IMF and Climate Change Commission suggest changes to the Emissions Trading Scheme are needed.

Like a never-ending Groundhog Day, every International Monetary Fund report on the New Zealand economy suggests tax reforms would promote efficiency. For example,

“There is a sense that the asset allocation in New Zealand households has a bit too much emphasis on housing versus other investments. We think a capital gains tax at the margin would help.”

That was IMF Mission Chief Thomas Helbling in 2017.

“…tax policy reforms are needed to promote investment and productivity and growth increase, increase the progressivity of income tax and mobilise additional revenue in response to long term fiscal challenges. To achieve these objectives, reforms should combine comprehensive capital gains tax, land value tax and changes to corporate income tax.”

And invariably the IMF’s conclusions are usually followed by a fairly dismissive response from the Minister of Finance of the day.

In 2002 it was the late Sir Michael Cullen responded to that year’s report: “The IMF’s credibility is not assisted by the fact that it tends to apply the same policy template regardless of the country’s circumstances”. This year Nicola Willis’s retort was “There are some things that are certain in life, death, taxes and the IMF recommending a capital gains tax.”

Associate Minister of Finance David Seymour also weighed in commenting. “I see the IMF again saying, oh, you need a capital gains tax. Every country has one. The only countries that don’t have one are New Zealand and Switzerland. But I say let’s be more like Switzerland.”

However, I’m not so sure that this was quite the zinger he hoped because as someone mischievously pointed out on Twitter, Switzerland has a wealth tax and a $59 per hour minimum wage in Geneva.

Deputy Prime Minister and former Treasurer Winston Peters was apparently not available for comment.

A de-facto capital gains tax – the bright-line test

Now, amidst all of the commentary about the IMF’s suggestions, one of the things that came up time and again is that in many ways, we do have a de-facto capital gains tax, except we don’t call it that. The bright-line test is an example of the approach that we’ve adopted, which has been ad hoc and responsive based on the government of the day’s policies at the time.

As you may recall the bright-line test was brought in with effect from 1st October 2015 by the National Government and it then applied to disposals within two years. In March 2018 the Labour Government introduced a five-year period and in 2021 it was increased a 10-year period. And so, a quite confusing scenario has developed as to which bright-line test applies because some of the exemptions have changed over time as well, particularly in relation to the main family home.

In one way, therefore, the reduction of the bright-line test back to two years again from 1st July is to be welcomed because it is clarifying and simplifying what has become an incredibly complicated area.

Tax Red Flags: More than just the bright-line test to be considered

The bright-line test and taxation of land has plenty of red flags when together with the excellent Shelley-ann Brinkley and Riaan Geldenhuys and moderator Tammy McLeod, I made a presentation about tax red flags on Tuesday to the Law Association. (Formerly the Auckland District Law Society). My thanks again for the invitation to present and to my excellent co-presenters, we had a very lively session talking around this.

In short when you drill into our current land taxation rules, they are very incoherent. The bright-line test is a backup test. It applies if none of the other land taxing provisions apply. And this is something that tripped up people before the bright-line test was introduced and will continue to do so even now it’s been reduced down to two years.

For many people, the particular issue to watch out for is the question of subdivision. If you own a property and undertake a subdivision within 10 years of acquisition it may still be caught under the existing rules, outside of the bright-line test. And in some cases, you may be caught by the combination of the provisions with the associated persons test which deem transactions to be taxable if at the time you acquired the land you were associated with the builder, dealer, or developer in land.

Sometimes the tax charge can be triggered way past the 10-year timetable since acquisition. That’s particularly the case in relation to a disposal of property where building improvements have been carried out. That particular provision, section CB 11 of the Income Tax Act, deems income to arise if a person disposes of land and

“within 10 years before the disposal”, the person or an associate of the person completed improvements to the land and at the time the improvements were begun, the person or an associated person carried on a business of erecting buildings. Note, the reference to “within 10 years before the disposal.” So, you may have owned that land for considerably longer than 10 years and yet still be subject to the provision.

