The lastest Rich List re-ignites wealth tax debate.

Late last year, the Finance Minister, Nicola Willis, suggested that the charities area was ripe for some tax reform. She expressed concern that the exemption for charities business profits could be being exploited. The sector has nearly 8000 entities, which apparently report a total of over $36 billion of gross income with potential taxable profits of $1.56 billion annually. Now, in theory, those profits would represent over $400 million of tax revenue if the exemption was removed in full. Given the Government’s current straitened circumstances $400 million is not an insignificant sum.

Inland Revenue subsequently issued a consultation document on the topic in late February which closed on 31st March. The consultation sparked quite a bit of concern throughout the charity sector although the main concerns under consultation appeared to be about large organisations making use of the business exemption and donor-controlled charities.

In April, following the end of the consultation period, it became clear from the Finance Minister that in fact, contrary to what was anticipated, there wouldn’t be any budget reforms for the charity sector contained in this year’s budget.

Matt Nippert, the redoubtable business investigations reporter for the New Zealand Herald, filed various Official Information Act requests to get more background on what happened in that consultation process, and an understanding of why the Government might have changed its mind, and he published a story in the New Zealand Herald last Monday.

Sector push back

In essence, the sector unsurprisingly pushed back very significantly with 901 submissions received, which is actually a significant number given there are about 8,000 charities in the sector. 86% of those responding were opposed to removing the charity business tax exemption.

Incidentally, as part of the process, Inland Revenue met with 14 large charities and sector groups as part of the consultation. This is actually quite standard when Inland Revenue is doing consultation. It does go out to interested sector groups and discusses proposals. There can be arguments as to whether or not this borders on lobbying, but it’s a part of the Generic Tax Policy Process and it gives Inland Revenue a boots on the ground insight on its proposals. What was actually discussed at those meetings won’t be released under the Official Information Act request, although the formal submissions on the consultation will be published in due course.

There were complaints it was a very short period of consultation. And obviously there were big concerns about the potential implications for many charities if the exemption was removed in terms of compliance costs and funding. Quite a few people responded that it might be better if Inland Revenue and the charity service focused on the bad actors within the system, rather than taking a blanket approach.

It also became clear following consultation that the possible tax gains from reforms were nowhere near the suggested amount, in fact, were more likely to be around $50 million per annum. As Matt Nippert explained the sector is quite fragmented, with a huge pool of tiny operators and then a very small pool of huge operators such as Sanitarium. Inland Revenue’s proposals would probably have left at least 85% of the organisations untouched.

“A bit scattershot”

Speaking to Matt Nippert KPMG principal Darshana Elwela remarked the Inland Revenue proposals were “a bit scattershot and there was in our view a bit of incoherence about what the potential problem was and how it was being proposed to be fixed.”

I think with Darshana’s comment, sometimes we’ve seen Inland Revenue propose something and it’s not exactly clear the extent of the issue to be resolved, the only references involving subjective word like “significant” without an explanation as to how much represents “significant “.

The other interesting feedback I saw reported by Matt Nippert is that in relation to the potential issue around donor-controlled charities – which I think is a concern – only 46% of respondents opposed a mandatory minimum for distributions for such entities.

I thought that was very surprising because the issue around donor-controlled entities is whether in fact they’re making donations or using the funds appropriately for charitable purposes. Darshana Elwela of KPMG also touched on this, commenting

“Transactions between the donor and the charity could result in the more favourable tax profile for the tax paying side. There were some genuine concerns some of that might be happening.

“The question we had does raise a wider question as to whether these entities should be charities to begin with.”

“A lot of complexity”

Willis denied there has been an about-face, commenting “There is a lot of complexity involved with designing new rules so as to ensure they have integrity and are simple to understand. Therefore, the Government has asked Inland Revenue to do more work on the options.”

The end result is Inland Revenue has gone away to think again because, as the Finance Minister’s office noted, “the Government is focused on fairness and integrity of the tax system. It is important that any changes be the right one, so it’s going to take the time needed to get it right.” In short, watch this space.

Rich List re-ignites the wealth tax debate

Moving on, this week saw the publication of the National Business Review’s annual rich list for 2025, and it showed that for the first time ever, the country’s wealthiest people are collectively worth more than $100 billion. That’s up nearly $7 billion from last year and the criteria now to be included in the rich list is over $100 million of estimated net worth.

It should be said, establishing the wealth of our richest is often educated guesswork, to be frank. That’s because unlisted companies often form the core of the wealth of many of the wealthiest families and persons on the rich list.

By contrast, overall, in 2024 the net worth of all households declined by over $4 billion. Infometrics’ chief forecaster Gareth Kiernan said that average household wealth had fallen since the end of 2021, but that was unsurprising because housing makes up more than half of household assets, and house prices remain below their 2021 peak.

That is the knock-on effect for the average person in New Zealand. And just this week councils have been releasing their rating valuations, and they are showing declines too.

By contrast, the super wealthy have very much more diversified portfolios, so the core of their wealth is actually held in businesses and not so concentrated in property. There are some property magnates in that group, of course, but you’ll find highly diversified wealth, and wealth generates wealth and Thomas Piketty’s famous r > g formula from his monumental Capital in the Twenty-First Century.

Time for a wealth tax?

The publication of the Rich List prompted Chlöe Swarbrick of the Green Party to set out the Green Party’s Budget proposal for a fairly chunky wealth tax of 2.5%. In theory it all sounds very attractive, but as we’ve just discussed, the valuation issues are far trickier than people anticipate in this area, particularly when you have large numbers of unlisted companies in the mix.

And then there is the real risk of capital flight. And as I’ve said before, in our case, I think it’s significantly bigger than people might imagine because moving to Australia is very common and Australia has the temporary residence exemption, which is highly tax favourable. It would mean that, for most Kiwis moving to Australia, their non-Australian assets would not be subject to Australian capital gains taxes unless they became Australian citizens.

Tax is politics and why New Zealand is unique

The key thing to be kept in mind in the debate around wealth tax, and with all debates around taxes, is that what is taxed is entirely a political decision. So, the wealth tax yay or nay debate is going to be resolved at the ballot box ultimately. What is interesting at the moment is that other accountants are reporting they are getting queries from clients concerned about what they could do about a wealth tax if it happened. What are the options around that? This is interesting because it may reveal a shift in thinking that something might be happening. The debate seems to have heated up with growing concerns about inequality and record numbers of people applying for benefits.

In terms of wealth taxes, the classic wealth tax that’s being described by the Greens is basically an annual charge on all wealth. It’s well known that New Zealand does not have a general capital gains tax, but what really makes us unique relative to other countries in the Organisation for Economic Cooperation and Development (OECD) is we don’t have an estate tax, we don’t have a gift tax, we don’t have land tax (other than rates), and we don’t have stamp duties (which, although they’re transfer taxes, are effectively also a tax on wealth, being the value of the land at the time of transfer).

We’ve none of these taxes. But they used to be quite a significant part of the tax base. Back in 1949 such taxes represented 5% of all government revenue at the time, which would be $6 billion now, a very significant sum.

