- the winners of this year’s Tax Policy Charitable Trust Scholarship are announced.

- A preview of next week’s United Kingdom Budget.

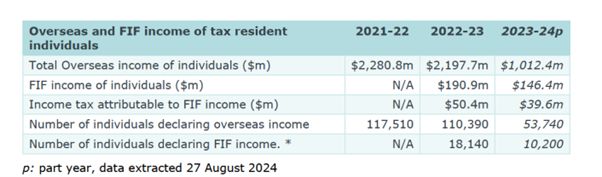

Inland Revenue regularly releases Official Information Act requests that it has answered. One from last month was in relation to the amount of overseas income reported by individuals. My attention was first drawn to this OIA by Robyn Walker of Deloitte (thanks Robyn) who like me, and many other professionals were quite surprised when we saw the number of people reporting Foreign Investment Fund (FIF) income.

Is there under-reporting?

According to Inland Revenue, which only really started gathering exact data on this in the 2023 income year, 18,140 individuals reported a total of $190.9 million of FIF income for that year.

When you consider that based on the latest Census 28% of the population of New Zealand were born outside the country, it seems to me that the amount of overseas income being reported, and in particular in relation to FIF income, is probably below what we would expect to see. And that’s what caught Robyn’s eye. One or two other advisors have made the same comment.

It could be because we deal in this space, there’s a bit of an echo chamber effect because we will regularly advise on these matters. If we’re dealing with a fairly high proportion of overseas migrants, and our practise Baucher Consulting does, then it’s natural we might think there is a broader scale of overseas investments generally.

But the number seems incredibly low in relation to the FIF income being reported, and also generally speaking, when you think about the number of overseas persons declaring overseas income.

A question of non-compliance

The issue therefore arises as to whether in fact we have non-compliance happening. I raised my concerns about this with Jenny Ruth of Good Returns. In our practice we regularly encounter clients coming to us who have realised that they have not been compliant with the Foreign Investment Fund regime. In some cases, they’ve come to us on another matter and in the course of discussions, it’s emerged that they have not been compliant. At any one time we are usually filing disclosures and bringing tax returns up to date.

Complexity and non-compliance

In my view this possible level of non-compliance speaks to the complexity of the Foreign Investment Fund regime. It’s not a capital gains tax, it operates as a quasi-wealth tax. That’s how I describe it to taxpayers and whenever I’m speaking to overseas advisors on the matter.

Old habits die hard

The FIF regime is not intuitive and I’m often dealing with people who come from overseas jurisdictions which have capital gains tax. They’re aware that where there’s a disposal there is a tax point that’s triggered. This may seem strange to say, but I’ve found in my practise that people’s tax habits developed in their country of origin take long to die even after many years in New Zealand.

Now, coincidentally, just to give some idea of the complexities involved in the FIF regime, Inland Revenue has just released a draft interpretation statement for consultation on the income tax issues involved in using the cost method to determine FIF income.

The Cost Method and the FIF regime

Those who have investments within the regime will be familiar that a fair dividend rate of 5% will apply to the value of your Foreign Investment Fund interest as of the start of the tax year. The alternative is to look at the total realised and unrealised gains of your portfolio including dividends over the year and report that instead, if that’s the lower amount. Incidentally that option way is not available for KiwiSaver funds or for the New Zealand Super Fund which is why it’s regularly one of the largest taxpayers in the country.

But what happens if your FIF interest is unlisted? The cost method generally applies when an investor is holding shares in an unlisted overseas company. And so this interpretation statement explains when that cost method may be applied and how it operates. As is now common, there are lots of examples and flow charts which explain the process. But the fact that there’s an interpretation statement on this matter which has set out and explains when you can or cannot use it the methodology, speaks to the complexity of the regime, and also the compliance costs involved in this.

The cost regime is generally to be used when the values of shares are not readily available. As part of that it will require the taxpayers to find and obtain an initial market value of the overseas stock, so they have a base cost for the purposes of the FIF calculations. It’s possible in some circumstances to use the net asset value of the accounts, usually if those accounts are audited.

Practical problems with the FIF regime

But as can be seen when people are required to obtain independent valuations this means additional compliance costs in what is already quite an involved regime. The other reason why the FIF regime causes consternation amongst taxpayers is the tax liability is not based on cash flows. A tax liability arises under the FIF regime even if the company in question is a growth company and not paying any dividends. Earlier this year I discussed a report The place where talent does not want to live, about the issues the FIF regime creates for startup companies and New Zealand resident investors.

