Every industry has a dirty secret which is known to its practitioners but is not generally known by a wider audience. In my view the New Zealand tax system’s dirty secret is how high effective marginal tax rates most impact our lowest earners.

The effective marginal tax rate (EMTR) is the highest rate of tax that is applied to the very last dollar that you earn. This also takes into consideration abatements or clawbacks which apply. Now for most persons, the natural assumption would be if the highest income tax rate is 39%, then the highest EMTR would be 39%. That’s a fairly logical, quite understandable and mostly correct approach.

How your EMTR can be above the maximum income tax rate

But, “mostly” is doing a lot of lifting because in certain instances a person’s EMTR can be above the highest tax rate. This is usually where a tax relief is withdrawn, or abatements apply. One example of where tax reliefs will be withdrawn is the Independent Earner Tax Credit, which is available to taxpayers who are not receiving New Zealand superannuation or Working for Families and have annual income between $24,000 and $70,000.

However, between $66,000 and the upper $70,000 threshold, it starts to get clawed back at a rate of 13%. This means that although the personal income tax rate for income between $66,000 and $70,000 is 30%, the effect of the clawback means a person’s EMTR within that income range is actually 43%.

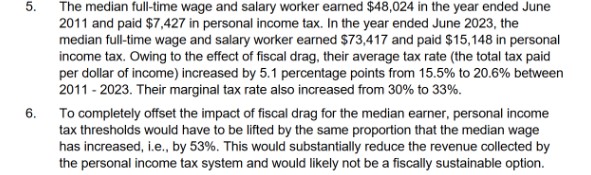

The most common example that impacts most people are the interlocking layers of abatements that apply when someone is claiming a tax credit or benefit. The most notable example, which we’ve discussed quite frequently, is Working for Families. These tax credits are abated at a rate of 27.5 cents on the dollar, where a family’s income exceeds $42,700. (Respectively 28 cents and $44,900 from 1st April 2026).

Abatements also apply in relation to Accommodation Supplement and Jobseeker and the combination of all these results in people on modest incomes having extremely high EMTRs.

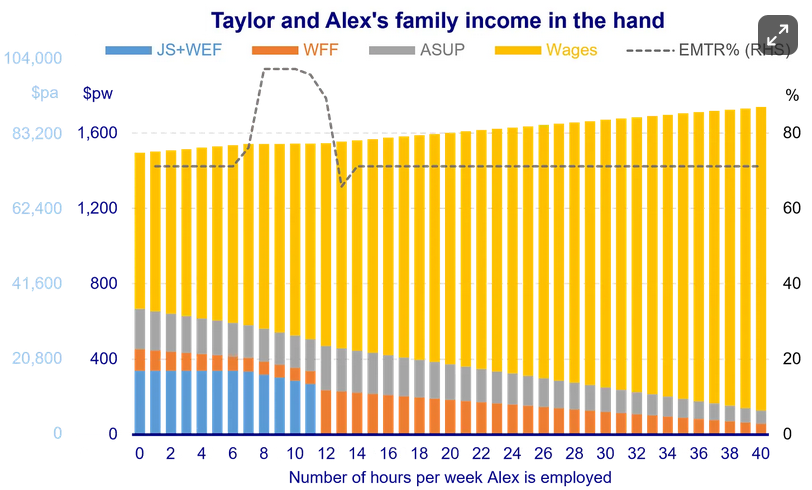

Working 40 hours a week for an additional $6.07 per hour

Ganesh Ahirao (Ganesh Nana), the last head of the recently disestablished Productivity Commission, has put together an illustration of how this Gordian Knot of abatements and benefits affects the family of Alex and Taylor and their two children.

The relevant facts are that Taylor is employed full-time at $25 per hour. So the family income is $1000 gross per week which, after deductions for income tax and ACC, is $829 per week net.

The family rent a two-bedroom house in Island Bay, paying the median rent for the suburb of $625 per week. This means that, after rent, the family has $204.30 per week to meet all other non-rent living costs and expenses. They’re therefore claiming additional assistance. Alex can claim Jobseeker Support there’s also Working for Families credits and Accommodation Supplement available.

However, as Ganesh illustrates, if Alex and Taylor do make a claim, they can find themselves trapped in nightmarish web of overlapping, interlocking benefits where the level of abatements can be dependent on what other assistance they’re receiving. Complicating matters is the requirement for anyone like Alex claiming Jobseeker Support to accept employment.

How to lose 71.2% in tax and abatements on the minimum wage

If Alex takes five hours at the minimum wage of $23.50 per hour (i.e. $117.50 per week) this won’t affect his Jobseeker Support because he’s allowed to earn up to $160 per week before abatement. His earnings will be subject to tax and ACC but crucially they also have an impact on the Working for Families and Accommodation Supplement because the family income is above the abatement thresholds.