The absence of these taxes and any real form of capital taxation is putting pressure on the tax system to respond to growing pressures on funding. The calls are coming in for variations on some form of capital taxation, whether it’s a capital gains tax, a wealth tax or potentially an estate tax.

We are, as I said, an outlier with the absence of capital taxes, but ultimately tax is political. The arguments will be decided by the electorate and politicians taking a stance and running on tax reform in the future.

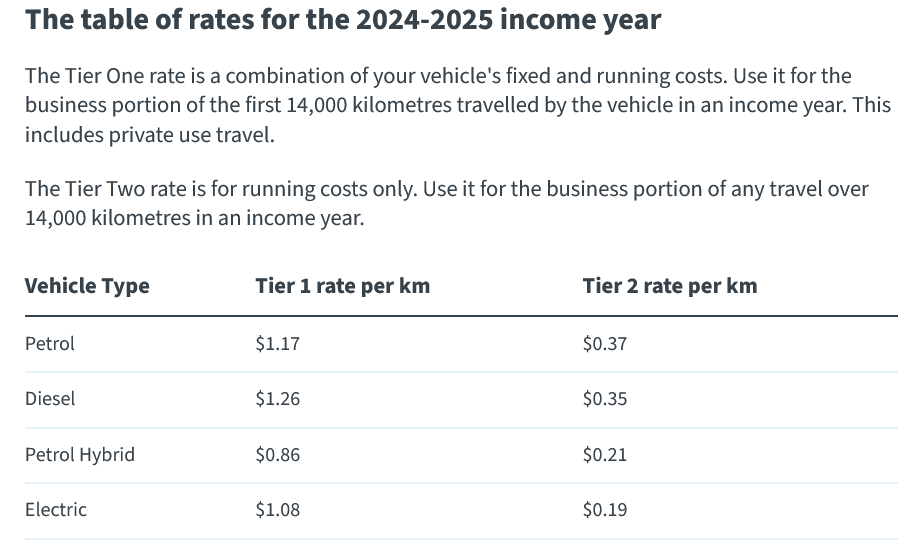

New Inland Revenue kilometre rates come with a change in approach

What makes these rates different this year is that, as Inland Revenue explained, traditionally the Commissioner has set a single Tier One rate. However, due to the significant difference in vehicle running costs between the different vehicle types (Petrol, Diesel, Petrol Hybrid and Electric), a Tier One rate has been set for each vehicle category – being petrol, diesel, petrol/ hybrid and electric – to ensure the rates accurately reflect reasonable expenditure related to the business use of that particular vehicle

The new approach may mean that you have to make adjustments to your mileage reimbursement processes going forward.

Inland Revenue performance targets

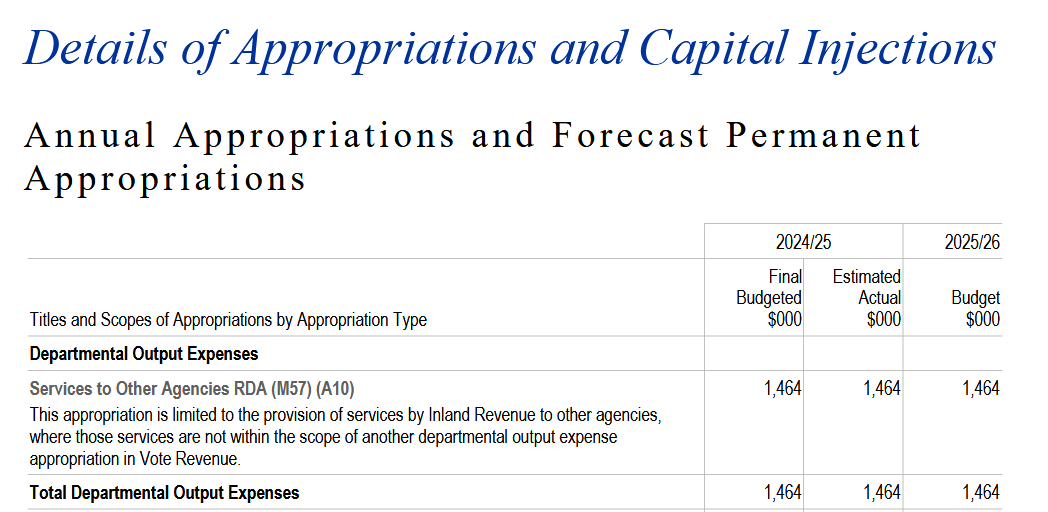

Finally this week, as part of the Budget, every government produces detailed breakdowns of spending for each ‘Appropriation’ or ‘Vote’ to be approved by Parliament as part of the Budget process. Reviewing the Vote Revenue Appropriation gives some useful guidance and detail about what specifically Inland Revenue is expected to do.

These appropriations are incredibly detailed. The Vote Revenue appropriation revenue runs to 40 odd pages setting out the various items of expenditure and what is to be spent or appropriated.

What’s also of interest are the performance criteria for each sub-part of the overall appropriation including a summary of what is intended to be achieved by the appropriation, and how performance will be assessed. Now, not every appropriation line item has an investment. Some get an exemption under the Public Finance Act.

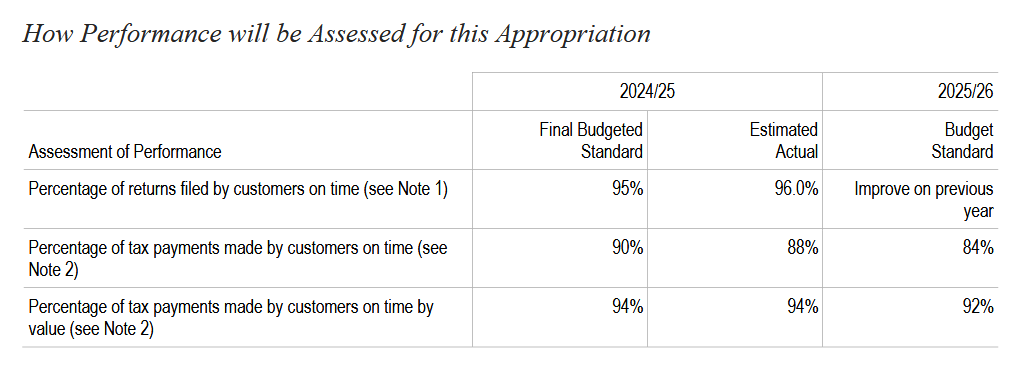

Tax payments & debt collection

As can be seen the performance expectation for tax payments made on time for the current year to June 2025 is 90% but for next year it’s expected to be 84% maybe reflecting harder conditions in the economy are expected.

We’ve recently discussed the issue of student loans and overseas based student loan borrowers. Inland Revenue has a new expectation that 31% to 35% of all such borrowers will be making payments or meeting their obligations in the 2025-26 year. The percentage of collectable debt that’s going to be over two years old is estimated for the current year to stand at 35.3% but is expected to be 40% or less going forward.

In other interesting snippets the percentage of litigation judgements found in favour of the Commissioner is expected to be 75%. The actual is running at 90%, and as we regularly report, there is a whole series of cases coming through where criminal prosecutions have been successfully taken by Inland Revenue.