Just a pro tip for anyone thinking ‘Great, with a two year bright-line test coming in, I can now sign a sale and purchase agreement, make sure settlement takes place after July 1st and it’s not going to be subject to the bright-line test.’ That’s not the case. The sale point for the bright-line test in that case is when the sale and purchase agreement is signed and not when settlement happens. I had at least one client get caught by that very provision because they went for a long settlement thinking that got past the two year period. It didn’t, and it is another case of always seek advice on transactions involving land, because as I’ve just outlined, the provisions are complicated.

Could a capital gains tax be ‘simpler?’

And this was the point we reinforced during our seminar. There is a lot of complexity already in our tax system around the taxation of land and in my view, in some ways a capital gains tax would actually clear away a lot of that uncertainty. It’ll become clearer that, broadly speaking, if you buy something, and you sell it subsequently, any gain will be taxable.

Now, how the gain is calculated and the rate at which it’s taxed are two different things. But often in the debate around the capital gains tax, those two things get conflated to run as an argument against the taxation of capital gains.

In my view, the point still remains that we have a confusing hotchpotch approach to taxing capital gains and at some point, grasping the nettle with a CGT as suggested by the IMF and also the OECD, would ultimately perhaps be a better approach.

Incidentally, doing so would be consistent with the well-established principle we have of the broad-based low-rate approach. There’s nothing to say that by broadening the tax base, we could not hold tax rates at current levels or even lower. Bear in mind that the when the last tax working group recommended the capital gains tax, it was intended to keep to help keep the top tax rate at 33%.

Watch out for trustees on the move across to Australia

One of the other issues that came up in our Tax Red Flag Seminar was the question of trustees, and beneficiaries and settlors moving cross-border, particularly to and from Australia. That is something all three of us are seeing quite a bit of and it is something to watch out for as a key red flag.

The IMF on how to tax wealth

If there is a certain repetitiveness to the IMF’s discourse about taxing capital, it’s part of a global discourse on the topic. Earlier this month the IMF released a How to Tax Wealth note. These how to notes are “intended to offer practical advice from IMF staff members to policy makers on important issues.” And this this was a very interesting read as you might expect.

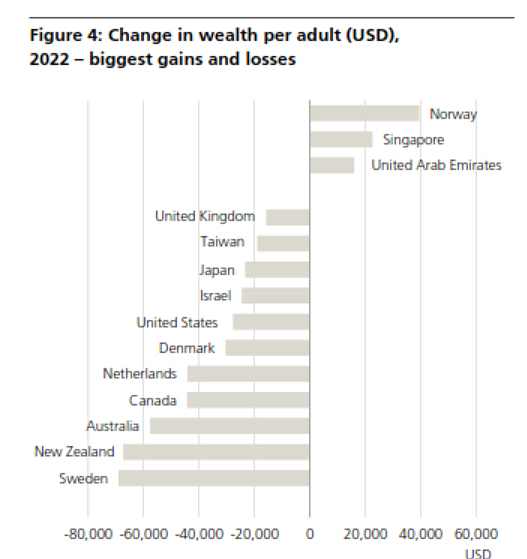

The IMF’s How to Tax Wealth note neatly coincided with the release of the UBS/Credit Suisse, Global Wealth Report for 2023. According to the report, in 2022 New Zealand ranked sixth in the world with an average wealth of US$388,760 per adult. On the basis of median adult wealth per adult, again in U.S. dollars, we ranked 4th behind Belgium, Australia and Hong Kong, with a median wealth of US$193,060.

Incidentally, these rankings were after a very sharp fall from 2021 levels, where New Zealand was only behind Sweden in the biggest loss in wealth per adult.

I am genuinely very surprised to see New Zealand rating so highly for both average wealth and median wealth. On the other hand this Credit Swisse/UBS report is another example of why there’s a great debate going on around the taxation of wealth not just here, but globally.

