Treasury Analytical Note examines the effects of taxes and benefits for the 2018-19 tax year

The Australian Tax Office gets heavy with the Exclusive Brethren – will Inland Revenue follow suit?

Understandably the start of the new tax year on 1st April and the increase in interest deductibility for residential investment property to 80% was generally greeted by residential property investors with enthusiasm. Users of apps such as Airbnb and Uber, on the other hand, were less enthusiastic because the provisions relating to GST on listed services also took effect on 1st April. It has become clear that this change has caused some confusion and led indirectly to price rises.

Now GST on listed services refers to online marketplace operators who “facilitate the sale of listed service”. This is the so-called “Apps Tax”, which National promised to repeal when it was campaigning in last year’s election but then decided to keep it because it needed the money to make up for the loss of its overseas buyers tax.

These rules apply to the likes of Airbnb, Uber, Ola, and Bookabach which facilitate the sale of related the services. They now have to collect and return GST when the relevant service is performed, provided or received in New Zealand. It doesn’t matter whether or not the seller, the actual person doing the providing of the Uber or Airbnb, is GST registered. (For those already GST registered the change will have little effect).

Confusion and an unnecessary price increase?

However, a significant number of those providing the Uber or Airbnb, are not GST registered because the total services they provide annually are below the GST registration threshold of $60,000. But the introduction of the apps tax has prompted some of these non-registered persons to effectively increase their prices 15% to take account of the GST charge. However, this overlooks that though as part of the changes those non-GST registered persons can expect a 8.5% rebate under the flat-rate credit regime scheme.

What happens here is the offshore marketplace (Uber or Airbnb) will collect 15% GST on the booking but then pass 8.5% of that to the persons actually providing the Uber or Airbnb. But as an article in The Press notes, it appears many people now think they are GST registered and have effectively increased their prices by 15%. As Robyn Walker of Deloitte said, there definitely appears to be some confusion around hosts about this law change, and probably many don’t fully appreciate that they’re getting this 8.5% rebate.

As GST specialist Allan Bullot of Deloitte, noted there is a lot of confusion with Airbnb. It’s a complicated area, and something Airbnb providers are very careful about is registering for GST because of the fear they might have to pay GST if they sell the property to someone who’s not GST registered. In which case they effectively had to pay GST on the capital gain.

It appears what we’re seeing here is that those who have been brought into the new flat rate credit scheme haven’t yet quite worked out how the new rules will work for them. I would expect things to settle down in time and maybe Inland Revenue might put out more guidance. But it would appear that some providers are getting an accidental windfall at this point, although the increase is taxable for income tax purposes. Anyway, watch this space to see how this plays out and whether there’s some tweaking to the rules as this scheme beds in.