How long to answer a call?

Now, how long does it take Inland Revenue to answer a telephone call? Well, the budgeted standard they try to meet is currently 4 minutes, 30 seconds or less. At present they’re managing 3 minutes 8 seconds, which is very good. And next year the standard is again set at 4 minutes 30 seconds.

So, if you call Inland Revenue and you’re waiting for more than 4 ½ minutes, it has not met its expectations. In fairness, just remember, this is currently the busiest time of year for Inland Revenue as they process the March 2025 tax returns for over two million people. The chances are if you do find yourself waiting for more than 4 ½ minutes, you won’t be the only one.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Inland Revenue consults on not-for-profit sector and more.

It’s been an extremely busy week in tax – just as we were planning to go to air, Parliament’s Finance and Expenditure Select Committee (“the FEC”) released its report on the Taxation, Annual Rates for 2024-25 Emergency Response and Remedial Measures Bill initially introduced last August.

We covered the bill’s main initiatives when it was initially released, and now the FEC is reporting back on submissions it received, what’s been amended and why, together with Inland Revenue’s accompanying report on submissions. There’s also a supporting report from the independent adviser to the Select Committee, John Cantin, a former guest of this podcast. Overall, there are no major real changes to the legislation. There are minor amendments resulting from issues brought to the attention of the FEC which is how the submission and Select Committee process is meant to operate.

Tax relief for future emergency events

The Officials’ Report on submissions had some interesting submissions on the issue of procedures to manage tax relief for any future emergency events.

The measure was uniformly supported but several submissions proposed making ready to go after a trigger event some of the measures that were brought in and employed relatively successfully during the initial COVID response in 2020, such as carry back of losses, accelerated depreciation, or cashing out of losses. In most cases the submissions were noted or declined.

I thought it was interesting to see that the main submitters involved the Big Four accounting firms, Chartered Accountants of Australia and New Zealand, and the Corporate Taxpayers’ Group. I think these submissions were prompted by our experience during COVID in 2020, where a lot of policy had to be devised and implemented on the hoof, with frantic consultation going on between Inland Revenue and various parties.

I was involved in some of those consultations, and I think it’s not unreasonable to have these measures ready to go if needed. On the other hand, I can see why Inland Revenue and the Government might be a little reluctant to have the ambit of the bill expanded.

Transferring UK pensions to New Zealand

Moving on, one of the measures I was interested in was the proposal for what they call a scheme pays measure in relation to Qualifying Recognised Overseas Pension Schemes or QROPS. These are schemes that are able to receive transfers of pensions from the United Kingdom.

There’s been some debate around this, as under our rules those transfers are taxable, and it has been a long-standing issue that in many cases this triggered a tax bill which taxpayers could not pay as the funds were locked up in the transferred funds.

One suggestion that had been made was this scheme pays proposal, where transfers are made into a scheme. The scheme may make a payment on behalf of the transferring taxpayer and that will be done at a flat rate of 28%, a “transfer scheme withholding tax”. There’s been a bit of tinkering with the proposal mainly about reporting requirements. Otherwise, the regime looks all set to go ahead with effect from 1st April 2026.

It’s a measure I feel ambivalent about. I was part of a group which lobbied for this change so it’s good to see it finally in place. On the other hand, as I’ve said previously, I do think that we ought to be thinking harder about why we’re taxed. (I also think taxing people years ahead of when they could access the funds is technically questionable – what if they died before reaching the required age?)

Crypto-Asset Reporting Framework

The other thing of note is that this Bill also introduced the legislation for the Crypto-Asset Reporting Framework. No amendments have been made to that regime. So that will be coming into force with effect from 1st April 2026. From that date New Zealand-based reporting crypto-asset service providers would be required to collect information on the transactions of reportable users that operate through them and report it to Inland Revenue by 30 June 2027. Inland Revenue would exchange this information with other tax authorities (to the extent it related to reportable persons resident in that other jurisdiction) by 30 September 2027.

Taxation and the not-for-profit sector

Moving on Inland Revenue has now released for consultation an Officials Issues Paper Taxation and the not-for-profit sector. This consultation is something that has been telegraphed for some time, there’s what might be termed unease around the exemption for the charitable sector and the merits of some entities apparently making use of the exemption. For example, the involvement of Destiny Church in the recent events at the Te Atatu library prompted calls for its charitable status being withdrawn.

Quite surprisingly, given the scale of the topic, the Issues Paper is a reasonably short paper running to just 24 pages in all. It covers three main topics. Firstly, a review of the issues involved in the charity business income tax exemption including the rationale for providing such an exemption, and then what potential policy design issues would need to be considered if that exemption was to be removed.

The second topic is donor-controlled charities, which is probably where the most controversy is emerging. It considers the integrity issues that arise from the absence of specific rules for donor-controlled charities in New Zealand, and again looks at possible design issues, including how other countries treat such entities.

And finally, the paper considers a number of integrity and simplification issues to protect against tax avoidance.

The charity business income tax exemption

Apparently, there are over 29,000 charities registered under the Charities Act. Many raise funds through business activities ranging from small op-shops to significant commercial enterprises. There’s been long-standing grumbling about how charities which run a business and have an exemption have an unfair advantage. So, it’s interesting to read the background behind this exemption which has been in place since 1940.

Para 2.3 of the Paper sets out the scope of the review:

“Some tax-exempt business activities directly relate to charitable purposes, such as a charity school or charity hospital. Other tax-exempt business activities are unrelated to charitable purposes, such as a dairy farm or food and beverage manufacturer. It is the unrelated business activities that are the focus of this review.”

“…an international outlier”

According to the Paper “The current tax policy settings make New Zealand an international outlier”. According to a 2020 OECD study Taxation and Philanthropy most countries have either restricted the commercial activities that charitable entity can engage in, or they tax charity business income if the business income is unrelated to charitable purpose activities. As the Paper notes

“These countries have typically been concerned with a loss of tax revenue from businesses if a broader tax exemption was applied, unfair competition claims, a desire to separate risk from a charity’s assets, and a desire to encourage charities to direct profits to their specified charitable purpose.”

New Zealand’s exemption is based on the “destination of income approach.” This means that income earned by registered charities is exempt because it would ultimately be destined for a charitable purpose. But, and this is again one of the key concerns that’s emerged over time, this approach allows income to be accumulated tax free for many years within a charity’s registered business subsidiaries before the public receives any benefit.

What competitive advantage?

Paras 2.7 to 2.14 of the paper look at the question of the exemption providing a competitive advantage because they don’t pay tax. This is an allegation I’ve seen repeatedly raised. As the Paper notes not paying tax means

“One element of a firm’s normal cost structure, income tax, is not present in the case of charity run trading operation. It is argued that this “lower” cost could be used by a large-scale entity to undercut its competitors, to improve its market share, or to deter new entrants.”

The Paper does not accept this argument stating:

“Although the exemption does provide a tax advantage, it does not provide a competitive advantage. Any one type of cost can be looked at in isolation.”