And this IMF How to Tax Wealth note is instructive in its approach. It starts by making a very obvious point, how much to tax wealth is a distinct question from how to tax wealth. The note argues that:

“returns to capital generally should be taxed for equity and possibly efficiency reasons. and that in many countries, wealth inequality and better tax enforcement strengthen the case for higher effective taxation than in the past.”

Now the IMF doesn’t make any particular proposal about a specific level of tax, the note is basically about ‘here are things you should consider.’ But on the question of wealth taxes, it does come down pretty much against them noting,

“Improving capital income taxes tends to be both more equitable and more efficient compared with replacing them with net wealth taxes. Countries hence should prioritise improving capital income taxation over considering the introduction of wealth taxes”.

Then it talks about – in terms of strengthening capital taxes – addressing loopholes, notably the under taxation of capital gains in many countries. There’s a passing comment, that perhaps you can use a one-off net wealth tax or maybe apply it to very, very high wealth levels.

Time for inheritance tax?

But the Note also concludes “taxing capital transfers through gifts or inheritance provides another opportunity to address wealth inequality.” The IMF comments that the efficiency costs of such taxes are modest, and notes that “inheritance taxes are better aligned with redistribution than estate taxes, since exemptions and rate structures can account for the circumstances of the heirs.”

What really makes the New Zealand tax system unique is not the absence of a capital gains tax because, as David Seymour pointed out, other countries don’t have that, namely Switzerland. It’s the complete absence of taxes on the transfer of wealth, which has been the case now since 1992. That’s what makes New Zealand unique – we have no general capital gains tax together with no estate or gift or wealth taxes.

And this is an area where I think a lot more consideration needs to go into because as the IMF noted, we’ve got fiscal challenges ahead, and where might the revenue be raised from to meet those challenges.

The IMF and Climate Change Commission suggest changes to the ETS

And finally, back to the IMF again. It concluded its mission report by noting that “New Zealand’s ambitious climate goals call for major reforms,” and it referenced the Emissions Trading Scheme, having helped limit net emissions by encouraging robust reductions and removals, particularly from afforestation.

But the IMF then went on to say that “significant reforms” are going to be needed to meet domestic and international targets, and these include reducing the number of available units in the ETS, pricing agricultural emissions and strengthening the incentives for gross emissions reductions within the ETS. The IMF finally note that given the ambition of New Zealand’s first nationally determined contribution under the Paris Agreement, the use of international mitigation i.e.; buying credits from offshore, is likely to be required.

Now the IMF report was a week after the Climate Change Commission, and pretty much said the same thing, and advised the coalition government they should halve the number of ETS units on offer in each of the next six years. The last ETS auction did not go brilliantly. That has a flow on effect in that by reducing the amount of income from emission trading unit sales, it’s going to limit crown revenue for tax cuts.

Vale Rod Oram

It’s interesting to see a confluence of opinion happening here and an appropriate time to remember the late Rod Oram someone who was a very strong environmental journalist. I was fortunate enough to know him all too briefly after we met at a panel discussion. We’d planned on him appearing as a guest on the podcast. Sadly, with his passing that will never happen now, and our thoughts go out to his family and friends.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue does not consider removal of commercial buildings depreciation “to be a fair and efficient way of raising revenue”.

New 12% online Gaming Duty still leaves $500 million gap in the Government’s tax package.

It’s been a busy week in tax, beginning on Sunday when the Associate Minister of Finance, David Seymour, announced that interest deductions for residential properties would be restored to 80% deductibility from 1st April.

There had been a proposal under the Coalition Agreement for the present 50% deductibility in in the current tax year to increase to 60% with backdated effect, but that has now been dropped. The Minister also confirmed interest on residential investment property will become fully deductible with effect from 1st April 2025, in line with the Coalition Agreement.

Interest deductibility “Yeah, Nah”

The announcement reignited a long running debate over the fairness of the measure restricting interest deductibility. The crux of the argument against it being that businesses are allowed to deduct their costs when deriving income, and the change made to restrict interest deductibility by the last government was contrary to standard business and tax practice.