Treasury analyses the effects of tax and income

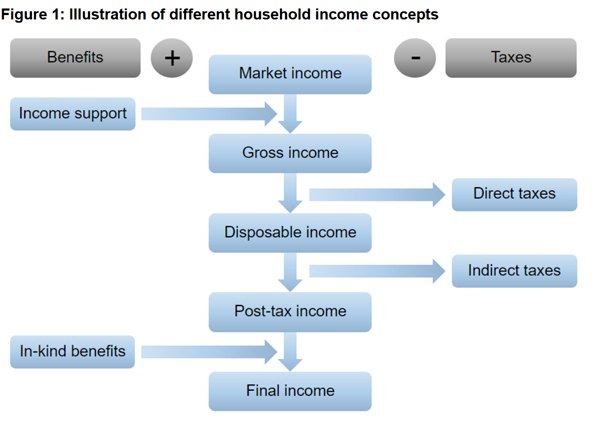

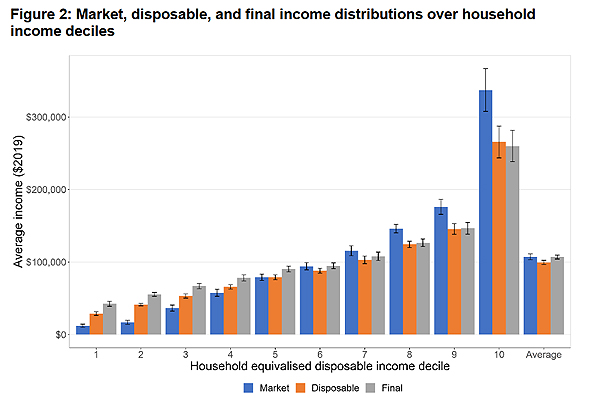

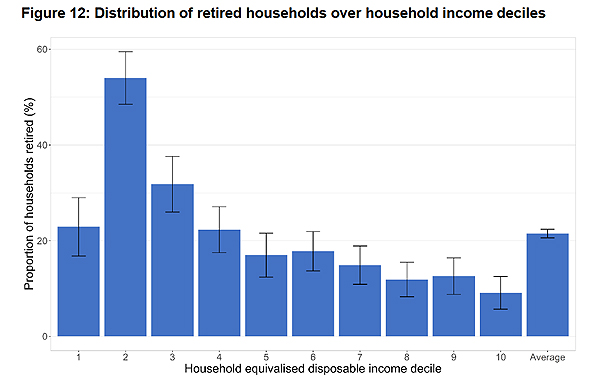

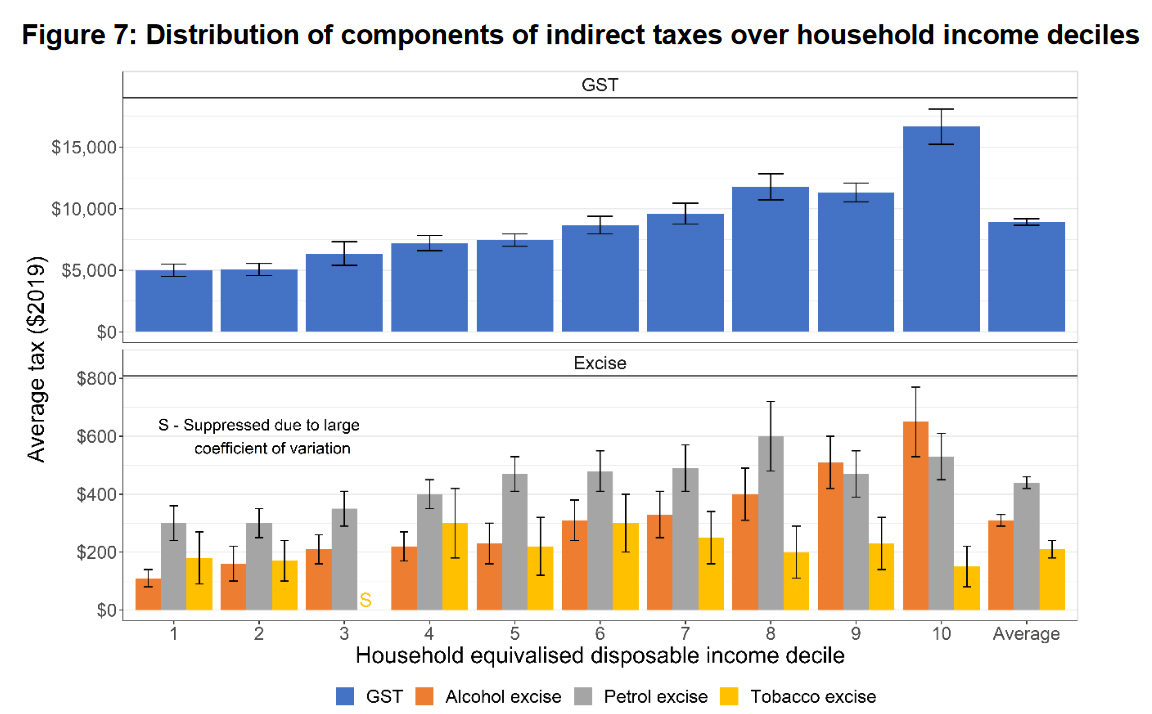

Moving on, just before the end of the tax year, Treasury produced an interesting Analytical Note on the effects of taxes and benefits on household incomes in tax year 2018 – 2019. This is interesting in a number of ways because frequently when people are talking about the effective tax burden, they look at the impact of direct taxation on a person’s pre-tax income.

Some have pointed out this is not really a true measure of a person’s net tax burden. They’re referring to the effect of transfers that people might receive from government in the form of Working for Families or New Zealand Super, but also the indirect transfers such as education and healthcare.

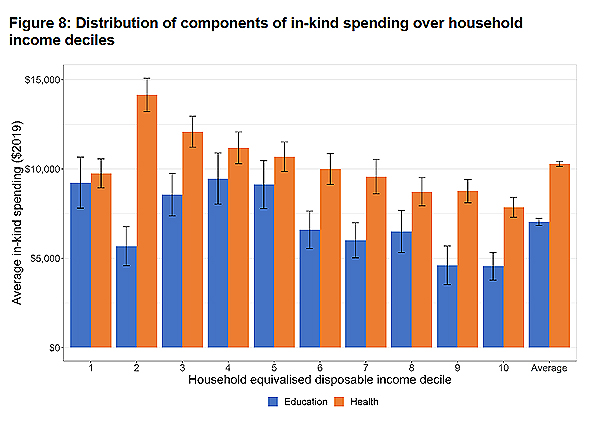

This paper tries to examine that for the 2018-19 tax year and what it does is calculate a household’s “final income” which represents net income after direct and indirect taxes and then adds an estimate of the government spending on health and education services received in kind.

As the paper notes basically when you just look at disposable income, that is market income plus transfers, such as Working for Families credits or New Zealand Super, these are incomes are generally lower than market incomes on average over the population of New Zealand, and fairly unequally distributed. However, once you bring in indirect taxes and in kind benefit payments to get final incomes as defined, these are significantly more equally distributed than disposable incomes and close to market incomes when averaged over all households.

Yes, but what about Gini?

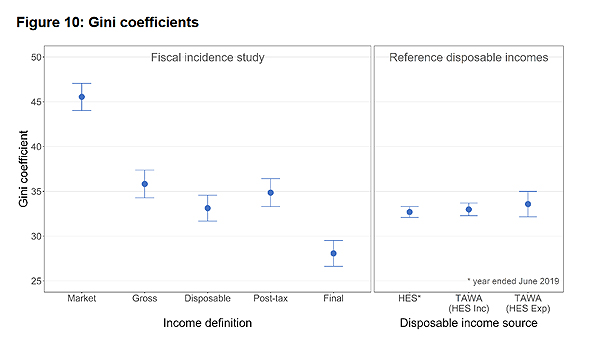

The Note also considers the Gini coefficient. This is the measure of inequality, where the higher the number, the more inequality society is. The Gini coefficient starts at 45.6 ± 1.5, and that drops to 35.8 once you bring in income support payments. Once you include consumption taxes and the benefits in kind such as health and education you end up with a Gini coefficient of 28.1 which is considerably lower and indicative of a much more equal society.

