Last week, as part of its continuing drive to increase compliance, Inland Revenue released an updated property tax decision tool.

What this does is help people work out when a property might be taxable under any of the land taxing rules, including the bright-line test. It’s been updated to take account of the bright-line test changes which took effect on 1st July this year.

The growing issue of helping families into housing – what are the tax implications?

Generally speaking, since 1st July, the bright-line test only applies where the end date for sale as determined under the rules is within two years of when the property was deemed to have been acquired. The aim of the tool is to work through all the various scenarios that might apply. So that’s something worthwhile, and I think we’re going to see more of people wanting to make more use of this because of a developing trend around shared home ownership where people who are not necessarily couples are coming together to purchase properties. There are also families wanting to help elderly parents.

We’re seeing some very interesting scenarios develop as a result. One of those scenarios was the subject of last week’s Mary Holm’s column for the New Zealand Herald.

“We’ve bought my wife’s parents’ house. They had a small mortgage on it, with no income, just super, coming in. They didn’t have enough money to keep paying the mortgage, hence they were going to start a reverse mortgage to keep things afloat.

If they sold the house they would’ve struggled to get into a retirement village and stay near family etc. So we bought the house so they don’t ever have to leave – so let’s say they will be there for at least another 10 years.

They pay us $750 rent per week. We took out a 30-year $800,000 mortgage, with just the interest on it at $1977 a fortnight, so we are topping up mortgage payments as the rent does not cover it. We also pay the rates, insurance and any maintenance costs.

How do we treat this in terms of any possible tax or claims as such?”

Mary asked Inland Revenue and me for comment. Notwithstanding that a net loss was foreseeable, my advice was you never always know what the full story is as there may be a detail which for whatever reason, the correspondent has overlooked. The basic approach I took was you should report it. Inland Revenue were much of the same view but noted that any excess deductions would be ring fenced.

As I mentioned to Mary, I think we’re going to see a lot more of this. Because they’re coming from both ends of the generational spectrum. In this case we’ve got the elderly parents wanting to stay near family and then at the other end, young people trying to get on the housing ladder.

Is shared home ownership an answer to housing affordability?

Over the last 20 years or so I’ve seen the practice develop quite rapidly of parents, grandparents and other relatives helping their children or grandchildren get their foot on the property ladder. This was the subject of an interesting report on shared home ownership released by Westpac called Next Step Forward. The report notes that the housing market is increasingly difficult, and “the home ownership dream is increasingly out of reach for some New Zealanders”. The report’s analysis is that shared home ownership will become increasingly common and how might that develop.

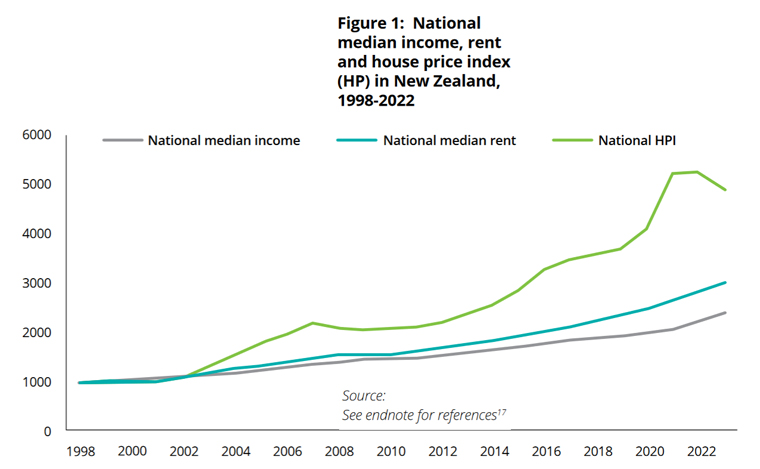

The report describes the housing market as “distorted”. To give you some idea of the scale of the problem, the report notes “As of February 2024, the median house price was 6.8 times the median income compared to 5.4 times in 2004 and roughly 2.3 times in 1984.” So over 40 years, the median house price relative to median income has practically trebled.

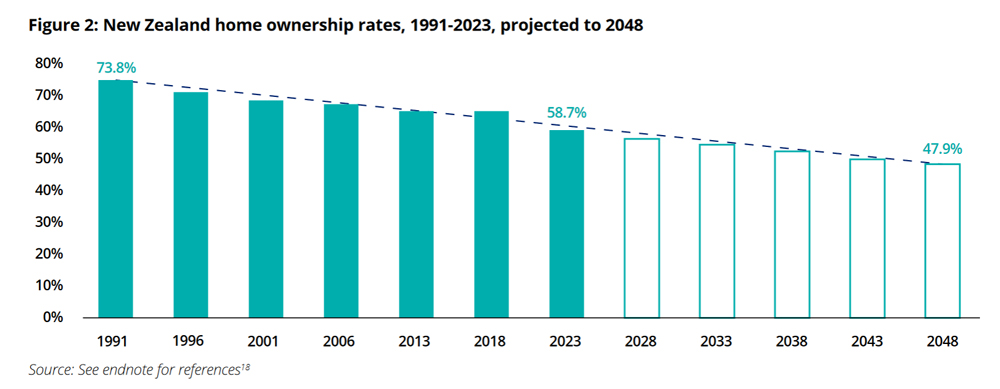

The report also notes that home ownership rates in New Zealand have been declining steadily since peaking in 1991 at 73.8%. They’re down to 58.7%, so a 15 percentage point drop over 30 years is pretty substantial. But the report projects that within 25 years, the proportion of homeowners will have dropped to 47.9%. (The report notes the outlook is even worse for Māori and Pacific peoples, where the home ownership rate is lower, at 47% and 35%, respectively, as of 2023).

What are we going to do about this? Well, as the report suggests shared home ownership is going to become more common. This in turn is going to trigger all sorts of tax issues. Which is why something like Inland Revenue’s property tax tool is handy. The report, incidentally, doesn’t really discuss tax other than mentioning tax free capital gains do play a part in people’s investment decisions and may have an impact on the housing market

There’s no real short answer to this issue. Raising incomes would be one thing, freezing or slowing the rate of house prices would be another, and building more homes would be a vital third factor. Pulling all this together is a huge problem and each solution comes with secondary effects.

International tax deal in trouble?

Moving on, an equally complicated scenario and one we’ve been covering for several years, is the question of the taxation of multinationals. Back in 2021, the OCED/G20 declared a breakthrough international tax deal over the taxation of the largest multinationals in the world. The deal proposed a Two-Pillar solution over the question of taxing rights. Ultimately this is where the idea of a minimum corporate tax rate of 15% emerged.

