30%. Under our current tax structure 12.5 percentage point jump is the highest such rate – the next jump at $70,000 is only from 30% to 33%.

So, I’ve been thinking for some time that we really ought to be looking at these thresholds and rate bands and maybe combining three into two, which is what TOP propose.

Now, TOP have got to either win an electorate or get across the 5% threshold before they’ll be in any position to propose their policy. (The second part of their policy would fund those tax cuts by a land value tax, which, of course, is longstanding TOP policy). We’ll have to wait and see until after next year’s election.

But if you want to hear more about what type of tax changes could happen and their implications then this week on RNZ’s The Detail podcast, Jenée Tibshraeny of the Herald and I spoke to Sharon Brettkelly about tax cuts here and in the UK, how our tax system works and what could be done if we’re helping people at the lower income level.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Change on the way for GST recordkeeping requirements

A clear-eyed dissent by a Supreme Court justice

Tax revenue exceeds $100 billion for the first time

Over the next few months, GST registered businesses will receive a stream of information from Inland Revenue explaining new recordkeeping requirements for GST purposes, which will take effect from the 1st April next year. These changes relate to what information needs to be shared or retained to support GST input tax claims.

These changes are permissive in nature, and existing invoicing practises and systems which are compliant with the previous GST rules will still remain compliant with the new information rules. The new rules are less prescriptive about the information required to support a GST input tax claim.

The key purposes of these changes are to try and reduce compliance costs for businesses and facilitate the introduction of e-invoicing. The changes will be done by way of requiring the supplier and recipient of a taxable supply to retain a minimum set of information relating to that supply. The current rules, which required formal documents such as tax invoice, credit notes, debit notes etc. to support input and output tax will be repealed.

One of the most noticeable changes will be that there will no longer be a requirement for an invoice to have the words ‘Tax Invoice’ in a prominent place. Tax invoices will now be caught termed ‘taxable supply information’ and the former debit and credit notes which had to be issued when a correction was made, will now be termed ‘supply correction information’, which is better terminology as it actually reflects what’s going on.

There are also changes to the buyer credit created tax invoice regime which are now called ‘buyer created taxable supply information’. And these changes have already come into effect and actually are pretty helpful because you now no longer need to get Inland Revenues permission to operate the buyer created taxable supply information.

There will be a minimum set of information required to be retained in business records under the new rules for a taxable supply. According to Inland Revenue these rules are generally consistent with the requirements of commercial contract law relating to invoicing and recordkeeping. The requirement to hold a tax invoice in order to claim an input tax deduction is now replaced with the requirement to have business records showing that GST has been borne on the supply.

Now key information for both a supplier and a recipient of a supply of goods or services is that of, ‘supply information’. This includes, at a minimum, all the following information:

– the name and registration number of the supplier,

– the date of supply,

– a description of the goods or services, and

– the amount of consideration for the supply.

Helpfully, the low value transaction threshold for taxable supplies has been increased from $50 to $200. And that is part of a drive to simplify recordkeeping requirements for a large number of low value transactions.

There are now three value thresholds for the general meaning of taxable supply information and the information requirements for each of these are mutually exclusive. The thresholds are:

– Supplies exceeding $1,000,

– Supplies between $200 and $1,000,

– and then those for supplies not exceeding $200.

All these changes come into effect from 1st April next year, although, as I mentioned, the changes to the buyer created taxable supply information have already taken effect. As noted, existing systems will still remain compliant. So, there’s no need to dramatically go out and change everything to meet the new requirements. Inland Revenue will continue to release information about the changes over the coming months.

Supreme Court justices display worrying lack of tax knowledge in key decision

Last Friday, the Supreme Court released its decision in the case of Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. This case has been watched with some keen interest by tax professionals. It relates to a series of transactions that took place in 2003, as a result of which DHNZ, a predecessor to Frucor Suntory, claimed interest deductions totalling $66 million in respect of an advance made by Deutsche Bank.

Inland Revenue sought to restrict the interest deductions totalling just over $22 million dollars claimed for the 2006 and 2007 income years on the grounds the funding arrangements constituted tax avoidance. Just for good measure, they also levied shortfall penalties totalling $3.8 million for the two years because they considered the tax avoidance was abusive.