What the Treasury analysis did was to take 66% of all core Crown tax revenue and 68% of core Crown expenditure and allocated that to New Zealand households. Although the effect is approximately neutral as the note describes the effect is unevenly distributed. Households in the bottom five “equivalised disposable income deciles” received on average more in government services than they paid in taxes, whereas the opposite is true for houses in the top four deciles.

The second decile is the one where there’s a large amount of support happening. This is because there’s a fairly high concentration of New Zealand super recipients in that second docile.

The Note also considers “retired households”, where one of the people in the household is receiving New Zealand super.

“Drink yourself more bliss”

I was amused to see in the analysis of indirect taxes a comment about the average alcohol excise amounts increasing reasonably steady with each decile household equivalent. In other words, the richer the decile, the more they drink. That is a crude summary but it did amuse me.

As I noted, the Treasury analysis covers GST and the effect of economic benefits in kind. There was some commentary at the time of last year’s High Wealth Individual report that it wasn’t really quite fair because it didn’t take into account what the impact of GST and government benefits in kind. This is interesting to see, and I definitely recommend having a read of the note which is a reasonably easy read.

The Australian Tax Office raids the Exclusive Brethren’s business operations

And finally this week, a story coming out of Australia caught my eye about the Australian Tax Office (“the ATO”) raiding multiple premises associated with the global headquarters of Universal Business Team (UBT) on March 19th. UBT is a Sydney registered company that provides services and advicee to about 3000 exclusive Brethren owned businesses in 19 countries.

ATO investigators also apparently raided the head offices of a number of Brethren run companies, including OneSchool Global. In what would also be the standard procedure here, they confiscated phones, computers, documents and other materials. This was done as part of what the ATO call a “no notice raid”. Inland Revenue can do such raids as well, but the point is, it’s not done very often, and the fact that this has happened is extremely intriguing to see.

One of the things that I see frequently pop up in the comments of these transcripts, are questions/ pushback about charities having an exemption from tax on their business profits. It’s more complicated than that, but it’s there’s an obvious tension there. (Again thank you to all those who contribute, your comments are read even if I don’t always respond).

On this point I recall a discussion I had with the late Michael Cullen when he was chairing the last tax working group. During a roadshow event I asked him if there was anything which had surprised him during his role. He replied that he had been surprised by the scale of the charitable sector. He and the group had some concerns about whether in fact, all the charitable donations were being used for charity. In particular whether donations made under an exemption to an exempt business were in fact being used for a charitable purpose. The Tax Working Group’s final report noted:

“80. …the income tax exemption for charitable entities’ trading operations was perceived by some submitters to provide an unfair advantage over commercial entities’ trading operations.

81. notes, however, that the underlying issue is the extent to which charitable entities are accumulating surpluses rather than distributing or applying those surpluses for the benefit of their charitable activities.”

The Sunday Star Times asked Inland Revenue to comment on the ATO’s action but Inland Revenue just dropped a dead bat on it. But I would think, as the Sunday Star Times said, any information relating to New Zealand businesses that came into the ATO’s hands would proactively be passed on under the Convention on Mutual Administration Assistance and Tax Matters, part of the double tax agreement between Australia and New Zealand.

The scale of information exchange which goes on between tax authorities is very largely unknown, but it’s probably one of the most revolutionary changes to the tax landscape which has happened in the last five to 10 years. I don’t think we’ve yet seen anything like the impact that it will have.

Will Inland Revenue follow suit?

In summary the ATO clearly feels that it’s justified in launching a “No notice raid”. The question is whether Inland Revenue is considering something similar or is it just going to sit back and watch carefully? We don’t know, it won’t say, but you can be sure that it will be watching very closely to see what findings that come out of the ATO raid. If it does get anything interesting from the ATO, expect to see something similar happen here.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Submissions close next Friday on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the tax bill introduced alongside the Budget. The bill, as is typical, sets the annual rates for the current year ending 31st March 2024, but also has key provisions relating to the establishment of the legislative basis for the implementation of the Pillar Two international tax proposals at a later date. Separately, there are key provisions for increasing the trustee tax rate from 33% to 39%, with effect from 1st April next year.

The main part of the bill involves preparing the groundwork for the OECD’s Pillar Two multinational tax proposals. These are part of the Global Base Erosion and Profit Shifting (BEPS) initiative which is intended to introduce a global minimum corporate tax rate of 15%. Now, I generally have no involvement with clients that would be affected by these proposals which are targeted at the large multinationals. Most of the clients I deal with on international affairs are much, much smaller scale operations.

But there will be plenty of expert commentary and submissions on this particular bill because it will affect significantly large multinationals, those with international presence and gross turnover exceeding €750 million annually in any two of the preceding four years. It’s a fairly select group. There may be some tweaks as a result of submissions being made, but I would expect this to go through largely unchanged. But it will be interesting to see what submissions are made around this.