Agreeing in principle was one thing, but the negotiations have been going on since then and increasingly it seems to be that they’re running into difficulty. A key 30th June deadline has now passed, and it appears that some governments are starting to lose patience with the whole process.

One of the ideas behind the agreement was to head off the implementation of digital services taxes (DSTs). As part of the process these DSTs were put on hold by several jurisdictions, including the UK, Austria, India and others. In the meantime, as negotiations have dragged on, other countries such as Canada have said “Well, we’ve had enough of this, we’re going to go ahead and impose a digital services tax.”

Meantime, the United States whose companies such as Alphabet and Meta are at the heart of the issue have threatened retaliatory tariffs on countries imposing DSTs. Nobody wants a trade war, but someone has to blink in terms of getting a deal past this impasse. So, they’re continuing to negotiate, even though the deadline theoretically has expired.

Time to go back to first principles?

On the other hand, as Will Morris, PWC’s Global Tax Leader points out in this short video. Maybe we should just go back to first principles instead of trying to hammer out a deal through the existing Pillar 1 process which some consider is not really fit for purpose.

It’s not a bad idea but it would delay further progress in the matter, and I think that’s where governments who’ve got elections to win may not be prepared to wait much longer. I think generally the public is a bit antsy about the question of corporate taxation. As I noted last week, when we looked at the OECD’s latest corporate tax statistics, statutory corporation tax rates have pretty much stabilised after 20 years of falling.

However, there are still substantial gaps in public finances as a result of first the Global Financial Crisis, then the pandemic and increasingly we’re having to deal with the impact of climate change as well. When the insurers are leaving the market, who picks up the tab? In my view, that’s going to be we the taxpayers.

There will be pressure to get some sort of deal across the line, but I also think although we may see corporate tax rates elsewhere in the world rise, I think with our 28% rate, we haven’t really got much room for manoeuvre for an increase at this point.

A place where talent does not want to live?

Finally, the New Zealand Institute of Economic Research released a fascinating report on Thursday. Provocatively titled The place where talent does not want to live, it looks at the question of New Zealand’s immigration policy and how that sits alongside our international tax regime.

The report was prepared for the American Chamber of Commerce in New Zealand, the Auckland Business Chamber, the Edmund Hillary Fellowship and the NZUS Council. It’s a fascinating document because it pulls together points, we don’t always hear discussed when we’re looking at immigration policy, how does our tax system interact with that policy?

The report notes that conceptually, we have developed tax rules which make sense in a tax context. However, they lead to wider issues once they start operating in a broader context. In particular the report really focuses on the Foreign Investment Fund (FIF) regime which it considers disadvantages many investors who come here hoping to use their skills and their capital to help build the economy and the tech sector in particular.

I’ve seen comments on this topic previously from entrepreneurs, and it’s easy perhaps to be cynical and say, “Well, they’re speaking out of self-interest” but 40 years of tax experience also tells me that behavioural responses to tax are very observable and policymakers should pay attention to such responses.

An in-depth examination of the Foreign Investment Fund regime

What makes this report particularly interesting are the authors, Julie Fry and Peter Wilson. Julie is a dual New Zealand and U.S. citizen who in her bio notes that “her location and financial decisions have been impacted by the tax rules covered in the report.” Peter was Manager of International Tax at the New Zealand Treasury from 1990 to 1997 and then Director of Tax Policy from 1998 to 2002. As such “He was responsible for advising the government on many of the tax issues contained in this report.” Consequently, outside of anything prepared for a tax working group, this report is one of the most in-depth examinations we’ve seen of our international tax regime and FIF regime.

The report notes that although we have a fairly open flow of migrants, “New Zealand has never been a particularly popular destination for talented people”. (Interestingly, we have no data on how long people on the various investor and entrepreneur visas stay).

As the report notes there’s a competition for global talent and New Zealand is not attracting as many as we would like. We should therefore be thinking hard about the implications of this.

The report hones in on the FIF regime as being a particular problem for many investors because of the way that it taxes unrealised gains. This creates a problem of a funding gap where an investor is expected to pay tax on an investment which very often isn’t producing cash because as a growth company cash is being reinvested. (By the way, this is often a common argument against wealth taxes).

As the report notes, “New Zealand’s tax rules were not designed with the idea of welcoming globally mobile talent in mind.” For example, as Inland Revenue’s interpretation statement on residency makes clear it’s deliberate policy to make it’s easy to be deemed tax residency in New Zealand, and hard to lose. This has long term flow implications because as the report points out, people who would perhaps want to commit to New Zealand are reluctant to do so because of the tax consequences of doing so.

Chapter Three is the very, very interesting section of the report as it explains the development of our current international tax regime and the rationale for the various FIF regimes and their design. The overall objective was to protect the tax base, but they didn’t really think about what was happening with migrants. As Ruth Richardson and Wyatt Creech then the respective Minister of Finance and Minister of Revenue explained in 1991:

“The objective of the FIF regime, where it applies, is to levy the same tax on the income earned by the FIF on behalf of the resident as would be levied if the fund were a New Zealand company. Because the FIF is resident offshore with no effective connection with New Zealand, the only way of levying the tax is on the New Zealand holder.”

This is conceptually correct from a tax perspective but as the report keeps pointing out, it doesn’t really take into account what happens with migrants who made investment decisions long before they arrived in New Zealand only to find their accumulated savings are being taxed here under the FIF regime. I have a similar problem with the taxation of foreign superannuation schemes. Although the tax treatment conceptually ties in with our system, it seems to me we are effectively taxing the importation of capital and this paper is basically saying the same thing in relation to FIF.

How much tax does the FIF regime raise?

Section 3.5.1 on page 26 of the report has an interesting analysis of how much revenue the FIF regime raises. Because our tax reporting statistics aren’t very detailed, the answer is we don’t really know. The report concludes

“The high-level finding is that the level of overseas investment is small compared to total financial assets at the national level. Portfolio foreign investment is, in some years, one-thousandth of domestic investments. This suggests that the current FIF tax base is likely only to make a minor contribution to direct revenue.”