The abatements and tax on $117.50 total $83.62 leaving net cash in hand of $33.88, or an EMTR of 71.2% – more than double the official income tax rate of 30% (31.67% once 1.67% ACC earner levy is added).

Remember this 71.2% EMTR is for a family earning a little bit under $60,000 a year, $1200 a week. As Ganesh’s analysis illustrates their EMTR can get even higher.

A well-known problem, at least amongst the experts

Earlier this year I discussed a paper prepared by Treasury which examined this issue of how the tax and transfer system affects financial incentives to work. In the paper Treasury noted that most New Zealanders have EMTRs below 50% with only 6% experiencing EMTRs over 50%.

The Treasury paper noted families with children are more likely to face higher EMTRs. Single parent families are particularly hard hit, with 30% of single parent families having EMTRs greater than 50%, and in some cases higher than 100%.

The lesson from the Treasury paper, and Ganesha’s substack, is that over time we have built a complicated, interlocking and confused system of means tested benefits.

We also have a not unreasonable expectation that people receiving benefits should attempt to work. However, the EMTRs of 70% or even more resulting from the abatements applied by means testing may make the actual return for any additional hours minimal.

In such situations, and faced with such disincentives, why would people work extra hours? What Ganesh’s substack hammers home is the need to be step back and have a real think about what we are trying to do with our work and benefits system and the interaction between tax and benefits.

Inconsistent approach

This problem has also been recently highlighted by the changes to the FamilyBoost initiative where the Government is reducing the abatement rates and increasing the abatement thresholds with effect from 1st October because the initiative – a key election promise – wasn’t reaching as many people as expected.

FamilyBoost is now available for families earning up to $229,100, well above the low threshold impacting families like Alex and Taylor. Understandably this has led to questions as to whether such families should be receiving assistance. Which is perhaps a bit rough, because raising children is not cheap.

A long-standing issue ignored for too long

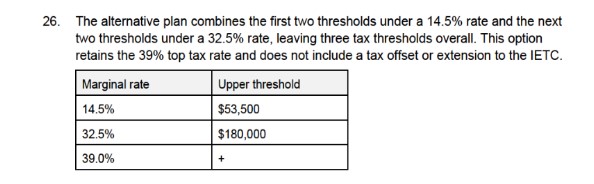

In my view the Government is sending wildly opposite messages here. In many cases, the abatement thresholds have not been increased with inflation for some time. Therefore, with the rise in cost of living and rent in particular, people on lower incomes are struggling to keep up.

This is leading to more applications for supplementary assistance, which then feeds this spiral of higher EMTRs applying. It’s time for someone to grasp the nettle and say, “Well, this is really not achieving very much. Let’s go away and rethink it.”

Strange bedfellows?

Now, in the strange story basket this week is one where the Green Party and the Taxpayers Union have found common ground.

This curious tale is a byproduct of the local government election in Wellington. Two Green Party candidates running there are proposing a change to the taxation rating system. Instead of taxing properties on their total value, including improvements, the Green party candidates want to base rates solely on the value of the underlying land.

Jordan Williams, the executive director of the Taxpayers Union, came out and endorsed this approach on the basis that the current system effectively penalises developments by taxing improvements.

Meanwhile the Green Party candidates are looking to target what they see as land banking, where people are just simply sitting on land, not paying rates. The move is intended to encourage the land to be used for productive purposes, whether it’s more housing or alternative commercial developments.

It’s interesting to see very opposite political bedfellows come together on this point. It’s probably a once in a Blue (or Green) Moon but certainly it’s an example where a principled tax approach can result in a common approach from what appear at first sight to be some unlikely bedfellows.

Is that a business you’re carrying on? New Inland Revenue guidance

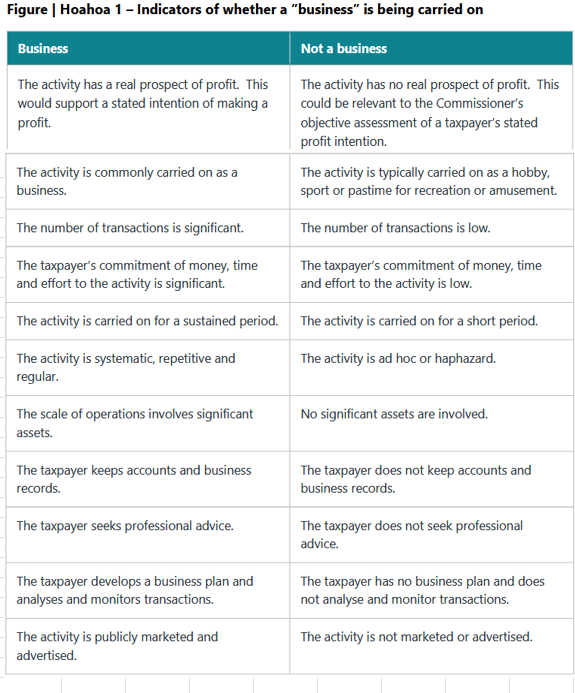

Inland Revenue has released a draft interpretation statement for consultation on the important issue of when and whether a taxpayer is carrying on a “business” for income tax purposes.