Increasing the trustee tax rate – maybe not quite such an obvious move

Of much more direct interest to many more clients and probably also much more controversial is the proposal to raise the trustee tax rate from 33% to 39%.

Now, conceptually aligning the trustee tax rate with the top personal income tax rate makes sense. We see that in other jurisdictions. Practically speaking, however, given the incredibly diverse and prolific nature of trusts in New Zealand, this would seem to be a much more practically difficult issue to implement it.

In discussions with other advisors, a couple of points have emerged. There seems to be a general consensus that some form of de minimis threshold is appropriate to take account of the fact that there are so many more trusts and they have operated on a policy of not generally distributing income because the 33% tax rate probably aligned with most of the income tax rates applicable to most of the beneficiaries. The 39% tax rate only kicks in above $180,000 income and that’s a much smaller group.

The argument which has been raised is that the measure, although conceptually correct, is actually in response to a small group. And therefore, it has a rather indiscriminate effect on people whose aggregate income including that of a trust, would not cross the $180,000 threshold. The suggestion has been made that we should have some form of de minimis threshold. I’ve seen suggestions raising between $15 and $50,000.

In response to this proposal Inland Revenue officials have asked “What’s to stop people setting up a number of trusts to maximise the advantage of the differing thresholds?” Well, two things. One, first of all, practically the cost involved of establishing these trusts, you would typically not get much change out $2-3,000 plus GST. But more importantly, you then have ongoing costs involved because following the Trusts Act 2019 coming into force in early 2021, trustees are much more conscious of their obligations including providing information to beneficiaries.

But more importantly, if someone established ten trusts like that and then divided up assets and income producing assets so as to maximise any potential threshold that would run square head on into Inland Revenue’s existing anti-avoidance provisions. Therefore, in practical terms, I think Inland Revenue’s arguments about the risk aren’t really a starter. There is also the question that there are there are increasing compliance costs involved with running trusts now as I just mentioned.

There’s also something Inland Revenue tends to glide around in my view and that’s its very, very narrow view of Section 6A of the Tax Administration Act. This states Inland Revenue’s duty is to collect the highest amount of revenue that is practicable over time, bearing in mind the costs of compliance. Keeping that in mind some form of de minimis seems a not reasonable approach. Otherwise, trustees may feel that they are obliged to do a load of distributions to beneficiaries just to minimise the tax payable.

I have actually encountered scenarios where trusts were established which could have done that and minimise the tax payable but didn’t do so for a variety of reasons. So it could be that inadvertently Inland Revenue may trigger the trustees to actually distribute income at lower tax rates than they were doing previously. I’m certainly watching to see how the Select Committee responds to this point.

Deceased estates potentially unfairly penalised?

The second point about the 39% tax rate increase is how it will apply to estates of deceased persons. The proposal is the 39% rate will apply to a deceased estate after 12 months have passed since the person died. Now, my immediate reaction to that proposal when I read it was that period was way too short, and that has been confirmed in subsequent discussions with other tax practitioners and lawyers. In fact, right now I’m involved with the tax affairs of an estate where more than three years has passed since the death of the deceased person.

The majority view of the lawyers I’ve spoken to on the matter is the minimum period should be at least 24 months and probably somewhere between 36 and 48 months would be much more realistic. I would be interested to see what happens here; particularly about just how many law firms do make submissions on this. I’ve made the law firms I work with aware of the issue and recommend they do submit. Select committees sometimes hear a lot from the same people, but they are always particularly interested in hearing from people who don’t normally submit but are doing so in this case on the practical basis “Our experience is this would be not a good move” or “We would support it”, whatever.

Anyway, submissions on this bill close next Friday. If you have concerns about any of these measures I’ve discussed, make a submission to the Finance and Expenditure Select Committee using this link.

The IMF holds forth on cryptocurrencies

Now moving on, this week the International Monetary Fund, the IMF, released a working paper on the taxation of crypto currencies. https://www.imf.org/en/Publications/WP/Issues/2023/06/30/Taxing-Cryptoc… This is an absolutely fascinating paper, it’s actually one of the most interesting papers on the taxation of cryptocurrencies than I have seen since crypto assets moved into the mainstream over the last five years.

In short, the IMF’s view is that tax systems need updating to handle the challenges posed by crypto assets, particularly in relation to their anonymity and their decentralised nature. And these, in the IMF’s view, make it hard to establish and maintain effective third-party reporting systems such as we use here in the banks or the international OECD’s Common Reporting Standards on the Automatic Exchange of Information.

It’s a very readable paper which starts by pointing out that after basically starting from zero in 2008, the market value of crypto assets peaked in November 2021 at about USD3 trillion USD (nearly NZD5 trillion). Although estimates vary because the surveys are self-selected, maybe perhaps 20% of the adult population in the U.S. and 10% of the adults in the U.K. hold or have held crypto assets. And the number of global users could be as many as 400 million people. On the other hand, although USD3 trillion sounds like a lot, it’s only about 3% of the global value of equities.

But the paper notes the potential for disruption, which is one of the founding ethos of Bitcoin and the crypto asset world, is quite significant. There are all sorts of questions around the tax impact of all these colossal capital gains suddenly arising and then the potential impact of losses, now that USD 3 trillion valuation is down to around $1 trillion. What’s going to happen with those $2 trillion of losses? Are they being claimed?