A suggested reform

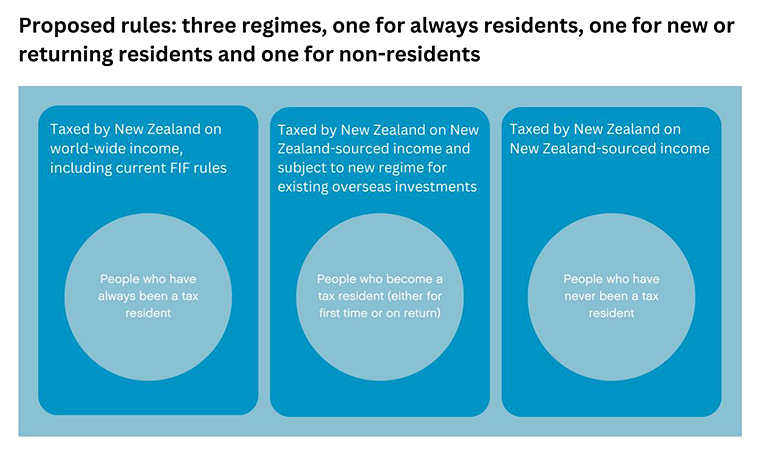

The report concludes that in an international context where we were trying to attract the right talent, maybe we should be looking at the FIF regime. What it suggests is to separate the tax treatment of people who have always been tax resident from those of new and returning tax residents. The existing FIF rules would continue to be applied to those have always been New Zealand tax resident. Meantime a new regime should be designed for new and returning tax residents.

The report does touch on the question of a general capital gains tax regime (which could be an answer) but considers the development of a comprehensive CGT is a long term political consensus building project.

In discussions I’ve had with other colleagues on this matter we’ve noted how our American clients in particular are very affected by the current FIF regime. As American citizens they are required to continue to file American tax returns and are therefore subject to capital gains tax. This creates a mismatch between when they pay New Zealand income tax and the final US tax liability on realisation. Although the FIF regime creates foreign tax credits for US tax purposes, clients are frequently not able to utilise the foreign tax credits.

As people told the report authors this is extremely frustrating and there is no doubt that people are upping sticks and moving because of it. (I’ve also seen other clients switch into property investment instead).

Overall, this is a very interesting and highly recommended report considering the intersection of tax driven behaviour with wider economic issues.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

About 10 years ago, myself and a group of other tax agents were on our way to a meeting with the then Minister of Revenue Peter Dunne. On the way someone mentioned whether we ought to raise the question of the law of unintended consequences in relation to a tax issue. Another replied that he’d never heard of such a thing law. So, we decided we shouldn’t say anything about that particular point.

We get into the meeting with Minister Dunne. And lo and behold in the course of our discussion, he brings up the law of unintended consequences, at which point we had to pause the meeting and explain to the Minister why we’d all cracked up.

(Incidentally, during that meeting, we raised a matter I discussed last week, the inequitable taxation of ACC lump sums. That was an issue which was supposed to be looked at by officials, and 10 years on, I guess they’re still looking).

The international impacts

I recalled this because last week I also talked about the Greensill decision in Australia, and the implications for trustees of New Zealand trusts. And on Monday, I got a new enquiry from a client where the impact of Greensill could come into play and it’s a classic example of the law of unintended consequences.

A mother had decided that she wanted all three of her children to be trustees of the family trust, and this change was made for good reasons in managing a family dynamic. Problem is, one of those children lives in Australia. As I mentioned last week under Australian tax law, if any trustee of a trust is tax resident in Australia, the trust is deemed resident in Australia. That means the Greensill decision may apply, which basically says capital gains even if realised offshore and even if distributed to a non-resident, are subject to Australian tax at the top rate of 47%.

The implications are therefore potentially quite serious for this trust. Looking into it in more detail, the trust is deemed resident from the first day a trustee is a tax resident of Australia. The trustees will have to prepare and file Australian tax returns reporting the trust’s income as calculated for Australian tax purposes.

Now, in many cases, the trusts will distribute income to beneficiaries and from an Australian perspective, if non-Australian sourced income is distributed to a non-resident, it’s not an issue. It’s just that in the law there is a technical inconsistency, which means that the Australian resident trustees are liable for Australian tax on non-Australian sourced capital gains distributed to non-residents.

This is the impact of the Greensill decision which to recap involved a capital gain of A$58 million and was held to be taxable at 47%. What’s more, with Australian trusts, the rate for retained income is 47%, and this is further complicated by rules about which beneficiaries have what is termed “present entitlement” as at the date of balance date. So overall, this is potentially quite a serious issue if substantial capital gains been raised.

Now the logical response, you’d think is, “Aha, let’s get the trustee to resign” and once the trustee resigns, that ends the connection with Australia. A logical move, except the Australian tax legislation has thought of that point. And what happens then is there’s a deemed disposal of the trust’s assets on the date of the resignation of the trustee (This is a feature of some jurisdictions with a capital gains tax). In other words the Australian Tax Office, believes in Blondie’s maxim, “One way or another we’re going to get you”.

We are currently working through all these issues. This is a textbook case of whenever there’s a family trust and there is family overseas if you want one of the family to become a trustee, you have to put a big pause on that and get tax advice, particularly in relation to Australian residents.

I’ve seen some trustees who are living in the UK pop up on trusts. This is not quite as potentially catastrophic but it’s still problematic. There’s this dichotomy between New Zealand’s tax treatment, which based around the settlor and many other jurisdictions, which is based around the residence of the trustee. So, to repeat the key point, if you have any trustees that are tax resident overseas, you need to get tax advice.

Helping your children

Moving on, the second instance of unintended consequences this week involves family members such as parents, grandparents or trusts trying to help children or beneficiaries purchase property, the bank of Mum and Dad as it’s sometimes called. This has become incredibly more relevant as a by-product of the horrendous escalation in housing prices.

The issue that has to be watched out for is when the parents or whichever other entity is involved, a trust, for example, actually takes a direct ownership interest in the property to be acquired. At that point, whoever it is, is probably setting themselves up for some issues further down the track in relation to the bright-line test.

And these of course have been magnified by the fact that the bright-line test as of 27th March this year now runs for 10 years. These issues were probably manageable when the two-year bright-line test was initially introduced back in October 2015 but have now been considerably magnified with the extension of the bright-line test period to 10 years.

What is emerging in some cases is that families might say, right, well, “We’ll take a 25% interest in the property. And then as the equity and your income rises you can pay us back and gradually take over our interest”. So ultimately, the children or beneficiaries will own 100% of the property. The problem is the reduction in those minority interests in the property represent a disposal for income tax purposes and for the purposes of the bright-line test.