But when you consider this point keep in mind that under the Income Tax Act, expenses are deductible to the extent to which they are incurred in deriving gross income or to the extent they’re incurred in the course of carrying on a business deriving accessible income.

“The extent to which” is the key phrase and the argument around non deductibility revolves around the fact that the economic return for landlords comprises of fully taxable rental income, and a capital gain which is largely tax free. But legislation generally has ignored this point of possible apportionment between what is taxable income and non-taxable capital income. This leads on to the never-ending debate as to whether we should tax capital gains. And so the argument of deductibility is just another continuation of this question.

It’s also worth noting that businesses with overseas owners are subject to the thin capitalisation regime. This also restricts interest deductions where the New Zealand company’s debt to asset ratio exceeds 60%. Now this measure also contradicts standard tax and business practice, but it’s part of many jurisdictions around the world as a means of countering the risk of excessive interest charges transfer pricing money out of the country. In other words, there are arguments for and against restricting interest deductibility.

Improving the position of renters

On Thursday, the Minister of Revenue released an Amendment Paper for the current tax bill along with five Regulatory Impact Statements two of which covered the restoration of interest deductibility and the reduction of the bright-line test period to two years. There was some interesting commentary by Treasury in both impact statements noting:

“Rental affordability is a significant issue in New Zealand. Based on Household Economic Survey data for the year ended June 2022, a quarter of renting households were spending over 40% of their disposable income on rent housing, and rents have risen faster than mortgage payments. Renters also have higher rates of reporting housing issues like dampness, mould and heating.”

Treasury, Inland Revenue and the Ministry of Housing and Urban Development all agreed that restoring interest deductibility should have a long-term effect of putting downward pressure on rents, but ‘should’ is doing a lot of work in this space. Other measures are going to be needed to improve rental affordability.

But restoring interest deductibility has the benefits of simplifying matters. Restricting deductibility was an imperfect measure, with a great deal of complexity and arguably went too far in the other direction of apportioning expenses relating to the split between taxable and non-taxable income.

Trustee tax rate increase to 39% confirmed subject to $10,000 exemption

The announcement on interest deductibility was followed on Monday by the Finance and Expenditure Committee (the FEC) reporting back on the Taxation (Annual Rates for 2023-24, Multinational Tax and Remedial Matters) Bill. There’s a great deal of interest around this Bill as it included the proposed increase in the trustee tax rate to 39%.

As had been hinted by Finance Minister Nicola Willis a couple of weeks back, there is going to be a de-minimis introduced for trusts with trustee income (undistributed income) of $10,000 or less. Such trusts will continue to have the 33% trustee rate apply to trustee income. However, for all trusts where the trustee income exceeds $10,000, a flat rate of 39% will apply. Therefore, if there’s $10,000 of trustee income the 33% rate applies but if it’s $10,001 the new 39% rate will apply on everything. It’s not the first $10,000 is taxed at 33% and the excess at 39%. It’s an all or nothing.

The FEC justified introducing the de-minimis exemption on the basis that the information it had received was that the compliance costs for many trusts were in the region of between $750 and $1,000 per annum. Therefore, the potential $600 benefit of a $10,000 threshold would be swallowed up by compliance costs, which is a fair point. But the reaction among my colleagues and myself is that the $10,000 threshold, although welcome is too low because, by the FEC’s own logic, something closer to $25,000 could easily have been justified.

It’s worth noting that the compliance costs for trusts have increased substantially in the last couple of years. Firstly, following the Trusts Act 2019 coming into force. And then secondly, Inland Revenue’s greater disclosure requirement for the March 2022 year onwards. By the way, we have seen nothing about those greater disclosure requirements being dialled back by Inland Revenue now there is the 39% tax rate in place. Back in 2021 part of the argument for not increasing the trustee rate to 39% at the same time as the individual tax rate went to 39% was to allow Inland Revenue to gather data on whether there was substantial amount of potential income sheltering through trusts. That theory seems to have been ditched for the moment.