As the draft interpretation statement notes:

“It is important to understand if you are carrying on a business, and when that business is being carried on, because carrying on a business is a requirement of many provisions in the Income Tax Act 2007. In particular, an amount that a person derives from a business is included in a person’s income for tax purposes and the person is allowed a deduction for expenditure incurred in carrying on that business.”

This draft statement is part of a project whereby Inland Revenue is modernising and updating its previous guidance, which in this particular case goes back to 1971. Unless otherwise stated these updates are not changing any previous interpretation.

The leading decision in this area is Grieve v CIR (1984) 6 NZTC 61,682 (CA). In Grieve the court ruled that deciding whether a taxpayer is in business involves a two-fold inquiry as to the nature of the activities carried on and the intention of the taxpayer in engaging in those activities.

The draft statement (which runs to 46 pages including references) discusses these relevant factors in depth but it also has a useful summary.

Overall, this is a useful guide to a commonly asked question.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Welcome back everyone. Apologies for the COVID induced intermission and thank you for all those good wishes for my recovery along the way.

An awkward discussion

On the morning of the Budget lockup, I had an awkward call with the client over an unpaid bill. The matter was resolved, but it struck me then and now, as kind of symbolic of the general approach by governments to the question of tax. It’s a very awkward conversation that they really would rather not have. This seems really surprising when you consider that budgets involve spending and government expenditure in the current Budget to June 2025 will be close to $140 billion. To pay for this the expectation is that tax revenue will be about $123 billion during that same period.

Tax is by definition a big part of governments’ budgets, because it raises the majority of the revenue which enable them to run the country. But as I have realised when attending 14 Budget Lockups we never talked very much about tax. On Budget Day, it’s all about splashing the cash. The accompanying ministerial releases are about how money is spent will be spent on this or that particular project. Often you’ll find that the bad news about student loan increases interest rate increases is tucked away on the second page of a ministerial press release.

This approach strikes me as highly symbolic. And by the way it’s the same for governments of whatever hue. Whether National or Labour-led both have pretty much the same approach “Here’s all this lovely cash we’re spending and tax, well we’re doing one or two things minor things.” This year was actually quite unusual because of the focus around the tax threshold changes.

Never mind the spending, where’s the tax legislation?

The other thing which is also slightly unusual as well is the relevant tax legislation isn’t released to us as part of the Budget Lockup. Now you might think, as I do, that when you’ve got a whole pile of tax experts locked up in a room, passing them the legislation which supports the main initiatives might actually be quite a useful thing for broadening people’s knowledge, but actually no, that’s not the practice.

Consequently, some of the detail which was released after the Budget Lockup contained a few surprises. Being cynical about it, the reason why governments are a little bit wary about giving people too much information beforehand is that the required Regulatory Impact Statements contain a lot of detail about tax initiatives and some of that detail is rather awkward for governments in general. To repeat my earlier point, generally speaking discussions about tax are often an awkward conversation governments would rather not have.

The devil in the detail…

As always, Regulatory Impact Statements (RIS) contain some very interesting details, and this is very true of the two that were released in in relation to the Budget. As is well known the tax cuts announced in the Budget involved increasing thresholds for the first time since October 2010. What was not explained during the Budget Lockup and actually only emerged afterwards was that some of the secondary thresholds, such as those relating to fringe benefit tax and employer superannuation contribution tax aren’t going to be adjusted until 1st April next year. The reason given for that is complexity of doing so now.

In fact, in the RIS on the personal income tax threshold changes, Inland Revenue and Treasury officials recommended that the tax threshold adjustments didn’t take place until 1st October. This would allow time for payroll providers and Inland Revenue to get ready and have all the thresholds ready to go as of 1st October. This was what happened back in 2010, when tax thresholds were last adjusted. The announcement was made in May as part of the Budget but didn’t take effect until 1st October. Incidentally, that also gave everyone 4 1/2 months to get ready for the increase in GST from 12.5% to 15% which also took effect on 1st October 2010.

The personal income tax change RIS’s begins with the Problem Definition

“When prices and income rise from generalised inflation and wage growth, but nominal income tax thresholds remain unchanged, individuals end up paying a larger proportion of their tax of their income in tax. Over time, this may result in the amount of tax being paid at different income levels not aligning with the Government’s intentions.