For example, let’s say parents co-owned a house with a child and the ownership structure was initially 50:50 between them, but change it to 75:25. In that case, there’s been change in the title in the ownership interest, and therefore there’s been a disposal by the parents of a 25% interest to their child. Therefore, this disposal would be subject to bright-line test. There would be no exemptions here because they’re not living in it and it’s not their main residence. Just bear in mind that even if that property was the main residence of the child, the parents having the interest would still have made a disposal for bright-line purposes.

There’s also a potential kicker for such a transaction if the property is sold or gifted below its market value within the bright-line period, the transaction is treated as having happened at market value. So, for example, if the market value of the property had increased from $500,000 to $1 million, then the parents reducing their interest would be taxed on whatever their share of that $1 million was, rather than what actual cash they might have received. So potentially there could be some very sticky tax bills arising.

Arguably, one potential way round this might be that the parents lend the money to the child and not take a direct ownership interest, but you know, horses for courses, individual circumstances will come into play.

So, you just have to be very careful and proceed with great care if you are taking a financial interest in your child’s property to help them on the ladder. Otherwise, it could be another example of unintended tax consequences.

Lessening inequality

And the third unintended consequences that we might see in tax relates to the recent announcements from the government about changes to working for families.

What the Government has done has announced increases to the amount payable. The family tax credit is going to be increased by $5 per child. And on average, families will be $20 a week better off. But, and there’s always a ‘but’ in this, what the Government has given with one hand it has quietly decided to take on the other by raising the abatement rate to 27%.

Now abatement is what happens when a family’s annual income exceeds $42,700 then working for families credits start to be abated. And what this means is that people on average incomes actually have the highest effective marginal tax rates in the country.

For example, a family earning $48,000, the point at which the tax rate moves from 17.5% to 30%, their effective marginal tax rate, once you add in the impact of abatement is 57%. In other words, for every dollar of extra income they earn, they will lose 30% in tax and 27% of their working for families tax credits

For family’s with income just over $70,000, the marginal tax rate rise to 60%. And if you’ve got a student loan, that’s another 12% on top of that. A person earning just above $48,000 with a student loan could be facing an effective marginal tax rate of 69%. This is the unintended consequences of the abatement rates. The theory is conceptually sound, but the problem is it traps people on low income and makes it very hard for them to break out of the need to receive social assistance.

This is one of these things that is consistently glossed over by politicians and has been one of those sneaky little tax increases that that previous finance minister Bill English did. Grant Robertson is just the latest to increase the abatement rate and so quietly claw back some of the assistance. The unintended consequence is that the step up makes it harder to get out of poverty.

There is meant to be a review of working for families going on at the moment, but that’s been paused. As we know, the Welfare Expert Advisory Group recommended significant increases in benefits and that report is now nearly over two years old.

To summarise this week’s lesson, tax is full of unintended consequences. Therefore, always proceed with caution if you’re making significant changes, such as appointing a trustee or wanting to co-invest with your children on a property purchase.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website, www.baucher.tax or wherever you get your podcasts. Thank you for listening, and please send me your feedback and tell your friends and clients. Until next week, party week, have a great week and go the Black Caps.

One of the positive matters coming out of the interest limitation rule changes is an extension of the rollover relief for bright-line test purposes. As is known, a change of ownership will often reset the timetable for the bright-line test purposes.

When the bright-line test was introduced in October 2015, the initial period was two years and so the resetting of the timetable wasn’t considered to be a great deal. But as of 27th of March this year, the bright-line period is 10 years, so it is now a very significant issue.

Accordingly, there has been pressure on Inland Revenue and the Government to include some rollover relief provisions, and the supplementary paper does include these. Now the proposals won’t go as far as people would like, but they’re a start. The key features are that certain transactions will now be eligible for rollover relief and that is mainly some transfers to family trusts and to/from look through companies and partnerships. There’s also going to be specific relief proposed for transfers to trusts constituted under Te Ture Whenua Māori Act 1993 and also transfers to land trusts as part of settling claims under Te Tiriti.

The key one for the family trusts is that rollover relief will apply. That is, the period of ownership will be combined, and not deemed to be a break for transfers of residential land to a family trust, provided that each transferor of the land is also a beneficiary of the trust. At least one of the transferors of the land must also be a “principal settlor” of the trust. That’s a loaded phrase in itself. And each beneficiary, except for those beneficiaries who are also principal settlors, has a family connection with a principal settlor, or is a company controlled by a family member beneficiary, or is a charity.

In relation to transfers to/from look through companies and partnerships, the rollover relief will also apply. The provisions are complicated but will apply where the persons transferring the residential land to or from a look through company or partnership, have ownership interests in the look through company or partnership in proportion to their individual interests in the land and their cost base relative to the total cost base of the land.

In addition to the above criteria, rollover relief is only going to be available if the transfer is made for an amount or consideration that is less than or equal to the total cost of the residential land to the transferor at the date of transfer.

All this is good, if complicated, but with care can be managed. But one issue that does stand out straight away is that the rollover relief does not cover transfers from trustees to beneficiaries. Therefore, the bright-line timetable will reset on such a transfer unless it is possible that another exemption relating to matrimonial relationship property agreements can be used. That also requires a great deal of care.

This is a little disappointing, and I would recommend people making submissions requesting that distributions or transfers of land to beneficiaries can also be included for bright-line test purposes. Or at least flush out from Inland Revenue the reason why it thinks this shouldn’t be the case.

If conditions are met for rollover relief, then under the new provisions, the trustees or the look through the companies would be deemed to have the acquisition cost and date mirrors the total cost of the land to the transferor and obviously at the same acquisition date as for the transferor. And similarly for transfers involving partnerships and look through companies.

Now this provision will come into force when the bill is passed, so that means the likely commencement date is going to be late March 2022. As I said, encouraging. But it would be useful at least, if the transfers from trusts could be covered by rollover relief as well.

A tax focus on HNW individuals

Moving on, Inland Revenue is in the early stages of starting a research project for high wealth individuals relating to their effective tax rates. And what they plan to do is to collect information to help Inland Revenue assess the fairness of the tax system.

This is something that the Government specifically allowed for in this year’s budget. Inland Revenue got five million this year to June 2022 as part of this project. Inland Revenue apparently selected some 400 individuals who are regarded as high wealth, and households in this particular group are expected to have or thought to have a net worth exceeding $20 million.

The project is based on household income, so the first stage is to confirm with the individuals selected who’s in the household. Then in stage two, which will be early next year, individuals will be sent a list of entities and business undertakings, such as trust in companies, Inland Revenue believes they have an interest in. They’ll be asked to confirm that interest and provide further details of any other entities Inland Revenue may not have identified That will similarly apply to partners and dependent children. And then finally, financial information relating to these entities must be provided.