The paper really is very, very interesting in covering a whole number of topics. And basically it sums up the problem as being tax systems were not designed for a world in which assets could be traded and transactions completed in anything other than national currencies. It has some interesting comments about the effect of crypto billionaires. Apparently 19 were on the Forbes list, the richest list in America in April 2022. In an interesting aside the paper comments about “a loosely defined sense that much wealth channelled into crypto escapes proper taxation appears to have become part of the wider mood of dissatisfaction around the taxation of the rich.”

Blockchain efficiencies for tax administrations?

Yes, there are certainly crypto billionaires, but a lot of ordinary people probably piled into crypto because they saw an opportunity to realise substantial gains. How they declare those is of course where this paper is focussed on. It also notes that much is made of blockchain technology and it the working paper notes that the information blockchains contain on the history of transactions is actually remarkably transparent which

“might ultimately prove valuable for tax administration; and the use of smart contracts (self-executing programs) within blockchains, for example, might in principle help secure chains of VAT compliance and enforce withholding.”

What this paper picks up on is concerns I haven’t seen too much discussion of around the VAT (value added tax) or GST consequences of transactions using crypto. The paper’s section on externalities picks up on an issue which has is often raised in relation to crypto, and that’s the carbon effect of mining. It notes that the associated carbon emissions are cause for considerable concern including an estimate that in 2021 Bitcoin and Ethereum mining used more electricity than either Bangladesh or Belgium and were responsible for generating 0.28% of global greenhouse gas emissions. It suggests there maybe should be a charge on mining in relation to that effect.

Overall, the paper does not propose solutions. It is a working paper which is really raising all the issues. Now, it notes which I’ve mentioned recently, that the OECD has introduced its Crypto-Asset Reporting Framework, which is to extend the Common Reporting Standards reporting to the crypto world. But in the IMF’s view, “implementation remains some way in the future and in any case will not in itself resolve the issues challenges proposal posed by decentralised trading.”

Overall, a very comprehensive and readable paper which brings a big picture thinking to the issues the taxation of crypto crypto presents. I highly recommend reading it.

Government tax revenue behind forecast

And finally this week, the Government released its financial statements for the 11 months to 31st May. Of note immediately was that total tax revenue of $102.8 billion was $2 billion below forecast. Now $1.87 billion of that shortfall related to lower corporate income tax. GST was also $104 million below forecast and also another note that the economy is slowing down.

On the other hand, the rise in interest rates means that the amount of resident withholding tax collected on interest is $242 million ahead of forecast. Incidentally, the withholding taxes on dividends are also $12 million higher than forecast. That latter point may be in reference to what we discussed at the opening of the podcast, with the trustee tax rate rising to 39%, some more dividends are being paid ahead of that rate taking effect.

Government core expenses at $145.6 billion were actually $120 million below forecast. Interest costs were just under $6.6 billion, $134 million higher than the Budget estimate. Overall, the government debt rose by $5.1 billion to $73.3 billion, but net that’s the equivalent of 18.9% of GDP. The Government is still in the black. Overall, based on 2021 numbers, its net worth of $170.4 billion, which is roughly 44% of GDP, keeps it as one of the few OECD countries with a positive net worth.

There’ll be plenty of talk about budget deficits, etc. going forward in the election campaign. And we’ll be paying attention to what the parties say on tax. But it’s probably just worthwhile keeping it in context that the Government’s balance sheet is reasonably solid. You wouldn’t want it to be running away rapidly, but when you look at what’s going on in the United States where they basically cobbled together ad lib budgets to just paper over the cracks until the next crisis emerges, we are in a reasonably strong position.

How that balance sheet is maintained and used to brace ourselves for the impact of climate change is a major challenge. I think we now have a major issue in terms of having to basically fund adaptation by having to fund moving people out of at-risk areas. Cyclone Gabrielle rendered 700 homes unliveable. That could add up to maybe a billion dollars. Although a billion dollars in the context of $145 billion government spending is well under 1%, a billion dollars year in, year out is money that is not going into other areas that people want for health, education, etc. So anyway, the Government’s books are in reasonably good shape, but there are strains ahead.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

As is well known, income tax thresholds have not been increased since October 2010. What also gets overlooked is that the GST threshold of $60,000 was last adjusted in April 2009. And this week, Stuff ran a story about Kristen Murray, who has petitioned Parliament to have the GST threshold increased to $75,000.

She argued in her petition that the lower threshold is crippling small businesses. Inland Revenue disagrees but Kristen has gained the support of BusinessNZ, who supports regular indexation of tax thresholds.

A BusinessNZ economist noted that the effect of inflation means that the $60,000 threshold set back in 1 April 2009 should now be roughly about $82,000. Now the driving principle of the GST system is a broad based, low-rate principal approach and a reasonably low threshold is consistent with that approach.

GST came into effect on the 1st of October 1986 and the threshold set then was $24,000.

Looking at the table above it has actually more or less kept pace with inflation based on where it started – until now.

Notwithstanding that, given that it’s now 14 years since it was last adjusted, some form of increase to the threshold is not unreasonable. And the number of businesses a threshold change could affect is quite significant.

According to Inland Revenue data supplied to Parliament’s Finance and Expenditure Committee in 2022 there were 264,457 taxpayers who are GST registered, but with turnover of $60,000 or less. There’s another 27,000 or so with turnover between $60 and $75,000. So, as we said, increasing the GST threshold could take a large number of taxpayers theoretically out of the GST net.