The case reached the High Court in 2018, which ruled in favour of Frucor which was something of a surprise at first sight for those not familiar with the facts. Inland Revenue unsurprisingly appealed the decision and in 2020 the Court of Appeal held that the deductions did represent tax avoidance. However, the Court of Appeal did not accept the criteria for shortfall penalties had been met, so both parties were unhappy with their decision and naturally both appealed to the Supreme Court.

Last Friday it ruled by a 4 to 1 majority that the arrangement did represent tax avoidance and the shortfall penalties were correct as the tax position adopted by DHNZ (Frucor) was unacceptable and abusive as DHNZ acted with the dominant purpose of obtaining tax advantages.

Now, in some ways, the Supreme Court’s ruling is unsurprising. New Zealand courts have taken a fairly hard line on what is perceived as tax avoidance for the last 15 years or so. But there’s still a number of points of interest here. Firstly, you will note the length of time involved: the transaction happened in 2003. The assessments, which are the subject of the appeal, were for the 2006 and 2007 tax years. And there’s nothing I’ve seen yet explaining why it took nearly so long to reach the High Court. Under the principle of justice delayed is justice denied it’s concerning to see the amount of time involved.

Then there is the imposition of shortfall penalties, which seems harsh. If you are taking something all the way to the Supreme Court, you know you’re arguing on the margins. Nine judges looked at the matter and five said no shortfall penalties were appropriate. The only four that did think they were appropriate were the ones that mattered most because they were all on the Supreme Court. And you often see this in in court cases, the lower courts rule one way and then the Supreme Court says, nope, it’s the other way, and that’s the end of it.

But most interesting of all is the strong dissent by Justice Glazebrook in the Supreme Court now. Dissenting justice judgements are often very interesting reads, and I suspect Justice Glazebrook’s will be read and examined in quite considerable detail, given what she rebutted completely the principles adopted by the other four justices. Just for the record it’s worth noting that before she became a judge back in 2000, Justice Glazebrook was a tax partner in a law firm. She’s actually one of the co-authors of a book on the financial arrangements regime. In fact, the first edition, published back in 1999, is still had not yet been updated. So she’s got a good background in tax.

But the paragraph, I think is going to raise a few eyebrows is the penultimate one of her judgement.

[247] “The majority say that the dominant purpose of the arrangement in this case was to reduce the tax liabilities of Frucor. This despite the fact that the whole reason for the restructuring was to ensure that Danone Asia did not incur tax liabilities in Singapore, unlike the position before the refinancing where direct debt funding was provided by Danone Finance. Given that, before the refinancing, Frucor was deducting interest payments roughly equivalent to the amounts it claimed deductions for under the current arrangement, it is difficult to see how its purpose could have been to achieve a result it was already receiving (deductibility of interest) and thus difficult to see its dominant purpose as being to reduce its tax liabilities or to achieve an illegitimate tax advantage in New Zealand.”

Now that’s quite some paragraph, I have to say I don’t think I’ve seen for a while a judgement where you’ve got such completely opposite views on between the judges.

You often see differences in interpretation, but here there’s a very marked difference on the core of the case. Justice Glazebrook has questioned how it is tax avoidance in New Zealand when you consider that the real purpose of the restructure was to resolve a tax problem for the offshore parent.

It will be interesting to see feedback from other, more experienced legal practitioners and tax specialists who work in this space about this decision. As I said, I find Justice Glazebrooks dissent there quite strong, and I suspect it will generate quite a bit of commentary.

Hiding the effect of fiscal drag

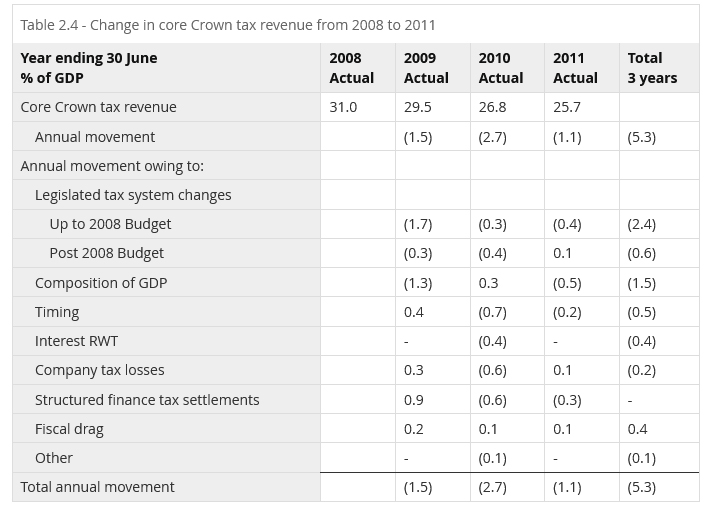

Moving on, the Government published its financial statements for the year ended 30th June 2022 on Wednesday. As you no doubt are aware by now these turned out to be better than expected and have generated quite a bit of chatter around the overall tax burden and the implications for next year’s election.