The plan is to analyse this information and then provide a report in June 2023. And it’s all part of gathering data for better public policy in this area. The information provided will cover the 2016-2021 income tax years, and there will be an estimate of the effective tax rate based to relative economic gain over that period.

This is quite a big project for Inland Revenue, as I told others earlier. One of the unintended consequences of having abolished estate duty in 1992, is that we don’t actually have a lot of good data around wealth because grants of probate and wills are no longer made public.

But generally, around the world there’s growing concern around inequality, but also to the question around the brutal fact that most governments have been hit very, very hard by COVID-19 and are looking in the long term at the question of raising revenue. But that’s a long way off. In this particular case it’s more about “let’s find out what what’s out there.”

The revenue is using a specific provision, section 17 GB of the Tax Administration Act. And all this information is not to be shared with any operational part of Inland Revenue. According to an information sheet published, it will be held in a database separate from Inland Revenue’s main START system and will not form part of any of the individual’s tax records.

Inland Revenue must be absolutely secure in doing this. Otherwise, it will be buried in lawsuits over a breach of privacy. The Privacy Commissioner no doubt will be watching this one very carefully. Inland Revenue have had to get some sign off from the Privacy Commissioner on this so far.

It’ll be interesting to see what comes out of this. It is early stages, but I think you can expect to see and hear about some pushback. But for the moment, Inland Revenue believes it has the statutory tools to do this. So, it will be interesting to see how this exercise plays out.

Last week, Professor Lisa Marriott and I talked about Inland Revenue’s debt management, and in our discussions Lisa raised the question of maybe a tool to be considered would be publicising the names of debtors.

And one of our listeners, James (thank you, James) followed up with an email pointing out that in fact, Inland Revenue does already have some powers to communicate information to an approved credit reporting agency regarding a taxpayer’s reportable unpaid tax. This is under section 18H and Clause 33 of Schedule Seven of the Tax Administration Act.

Under this clause, if the reportable unpaid tax is in excess of $150,000 and the Commissioner of Inland Revenue has notified the taxpayer of this amount, then the Commissioner may give an approved credit reporting agency information in relation to the taxpayer and any amount of reportable unpaid tax. But they must have made reasonable attempts to recover this unpaid tax from the taxpayer before formally notifying the taxpayer that this is going to happen.

So, this is a first step, and the threshold is reasonably high, which gives me some comfort. It’s actually quite interesting to look back on this clause and see not much was said about it at the time. And certainly, the commentary issued in the bill doesn’t really refer to this in great detail. So this clause went through without too much comment. I’m not aware of it having been used, but we’ll put in an Official Information Act request and find out more on that and update you at a later time. So, thank you James, for letting us know on that. As always, we welcome feedback, good and bad from listeners and readers.

Well, that’s it for today. Next week, I’ll be reviewing Inland Revenue’s just published 2021 annual report together with the latest developments, as always.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax cor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week kia pai te wiki, have a great week!

It has been a massive week in tax beginning with the G7’s announcement that it had agreed a minimum corporate tax rate of 15% (more here), we had the Climate Change Commission’s release of its final advice to the Government, Propublica releasing Internal Revenue Service data about the tax affairs of the 25 richest Americans, the same day as Revenue Minister David Parker raised the same topic in his appearance before Parliament’s Finance and Expenditure Committee.

But the biggest news, and our topic today, is the release of the Government’s long-awaited discussion document on the design of the interest limitation rule and additional bright-line rules.

You will recall that on March 23rd the Government dropped a huge bombshell by announcing that it was proposing to limit interest deductions for residential rental investment properties starting October 1st.

Now, there’s been a flurry of activity since then with Inland Revenue consulting with an External Reference Group discussing the issues that came out of the Government’s announcements as part of preparing the discussion document which was released yesterday.

At 143 pages it’s a big document and it’s one of the largest such discussion documents issued in recent years. Just for comparison, the issues paper on loss ring-fencing released in 2018 was a mere 20 pages, and that for the introduction of the bright-line test back in 2015 just 36.

I was part of the External Reference Group, and it became very apparent very quickly that we were dealing with considerably complex issues, and we would be looking at quite a lot of very detailed legislation. So, there’s a massive amount of detail to consider here.

I don’t propose to go through everything in detail today because we’re still working our way through the document and considering the implications. Instead, what I’m going to do today is give an overview of the key points in the discussion document points, and then in the coming weeks, focus on specific issues of interest.

Now, the discussion document starts with an overview of the proposals and then works its way through another 13 chapters so there are 14 chapters, including the introductory chapter, in all. And one of the things that I think we might well appreciate is the document has been drafted so that it is not necessary for everyone to read the entire document unless you’re a tax adviser like me. But if you have a particular interest, you can go to the chapter that is relevant to you. And each chapter also contains specific questions that Inland Revenue and the Government are looking for responses about.

To summarise, the restriction will happen from 1st October 2021. The amount of the restriction will depend on whether the interest is “grandparented”, and that’s going to be one of the first points of interest. This is interest on debt drawn down before 27th March 2021 relating to residential investment property acquired before that. The deductions will be gradually phased ou between 1st of October 2021 and 31 March 2025. For grandparented interest, deductions will be gradually phased out between 1 October 2021 and 31 March 2025 as follows:

Date interest incurred

Percent of interest you can claim

1 April 2020–31 March 2021

100%

1 April 2021–31 March 2022

(transitional year)

1 April 2021 to 30 September 2021 – 100%

1 October 2021 to 31 March 2022 – 75%

1 April 2022–31 March 2023

75%

1 April 2023–31 March 2024

50%

1 April 2024–31 March 2025

25%

From 1 April 2025 onwards

0%

Chapter 2 looks at what residential property is subject to the interest limitation. Now, there’s a good part here is that there are some exclusions.

Land outside New Zealand

Employee accommodation

Farmland

Care facilities such as hospitals, convalescent homes, nursing homes, and hospices

Commercial accommodation such as hotels, motels, and boarding houses

Retirement villages and rest homes; and

Main home – the interest limitation proposal would not apply to interest related to any income-earning use of an owner-occupier’s main home such as a flatting situation.

Chapter 3 then looks at the entities affected by interest limitation, such as companies, Kāinga Ora and other organisations,

What interest expense is going to be non-deductible?

Then Chapter 4 – one of the ones going to get into quite a bit of detail – involved interest in allocation, which is how do you identify which interest expenses are going to be subject to the limitation?