The reasoning for this conclusion is:

[2.9] “Because the tax-exempt entity can generally earn tax free returns from all forms of investment, the “after tax” return it expects from a trading activity is correspondingly higher than that of its tax competitors. Therefore, an income tax exempt entity cannot rationally afford to lower its profit margins on a trading activity because alternative forms of investments would then become relatively more attractive.

[2.10] On this basis, the tax exempt entity will charge the same price as its competitors. The tax exemption merely translates to higher profits and hence higher potential distributions to the relevant charitable purpose. Consequently, funding the charitable activity from trading activities is no more distortion than sourcing it from passive investments such as interest on bank deposits or from direct fund raising.”

What about predatory pricing?

The Paper also discusses whether a charity has a greater ability to use predatory pricing to gain an advantage. Again, that’s dismissed because “the value of tax losses for taxable businesses mitigates this advantage. Taxable businesses can carry forward losses to offset future profits.” That said, if the taxable company goes bust then it has no use for those losses so maybe that is an actual advantage.

“Second order imperfections”

On the other hand, the Paper acknowledges that there are “various ‘second order’ imperfections in the income tax system that may need to be taken into account.” One is that charitable trading entities do not face compliance costs associated with meeting their tax obligations. This lowers their relative costs of doing business.

Another is the non-refundability of losses for taxable businesses and can result in a disadvantage for such businesses relative to tax exempt business resulting in a higher relative rate of return for non-tax paying entities when there has been a loss in one year.

A third is the costs associated with raising external capital such as negotiating with investors or banks can be significant. These costs often make retained earnings the most cost effective form of financing. Because charities retained earnings are higher, this may give them lower costs for raising capital. On the other hand, charities can’t raise equity capital because private investors cannot receive a return.

How much is ‘significant’?

Interestingly, the Paper describes the fiscal cost of not taxing charity business income unrelated to charitable purposes as “significant and is likely to increase.” But no numbers are given and I’m curious to know exactly what is the cost of this particular concession?

The Paper asks submitters to consider what are the most compelling reasons to tax or not tax charity business income before it analyses the potential implications and design issues involved. A major issue will be distinguishing between related and unrelated business activities which could prove difficult in practice without clear legislation and guidance.

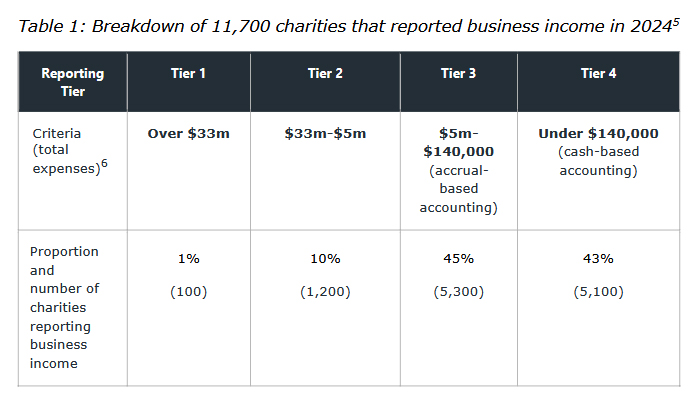

There’s more detail about the trading activities of charities. According to the Paper 11,700 of New Zealand’s 29,000 registered charities reported business income in their published 2024 financial accounts.

These four defined tiers follow the reporting requirements within the Charities Act.

A de minimis exemption?

Based on this initial analysis the Paper suggests a de minimis exemption for charities within Tiers 3 and 4. This would take 10,400 charities out of scope with only 1,300 subject to any policy change. Part of any policy change would involve the treatment of accumulated surpluses and whether there should be minimum distribution requirement.

According to the Paper a donor-controlled charity is any “charity registered under the Charities Act that is controlled by the donor, the donor’s family or their associates.” The current issue that there’s no distinction between donor-controlled charities and any other charitable organisations. The concern is growing that this can enable tax avoidance and raised compliance concerns “because of the control the donor or their associates can exercise over the use of charity funds.”

The Paper gives a few examples of potential abuse such as ‘circular arrangements’ when the donor gifts money to a charity they control, claim a donation tax credit or gift deduction, and the charity immediately invests the money back into the businesses controlled by the donor or their associates.

Also of concern with donor-controlled charities there can be a significant lag between the time of tax concessions for the donor and the charity, and the time of ultimate public benefit. This occurs because funds are accumulated and no or very minimal charitable distributions are made.

Another issue arises when donor-controlled charities purchase assets, or goods and services from the donor or their associates, at prices exceeding what would normally be paid by unrelated parties. These acquisitions are often made on terms that would not normally exist between unrelated parties.

Defining donor-controlled charities

This is the nub of the matter what criteria should be used to define a donor-controlled charity? The funds contributed and level of control a founder has. In Canada for example a charity is considered a private foundation if it is controlled by a majority (more than 50%) of directors, trustees, or like officials that do not deal with each other at arm’s length, or more than 50% of capital is contributed by a person, or a group of persons, not dealing with each other at arm’s length and who are involved with the private foundation.

The Paper suggests that transactions between donor-controlled charities and their associates could be required to be on arm’s length terms or prohibited outright noting in para 3.13:

“This approach was supported by the Tax Working Group in 2019, which found that the rules were private charitable foundations in New Zealand appeared to be unusually loose. The group recommended that the government considering removing tax concessions for private controlled foundations or trusts that do not have arm’s length, governance or distribution policies.”

Apart from citing the Canadian approach the Paper considers the approach to this issue in Australia, the United Kingdom and the United States. It suggests there should be a minimum distribution rule to deal with the question of the time lag between the charity and a donor claiming a benefit and the actual public benefit accruing from the distribution.

Taxing membership fees?

Chapter 4 considers integrity and simplification. This section has already attracted some media comment because it raises the possibility of taxing membership fees which could affect as many as 9,000 not-for-profit organisations.

At issue is the concept of mutuality and member transactions. Generally speaking, most not-for-profit organisations are treated as mutual associations. That includes many clubs, societies, trade associations, professional regulatory bodies.

Up until the early 2000s Inland Revenue’s guidance was that mutual associations were not liable for income tax from transactions with their members, including membership subscriptions and levies. Inland Revenue has withdrawn that advice and has drafted a replacement operational statement which will be released pending what feedback it receives on this Issues Paper.

The impact of Inland Revenue’s revised position would be that trading and other normally taxable transactions with members, including some subscriptions, would be deemed to be taxable income regardless of whether the common law principle of mutuality would apply. The Paper notes that most not-for-profits would not qualify for mutual treatment anyway, because their constitutions will prohibit distribution of surpluses to members including on winding up. This prevents the necessary degree of mutuality required.

Fringe Benefit Tax exemption under review

Finally, the paper touches on the FBT exemption for charities, which has been available since 1985. The paper notes “there are weak efficiency grounds for continuing this exemption” which “lacks coherence”. Inland Revenue is currently reviewing FBT generally and these comments suggest the FBT not-for-profits exemption is likely to go.

Submissions are open on the Issues Paper now, and close on the very unhelpful date it has to be said, of 31st March, when we’re all rather tied up with tax year-end issues. Notwithstanding that I expect there will be plenty of submissions particularly around the potential impact of taxing membership transactions.