As you can imagine, if you’ve not done anything in this space for 14 years, it can get very problematic. The RIS primarily discusses National’s election proposals, but also references the ACT Party’s election proposals because, as the paper notes

“In the National-ACT Coalition agreement, a commitment was made to ensure the concept of ACT’s income tax policy are considered as a pathway to delivering National’s promised tax relief subject to no earner being worse off than they would be under National’s plan.”

The starting point for Treasury and Inland Revenue officials was Nationals tax proposals, but they also considered variations on the ACT plan, which if you to quickly recall, involved compressing the five current tax brackets down to three combined with a Low and Middle-Income Tax Credit.

Officials also considered several cost savings initiatives, one of which was deferring implementation until 1st October 2024. They also recommended not proceeding with the proposed expansion of the Independent Earner Tax Credit.

“The long-standing view of officials has been the objective of improving work incentives could be achieved more effectively by removing the IETC and making other changes to tax and transfer settings for the same fiscal cost.”

Removing the IETC was something I thought was going to happen to help pay for the tax threshold adjustments. I note by the way, that subsequent to the Budget, Steven Joyce said he would have done that as in fact he proposed to do so back in May 2017.

But as we know, Cabinet went along with National’s plan and chose an implementation date of 31st July. According to the officials, the estimated cost over the forecast period to June 2028 of the threshold adjustments is $10.3 billion. Officials thought they could have reduced that cost by between $1 to $2 billion through some adjustments.

The scale of fiscal drag

Paragraphs 5 and 6 of the RIS underlined the question of just how much of an issue fiscal drag had become.

As the RIS notes, one of the objections about not making regular changes in thresholds is that the “increase in tax from fiscal drag is arguably less transparent than explicit changes to tax settings and may engender less public debate.” Furthermore, when inflation exceeds wage growth, people’s tax burdens increase, even as their ability to pay for goods and services decreases because of inflation.

The conversation we’re not having

But tax is always politics and as paragraph 17 of the RIS notes;

“The desired level of progressivity in the personal tax system is a judgement for ministers to make. Any decision to address fiscal drag by adjusting thresholds will also depend on the revenue needs of the Government and their economic goals.”

This is the discussion we’re not really having. We, the public are saying we’d like this, that and the other to be spent on various public services such as hospitals, schools, roads, pensions. The Government is saying ‘fine, we’ll do that’ but isn’t really talking to us on a serious level about the level of tax we need to meet those demands. If more services are demanded either tax is going to have to be increased or other services must be reduced. That’s a debate that’s not happening, but that’s politics and it’s the same the world over. I’m seeing the same thing play out in the current UK election.

Simplifying the tax thresholds

Interestingly, apart from considering ACT’s proposals, officials developed an alternative which would also have reduced the five tax brackets to three.

The key difference between this proposal and that of the ACT Party is that it would have retained the 39% rate. It would also not have included an extension of the IETC, or the tax offsets proposed by ACT.

Giving with one hand, and taking with the other

The RIS relating to the increase in the In-Work Tax Credit to $25 per week highlights an issue which I actually raised with the Minister of Finance in the Budget Lockup, and that’s that is the interaction of abatements and low thresholds. Currently, the family income threshold for those receiving Working for Families’ tax credits (WFF) is $42,700. This threshold has not been increased since 1st July 2018. Above that threshold WFF are abated at a rate of $0.27 on the dollar. As I told the Minister of Finance, this means that people on very modest incomes are on a higher effective marginal tax rate than her. That did not go down well, to be honest.

As the RIS shows the effect of the abatement regime for the 170,000 families benefiting from the package is that though the Government might talk about an increase of $25 per week, on average the net amount received will be $16.97 per week. The difference is the the effect of abatement.

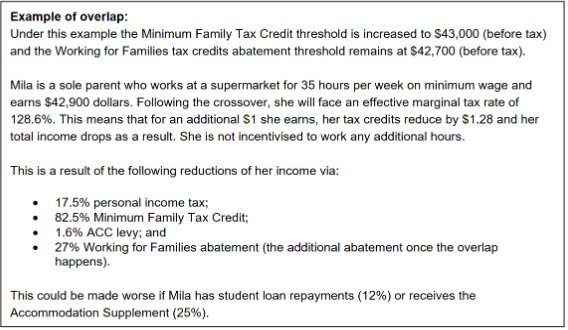

The RIS also notes that unless something is changed the minimum family tax credit threshold, which is increased annually, will soon overlap the threshold at which WFF abatement starts. On present settings this expected to happen on 1st April 2027. As the RIS notes this will result in WFF customers “facing effective marginal tax rates of well over 100%.”

How someone earning $42,900 could have a marginal tax rate of 165.6%

Page 11 of the RIS has the following example illustrating the pending overlap problem.