But GST has an interesting effect and it’s also seen officially as a main pillar against tax evasion because of its comprehensive nature. Pretty much everyone finishes up paying GST somewhere along the line, even those within the cash economy. They still finish up paying GST when they’re purchasing supplies, food, petrol and the like. So, there would be a natural reluctance on the part of Inland Revenue to increase that threshold substantially. But to repeat an earlier point after 14 years, it’s not unreasonable.

By the way, Kristen’s suggested $75,000 threshold would actually bring it in line to the Australian threshold, which is A$75,000. I think one of the things they could also borrow from Australia is perhaps allow for quarterly GST returns.

There are therefore risks about the GST threshold being too high and the base being narrowed, but if they kept it too low then businesses may deliberately hold back from growing and crossing the GST registration threshold.

Over in the UK, where the equivalent of GST, value added tax or VAT, registration threshold is £85,000, there is in fact a very noticeable drop-off effect around that threshold.

The reason possibly might be because once you are VAT registered, you’re charging VAT at 20%, so businesses that can’t see themselves growing substantially quickly pass that threshold may be quite reluctant to effectively increase prices by 20%.

Now, I’m not aware of any such evidence here in New Zealand. And I think the issue, which Kristen pointed out, compliance is a bigger issue for micro-businesses. With compliance there comes a point where there is an irreducible minimum. Whether we’re at that point there know I don’t know. As I mentioned earlier, offering opportunities around quarterly reporting would perhaps help. And these days, the advent of software programs such as Xero, MYOB, and Hnry do help micro-businesses manage their tax much more effectively.

But in terms of GST and tax administration, I think the next big step would be to zero rate all supplies between GST registered businesses. That would help put an end to the merry go round which goes on right now where a GST registered business charges another GST registered business GST, collects and pays that GST to Inland Revenue, while the GST registered business, which has just paid GST, then claims it back from Inland Revenue. Overall, there’s no net GST effect. I therefore think moving to zero rate such B2B transactions is a logical step. How far away that is, I don’t know. It doesn’t appear to be on Inland Revenue’s work programme at this point.

At the moment, we’re left with the only other adjustment that might help microbusinesses would be to increase the GST threshold. As I said, my view is something like that should happen soon, but we’ll have to just wait and see.

Airbnb, GST and unintended consequences

Moving on, and still on GST, I came across a case this week where a residential property owner couldn’t let the property so decided to change his approach and started letting it out as an Airbnb. Airbnb letting represents taxable supplies for GST purposes. He was GST registered for another activity and he did include the Airbnb income in his GST returns.

The issue has now popped up that he wants to sell the property. And it looks like unless he is selling to a GST registered person when compulsory zero rating will apply, then he has inadvertently given himself a GST problem. If he sells the property, which remember was originally a residential property to a non-GST registered purchaser, the sale price the price will become GST inclusive, which basically will bite into his margin.

This is a good example of paying attention to what’s going on around your activities and that you should always seek advice when you propose to do something that may have GST implications. Tax is full of unintended consequences and for this particular taxpayer, I’m afraid there probably is a huge unintended consequence of basically surrendering the equivalent of 13% (the GST inclusive portion of the sale price) on a residential property sale. He was already carrying on a GST activity already and Airbnb just represented additional taxable supplies. So, for anyone thinking of switching from residential property letting to Airbnb that’s a trap to watch out for.

The Great Tax Debate – “Think of the consulting fees!”

And finally, on Friday night I was part of the Great Tax Debate organised by the Tax Policy Charitable Trust, where I and several other tax practitioners debated the proposition: A wealth tax is the best solution to wealth inequality.

I was the leader of the affirmative team, and I was ably assisted by Mat McKay of Bell Gully and Sladjana Freakley of EY. Opposing us were Robyn Walker of Deloitte, Simon Coosa of Minter Ellison, Rudd Watts and Jeremy Beckham of KPMG. Professor John Prebble, one of THE gurus of New Zealand tax, chaired the debate. We had a lot of fun on the topic including an interesting Q&A session where someone asked, “Has EY gone woke?” The answer, of course, is no.

In the end thanks mainly to some pretty shameless populism including an appeal to the base instinct of the tax consultants in the audience, “Think of the consulting fees!”, we in the affirmative team sneaked home. Before the debate started everyone was asked to register their position as a yay or nay. And then the net movement from that would determine the winner. And we managed to move the dial several points in our favour. But before the Green Party start jumping up and down celebrating “We told you people wanted a wealth tax”, over 60% were still against a wealth tax.

As I said, it was a lot of fun with plenty of laughs all around. The question about whether EY has gone woke raising one of the bigger laughs. I’d like to thank the organisers, the Tax Policy Charitable Trust, hosts Bell Gully, Professor Prebble, my team-mates, Mat and Sladjana and our opponents, Robyn, Simon and Jeremy together with the 80 plus attendees in the audience for a fun night. We hope to see more of these debates in the future.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Friday was the due date for the first instalment of Provisional ax for the year ending 31st March 2021, Provisional tax is going to be payable by anyone whose net tax for this year will exceed $5,000.