And the proposal here is to follow the long-established practice that where a loan has been used for a mixture of taxable and non-taxable purposes, we trace the funding through to each purpose to determine the deductibility. The Government’s proposal is to use this existing approach for loans used to fund residential investment property. Now, the discussion document also covers refinancing, existing loans and some transitional issues around debt which existed prior to 27th March.

One of the issues considered in the paper is the question of what to do about loans that can’t actually be traced. In other words, because previously this wasn’t a requirement for many investors, and they don’t have the records to be able to trace. What do you do where you want to show that a loan that was taken out prior to 27th March was applied to, say, business use rather than residential property investment? A mixed-use loan, if you like.

There are two proposals to deal with this issue. One is to take an apportionment based on the value of the loans across the assets, based on the original acquisition costs and the cost of any improvements. The other option is what they call ‘debt stacking’, which is where taxpayers would allocate their pre-27th March loans firstly to assets that are not residential investment properties but qualify for interest deductions.

This is actually quite generous, by the way. The rationale for this is that well advised taxpayers would be able to restructure to achieve the same tax outcome under the tracing approach anyway. This is actually an acknowledgement of the disparity of investors we’re dealing with here. Some are quite sophisticated and would be across all the detail. Others, less so, perhaps because they may not have many properties and have not really been as diligent as perhaps they should have been in keeping records. So that’s a little bit of a generous exemption there. But the point is you’re still dealing with a great deal of complexity in approaches and the Government is asking us to say, well, which one would you prefer to use?

A particular point here to note is that with pre-27th March loans, while interest on those loans will be deductible, subject to phasing out, and any borrowing subsequent to that date will be completely limited. What’s proposed to help calculate this proportion is determining a “high watermark”, which is the amount of funding allocated to residential rental property as of 26th March 2021. And then from that point, variations above that are the ones that are going to be most closely subject to interest limitation. As you can see, we’re already into quite a lot of detail and we are just getting started.

Non-deductible interest and bright-line test sales

Chapter 5 looks at the proposals for the disposal of property subject to the interest limitation rule. This was the subject of a lot of discussion during the External Reference Group consultation. Because the issue here is if interest has been limited, but the property has been sold and the gain on the disposal is treated as taxable, what are we going to do with the interest that was treated as non-deductible? Can this now be allowed as a deduction on sale? This is targeting people caught under the bright-line test, and remember we are also talking about an extended 10-year period for the bright-line test.

There are several options under consideration. One is that deductions are denied in full stop. Secondly, the deductions are allowed at the point of sale. Thirdly, deductions are allowed at the point of sale to the extent they do not create a loss. And finally, there’s an anti-arbitrage rule to counter attempts to arbitrage the interest deductions available because some people might know they’ve got a taxable transaction coming up.

The Government’s looking for feedback on people’s preferred approach. My impression is that they will be allowing a deferred deduction of previously denied interest at the point of sale. But exactly how those rules will operate is what the Government wants to hear more about.

Chapter 6 considers the treatment of property development and related activities. The Government has determined that property developers should be exempt from the proposed rules. So that chapter looks at what is the definition of development and how far should this development exemption go. It also looks at what do we do in applying that exemption to one-off developments as well as professional developers?

A particular point of interest, because we’ve got ongoing issues around leaky homes and earthquakes strengthening, is remediation work. Will that qualify for the development exemption? So there’s a lot to consider in this chapter.

What is a new build?

Chapter 7 is one which also generate a lot of discussion – what is the definition of a “new build”? Under the proposals, new build residential properties are exempted from the proposed interest limitation rules, and they’re subject to a five year bright-line test rather than the 10-year test.

The chapter suggests the following could be considered a new build:

a dwelling is added to vacant land,

an additional dwelling is added to a property, whether stand-alone or attached,

a dwelling (or multiple dwellings) replaces an existing dwelling,

renovating an existing dwelling to create two or more dwellings,

a dwelling converted from commercial premises such as an office block converted into apartments. This is one which I think is of particular interest. Following the announcement in March we heard one or two of these developments were put on hold so clarity around this is needed.

Chapter 8 then deals with the new build exemption from interest limitation and how long that exemption should apply to new owners? It’s also proposing that early owners, those who acquire a new build no later than 12 months after its Code Compliance Certificate is issued or add a new build to the land, would be eligible for the new build exemption. It then looks at what about subsequent purchases? Maybe the exemption is available for those who acquire a new build more than 12 months after the new build’s Code Compliance Certificate is issued and within a fixed period such as, say, 10 or 20 years. There’s a lot to consider in this issue.

Chapter 9 then discussed how the five-year bright-line test will apply for new builds.

A pleasant surprise

Chapter 10 is where we have a pleasant surprise. It deals with what we call rollover relief when the application of the bright-line test and interest limitation is “rolled over”. This is where the property is transferred between two parties and that transfer, which is a disposal for tax purposes, does not trigger an immediate tax charge under the bright-line test provisions.

The lack of a comprehensive rollover test was something that has been an issue before this interest and limitation issue arose. What’s proposed in here is some limited relief from the interest limitation and bright-line test in relation to transfers to trusts and transfers where there is, quote, “no significant change of ownership.”

What this means is in those circumstances, the taxing point will be deferred until there is a future disposal of the property that does not qualify for rollover relief. So, if the transfer qualifies for rollover relief, then the disposal of the residential land would be at cost to the transferral or original owner rather than market value, which is the current rules. The recipient would then be deemed to have the same acquisition date and cost base as the transferor.

Now, the critical thing is disposals where there is non-zero consideration, either at market value or not, will not be eligible for rollover relief. That means if you are transferring property into a trust you must gift it in. If there’s any consideration received for the transfer you won’t qualify for rollover relief. (That may also mean the bright-line test applies and a tax charge on transfer arises).

There’s also a clarification here that rollover relief will apply where property is transferred between company or partnership and its owners so long as the property continues to be owned in the same proportion.

Now, all this is, as I said, is actually a pleasant surprise. It may be limited, but it does deal with an issue that had been of some concern previously. So it’s welcome to see the matter being addressed.

Chapter 11 then looks at the question of what to do with interposed entities. This is a quite technical point as they’re proposing new rules to ensure that taxpayers can’t claim interest deductions for borrowings used to acquire residential property investment property indirectly through a company or other interposed entity.

As I said it’s quite technical and as part of it involves one of the new definitions we’re going to see appearing in the Income Tax Act, what’s called the “affected assets percentage” as part of defining the terminology of a residential interposed entity. Basically, the idea is to stop people claiming a deduction for borrowing to buy shares in a company which then buys residential investment property. This is unsurprising, but just adds more complexity to the matter.