If Mila was receiving the accommodation supplement, that would be another 25% and if she had a student loan 12% would be deducted. In a worst-case scenario Mila’s effective marginal tax rate would be 165.6%.

Time to regularly index income tax thresholds?

So that leads on to a question which we’re starting to hear more frequently – should we be increasing thresholds regularly? My longstanding view is yes, because it deals with this question of fiscal drag and it’s more transparent. When governments rely on fiscal drag by not adjusting thresholds regularly that is quietly increasing the tax take in the hope nobody pays too much attention to it, other than tax geeks like me. But this approach leads to an ever-increasing problem which after a while means full indexation becomes too expensive as officials noted.

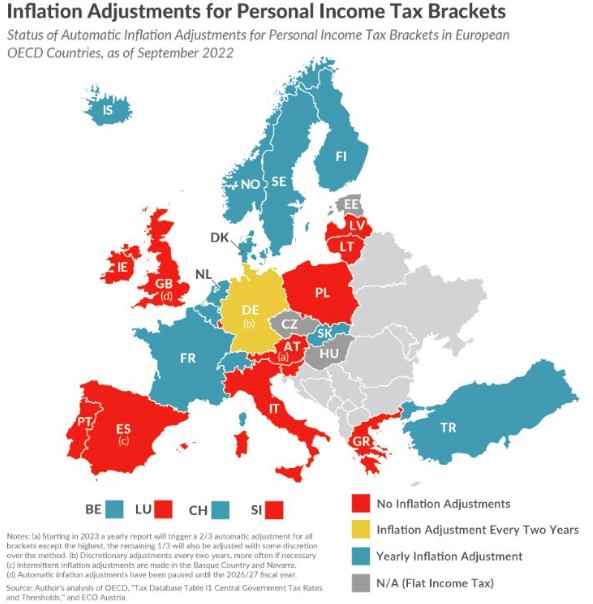

Interestingly, Dr Benjamin Walker of BDO published a LinkedIn post this week with a map illustrating what happens in European OECD countries around indexation.

As you can see a number of countries do regularly adjust thresholds. Germany does it every two years. Several, such as France, the Netherlands, Denmark and Denmark, do so annually. Other jurisdictions such as the Czech Republic, Hungary and Estonia have a flat or single income tax rate so fiscal drag is less of an issue. And then there are other countries that presently don’t index thresholds such, such as Italy, Spain, Ireland and the UK.

I would add in relation to the UK, they’re statutorily they are required to increase thresholds and personal allowances each year, but Parliament may override that as part of its annual budget. And that’s actually been done recently and has been in place for several years. The Conservative Government has therefore deliberately relied on fiscal drag to help increase the tax take. As a result, there are increasing pressures around some very high effective marginal tax rates.

Incidentally, some of the tax discussion coming out of the British election is quite interesting and I’ll probably cover it off in a future podcast. As an aside, I’ve had three UK related assignments come in this week, so UK tax is not as an abstract an issue for New Zealanders as you might imagine.

Another awkward conversation to be had

My view is that thresholds should be regularly indexed for inflation. But we also really need to have a serious discussion about the relationship between abatement rates on benefits and tax credits and the resulting very high effective marginal tax rates for workers on fairly low and sometimes below average wages.

As Geof Nightingale said in the recent podcast with him, Rob McLeod and Robin Oliver, the biggest surprise for him about our tax system is how little discussion goes on around this particular issue which is quite scandalous. When people hear a lot about high tax rates they think of 39% and happening to people on very high incomes. I believe most people would be absolutely staggered to find out that someone on $42,900 per annum could have a marginal tax rate of up to 165%.

GST and landlords supplying properties for use as transitional housing

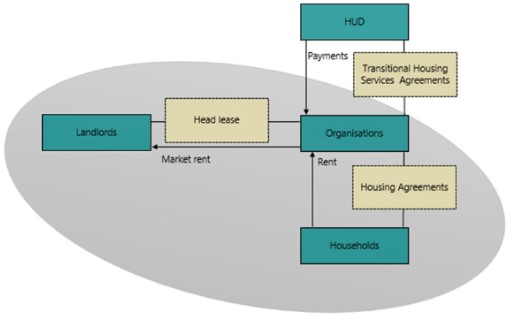

Finally this week, Inland Revenue has released an interesting Operational Position together with three public rulings on the GST treatment of landlords who supply properties for use as transitional housing. Organisations that provide transitional housing services on behalf of the Ministry of Housing and Urban Development (HUD) generally lease properties from landlords under a head lease and pay market rent. Then those organisations will enter into various agreements with the transitional housing tenants.

As always housing is a big topic, and the arrangements involve somewhat tricky GST issues. These binding rulings and Operational Position have been issued to clarify the GST position because it appears that several landlords adopted an incorrect position.