Now in the past, we’ve covered the ability to use tax pooling to give more flexibility about payments of tax, and that’s going to be particularly important for the current tax year, given our ongoing uncertainties arising from the COVID-19 pandemic. My recommendation to clients at this moment is to adopt a conservative approach. Look at paying the first instalment of tax due today but keep watching your progress and how your turnover is going. And if matters move into a tax loss position as a downturn comes through soon, then we will take steps to mitigate or deal with the next two instalments of Provisional tax.

But what if you already know you’ve got losses this year and it’s not likely to get much better for the current year? Say you’re a restauranteur or you’re in the tourism business. These are two sectors which are very clearly hit hard by the pandemic and the various lockdown measures.

Well, one of the measures introduced as part of the government’s response to the pandemic was the ability to carry tax losses back. Under this measure, if you have a tax loss for the 2020 or 2021 income years, you can carry those losses back one year. And the idea is that if you carried back to a profitable year this will mean you have overpaid tax in the prior year, and that tax can be released to help smooth your time through this ongoing pandemic.

And for most larger companies the tax loss carry-back regime is pretty straightforward. Carry back the loss one year, get a tax refund at 28% percent, and then you’ve got funds, which you can either use to meet other bills you may be behind on, or bring it forward and apply it against your current tax year liabilities such as GST or PAYE, depending on how dire the situation might be.

But one of the problems that’s emerged with the tax loss carry back rules affects a lot of smaller companies where their shareholder is also an employee. And under the rules that apply to these companies, these companies can pay out their profits to a shareholder-employee who is then responsible for the tax.

For example, say a company makes a profit of $100,000. Instead of paying tax at 28% it instead distributes it as a salary to a shareholder-employee and he or she is taxed on it at their relevant marginal rates. For someone on $100,000 with no other income, that roughly works out to about $24,000. So, there’s a tax benefit to shareholder-employees because of the gradual increase in tax rates for individuals.

But the problem that’s emerged wasn’t really addressed in the current legislation. What do you do if you carry a loss back for a company with a shareholder employee? The carried back loss is not much used to that particular company because they’ve already reduced their profit to nil by distributing it to the shareholder-employee.

And by the way, I note there was a Radio New Zealand report noting that about $2 billion dollars in wage subsidies has been paid to companies that do not appear to have paid any company income tax. It’s highly likely many of those companies have shareholder employees and it is the shareholder employee who has paid the tax using the mechanism I just explained where the whole or substantial amount of the company’s profit is paid out to the shareholder-employee.

So the tax loss carry back rules don’t work too well for small micro businesses that use a shareholder-employee mechanism. And it’s something we’ll need to be looked at if there is a permanent iteration of these rules, which I believe should happen.

But it’s also why the small business sector and accountants have not looked on this particular measure with a great deal of enthusiasm yet. Because of those complexities how do we deal with these tax losses that are brought back? Do you rewrite the whole position in the prior year? And then what does that do for other matters that are related to that person’s income, such as social assistance, ACC earner levies? The amount of ACC you may claim if you have an accident is dependent on your salary as a shareholder-employee.

So, there’s a lot of complicated issues to work through. But the tax loss mechanism is there. It works very well for companies which don’t have shareholder-employees and individuals trading for themselves or trusts can use the loss carryback rules in either the 2020 or 2021 income years.

Converting from short-term to long-term rental accommodation.

Moving on, Airbnbs in the tourism sector will also have been hit very hard by the pandemic and the collapse in overseas tourism and the substantial decline in domestic tourism. So what has happened is some of these Airbnbs have reversed a trend that was developing, and have moved back into providing longer term residential accommodation.

As always, there’s a tax consequence to that and for GST purposes it means that if the GST activity is stopped, then the person is required to de-register for GST. Part of the de-registration process will mean a deemed supply of the goods that were brought into the business. You’re deemed to have sold them and pay GST output tax on the way out. And if you’ve claimed a big input tax credit for, say, a whole property, moving it over to Airbnb, that means that you could have a substantial output tax payable on de-registration, as it’s done at a market value.

Now, under the GST Act, there is a provision that where someone is no longer carrying on a taxable activity they are obliged to let the Commissioner of Inland Revenue know within 21 days of their taxable activity ceasing, and then that registration must be cancelled unless there are reasonable grounds to think the taxable activity will be carried on within 12 months. So, this could apply if you think that within 12 months-time, we could be back up and running again.

What Inland Revenue has done is extended this twelve-month period to 18 months through a special COVID-19 determination which has just been issued and this will apply until 30th September 2021. So you now have 18 months, a lot more flexibility about whether you’re going to resume your Airbnb activities or drop out of the picture completely.

Just a caveat though – if you are currently using a property for residential accommodation, but you anticipate going back to making taxable supplies in Airbnb, you have to do what’s called a change in use calculation. This is basically an apportionment of the value of the property brought into the GST net over the expected time it’s being used for taxable activities. A little bit complicated, but you produce one of those calculations as part of your GST returns.

Political tax policy

Yesterday National released its small business tax policy. In terms of tax rates it has come straight out and said it does not plan on increasing taxes or introducing any new taxes.

Other than tax rates, National’s tax policy has a number of other measures. Firstly, they’re going to lift the threshold for the purchase of new capital investment from $5,000 to $150,000 per asset. That is you can take a complete deduction for an asset costing up to $150,000. Now apparently this only applies to “productive assets” so there’s a question as to what that might mean. It’s a temporary two-year change. Something similar has been done overseas.