How does this fit with loss ring-fencing rules?

Chapter 12 deals with a particularly interesting issue which has cropped up about the implications for the rental loss ring-fencing rules. The chapter looks at the overlap between the ring-fencing rules and the proposed interest limitation rules. What it’s saying is the interest limitation rules should apply first to determine whether interest is potentially deductible in income year and then the ring-fencing rules will apply on the balance.

Now, if you’ve been working in this space, you’ll be aware that the loss ring-fencing rules can be applied on either a portfolio basis, that is across the entire portfolio, or on a property-by-property basis. Now, that’s not such an easy fit when you consider that the rules about tracing the purpose of loans really work on a property-by-property basis. So that chapter confirms that is the intention, that the interest limitation rules must be applied on a property-by-property basis.

Chapter 13 looks at the question of property, subject to an existing set of interest and deduction restriction rules called the mixed asset rules. When we started talking about this in the External Reference Group, quite a few brains, including my own, went clunk because we really are into very great technical detail.

And then finally, Chapter 14 looks at compliance administration and how are we going to manage this? What information is going to be required by Inland Revenue in order to enforce these rules? Does Inland Revenue need more powers? The likelihood is that the amount of detail to be included in a tax return will increase. That seems inevitable.

So that’s a brief overview of a highly complex position. I’m particularly concerned about how this is going to impact small investors with one or two properties. Unless they happen to be debt free, they face significantly increased compliance costs relative to the size of their portfolio.

It’s not just taxpayers who face an increased risk. Tax agents and advisers face greater risks because there’s so much more detail to get across. If we get the deductibility issue wrong, we could be liable. So one of the things that the Government’s saying is we do want to try and minimise compliance as much as possible.

So, I would urge people to submit. In doing so I think you should focus on what making the proposals as workable as possible. So be constructive. I know a lot of people are very unhappy about these rules. The Government knows you’re unhappy, I’ve discussed it with the Parliamentary Under-Secretary to the Minister of Revenue, Deborah Russell. The Government knows that people are unhappy about it but telling them that and railing against the proposals is just not going to make any difference.

So be constructive in your approach. Submissions have now opened, and they close on 12th July, because the whole thing has to come into force by 1st October. Now, we’ll be tracking this and as I say, we’re going to come back and pick up particular points of interest. And I’m very, very interested in hearing your feedback on this.

Well that’s it for today. Next week, barring any more tax bombshells, we’ll take a closer look at the G7 tax announcements and what the Climate Change Commission had to say about tax.

I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients until next week, ka kite āno.

It would be fair to say that the shockwaves from Tuesday’s announcements are still reverberating around investors and analysts and tax professionals.

The increase in the bright-line test period to 10 years was widely anticipated. But the move to completely eliminate, over time, interest deductions for residential property investors was a complete shock and has caused quite a considerable amount of commentary.

I would say at this point, I think several people have been extremely ill guided in some of the comments they have made online. Inland Revenue monitors social media, and some of the comments I’ve seen by property investors, understandably, given the shock and the implications for them, upset about what has happened and probably reacting somewhat intemperately, may come back to haunt them.

For example, saying that rent doesn’t cover the cost of a mortgage and other costs, as one investor said in print, is an open invitation to Inland Revenue to raise questions as to why if that was the case, that person had purchased property. It opens the door for Inland Revenue to then go on and say, “Well, you must have acquired that with a purpose or intent of sale.” Which if that is argued bypasses the bright-line test. It doesn’t matter how long you’ve held it in those in those circumstances, any gain will be taxable.

Now, that’s an extreme response Inland Revenue could take. But as I said, I think some people might, to borrow a phrase, that my mother would use “Cool their heels a wee bit” and sit back and reflect on the implications of what’s going on, rather than rushing to social media and excitedly make a comment that they may regret at a later date.

But still, there are good reasons for people to respond passionately given its surprise. Under the Generic Tax Policy Process, changes like this are usually signaled in advance. The Government issues consultation papers, and there’s a back and forth between industry specialists and Inland Revenue and Treasury on the implications of these proposals. That isn’t going to happen here.

In the course of the group call made to tax agents and tax advisors before the announcement, Inland Revenue made it clear that there would be no consultation about the bright-line test period and on restricting interest deduction issue. Inland Revenue would, however, consult around a key point that is emerging. What is the definition of “new builds”?

So these proposals are all outside the normal process and have understandably drawn criticism along the lines of “Can the Government do that?” They can. And in many ways, it’s surprising this doesn’t happen more often in tax policy.

Governments around the world will move very quickly when it suits them or when they feel that they need to close off loopholes. Coming from Britain, Budgets were always full of surprises and policy announcements. Sometimes there might be some leaks ahead of the announcement, but generally speaking, every Budget always contained a few surprises.

Now, the other thing attracting criticism is how the Government has rather deliberately phrased the move against interest deductions as closing a loophole. As a few people have pointed out, this is not correct. The position is that interest borrowed to derive gross income, such as rental income is deductible.

But what has become apparent in the residential property investment market is that there’s two parts of the economic return. There is the rental and then there’s the capital gain.

And the issue was that many leveraged investors who are most affected was that they were getting a full interest deduction but would only be taxed on part of the economic return. That is the rental income. All things being equal the capital gain would not be taxed unless the bright-line test applied. Restricting interest deductions in that context is actually consistent with the general income tax rule that an expense is only deductible to the extent it’s incurred in deriving gross income.

The current treatment is therefore an anomaly. What the Government has done is closed off an anomalous position, but only in respect of a certain group of investors, which again leads to outrage about the treatment. But that group is probably losing that argument about it not being a loophole, because to borrow a political phrase, “Explaining is losing” particularly if as in this instance a very technical argument applies.

Always at risk

But the overall point should be kept in mind, and this has happened before with the removal of the loss attributing qualifying company regime, tax preferred investments or rules that give a tax advantage will always be scrutinised by government. They are always therefore at risk of being abruptly closed off.

So, if you built an economic business model around relying on that, you are actually making yourself very vulnerable to a move like this.

Work in progress?

Moving on, one other point has emerged, which is surprising, and in the context of the General Tax Policy Process, concerning, is that it appears no details of the advice that was given by Treasury and Inland Revenue on the interest deduction move has been made publicly available.

This is surprising because it implies that this policy is still being worked out. As a result of that the fiscal impact is not clear.