Essentially the Operational Position draws a line under what’s gone on previously and gives guidance on how Inland Revenue is going to apply the technical view set out in the three associated rulings where landlords have previously taken incorrect tax positions. In most cases Inland Revenue is unlikely to issue assessments regarding incorrectly claimed input tax deductions. Each situation will be fact dependent.

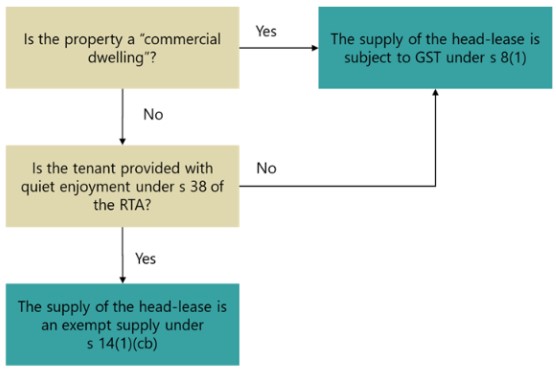

As is now standard practice, there’s a helpful fact sheet which summarises the position in the three binding rulings. The GST treatment depends on whether the buildings leased are “commercial dwellings” and the terms of the housing agreement. If the properties are provided to the tenants with the right to quiet enjoyment as defined in section 38 of the Residential Tenancies Act, then it’s an exempt supply and GST will not apply. If there is no right to quiet enjoyment, then GST will apply. (In some circumstances it may be possible to use the reduced 9% or 60% of the full GST rate).

So that’s a quick summary of the of the position. Obviously Inland Revenue has encountered a number of issues here and decided to clarify its view on the proper interpretation of the legislation.

Well, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue has released Interpretation Statement IS 22/04 on claiming depreciation on buildings. Critical to this issue is determining the meaning of a “building” for depreciation purposes and the distinction between residential and non-residential buildings. The Interpretation Statement addresses this issue when it sets out when depreciation may be claimed for non-residential building and also for some fit outs. It confirms that no depreciation is available for residential buildings.

The Interpretation Statement then sets out where you can find the right depreciation rate for buildings when fit outs attached to buildings may be depreciable. How to treat an improvement of a building for depreciation purposes. And then finally, what happens when the building is disposed of or its use changes?

To recap, depreciation for all buildings was reduced to zero, with effect from the 2011-12 income year. Back in 2020 as part of the initial response to the pandemic, the Government reintroduced depreciation for non-residential buildings with effect from the start of the 2020-21 income year. Generally, the depreciation rate is 2% on a diminishing value basis, or 1.5% on a straight-line basis. Some other depreciation rates may be used where the building has a shorter than normal useful economic life. Examples would be barns, portable buildings or hot houses. Additionally, it’s possible to claim a special rate if the building is used in an unusual way.

Now for depreciation purposes “building’ retains its ordinary meaning which means anything that is structural to the building or used for weatherproofing the building. The Interpretation Statement emphasises that whether a building is residential or non-residential is an all or nothing test. If the building is non-residential depreciation is available, otherwise not, there’s no apportionment.

Residential buildings are any places mainly used as a place of residence. This includes garages or sheds included with that building. Places used as residential residences for independent living in retirement villages and rest homes are residential buildings are is short stay accommodation where there’s less than four separate units.

On the other hand, non-residential buildings include buildings used predominantly for commercial and industrial purposes, but not residential buildings. This also includes hotels, motels, inns, boarding houses, serviced apartments and camping grounds. Retirement villages and rest homes where places are not being used for independent living are non-residential buildings as is short stay accommodation where there are four or more separate units.

If improvements are made to a building, you must treat it as a separate item of depreciable property in the first tax year. Then you can either continue to treat it as a separate item of depreciable property or simply add it to the building by increasing the adjusted taxable value of the building.

In some cases, a fit out can be separately depreciated depending on the nature of the building and the nature of the fit out. Where the fit out is considered structural to the building or used to weatherproof the building it must be treated as part of building and not depreciated separately. Fit outs are depreciable in a wholly non-residential building and sometimes in a mixed-use building. But remember, the key point is that depreciation is not available under any circumstances for a residential building. So overall, this is a useful Interpretation Statement and is also, as has become the norm, accompanied by a very handy fact sheet.

The agencies tackling organised crime and its tax evasion

Moving on, last week I discussed a suggestion by ACT Party leader David Seymour to use Inland Revenue against the gangs. I looked at the powers available to Inland Revenue and discussed how practical his proposal was. To summarise, Inland Revenue has extensive powers which would be useful in tackling gangs and organised crime. However, this is a resource intensive approach which probably in Inland Revenue’s view, would divert its attention from other areas it considers equally important.