Energy Consumer and deceased estates remain at 33%

Separately the FEC confirmed that the trustee rate for energy consumer trusts would remain at 33%. It also made changes to the treatment of deceased estates following submissions. A flat rate of 33%, will apply to all deceased estates rather than the deceased persons personal tax rate as originally proposed. More importantly, the trustee rate of 33% will now apply for the year of the person’s death and three subsequent income years. That was in the in the wake of many submissions pointing out that deceased estates typically don’t get wound up inside 12 months. These changes are welcome.

The Bill also covered off a number of amendments to other key topics, including the introduction of the global anti base erosion rules, the taxation of backdated lump sum payments for ACC and social welfare, rollover relief in respect of bright-line property disposals and relief under the bright-line tests for people affected by the Nelson floods.

Those global anti avoidance rules will take effect in two parts, the so-called income inclusion rule with effect from 1st January 2025 and then the ‘domestic income inclusion rule from 1st January 2026. This is a little later than the rest of the OECD and the intention is to give the affected multinational enterprise entities (those with consolidated revenue above €750 million per annum) time to get ready.

Inland Revenue recommended against removing building depreciation

On Thursday the Minister of Revenue published an Amendment Paper containing details of the proposals regarding the restoration of interest deductibility for residential investment properties, replacing the current five and ten year bright-line tests with a two year bright-line test period, removing the ability to depreciate commercial buildings and introducing a new Casino Gaming Duty. The Amendment Paper was accompanied by a detailed commentary . and, as I mentioned earlier, the relevant Regulatory Impact Statements. Now as usual, these Regulatory Impact Statements (RIS) contain some interesting reading.

The ability to depreciate commercial buildings is being removed in order to help pay for the Coalition Government’s tax package. However, in the relevant RIS Inland Revenue recommended recommends retaining the status quo and that “the Government reconsider introducing commercial and industrial building depreciation when fiscal conditions allow.”

Citing its last Long-Term Insights Briefing Inland Revenue noted that in paragraphs 19 and 20 of the RIS, that under some assumptions made by the OECD:

“…New Zealand was likely to have had the highest hurdle rate of return for investment in and industrial buildings for the 38 countries in the OECD. This was when New Zealand allowed 2% depreciation on these buildings. Denying depreciation deductions will drive up these hurdle rates of returns even higher and make New Zealand a less attractive location for investment.

This tax distortion does not only impact building owners. To the extent the additional cost is passed on and there is less investment, it also impacts any business that needs to use a building and the customers of such a business. It thereby negatively impacts productivity more generally.”

Inland Revenue conclude in paragraph 32 of the RIS:

“We do not consider the removal of building depreciation to be a fair and efficient way of raising revenue. We are particularly concerned about the efficiency impacts which will make New Zealand even more of an outlier in pushing up cost of capital for commercial and industrial buildings. We therefore recommend retention of the status quo. We note this RIS is not evaluating the merits of the Government’s tax package as a whole.”

So, why is the Coalition Government withdrawing building depreciation? Because doing so is worth $2.31 billion over four years which was understood before the election. Even so it’s fairly interesting and unusual to see such a blunt assessment.

A new Gaming Duty

National’s Election policy included a new online gaming duty which was expected to raise something like $700 million over a four-year period. I was one of the those who was a bit sceptical about the revenue forecast. And it transpires that the numbers were indeed a bit optimistic.

What is now being proposed is a new 12% gaming duty for online offshore casino websites and this is in addition to GST, which is already payable when gambling on offshore sites. This new duty would be in line with how some other countries tax offshore casino websites. It’s estimated to collect $35 million of additional tax revenue in the forthcoming year ended 30th June 2025 and expected to grow by 5% each subsequent year. This still leaves a gap of about $500 million over four-years in the original revenue forecasts.