Meanwhile in America…

Finally, a quick update on last week’s comments in relation to my concerns about potential leaks coming out of the US Internal Revenue Service (“the IRS”), following the Department of Government Efficiency (DOGE) trawling through the IRS and every other U.S. government agency.

The update I’ve had is that the DOGE people are looking more at IRS internal processes and nothing to do with any data that the IRS has received from Inland Revenue, or any other agency. There are a number of international obligations that the US has still to meet, but no doubt some concerns will have been raised.

But as I said at the time, which I believe is almost certainly the case, IRS officials will be highly professional in making sure that that information shared by other tax authorities is not leaked, accidentally or otherwise, to outside parties.

An interesting choice…

On the other hand, the IRS is getting a new Commissioner. The nominee is William Hollis Long II, or Billy Long, who is a former Republican House of Representatives member from Missouri.

He’s a controversial pick to say the least. He’s not a tax professional, and of particular note is that he was a co-sponsor of a bill in 2015 that would have abolished the IRS and introduced a national sales tax. He is also long-time supporter of a flat income tax for the US system. It’ll be interesting to see how this plays out, and as always, we will bring you developments as they emerge.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

how effective marginal tax rates act as disincentives

Last week was Scrutiny Week at Parliament. This is a new initiative where the select committees get to grill ministers for longer than normally would be the case. In total, there were over 134 hours of hearings across all the select committees.

(Minister of Revenue Simon Watts flanked by Inland Revenue officials during his appearance before the Finance & Expenditure Committee)

A large part of the inquiries directed at the Minister of Finance focused on the Budget and spending choices made or not made, particularly in relation to funding of cancer drugs.

Inland Revenue to review Charity Sector?

The Minister of Finance Nicola Willis was also quizzed on general tax policy and in the course of that she dropped a big hint about a sector of the economy which is going to come under inquiry. In response to a question on tax policy she commented

“We will put together a tax policy programme that looks at other issues. In particular, I have previously identified that we have some concerns around whether all charities are effectively meeting the expectations that we have [regarding] genuinely charitable activity. We don’t want to see [concessionary tax rates] being exploited for activities, which are more clearly more commercial in nature.”

This is a clear shot across the bow of the Charity Sector, although the Minister has foreshadowed this before. It’s now apparent Inland Revenue will undertake an in-depth review of the sector.

The Revenue Minister Simon Watts faced more detailed scrutiny over the operation of his portfolio. He confirmed that one of the Budget initiatives provided funding which would enable Inland Revenue to take on a further 200 full time employees. These additional staff would be directed to improve Inland Revenue’s compliance and investigation activities. This group will be expected to return $8 for every dollar spent on investigation and compliance activity. As the government has allocated $116 million over the next four years to this initiative that means it could reasonably expect to see a return of close to a billion dollars.

When he was questioned about a potential structural deficit and how the government might respond to that, he made it clear that there were no intentions at this stage of introducing new any new taxes. This is what you would expect to hear from the current coalition Government. Clearly the intention is that extra funds will be found by more efficient administration and boosting Inland Revenue’s compliance activities.

Inland Revenue checks out smaller liquor outlets

By coincidence, this week, Inland Revenue announced some insights from a hidden economy campaign which it had run focusing on smaller liquor outlets throughout the country. According to Inland Revenue the number of off-licence liquor stores has grown quite rapidly since 2020 and now there are nearly 3,000 throughout the country.

In 2020, the total sales of these outlets amounted to $1.95 billion with taxable profits of 34.7 million and income tax paid of $11.41 million with a further $29.4 million of net GST collected.

In the first stage of this campaign Inland Revenue compliance staff made 220 unannounced visits looking for signs of issues such as income suppression, unreported sales and non-registered staff. There’s nothing dramatic about what Inland Revenue do here. Their practice is to wander in quietly and have a look around a store. They may or may not buy anything, but they will certainly watch to see what happens behind the till. This is a long-standing technique that it has used for decades across many businesses and it’s highly successful. The truth is when you put boots on the ground with investigations, you get results.

What Inland Revenue found

During these visits, Inland Revenue found more than 100 employees had had PAYE deducted from their wages, but not then paid on to Inland Revenue. Inland Revenue also found issues around migrant exploitation issues with wages paid under the table and use of family labour who are not registered workers. They also found high levels of unreported cash and poor record keeping. In addition, “there was evidence of poor employee relations” None of this is particularly surprising to me as I have encountered similar issues.

Inland Revenue made 220 visits and as a result, 9 outlets have been referred for audit. That’s nearly 5% of all of those that were reviewed. It’s quite likely Inland Revenue already had suspicions about some of these outlets which is why they got chosen for an on-site visit in the first place.

There were a couple of other interesting points of note. Inland Revenue found that companies with multiple family members and changes of ownership demonstrated “less clear money trails”, and some directors appeared to be in name only with minimal knowledge of the business or their director responsibilities. By the way with such shadow, or nominal directors, if in fact someone is behind the scenes pulling all the strings that person can be treated as the director for company law purposes.

What next?

Inland Revenue said this was a “deliberate light touch campaign” and therefore only the beginning, obviously, of a wider look into smaller liquor stores nationwide. Clearly if you’ve just done a “light touch” review and you’ve basically found close to 5% of businesses are worth auditing it’s easy to imagine there’s scope for much greater investigation work if a more detailed and less light-handed approach is taken.

We will watch this space to see what further developments we hear from Inland Revenue. Clearly, as both the Minister of Finance and Minister of Revenue both noted in in their appearances before the Finance and Expenditure Committee, this is an area where they’re happy to give Inland Revenue more funding with the expectation that they Inland Revenue will deliver significant returns.

What about them EMTRs?

Returning to our discussion last week about high effective marginal tax rates (EMTRs) and the shocking realisation that unless something is done soon, some people on the family minimum family tax credit will be facing effective marginal tax rate of 128.6% or even more, this story got picked up by RNZ and was then circulated quite widely. This issue was raised by the Finance and Expenditure Committee, with both the Minister of Finance and the Minister of Revenue. Simon Watts, the Minister of Revenue, acknowledged that there was an issue and he had sought information from Inland Revenue on what options were available to address it. The Minister of Finance was rather more pugnacious when quizzed about the issue. Instead, she was happier to focus on the fact that only a small group of people were affected and made no particular commitment to addressing the matter.

EMTRs and the UK election

Now it so happens that effective marginal tax rates have become a bit of a political issue in the UK general election campaign. Parties are releasing their manifestos and as a result there’s been some interesting commentary emerge about the impact of high effective marginal tax rates as a result of some of the proposed policies. What stands out over there is, as here, there is a general widespread lack of knowledge about how effective marginal tax rates operate and how high they can be.

What’s sparked the debate is what happens with child benefit, the equivalent of Working for Families. There is a High-Income Child Benefit Charge which starts clawing back Child Benefit when income exceeds £60,200. The charge means for people earning above that threshold and up to about £80,000, their effective marginal tax rate jumps from 42% to 56.5%. And some of the proposals made by parties would push it even higher to over 70%.