This prompted some discussion in the comments section and thank you again to all those who contributed. As I said, my view is Inland Revenue probably thinks other agencies, such as the Police, are better suited for this activity. But it will cooperate with those agencies. Its annual reports make clear they pass information to other agencies. So Inland Revenue is probably working on this matter in the background.

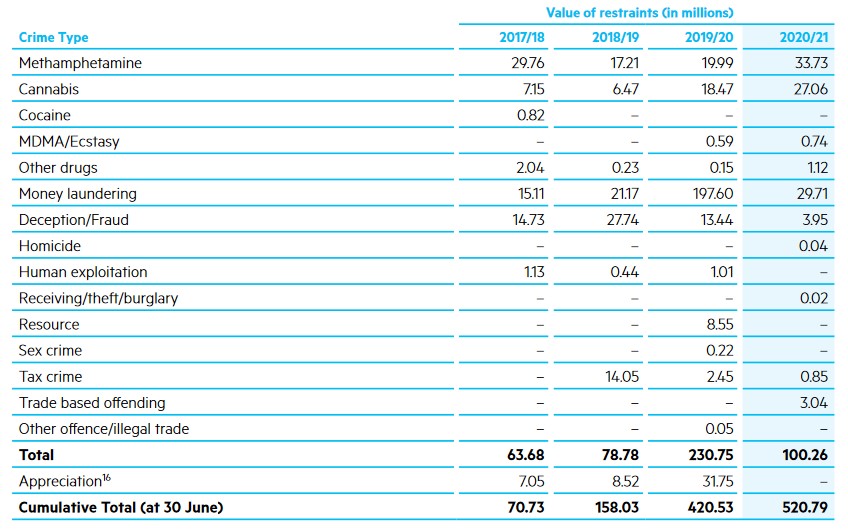

It was interesting just to take a look to see what other agencies were doing in this space and get a gauge of what’s happening. A key tool for the Police is the use of restraining orders to seize assets. According to the Police’s Annual Report for the year ended 30th June 2021 the value of restraints for the year totalled just over $100 million, including nearly $30 million seized from anti-money laundering.

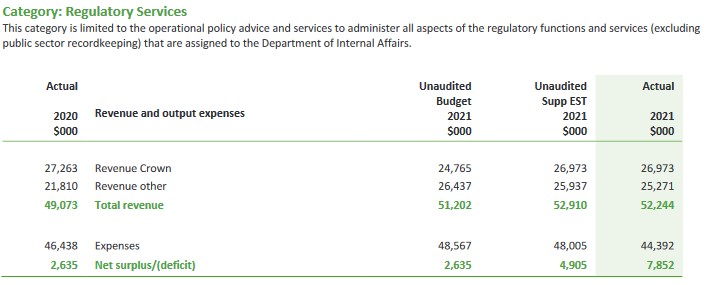

The Department of Internal Affairs also has responsibilities for anti-money laundering, as it’s a key regulator on that. Its Annual Report to June 2021 indicates that perhaps it could do more in this space, as its budget for its regulatory services for the year was set at $52 million, but it only spent $44 million.

And then when you look at the DIA’s performance metrics, such as desk-based reviews of reporting entities, it’s supposed to be targeting between 150 and 350 such reviews annually, but managed only 219 for the year, up from 198 in the previous year. And on-site visits were meant to be somewhere between 70 and 180 but came in at 79. To be fair these were probably disrupted by the impact of COVID 19.

Still, there are other agencies involved in pursuing gangs including Customs who will also be very interested. Inland Revenue will be playing a role, it shares information with these other agencies. So even if it’s not wielding a very big stick publicly, it’s working in the background.

The interaction of tax and abatements on social assistance

Now tax has been in the news a lot recently with the election coming up even though it’s still just over a year away probably. National and the ACT Party have both set out they would proposed some tax cuts. Last Saturday, Max Rashbrooke, a senior associate at the Institute of Governance and Policy Studies, who has written quite a lot on wealth and taxation put out some counter proposals to National and ACT’s proposals.

He suggested that really the focus should be on middle income earners. And he made a suggestion, for example, that we could have a $5,000 income tax free threshold, something we see in other jurisdictions. Britain’s is just over £12,500, Australia’s is A$18,200 and the US has a slightly different thing. It gives you a standard deduction of US$12,000. But anyway, let’s take that comment elsewhere. And Max suggested that something could be done in that space.

But it got me thinking about the question of who does actually pay the highest tax rates in the country. And the answer isn’t those on over $180,000 where the tax rate is 39%, it’s actually more around $50,000 mark if those people are receiving any form of government assistance, such as Working for Families. If they have a student loan as well, then an additional 12% of their salary after tax gets deducted.