The Budget in May is becoming more and more interesting for finding out how the Government will follow through on its commitment to increase personal income tax thresholds. Even though they won’t compensate for the effect of inflation since 2010 those threshold adjustments come at a substantial cost. I could see that further cost reductions may be imposed further down the track. Those are political matters which we’ll have to wait and see how they work out.

Foreshadowing a capital gains tax?

Some commentary in the bright-line RIS raised the prospect of a capital gains tax. Treasury, for example, proposed a 20-year bright-line test or longer as it

“…would capture more capital gains, thereby improving the fairness of the tax system and supporting more sustainable house prices.”

Inland Revenue meantime felt the 10-year bright-line test was not an efficient way of taxing capital income before adding “If the government wanted to tax the income, it would be preferable to have a tax on these gains, irrespective of when the assets were sold.” It’s interesting to see Treasury and Inland Revenue raising the bogeyman of a capital gains tax to address funding and fairness issues within the tax system.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

“As-salamu alaykum. Peace be upon you and peace be upon all of us.”

In last week’s Sunday Star Times, Miriam Bell looked at the question of how New Zealand’s taxation of property compares with other jurisdictions.

In doing so, she spoke to myself, Robyn Walker of Deloitte, and John Cuthbertson, the tax director for Chartered Accountants Australia and New Zealand. We all gave differing takes on the position.

According to the OECD statistics, we are near the bottom end of the range as a percentage of GDP. Including local government rates, New Zealand’s taxes on property for 2020 was approximately 1.9% of GDP and the total tax take for the year of 32.18% of GDP. By comparison, Australia’s taxes on property was 2.718% of GDP (2019 numbers), the UK was 3.855% and Canada 4.15% of GDP (both 2020 numbers).

As you can see, Canada and the UK are significantly above New Zealand. One of the reasons for this, as Robyn and John pointed out, is that they have a range of stamp duties that may apply. But also, as we all pointed out, all three jurisdictions, Australia, Canada and the UK, also have capital gains tax and in the case of the UK, inheritance tax may also apply on some properties on transfer.

The article provoked a fairly lively debate, as you would expect. The range of views across the board is that, yes, it looks like we’re under taxed. But the bright-line test is in place which is problematic in that although it looks like a capital gains tax, it doesn’t apply comprehensively, unlike in the other three jurisdictions.

Robyn Walker then made a very good point following through that the design of the bright-line test is basically all or nothing. If you hold property for more than 10 years, you’re outside the test, which means that you’re likely not to be taxed on it. So you get this wide variance in the tax effect of sales or property, which you don’t see to the same extent in other jurisdictions.

Robyn subsequently did a nice little post on LinkedIn, in which she looked at what would be the tax consequences in Australia, Canada, the UK, and New Zealand for the sale of a property which realised a $100,000 gain. Because we treat it as income, we’ll tax the full gain at the relevant marginal rate and for the purpose of the example that was 33%. Canada and Australia will tax only half the gain at the relevant marginal rate, although non-residents in Australia will be taxed on the full gain. And although the UK will tax the full gain the top rate applicable is 28%.

The end result was that if the bright-line test applied, then the tax payable in New Zealand would be highest relative to the other three jurisdictions. But if the bright-line test didn’t apply, then it was the lowest. In fact, it would be nil. And this reinforces Robyn’s point that it is a poorly designed test which can be very unfair in its application. You hold a property for nine years and 363 days, you’re taxed. Hold it for 10 years and one day you’re probably not.

The point I stressed in the article is that we want to look at broadening the range of taxation, and it’s fair if we do so because we start to get round these arbitrary distinctions. As I’ve previously said, my preferred methodology for expanding the taxation of capital is that promoted by Associate Professor Susan St John and myself the fair economic return, not a transactional based capital gains tax.

Anyway, this debate will continue to run and run. Miriam Bell’s article provoked a fierce reaction on Stuff, unsurprisingly, and there’s been an interesting debate around Robyn’s LinkedIn article. I urge you to take a look at that.