From a tax perspective, what’s interesting to see is the strong rebound in company income tax. The forecast in the 2021 Budget was that corporate tax would be just over $13 billion. By the time of this year’s budget in May the estimate had risen to $17.25 billion. In fact the total for the year was just under $19.9 billion.

For individuals the tax source deduction payments (PAYE) are up. Two factors are at play here: the well-known one of fiscal drag or bracket creep which means as people’s wages rise, they cross tax thresholds and their tax increases. On top of that, you’ve got the introduction of the new 39% tax rate. Those two combined, according to the commentary to the financial statements, represented about $1 billion of extra tax.

You have to dig very hard to find out what is the effect of bracket creep or fiscal drag, because that’s not being reported in the budget statements. You can draw your own conclusions as to why that is so. But we do know that when it was included in the 2012 Budget the effect was between 0.1 and 0.2% of GDP.

At a rough guess the current effect of fiscal drag would be somewhere around $500 Million a year.

The GST take rose to $43 billion gross with the net GST for the year being $26 billion through. Overall, as I mentioned at the top of the podcast, tax revenue, including indirect taxation, exceeded $100 billion for the first time at just under $107.9 billion.

So, lots of excitable chatter about what that means politically for tax cuts and other changes. Speaking on RNZ’s The Panel yesterday afternoon, (about 12 minutes in) I reiterated what I have said elsewhere that we need to do more about the tax brackets at the bottom end because that’s where the effects of fiscal drag are the hardest. The non-indexation of income tax and Working for Families thresholds means there are people on say $50,000 a year & receiving Working for Families who are on an effective marginal tax rate of 57%.

Roasting the idea of GST exemptions

Obviously what went on over in the UK has also attracted attention. This week the UK Government abandoned its higher rate tax cuts in the face of extreme political pressure from all sides, including Conservative MPs. It’s been very interesting and entertaining to watch a really classic example of the “Order, Counter-order, Disorder” maxim. And I do wonder how Prime Minister Liz Truss and her [Finance Minister] Kwasi Kwarteng are going to survive.

And finally, speaking of the UK, one of the things that comes up in discussions about how do we help with the cost of living is a not unreasonable suggestion on the face of it, to remove GST on certain foods. Now I’m in the GST purist camp here. I don’t believe we should do that. To repeat a point I’ve made several times, if you are trying to help people who have not enough income, give them more income. Any changes to the GST system such as zero-rating food benefits everybody and therefore are also more expensive as a consequence. And that idea of targeted assistance is consistently noted by the Tax Working Group and also the Welfare Expert Advisory Group.

But there’s another reason why you wouldn’t want to do it unless you wanted some inadvertent laughs. And that is the absurdity of the distinction which happens at the point where you are trying to determine whether a particular product is zero rated or standard rated. Now, Britain, with its VAT (value added tax) regime, has produced a number of very entertaining cases on this. I think people may be aware of the Max Jaffa case, which involves the distinction between a biscuit (standard rated) and a cake (zero-rated).

But this week I was alerted to one which is even more spectacularly hilarious, and it involved marshmallows of unusual size, which really sounds like something a line from The Princess Bride. A VAT tribunal case ruled that marshmallows of an unusual size are 0%, but standard sized marshmallows were standard rated at 20%. As one commentator noted, it’s sometimes very difficult to decide whether a VAT case is indistinguishable from satire.

This case involved a £470,000 dispute between Innovative Bites Ltd and H.M. Revenue Customs about the product “Mega marshmallows”. The VAT tribunal ruled that mega marshmallows were zero rated because they have to be roasted before they could be consumed and therefore not a standard rated snack.

On that bombshell, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!