The interaction of tax and abatements on social assistance, such as the family tax credit and parental tax credit can mean in some cases, the effective marginal tax rate for some families is more than 100% on every extra dollar they’re earning. This is an issue which the Welfare Expert Advisory Group touched on, but the Tax Working Group wasn’t allowed to address. But it’s a huge problem.

Take, for example, someone earning $50,000, just above the $48,000 threshold where the tax rate goes from 17% to 30%. And that, by the way, is the rate where I think we need to focus our attention on adjustments to thresholds and tax rates. At that level every extra dollar they’re earning is taxed at 30%. If they’ve got a student loan then they pay a further 12%. If they have a young family and are receiving Working for Families tax credits, then these are abated at 27%. Incidentally, the abatement threshold is $42,700. So that means that that person is on a marginal tax rate of 69%. Definitely not nice.

Then there’s a separate credit, the Best Start tax credit which has a separate abatement regime in addition to the Working for Families abatement regime I just explained. So that’s why people could be suffering an effective marginal tax rate of over 100%.

In my view, this is the area where we really need to be thinking about changing the tax system, because to compound matters, governments have been very cynical about not adjusting thresholds for inflation, something I’ve raised repeatedly in the past.

Working for Families thresholds were adjusted for inflation every year until National was elected in 2008. Starting in the 2010 Budget they started freezing thresholds. They also increased the abatement rate which used to be 20% and is now 27%. The current Working for Families abatement threshold is $42,700, which is less than what someone working full time on the minimum wage will earn annually

Looking at student loans the threshold where repayments start in 2009 was $19,084. That is now $21,268 but for a long period of time under the last government it was frozen. National also increased the repayment rate from 10% to 12% in 2013.

So this is an area where governments of both hues have been really quite cynical in my view, and where a lot of serious thought needs to go in about trying to address the inequities that have arisen. The Welfare Expert Advisory Group suggested the abatement rate should be 10% on incomes between $48,000 and $65,000, then increase to 15% before rising to 50% on family incomes over $160,000. (Yes, large families with that level of income could be receiving social assistance in some instances).

There’s a lot of work to be done in this space and inflation adjustments to thresholds is something that should be done anyway. But I think we need to think carefully around the thresholds and how the interaction with social assistance works. At the moment we’re not getting that sort of analysis from either any of the main parties and that’s disappointing, as it’s something that really needs to be addressed.

Why the FER deals with recurrent taxes better

And finally this week, just hot off the press is an OECD report on Housing Taxation in OECD countries. This makes for some interesting reading. Briefly, the report is concerned about how housing wealth is mostly concentrated amongst high income, high-wealth and older households. And in some cases, they believe that a disproportionately large share of owner-occupied housing wealth is held by this group. There’s been unprecedented growth in house prices, not just in New Zealand, but across the whole OECD, making housing market access increasingly difficult for younger generations.

In terms of suggestions the OECD believes that housing taxes are “of growing importance given the pressure on governments to raise revenues, improve the functioning of housing markets and combat inequality.” The report notes the way housing taxes are designed often reduces their efficiency. Recurrent property taxes, such as rates, are often levied on outdated property values, which significantly reduces their revenue potential. This also reduces how equitable they are because where housing prices have rocketed up, people are underpaying based on current values. And conversely people in places where prices are falling or have been stagnant are paying more relative to those in richer areas.

One of the suggestions the report makes is that the role of recurrent taxes on immovable property should be strengthened, by ensuring that they are levied on regularly updated property values. And this is one of these reasons why Professor Susan St John and I have been promoting the Fair Economic Return approach. One of the strongpoints of our proposal would be strengthening the role of recurrent taxes.

Capping a capital gains tax exemption on the sale of a primary residence

Another proposal would not at all popular. It is to consider capping the capital gains tax exemption on the sale of main houses so that the highest value gains are taxed. This should strengthen progressivity in the system and reduce some of the upward pressures. This is what happens the U.S. There is a US$250,000 exemption on the main home per person, and above that the gains are taxed. There’s no reason why we shouldn’t have a similar type exemption here if we want to introduce a capital gains tax. But as I said, that would be particularly unpopular.

The OECD also believes there should be better targeted incentives for energy efficient housing, because housing, according to this report has a significant carbon footprint, maybe 22% of global final energy consumption and 17% of energy related CO2 emissions.

So, there’s a lot to consider in this report, and we come back to it and consider it in more detail. But again, it sort of comes to this point we’ve talked about repeatedly on the podcast, the question of broadening the tax base and the taxation of capital. These issues aren’t going to go away, particularly when you consider, as I mentioned a few minutes ago, how very high effective marginal tax rates are paid by people on modest incomes who may not have any housing. No doubt we’ll be discussing all these issues sometime again in the future.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!