Dan Neidle of Tax Policy Associates wrote a very interesting and informative blog post on the whole matter explaining how EMTRs operate.

Dan also referred to a very useful paper from the Tax Foundation which highlighted that these issues around EMTRs are quite common internationally.

The disincentive effect of EMTRs

Where this is relevant for all of us here is the disincentive effect of high EMTRs. What is emerging as another particular EMTR problem in the UK is there’s another threshold that kicks in at £100,000 which also triggers some very high EMTRs. As Dan Neidle noted:

“We’ve received many reports saying that high marginal rates affecting senior doctors/consultants are an important factor in the NHS’s current staffing problems – exacerbated by the fact that the starting salary for a full time consultant is just under £100,000.”

The normal marginal tax rate for someone earning £100,000 in the UK is 42%. But above that threshold there’s an income bracket where the EMTR jumps to 62% and in some circumstances even higher, before the EMTR settles down around the £150,000 mark. The state of the National Health Service (NHS) is a major election issue so if high EMTRs are acting as a disincentive to recruiting NHS that is something voters will want addressed.

The New Zealand conundrum – high EMTRs on below average incomes

As I said last week EMTRs are a feature of every tax system. What I think is interesting when you look at the UK debate over EMTRs is there’s a big difference in the level of income under discussion. £60,000 in the UK is well above the average salary in the UK and the standard marginal tax rate for people on that income is 42%. (40% income tax plus 2% National Insurance Contributions).

However, here we’re looking at EMTRs of at least 45.1% (17.5% tax plus 1.6% ACC plus 27% Working for Families clawback) kicking in at a very low level – just $42,700. That threshold is currently below what someone on the minimum wage of $23.15 per hour working 40 hours a week would earn. Our problem here is not that we have high effective marginal tax rates, that’s a common issue around the world, it is that we have people on very modest levels of income suffering those high effective marginal tax rates. And, just as in the UK, it acts as a disincentive. After last week’s podcast I had some correspondence from a relative who as a young solo mother explained that she often found it wasn’t worth her while to take additional work because of the impact of the abatement of Working for Family credits. Often 50% or more of her additional income would be lost.

Over to you politicians

This is not a new issue and from my perspective I find it rather frustrating to see to hear the Minister of Finance be very dismissive when quizzed on the topic. She does not appear to acknowledge that this is a major issue which needs to be addressed. Perhaps she’s looking at it through an entirely political lens and does not want to acknowledge the other side has a point. As I always say, tax is politics.

But the question about high effective marginal tax rates and the abatement thresholds around Working for Families is a multi-government multiparty failure. The present situation is the result of decisions taken by governments since 2009. So that involves both Labour led and National led governments.

To me this is one of those scenarios where it would be good to put the politics aside and focus on actually trying to fix the problem. The two issues around that are ‘Have we made the interaction between tax and benefits too complicated?’ and ‘What are we going to do about the abatement threshold? Are we going to let it linger or are we going to return to having it indexed regularly?’ The Minister of Revenue was noncommittal on that point and as I said, the Minister of Finance wasn’t prepared to discuss the point either.

I would hope that there’s common ground here for all the parties to try and find a more rational approach to this by focusing on the fact that if we want to get people into work, improve their lives, we need to remove the tax incentives that happen to prevent them from doing so. Fingers crossed we’ll see some movement on this issue in due course.

Well, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Originally loaded to Soundcloud 21 June 2024. Appeared in interest.co.nz 23 June 2024)

Canada loses patience and imposes a Digital Services Tax effective 1 January 2024

Inland Revenue appears to be gearing up for a fringe benefit tax initiative.

Late last week, in response to some questions about a review the charitable exemption that religious organisations enjoy, the Prime Minister responded he was “quite open” to the idea, adding “I’ve actually been thinking through the broader dimension of our charitable taxation regimes…We will certainly be looking at things like that this term.”

The hint that a review of the exemption religious organisations and churches enjoy provoked a testy response from Brian Tamaki, among others which was in turn rebuffed by the Finance Minister, Nicola Willis.

But this is a topic which keeps popping up and obviously people have some concerns about how the exemption operates. It was also reviewed in some depth by the last Tax Working Group.

So what’s the exemption worth?

Putting some numbers around the value of the charitable exemption is a little difficult. Every Budget Treasury prepares a paper on the value what are called “Tax Expenditures” that is specific tax exemptions granted under the Income Tax Act. According to the Tax Expenditure statement prepared by Treasury for Budget 2023,

the forecast value for the year ended 31 March 2023 of charitable and other public benefit gifts given by companies was $32 million. In relation to the donations tax credit for charitable or other public benefits (including to religious organisations), value for the same period was estimated to be $315 million. (Which grossed up at 33% is ~$945 million.)

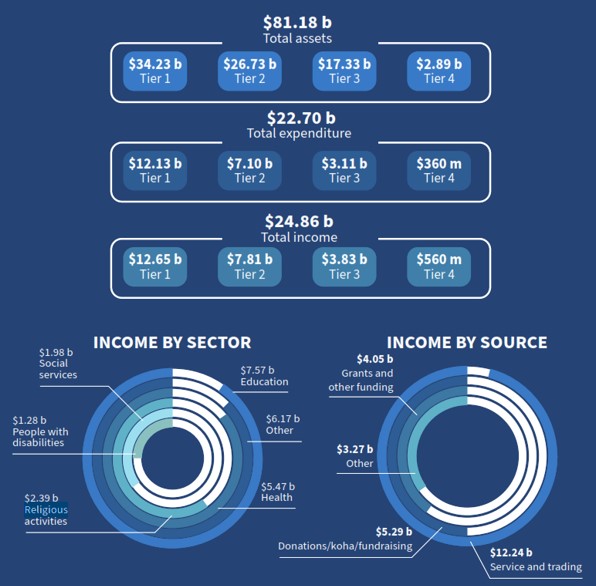

The annual report of Charities Services include a snapshot of the finances for 27,000 charities registered with it. According to the report for the year ended 30th June 2023 the income of the religious activities sector was $2.39 or just under 10% of the total income across all charities.

It’s interesting to consider charities income by source for the same period. $5.29 billion represented donations, koha and fundraising activities. Based on Treasury’s Tax Expenditures statement it appears donations tax credit or charitable donations by companies has been claimed for maybe only a billion dollars of this sum. Interestingly, about half of the total income charitable sector earns during the year comes from services and trading.

Overall Charities Services estimated that the total expenditure by charities was about $22.7 billion. In other words about $2.1 billion of the funds raised were not spent or distributed for whatever reason.