All of this just underlines the complexities of the FIF regime. As I told Jenny Ruth of Good Returns, whenever I hear someone arguing “Oh well, capital gains tax is very complicated” I immediately think, ‘Well, they’ve clearly never dealt with the Foreign Investment Fund or financial arrangements regimes.’

Complexity leads to non-compliance?

Anyway, the upshot of all of this is there’s probably a considerable amount of non-compliance happening in in relation to reporting of FIF income. And Inland Revenue are now cracking down on this by making use of the information now available to them under the Common Reporting Standards on the Automatic Exchange of Information.

Now this is an OECD information sharing initiative which started in 2017. Inland Revenue which started a compliance project in late 2019 using this data. But then Covid turned up so that project had to be parked but it has now been reinitiated. As a result, I’ve recently taken on clients contacted by Inland Revenue advising it has received information under the Common Reporting Standards. The clients have been asked for an explanation about their apparent non-disclosure of overseas income and ‘invited’ to make the relevant income disclosures.

Keep in mind also that in the May Budget Inland Revenue was given $116 million over the next four years for investigation activity. The upshot is we’re probably going to see a lot more disclosures about FIF income when we’re looking at the numbers for the 2025 year.

In the meantime, I urge readers and listeners to consider their position and check with their tax advisor if they think they may have investments within the Foreign Investment Fund regime and have not made the disclosures they should have.

And the winners are…

Now moving on, the winners of this year’s Tax Policy Charitable Scholarship were announced in Wellington on Tuesday night. The Tax Policy Charitable Trust was established by Tax Management New Zealand and its founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa New Zealand. Three of this year’s finalists, Matthew Handford, Claudia Siriwardena and Matthew Seddon have appeared on the podcast over the past few months discussing their proposals.

The format for Tuesday night was that the four finalists, having already prepared a 4000-word final submission, would then present their proposals to a judging panel and the audience, as part of a Q&A.

The judging panel consisted of Joanne Hodge, who’s a former tax partner at Bell Gully and a member of the last Tax Working group. Professor Craig Elliffe Professor of Law at the University of Auckland and another member of the last Tax Working Group. Nick Clark, Senior Fellow of Economics and Advocacy at the New Zealand Initiative and Chris Cunniffe, Strategic Advisor of Tax Management New Zealand. A pretty daunting panel to be frank.

According to Chris Cunniffe “the quality of the presentations on Tuesday night was exceptionally good” and in the end the judges were unable to separate Matthew Seddon and Andrew Paynter.

Winners Andrew Paynter (left) and Matthew Seddon (right) with the judging panel

Matthew’s proposal, is to extend withholding taxes to payments received by independent contractors.

Andrew works as a policy adviser in Inland Revenue. His proposal is to increase the GST rate to 17.5% and introduce a GST refund tax credit for lower and middle income individuals. This would be a means tested individualised credit and would be paid at a flat rate to all qualifying tax resident individuals under a particular income threshold. It’s a fascinating proposal and I’ve reached out to Andrew about appearing on the podcast in the near future.

In the meantime, congratulations to the winners Andrew and Matthew and also to the runners up Claudia and Matthew Handford. Don’t be surprised if you see something popping up in legislation in the near future involving one or more of these proposals. They were all of a very high standard this year, so well done everyone.

UK Budget preview

And finally this week, a brief preview of next week’s UK budget. The new Labour government has been in office now for three months and it’s finally getting around to announcing its first budget. That is part of what they call the Autumn budget statement.

The UK has two budget statements a year, but this one is going to be quite significant because there’s a lot of noise and chatter around tax changes. A quite significant part of my practice at the moment is advising New Zealanders going to the UK, and migrants coming here, and the tax implications involved.

I’m therefore watching this budget with some interest because we know there are going to be two proposals, the final details of which will come out, which will have an impact for quite a number of people. Firstly the so-called foreign income and gains exemption, which is the UK equivalent of our transitional resident’s exemption. This was first announced by the Conservatives in their Spring budget in March this year, but then the General Election happened so full details of the proposals were not released.

Related to that, and this is surprisingly important for a large number of people, are changes to the domicile regime also announced by the Conservatives. At present domicile is incredibly important for determining a person’s liability for UK inheritance tax, which is payable at 40% above net assets over £325,000. It appears the UK will move to a more residence-based regime, but we don’t yet know the details.

I’m therefore watching this with great interest and there are bound to be other measures which are likely to affect New Zealanders going to the UK, or the UK migrants moving here. We’ll therefore keep you abreast of developments in next week’s podcast.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.