If the interest deductions are restricted completely, that means the Government’s tax take will increase. And me and my fellow tax advisors have been crunching the numbers for our clients who will be affected. And we are giving them projections as to the likely additional amount of tax that would be payable. And that potentially could be quite significant, although it could be that property investors deleverage as a result, which may have a wider economic impact.

This whole policy, in fact, is a good example of something that came up at a seminar last night, which I will talk about a little later, the law of unintended consequences. This is something that hasn’t been done before and the consequences are still being worked out. One or two things I think that come to mind is we might see investors make more use of company structures because the corporate income tax rate at 28% is less than the 33% for property held in trust or possible 39% if properties are held individually.

I also wonder whether the Government should be looking carefully at the question of is the loss ring-fencing rule required any longer? One of the reasons that rule was introduced was the ability of people to leverage and get deductions for interest. But then, since interest deductions often represented the biggest single cost at a time when interest rates were higher, if they ran into losses, investors were then able to offset those losses against their other income.

Now, that loophole was closed off with effect from 1st April 2019. But the question remains now, given that the ability to leverage, which was the main issue around the need for loss ring-fencing, has been restricted, do we need the loss ring-fencing rules?

The other thing is, and this is something I think the Government will need to address as it was a stumbling block for the introduction of a capital gains tax, is that any gains will be taxed at a person’s marginal rate. In a company the rate is 28%, but for an individual from 1st April, it could be 39%. So, there’s a lot of unintended consequences and it’s understandable to see why investors feel rather picked on at the moment.

There’s interesting commentary from the Bank of New Zealand which started its newsletter on this issue by saying that “The New Zealand government is dead set on containing soaring house prices. It has been saying so for some time now and prices have just kept soaring. So it should come as no surprise that their patience has now been exhausted and a full attack on prices is now under way.”

BNZ’s view is “Watch this space.” There will be a lot of arguments around the fall-out of this proposal.

The interest rate restriction rules, as an article in the Herald points out, are actually more restrictive than a similar measure introduced in the UK. What the British did was restrict the rate of the tax relief to the basic rate of tax, roughly 20%. These measures go completely further.

I feel that using something completely unknown whilst a shock to the system, and in line with what BNZ is saying the Government is determined to try and do, is leading the Government into untested waters.

And the alternative might have been to use an existing set of rules, the thin capitalisation rules, which might have achieved much the same sort of objective. But there will be a lot of fallout on this, and it’ll be interesting to see whether there is some tinkering around the edges of these measures.

The bright-line test

On the bright-line test itself, it’s been extended from two to 10 years. And there’s going to be a lot of questions on this about the impact of that, but particularly for people who are in the middle of settling on properties.

Extending the bright-line test period to 10 years has now been passed into law as part of a tax bill. But it has also provided some commentary with useful examples of what happens with sale and purchases underway at the time the proposals were announced.

Basically, if an offer was made before the announcement on 23rd March and accepted before 27th March, then the five-year test would apply. But if, an offer was made on 21st March, but the seller accepted the offer and signed the sale and purchase agreement on 27th March, then the extended 10-year period would apply.

Another of the examples given was of a verbal acceptance before 27th March but the agreement is not actually signed until 27th March. Then the 10-year rule will apply.

So people will have been pressured to making quick adjustments right now to finalise their sale and purchase agreements. Not ideal, and there will be a few people who have been caught on the wrong side of the new 10-year period as a result.

In relation to conditional offers, for example, someone submitted an offer on 18th March, which is accepted, and the agreement was signed prior to 27th March, conditional on finance. If the offer goes unconditional after 27th March, in this case, the 5-year rule would apply. Alternatively, there’s a change in the agreed purchase price which happens after 27th March, the 5-year rule would be applicable.

There’ll be plenty more commentary on this going forward. And it will be interesting to see the commentary in relation to the question of what expenditure becomes deductible as a result of a sale becoming taxable. We don’t know yet if interest expenditure, which has been disallowed, will then become deductible if a property is sold and it’s taxable under the bright-line test or any other measure. The implication is it should be. But we are we’re going to have to wait till May when consultation on this will arrive.

The future of tax

Moving on to an interesting bit of fun I had last night with some colleagues. The New Zealand Centre for Law and Business ran an event where myself, Paul Dunne of EY and Geof Nightingale of PWC where part of a panel.

We were asked four questions around the future of tax. Do we need more tax? Can tax help the runaway residential property market? Will changing demographics result in a changing tax mix? And reducing taxes on the wealthy is this a discredited theory? And if so, what are the implications for that?

This whole thing would be a worthwhile podcast in itself, but it was interesting to see how Paul, who was a member of the 2010 Victoria University Tax Working Group, and Geof, who was a member of that same 2010 tax working group and the recent Sir Michael Cullen-chaired group were mostly in agreement with the need for a comprehensive capital gains tax or rather better designed set of rules around that.

I think the discussion is still there as to whether we need a comprehensive capital gains tax or should it be limited to a particularly troublesome asset class at the moment, property. All of the members of the 2018 Tax Working Group agreed with increasing capital taxes on property. And you’ll note, by the way, some of the discussions that come out about the Government’s bright-line test period, with Treasury suggesting a 20-year period with no exemption for “new builds”.

By the way, as I said we don’t yet know what the definition of “new builds” will be. We’re going to have to wait and see. And on that point, Paul and Geof both made very pertinent points that the law of unintended consequences is very applicable here. They have clients who are involved in property syndicates who were in the process of converting commercial property into residential property. The question now is, are these “new builds”? They don’t know. So, there may be a pause while everyone waits to find out. What does that mean? No-one is going to commit millions of dollars to a project with an unknown tax outcome. So that was one theme of our discussions.

Do we need more tax? The view was that at roughly 30% of GDP, we should be OK. All three of us were in agreement that the ratio of government debt to GDP was not an issue, but we were all not so enamoured of high private debt as we see that as more concerning. So we had an interesting discussion and hopefully I can make the video recording available in due course.

Error correction

And finally, last week, I talked about charging interest at the prescribed rate of interest on overdrawn current accounts. I mentioned that from 1st April 2021 that rate was going to increase from 4.5% to 5.77%.

Well, another of my listeners from Inland Revenue has been in touch and thanked me for drawing their attention to this. It turns out that was a transcription error in their website and that 5.77% rate is incorrect. It will in fact remain at 4.5% going forward. So, thank you Rowan, for getting in touch. And thank you again to all my listeners and readers at Inland Revenue.

Well, that’s it for today, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week Ka kite āno!