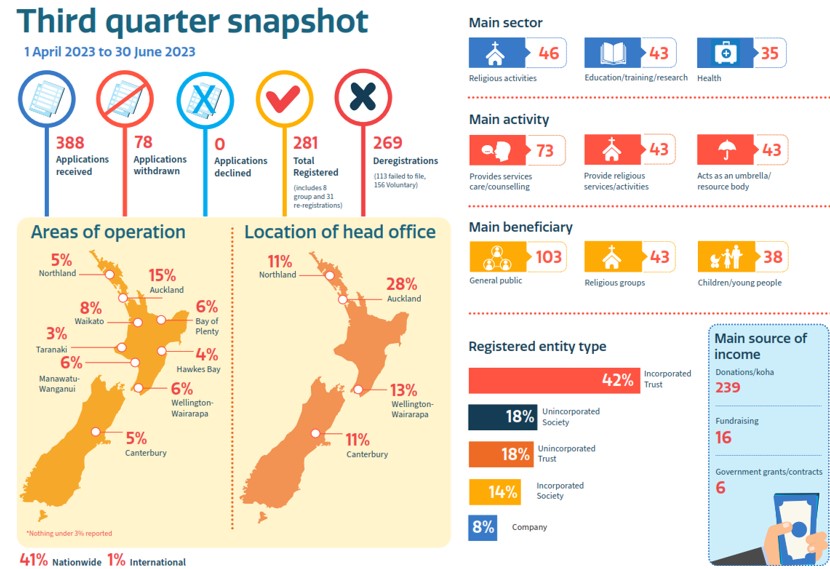

Charities Services also provides a quarterly snapshot of new registrations. The latest available is for the period to 30 June 2023 when it received 388 applications (of which 78 were subsequently withdrawn). Religious activities seem to represent a fairly substantial portion of the new registrations.

What did the Tax Working Group recommend?

The last Tax Working Group took a look at this issue and the best place to consider its views is in Chapter 16 of its interim report which sets out the issues involved.

In its final report the Tax Working Group noted it had “received many submissions regarding the treatment of business income for charities and whether the tax exemption for charitable business income confers an unfair advantage on the trading operations of charities.”

The Tax Working Group responded as follows:

“[39] It considers that the underlying issue is more about the extent to which charities are distributing or applying the surpluses from their activities for the benefit of the charitable purpose. If a charitable business regularly distributes its funds to its head charity or provides services connected with its charitable purposes, it will not accumulate capital faster than a tax paying business.

[40] The question then, is whether the broader policy tax settings for charities are encouraging appropriate levels of distribution. The Group recommends the Government periodically review the charitable sector’s use of what would otherwise be tax revenue to verify that the intended social outcomes are actually being achieved.

I think if the Government is going to review the charitable sector, and religious organisations in particular, the Tax Working Group’s recommendations will be starting point. In April 2019 when the last Government responded to the Tax Working Group’s eight recommendations on charities it noted that Inland Revenue’s Policy Division was already working on five of the recommendations. Two of the remaining three were under consideration for inclusion in Inland Revenue’s policy work programme. The other, in relation to whether New Zealand should apply a distinction between privately controlled foundations and other charitable organisations, would be undertaken by the Department of Internal Affairs, which oversees Charities Services. It’s likely the COVID pandemic disrupted this proposed work programme.

We may get a clue as to the Government’s thinking in next month’s budget, but I think the Government’s focus will be on getting its tax relief package out of the way first so Inland Revenue’s resources will be applied there. The Government and Inland Revenue may then look at this exemption, but I imagine given the fuss and general controversy around such a move, it’s probably relatively low priority. Maybe we’ll see something in the Budget.

Canada loses patience and introduces a digital services tax

There was an interesting development in the Canadian budget, which was released earlier this week. The Canadian Government has decided to push ahead with the introduction of a digital services tax (DST) on large tech companies. Over a five-year period, this was expected to raise ~C$5.9 billion (about NZ$7.3 billion).

Canada had held off for two years to allow for the conclusion of the international negotiations on Pillar 1 and Pillar 2 to conclude, but they’ve dragged on with no clear conclusion in sight. The Canadians have therefore decided to push the button on a DST commenting:

“In view of consecutive delays internationally in implementing the multilateral treaty, Canada cannot afford to wait before taking action….The government is moving ahead with its longstanding plan to enact a Digital Services Tax.”

The tax would begin to apply for the 2024 calendar year, with the first year covering taxable revenues earned since January 1st, 2022. Understandably, this has provoked a pretty vigorous reaction from the United States, where the headquarters of all these tech companies are situated.

What does that mean for us down here? Well, again, we may find out more in the Budget. The Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill which was enacted just before 31st March included legislation for our digital services tax. The Government is therefore in a position that it can watch to see if other countries follow Canada’s lead and then decide whether it should follow suit.

The whole purpose of the digital services tax legislation is to act as a backstop in the event the Two-Pillar solution does not reach a satisfactory conclusion. At the moment negotiations are stalled thanks to vigorous push back by the the companies most affected, such as Alphabet, the owner of Google, Amazon and Meta, owner of Facebook. It’s interesting to see this Canadian move and I wonder if other countries will push ahead with their own DSTs. There are quite a number lot of digital services taxes around the world, with many on hold pending the outcome on the Two-Pillar negotiations.

Taxing Google to help New Zealand media?

Just as an aside, as is well known the media in New Zealand is in desperate financial straits and a question that keeps coming popping up is taxing the digital giants more effectively. That’s because a substantial portion of the advertising revenue that in the past went to New Zealand media companies is now going overseas in the form of (little taxed) various licence payments and fees for services to the the likes of Alphabet and Meta. Watch this space I think things are about to get very interesting.

Inland Revenue gearing up for fringe benefit tax initiatives?

This week, Inland Revenue consolidated the various advice and commentary on fringe benefit tax advice it’s published over the years under a single link. This seems to me to be further signs that Inland Revenue is gearing up to launch a fringe benefit tax initiative. It follows comments by the Minister of Revenue Simon Watts, in several speeches in which he referred to Inland Revenue’s regulatory stewardship review of FBT released in 2022. I got the clear impression that he, and therefore Inland Revenue were keen to look further at this matter and investigate what revenue raising opportunities may arise through a more through stricter enforcement of the FBT rules.

As a very good article by Robyn Walker of Deloitte noted FBT is nearly 40 years old. It’s a very strong behavioural tax. It exists to stop people converting taxable salaries into non-taxable benefits. So, it never really should be an extensive tax raise revenue raiser.

That said, I think there have been issues particularly in relation to the status of twin cab utes and the work-related vehicle exemption as to whether there is sufficient enforcement going on. My expectation therefore is Inland Revenue is gearing up to launch a number of fringe benefit tax reviews and this small step consolidating its previous commentary and advice into a single space is another sign.

Got an idea to improve our tax system? Enter the Tax Policy Charitable Trust scholarship competition

Finally, this week, the Tax Policy Charitable Trust has announced its 2024 scholarship competition. This is designed to support the continuation of leading tax policy research and thinking and to inspire future tax policy leaders. Regular listeners to the podcast will know we’ve had past winners Nigel Jemson and Vivien Lei as guests, and I’m looking forward to meeting the next batch of scholarship recipients.

Entrants may submit proposals for propose significant reform of the New Zealand tax system, analyse the potential unintended consequences from existing laws and changes, and suggest changes to address them. It’s open to young tax professionals aged 35 and under on 1st January 2024 working in New Zealand with an interest in tax policy. The winning entry this year will receive a $10,000 cash prize. The runner up will receive $4000 and two other finalists will each receive $1000 each.