I think we really do need to address the issue of taxing property particularly when you consider what the Infrastructure Commission said earlier this week about property owners benefiting to the extent of house prices being 69% higher than they would have been without actions being taken to restrict the supply of housing. Housing and the taxation of property is a touchpoint now and will be in next year’s election. We’re going to see plenty more of this debate

Taxes on crypto assets are coming

Moving on to another controversial asset class – crypto assets. Now the value of crypto assets has just simply exploded in the last 10 years. Because of the explosion of the value, it has forced its way onto the tax agenda and tax authorities all around the world are looking to see how this new asset class fits in with their existing rules. New Zealand is no different from other jurisdictions which are all struggling with this. The recent tax bill that was passed last week, by the way, had provisions relating to the application of GST on crypto-assets.

A couple of weeks back, the OECD released a public consultation document proposing a new tax transparency framework for crypto assets. What it has identified is that crypto assets can be transferred and held without going through the normal financial intermediaries, such as banks, and fund managers. And from a tax perspective, there’s no central administrator having what the OECD calls full visibility on either the transactions carried out or on the location of crypto asset holdings.

It also appears that malware attacks and ransomware attacks, payments are increasingly demanded in crypto-assets, which are largely untraceable. So that’s obviously a matter of concern to not just tax authorities.

The OECD paper also points out that some new paid payment products. Such as digital money products and central bank digital currencies, which also provide electronically storage and payment functions similar to money held in traditional bank accounts.

But at the moment, none of these are covered by the Common Reporting Standard on the Automatic Exchange of Information. A reminder the Common Reporting Standard is an agreement between almost 100 jurisdictions where they agree to swap information on financial accounts held in their country by citizens or tax residents of another jurisdiction. It’s been a huge step forward in tackling adn improving tax transparency and tackling tax evasion.

And what the OECD is proposing is, it wants to develop a new global tax transparency framework, which will involve the same reporting for transactions related to crypto assets as for financial assets covered by the Common Reporting Standard. And it’s calling this the Crypto Asset Reporting Framework, or CARF. The paper proposes that the following types of transactions involving crypto assets will be reportable under the CARF:

exchanges between crypto assets and fiat currencies;

exchanges between one or more forms of crypto assets;

reportable retail payment transactions; and

transfers of crypto assets.

This would bring about a very significant change in the crypto asset world as a result. It will basically be bringing the whole crypto asset world in line with other reportable transactions under the existing Common Reporting Standard framework. I doubt that will be very popular with investors in the crypto world, but it certainly will be for tax authorities and other authorities, such as financial regulators and police, as they deal with the implications of the arrival of this asset class. Consultation is now open on the document through until 29th April.

Same old problem returns

And finally, this week, a couple of weeks ago I discussed the new Inland Revenue consultation paper on countering attempted top tax rate avoidance. It so happens that yesterday RNZ had a story on the paper and Inland Revenue’s concerns that “structures may be being used to reduce incomes below $180,000.”

Inland Revenue has provisionally estimated that income from these high earners will be down $2.88 billion, or about 14% from the year prior. This is on the basis that the average self-employed person – who has the most control over their income – might declare 13% less income than they did the year before, to drop from $191,000 to $166,000 (and by happy coincidence below the $180,000 threshold). The number of PAYE earners is expected to reduce, and also declare lower incomes, from an average of $228,000 to $217,000.

If that is happening then I would expect Inland Revenue to react aggressively. On the other hand, Inland Revenue has known for some time that self-employed income spikes around the $48,000 mark (the threshold when the tax rate increases from 17.5% to 30% and $70,000 dollars when the threshold tax rate increases to 33%). I’m not yet aware of increased Inland Revenue investigation activity into such apparent income manipulation. It seems to me that although Inland Revenue has concerns about manipulation involving the new 39% tax rate, what appears to be happening around the $48,000 and $70,000 thresholds seems very blatant.