And it’s a good idea although it is a question, of course, of what will and won’t meet the definition of ‘productive’. But you could see some fairly substantial plant and machinery being purchased and as a means of getting investment into productivity in the economy it’s a measure to be to be welcomed.

National proposes increasing the Provisional Tax threshold from its current $5,000 to $25,000. I’m not so sure about this one, because one of the reasons the threshold stayed at $2,500 for a long time was concern that if it was increased substantially taxpayers might forget they’ve got terminal tax to pay and find themselves short of funds. And obviously that risk increases the greater the threshold, so $25,000 is extremely generous.

It would also have an impact on the Government’s cash flow, by the way, because it would drop quite a lot of people out of the provisional tax requirements. So the Government’s income, so to speak, was will be reduced temporarily before these payments will then come in at terminal tax time. I think $25,000 is too generous, $10,000 is probably manageable. Still it’s a measure in the right direction.

Next, they want to raise the GST threshold from $60,000 to $75,000. Big tick for that, the GST threshold hasn’t been increased since 1 April 2009. So it’s well overdue and on an inflation basis $75,000 is about right.

Businesses will be allowed to write off an asset once its depreciated value falls below $3,000 as opposed to continuing to depreciate it until its tax value reaches zero. Really good measure here. Should be done straightaway regardless of who’s in power. Keeping a track of all these assets when they’ve fallen below that threshold is hard and causes needless complexity. So I like that a lot.

I also like this next one – change the timing of the second Provisional Tax payment for those with a 31 March balance date from 15th January to 28th February. That’s really quite sensible. It’s bizarre it’s in the middle of January when we’re all supposedly on holiday and it’s not a great time for cash flow. February makes a bit more sense.

Ensure the use of money interest rates charged by Inland Revenue more properly reflect appropriate credit rates. So right now, if you overpay your tax Inland Revenue will pay nothing. National are saying, well, we want something that’s a little bit more realistic than that. It’s not a bad move and it certainly would be popular with small businesses, but it’s rather based on an assumption that taxpayers would be using Inland Revenue as a bit of a bank. They won’t. A better option in this case would be tax pooling which takes care of a lot of those issues.

Increase the threshold to obtain a GST tax invoice from $50 to $500. A very generous upper limit there. I’m not sure I’d go as high as that, but that $50 threshold below which you don’t need to have a full GST invoice with all the required details on it has not been changed since 28th September 1993. So an increase in the threshold is welcome. I’d say $150 might be a better option.

Implement a business continuity test rather than an ownership test for carry-forward of tax losses. Moves in this space are already happening but the measure is to be welcomed.

Next and also welcome, review depreciation rates for investments in energy efficiency and safety equipment. That’s not a bad idea. And then consolidate the number of depreciation rates to reduce administration costs. That’s another big tick from me on that, because there are so many different rates and there’s options to probably get it wrong more often than right. And the level of micro detail required probably isn’t really appropriate for small businesses.

So those measures I think are mostly all welcome. And frankly, they’re sort of pretty much apolitical. Whoever is in power should be adopting almost all of those proposals.

Just a matter of time?

And finally, talking of parties’ tax policies, the Greens released as part of their tax policy, a proposal for a wealth tax to apply on net wealth over $1 million. Earlier this week, former legal practitioner, Human Rights Commissioner and retired Family Court Judge Graeme MacCormick picked up on the Green Party’s proposal when he wrote about the question of a wealth tax. He suggested a one percent levy on net assets of more than $10 million per person.

He also argued that it was time for the wealthy to step up and help out in this the crisis. He was sceptical of the idea of the trickle-down effect, that wealth trickles down and dissipates out through the country. He was of the view that basically we’ve got 30 years to show that hasn’t happened.

One of the interesting points he raised was that New Zealand not only doesn’t have a comprehensive capital gains tax, it also doesn’t have an estate tax or a gift tax nor a wealth tax. It’s highly unusual in the OECD for one jurisdiction to be not have at least one of those taxes applying on a comprehensive level. Some have capital gains tax and no wealth tax or estate tax. Others have a wealth tax, but no capital gains tax and some like the UK and the US, have capital gains taxes and estate and gift taxes.

The position varies across the OECD, but New Zealand is pretty unique in not having either a comprehensive capital gains tax, estate tax, gift duty or wealth tax.

Wealth taxes have fallen out of favour in the past few years, but they’re back on the agenda because, as I discussed with Radio New Zealand panel and Patrick Smellie of Business Desk, the pandemic and Thomas Piketty has opened the door on that.

And I was very interested to see this week that former Reserve Bank governor Dr Alan Bollard said in his presentation to the New Zealand CFO summit that, like it or not, given the scale of the borrowing the Government has had to engage in, capital gains tax may be an unpalatable option for governments to consider as they want to pay down the debt.

So this matter of capital taxation hasn’t gone away. We’ll hear more from other politicians no doubt, Labour and New Zealand First have still to release their tax policies. But we’ve still got another seven weeks to go to the election so there’s plenty of time for discussion on that.

Well, that’s it for this week. Thank you for listening. I’m Terry Baucher and this has been The Week in Tax. Please send me your feedback and tell your friends and clients until next week. Ka kite āno.