I look forward to seeing what comes out of this and hopefully we will have the winners on our podcast sometime in the future. In the meantime good luck to all those who enter.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week, New Zealand entered the new COVID-19 protection framework, or the traffic light system. Currently here in Auckland, we are on red and most of the rest of the country is on orange, with a few other exceptions. As part of this, the Government has made a new transition payment available, which is aimed particularly at businesses in the Auckland, Waikato and Northland regions, because these are the ones who have had the longest period under the old alert level system.

This transition period payment will be paid through the Resurgence Support Payment system starting in a week’s time from 10th December. It’s set at a higher base level than the current Resurgence Support Payments, applications for which closed last night, by the way. The payment is $4,000 per business, plus $400 per full time equivalent employee, up to a cap of 50 full time equivalent employees. The maximum that any business can receive is $24,000. Treasury estimates the likely total cost of the payment is going to be somewhere between $350-490 million.

This is a new support being made available. The Leave Support Scheme and Short-Term Absence Payment are also available. The Government will be considering further targeted support once the new Covid-19 protection framework beds in.

One other thing to note is that the rules have been changed so that recently acquired businesses can access the Resurgence Support Payment. This is because under the previous rules, the applicant had to have been operating as a business for at least one month before August 17th. So, businesses acquired after July 17th were not eligible for any payment. Although few businesses were affected by the previous criteria, it made a difficult time even worse.

The test will be that the business that was sold must have been in operation for at least a month prior to August 17th and the new business is carrying on the same or similar activity as before the change in ownership. This is a welcome little break. However, there will still be pressure on businesses. As is well known, hospitality and tourism have had a very, very hard time of it over the last 16 weeks of lockdown

Mega landlords

Moving on, there’s been quite the debate this week over the taxation of property as a number of factors came together. Stuff has been running stories on what it calls mega landlords. One story noted that the proposed changes to the interest limitation rules have led investors to start reconsidering their investment portfolio. And also there’s been changes in the Bright-line test, which is now runs for 10 years.

A survey from the Chartered Accountants Australia and New Zealand (CAANZ) and in conjunction with Tax Management New Zealand, found that the proposed tax policies had already affected many property investors’ behaviour. 70% of the 360 odd respondents reported that their clients had changed or were planning to change their investment behaviour. What exactly that might be obviously depends on individual circumstances. According to CAANZ’s New Zealand tax leader John Cuthbertson, it’s likely to be not purchasing additional properties. However, as he also pointed out there’s still some confusion and uncertainty around the complexity of the rules.

Multi property owners

And then Christopher Luxon, the new leader of the National Party, came under some fire when it was revealed that he had seven properties as part of his investment portfolio. However, as business journalist Bernard Hickey pointed out this is actually an entirely rational investment approach under current rules.

This is the crux of the matter. Property has been very tax-preferred, particularly in relation to the non-taxation of gains, and the deductibility of interest even though there are two parts to the economic return, i.e. the taxed rental income and the (usually untaxed) capital growth. Apparently, the value of Luxon’s properties increased by approximately $4 million over the last 12 months. He can reasonably expect that none of this gain will be taxed.

These themes form the background behind the new legislation to limit interest deductions. It so happened that last Monday Parliament’s Finance and Expenditure Select Committee heard oral submissions on the new tax bill, the Taxation (Annual Rates for 2021-2022, GST and Remedial Matters) Bill to give it its full title.

The FEC received 83 written submissions, which are available on its website, including a monster 216 page submission from CAANZ. The size of that submission, which was one of the largest I’ve ever seen, gives you some idea of the complexity involved in this whole matter.

Listening to the oral submissions, the constant refrain was that the proposed rules are far more complicated than people realise, and we don’t know what the unintended consequences might be. The Corporate Taxpayers Group (their submission was a more manageable 21 pages) suggested that really the introduction of the interest limitation rules should be deferred until 1st April so that people can get their head around what’s going on. I think this is a fair point and one other submitters made.

CAANZ and the Corporate Taxpayers Group were concerned about how rushed this whole process has been and how that fits in with the Generic Tax Policy Process (GTTP). I and one or two other submitters suggested that there really needs to be a thorough review of the bright-line test and this legislation in line with the GTPP, because that’s what’s supposed to happen and hasn’t been happening recently. The bright-line test, for example, was introduced six years ago so it’s time for a review as to how it’s working. Since its introduction the bright-line period has gone from two years to ten years period. How is that working? is a fair question to ask.

Talking about the distortions

In the course of the hearing Green MP Chloe Swarbrick rather mischievously raised the issue of an inheritance tax with one submitter. That promptly earned her a bit of a telling off from the chair of the FEC. In my oral submission, I took the opportunity to put forward the Fair Economic Return proposal Susan St John and myself have developed. Whether that gets any traction remains to be seen.

To perhaps unfairly reference Christopher Luxon again, the concern we have is that his $4 million of capital appreciation in the past 12 months is most likely not to be taxed. And whether that’s actually an appropriate tax setting is something we don’t believe is correct. And I think the evidence is growing about how distortionary it is and that something needs to change.

This whole debate, which went on this week and will continue, reinforces the point that Craig Elliffe made in last week’s podcast that the debate over the taxing of property or capital isn’t going away because the current position is unsustainable. A point that rarely gets made is that Aotearoa-New Zealand is really unique in not either having a capital gains tax, or a wealth tax or estate and gift duties or taxing imputed rental. All of those exist in one form in most of the major jurisdictions of the OECD and G20, but there is none of them that don’t have any of those except for ourselves. So that’s why I think this debate will continue.

Doing charity, or accumulating wealth?

Moving on, I remember listening to the late Sir Michael Cullen talking about his experience on the Tax Working Group. I asked him about whether anything had been a surprise to him, and he replied he had been surprised by the extent of what was happening in the charitable sector,

This is something that pops up from time to time with criticism and accusations of charities abusing their charitable status to get an unfair advantage over other businesses. Sanitarium is the one charity (of the Seventh-day Adventist Church) that often pops up when this happens. The Tax Working Group’s view on charitable donations was that it is a long-standing relief. In its view the issue will be around whether, in fact, those charitable organisations are making charitable donations. The concern that arises is when they’re not and they are accumulating wealth without distributing it.

Now it so happens that this week Inland Revenue released a draft operational statement on charities and donee organisations. Now this is a bit of a monster statement, it runs to 105 pages. It outlines the tax treatment and obligations that apply to charities and donee organisations and how the Commissioner of Inland Revenue will apply the relevant legislation.

As I said, the statement is so big it’s been split into two parts, one for charities and one for donee organisations. I’m not proposing to run through this in detail right now, but the statement sets out briefly what exemptions are available and how Inland Revenue is expecting that process to be managed. Inland Revenue is taking submissions until the end of next February. And I would expect that this would generate quite a bit of feedback.

It’s good Inland Revenue has set out formal rules for charities and donee organisations. It is also, in my mind, an indicator that Inland Revenue has some concerns about what’s been happening in this sector, and it is now making very clear what are the rules, what it expects to see, and there will be consequences if the rules aren’t followed.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening (and reading) and please send me your feedback and tell your friends and clients. Until next week kia pai te wiki, have a great week!