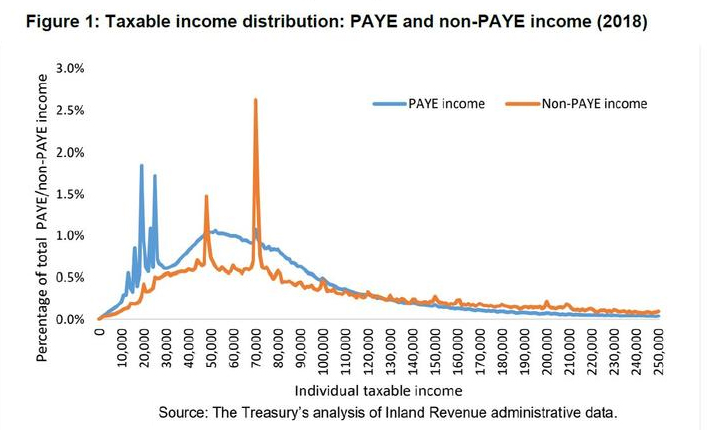

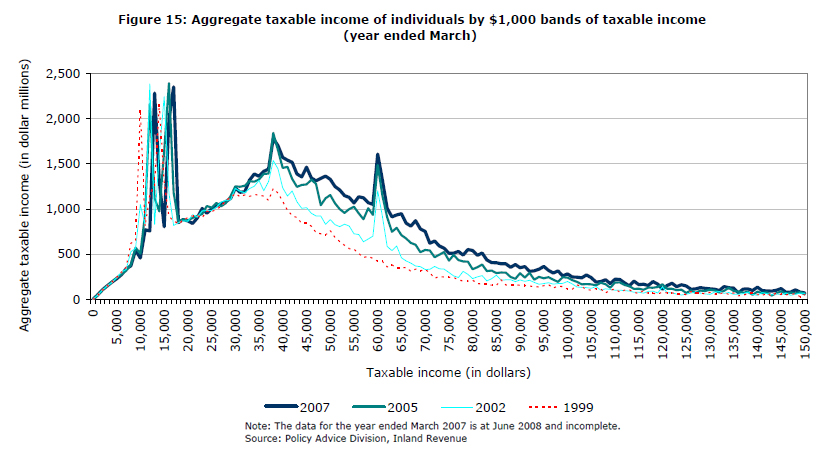

The RNZ report included a chart from Inland Revenue of the taxable income distribution for the 2018 income year which illustrated these spikes occurring at the $48,000 and $70,000 thresholds.

The graph mirrors one produced in 2008 (when the top tax rate was 39%). You can see exactly the same pattern of income spikes around $38,000, the threshold at which the tax rate increased from 19.5% to 33% and then at $60,000 when the tax rate rose from 33% to 39%.

In other words this is a very longstanding problem and the question arises why that issue has been allowed to continue? Does Inland Revenue have the resources to address it? They most certainly will say they do, and they would also probably say that they have had a lot to deal with managing the COVID-19 response over the last two together with finalising the Business Transformation project. Either way you should expect action on this from Inland Revenue.

Incidentally on the question of high tax rates, another news report covered the effect of increases for working for families tax credits. It pointed out that the effective marginal tax rate for recipients of working for families can in some cases be 57%. This is the combination of 30% tax rate on incomes over $48,000 and the 27 cents in the dollar abatement, which applies above a threshold of $42,700.

So before people start complaining about 39% being a very high tax rate, think about what’s going on with working for families, accommodation supplement and other social welfare payments. It’s quite conceivable that someone on $60,000 per annum, receiving working for families with a student loan could have a marginal tax rate on every dollar earned of 69%. This represents 30% income tax, 27 cents on the dollar abatement on their working for families and 12% student loan repayments.

By the way, the $42,700 threshold when the working for families’ abatement kicks in is now, by my calculations, less than the annual income of someone working 40 hours a week on the current minimum wage would earn. It’s another case of where governments have allowed inflation to quietly increase the tax take with worse consequences for people at the lower end of the scale. Yet another issue we’ve talked about repeatedly.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.